Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

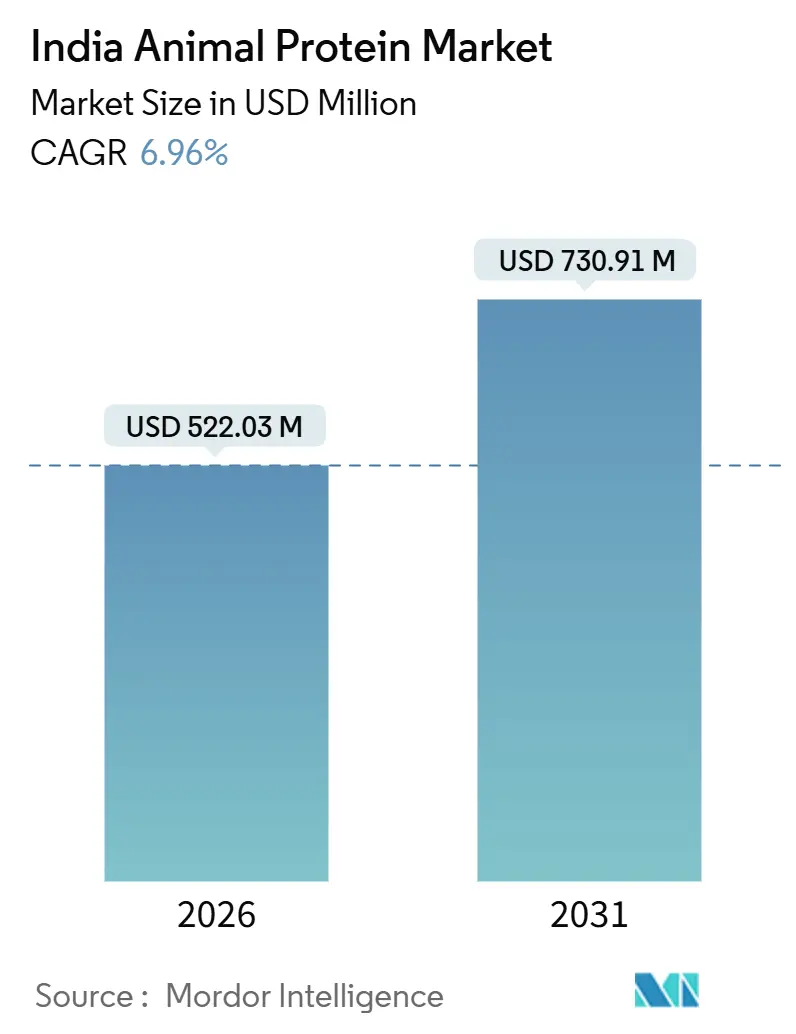

| Market Size (2026) | USD 522.03 Million |

| Market Size (2031) | USD 730.91 Million |

| Growth Rate (2026 - 2031) | 6.96% CAGR |

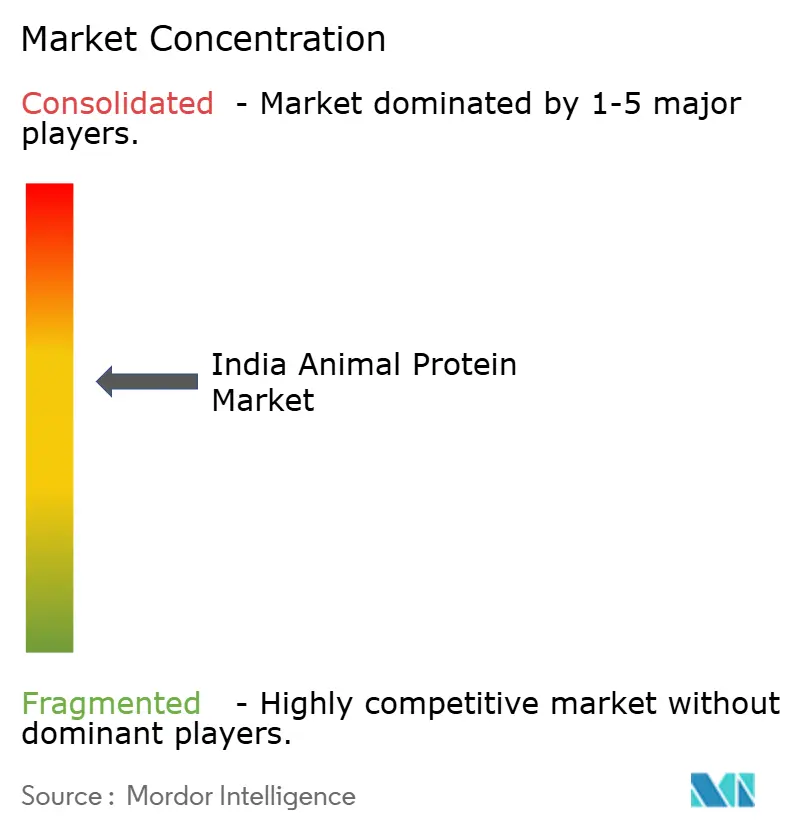

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Animal Protein Market Analysis by Mordor Intelligence

The India animal protein market size is USD 522.03 million in 2026 and is projected to reach USD 730.91 million by 2031, advancing at a 6.96% CAGR. This growth is buoyed by rising household incomes, swift urban migration, and a notable USD 3.8 billion government investment in dairy and livestock infrastructure, as highlighted by the Press Information Bureau[1]Source: Press Information Bureau, “Government Schemes Boost Dairy Infrastructure,” pib.gov.in . Both private and cooperative processors are enhancing their membrane-filtration and cold-chain capabilities. This not only reduces import reliance but also makes whey, casein, and collagen ingredients competitively priced for both mainstream and premium brands. Demand is further bolstered by a robust base of 50 million fitness enthusiasts in India, who prioritize convenient, high-quality protein. Additionally, the launch of nutricosmetics combining collagen peptides with Ayurvedic botanicals is tapping into new consumer demographics. While challenges like disease outbreaks and feed price volatility loom in the short term, the long-term outlook for the India animal protein market remains optimistic. Factors such as product innovation, diverse distribution channels, and clearer regulations in the nutraceutical space bolster this confidence.

Key Report Takeaways

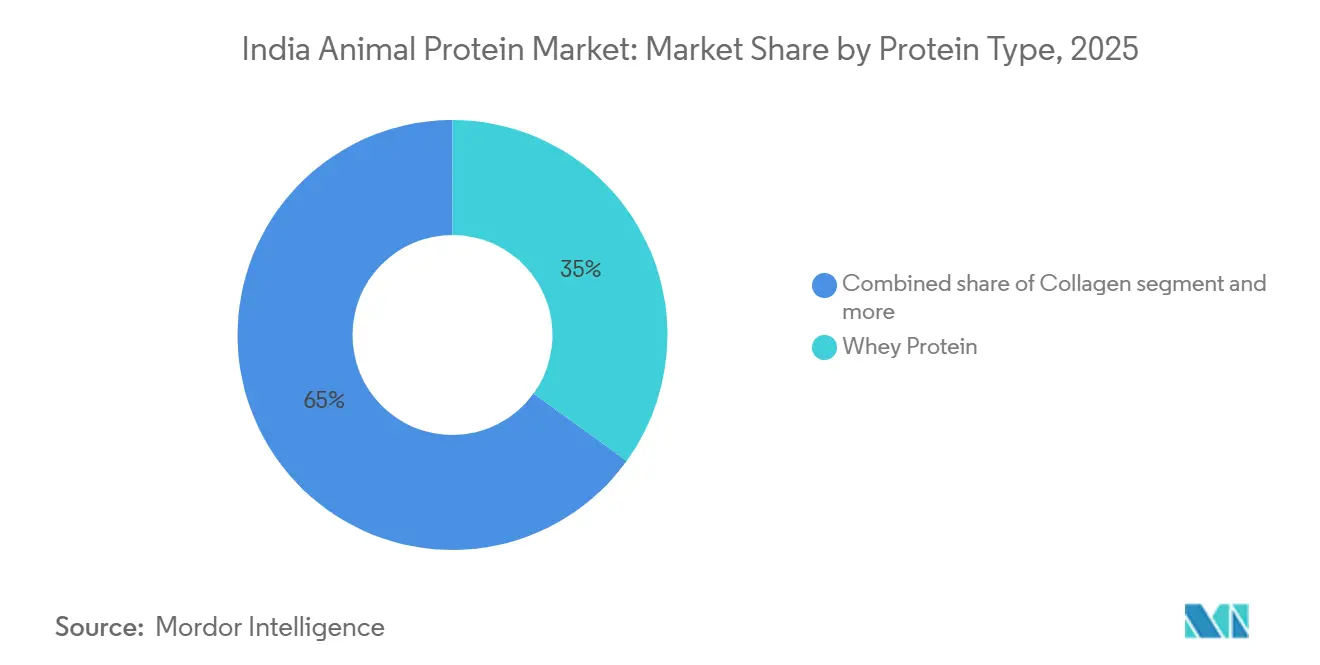

- By protein type, whey protein captured 34.96% of the India animal protein market share in 2025, while collagen peptides are forecast to post the fastest 7.80% CAGR through 2031.

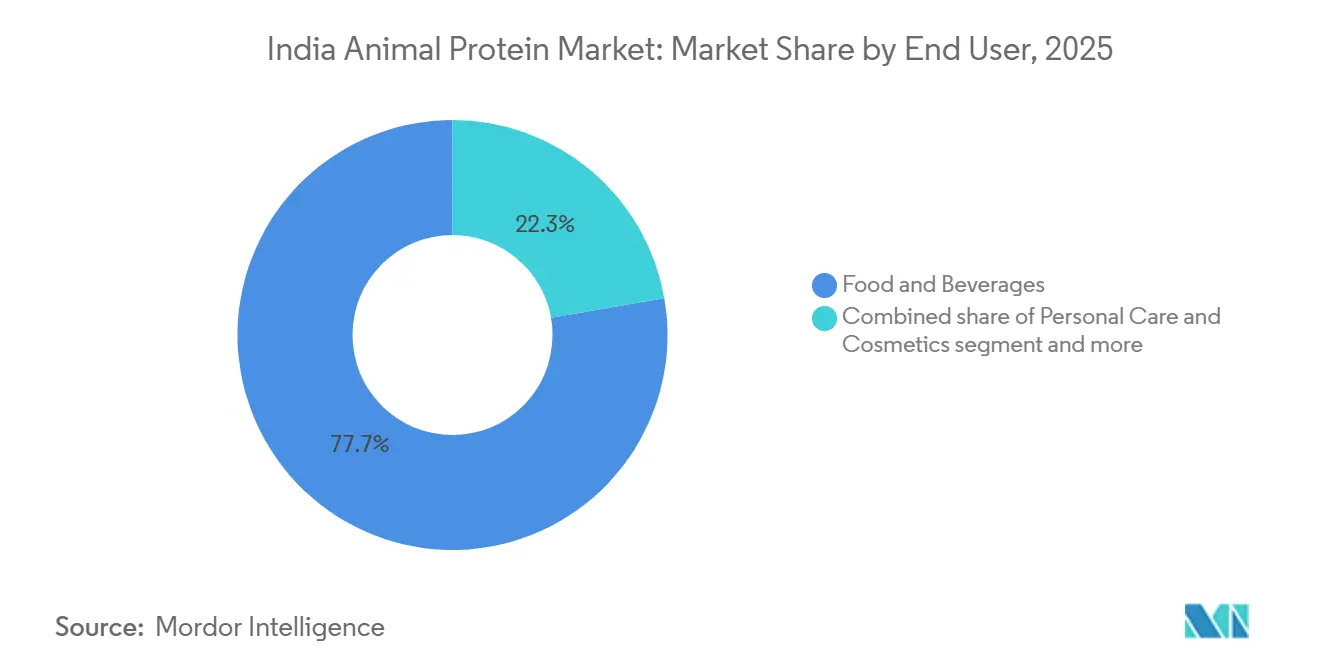

- By end user, food and beverages held 77.74% of the India animal protein market size in 2025, while the personal care and cosmetics segment is projected to accelerate at an 8.13% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Animal Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing fitness culture and active lifestyles | +1.2% | National, with concentration in metro clusters (Mumbai, Delhi-NCR, Bengaluru, Hyderabad) | Medium term (2-4 years) |

| Adoption of precision feeding technologies | +0.8% | National, early gains in Gujarat, Punjab, and Haryana dairy belts | Long term (≥ 4 years) |

| Shift toward value-added dairy products | +1.0% | National, led by urban markets and modern retail expansion | Medium term (2-4 years) |

| Advancements in breeding and genetics | +0.7% | National, focused on indigenous breed clusters in Rajasthan, Gujarat, and Madhya Pradesh | Long term (≥ 4 years) |

| Nutraceutical and functional food growth | +1.1% | National, with premium segment concentration in tier-1 cities | Short term (≤ 2 years) |

| Expansion of domestic processing infrastructure | +1.3% | National, spill-over to rural milkshed areas in Uttar Pradesh, Maharashtra, Tamil Nadu | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing fitness culture and active lifestyles

In 2025, India's fitness culture hit a pivotal moment. Cult.fit boasted 2.5 million active subscribers across over 300 centers. By 2024, the broader fitness market was valued at USD 2.6 billion, signaling a shift from passive wellness to a focus on performance-oriented nutrition. This change in behavior is further fueled by government initiatives like the Fit India Movement[2]Source: Ministry of Youth Affairs and Sports, “Fit India Movement Participation Data,” yas.nic.in. In 2024 alone, this movement drew over 50 million participants to community sports events. Such enthusiasm has spurred demand for whey protein products in India, known for their promise of quick muscle recovery and lean mass gains, as highlighted by the Ministry of Youth Affairs and Sports. Responding to this surge, domestic manufacturers have localized production. Parag Milk Foods, for instance, invested INR 300 crore to set up India's largest whey protein concentrate facility, aiming for an annual capacity of 10,000 metric tons by late 2026. Meanwhile, Karnataka Milk Federation joined forces with HealthKart to create a Nandini-branded protein range, now available at 5,000 retail outlets. Transitioning from imported isolates to locally fractionated whey has slashed landed costs by about 20%. This cost reduction allows for competitively priced offerings, especially appealing to the aspirational middle class. Yet, growth in this segment faces hurdles. In tier-3 towns, where traditional dairy habits prevail, consumer awareness remains limited. This suggests a bumpy road to market penetration, likely extending until 2028.

Expansion of domestic processing infrastructure

In March 2024, Mother Dairy announced an INR 750 crore investment to establish two advanced processing plants in Uttar Pradesh and Rajasthan. These greenfield facilities, equipped with ultra-high-temperature sterilization and membrane filtration lines, will produce caseinates and milk protein concentrates. In February 2025, Amul inaugurated the world's largest curd manufacturing plant in Kolkata, with a daily capacity of 1 million kilograms, enabling whey stream extraction for protein fractionation. These expansions are supported by the Animal Husbandry Infrastructure Development Fund, which disbursed INR 29,610 crore in concessional credit to 450 projects in 2024, driving private-sector investments in cold-chain logistics, automated milking parlors, and effluent treatment systems. New capacities are strategically located in milk-surplus states like Uttar Pradesh, which contributed 18% of India's 239.30 million metric tons of milk production in 2023-24, ensuring proximity to raw materials and reducing spoilage. This infrastructure growth addresses a key issue: in 2024, India's protein ingredient self-sufficiency ratio was only 42%, with imports from New Zealand, the European Union, and the United States exposing the market to foreign-exchange and tariff risks.

Nutraceutical and functional food growth

Regulatory changes and clinical validation requirements are reshaping nutraceutical demand. In 2024, the Food Safety and Standards Authority of India (FSSAI) introduced draft regulations mandating pre-market submissions, including human clinical trial data, for claims related to immunity, cognitive health, or metabolic wellness[3]Source: Food Safety and Standards Authority of India, “Draft Nutraceutical Regulations 2024,” fssai.gov.in . This raises the evidentiary bar and favors scientifically backed brands. Nestlé India and Dr. Reddy's Laboratories responded by forming a joint venture in 2024 to co-develop protein-fortified medical nutrition products, such as Resource High Protein, targeting elderly sarcopenia and post-surgical recovery, segments underserved by traditional dairy products. Simultaneously, infant formula manufacturers are reformulating with hydrolyzed whey peptides to reduce allergenicity, driven by FSSAI's 2025 directive requiring allergen labeling on protein supplements and baby foods. These regulations benefit established players with strong in-house research and development while sidelining smaller entities lacking clinical trial resources, leading to market concentration. Compliance costs for a structure-function claim now exceed INR 1 crore, creating a barrier for niche disruptors and protecting established brands.

Shift toward value-added dairy products

Consumer expectations and profit margins are being reshaped by the launch of value-added dairy products. In October 2024, Britannia Industries and Bel Group inaugurated a cheese manufacturing plant in Maharashtra, investing INR 220 crore. This facility, leveraging enzyme-modified cheese technology, aims to produce creamier textures with a longer shelf life, specifically catering to the burgeoning pizza and quick-service restaurant markets. In November 2024, Karnataka Milk Federation's Nandini brand made its debut in the Delhi market, rolling out Greek yogurt, paneer, and flavored milk. With a distribution of 250,000 liters daily via modern trade and e-commerce, Nandini is ramping up competition against established giants like Amul and Mother Dairy. The trend of premiumization in the dairy sector is evident: while value-added dairy products enjoy gross margins between 28% to 35%, commodity liquid milk lags with margins of just 12% to 18%. This disparity is driving cooperatives to channel investments into cheese, yogurt, and protein-enriched beverages. Such margin growth not only boosts profits but also funds upstream ventures like precision feeding and genetic enhancements, establishing a feedback loop that ties consumer premiumization to production efficiency. Yet, this transition comes with challenges; producers face the risk of ingredient cost fluctuations. Given that cheese and yogurt depend on stable milk-fat and protein ratios, this demands advanced procurement and blending strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pervasive animal disease outbreaks | -0.9% | National, acute in Kerala, West Bengal, and Assam poultry clusters | Short term (≤ 2 years) |

| Competition from the plant-based "smart protein" sector | -0.6% | National, led by metro markets and tier-1 cities | Medium term (2-4 years) |

| Acute fodder and feed scarcity | -0.7% | National, severe in rain-deficient regions (Maharashtra, Karnataka, Rajasthan) | Short term (≤ 2 years) |

| Low genetic productivity of indigenous breeds | -0.5% | National, concentrated in indigenous breed belts (Rajasthan, Gujarat, Madhya Pradesh) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pervasive animal disease outbreaks

In 2024 and 2025, avian influenza outbreaks in Kerala and West Bengal led to the culling of over 1.2 million birds. This not only disrupted egg protein supply chains but also increased biosecurity compliance costs for hatcheries and layer farms. Venkateshwara Hatcheries, one of India's largest integrated poultry producers, experienced an 11.6% year-on-year revenue drop in fiscal 2024. The company attributed this decline to production halts caused by diseases and rising vaccination costs. Despite mass vaccination campaigns in 2024, which inoculated 500 million bovines under the National Animal Disease Control Programme, foot-and-mouth disease and lumpy skin disease still sporadically affected cattle herds. The economic impact of these diseases goes beyond just direct mortality. Quarantine measures have disrupted milk collection routes, and export bans on egg powder and gelatin to markets sensitive to diseases, like Japan and South Korea, have reduced foreign-exchange earnings. Furthermore, the risk of disease has made institutional investors wary of large-scale concentrated animal feeding operations. This hesitance has resulted in a continued fragmented farm structure, limiting economies of scale and making it challenging for buyers of protein ingredients to ensure quality and traceability.

Competition from plant-based "smart protein" sector

In 2024 and 2025, plant-based protein ventures secured over USD 15 million in venture capital. Good Dot raised USD 10 million in Series A funding to expand its textured vegetable protein offerings, while Wakao Foods introduced jackfruit-based meat alternatives to 8,000 retail outlets nationwide. Blue Tribe and Imagine Meats, backed by Reliance Retail, are leveraging modern trade distribution and aggressive promotional pricing to attract flexitarian consumers seeking lower environmental impact without compromising taste or texture. The Good Food Institute India reported a 22% rise in alternative protein adoption among urban millennials in 2024, driven by concerns over antibiotic residues in animal products and the carbon footprint of livestock systems. While plant-based proteins account for less than 3% of India's total protein consumption, their rapid growth challenges animal protein sources, particularly in ready-to-eat and snack segments where taste parity has been achieved. In response, animal protein brands are emphasizing bioavailability, complete amino acid profiles, and clean-label sourcing, while exploring hybrid formulations blending whey or collagen with pea or soy isolates to appeal to health-conscious consumers unwilling to fully abandon animal-derived nutrition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protein Type: Whey Dominance Meets Collagen Momentum

In 2025, whey protein commanded a dominant 34.96% share in the protein-type segmentation, driven by its rapid digestion and rich branching-chain amino acid content, making it a favorite for sports nutrition and infant formulas. Meanwhile, collagen is set to grow at a robust 7.80% CAGR from 2026 to 2031, largely fueled by India's booming collagen nutricosmetics market. Beauty brands are now infusing marine and bovine collagen peptides into their ingestible skincare lines, focusing on benefits like wrinkle reduction and enhanced joint health. In a significant move, Laurus Bio secured a nod from the Genetic Engineering Appraisal Committee in 2024, allowing it to produce recombinant human collagen through microbial fermentation. This positions India as a promising export hub for pharmaceutical-grade collagen, sidestepping concerns tied to animal sourcing. Further underscoring the industry's confidence, Nitta Gelatin India pledged INR 60 crore in May 2024 to bolster its collagen peptide manufacturing in Kerala, with operations set to kick off by mid-2025, anticipating robust demand from the personal care and nutraceutical sectors.

Casein and its derivatives find niche roles in processed cheese, coffee whiteners, and clinical nutrition, thanks to their slow-release properties that ensure amino acids are available for 6 to 8 hours. Milk protein concentrates and isolates are becoming popular in high-protein yogurt and beverages, spurred by a clean-label trend that prefers straightforward ingredient lists over complex stabilizers. While egg protein has been a staple in bakery and confectionery, supply disruptions from avian influenza have nudged producers to explore blends of whey and pea proteins. Gelatin is a go-to for gummies, capsules, and confections, but its growth faces hurdles due to halal and vegetarian certifications, pushing some towards plant-based substitutes like pectin and agar. Insect protein, still in its infancy, is drawing interest from aquaculture feed producers eyeing sustainable fishmeal alternatives. However, regulatory uncertainties around novel food approvals have tempered its commercial rollout. The "other animal protein" segment, featuring hydrolyzed collagen, bone broth concentrates, and organ-meat peptides, is carving out a niche, especially in ancestral nutrition and gut health markets, highlighting its lucrative potential.

By End User: Food Supremacy, Cosmetics Acceleration

In 2025, food and beverages dominated end-user demand, accounting for 77.74%. This included bakery items, beverages, breakfast cereals, condiments, confectionery, dairy alternatives, ready-to-eat meals, and snacks, with protein fortification as a universal enhancement. Meanwhile, the personal care and cosmetics sector is set to grow at an 8.13% CAGR from 2026 to 2031, driven by the shift of collagen-infused serums, oral beauty supplements, and hair-care formulations from boutiques to mainstream retail and e-commerce. Supplements, including baby food, elderly nutrition, medical nutrition, and sports performance products, are experiencing significant growth due to aging demographics and rising chronic diseases. Parag Milk Foods and Karnataka Milk Federation are targeting the sports nutrition segment with domestically produced whey isolates priced 25% lower than imports, aiming to capture market share from global brands like Optimum Nutrition and MuscleBlaze.

Within food and beverages, dairy and its alternatives are the largest consumers of animal protein ingredients. Manufacturers are reformulating products with whey protein isolates to increase protein content from 3 grams to 10 grams per serving, meeting demand for functional nutrition. Hydrolyzed collagen and egg protein are being added to ready-to-cook and ready-to-eat meals to enhance satiety and nutritional value for busy urban professionals. Beverages, especially protein shakes and fortified milk, are seeing strong volume growth due to on-the-go consumption. In the bakery sector, egg albumin aids leavening, while whey protein retains moisture. Confectionery relies on gelatin for gelling and texture. Although animal feed applications are smaller in value, they are critical for aquaculture and pet food, where high-quality proteins improve feed conversion ratios and palatability. This segmentation underscores the versatility of animal proteins but also highlights competition from plant-based and fermentation-derived alternatives encroaching on traditional uses.

Geography Analysis

India's animal protein market showcases a rich tapestry of production and consumption, with distinct regional hubs taking center stage. The West and South regions, bolstered by India's title as the globe's top milk producer, lead the charge in the dairy protein sector. In Gujarat, major dairy cooperatives, alongside private entities in Maharashtra and Karnataka, have ramped up their whey protein processing capabilities. This move is in response to the soaring demand for protein-enriched foods, which now dominate the animal protein market's value. In a notable 2024 shift, Maharashtra has positioned itself as a pivotal hub for aquaculture feed production, unveiling new facilities to cater to the state's burgeoning inland and marine fish farms. Urban powerhouses like Mumbai and Bengaluru are at the forefront of consumption, with about 33% of their populace having direct gym access, propelling the animal protein sector's demand through 2030.

The Eastern and Central regions are witnessing the swiftest growth, driven largely by a seismic shift in organized poultry and aquaculture. West Bengal, now the leading meat-producing state, has also set records in egg production. Take, for instance, the 2024 debut of mega-poultry processing plants in Bihar and Telangana, eyeing a combined daily capacity of 1.5 lakh birds by 2025, catering to the protein-hungry rural and semi-urban demographics. Farmers in these regions are pivoting towards commercial livestock farming, increasingly opting for industrial feed formulations over traditional mixes to enhance protein conversion. This regional growth spurt is further energized by government infrastructure funds, which have subsidized the growth of slaughterhouses and cold storage facilities in states like Odisha and Chhattisgarh in 2025.

In Northern India, the market stands out with its emphasis on milk-derived proteins and a burgeoning dietary supplement sector. Uttar Pradesh shines as a dual titan, being the second-largest meat producer while also topping the charts in milk and casein output. The region is witnessing a surge in Ready-to-Eat (RTE) and Ready-to-Cook (RTC) animal protein products, especially in urban North Indian markets. A noteworthy 2024 development is the adoption of artificial intelligence (AI) by major producers in Punjab and Haryana, streamlining their intricate protein procurement and distribution systems. By early 2026, national per capita meat availability hit 7.51 kg, marking a consistent rise from 2023, underscoring the successful outreach of essential animal-based nutrition into Tier 2 and Tier 3 cities.

Competitive Landscape

The Indian animal protein market is moderately fragmented, with multinational ingredient suppliers, domestic dairy cooperatives, and specialized protein processors competing across overlapping value chains. Fonterra, Glanbia, Kerry Group, and Arla Foods utilize global procurement networks and technical application support to serve large food manufacturers. Meanwhile, Amul, Mother Dairy, Parag Milk Foods, and Karnataka Milk Federation capitalize on vertically integrated dairy operations and strong regional brand equity. Strategic initiatives include backward integration into whey fractionation, forward integration into branded consumer products, and horizontal expansion through acquisitions of niche protein specialists. For instance, Godrej Agrovet's INR 150 crore investment in a Telangana dairy facility in December 2025 highlights the shift toward captive protein ingredient capacity, which helps insulate margins from import price volatility. White-space opportunities include halal-certified collagen for Middle Eastern export markets, organic whey protein for premium domestic segments, and hydrolyzed egg protein for clinical nutrition. These niches require specialized certifications and supply-chain traceability, favoring incumbents with established quality-management systems.

Emerging disruptors are leveraging biotechnology to overcome animal-sourcing constraints. Laurus Bio's recombinant collagen platform and pilot-scale insect protein ventures indicate a long-term shift toward precision fermentation and alternative feedstocks. Technology adoption remains uneven; large cooperatives deploy IoT-enabled milk analyzers and blockchain traceability, while smaller processors rely on manual quality checks and paper-based documentation. The competitive intensity is expected to rise as plant-based protein brands expand into hybrid formulations blending animal and plant proteins. This trend will push traditional players to articulate clear value propositions focusing on bioavailability, taste, and functional performance. Regulatory compliance under FSSAI's nutraceutical and fortification standards is becoming a critical differentiator. Brands with in-house laboratories and clinical trial partnerships can substantiate health claims more efficiently than resource-constrained competitors.

The market is also witnessing a growing emphasis on sustainability and ethical sourcing. Companies are increasingly adopting eco-friendly practices, such as reducing carbon footprints in production and ensuring humane treatment of livestock. These efforts align with evolving consumer preferences for transparency and sustainability in the supply chain. Additionally, the rise of e-commerce platforms is reshaping distribution strategies, enabling brands to reach a broader audience while offering personalized product options. As the market evolves, players that can effectively integrate innovation, sustainability, and consumer-centric approaches are likely to gain a competitive edge.

India Animal Protein Industry Leaders

Fonterra Co-operative Group Limited

Glanbia PLC

Kerry Group PLC

Nakoda Dairy Private Limited

Nitta Gelatin Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Godrej Agrovet commissioned an INR 150 crore dairy processing facility in Telangana, equipped with membrane filtration technology for producing milk protein concentrates and caseinates. The plant's 500,000-liter daily processing capacity will supply protein ingredients to Godrej's animal feed and human nutrition divisions, reducing reliance on imported whey and casein.

- February 2025: Amul inaugurated the world's largest curd manufacturing facility in Kolkata, with a daily production capacity of 1 million kilograms, enabling the cooperative to extract whey streams for downstream protein fractionation and casein production. The USD 72 million (INR 600 crore) investment positions Amul to serve the eastern India market with fresh dairy products while capturing value from whey by-products previously discarded or sold as animal feed.

- May 2024: Nitta Gelatin India announced an INR 60 crore expansion of its collagen peptide manufacturing facility in Kerala, with commissioning scheduled for mid-2025. The investment responds to rising demand from nutricosmetics and sports nutrition brands seeking hydrolyzed collagen with specific molecular weight profiles for enhanced bioavailability.

India Animal Protein Market Report Scope

Animal protein is defined both scientifically and industrially as high-quality protein derived from animal tissues and fluids. The Indian animal protein market is segmented by protein type and end user. By protein type, the market is segmented into casein and caseinates, collagen, egg protein, gelatin, insect protein, milk protein, whey protein, and other animal protein. By end user, the market is segmented into animal feed, food and beverages, personal care and cosmetics, and supplements. The food and beverages segment is further sub-segmented into bakery, beverages, breakfast cereals, condiments/sauces, confectionery, dairy and dairy alternative products, RTE/RTC food products, and snacks. Similarly, the supplements segment is further sub-segmented into Baby Food and infant formula, elderly nutrition and medical nutrition, and sport/performance nutrition. The Market forecasts are provided in terms of value (USD) and volume (Tons).

Protein Type

| Casein and Caseinates |

| Collagen |

| Egg Protein |

| Gelatin |

| Insect Protein |

| Milk Protein |

| Whey Protein |

| Other Animal Protein |

End User

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternative Products | |

| RTE/RTC Food Products | |

| Snacks | |

| Personal Care and Cosmetics | |

| Supplements | Baby Food and Infant Formula |

| Elderly Nutrition and Medical Nutrition | |

| Sport/Performance Nutrition |

| Protein Type | Casein and Caseinates | |

| Collagen | ||

| Egg Protein | ||

| Gelatin | ||

| Insect Protein | ||

| Milk Protein | ||

| Whey Protein | ||

| Other Animal Protein | ||

| End User | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternative Products | ||

| RTE/RTC Food Products | ||

| Snacks | ||

| Personal Care and Cosmetics | ||

| Supplements | Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms