Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 32.12 Billion |

| Market Size (2031) | USD 42.18 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

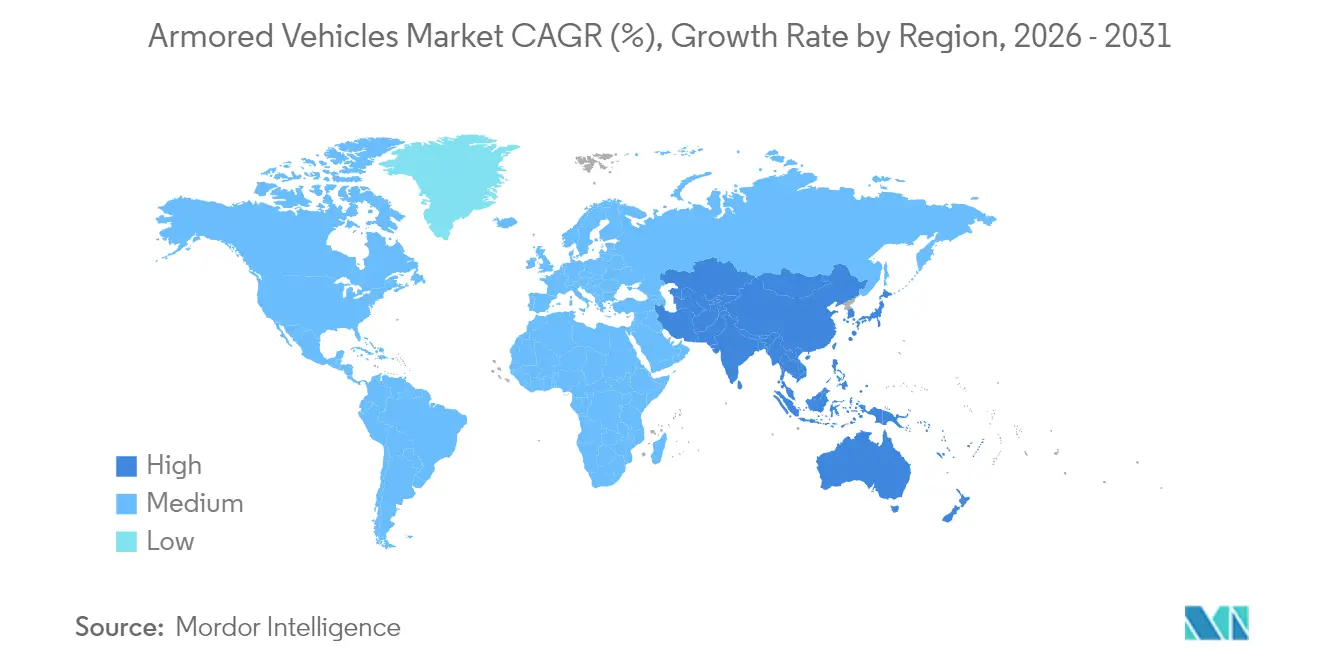

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Armored Vehicles Market Analysis by Mordor Intelligence

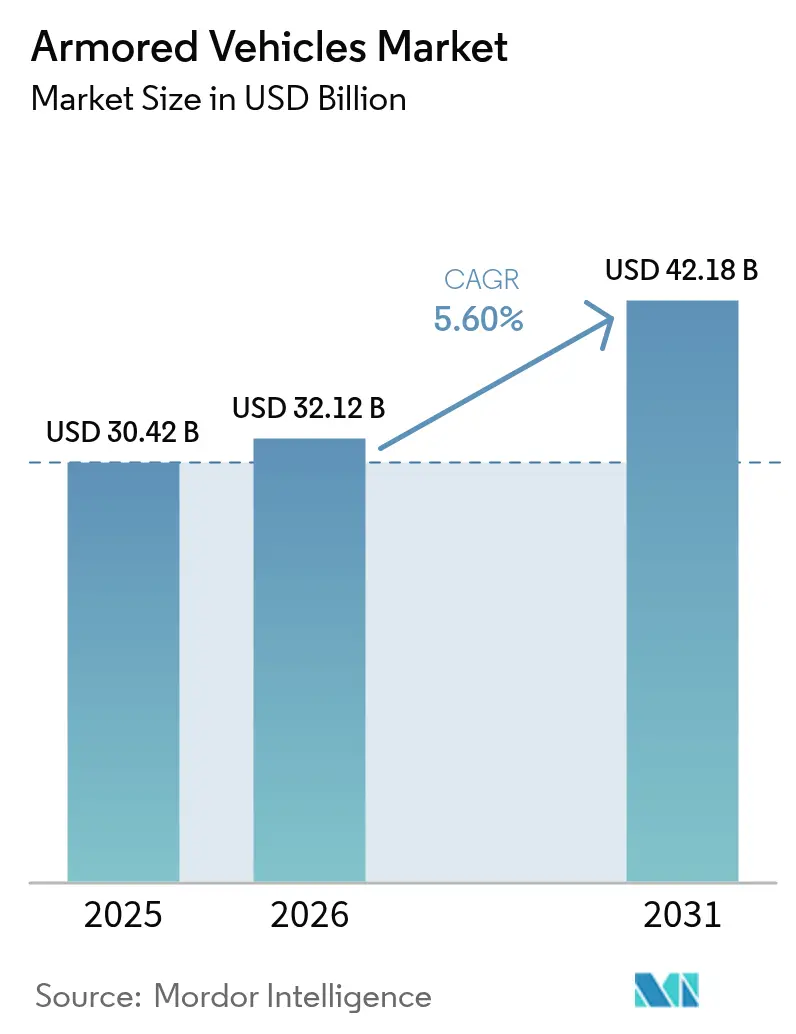

The armored vehicles market size is expected to grow from USD 30.42 billion in 2025 to USD 32.12 billion in 2026 and is forecast to reach USD 42.18 billion by 2031 at 5.6% CAGR over 2026-2031. The demand uptrend reflects intensified recapitalization programs across NATO, elevated procurement in the Asia-Pacific region, and a fast-rising interest in silent-watch electric variants that enhance survivability while reducing fuel burn. Germany’s decision to order 8,500 new vehicles, Poland’s rapid tank buys from South Korea, and India’s Future Infantry Combat Vehicle requirement illustrate how governments are shortening acquisition timelines and favoring modular designs that can be fielded quickly. Competitive rivalry escalates as primes pursue mega-contracts, such as the USD 45 billion XM30 program, and bolt-on acquisitions that shore up US supply-chain access and active-protection know-how. Supply-side friction remains, however, with rare-earth and armor-ceramic shortages slowing line-rate increases and prompting Western governments to subsidize domestic forging capacity.

Key Report Takeaways

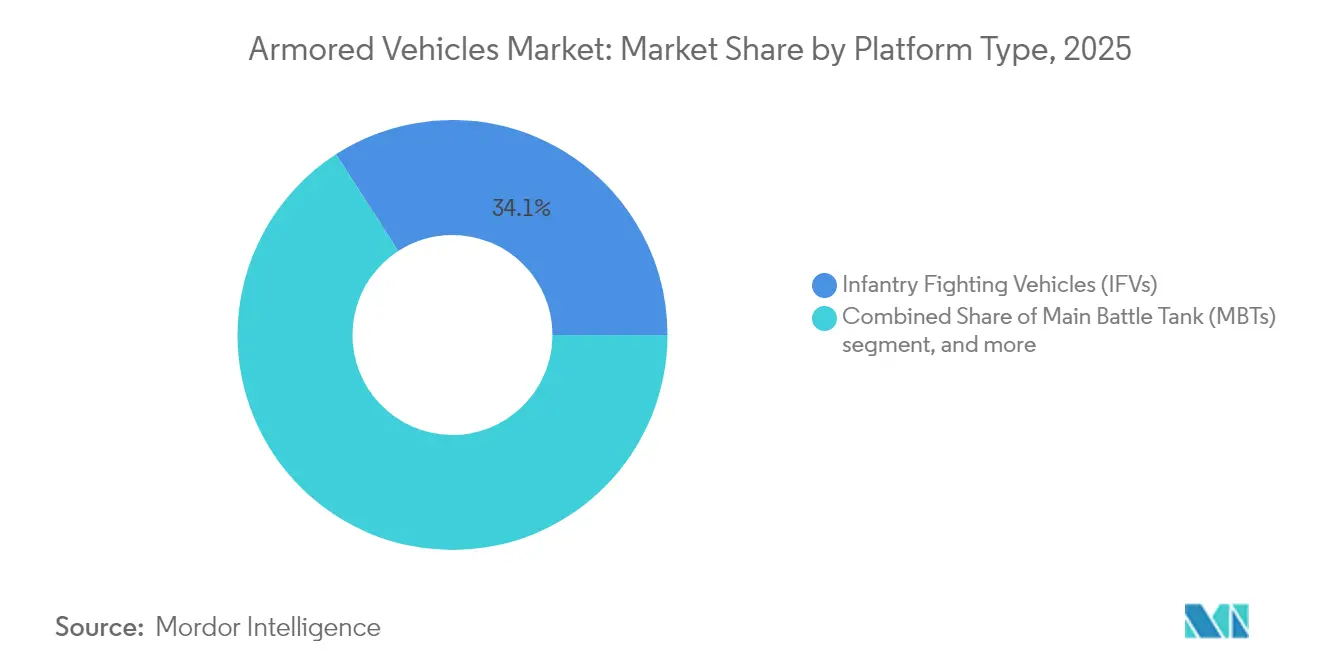

- By platform type, infantry fighting vehicles (IFVs) held 34.12% of the armored vehicle market share in 2025, while armored personnel carriers (APCs) are projected to advance at a 6.95% CAGR to 2031.

- By mobility, wheeled systems commanded a 72.63% share of the armored vehicles market size in 2025, and tracked platforms are expected to expand at an 8.65% CAGR through 2031.

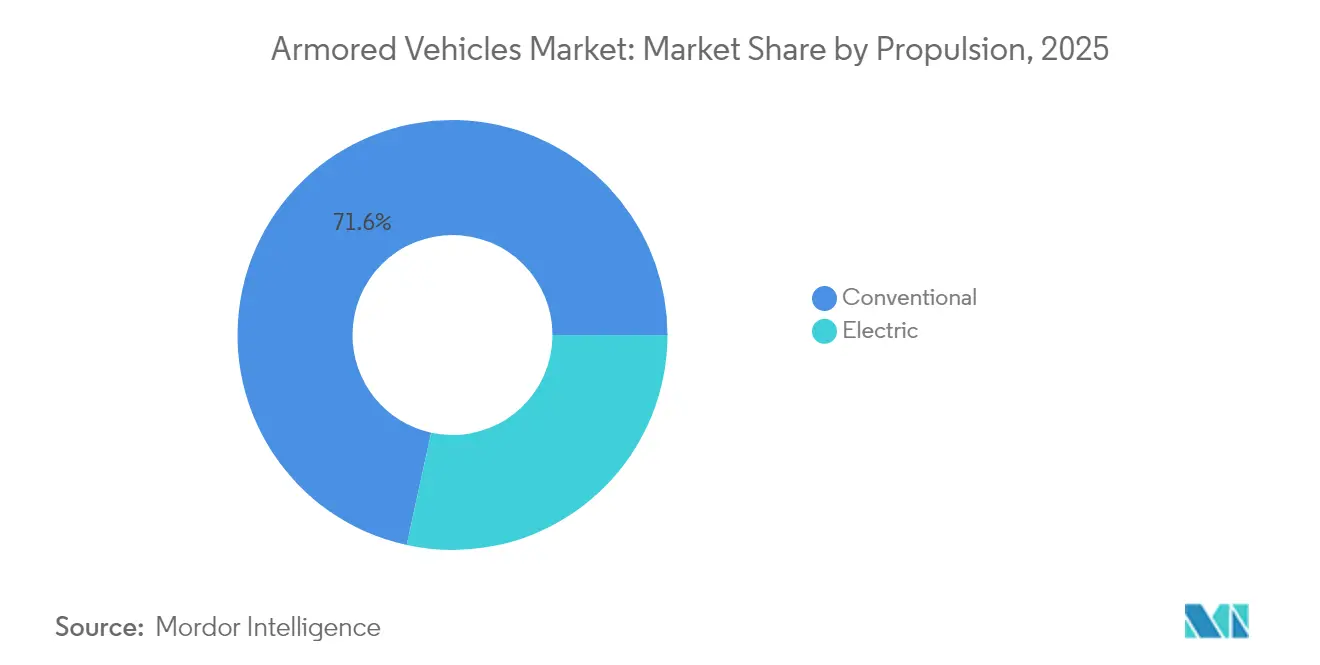

- By propulsion, conventional powertrains accounted for 71.58% of the armored vehicles market in 2025, whereas electric systems are forecasted to post a 8.92% CAGR between 2026 and 2031.

- By end-user, armies controlled 53.64% of the armored vehicles market share in 2025, and demand from special forces is projected to grow at an 8.19% CAGR through 2031.

- By geography, Europe led with a 42.41% revenue share in 2025, and the Asia-Pacific region is projected to grow at a 6.98% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Armored Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid recapitalization programs in NATO and Asia | (+) 1.20% | North America and Europe, APAC core | Medium term (2-4 years) |

| Elevated land-warfare demand post-Ukraine conflict | (+) 1.00% | Global, concentrated in Europe and NATO allies | Short term (≤ 2 years) |

| Wheeled 8×8 platforms favored for expeditionary ops | (+) 0.80% | Global, particularly NATO and allied nations | Medium term (2-4 years) |

| Battlefield electrification and silent-watch capability | (+) 0.60% | North America and Europe, spill-over to APAC | Long term (≥ 4 years) |

| Modular active-protection system (APS) retrofits | (+) 0.70% | Global, concentrated in NATO and APAC | Medium term (2-4 years) |

| IFV surge to modernize combined-arms doctrine | (+) 0.50% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Recapitalization Programs in NATO and Asia

NATO members inject a record amount of funds into their heavy-armor fleets, reversing three decades of drawdowns. Germany increased its defense spending to 5% of GDP and placed multi-billion-dollar orders for Boxer and Patria vehicles, which will reshape the European force structure. Poland directed USD 6.5 billion toward K2 tanks from South Korea to speed deliveries outside traditional Western channels. The Netherlands reactivated a tank battalion with 46 Leopard 2A8 units, highlighting how even former post-tank nations now regard tracked armor as indispensable. India’s Future Ready Combat Vehicle call for 1,770 platforms in Asia, combined with China’s ongoing Type 99A upgrades, signals a parallel surge in demand. The synchronized orders underpin a multi-year production boom that allows OEMs to amortize new welding halls, robotic paint lines, and modular digital-assembly tooling across global programs.

Elevated Land-Warfare Demand Post-Ukraine Conflict

The Ukraine war has affirmed the centrality of armored vehicles in peer warfare. Kyiv’s need for 23,000 vehicles demonstrated extreme battlefield burn rates, forcing NATO planners to audit inventories and accelerate backfill orders. Survivability gaps became clear, driving retrofits such as the USD 37 million Iron Fist APS award for US Bradley fleets after combat validation.[1]Elbit Systems Press Office, “Elbit Systems Awarded USD 37 Million Contract to Supply Iron Fist APS,” elbitsystems.com Once set at 10-15 years, procurement cycles are collapsing to 3-5 years, compelling primes to front-load production capacity and governments to accept incremental upgrades while full-rate lines are ramping up.

Wheeled 8×8 Platforms Favored for Expeditionary Operations

Strategic planners now favor wheeled 8×8 chassis for rapid theater shifts, eliminating the need for heavy-equipment transporters. Germany’s 5,000-unit Boxer framework order underscores the shift, with plug-and-play mission modules supporting infantry, command, and medical evacuation roles. Wheeled fleets deliver higher road speed and lower maintenance cost than tracked peers, attributes prized for dispersed Indo-Pacific operations. Survivability remains a focus after Ukraine revealed tire vulnerability, prompting the adoption of thicker appliqué armor, run-flat inserts, and APS integration as a standard fit across NATO programs.[2]Courtney Albon, “Army Rethinks Survivability for Tactical Wheeled Vehicles,” National Defense Magazine, nationaldefensemagazine.org

Battlefield Electrification and Silent-Watch Capability

Hybrid-electric drivetrains enable silent creep and persistent sensor watch without engine idle, reducing acoustic and thermal signatures. The US Army validated a 20% fuel-burn cut on its hybrid Bradley demonstrator while proving silent mobility in extended observation posts. GM Defense’s NGTV-H further adds exportable power for drones and jammers that demand stable onboard generation. Industry consensus aligns around hybrid bridges transitioning to full battery vehicles once energy density surpasses the 300 Wh/kg threshold, anticipated near the end of the forecast window.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ballooning unit costs and stretched defense budgets | -0.80% | Global, particularly acute in Europe and developing nations | Short term (≤ 2 years) |

| Industrial supply-chain chokepoints in armour ceramics | -0.60% | Global, concentrated impact in North America and Europe | Medium term (2-4 years) |

| ESG pressure against heavy carbon-footprint fleets | -0.40% | North America and Europe, limited impact in APAC and MEA | Long term (≥ 4 years) |

| Complex export-licensing/ITAR barriers | -0.30% | Global, most acute for cross-border programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ballooning Unit Costs and Stretched Defense Budgets

Modern armor platforms now cost well into eight figures. The M10 Booker price has climbed to USD 19 million per unit, while Germany’s Leopard 2A8 buy totals EUR 2.9 billion (USD 3.35 billion) for 105 tanks, squeezing even affluent treasuries.[3]Marcus Weisgerber, “General Dynamics Gets USD 323M Production Contract for Booker Combat Vehicles,” Inside Defense, insidedefense.com The US Army’s 2025 force-structure reset cancelled multiple vehicle lines and trimmed Stryker orders to cap spending. Smaller nations are extending the service lives of their vehicles or sourcing surplus MRAPs, as Morocco did with 50 M-ATVs, thereby bypassing new-build queues. Rising interest rates and inflation compound affordability concerns, forcing ministries to trade off between airpower, drones, and ground-force recapitalization.

Industrial Supply-Chain Chokepoints in Armor Ceramics

Armor ceramics, rare-earth magnets, and high-strength forgings are subject to chronic shortages. The US forging sector has lost 241 plants since 2000 and now runs at 52% capacity, restricting hull and turret output pace. China refines the bulk of global rare earths, presenting a strategic chokepoint should geopolitical tensions escalate. European chemical supply disruptions threaten propellant coatings and fire-suppressant agents vital to crew-survivability systems.[4]Giulia Tarpanelli, “Running on Empty: The Chemical Shortage Undermining European Defence,” European Policy Centre, epc.eu Governments fund stockpiles and domestic mines, but the lead times of five years or more limit near-term relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: IFV Dominance Drives Combined-Arms Evolution

IFVs generated 34.12% of the armored vehicles market in 2025 and remain the centerpiece assets in mechanized brigades. Their balance of troop-carrying capacity and 30–50 mm cannons supports combined-arms tactics from the Baltic forests to the Indo-Pacific littorals. Nations are upgrading legacy fleets with situational-awareness suites and programmable airburst rounds that counter unmanned aerial targets. Supplier consolidation, such as Leonardo's takeover of Iveco Defence, is expected to streamline turret integration, steering the armored vehicle market toward a standard digital backbone.

APCs are expanding at a 6.95% CAGR, fueled by lessons from Ukraine that stress troop protection over firepower. Lightweight MRAP designs with V-hulls and blast-attenuating seats are entering police special-operations arsenals, a spillover that diversifies revenue beyond defense ministries. MBTs are undergoing modernization rather than fleet growth, with active-protection kits and sensors extending the platform's relevance. Light reconnaissance vehicles capture niche demand for rapid-strike missions, integrating AI-powered crew aids that reduce operator workload.

By Mobility: Wheeled Platforms Reshape Strategic Doctrine

Wheeled designs held 72.63% of the armored vehicles market share in 2025, a dominance rooted in their ability to self-deploy over paved networks without tank transporters. NATO rapid-reaction brigades favor 8×8 chassis that cruise at highway speeds while offering scalable armor packages. The design trend in the armored vehicle market emphasizes independent suspension, run-flat tires, and central tire inflation to navigate mixed terrain.

Tracked platforms, though smaller in number, are rebounding at an 8.65% CAGR as armies relearn the need for cross-country mobility and heavy frontal protection against tandem-warhead threats. Modern tracks utilize segmented rubber composite pads that enhance road life while maintaining off-road traction. The hybrid fielding of both mobility types allows commanders to tailor task forces, a flexibility that underpins future doctrine.

By Propulsion: Electric Revolution Accelerates

Conventional diesels still power 71.58% of the armored vehicles market, valued for their reliability and global fuel logistics. Yet electric propulsion is pacing the market at a 8.92% CAGR as silent-watch missions and carbon targets converge. Hybrid gensets that supply 300 kW of peak electric drive are already equipped on demonstrators and can be retrofitted to legacy hulls via drop-in power packs. The armored vehicle industry is investing in solid-state batteries and cooling loops capable of handling 100 °C desert environments, overcoming earlier thermal constraints. Charging infrastructure remains a barrier to expeditionary operations, limiting the adoption of fully electric vehicles to modest levels until theater micro-grid solutions mature.

By End-User: Army Dominance and Special Forces Surge

Army formations accounted for 53.64% of the armored vehicles market demand in 2025, outpacing other buyers, as the combined-arms doctrine relies on tanks, IFVs, and APCs in integrated task forces. Force-structure growth in Eastern Europe and Indo-Pacific border regions underwrites long-term baseline orders. Special forces are the fastest-growing segment, with an 8.19% CAGR, favoring lightweight platforms equipped with swarm-drone control consoles and signature-management coatings for clandestine raids. Marine and naval infantry procure amphibious combat vehicles that enhance mobility and survivability, as proven by the US Marine Corps’ first Indo-Pacific deployment in 2025.

Geography Analysis

Europe accounted for 42.41% of the armored vehicles market revenue in 2025, driven by Germany’s record orders for the Boxer and Patria, as well as purchases from Nordic consortiums. Eastern members allocate more than 3% of GDP to defense, channeling funds to tracked fleets that bolster Article 5 deterrence. Western states emphasize wheeled fleets for out-of-area deployments, blending strategic lift economy with urban maneuverability.

Asia-Pacific follows as the fastest climber at a 6.98% CAGR. India’s Future Infantry Combat Vehicle tender for 1,750 units worth INR 600 billion (USD 7.2 billion) and China’s Type 99A progressive upgrades energize regional integrators. Japan explores wheeled modular chassis to supplement its Type 10 tank fleet, and Australia pivots to Land 400 Phase 3, reinforcing its infantry close-combat edge.

North America maintains steady modernization budgets, anchored by the XM30 and JLTV A2 programs, which incorporate AI mission cores and hybrid drivetrains. Canada backfills LAV 6.0 attrition losses with domestically produced variants, ensuring supply-chain sovereignty. Mexico invests in refurbished MRAPs for internal security, representing a small but steady aftermarket.

The Middle East allocated USD 78 billion in Saudi defense outlays for 2025, including prospective AyM 2030 armored formations tailored for desert warfare. Gulf buyers prefer high power-to-weight ratios for dune mobility and active cooling kits. Africa remains opportunistic, sourcing surplus vehicles via US Excess Defense Articles and refurb projects.

Competitive Landscape

The armored vehicles market exhibits moderate concentration, with the top five suppliers accounting for a significant global revenue share. General Dynamics, Rheinmetall, KMW, BAE Systems, and Leonardo anchor this tier and battle for the USD 45 billion XM30 program, which could significantly swing their share. M&A momentum is reshaping capabilities; Rheinmetall’s USD 950 million acquisition of Loc Performance secures transmission expertise and a US manufacturing footprint. Leonardo’s EUR 1.70 billion (USD 1.96 billion) integration of Iveco Defence creates an Italian land-systems leader capable of bidding as prime on European Tank Main Ground Combat System (MGCS) efforts.

Tier-two entrants specialize in electric propulsion, APS, and autonomy, siphoning sub-system revenues from primes. GM Defense partners with battery start-ups, and Raytheon prototypes virtual crew assistants that could slash manpower needs by 30%. Supply-chain resilience is now a key competitive metric; OEMs are realigning their strategies toward dual-sourcing of armor ceramic lines and investing in domestic rare-earth magnet production facilities.

Joint-venture structures proliferate to localize content, meeting offset rules in Greece, Indonesia, and Brazil while tapping lower labor costs. These partnerships complicate ITAR compliance but grant market entry where single-nation primes lack incumbent status.

Armored Vehicles Industry Leaders

Rheinmetall AG

General Dynamics Corporation

BAE Systems plc

Oshkosh Corporation

KNDS N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Germany confirmed plans to acquire 3,000 Boxer and 3,500 Patria vehicles under new constitutional defense spending.

- May 2025: The Netherlands fielded a new battalion with 46 Leopard 2A8 tanks stationed in Germany.

- April 2025: KNDS and Metlen agreed to produce 370 VBCI Philoctetes IFVs in Greece under the EU ReArm program.

- April 2025: Four Nordic countries launched a EUR 8 billion (USD 9.24 billion) procurement for 870 CV90 vehicles to build an integrated mechanized force.

Global Armored Vehicles Market Report Scope

An armored vehicle is a technologically advanced vehicle that is fitted with partial or complete armor plating for protection against bullets, shell fragments, and other projectiles. Armored vehicles are majorly used by armed forces and move either on wheels or on continuous tracks.

The armored fighting vehicles market is segmented based on type and geography. By type, the market is segmented into armored personnel carrier (APC), infantry fighting vehicle (IFV), mine-resistant ambush protected (MRAP), main battle tank (MBT), and other types. The other types consist of self-propelled artillery, light armored vehicles, reconnaissance vehicles, light utility vehicles, bridge vehicles, engineering vehicles, recovery vehicles, military trucks, and heavy equipment transport (HET) military vehicles. By geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, Middle-East, and Africa. The report also covers the market sizes and forecasts across the major regions.

For each segment, the market sizing and forecasts have been done based on value (USD).

By Platform Type

| Armored Personnel Carriers (APCs) |

| Infantry Fighting Vehicles (IFVs) |

| Mine-Resistant Ambush-Protected (MRAP) |

| Main Battle Tanks (MBTs) |

| Light Protected/Recon Vehicles |

| Others |

By Mobility

| Wheeled (4×4, 6×6, 8×8) |

| Tracked |

By Propulsion

| Conventional |

| Electric |

By End-User

| Army |

| Marine/Naval Infantry |

| Special Forces |

| Homeland Security |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform Type | Armored Personnel Carriers (APCs) | ||

| Infantry Fighting Vehicles (IFVs) | |||

| Mine-Resistant Ambush-Protected (MRAP) | |||

| Main Battle Tanks (MBTs) | |||

| Light Protected/Recon Vehicles | |||

| Others | |||

| By Mobility | Wheeled (4×4, 6×6, 8×8) | ||

| Tracked | |||

| By Propulsion | Conventional | ||

| Electric | |||

| By End-User | Army | ||

| Marine/Naval Infantry | |||

| Special Forces | |||

| Homeland Security | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Poland | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the armored vehicles market size in 2026 and how fast will it grow through 2031?

The armored vehicles market is valued at USD 32.12 billion in 2026 and is projected to climb at a 5.6% CAGR, reaching USD 42.18 billion by 2031.

Which region currently generates the highest share of armored vehicle sales?

Europe leads with 42.41% of global revenue in 2025.

Which region is expected to record the quickest expansion?

Asia-Pacific is set to advance at a 6.98% CAGR between 2026 and 2031.

How dominant are wheeled armored vehicles compared with tracked variants?

Wheeled platforms commanded 72.63% of 2025 revenues, reflecting preference for rapid self-deployability.

Who buys the most armored vehicles by end user?

Army formations account for 53.64% of global purchases in 2025.

What is the growth outlook for Armored Personnel Carriers?

Armored Personnel Carriers (APCs) are projected to increase at a 6.95% CAGR through 2031.

Which technology segment shows the highest projected CAGR?

Electric propulsion tops the field with a 8.92% CAGR, driven by silent-watch and fuel-efficiency benefits.

Page last updated on: