Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

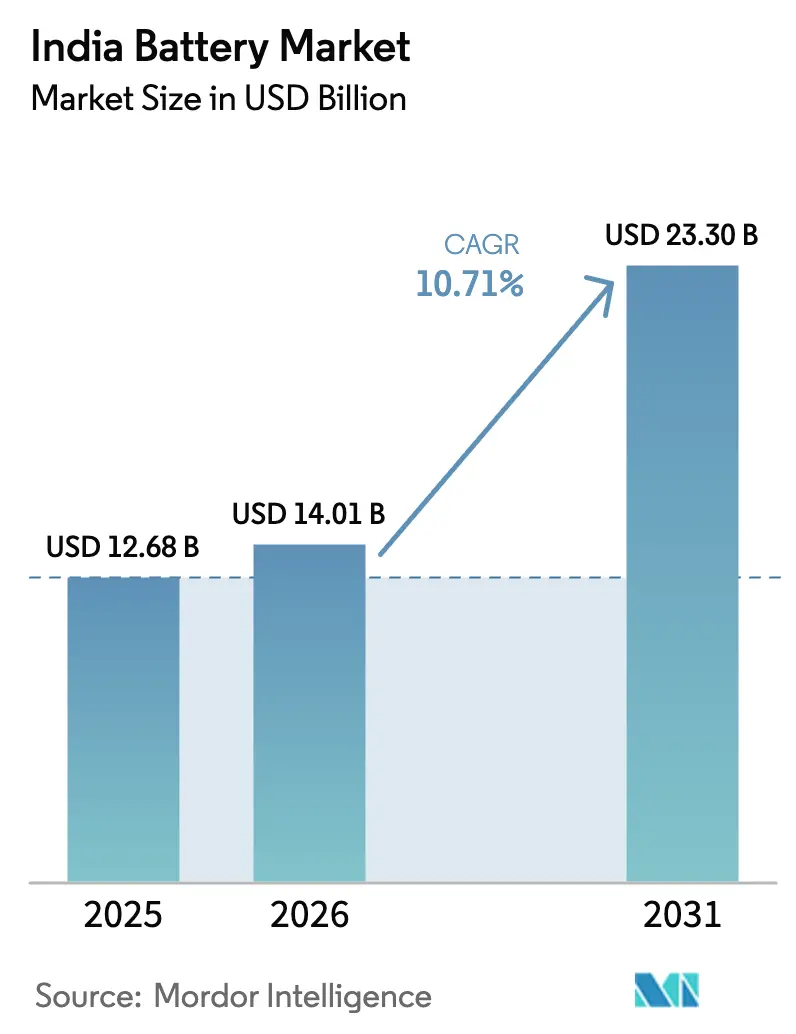

| Base Year Market Size (2025) | USD 12.68 Billion |

| Market Size (2026) | USD 14.01 Billion |

| Market Size (2031) | USD 23.30 Billion |

| Growth Rate (2026 - 2031) | 10.71% CAGR |

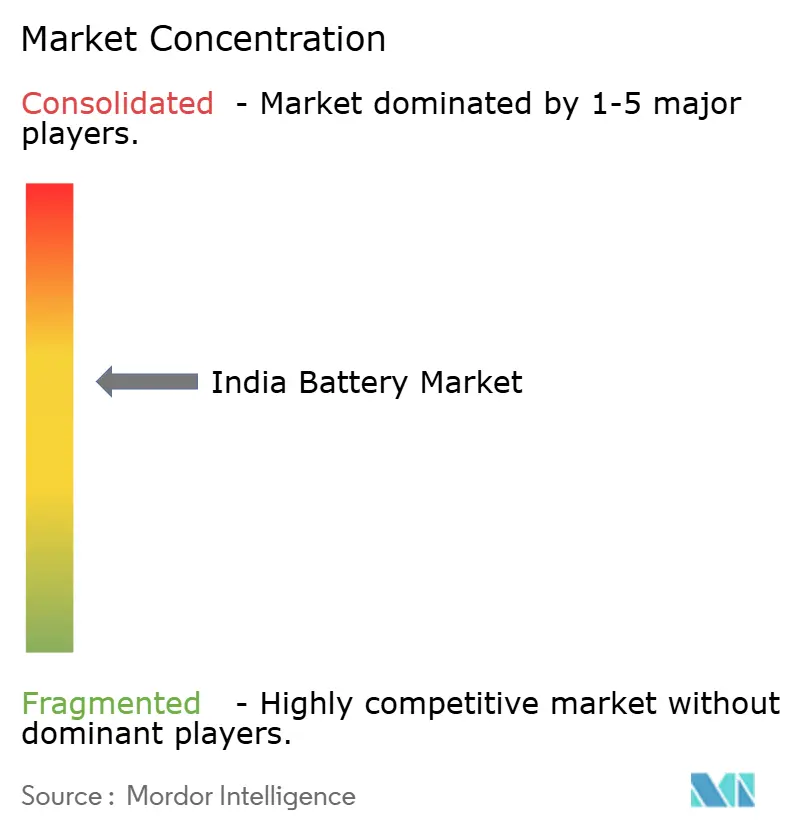

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Battery Market Analysis by Mordor Intelligence

The India Battery Market size is projected to expand from USD 12.68 billion in 2025 and USD 14.01 billion in 2026 to USD 23.30 billion by 2031, registering a CAGR of 10.71% between 2026 to 2031.

Growth is propelled by rapid electrification of two- and three-wheelers, gigafactory investments under the Production-Linked Incentive for Advanced Chemistry Cell scheme, and surging demand from telecom and data-center backup segments. Declining global lithium-ion pack prices, state-level fiscal incentives, and technology migration from lead-acid to lithium-ion are compressing payback periods and widening addressable use-cases for domestic cell suppliers. Meanwhile, the India battery market is diversifying chemistry portfolios: solid-state, sodium-ion, and LFP lines are moving from pilot to commercial scale to mitigate critical-mineral exposure and improve thermal safety. Competitive intensity is shifting toward vertical integration as OEMs such as Ola Electric operationalize in-house 4680 cylindrical-cell production and legacy leaders Exide Industries and Amara Raja redirect capital expenditure to lithium-ion units.

Key Report Takeaways

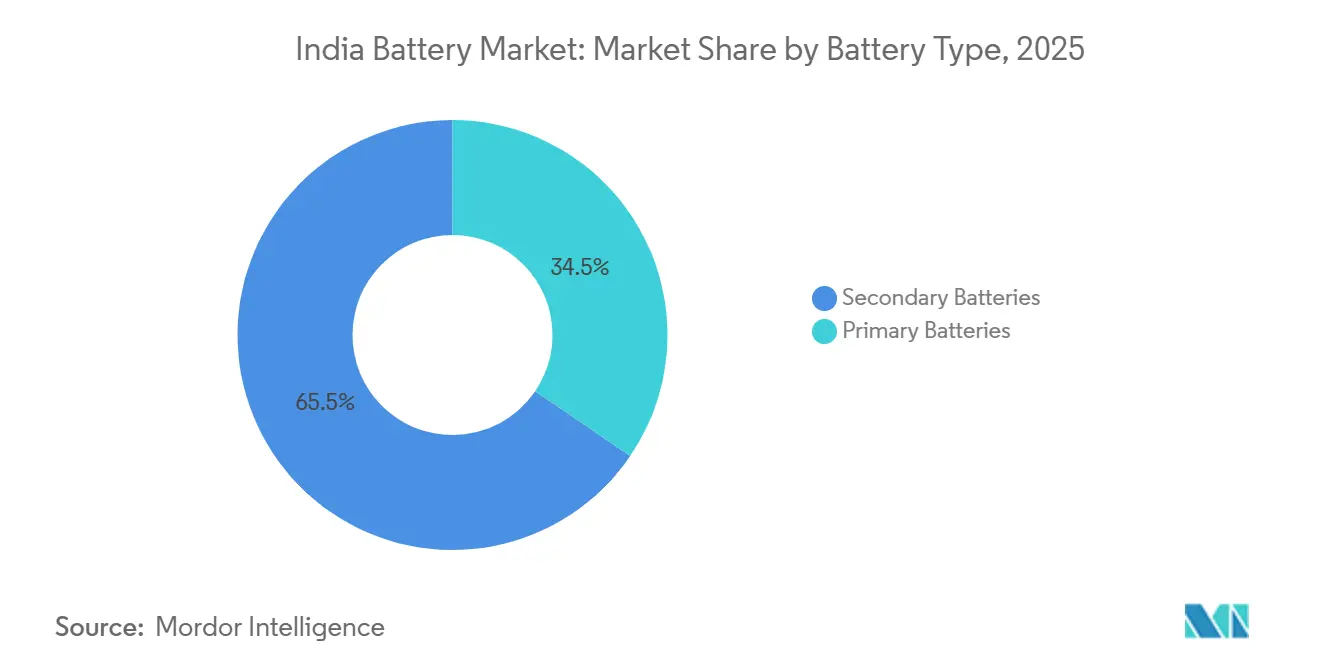

- By battery type, secondary batteries led with 65.5% revenue in 2025 and are projected to grow at a 15.9% CAGR through 2031, outpacing primary cells.

- By technology, lead-acid retained 53.2% share of the India battery market size in 2025, while solid-state batteries are forecast to expand at a 33.5% CAGR to 2031.

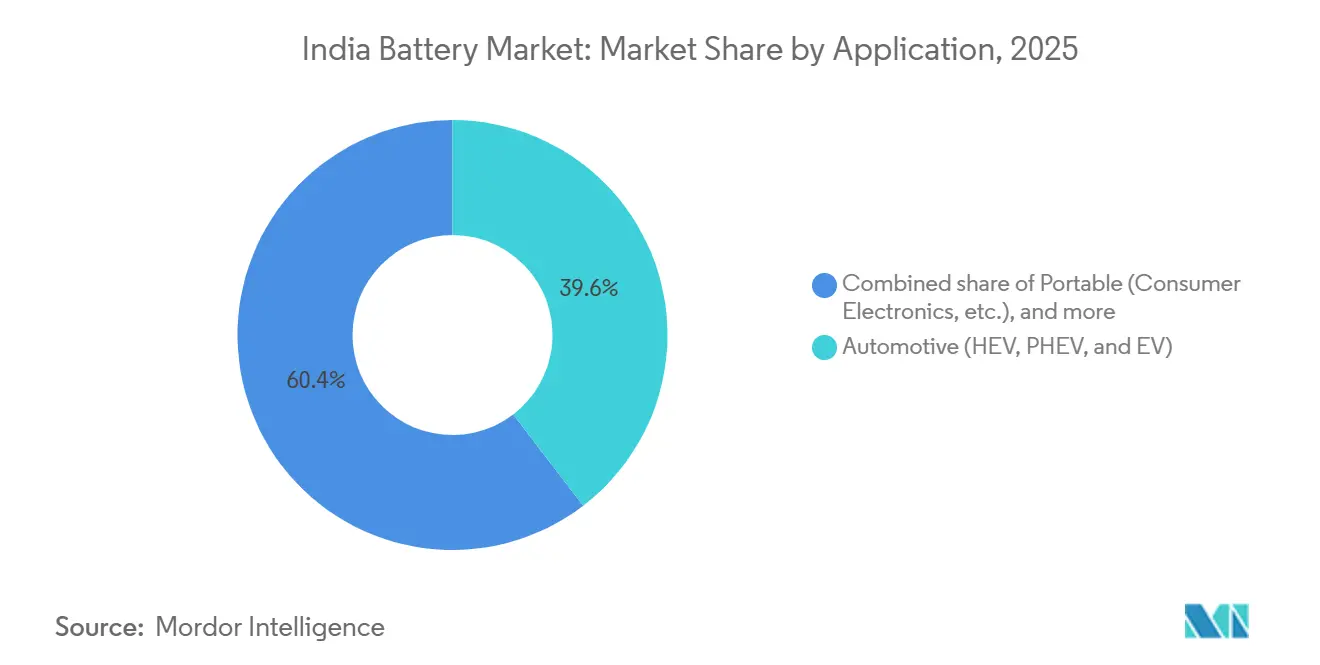

- By application, automotive captured 39.6% of India's battery market share in 2025, and the segment is advancing at a 15.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive Government Incentives & Policies | +2.8% | National, with early gains in Gujarat, Maharashtra, Tamil Nadu | Medium term (2-4 years) |

| Declining Lithium-ion Battery Prices | +1.9% | National | Short term (≤ 2 years) |

| Rapid EV Adoption in Two- & Three-Wheelers | +3.2% | National, urban clusters in Bangalore, Delhi, Pune | Short term (≤ 2 years) |

| Expanding Telecom & Data-Center Backup Needs | +1.5% | National, metro hubs | Medium term (2-4 years) |

| PLI-ACC Scheme Catalyzing Domestic Gigafactories | +2.1% | Gujarat, Karnataka, Tamil Nadu | Long term (≥ 4 years) |

| Emergence of Sodium-ion & Alt-Chemistries | +0.9% | National, pilot clusters in Gujarat | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supportive Government Incentives & Policies

Multi-tiered fiscal measures are lowering entry barriers across the India battery market. The PM E-DRIVE scheme, launched in 2024 with a Rs 10,900 crore (USD 1.3 billion) corpus, extends demand incentives to e-ambulances and e-trucks, broadening the subsidy horizon beyond FAME-II, which had earlier supported 1.6 million electric vehicles.[1]Press Information Bureau, “Cabinet Approves PLI Scheme for Advanced Chemistry Cell (ACC) Battery Storage,” pib.gov.in Maharashtra’s 2025 EV policy adds capital subsidies of up to Rs 10 lakh per charging station, while Tamil Nadu waives road tax and registration fees until 2030 to accelerate fleet turnover.[2]Ministry of Heavy Industries, “FAME-II Scheme Performance Report FY 2024-25,” mhi.gov.in These incentives shorten payback cycles for OEMs and encourage gigafactory siting in states that layer state perks atop federal grants. As a result, domestic capacity commitments reached 68 GWh in 2025, a 40% jump over 2024 announcements.

Declining Lithium-ion Battery Prices

Global pack prices fell to USD 115 per kWh in 2024 and are trending toward USD 80 per kWh by 2026, easing the cost barrier that historically constrained India's battery market penetration.[3]BloombergNEF, “Battery Pack Prices Fall to USD 139/kWh,” about.bnef.com Ola Electric sources cathode precursors at spot rates 18% below 2023 averages, allowing its S1 scooter pack to retail at Rs 45,000, undercutting lead-acid alternatives across a ten-year lifecycle. Exide Industries and Amara Raja target sub-Rs 50,000 packs for three-wheelers by late 2026, signaling imminent price inflection for commercial fleets. Falling input costs thus reinforce demand-side incentives, giving the India battery market dual momentum on the supply and demand fronts.

Rapid EV Adoption in Two- & Three-Wheelers

Unit sales of electric two-wheelers hit 1.149 million in fiscal 2024-25, up 21% year-on-year, while electric three-wheelers surged 57% to 159,235 units. Lower upfront prices, urban ride distances below 100 kilometers, and densifying charge networks in Bangalore, Delhi, and Pune underpin this outperformance versus passenger cars. Ather Energy’s 3.7 kWh swappable pack ecosystem spans 1,800 fast chargers across 100 cities, proving that infrastructure density can offset range anxiety. Fleet operators in Delhi show annual conversion rates above 40%, yielding total-cost-of-ownership savings of Rs 1.2 lakh per vehicle over five years compared with compressed natural gas autorickshaws. Each incremental two-wheeler needs 2-4 kWh, whereas three-wheelers demand 8-10 kWh, creating predictable procurement pipelines that anchor gigafactory utilization.

Expanding Telecom & Data-Center Backup Needs

More than 500,000 telecom towers are shifting from diesel gensets to lithium-ion modules offering 3-5 times the cycle life and 40% lower lifetime costs. Bharti Airtel and Reliance Jio ordered 80,000 lithium tower-backup units in 2024, each rated at 5 kWh. Parallelly, hyperscale data-center capacity is set to reach 2,070 MW by 2025 as AWS, Microsoft, and Google deepen their India footprints, bringing 10-20 MWh UPS requirements per site. Industrial customers favor LFP batteries for thermal stability, widening chemistry diversification, and buffering manufacturers from EV-specific demand volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical Mineral Supply Vulnerabilities | -1.4% | National | Medium term (2-4 years) |

| Under-developed Battery Recycling Ecosystem | -0.8% | National | Long term (≥ 4 years) |

| Peak-Hour Tariff Caps Hindering BESS Viability | -1.1% | National, state grids | Short term (≤ 2 years) |

| Global Patent Barriers for Next-Gen Chemistries | -0.6% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Critical Mineral Supply Vulnerabilities

The India battery market remains fully import-dependent for lithium and cobalt, leaving domestic producers exposed to geopolitical shocks. Although lithium carbonate prices cooled to USD 12,000 per tonne in 2024, long-term contracts still track Chinese benchmarks influenced by strategic stockpiling. Government auctions of lithium blocks in Jammu & Kashmir and Rajasthan revealed reserves equal to just 3–4 years of projected demand at 2031 run-rates. Cobalt risks are starker because 70% of global supply comes from the Democratic Republic of Congo, where artisanal mining raises social and delivery uncertainties. OEMs are pivoting to cobalt-free LFP cathodes, yet premium NMC batteries still anchor high-range vehicles, keeping supply-chain fragility in focus.

Under-developed Battery Recycling Ecosystem

Only 10% of end-of-life lithium-ion packs were recovered in 2024, far below the 70% target set by draft Extended Producer Responsibility guidelines for 2030. Attero Recycling’s 12,000-tonne hydrometallurgical facility struggles with feedstock scarcity because informal scrap channels siphon 60% of discarded packs for export to Southeast Asia. Non-standardized pack designs inflate disassembly costs to Rs 22 per kilogram, double the viable threshold. The absence of clear liability rules for second-life batteries further stalls investment in circular supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeables Drive Volume and Value

Secondary batteries accounted for 65.5% of India's battery market share in 2025, and this slice is projected to expand at a 15.9% CAGR through 2031 as automotive electrification accelerates and stationary storage scales. The India battery market size for secondary cells is projected to rise from USD 8.30 billion in 2025 to almost USD 18 billion by 2031, cementing its dominance. Lithium-ion chemistries make up 42% of secondary-battery revenue, propelled by OEM transitions from lead-acid starter-lighting-ignition units to traction packs that deliver 2,000–5,000 charge cycles. Ola Electric's 5 GWh block and Exide's Rs 7,000 crore lithium line exemplify capital flowing toward rechargeables.

Primary batteries still serve remote sensors and medical devices, but will grow only 3.2% annually as portable-electronics makers adopt integrated lithium-polymer modules. NiMH packs persist in select hybrids such as Toyota's Camry because of superior high-heat tolerance.[4]Toyota Kirloskar Motor, “Hybrid Vehicle Technology Overview,” toyotabharat.com NiCd use is shrinking after Bureau of Indian Standards tightened cadmium limits. Flow and sodium-sulfur technologies are piloting grid projects, but high capital costs keep them niche.

By Technology: Lead-Acid Incumbency Meets Solid-State Disruption

Lead-acid retained a 53.2% share in 2025, thanks to entrenched automotive SLI and UPS usages serviced by nationwide dealer networks of Exide and Amara Raja. However, safety incidents, 47 EV fires linked to thermal runaway between 2022 and 2024, fuel consumer preference for advanced chemistries. Solid-state cells, with energy densities above 400 Wh/kg and non-flammable electrolytes, are forecast to grow at a 33.5% CAGR, albeit from a low base. Log9’s graphene-enhanced quasi-solid prototypes enable 15-minute charging for fleet operators, while Reliance New Energy sees sodium-ion as a transitional step until solid-state costs drop below Rs 8,000 per kWh.

Lithium-ion held a 38% share in 2025, split between NMC 811 cathodes for range-sensitive scooters and LFP for cost-focused two-wheelers and stationary storage. Ola Electric’s 4680 cylindrical-cell architecture achieves 260 Wh/kg, enabling a 181-kilometer range in the S1 Pro scooter. Emerging chemistries such as aluminum-air and lithium-sulfur collectively hold a 1.8% share but draw disproportionate R&D funding under the National Mission on Transformative Mobility and Battery Storage, which earmarked Rs 500 crore for pre-commercial validation.

By Application: Automotive Electrification Anchors Demand

Automotive batteries captured 39.6% of value in 2025 and are forecast to progress at a 15.2% CAGR through 2031, driven mainly by two- and three-wheeler electrification. The India battery market size for automotive use is expected to nearly triple over the forecast window, reflecting robust subsidy support under PM E-DRIVE. Each electric scooter requires up to 4 kWh, while a three-wheeler carries 8-10 kWh, underpinning cell demand regardless of passenger-car uptake.

Industrial segments, motive power, telecom backup, and data-center UPS, held a 34% share in 2025. Operators like Airtel and Jio swapped 80,000 tower-backup batteries in 2024, cutting replacement cycles to once a decade. Portable electronics added 18%, whereas power tools and SLI batteries filled the balance. Diversified demand streams shield suppliers from single-application downturns, a key resilience factor in the India battery market.

Geography Analysis

Gujarat, Maharashtra, Karnataka, and Tamil Nadu concentrated 72% of installed capacity in 2025, reflecting port access for imported lithium carbonate and state subsidies for capital-intensive gigafactories. Gujarat hosts Reliance’s Jamnagar complex, which will integrate 10 GWh of sodium-ion and lithium-ion lines by 2028. Tamil Nadu secured Ola Electric’s inaugural 5 GWh facility and Hyundai Global Motors’ PLI allocation owing to electricity-duty exemptions and 15% capital grants. Karnataka’s Bangalore-Mysore corridor is an R&D hub for Log9, Ather Energy, and Tata AutoComp, benefiting from proximity to high-tech labor pools.

Maharashtra’s EV policy mandates a 25% battery-electric share in state purchases, anchoring demand for Exide’s Pune line and Amara Raja’s Chakan project. Northern states, Uttar Pradesh, Haryana, and Delhi, contribute 18% of consumption, bolstered by e-commerce last-mile fleets run by Amazon and Flipkart using 45,000 electric delivery vehicles. Eastern and northeastern zones remain under-penetrated at 6% due to sparse charging infrastructure and lower disposable incomes. Potential reserves in Jammu & Kashmir and Rajasthan could seed mining-linked clusters post-2028, though commercial viability awaits resource confirmation.

Competitive Landscape

The top five suppliers, Exide Industries, Amara Raja Energy & Mobility, Luminous Power Technologies, Ola Electric, and Reliance New Energy, held roughly 58% of 2025 revenue, giving the India battery market a moderate concentration profile. Exide and Amara Raja defend lead-acid margins via 12,000-dealer networks while allocating 25–35% of capex to lithium-ion expansions (12 GWh and 16 GWh, respectively, by 2028). Ola Electric’s vertical integration shaves 12–15% off pack costs and reduces development lead-times for new scooter models.

Reliance New Energy leverages Faradion IP to diversify into sodium-ion stationary systems and benefits from parent-company cash flows to scale Jamnagar output in step with renewable investments. Luminous Power and Su-Vastika focus on residential storage, an emerging whitespace as rooftop solar adoption rises in tier-2 cities. Recycling specialists Lohum and Attero are positioning to capture mineral credits once EPR rules become enforceable, partnering with OEMs to offer closed-loop solutions.

Strategically, players are experimenting with battery-as-a-service. Ather Energy’s Bangalore swapping network processes 8,000 transactions daily and aims for 200 stations by 2026, signaling a pivot from product sales to energy-delivery models. Patent filings grew 34% in 2024, led by Log9 and Reliance, indicating a shift from assembly to indigenous IP creation.

India Battery Industry Leaders

Exide Industries Ltd

Luminous Power Technologies Pvt. Ltd.

HBL Power Systems Ltd

TATA AutoComp GY Batteries Pvt. Ltd.

Amara Raja Energy & Mobility Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: JSW Energy announced a 10 GWh LFP facility in Karnataka to serve its renewable-plus-storage pipeline.

- September 2025: Reliance New Energy Commissioned Phase 1 of its Jamnagar gigafactory, adding 2 GWh of sodium-ion capacity with offtake contracts totaling 500 MWh for grid projects.

- July 2025: Exide Industries opened a 3 GWh lithium-ion line in Pune after investing Rs 2,100 crore.

- June 2024: Amara Raja’s management informed investors that the initial capacity of the facility is expected to be approximately 4–6 GWh, with final details still being finalized. The INR 9,500 crore gigafactory is planned to scale up to a 16 GWh cell capacity and a 5 GWh battery pack capacity over the next decade.

India Battery Market Report Scope

A battery is a device that converts chemical energy contained within its active materials directly into electric power using an electrochemical oxidation-reduction (redox) reaction.

The Indian battery market is segmented by Battery Type (Primary and Secondary), Technology (Lead-acid, Li-ion, Nickel-metal hydride, Nickel-cadmium, Sodium-sulfur, Solid-state, Flow Battery, Emerging chemistries), Application (Automotive, Industrial, Portable, Power Tools, SLI, Other Applications), and Geography. Market Forecasts are Provided in Terms of Value (USD).

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

| By Battery Type | Primary Batteries |

| Secondary Batteries | |

| By Technology | Lead-acid |

| Li-ion | |

| Nickel-metal hydride | |

| Nickel-cadmium | |

| Sodium-sulfur | |

| Solid-state | |

| Flow Battery | |

| Emerging chemistries | |

| By Application | Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications |

Key Questions Answered in the Report

How large is the India battery market in 2026?

The India battery market is valued at USD 14.01 billion in 2026, tracking a 10.71% CAGR toward USD 23.30 billion by 2031.

Which battery type dominates demand?

Secondary, or rechargeable, batteries led with 65.5% revenue share in 2025 and are scaling at nearly 16% annually.

What is driving rapid adoption in mobility?

Subsidies under PM E-DRIVE and falling lithium-ion prices have pushed electric two- and three-wheeler sales past 1.3 million units, anchoring automotive battery demand.

Where are most gigafactories located?

Gujarat, Tamil Nadu, Karnataka, and Maharashtra host 72% of installed and announced capacity thanks to port access and state incentives.

Are alternative chemistries gaining ground?

Yes, sodium-ion and solid-state pilots are underway, with Reliance New Energy commissioning 2 GWh of sodium-ion capacity in 2026 for stationary storage.

What challenges threaten growth?

Mineral import dependence, limited recycling, tariff-capped storage economics, and international patent barriers could shave 4% off projected CAGR if unresolved.

Page last updated on: