Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.08 Billion |

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 1.87 Billion |

| Growth Rate (2026 - 2031) | 9.61% CAGR |

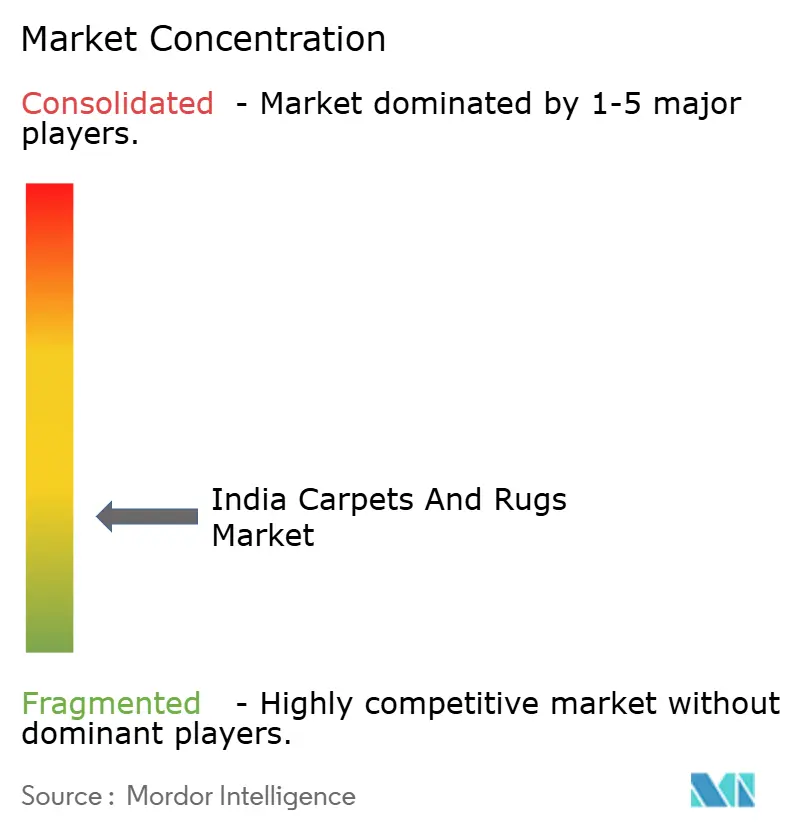

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Carpets And Rugs Market Analysis by Mordor Intelligence

India carpets and rugs market size in 2026 is estimated at USD 1.18 billion, growing from 2025 value of USD 1.08 billion with 2031 projections showing USD 1.87 billion, growing at 9.61% CAGR over 2026-2031. This robust trajectory mirrors strong domestic demand, the country’s 40% share of global handmade-carpet exports, and sustained government incentives that strengthen artisanal clusters[1]Source: Indian Brand Equity Foundation, “Handicrafts Industry & Exports,” ibef.org. Technology-driven machine-tufting, widening e-commerce reach, and luxury-oriented sustainability preferences further accelerate uptake across residential and commercial renovations. At the same time, policy tools such as PM MITRA parks and Production Linked Incentives lower entry barriers, enlarge formal employment, and draw global buyers toward traceable, premium offerings. Strategic investments in renewable energy, digital authentication, and modular tile formats position manufacturers to capture margin upside while meeting ESG expectations.

Key Report Takeaways

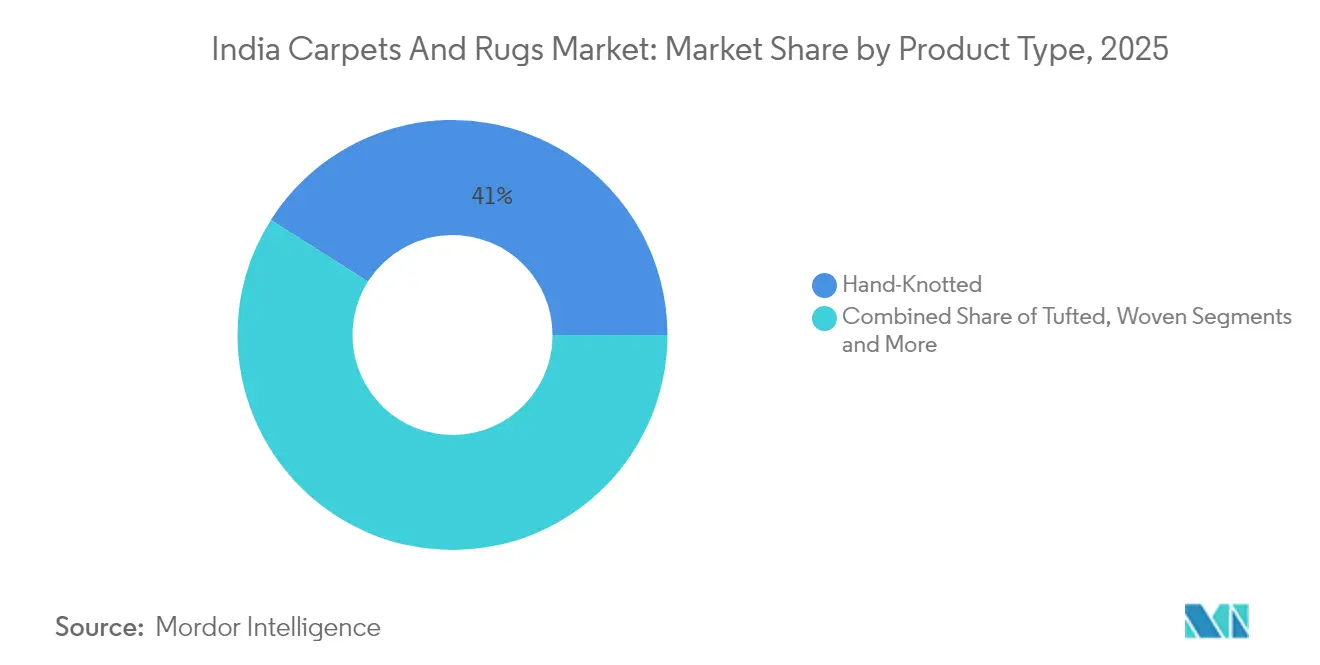

- By product type, hand-knotted carpets held 41.02% of the India carpets and rugs market share in 2025, while machine-tufted products are forecast to expand at a 10.98% CAGR through 2031.

- By material, wool commanded a 46.55% share of the India carpets and rugs market size in 2025, whereas polypropylene is projected to grow at a 10.08% CAGR to 2031.

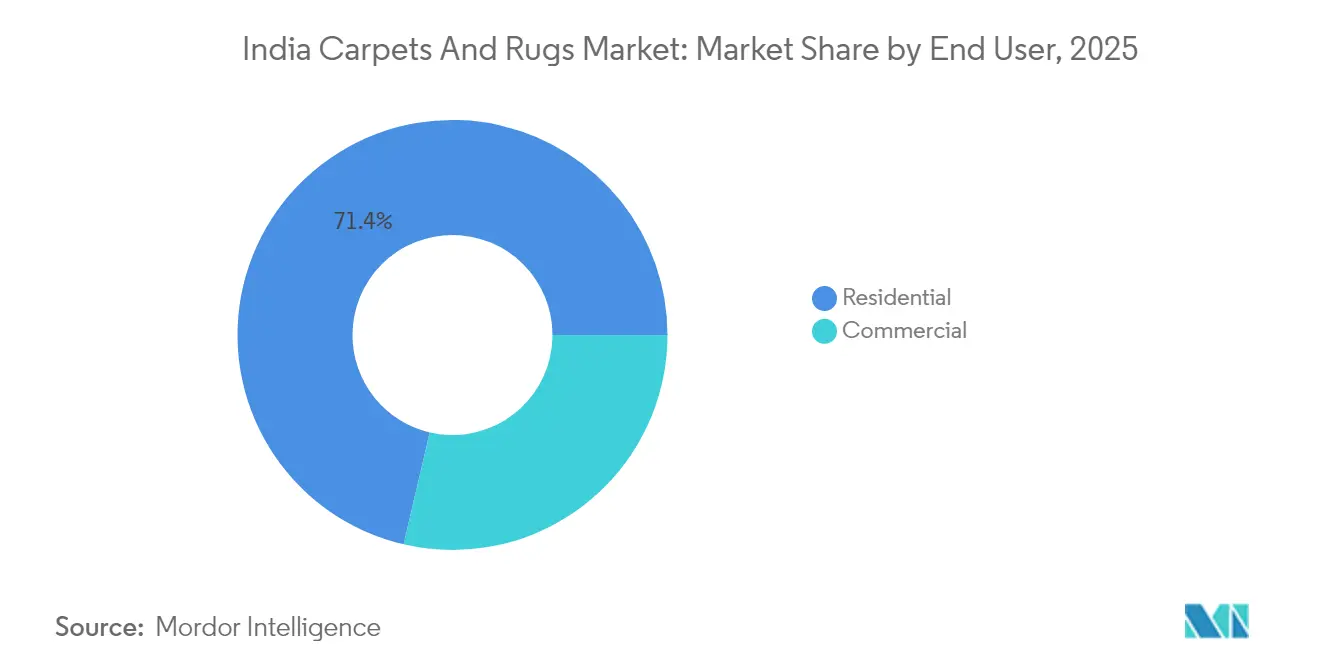

- By end user, residential applications accounted for a 71.35% share in 2025, and commercial demand is advancing at a 11.76% CAGR through 2031.

- By distribution channel, B2C retail maintained 83.92% revenue share in 2025; B2B direct sales are rising at a 9.41% CAGR between 2026-2031.

- By region, North India led with a 33.72% share in 2025, whereas West India is on track for an 11.36% CAGR to 2031.

- The India carpets and rugs market exhibits moderate fragmentation, top players such as Jaipur Rugs Company, Welspun India Ltd, Obeetee Pvt Ltd, Shaw Industries Group Inc, Surya Carpets Pvt Ltd holds major market share.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Carpets And Rugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of organised décor retail & e-commerce | +1.8% | North & West India, global reach | Short term (≤ 2 years) |

| Government incentives and textile-cluster expansion | +1.5% | UP, Gujarat, Rajasthan | Medium term (2-4 years) |

| Premiumization & demand for sustainable natural-fiber carpets | +1.2% | Urban India, US & EU export markets | Medium term (2-4 years) |

| Export-oriented hand-knotted gains from US/EU tariff preferences | +1.0% | Northern hubs, global buyers | Long term (≥ 4 years) |

| Adoption of carpet tiles in hybrid-office refurbishments | +0.7% | Metro commercial districts | Short term (≤ 2 years) |

| Hospitality boom ahead of major sporting & G20 projects | +0.6% | Tourism corridors, metro infrastructure zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Organized Décor Retail & E-Commerce

Amazon’s Global Selling program alone enabled 150,000 Indian exporters to ship USD 13 billion worth of goods by 2024, with home textiles among the top categories. Mobile apps now aggregate micro-orders, streamline raw-yarn procurement, and ensure timely digital payments, thereby empowering over 2 million weavers who historically relied on multi-tier intermediaries. Government-run AIICE underscores the creative economy’s 8% workforce share and spotlights digital intelligence as essential for sustaining cottage industries. These converging forces expand the India carpets and rugs market’s effective addressable audience, compress fulfillment lead times, and reinforce price transparency that rewards genuine craftsmanship.

Government Incentives and Textile-Cluster Expansion

Union Budget 2025-26 raised textile outlays 19% to INR 5,272 crore, earmarking modern parks, R&D centers, and skill missions that directly support carpet production[2]Source: Invest India, “Union Budget 2025-26 Textile Allocations,” investindia.gov.in.. Seven PM MITRA parks are slated to generate 300,000 jobs each, while the PLI scheme reserves more than INR 10,000 crore for export-ready value addition. Uttar Pradesh is fast-tracking private parks, with Lonex Textile Park in Shamli set for December 2025 commissioning and 5,000 new positions. The RoSCTL rebate extension keeps zero-rated export status intact, buffering SMEs against logistics-driven cost spikes. Collectively, these incentives sharpen India’s comparative edge over Bangladesh and Vietnam and channel fresh capital into the India carpets and rugs market’s core manufacturing belts.

Premiumization & Demand for Sustainable Natural-Fiber Carpets

Urban consumers and foreign buyers increasingly reward low-carbon, traceable carpets. Welspun Living pledges carbon neutrality by 2030, leveraging biomass-based energy and recyclable backing layers. Reliance Industries’ ECOTHERM fiber debuted at Bharat Tex 2024, offering lightweight insulation without compromising dyeability. Mohawk Industries reports a 36% greenhouse-gas-intensity cut since 2010, pointing to sector-wide environmental gains[3]Source: Mohawk Industries 2024 Annual Report, mohawkindustries.com. Wool carpet exports touched USD 1.34 billion in FY 2024, aided by the Integrated Wool Development Programme’s INR 126 crore quality push. Such initiatives allow producers to command premium tags, diversify revenue toward ESG-compliant niches, and future-proof the India carpets and rugs market against stricter Western procurement codes.

Export-Oriented Hand-Knotted Segment Gains from US/EU Tariff Preferences

Hand-knotted exports delivered USD 1.39 billion in FY 2024 and still enjoy favorable duties in the EU, preserving India’s 40% global share. Recent US tariff hikes, however, threaten 70% of outbound volumes, compelling the Carpet Export Promotion Council to lobby for separate HSN codes that shield artisanal SKUs. The RoDTEP rebate now clears within 15 days, easing liquidity for SME exporters. Large B2B trade fairs continue to secure multibillion-rupee orders and uphold artisanal livelihoods across Bhadohi and Mirzapur. Authenticity certificates and QR-based tracking reinforce buyer confidence, sustaining export premiums and supporting the India carpets and rugs market’s foreign-exchange inflow.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility squeezing SME margins | -1.3% | National, small manufacturers | Short term (≤ 2 years) |

| Shift to hard-flooring alternatives | -1.0% | Urban residential markets | Medium term (2-4 years) |

| Informal labor practices limit ESG sourcing | -0.7% | Traditional clusters, export buyers | Long term (≥ 4 years) |

| Water-scarcity regulation curbs dyeing capacity | -0.5% | UP & Rajasthan clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility Squeezing SME Margins

Polyester staple fiber was quoted at INR 93,000-95,000 per ton for November 2024, stubbornly high versus falling PTA feedstock, eroding pass-through ability for exporters. Cotton imports more than doubled in FY 2025, while oil-linked synthetic fibers remain volatile, bloating yarn costs. The new Textile Production Subsidy offers 15% relief, but adoption lags among cash-constrained clusters. Gujarat mills cite seasonal worker attrition and wage inflation as compounding stressors. Unless raw-material hedges mature and scale purchasing cooperatives grow, volatile inputs will continue to drag margins in the India carpets and rugs market.

Shift to Hard-Flooring Alternatives (Laminate, Vinyl, Tiles)

Ceramic tile, vinyl plank, and laminate suppliers tout easy maintenance, modern aesthetics, and antimicrobial surfaces, tempting urban homeowners away from fiber-based coverings. Mohawk Industries diversified beyond carpets to log USD 11.1 billion in broader flooring sales during 2024. Tarkett posted EUR 3.36 billion revenue from flexible flooring, illustrating the scale of substitution pressure. Yet carpet tiles partially offset the threat by delivering acoustics and warmth hard floors cannot replicate. Balanced product-mix strategies help manufacturers defend share, but the substitution trend trims India carpets and rugs market growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Machine-Tufted Scale Meets Hand-Knotted Heritage

Hand-knotted carpets accounted for 41.02% of the India carpets and rugs market share in 2025, reflecting deep artisanal roots across Bhadohi, Mirzapur, and Kashmir clusters. International collectors prize their complex knot counts, allowing exporters to secure premium margins despite longer lead times. Machine-tufted ranges, by contrast, are forecast to register an 10.98% CAGR through 2031 as automated looms lift daily output and lower per-square-foot costs. The India carpets and rugs market size attributed to machine-tufted lines is therefore expanding faster than its handmade counterpart, especially for mid-priced domestic renovations.

Technology now bridges tradition with efficiency. AI-augmented talim code software assists Kashmir weavers in color mapping, cutting rework, and protecting ancestral motifs. QR-based provenance labels reassure buyers about authenticity, reinforcing hand-knotted value even as tufted formats compete on affordability. As a result, blended retail portfolios, premium wool knots alongside entry-level synthetic tufts, help brands hedge demand cycles while broadening the India carpets and rugs market footprint across income cohorts.

By Material: Polypropylene Momentum Tests Wool Dominance

Wool retained 46.55% of material demand in 2025, sustained by India’s strong clip supply and USD 1.34 billion wool-carpet export tally. The Integrated Wool Development Programme funds improved shearing, grading, and scouring that lift yield quality. Simultaneously, polypropylene products are set for a 10.08% CAGR to 2031, favored in offices, hospitality corridors, and outdoor patios for stain resistance and lighter weight. This blend positions synthetics as the quickest-growing slice of the India carpets and rugs market.

Nylon and PET fibers occupy niche commercial sites where traffic intensity or moisture demands exceed wool capabilities. Innovations like ECOTHERM fiber showcase synthetic upgrades that reduce gram-weight without sacrificing thermal comfort. On the natural side, jute and sisal flat-weaves cater to eco-minded décor shoppers seeking tactile, biodegradable surfaces. Recycled yarn adoption remains nascent but gains policy backing under circularity drives at Bharat Tex 2025. Material diversification therefore future-proofs the India carpets and rugs market against raw-wool scarcity and synthetic price swings.

By End User: Commercial Demand Surges on Infrastructure Roll-Out

Residential households generated 71.35% of the 2025 volume, cementing floor-covering relevance for comfort and visual warmth in India’s urban homes. Rising disposable incomes, coupled with flexible financing for home improvement, sustain this core. The commercial segment, however, is forecast to race ahead at a 11.76% CAGR, energised by hotel pipelines, mall retrofits, and airport expansions tied to tourism-driven GDP agendas. These trends widen the India carpets and rugs market share gap between legacy residential uptake and emergent institutional orders.

Hospitality brands specify high-twist nylon or wool-blend carpets that survive luggage wheels and floor-polishing chemicals. Hybrid work formats push corporate fit-outs toward acoustic carpet tiles, leveraging modularity for desk-ratio changes. Education and healthcare settings follow suit, adopting low-VOC, antimicrobial coatings that comply with indoor air standards. OEM automotive and aviation niches add incremental volume through needle-punched mats and aisle runners. Together, these use cases diversify revenue streams and insulate the India carpets and rugs market against cyclical homebuilding downturns.

By Distribution Channel: Direct-to-Project Routes Gain Traction

Traditional B2C retail, multi-brand showrooms, furnishing outlets, and high-street boutiques, still captured 83.92% of 2025 sales. Carpets remain tactile goods; consumers like to touch pile height and test color shift in ambient light. Growing smartphone penetration, however, propels a vibrant digital path: B2B direct sales are expanding at a 9.41% CAGR as manufacturers court architects, facility managers, and hospitality procurement teams online. E-catalogs with augmented-reality room visualizers truncate design cycles, shrinking project overheads across the India carpets and rugs industry.

Home-improvement chains cater to do-it-yourself renovators seeking in-stock SKUs, while specialty flooring franchises provide stitching, hemming, and site-measurement services for upscale clientele. Rural pop-up exhibitions engage tier-3 consumers unfamiliar with online checkout. Manufacturers, in response, adopt omnichannel stacks that unify inventory views between factory, warehouse, and front-end platforms. Such integration reduces markdowns, accelerates cash turns, and anchors loyalty within the India carpets and rugs market.

Geography Analysis

North India accounted for 33.72% of 2025 shipments, anchored by Bhadohi’s “City of Carpet” status and Mirzapur’s dense loom network. Export agents crowd Varanasi’s logistics hubs, linking finished lots to Delhi’s ICD for outbound sailings. Government-sponsored craft clusters and road upgrades further cement northern dominance within the India carpets and rugs market size.

West India is the fastest climber, registering an 11.36% CAGR through 2031 on the back of Gujarat’s petro-chem feedstock, integrated weaving units, and proactive subsidy regimes. Surat daily extrudes 30 million meters of grey fabric, feeding tufting plants in adjoining districts. Policy clarity on power tariffs and land acquisition accelerates expansion plans, bringing new capacity online that plugs supply gaps for domestic and export buyers.

Southern mills in Tamil Nadu and Telangana support blended-fiber carpets and command shorter shipping lanes to Chennai and Krishnapatnam ports. Eastern jute belts furnish backing cloth and natural-fiber flat-weaves aimed at eco décor boutiques. Kashmir’s artisanal revival—evidenced by the record 72 x 40-foot carpet completed in 2024—adds cultural cachet yet remains capacity constrained. Diverse regional strengths thus ensure resilient sourcing for the India carpets and rugs market, even as water-stress or labor shortages challenge individual hubs.

Competitive Landscape

The India carpets and rugs market features a moderate concentration of scale players coexisting with thousands of cottage units. Welspun Living is steering toward USD 1.8 billion (Rs 15,000 crore) turnover by FY 2027, with its Telangana flooring plant adding 40 million m² annual capacity. Jaipur Rugs differentiates via a social-enterprise model that integrates 40,000 artisans across five states and delivers to 60-plus export destinations[4]Source: Jaipur Rugs Foundation, “Artisan Impact Report,” jaipurrugs.com. Obeetee, founded in 1920, leverages SA 8000 accreditation and industry-first effluent treatment to win ESG-sensitive tenders.

QR-code authentication combats knock-offs and enhances storytelling on global marketplaces. AI-driven demand planning cuts stockouts and guides small-batch dyeing that preserves cash. Sustainability parity is the second battleground: biomass boilers, solar rooftops, and recycled PET yarns are entering mainstream collections to meet EU green-deal norms. Players that synchronize digital, ESG, and artisan narratives thus command a higher wallet share in the India carpets and rugs market.

Horizontal diversification also intensifies. Mohawk leverages Indian subcontractors post-Karastan’s U.S. line exit to shift best-sellers like Spice Market, illustrating how global alliances reshape domestic value chains. Start-ups focusing on direct-to-consumer wool dhurries invest in Instagram-first launches, eroding legacy retail markup. Mid-tier exporters hedge against tariff swings by onboarding composite product families, carpet tiles, entry mats, and luxury throws, to buffer customer budgets. Adaptive positioning keeps competition fluid and ensures continuous innovation for the India carpets and rugs industry.

India Carpets And Rugs Industry Leaders

Jaipur Rugs Company

Welspun India Ltd

Obeetee Pvt Ltd

Shaw Industries Group Inc

Surya Carpets Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Bharat Tex 2025 opened with 5,000 exhibitors from 110 countries, spotlighting circularity and digitization across carpets and rugs.

- December 2024: Bharat Tex 2025 opened with 5,000 exhibitors from 110 countries, spotlighting circularity and digitization across carpets and rugs.

- September 2024: Welspun Living invested Rs 1.15 crore in a captive solar project to reach 100% renewable energy by 2030.

- September 2024: Paramount Dye Tec launched an IPO to boost recycled yarn capacity in Punjab.

India Carpets And Rugs Market Report Scope

The report covers a complete background analysis of India's carpet and rugs market, including an assessment of the parental market, emerging trends in the segments and regional market, and significant changes in market dynamics and market overview. The report also offers qualitative and quantitative assessments by analyzing the data gathered from industry analysts and market participants across various key points in the value chain.

By Product Type

| Tufted |

| Woven |

| Needle-Punched |

| Knotted / Hand-Knotted |

| Others (Flat-weave, Hooked, Braided) |

By Material

| Nylon |

| Polyester (PET & PTT) |

| Polypropylene |

| Wool |

| Other Natural Fibres (Jute, Sisal, Cotton, Silk) |

| Recycled & Bio-based Fibres |

By End User

| Residential | |

| Commercial | Hospitality & Leisure |

| Corporate Offices | |

| Retail | |

| Healthcare & Educational Institutions | |

| Other Commercial Facilities |

By Distribution Channel

| B2B/Direct from the Manufacturers | |

| B2C/Retail | Home-Improvement & DIY Stores |

| Specialty Flooring Stores (includes exclusive brand outlets) | |

| Furniture & Furnishing Stores | |

| Online | |

| Other Distribution Channels |

By Geography

| North India |

| West India |

| South India |

| East India |

| By Product Type | Tufted | |

| Woven | ||

| Needle-Punched | ||

| Knotted / Hand-Knotted | ||

| Others (Flat-weave, Hooked, Braided) | ||

| By Material | Nylon | |

| Polyester (PET & PTT) | ||

| Polypropylene | ||

| Wool | ||

| Other Natural Fibres (Jute, Sisal, Cotton, Silk) | ||

| Recycled & Bio-based Fibres | ||

| By End User | Residential | |

| Commercial | Hospitality & Leisure | |

| Corporate Offices | ||

| Retail | ||

| Healthcare & Educational Institutions | ||

| Other Commercial Facilities | ||

| By Distribution Channel | B2B/Direct from the Manufacturers | |

| B2C/Retail | Home-Improvement & DIY Stores | |

| Specialty Flooring Stores (includes exclusive brand outlets) | ||

| Furniture & Furnishing Stores | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North India | |

| West India | ||

| South India | ||

| East India | ||

Key Questions Answered in the Report

How big is the India carpets and rugs market in 2026?

The market is valued at USD 1.18 billion in 2026 and is set to grow at a 9.61% CAGR to USD 1.87 billion by 2031.

Which segment is growing fastest within Indian carpets?

Machine-tufted carpets are the fastest, projected at an 10.98% CAGR through 2031 due to automated looms and cost efficiency.

Why are polypropylene carpets gaining popularity?

Polypropylene offers lower price, stain resistance, and suitability for high-traffic commercial spaces, driving a 10.08% CAGR outlook.

What government policies support carpet exporters?

PM MITRA parks, Production Linked Incentives, and extensions of RoSCTL and RoDTEP rebates collectively lower production costs and preserve export competitiveness.

How are companies addressing sustainability demands?

Firms like Welspun and Obeetee invest in renewable energy, recycled fibers, and effluent treatment, enabling ESG-compliant products that fetch premium pricing.

Page last updated on: