India Combat Vehicle Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2019 - 2024 |

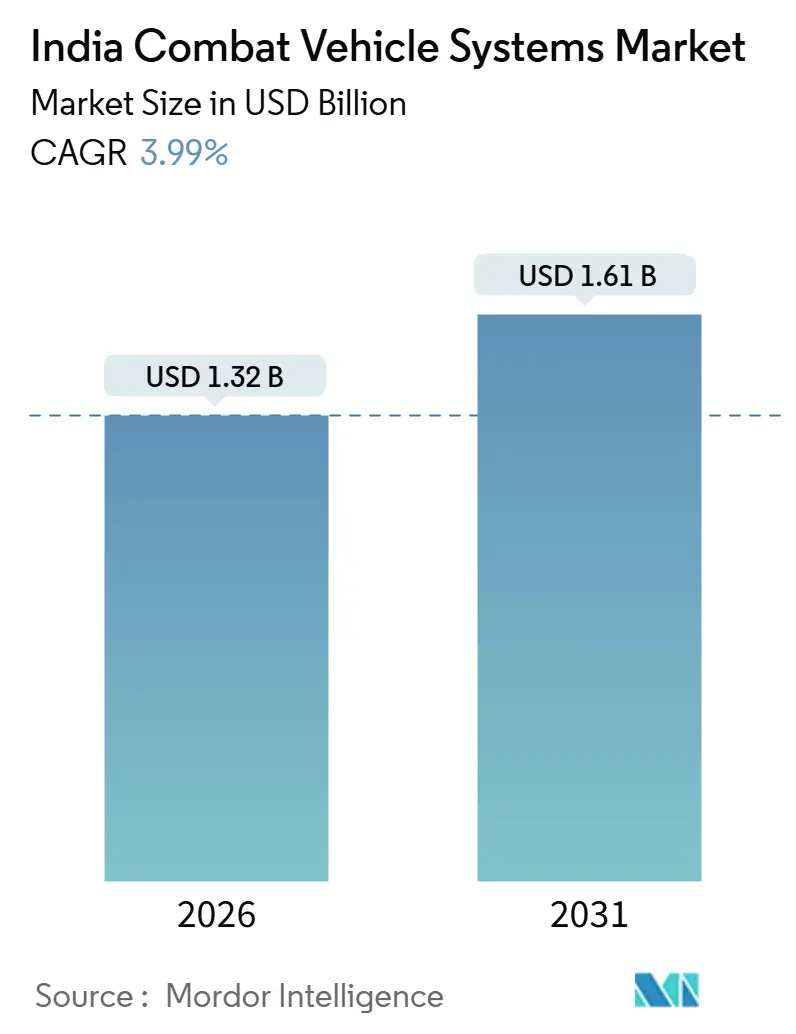

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 1.61 Billion |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Combat Vehicle Systems Market Analysis by Mordor Intelligence

The India combat vehicle systems market size is valued at USD 1.32 billion in 2026 and is projected to reach USD 1.61 billion by 2031, reflecting a 3.99% CAGR over the period. The budgetary expansion under the FY 2025-26 Union Budget, with an allocation of INR 6.81 lakh crore (approximately USD 81.72 billion) for defense, including INR 1.80 lakh crore (approximately USD 21.62 billion) for modernization, anchors long-term demand. Indigenous manufacturing mandates, multi-year upgrade cycles for T-72, T-90, and BMP-2 fleets, and the doctrinal shift toward sensor-rich vetronics shape a procurement landscape in which platform volumes rise steadily rather than sharply. Main battle tanks (MBTs) retain numerical dominance, yet wheeled and lightweight vehicles are gaining traction as the Army adapts to high-altitude and rapid-deployment requirements. Simultaneously, sensing and display subsystems outpace hull production as vetronics, AI-enabled fire-control, and counter-UAS suites become mandatory in new tenders. Competitive intensity is moderate: Armoured Vehicles Nigam Limited and Bharat Electronics Limited leverage their legacy positions, while private integrators, such as TATA Advanced Systems, Larsen & Toubro (L&T), Kalyani Strategic Systems, and Mahindra Defence, win prototype orders under Make-II, gradually eroding their historic monopolies.

Key Report Takeaways

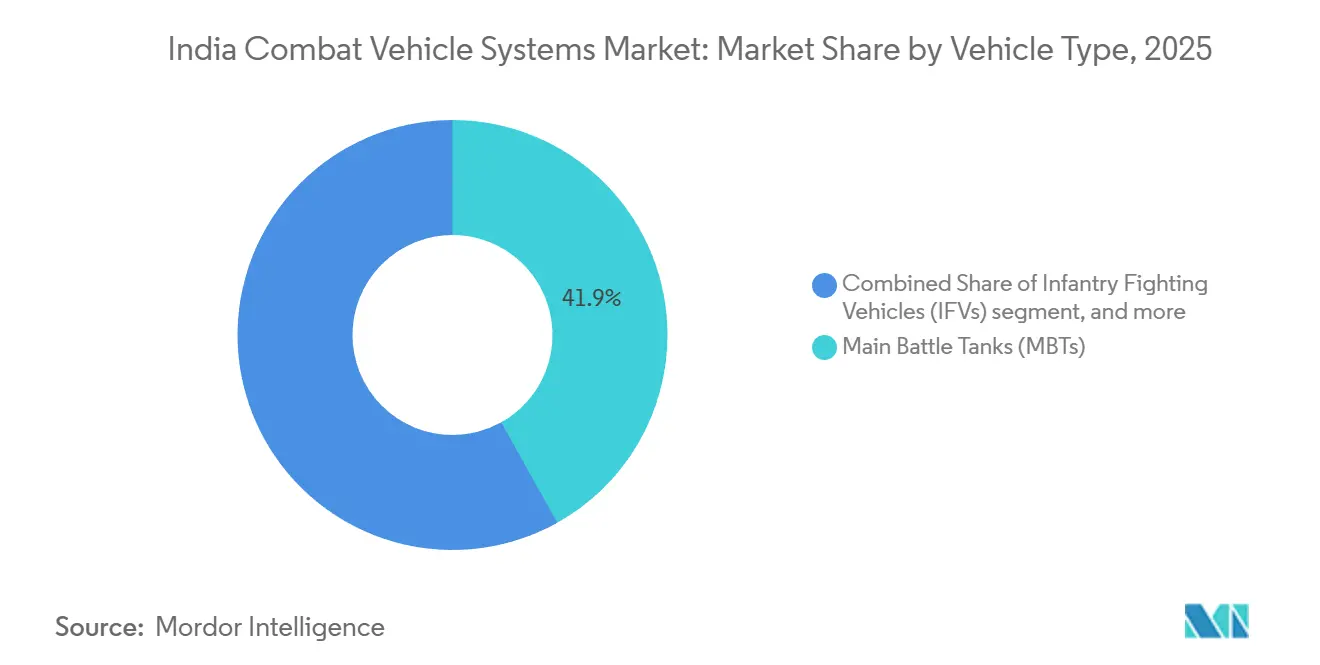

- By vehicle type, main battle tanks (MBTs) accounted for 41.89% of the India combat vehicle systems market share in 2025, while infantry fighting vehicles (IFVs) are projected to advance at a 4.87% CAGR through 2031.

- By system, weapon systems held 32.45% of the India combat vehicle systems market size in 2025, whereas sensing and display systems are forecast to expand at a 5.41% CAGR to 2031.

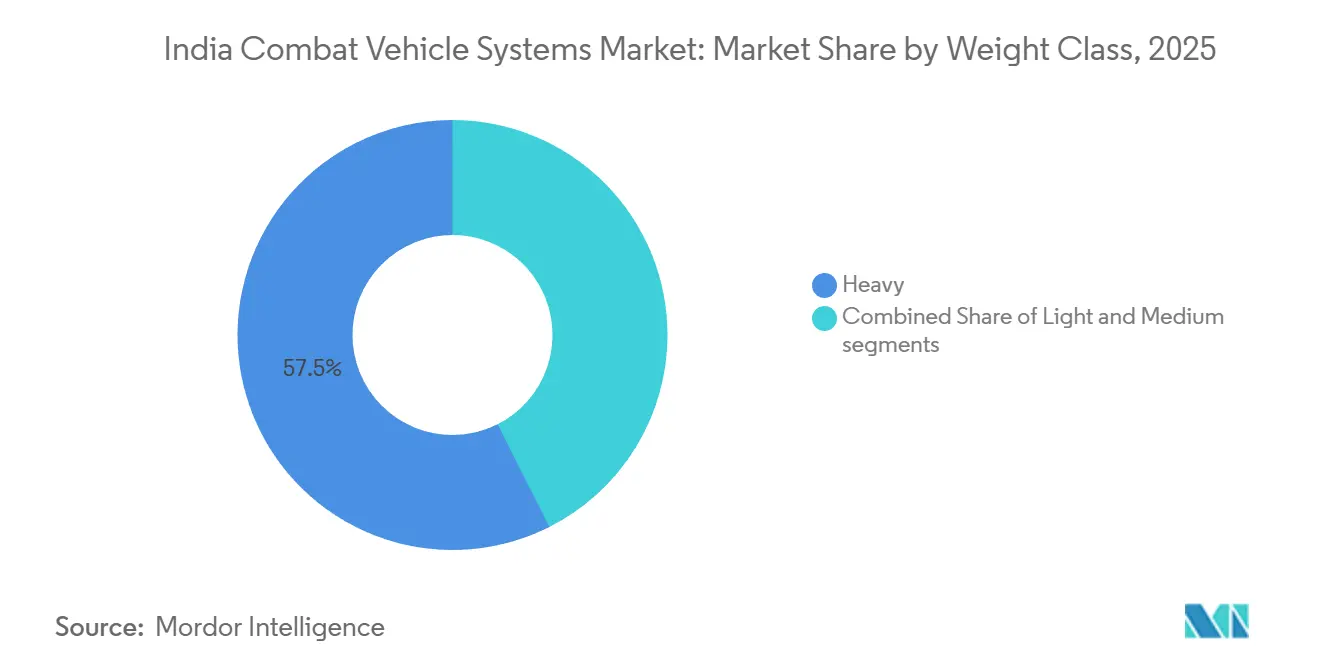

- By weight class, heavy platforms accounted for a 57.45% share of the India combat vehicle systems market in 2025; yet, light platforms are set to grow at a 7.14% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Combat Vehicle Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense budgets driving armored fleet modernization | +1.2% | National, northern and eastern commands | Medium term (2-4 years) |

| Indigenous manufacturing and localization mandates in defense procurement | +0.9% | National, Tamil Nadu, Gujarat, Maharashtra hubs | Long term (≥ 4 years) |

| Flagship combat vehicle procurement and upgrade programs | +1.5% | National, Ladakh, Rajasthan, Arunachal Pradesh | Short term (≤ 2 years) |

| Upgrade and life-extension cycles for legacy armored platforms | +0.7% | National, BMP-2/2K, T-72 fleets | Medium term (2-4 years) |

| Adoption of hybrid-electric power-pack technologies | +0.4% | National, light and medium platforms | Long term (≥ 4 years) |

| Integration of AI-enabled vetronics and predictive maintenance systems | +0.5% | National, Arjun Mk-1A, FICV prototypes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Budgets Driving Armored Fleet Modernization

The FY 2025-26 capital allocation of INR 1.80 lakh crore (USD 21.62 billion) reserves 75% for domestic procurement, guaranteeing predictable funding lines for master programs such as the 1,770-unit Future Ready Combat Vehicle (FRCV) and the roughly 1,750-unit Future Infantry Combat Vehicle (FICV). Acceptance-of-Necessity (AoN) approvals ensure multi-year contracting; however, the pivot from imports to indigenous design adds qualifying trials and manufacturing readiness reviews, thereby stretching delivery schedules. Phased induction of 590 FRCVs in the first tranche mitigates production risk but tempers near-term volumes. In parallel, life-extension packages for frontline T-72 and T-90 formations absorb a sizeable share of modernization funds, balancing readiness with new-build ambition.

Indigenous Manufacturing and Localization Mandates in Defense Procurement

The Defence Acquisition Procedure 2020 reserves 68% of capital outlays for Indian-IDDM and Make categories. Saab’s 100% FDI-backed Carl-Gustaf plant, launched in March 2024, demonstrates that design intellectual property is integral to assembly work.[1]Saab Group, “Carl-Gustaf Manufacturing in India,” saab.com Positive Indigenisation Lists released in 2024 included fire-control computers and active-protection radars, prompting integrators to consider domestic options such as Tonbo Imaging’s Elpeos, which meets 6-kilometer laser-ranging needs at 40% lower cost than imported systems.[2]Tonbo Imaging, “Elpeos Fire Control System,” tonboimaging.com Offset credits worth INR 12,000 crore (USD 1.34 billion) are set to expire between 2025 and 2027; foreign primes have begun channeling them into electric-drive research tie-ups with Indian Institutes of Technology (IITs), hedging against potential tighter future localization rules.

Flagship Combat Vehicle Procurement and Upgrade Programs

The 1,750-unit Future Infantry Combat Vehicle (FICV) program entered the Expression of Interest stage in April 2025, requiring amphibious capability and the ability to operate at altitudes of up to 5,000 m. The Zorawar light tank completed its trials in Ladakh in September 2024 and secured a 350-unit order, with deliveries scheduled to begin in 2027. Meanwhile, 693 BMP-2s are being upgraded with Nag anti-tank missiles and digital fire-control suites, extending service life by another 15 years. The Future Ready Combat Vehicle (FRCV) tender for 590 units is currently under technical evaluation, with domestic primes partnering with Korean and Russian design houses in competing bids.

Upgrade and Life-Extension Cycles for Legacy Armored Platforms

Budget discipline steers the Army toward refurbishment. Bharat Electronics is retrofitting 957 T-90s with third-generation commander sights under an INR 1,075 crore (USD 0.12 billion) contract. The BMP-2M program incorporates explosive reactive armor and digital fire control, enhancing survivability while incurring one-third of the cost of new-build alternatives. Heavy recovery vehicles ordered from Bharat Earth Movers in December 2024 ensure disabled tanks can be retrieved in contested zones, a gap highlighted by the 2020 Ladakh incident.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Procurement delays and cost overruns in major vehicle programs | -1.1% | National, all acquisition programs | Short term (≤ 2 years) |

| Dependence on imported power-train and propulsion components | -0.6% | National, Europe and Russia supply chains | Medium term (2-4 years) |

| Exposure of armored platforms to loitering munition threats | -0.4% | National, forward deployment areas | Short term (≤ 2 years) |

| Reliability and performance challenges in extreme terrain conditions | -0.3% | Northern and western commands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Procurement Delays and Cost Overruns in Major Vehicle Programs

The Arjun main battle tank’s 50-year gestation saw real per-unit costs climb 340%.[3]Comptroller and Auditor General of India, “Performance Audit of Arjun Main Battle Tank Program,” cag.gov.in FICV contracting has slipped past 2026 after three revisions, leaving 32-year-old BMP-2s awaiting replacements. Multi-layer approvals by the Defence Acquisition Council and the Directorate General of Quality Assurance routinely add 18-24 months to the timeline beyond international norms. FRCV overshot the budget by 23% in 2024; as a result, specifications had to be renegotiated, delaying induction by two more years.

Exposure of Armored Platforms to Loitering Munition Threats

Ukraine’s experience showed loitering munitions destroying 38% more armored vehicles than guided missiles, a trend that forced the Indian Army to seek 360-degree active protection in January 2024. Rafael’s Trophy system offers a 95% intercept success rate but costs very high per vehicle, exceeding the legacy T-72 electronics budgets. DRDO’s AMAP-ADS soft-kill suite cuts targeting accuracy by 70% but will not field hard-kill interceptors before 2027. Doctrinal updates require electronic warfare payloads on all vehicles within 40 kilometers of the Line of Actual Control, adding INR 2.8 crore (USD 28 million) per platform and stressing already thin capital accounts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Infantry Fighting Vehicles Gain on Doctrine Shifts

Infantry Fighting Vehicles (IFVs) are expected to post a 4.87% CAGR during the forecast period, outpacing growth in Main Battle Tanks (MBTs), despite tanks holding 41.89% of India's combat vehicle systems market share in 2025. The India combat vehicle systems market size for tracked troop carriers is expanding as the Army demands amphibious, high-altitude platforms capable of quick-change mission modules. The FICV's 1,750-unit pipeline anchors this momentum and bundles decades-long sustainment revenue. Tank fleets, by contrast, focus on electronics upgrades such as Bharat Electronics' commander-sight retrofit for 957 T-90s.[4]Bharat Electronics Limited, “Contract Awards,” bel-india.in

Secondary platforms follow similar logic. Armoured Personnel Carriers receive remote weapon stations and mine-resistant hulls, while Engineering and Maintenance Vehicles attracted fresh orders for heavy recovery trucks essential in high-altitude contingencies. The Ministry of Defence (MoD) directs that 15% of any large platform contract cover niche derivatives, thereby guaranteeing demand for bridge layers and command variants. Tonbo Imaging's Elpeos system demonstrates that indigenous sensors can now replace imports without compromising performance.

By System: Sensors and Displays Outpace Hull Fabrication

Sensing and display subsystems are projected to expand at a 5.41% CAGR, the fastest among system categories. India's combat vehicle systems market size for sensors is expected to grow on the back of BEL’s program, and commander sight retrofits, both of which deliver immediate lethality gains without the need for protracted hull assembly. Weapon systems retain a 32.45% anchor share, yet their growth rate softens as legacy gun calibers persist across life-extended fleets.

Hybrid power-distribution modules integral to DRDO’s IAVS open a novel profit pool, while Electrical Wiring and Interconnection Systems (EWIS) scale with node counts that triple in AI-driven vetronic architectures. Active protection, counter-UAS, and loitering-munition launchers fall within the others category, and Army RFIs in 2024-25 signal an accelerated procurement path, likely to lift this niche above a single-digit share by 2031.

By Weight Class: Light Platforms Accelerate for High-Altitude Agility

Light vehicles are set to expand at a 7.14% CAGR, powered by the Zorawar light tank’s 350-unit order tailored for 5,000 m operating altitudes. Heavy platforms still occupy 57.45% of the volume, but future budgets prioritize upgrades over new hull production. The India combat vehicle systems market size for light platforms benefits from air-transportability, higher power-to-weight ratios, and lower logistical footprint. Medium platforms, such as the FICV, which weighs 35 to 45 tons, strike a balance between amphibious capability and survivability.

The Infantry Protected Mobility Vehicle (IPMV) 8x8 illustrates the shift: an 18-ton platform delivering 33 horsepower per ton and a road speed of 80 km/h entered service in 2024. Tata’s WhAP 8x8 extends modularity further, allowing for the swapping of mission bays in under four hours. The FRCV’s 55-ton envelope seeks a compromise, powerful yet rail-portable, underscoring how weight considerations now shape design as much as firepower.

Geography Analysis

Northern Command received 34% of new vehicle deliveries in 2025, stocking Ladakh with Zorawar light tanks and IPMVs, which operate in thin air and require derated legacy diesel engines. Western Command concentrates on MBTs and K9 Vajra-T howitzers for desert operations; Larsen & Toubro’s December 2024 artillery award places most units in Rajasthan sectors. Eastern Command, facing jungles and rivers, drives demand for amphibious FICVs that can ford 1.5 m without special preparation.

Manufacturing clusters in Tamil Nadu, Gujarat, and Maharashtra account for 68% of production value. L&T’s Talegaon campus co-locates fabrication, assembly, and test tracks on 250 acres, cutting logistics costs by 12%. Bharat Electronics leverages Pune and Bangalore ecosystems for algorithm co-development and integration trials. Armoured Vehicles Nigam Limited upgraded its Avadi line in 2024 to handle BMP-2M retrofits, adding a 1,200 m test track.

The Directorate General of Quality Assurance operates 41 field offices that enforce MIL-STD-1553B across a range of temperature extremes, from minus 40 °C in Leh to 55 °C in Jaisalmer, creating a certification gauntlet that some foreign suppliers label a barrier, yet one that domestic firms cite to justify premium pricing. Export traction remains limited; Bharat Forge shipped 12 armored vehicles to Southeast Asia in 2024, but India lacks recent combat-proven credentials, dampening competitiveness against Israeli or Turkish peers.

Competitive Landscape

Armoured Vehicles Nigam Limited, Larsen & Toubro Limited, TATA Advanced Systems Limited, Bharat Electronics Limited, and Amphenol Interconnect India Pvt Ltd. controlled a prominent share of the 2025 contract value, leaving the remainder to more than 100 specialist vendors. Public-sector firms retain design authority for tracked platforms, while private players excel in wheeled vehicles and vetronics, where project cycles are shorter. Joint ventures satisfy offset rules and import-substitution mandates: L&T’s partnership with Hanwha Defense on the K9 Vajra-T and Tata’s long-running tie-up with Lockheed Martin Corporation exemplify this dual-track model.

Nimble entrants are carving out niches. For instance, Tonbo Imaging’s Elpeos fire-control suite displaced Israeli imports on the Arjun Mk-1A and secured multi-program traction. Paras Defence & Space Technologies supplies optronic masts to eight platforms. Intellectual property fences are being erected; L&T filed 14 patents in 2024 related to modular armor and wireless turret controls, securing design advantages for the Zorawar light tank. The Strategic Partnership route in the Defence Acquisition Procedure intentionally awards long-term production monopolies to a single Indian prime plus one foreign collaborator, further tightening the field.

India Combat Vehicle Systems Industry Leaders

TATA Advanced Systems Limited

Larsen & Toubro Limited

Amphenol Interconnect India Pvt Ltd.

Bharat Electronics Limited

Armoured Vehicles Nigam Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: The Indian Army contracted L&T to produce BvS10 Sindhu vehicles domestically, with technical and design support from BAE Systems Hagglund's as part of a collaboration between L&T and BAE Systems plc.

- March 2024: The Indian Ministry of Defence (MoD) signed a Memorandum of Understanding (MoU) for next-generation combat vehicle technologies. Three defense public sector undertakings, BEML Limited, Bharat Electronics Limited, and Mishra Dhatu Nigam Limited (MIDHANI), united to develop an Advanced Fuelling and Control System. This MoU aims to bolster the indigenous development of this system for engines tailored to heavy-duty applications.

- February 2023: India's Defence Acquisition Council approved the procurement of the Futuristic Infantry Combat Vehicle (FICV) for the Indian Army. The FICV should have an automated activation response system that will suppress the fire within 130 milliseconds in the crew compartment and 10 seconds in engine compartments.

India Combat Vehicle Systems Market Report Scope

A combat vehicle is a technologically advanced vehicle used in war that is fitted with partial or complete armor plating for protection against bullets, shell fragments, and other projectiles. Militaries primarily use combat vehicles, which move either on wheels or continuous tracks.

The Indian combat vehicle systems market is segmented based on vehicle type, system, and weight class. By vehicle type, the market is segmented into main battle tanks (MBTs), infantry fighting vehicles (IFVs), armored personnel carriers (APCs), engineering and maintenance vehicles, and others. The market is segmented by systems into sensing and display systems, power distribution systems, electrical wiring interconnection systems (EWIS), control systems, and others. By weight class, the market is segmented into light, medium, and heavy. For each segment, the market size is provided in terms of value (USD).

| Main Battle Tanks (MBTs) |

| Infantry Fighting Vehicles (IFVs) |

| Armored Personnel Carriers (APCs) |

| Others |

| Sensing and Display Systems |

| Power Distribution Systems |

| Electrical Wiring and Interconnection Systems (EWIS) |

| Navigation Systems |

| Weapon Systems |

| Others |

| Light |

| Medium |

| Heavy |

| By Vehicle Type | Main Battle Tanks (MBTs) |

| Infantry Fighting Vehicles (IFVs) | |

| Armored Personnel Carriers (APCs) | |

| Others | |

| By System | Sensing and Display Systems |

| Power Distribution Systems | |

| Electrical Wiring and Interconnection Systems (EWIS) | |

| Navigation Systems | |

| Weapon Systems | |

| Others | |

| By Weight Class | Light |

| Medium | |

| Heavy |

Key Questions Answered in the Report

How large is the India combat vehicle systems market in 2026?

The India combat vehicle systems market size is valued at USD 1.27 billion in 2026.

What is the expected growth rate for India’s combat vehicle systems between 2026 and 2031?

The market is forecasted to grow at a 3.99% CAGR during the period.

Which segment will grow fastest through 2031?

Infantry Fighting Vehicles (IFVs) are projected to expand at a 4.87% CAGR, the quickest among vehicle types.

Why are light platforms attracting attention?

Light vehicles such as the Zorawar tank enable rapid deployment to high-altitude sectors and are forecasted to grow at a 7.14% CAGR.

Which system category is seeing the highest growth?

Electrical Wiring and Interconnection Systems (EWIS) will advance at a 5.41% CAGR as hybrid-electric architectures proliferate.

Page last updated on: