Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

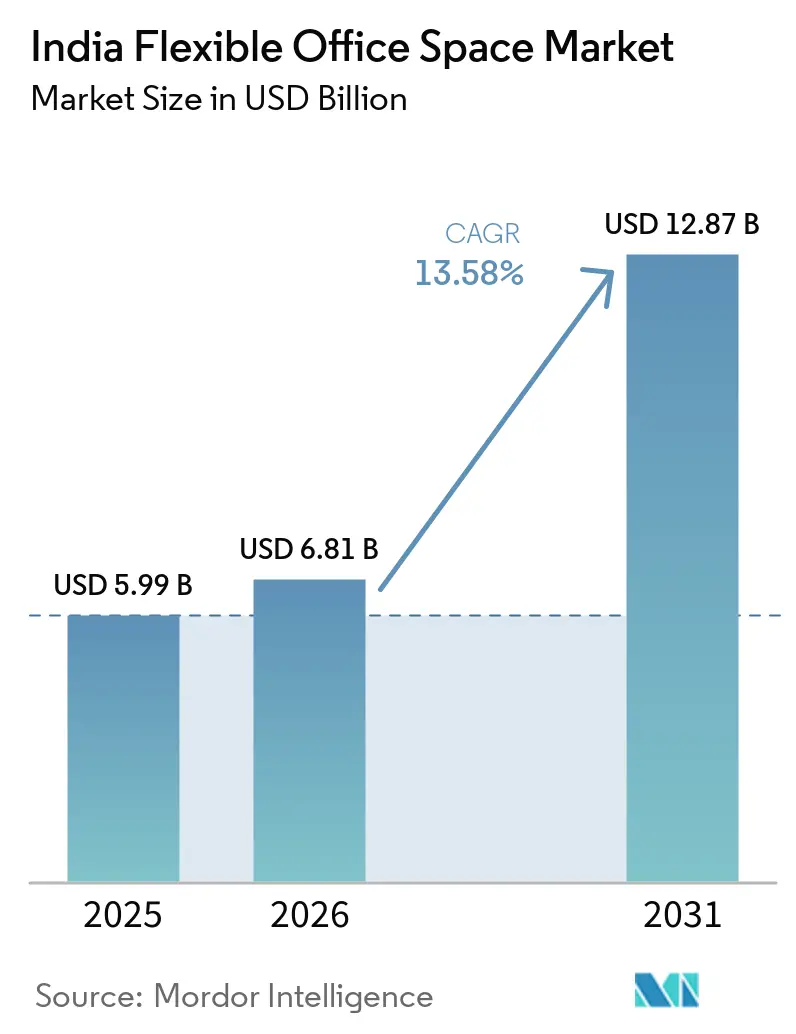

| Base Year Market Size (2025) | USD 5.99 Billion |

| Market Size (2026) | USD 6.81 Billion |

| Market Size (2031) | USD 12.87 Billion |

| Growth Rate (2026 - 2031) | 13.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Flexible Office Space Market Analysis by Mordor Intelligence

India Flexible Office Space Market size in 2026 is estimated at USD 6.81 billion, growing from 2025 value of USD 5.99 billion with 2031 projections showing USD 12.87 billion, growing at 13.58% CAGR over 2026-2031. Several forces propel this growth: hybrid work policies adopted after the pandemic, the cost advantage of plug-and-play space over long leases, and the steady inflow of enterprise clients seeking nationwide seat supply. Operators are scaling quickly to meet demand for technology-enabled space that trims real-estate outlays by 25-30% per employee while raising amenity standards. Aggressive capital raisings—including public listings—signal institutional faith in the India flexible office market’s long-term prospects. The Special Economic Zone (SEZ) denotification policy is unlocking grade-A inventory that will temper rent inflation, although micro-market oversupply remains a tactical concern.

Key Report Takeaways

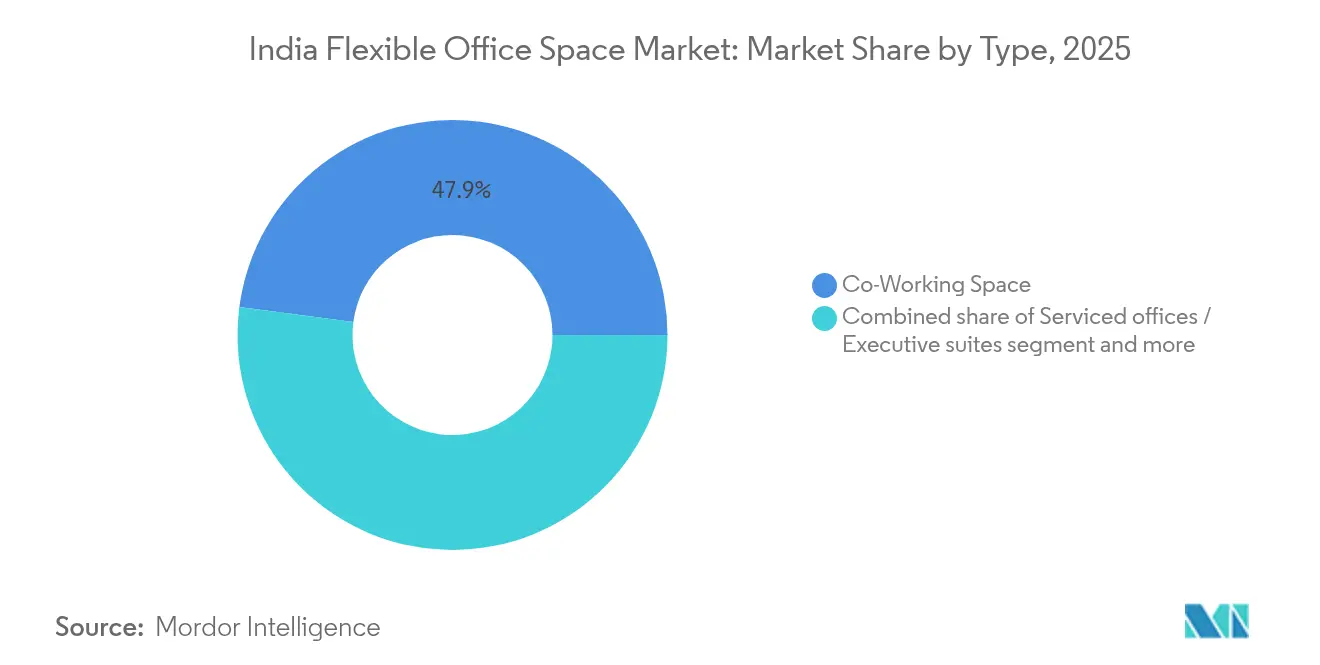

- By type, Co-working Spaces captured 47.92% India flexible office market share in 2025; the Hybrid & Virtual Office sub-segment is advancing at 14.35% CAGR to 2031.

- By sector, Information Technology held 42.75% of the India flexible office market share in 2025; Business Consulting & Professional Services is projected to expand at 15.02% CAGR to 2031.

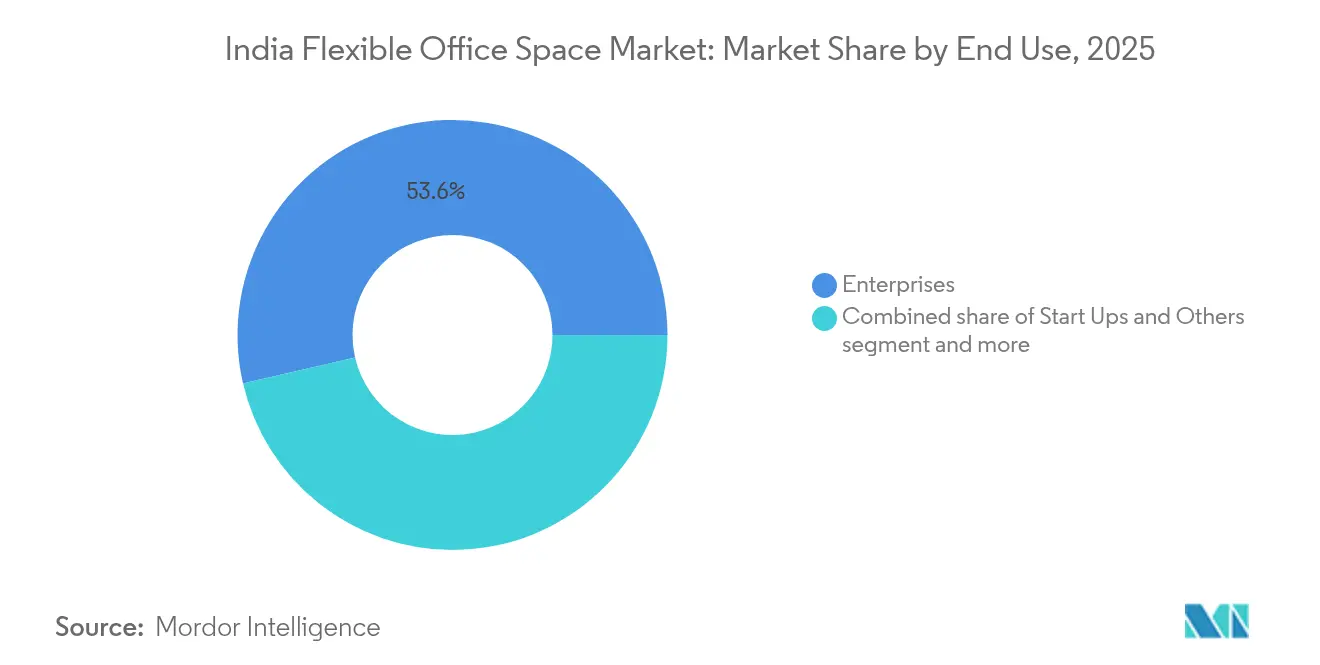

- By end use, Enterprise clients accounted for 53.62% of the India flexible office market size in 2025, whereas Start-ups & Others are forecast to climb at 15.21% CAGR during 2026-2031.

- By city, Bengaluru led with a 24.55% India flexible office market share in 2025, while “Rest of India” is set to grow at 15.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Flexible Office Space Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID hybrid work models | +2.1% | Mumbai, Delhi NCR, Bengaluru and other metros | Medium term (2-4 years) |

| Startup and SME boom | +1.8% | Tier-1 expanding to Tier-2 markets | Short term (≤ 2 years) |

| Rapid metro expansion by brands | +1.5% | All six major metros | Medium term (2-4 years) |

| Corporate suburban & satellite hubs | +1.2% | Metro suburbs and Tier-2 cities | Long term (≥ 4 years) |

| Digital amenities integration | +0.9% | National | Short term (≤ 2 years) |

| LEED/IGBC-certified flex spaces | +0.8% | Green-building focused metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-COVID Hybrid Work Models Drive Enterprise Flexibility Demand

The shift to hybrid work models post-COVID-19 has significantly transformed workspace strategies for Indian corporates. Indian corporates are increasingly viewing flexible workspaces as essential infrastructure rather than mere contingency options. The demands of hybrid work schedules necessitate on-the-fly seat allocations, a feat that traditional leases struggle to provide. Companies are turning to plug-and-play centers, armed with occupancy-management software, allowing them to slash real estate costs by up to 30% per desk, all while enjoying top-tier amenities. Once bound by nine-year leases, multinationals are now favoring one- to three-year managed-office contracts, shifting operational risks to the providers but ensuring scalability. What began as experimental projects in Mumbai and Bengaluru has now expanded to encompass full portfolios in five or more cities. As head-office spaces become predominantly reserved for branding and client interactions, these flexible hubs are not only managing daily operations but also playing a pivotal role in talent retention amidst a competitive labor market[1]NITI Aayog, “Hybrid Work and India’s Digital Economy,” niti.gov.in.

Startup Ecosystem Expansion Fuels On-Demand Workspace Growth

India's start-up ecosystem continues to thrive, with Haryana alone witnessing the registration of over 700 new start-ups in 2024, underscoring nationwide entrepreneurial momentum. These firms prize operational-expenditure models over capex-heavy leases and migrate to flex space that scales in weekly or monthly blocks. Venture funding rounds often translate into sudden head-count jumps; coworking contracts provide rapid seat additions without lease renegotiation. Operators, therefore, design variable seat packs, dynamic pricing, and investor lounge zones aligned with start-up cultures. As start-ups move from seed to Series B, they tend to graduate into managed offices within the same campus, giving operators built-in customer life-cycle growth.

Rapid Metro Expansion by Brands Enhances Tier-2 Market Penetration

The coworking market is witnessing a strategic shift as operators expand from single-city dominance to multi-city operations. A prime example of this strategy is WeWork India's recent launch of a 2,000-seat facility in Chennai, which aims to secure premium towers in rapidly growing secondary metros before competitors. In Tier-2 cities like Jaipur and Kochi, lower real estate costs enhance unit economics, allowing for attractive seat pricing while simultaneously increasing profit margins. Furthermore, a national presence becomes more enticing for enterprise accounts with staff spread across India. Consequently, operators are channeling fresh capital into both major metros and emerging hubs, striking a balance between risk and ambitious growth targets. This multi-city approach is shaping the future of coworking office spaces.

Corporate Suburban and Satellite Hubs Support Distributed Teams

The shift towards decentralized office models is transforming workplace strategies for large enterprises. Large enterprises are now commissioning operators to establish smaller suburban nodes, functioning as "spokes" to their central HQ "hubs." This decentralized approach not only curtails lengthy commutes and boosts employee retention but also resonates with ESG directives aimed at reducing travel emissions. Take, for instance, global capability centres located in Bengaluru's Whitefield district; they have set up satellite sites in Mysuru, catering to specialized teams, all governed by a unified managed-office contract. These hubs typically operate on flexible leases averaging three years, aligning with project cycles and offering exit options in response to headcount changes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High rental escalation and maintenance costs compressing operator margins | -1.2% | Mumbai, Delhi NCR, Bengaluru | Short term (≤ 2 years) |

| Emerging oversupply in major metros increasing vacancy risk | -0.9% | Mumbai, Delhi NCR, Bengaluru, Pune | Medium term (2-4 years) |

| Diverse state-level lease and commercial regulations complicating multi-city rollouts | -0.8% | National, with varying complexity across states | Long term (≥ 4 years) |

| Security and data privacy concerns in shared networks limiting corporate adoption | -0.6% | National, particularly affecting BFSI and enterprise clients | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rental Cost Inflation Pressures Operator Profitability

Rising rental costs are increasingly challenging the profitability of flex-space operators in prime locations. In South Mumbai, Grade-A office rents have crossed the USD 2.40 per sq ft per month mark, putting a pinch on flex-operator margins, even with optimised seat density. While annual step-up clauses in master leases can hit 6%, operators frequently limit client escalations to 4%, leading to a negative spread. Since 2023, maintenance costs—covering power, cleaning, and internet—have surged by 8-10%, further constraining operating profits. To counteract these pressures, operators are pivoting to revenue-share models and seeking longer lock-ins for bulk discounts. However, the risk to margins remains significant, especially in prime CBD areas.

Oversupply Conditions Threaten Pricing Power

Oversupply in the flexible workspace market is reshaping pricing dynamics across major metros. Between 2021 and 2024, the inventory of flexible seats in the top six metros surged, doubling in number and outpacing demand growth. This oversupply is particularly pronounced in suburban areas. New market entrants, lacking established enterprise pipelines, have turned to discounting strategies. As a result, some micro-markets have witnessed effective desk rates plummet by 12-15%. With vacancies on the rise, clients are leveraging their position, negotiating for shorter commitments and enhanced amenity packages. This trend inflates costs for operators, yet offers minimal price advantages. While operators with substantial capital reserves can endure this downturn, smaller firms find themselves at a crossroads, facing potential consolidation or exit from the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hybrid Solutions Drive Innovation

Co-working spaces accounted for 47.92% India flexible office market share in 2025, underscoring enduring demand for open, collaborative environments that suit agile teams. Meanwhile, the Hybrid & Virtual Office category is forecast to post a 14.35% CAGR, the fastest among formats, as corporates look to blend private managed suites with day-pass access for distributed staff. Within the India flexible office market size, hybrid products bundle physical seats, virtual addresses, and on-demand meeting rooms, giving tenants modular cost control. Awfis, Smartworks, and Table Space now allocate more than 35% of new supply to hybrid layouts.

Technology is the linchpin: mobile apps let employees reserve desks in 15-minute increments, while AI-driven utilisation dashboards inform real-time space reconfiguration. Operators invest in acoustic zoning and air-quality monitoring to meet ESG and employee-wellbeing metrics. As large enterprises pivot to hub-and-spoke networks, hybrid centres capable of toggling between open and enclosed zones gain strategic relevance, reinforcing the India flexible office market’s gradual tilt toward multi-format service lines.

By Sector: Professional Services Accelerate Adoption

Information Technology held a commanding 42.75% India flexible office market share in 2025, leveraging flex space to support project teams and client war rooms. The Business Consulting & Professional Services cohort is projected to outpace all sectors at a 15.02% CAGR until 2031, reflecting its need for client-site proximity and confidentiality-friendly private suites. Consulting majors increasingly favour plug-and-play managed offices in Gurugram, Mumbai Bandra-Kurla Complex, and Bengaluru Outer Ring Road, citing seamless IT integration and quick seat scalability.

Operators respond with sector-specific buildouts: soundproof pods for confidential calls, secure printing stations, and reception staff trained in professional-services etiquette. For BFSI tenants, biometric access and dual-ISP redundancy are bundled as standard. Such features allow managed-office centres to fetch a 12-18% premium over generic co-working halls, bolstering the India flexible office market size allocated to high-margin enterprise products.

By End Use: Enterprise Segment Drives Revenue Stability

Enterprises contributed 53.62% of the India flexible office market size in 2025, cementing their role as the industry’s revenue anchor. Contracts from global banks, tech giants, and GCCs often span 500-1,000 seats and run three to five years, giving operators predictable cash flow. The Start-ups & Others segment, though smaller, is slated to expand at 15.21% CAGR, propelled by the robust venture-capital cycle and government incubation schemes.

Enterprise clients now demand dedicated account managers, custom brand signage, and on-premises compliance audits, prompting operators to enhance service depth. Simpliwork, for example, designs turnkey floors that mirror a client’s HQ look-and-feel, integrating proprietary IT and security stacks. This evolution from generic shared desks to bespoke managed space re-defines the India flexible office market, anchoring tenant loyalty and raising switching costs.

Geography Analysis

Bengaluru retained 24.55% India's flexible office market share in 2025, fuelled by its 600-plus global capability centres and deep technology labour pool. Seat absorption remains brisk in Outer Ring Road and Whitefield, where operators secure whole towers inside integrated townships to guarantee expansion rights for anchor tenants. The Rest of India is forecast to grow at 15.53% CAGR through 2031, a reflection of tier-2 and tier-3 cities progressing from pilot centres to full-scale managed campuses. Cities like Jaipur and Coimbatore benefit from ITES and life-science investments that prize cost-efficient yet premium space, ensuring the India flexible office market continues to decentralise.

Mumbai Metropolitan Region and Delhi NCR deliver high yields despite expensive rentals, thanks to entrenched financial-services clusters and professional-services headquarters. To manage rent pressure, operators deploy hybrid suites in Thane and Noida that scoop up commuter-rich suburbs at 30-40% lower cost than CBD towers. The balance between premium city-centre hubs and suburban satellites helps maintain blended gross margins.

Pune, Hyderabad, and Chennai provide a middle path: modest rent, mature tenant base, and supportive civic infrastructure. WeWork’s 2,000-seat Chennai facility reached 60% pre-leasing within three months, illustrating latent demand in secondary metros. Real-estate regulations are comparatively benign, allowing faster fit-out cycles. Across all geographies, the SEZ denotification pipeline is set to inject new grade-A stock, which should dampen rent spikes and sustain absorption momentum.

Competitive Landscape

The India flexible office space market is moderately concentrated. The top 10 operators control a substantial share of seats across more than 1,000 centres, indicating moderate concentration in India's flexible office industry. Scale advantages include lower rents, multi-city client mandates, and technology investment capacity. Awfis’ USD 19 million IPO and Embassy Group’s USD 84 million WeWork India buyout underscore investor conviction in the segment’s double-digit growth runway.

Competition is shifting from pure desk pricing to value-added services. Smartworks offers embedded managed IT, while CoWrks pitches enterprise-ready disaster-recovery suites. Operators integrate real-time occupancy analytics, predictive cleaning, and ESG dashboards, raising switching costs for large tenants. Consolidation continues: Incuspaze acquired Trios in Pune to gain local market share and cross-sell to its national client list.

White-space opportunities lie in life-sciences corridors near Hyderabad Genome Valley and legal-service hubs in Delhi’s Aerocity, where sector-specific compliance drives demand for customised layouts. International funds such as Blackstone back REIT platforms that allocate a portion of grade-A assets to managed flex blocks, blending steady real-estate returns with higher-yield flex space revenue. Operators that master multi-format delivery, sector expertise, and suburban expansion are best placed to defend and grow India flexible office market share.

India Flexible Office Space Industry Leaders

WeWork

Awfis Space Solutions

Smartworks

IndiQube

Simpliwork Offices

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nuvama Asset Management and Cushman & Wakefield set up a joint venture that has already raised USD 204 million toward grade-A+ office assets across six metros. The partners aim to grow the vehicle to USD 360 million within six months, signalling sustained institutional appetite for income-yielding flex-ready buildings.

- September 2024: Mindspace Business Parks REIT disclosed plans for a 1 million sq ft data-center campus in Navi Mumbai with Princeton Digital Group. The project lifts the REIT’s data-center pipeline to 1.65 million sq ft and diversifies rental streams beyond traditional offices.

- April 2024: Embassy Group completed acquisition of WeWork Global's 27% stake in WeWork India for INR 700 crore (USD 84 million), planning to take the company public after raising INR 1,200 crore from investors while retaining 60% ownership.

- March 2024: Blackstone partnered with Sattva Group and Panchshil Realty to launch India's fourth commercial REIT in FY25, encompassing over 40 million square feet including 1-1.5 million square feet of office development.

India Flexible Office Space Market Report Scope

Flexible workspaces, often referred to as shared office spaces or flex spaces, come equipped with essentials such as phone lines, desks, and chairs. This setup caters to employees who typically work from home or telecommute, granting them the option of a physical office for a few hours weekly or monthly. The report delves deep into the India Flexible Office Space market, offering insights into prevailing trends, potential restraints, technological advancements, segment-specific details, and a look at the competitive landscape.

India's flexible office space market is segmented by type (private offices, co-working space, and virtual offices), by end-user (IT and telecommunications, media and entertainment, retail and consumer goods, and others), and by city (Delhi, Mumbai, Bangalore, Hyderabad, Pune, and Rest of India). The report offers market size and forecasts for India's flexible office space market in value (USD) for all the above segments.

By Type

| Co-Working Space |

| Serviced offices / Executive suites |

| Others (Hybrid, Virtual Office) |

By Sector

| Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) |

| Business Consulting & Professional Service |

| Other Services (Retail, Lifesciences, Energy, Legal Services) |

By End Use

| Freelancers |

| Enterprises |

| Start Ups and Others |

By City

| Mumbai Metropolitan Region |

| Delhi NCR |

| Pune |

| Bengaluru |

| Hyderabad |

| Chennai |

| Kolkata |

| Rest of India |

| By Type | Co-Working Space |

| Serviced offices / Executive suites | |

| Others (Hybrid, Virtual Office) | |

| By Sector | Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) | |

| Business Consulting & Professional Service | |

| Other Services (Retail, Lifesciences, Energy, Legal Services) | |

| By End Use | Freelancers |

| Enterprises | |

| Start Ups and Others | |

| By City | Mumbai Metropolitan Region |

| Delhi NCR | |

| Pune | |

| Bengaluru | |

| Hyderabad | |

| Chennai | |

| Kolkata | |

| Rest of India |

Key Questions Answered in the Report

What is the current size of the India flexible office market?

The India flexible office market is valued at USD 6.81 billion in 2026.

How fast will the India flexible office market grow by 2031?

It is projected to expand at a 13.58% CAGR, reaching USD 12.87 billion by 2031.

Which city holds the largest share of flex-space demand?

Bengaluru leads with 24.55% India flexible office market share in 2025.

Which segment is growing the fastest by workspace type?

Hybrid and virtual office solutions are forecast to grow at 14.35% CAGR through 2031.

Why are enterprises choosing flexible offices over traditional leases?

Hybrid work models, lower upfront costs, and technology-enabled seat management make flexible offices more economical and adaptable than long-term leases.

What risks could slow market growth?

High rent escalation in tier-1 metros and oversupply in certain micro-markets threaten operator margins and pricing power.

Page last updated on: