IGBT And Super Junction MOSFET Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

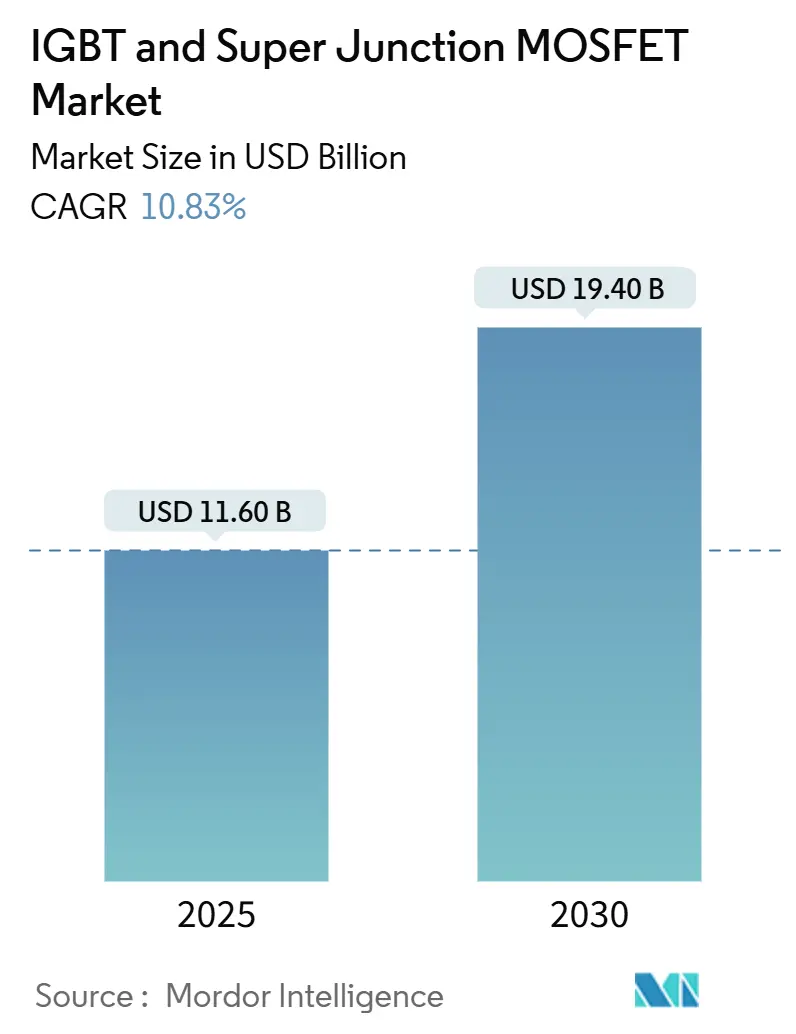

| Market Size (2025) | USD 11.60 Billion |

| Market Size (2030) | USD 19.40 Billion |

| Growth Rate (2025 - 2030) | 10.83% CAGR |

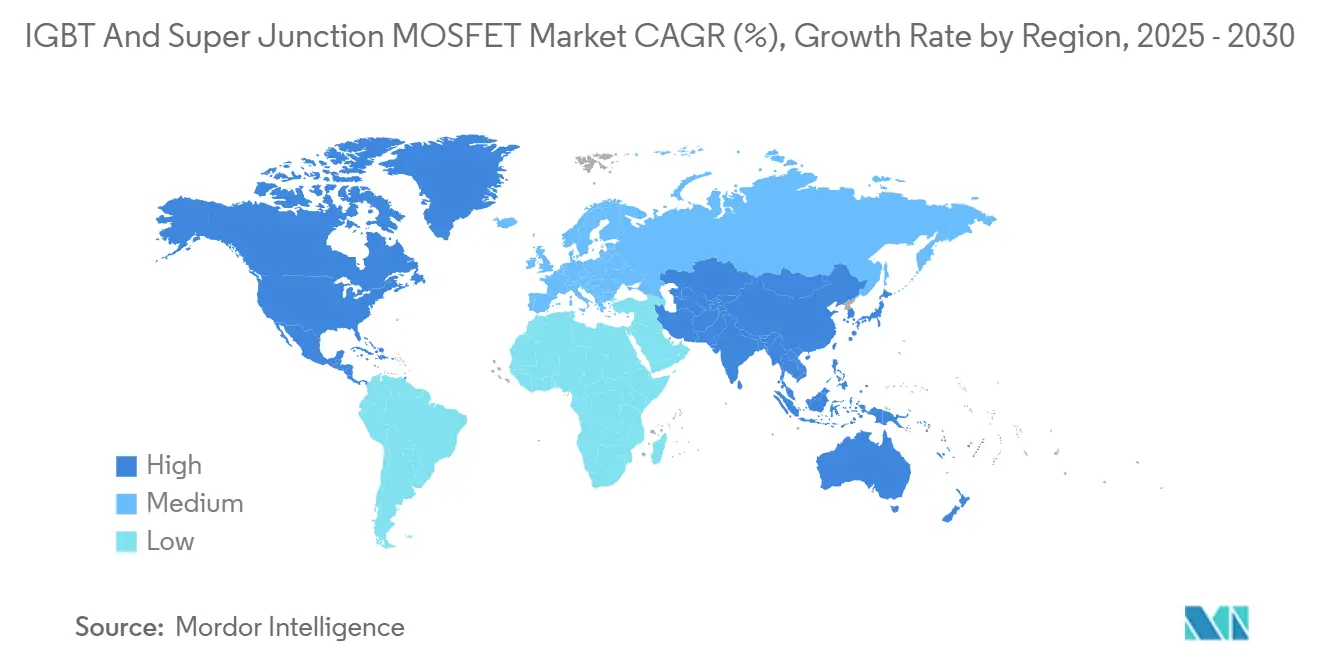

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IGBT And Super Junction MOSFET Market Analysis by Mordor Intelligence

The IGBT and Super Junction MOSFET market size stands at USD 11.6 billion in 2025 and is projected to achieve USD 19.4 billion by 2030, translating into a 10.83% CAGR during the forecast period. Robust demand from electric vehicle (EV) traction inverters, renewable-energy inverters, and industrial motor drives underpins this expansion. Automakers shifting from 400 V to 800 V electrical architectures, renewable portfolio standards that mandate faster grid balancing, and factory automation trends that favor high-efficiency drives collectively accelerate device adoption. At the same time, competitive pressures from silicon-carbide (SiC) alternatives spur continuous silicon device innovation in switching speed, thermal handling, and package integration. Medium-voltage modules remain the economic workhorse for most traction inverters and industrial drives, yet high-voltage modules above 1,200 V garner rising attention in grid-scale batteries and railway traction, where switching losses directly affect lifetime operating expenditure.

Key Report Takeaways

- By end-use industry, automotive captured 40.7% of the IGBT and Super Junction MOSFET market share in 2024. Energy and Power are forecast to grow at a 12.5% CAGR through 2030.

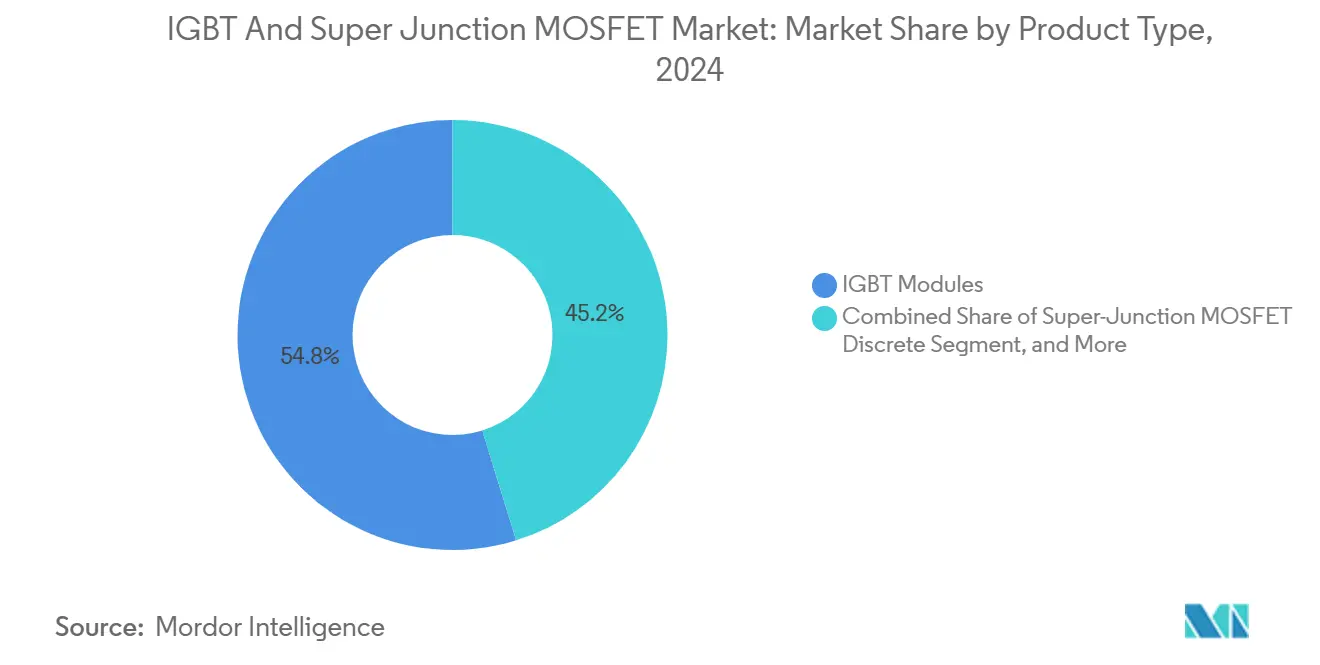

- By product type, IGBT modules led with 54.8% revenue share in 2024; Super-Junction MOSFET modules are projected to accelerate at an 11.3% CAGR during 2025-2030.

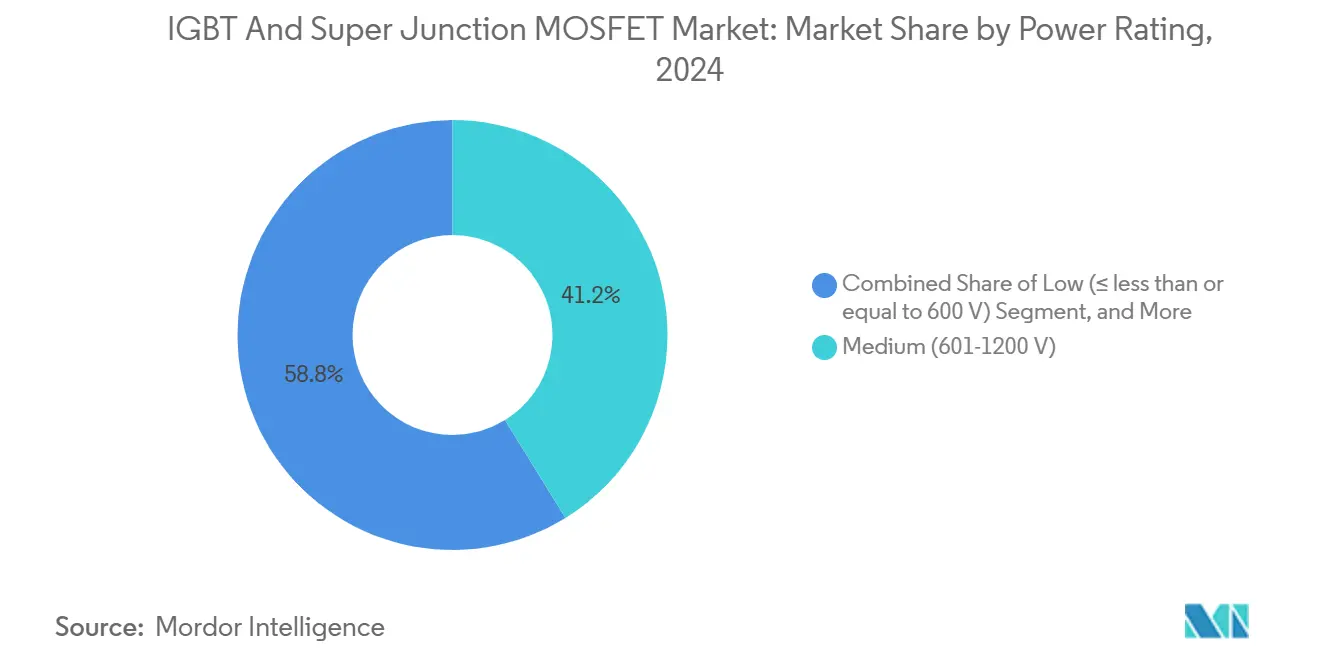

- By power rating, medium-voltage devices (601-1,200 V) held 41.2% of the 2024 IGBT and Super Junction MOSFET market size, while high-voltage devices above 1,200 V will advance at an 11.6% CAGR to 2030.

- By geography, Asia-Pacific maintained a 39.6% revenue share in 2024; North America is expected to deliver the fastest 12.7% CAGR over the forecast period.

Global IGBT And Super Junction MOSFET Market Trends and Insights

Driver Imapct Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| EV-led power electronics demand surge | +2.8% | Global (Asia-Pacific and North America lead) | Medium term (2-4 years) |

| Renewable inverters adoption | +2.1% | Global (Europe and North America focus) | Long term (≥ 4 years) |

| Industrial automation shift to silicon-based modules | +1.9% | Asia-Pacific core; Europe spill-over | Medium term (2-4 years) |

| Power density pushes in data centers | +1.7% | North America and Europe; Asia-Pacific emerging | Short term (≤ 2 years) |

| Railway electrification programs | +1.4% | Europe and Asia-Pacific | Long term (≥ 4 years) |

| Grid-connected battery storage roll-out | +1.2% | Global; early Australia and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV-Led Power Electronics Demand Surge

Traction inverters inside battery electric vehicles represent the single-largest growth lever for the IGBT and Super Junction MOSFET market. Automakers’ migration to 800 V architectures halves DC-link current, trims copper weight, and facilitates sub-20-minute ultra-fast charging, all of which heighten the value of low-loss switching devices capable of managing elevated junction temperatures. Infineon’s CoolSiC hybrid modules co-packaging trench-stop IGBTs with SiC diodes lower conduction losses in 160 kW traction inverters while retaining cost competitiveness for mid-price EVs. Onsemi’s multi-year supply agreement with Volkswagen Group further highlights how synchronous EV capacity expansions lock in power-module supply to mitigate silicon-wafer volatility.[1]Source: Onsemi, “Onsemi selected to power Volkswagen Group’s next-generation electric vehicles,” onsemi.com Beyond passenger cars, electric buses, and light commercial vans incorporate auxiliary 48 V converters based on Super-Junction MOSFETs whose reduced reverse-recovery charge enhances transient efficiency in stop-and-go duty cycles.

Renewable Inverters Adoption

Utility-scale solar and onshore wind additions correlate directly with gigawatt-scale inverter demand, benefitting high-voltage IGBT stacks that can withstand 1,500 VDC string voltages and deliver 99% peak conversion efficiency. Wärtsilä’s 200 MWh grid-storage projects in Scotland employ half-bridge IGBT modules inside four-level neutral-point-clamped topologies, demonstrating how higher device blocking voltages reduce inverter part counts and field-maintenance complexity. Parallel roll-outs of reactive power-compensating STATCOMs across continental Europe also reinforce sustained procurement of medium-voltage press-pack IGBTs. Meanwhile, Super-Junction MOSFETs dominate boost-stage designs in residential micro-inverters where their sub-100 ns turn-on speed improves partial-shade efficiency thresholds and compliance with IEEE 1547 requirements on anti-islanding response times.

Industrial Automation Shift to Silicon-Based Modules

Variable-frequency drives, servo packs, and weld controllers favor mature silicon platforms that align with factory uptime mandates and decades-old thermal interface standards. Toshiba’s dual-sided multi-gate IGBT architecture delivers 34% lower turn-off loss than previous planar generations, enabling 200 kW presses and pick-and-place robots to operate within constrained control-cabinet airflow envelopes.[2]Source: Toshiba Corporation, “TOSHIBA REVIEW Science and Technology Highlights 2024,” toshiba.com In many discrete-device retrofit projects, line engineers prefer standard TO-247 IGBTs because existing mounting fixtures and gate-driver layouts can be retained; thus, silicon’s installed-base inertia shields it from rapid SiC substitution. Even so, module suppliers incorporate AlSiC baseplates and solder-less pressure-contact designs that stretch mission-profile life to 20 years under repetitive thermal cycling.

Power Density Push in Data Centers

Artificial-intelligence (AI) servers exceed 100 kW per rack, magnifying the enterprise value of each efficiency percentage point in AC-DC front-ends. Onsemi’s USD 115 million acquisition of SiC JFET IP aims squarely at that compute-cluster inflection, targeting 3-level T-type rectifiers that can slash conduction loss versus legacy diode-clamped stages. Nevertheless, Super-Junction MOSFETs retain a share in 48 V intermediate bus converters up to 3 kW, where their fast body-diode recovery curtails reverse energy and EMI within conduction-cooled power shelves. High-density colocation operators experiment with liquid-cooling cold plates that keep silicon junction temperature below 90 °C, permitting MOSFET RDS(on) parity against more expensive SiC offerings in the 600 V class.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| SiC device price competition | -1.8% | Global premium applications | Medium term (2-4 years) |

| Supply-chain silicon wafer tightness | -1.5% | Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Thermal management limits above 650 V | -1.2% | High-power markets worldwide | Long term (≥ 4 years) |

| Export-control compliance costs | -0.9% | U.S.–China corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

SiC Device Price Competition

Wolfspeed’s Mohawk Valley 200 mm fab scales SiC wafer output tenfold, compressing cost curves and narrowing the silicon–SiC price differential in 800 V traction inverters. Car OEMs lured by 4% vehicle-range gains eye partial SiC adoption, particularly in top-trim EVs, diverting share from traditional trench-stop IGBTs. Legacy suppliers counter with reverse-conducting IGBT (RC-IGBT) designs that integrate free-wheel diodes and cut the bill of materials by 15% in motor inverters.

Supply-Chain Silicon Wafer Tightness

Global foundry prioritization of advanced logic nodes occasionally curtails 6-inch and 8-inch wafer availability for power devices, prompting Infineon to build a backend module facility in Samut Prakan, Thailand, to localize assembly and buffer frontend volatility. Device makers increasingly sign multi-year take-or-pay wafer agreements and invest in captive poly-silicon supply to lower exposure to geopolitical disruptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Module Integration Redefines Packaging Choices

IGBT modules held 54.8% revenue contribution to the IGBT and Super Junction MOSFET market in 2024, reflecting OEM preference for pre-validated, thermally optimized building blocks. These modules combine multiple dies, integrated NTC thermistors, and press-fit pins, trimming inverter assembly time by 30% versus discrete implementations. Over the forecast horizon, automakers deploy double-sided cooling substrates that cut thermal resistance by 40%, which in turn supports 25% higher current density at identical junction temperatures.

Super-Junction MOSFET modules, though accounting for a smaller revenue base, expand at an 11.3% CAGR thanks to server power supplies, telecom rectifiers, and residential hybrid inverters demanding up to 65 kHz switching. In half-bridge PFC stages, MOSFET modules lower EMI filter sizing and facilitate >99% efficiency at 230 VAC input. Discrete devices still dominate cost-sensitive appliances, air-conditioner inverters, washing-machine drives, and microwave ovens, where a single TO-220 or D-PAK meets output-power needs under 2 kW. Even here, device makers add Kelvin-source leads and sense pins to optimize gate-driver slew-rate control, squeezing incremental efficiency gains without package cost inflation.

By Power Rating: Voltage Class Dictates Architecture Evolution

Medium-voltage devices spanning 601-1,200 V command 41.2% of 2024 revenue, benefitting EV traction inverters, industrial drives, and three-phase UPS systems that cluster around 800 V DC-link levels. For traction, OEMs often deploy 750 V IGBTs to accommodate regenerative over-voltage transients and auxiliary-load fluctuations without derating. The IGBT and Super Junction MOSFET market share of the medium-voltage class is anchored by long qualification cycles and abundant supply capacity across multiple fabs.

High-voltage devices exceeding 1,200 V exhibit an 11.6% CAGR propelled by grid-tied storage converters, central-station PV, and locomotive traction. In multi-megawatt wind turbines, 1.7 kV press-pack IGBTs embedded in 3-level neutral point clamped topologies handle reactive-power support and fault-ride-through compliance at 690 VAC generator outputs. Device manufacturers introduce soft-punch-through structures and field-stop layers to tame tail current, thereby reducing switching loss by 20% relative to prior generations. Low-voltage (≤ 600 V) MOSFETs endure in appliance PFC, laptop adapters, and LED drivers, where their high-frequency merit outshines IGBTs; nonetheless, revenue growth remains muted as unit ASPs erode under intense commoditization.

By End-Use Industry: Electrification Drives Energy and Power Upswing

Automotive applications commanded 40.7% 2024 revenue, encompassing traction inverters, DC-DC converters, climate-compressor inverters, and onboard chargers. Typical battery-electric sedans integrate devices worth USD 92 per vehicle, roughly 4× higher than internal-combustion counterparts.

Energy and Power emerges as the fastest-growing vertical at a 12.5% CAGR through 2030 as utilities expand grid-scale battery banks and retire synchronous generation assets. This transformation elevates demand for four-quadrant inverters capable of synthetic inertia, black-start, and frequency-regulation services. In pump-storage retrofits, modular multilevel converters equipped with 3.3 kV IGBTs replace legacy thyristor bridges to enable variable-speed operation, enhancing round-trip efficiency by 5 percentage points.

Industrial manufacturing maintains a sizeable addressable base across conveyor drives, CNC machines, and plastic extruders that collectively number in the tens of millions. Here, equipment vendors favor silicon IGBTs’ predictable safe-operating-area curves amid abrasive dust and ambient temperatures that often exceed 55 °C. Data-center and ICT customers lean on Super-Junction MOSFETs inside high-efficiency LLC resonant supplies; hyperscale operators project total rack-level power to triple by 2028, sustaining volume pull for 650 V fast-recovery parts.

Geography Analysis

Asia-Pacific retained 39.6% revenue in 2024, powered by China’s 1.6 million EV unit shipments and South Korea’s leading memory-fabrication energy-storage retrofits. Local governments subsidize 300 mm analog fabs and backend assembly clusters, reinforcing cost advantages. As capital intensity rises, however, the region actively pursues dual-sourcing initiatives to mitigate single-source wafer risks.

North America’s 12.7% CAGR stems from USD 52 billion CHIPS Act incentives that catalyze domestic wide-bandgap fabs in Arizona, Texas, and New York. Automotive original-equipment manufacturers are localizing battery-electric assembly lines in Tennessee, Michigan, and Ontario, triggering parallel demand for traction-inverter modules and on-board charger MOSFETs. The U.S. also commands half the global hyperscale data-center footprint, and AI accelerator clusters in Ohio and Iowa already quote 100 MW campus power blocks that require high-density AC-DC conversion.

Europe maintains a technology leadership role, especially in 400 Hz aerospace power supplies and 25 kV rail electrification. Germany’s Fraunhofer IISB pilots adaptive gate-drive algorithms that exploit IGBT current-tail cancellation to raise switching frequencies without elevating dv/dt stress on insulation coordination. Meanwhile, the European Union’s REPowerEU plan funds 30 GW of additional solar and 10 GW of battery storage annually, cementing long-run demand for both 1.2 kV IGBTs and 650 V Super-Junction MOSFETs.

Competitive Landscape

The top five suppliers, Infineon, onsemi, Mitsubishi Electric, Fuji Electric, and Renesas, collectively hold a significant revenue share, placing the market at a moderately consolidated equilibrium. Scale economies in epitaxial wafer growth, power metallization, and automated wire-bond inspection constitute high entry barriers. Strategy pivots around vertical integration: Infineon’s backend fab in Thailand de-risks geographic supply concentration, while onsemi’s silicon-carbide JFET acquisition expands its lattice of proprietary intellectual property across both silicon and SiC portfolios.

Technology differentiation remains decisive. Infineon launched its seventh-generation TrenchStop IGBT featuring micro-pattern trench gating that lowers turn-off energy 24% without sacrificing conduction drop, directly answering SiC’s efficiency narrative. Mitsubishi Electric’s compact T-series module relies on solder-less press-contact construction that quadruples power-cycling capability relative to soldered designs. White-space opportunities include factory-installed rail-traction upgrade kits and bidirectional 1.2 kV solid-state circuit breakers, both of which reward providers offering application-specific testing services and long-term failure-analysis support.

Emerging disruptors such as Navitas and Nexgen aim to deliver GaN power ICs that integrate driver, FET, and protection inside monolithic packages at parity cost to discrete Super-Junction MOSFETs in 3 kW chargers. Established vendors respond by emphasizing mixed-technology roadmaps; Renesas’ July 2025 GaN FET launch explicitly targets AI server backplane converters where switching speeds above 1 MHz deliver form-factor advantages.[3]Source: Renesas, “Renesas strengthens power leadership with new GaN FETs,” renesas.com

IGBT And Super Junction MOSFET Industry Leaders

Infineon Technologies AG

Mitsubishi Electric Corporation

Fuji Electric Co., Ltd.

ON Semiconductor Corporation

STMicroelectronics N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Toshiba showcased 2-in-1 SiC modules for 250 kW light-commercial-vehicle inverters at PCIM 2025.

- January 2025: Infineon Technologies broke ground on a backend power-module plant in Samut Prakan, Thailand, slated to commence volume production in early 2026.

- January 2025: Onsemi finalized a USD 115 million purchase of Qorvo’s SiC JFET assets, broadening EliteSiC for AI data-center power shelves.

- June 2024: Renesas completed the USD 339 million takeover of Transphorm, adding GaN competence for EV chargers and renewable-energy inverters.

Global IGBT And Super Junction MOSFET Market Report Scope

| IGBT Discrete |

| IGBT Modules |

| Super-Junction MOSFET Discrete |

| Super-Junction MOSFET Modules |

| Low (≤600 V) |

| Medium (601-1200 V) |

| High (>1200 V) |

| Automotive |

| Energy and Power |

| Industrial Manufacturing |

| ICT and Data Centers |

| Consumer Appliances |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | IGBT Discrete | ||

| IGBT Modules | |||

| Super-Junction MOSFET Discrete | |||

| Super-Junction MOSFET Modules | |||

| By Power Rating | Low (≤600 V) | ||

| Medium (601-1200 V) | |||

| High (>1200 V) | |||

| By End-Use Industry | Automotive | ||

| Energy and Power | |||

| Industrial Manufacturing | |||

| ICT and Data Centers | |||

| Consumer Appliances | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the IGBT and Super Junction MOSFET market in 2025?

The IGBT and Super Junction MOSFET market size is valued at USD 11.6 billion in 2025.

What CAGR is forecast for these devices through 2030?

The market is projected to expand at a 10.83% CAGR from 2025 to 2030.

Which end-use industry holds the highest revenue share?

Automotive applications lead with 40.7% market share in 2024.

Which product category grows quickest?

Super-Junction MOSFET modules are forecast to grow at an 11.3% CAGR.

Page last updated on: