Impact Modifier Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

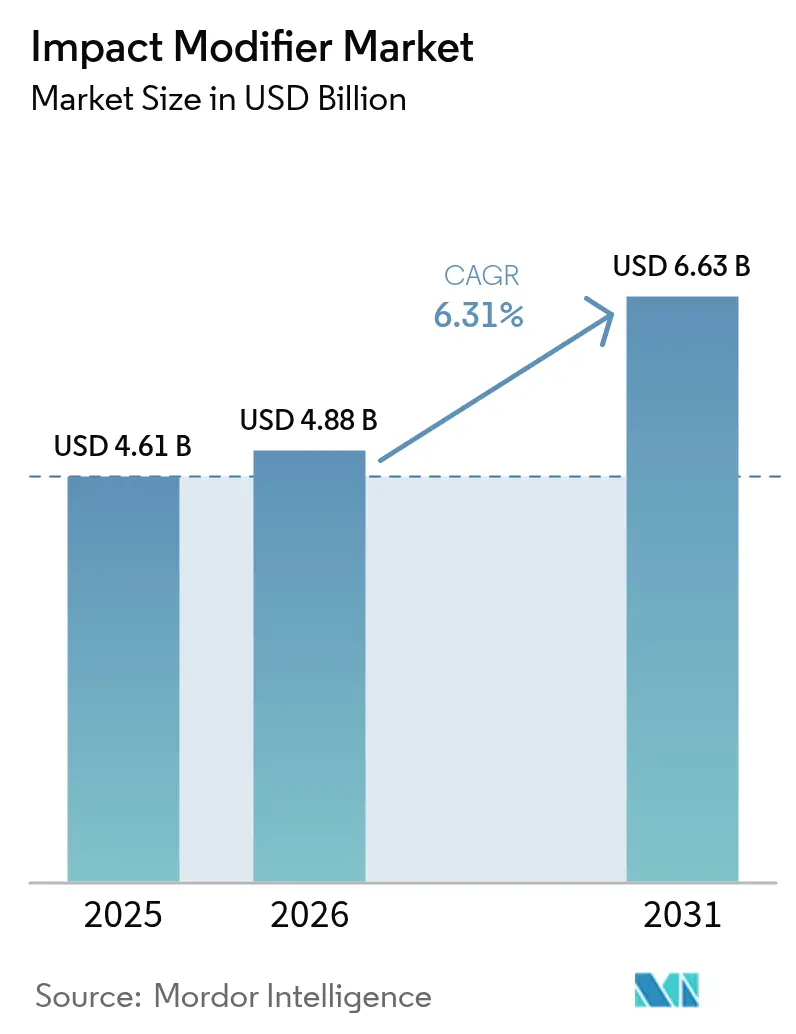

| Market Size (2026) | USD 4.88 Billion |

| Market Size (2031) | USD 6.63 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

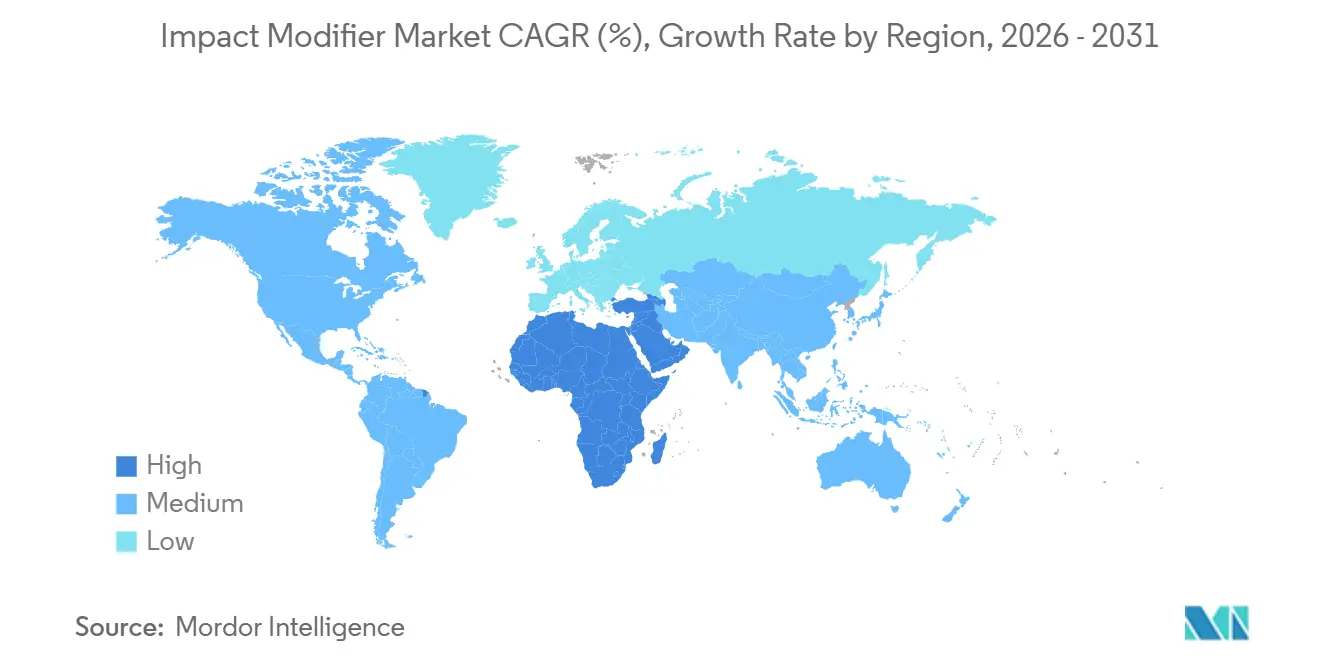

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Impact Modifier Market Analysis by Mordor Intelligence

The Impact Modifier Market size is projected to expand from USD 4.61 billion in 2025 and USD 4.88 billion in 2026 to USD 6.63 billion by 2031, registering a CAGR of 6.31% between 2026 to 2031. Polyvinyl chloride (PVC) pipe networks are replacing aging metal infrastructure across emerging economies, while automotive original equipment manufacturers (OEMs) keep substituting steel with polymer composites to meet the 2027 U.S. fuel-economy target of 49 miles per gallon. In parallel, the European Union requires 30% recycled content in rigid plastic packaging by 2030, accelerating demand for compatibilizer-rich acrylic grades. Acrylonitrile butadiene styrene (ABS) led with 33.48% revenue share in 2025, yet acrylic impact modifiers are expanding faster because they enable transparent PVC window profiles that pass ISO 9227 salt-spray tests without yellowing.

Key Report Takeaways

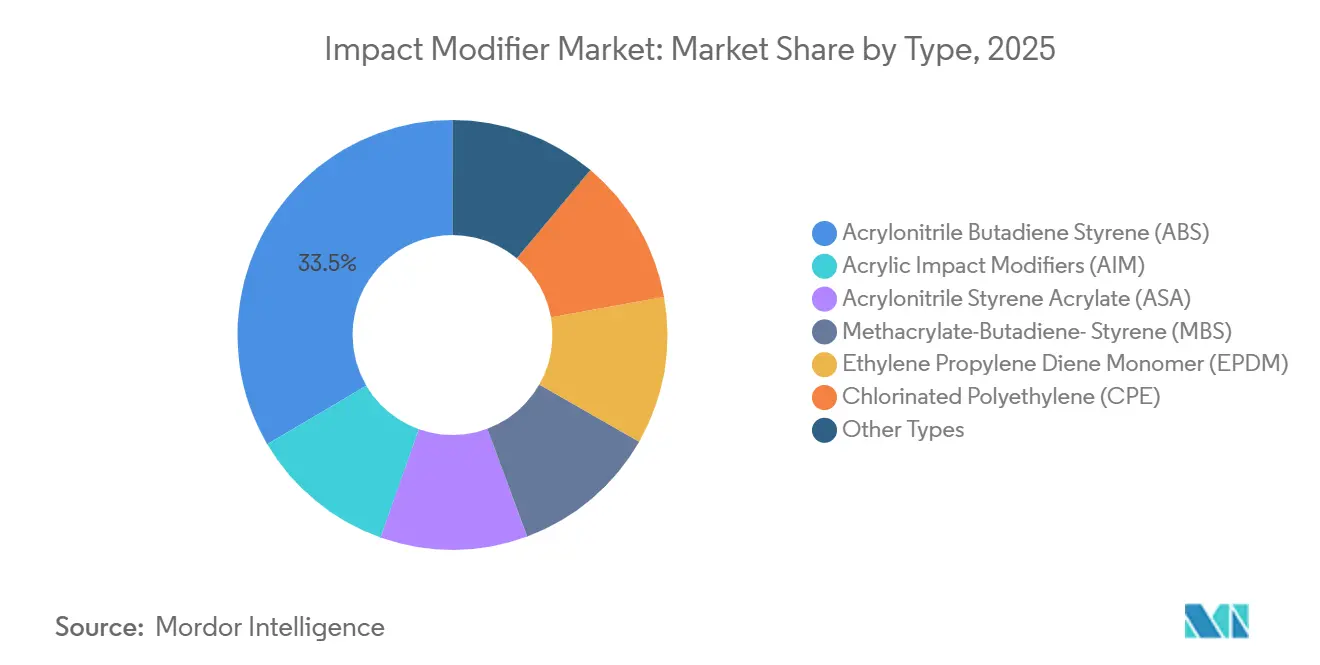

- By type, Acrylonitrile Butadiene Styrene (ABS) held 33.48% of the impact modifier market share in 2025; Acrylic Impact Modifiers (AIM) are forecast to expand at a 6.42% CAGR through 2031.

- By application, Polyvinyl Chloride (PVC) captured 42.67% of the impact modifier market share in 2025. However, the growth of engineering plastics is expected to be at a CAGR of 6.63% during the forecast period (2026-2031).

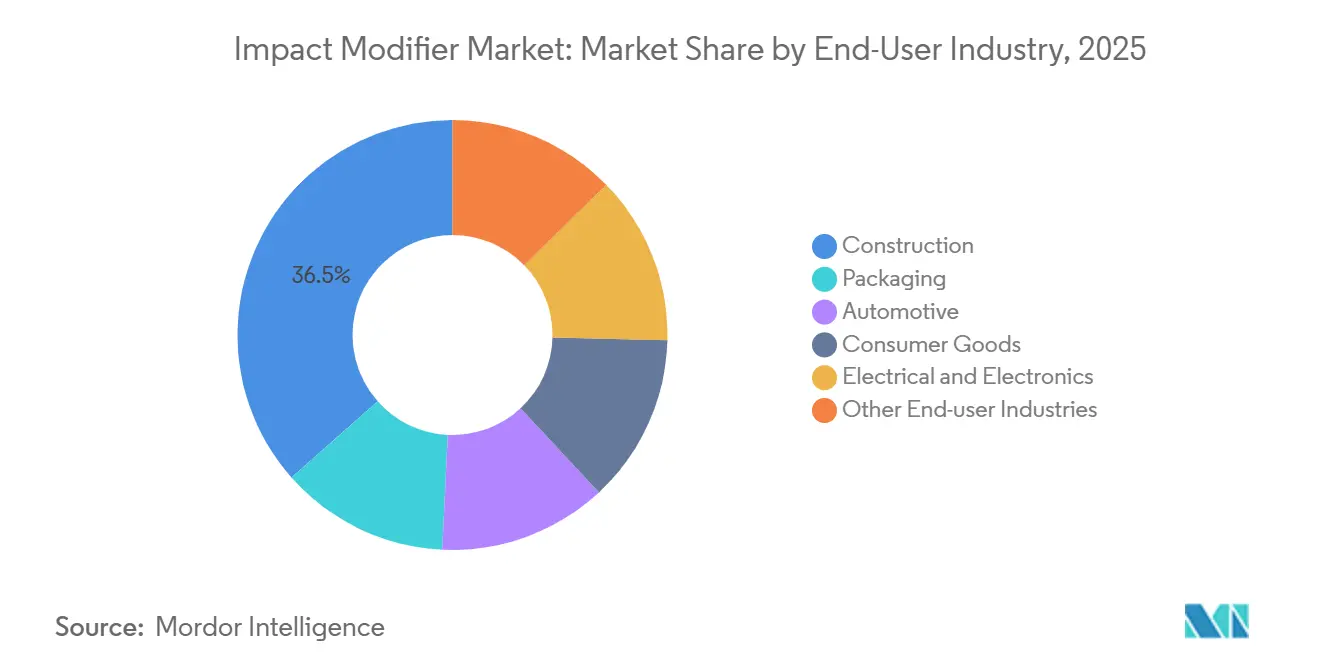

- By end-user, construction led with 36.54% revenue share in 2025; automotive is projected to record the highest 6.45% CAGR to 2031.

- By geography, Asia-Pacific commanded a 47.26% share in 2025, while the Middle East & Africa region is poised for the fastest 6.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Impact Modifier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing packaging demand | +1.2% | Global, concentrated in APAC and North America | Medium term (2-4 years) |

| PVC pipe & profile boom | +1.5% | India, China, ASEAN; spill-over to MEA and South America | Long term (≥4 years) |

| Construction-led resin uptake in APAC | +1.3% | China, India, ASEAN; Saudi Arabia, UAE | Long term (≥4 years) |

| Automotive lightweighting & safety focus | +0.9% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Recycled-content plastics need hybrids | +0.8% | Europe, North America, early urban APAC | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Packaging Demand

Global e-commerce has tightened package-drop durability standards, lifting impact-modified resin offtake for rigid clamshells and tubs by 7.2% year over year in 2025[1]PMMI, “E-commerce Packaging Trends,” pmmi.org. Acrylic grades permit clear PET trays to retain transparency after repeated freeze–thaw cycles, a performance essential for North American meal-kit services that expanded 22% in 2025. Reusable-container legislation in 89 countries channels demand toward ethylene-propylene-diene-monomer (EPDM) modifiers that withstand 500 dish-washer cycles at 75°C. Food-contact rules published by the U.S. FDA in 2025 cap residual acrylate monomers at 50 parts per billion, prompting producers to adopt super-critical CO₂ extraction that raises manufacturing cost by USD 0.18 per kilogram. Larger producers with in-house extraction systems are therefore capturing share from contract blenders unable to absorb the added expense.

PVC Pipe & Profile Boom

Municipal programs across India, Indonesia and Vietnam accelerated the switch from galvanized iron to PVC, citing installed costs of USD 42 per meter for PVC versus USD 68 for ductile iron and a 50-year service-life guarantee. Chlorinated polyethylene (CPE) modifiers captured 62% of the pressure-pipe segment in 2025 because they retain weld-line strength above 85% of base-resin values, enabling joints to pass ISO 13953 hydrostatic tests at 2.5 MPa[2]ISO, “Plastics — Hydrostatic Pressure Tests,” iso.org. China’s 14th Five-Year Plan earmarked CNY 4.8 trillion (USD 670 billion) for urban water networks, absorbing 780,000 metric tons of impact-modified PVC in 2025. In Europe, triple-glazed PVC window profiles satisfying the Passive House 0.8 W/m²K standard consumed 290,000 metric tons of acrylonitrile-styrene-acrylate (ASA) in 2025. Certification under the EU Construction Products Regulation 2024 lifted third-party testing expenditure by EUR 0.09 per kilogram, favoring vertically integrated compounders able to amortize the added cost.

Construction-Led Resin Uptake in APAC

Ongoing megaprojects such as Indonesia’s Nusantara capital city and India’s Pradhan Mantri Awas Yojana collectively added 2.3 million metric tons of impact-modified polymers to regional demand in 2025. Methacrylate-butadiene-styrene (MBS) grades dominate exterior cladding because they pass ASTM D256 impact tests at –40 °C, a benchmark for northern China and South Korea. High humidity and 45 °C ambient temperatures along Southeast Asian rail corridors require UV-stabilized acrylic modifiers that cost USD 0.31 per kilogram more than conventional variants. ASEAN’s infrastructure funding shortfall of USD 210 billion per year through 2030 is therefore a sustained pull-through for durable PVC conduit and siding. From 2025, Japan, South Korea and Singapore made ISO 4892-2 xenon-arc weathering mandatory for exterior parts, boosting demand for premium light-stable chemistries.

Automotive Lightweighting & Safety Focus

Battery-electric vehicle (BEV) production reached 14.2 million units in 2025, each requiring 38 kilograms of impact-modified engineering plastics for battery enclosures and structural trim, 12 kilograms more than internal-combustion counterparts. The 2024 Corporate Average Fuel Economy final rule creates a 6.2% vehicle fuel-economy gain when 18 kilograms of steel are swapped for glass-fiber-reinforced nylon blended with 8-12% impact modifiers. Insurance Institute for Highway Safety protocols updated in 2025 demand 15% higher side-impact energy absorption, accelerating the use of core-shell acrylic modifiers that treble polybutylene-terephthalate (PBT) toughness while adding only 3% weight. Transparent interior bezels are shifting from ABS to acrylic modifiers able to survive 50,000 thermal cycles between –30°C and 80°C without hazing. Tier-1 suppliers in Germany and Japan filed 47 patents during 2024-2025 for modifiers compatible with carbon-fiber-reinforced thermoplastics, targeting mass-production BEV battery cases by 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | –0.6% | Global, acute in Asian spot markets | Short term (≤2 years) |

| Tightening VOC & PVC regulations | –0.4% | Europe, North America, tier-1 Chinese cities, Japan, Korea | Medium term (2-4 years) |

| Processing issues with high-recycle streams | –0.3% | Europe, North America, early-stage urban APAC | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Styrene spot prices swung between USD 950 per metric ton in January 2025 and USD 1,280 in September, a 35% intra-year spread triggered by Asian cracker outages and derivative-demand dips. Butadiene touched USD 1,520 per metric ton in Q4 2025 as U.S. Gulf Coast crackers favored ethane feedstocks that yield 40% less butadiene per ton of ethylene. Non-integrated compounders lacking long-term monomer contracts absorbed USD 0.41 per kilogram cost upticks, yet downstream PVC-pipe extruders kept pass-through below 3% because public tenders in India cap annual escalation at inflation plus one point. Vertically integrated producers representing 38% of global capacity preserved margins by internalizing feedstock swings, widening the competitive gap.

Tightening VOC & PVC Regulations

China’s 2024 update to GB 18581 sliced permissible VOC emissions from polymer plants to 50 milligrams per cubic meter, compelling 34% of Shandong and Jiangsu facilities to install thermal oxidizers costing as much as USD 2.8 million per line. The European Chemicals Agency added four phthalate plasticizers to REACH Annex XIV in 2025, nudging converters toward higher-cost non-phthalate impact modifiers. California’s Safer Consumer Products rule, effective 2025, classified styrene-containing additives used in rigid food packaging as Priority Products, elongating development cycles by up to two years. India’s proposed ban on single-use PVC packaging by 2028 creates demand uncertainty for modifiers tailored to flexible-film markets. Across Europe, ISO 16000-6 indoor-air-quality certification fees rose to EUR 8,500 per formulation, deterring small entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: ABS Retains Lead while Acrylic Grades Accelerate

ABS commanded 33.48% of the impact modifiers market in 2025 on the back of cost-effective toughness for appliance housings and automotive interiors. Within this segment, ABS contributed USD 1.54 billion to the impact modifiers market size, reflecting broad acceptance where opaque finishes and 15 kJ/m² notched Izod impact strength are sufficient. Acrylic grades, though smaller, are growing at 6.42% CAGR because transparent PVC window profiles and PET clamshells demand weather-stable clarity after 500-hour QUV exposure. MBS occupied 22% of rigid-PVC pipe consumption in 2025 but faces price pressure as Chinese exporters undercut European equivalents by 14%.

Acrylonitrile-styrene-acrylate (ASA) expands for outdoor siding and automotive exterior panels where –30°C impact retention and UV durability are decisive. CPE secured a share owing to its ability to maintain ductility at 2.5 MPa hydrostatic stress for potable-water pipes. EPDM remains niche, yet its dishwasher-cycle endurance aligns with reusable-container mandates. Maleic-anhydride-grafted acrylic variants launched in 2025 now reclaim 92% of virgin toughness in PCR PVC, attracting a USD 0.90 per kilogram premium over standard grades.

By Application: PVC Dominates, Engineering Plastics Surge

PVC represented 42.67% of the impact modifiers market share in 2025, equivalent to USD 2.07 billion of the impact modifiers market size, with rigid pipes accounting for 58% of PVC demand. Engineering plastics, however, are forecast to grow at a 6.63% CAGR through 2031 as BEV battery packs require flame-retardant nylon housings that keep impact strength above 25 kJ/m² at 150°C. Glass-fiber-reinforced PA 66 blended with 9-13% modifiers is displacing steel in structural battery trays, shaving 18% mass.

Polybutylene-terephthalate (PBT) applications advanced in 2025, driven by autonomous-vehicle sensor housings that demand dimensional stability at 150°C. Polycarbonate blends for consumer electronics and safety glazing filled 14% of overall volume, posting growth as laptop makers adopted PC/ABS alloys that pass 1.2-meter drop tests. California’s styrene-additive scrutiny is restraining new PVC film grades, whereas IIHS side-impact revisions propel acrylic-modified PBT adoption.

By End-User Industry: Construction Anchors, Automotive Accelerates

Construction absorbed 36.54% of revenue in 2025, lifted by India’s household-water push and Southeast Asian housing booms. Each completed rural home in India incorporated 42 kilograms of impact-modified PVC conduit and plumbing as of 2025. Automotive is projected to log the steepest 6.45% CAGR because BEVs need 15% more impact-modified polymers than internal-combustion vehicles to protect lithium-ion cells from side-impact intrusion.

Consumer goods grew as reusable-container standards proliferated, demanding three-to-five-fold higher impact strength than single-use versions. Electrical and electronics applications share was centered on cable trays and junction boxes certified to UL 746C for 125°C thermal aging.

Geography Analysis

Asia-Pacific controlled 47.26% of the impact modifiers market in 2025 and will compound at 6.35% through 2031. China alone produced 6.8 million metric tons of PVC pipes for Belt-and-Road projects, while India’s affordable-housing scheme consumed 470,000 metric tons of impact-modified PVC conduit. ASEAN nations placed 12,400 kilometers of rural water pipelines in 2025, with Vietnam and Thailand leading installations. Japan and South Korea filed 47 patents for carbon-fiber-compatible modifiers targeting mass-production BEV battery enclosures from 2027. Regulatory tightening under GB 18581 forced over one-third of Chinese modifier plants to install VOC oxidizers, consolidating capacity among integrated majors.

North America’s share expanded as the US EPA fuel-economy rule accelerated steel-to-polymer substitution. Canada upgraded potable-water systems, while Mexico’s USD 18 billion automotive near-shoring boom widened engineering-plastic demand. California’s Safer Consumer Products framework introduced additional testing layers for styrene-based additives, momentarily delaying rigid-packaging launches.

Europe faces margin pressure from ECHA’s 2025 phthalate restrictions and the 30% PCR requirement under the Packaging and Packaging Waste Regulation. Germany, France and Italy jointly absorbed the majority of regional volumes, predominantly window-profile extrusion that must meet the Passive House 0.8 W/m² K threshold.

South America represented the lowest demand, with Brazil’s 7.8 million-unit housing shortfall fueling PVC uptake, and Argentina’s lithium operations specifying impact-modified liners for evaporation ponds. The Middle East and Africa are forecast to post the quickest CAGR as Saudi Arabia’s USD 3.2 trillion Vision 2030 pipeline specifies impact-modified polymers for 1.5 million homes and 8,500 kilometers of roads. Differential standards persist: SASO allows 120 mg/kg residual styrene versus the EU cap of 100 mg/kg, enabling Gulf producers to underprice European exporters by up to 12% for non-food applications.

Competitive Landscape

The Impact Modifier market is moderately concentrated. Vertically integrated players with captive styrene and acrylate monomer lines maintained 6-8 percentage-point gross-margin cushions during 2025’s 35% styrene swing. Technology adoption is bifurcated. Integrated majors employ AI-enabled rheology controls that cut off-spec waste by up to 55%. Growth white-spaces cluster in bio-based acrylic monomers, plasma-oxidation pretreatment for recyclate, and core-shell architectures that treble toughness at minimal weight penalty.

Impact Modifier Industry Leaders

Arkema

Dow

Kaneka Corporation

LG Chem

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: ARKEMA is set to showcase its latest innovations at K2025 in Düsseldorf, Germany. The company will highlight its advanced impact modifiers, including Durastrength and Clearstrength. These innovations are expected to strengthen ARKEMA's position in the impact modifiers market by addressing evolving industry demands and enhancing product performance.

- July 2024: Kaneka Corporation has announced a price revision for its impact modifiers - Kane Ace B, Kane Ace M, and Kane Ace FM. This decision is aimed at enhancing profitability by reducing costs and ensuring a stable supply in the future. The price adjustment is expected to influence the impact modifiers market by potentially maintaining consistent availability.

Global Impact Modifier Market Report Scope

Impact modifier resins increase the durability of molded and extruded plastics, especially for impact strength or cold-weather services. They are important supplements added to increase elasticity to overcome the rigidity of materials.

The Impact Modifier Market is segmented by type, application, and end-user industry. By type, the market is segmented into acrylonitrile butadiene styrene, acrylic impact modifiers, acrylonitrile styrene acrylate, methacrylate-butadiene-styrene, ethylene propylene diene monomer, chlorinated polyethylene, and other types. By application, the market is segmented into polyvinyl chloride, nylon, polybutylene terephthalate, engineering plastics, and other applications. By end-user industry, the market is segmented into automotive, construction, consumer goods, packaging, and other end-user industries. The report also covers the market size and forecasts for the impact modifier market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Acrylonitrile Butadiene Styrene (ABS) |

| Acrylic Impact Modifiers (AIM) |

| Acrylonitrile Styrene Acrylate (ASA) |

| Methacrylate-Butadiene- Styrene (MBS) |

| Ethylene Propylene Diene Monomer (EPDM) |

| Chlorinated Polyethylene (CPE) |

| Other Types |

| Polyvinyl Chloride (PVC) |

| Nylon |

| Polybutylene Terephthalate (PBT) |

| Engineering Plastics |

| Other Applications |

| Packaging |

| Construction |

| Automotive |

| Consumer Goods |

| Electrical and Electronics |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Acrylonitrile Butadiene Styrene (ABS) | |

| Acrylic Impact Modifiers (AIM) | ||

| Acrylonitrile Styrene Acrylate (ASA) | ||

| Methacrylate-Butadiene- Styrene (MBS) | ||

| Ethylene Propylene Diene Monomer (EPDM) | ||

| Chlorinated Polyethylene (CPE) | ||

| Other Types | ||

| By Application | Polyvinyl Chloride (PVC) | |

| Nylon | ||

| Polybutylene Terephthalate (PBT) | ||

| Engineering Plastics | ||

| Other Applications | ||

| By End-user Industry | Packaging | |

| Construction | ||

| Automotive | ||

| Consumer Goods | ||

| Electrical and Electronics | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR is projected for the impact modifiers market through 2031?

A 6.31% CAGR is forecast for 2026-2031, lifting value to USD 6.63 billion.

Which polymer type leads current demand?

ABS leads with 33.48% share, mainly in automotive interiors and appliances.

Why are acrylic impact modifiers growing fastest?

They enable transparent, weather-stable PVC and PET applications and comply with tougher recycled-content rules.

Which end-user segment will expand most rapidly?

Automotive is set for a 6.45% CAGR as BEVs require more impact-modified engineering plastics.

Which region offers the highest incremental opportunity?

Asia-Pacific remains largest, but the Middle East and Africa show the quickest growth at 6.58% CAGR under Vision 2030 infrastructure programs.

Page last updated on: