Gate Driver Integrated Circuit Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

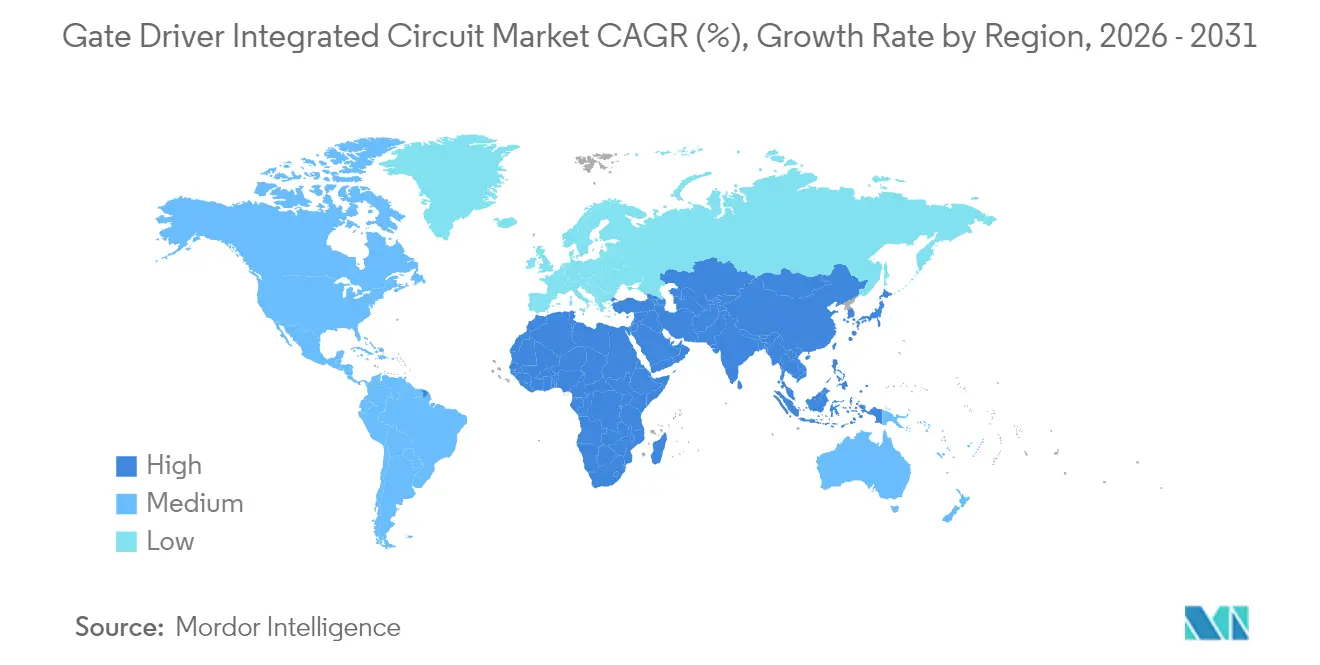

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

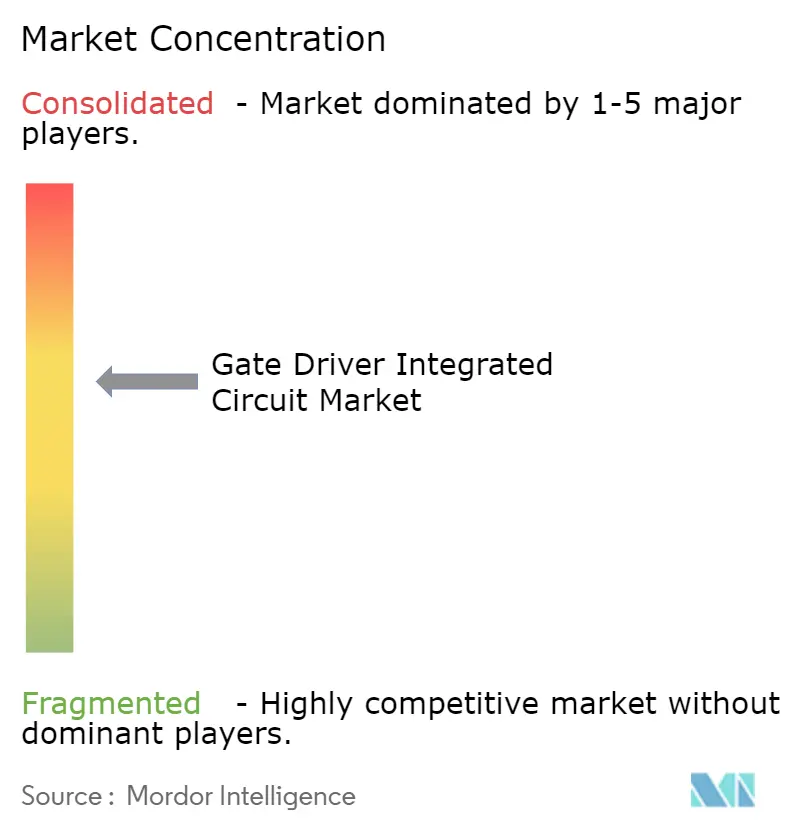

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gate Driver Integrated Circuit Market Analysis by Mordor Intelligence

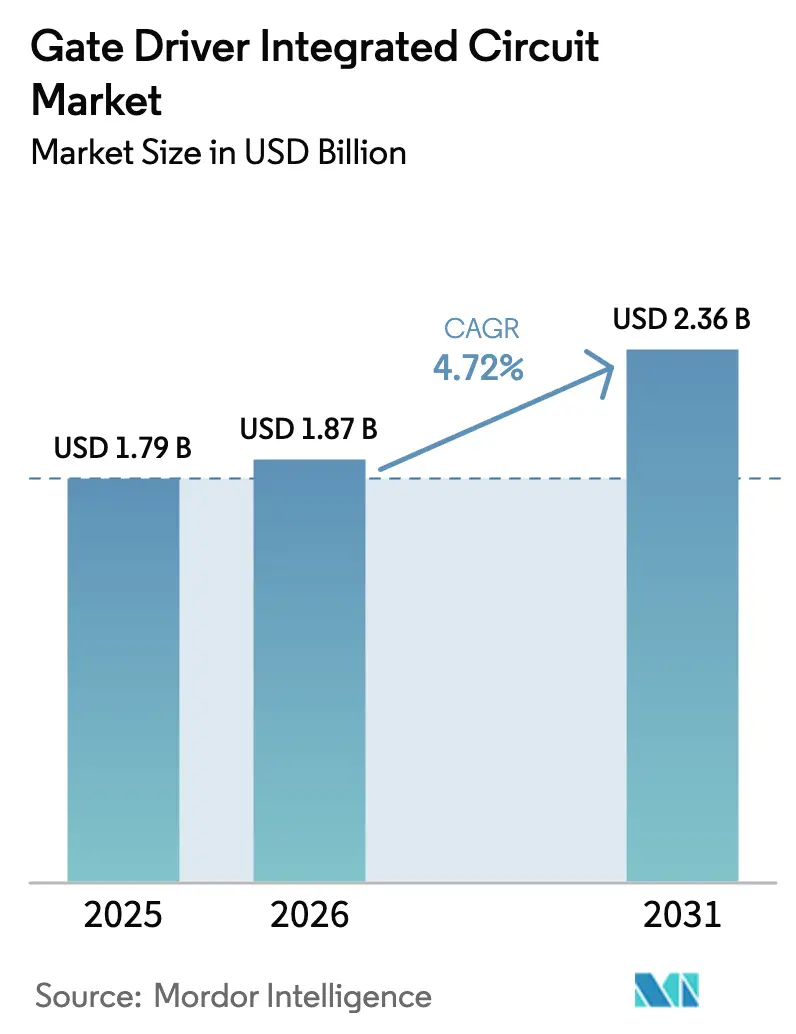

The gate driver integrated circuit market size was valued at USD 1.79 billion in 2025 and estimated to grow from USD 1.87 billion in 2026 to reach USD 2.36 billion by 2031, at a CAGR of 4.72% during the forecast period (2026-2031). Wide-bandgap semiconductor deployment, accelerated electrification mandates, and hyperscale data-center power-density targets collectively raise the performance bar for gate-drive solutions. Suppliers respond by pairing proprietary silicon-carbide or gallium-nitride power devices with application-specific driver ICs that offer sub-35 ns propagation delay and reinforced isolation. Competitive pressure from Chinese foundries compresses device margins, yet system-level integration cushions pricing by bundling diagnostics, protection, and communication features. Automotive OEM preference for ISO 26262-compliant driver-device platforms further amplifies content per vehicle, while utility-scale battery storage projects underpin long-term volume growth across industrial channels. Taken together, the gate driver integrated circuit market is maturing yet remains innovation-led, with design wins shifting toward solutions that optimize speed, safety, and thermal robustness.

Key Report Takeaways

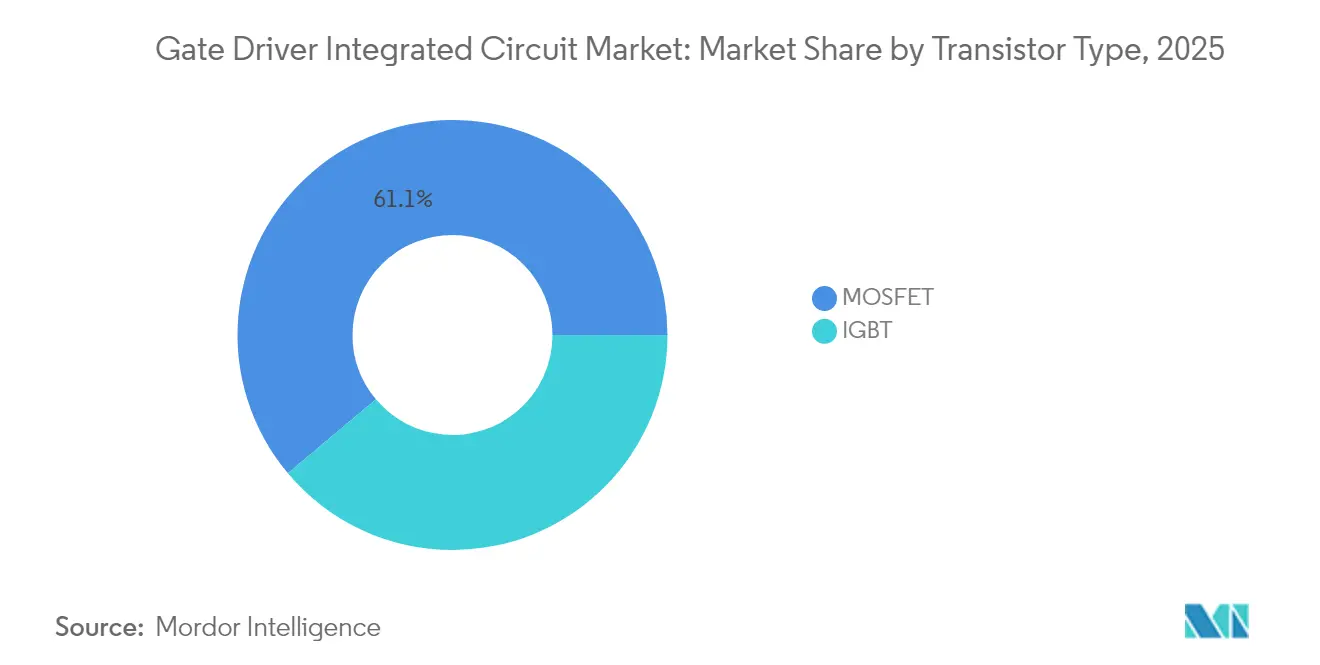

- By transistor type, MOSFETs led with 61.12% revenue share of the gate driver integrated circuit market in 2025; IGBTs are projected to expand at a 7.35% CAGR through 2031.

- By isolation type, isolated gate driver ICs held 69.05% of the gate driver integrated circuit market share in 2025, while non-isolated gate driver ICs will grow at 9.18% CAGR through 2031.

- By semiconductor material, silicon (Si) accounted for 78.15% share of the gate driver integrated circuit market size in 2025, whereas silicon carbide (SiC) is forecast to expand at 10.92% CAGR through 2031.

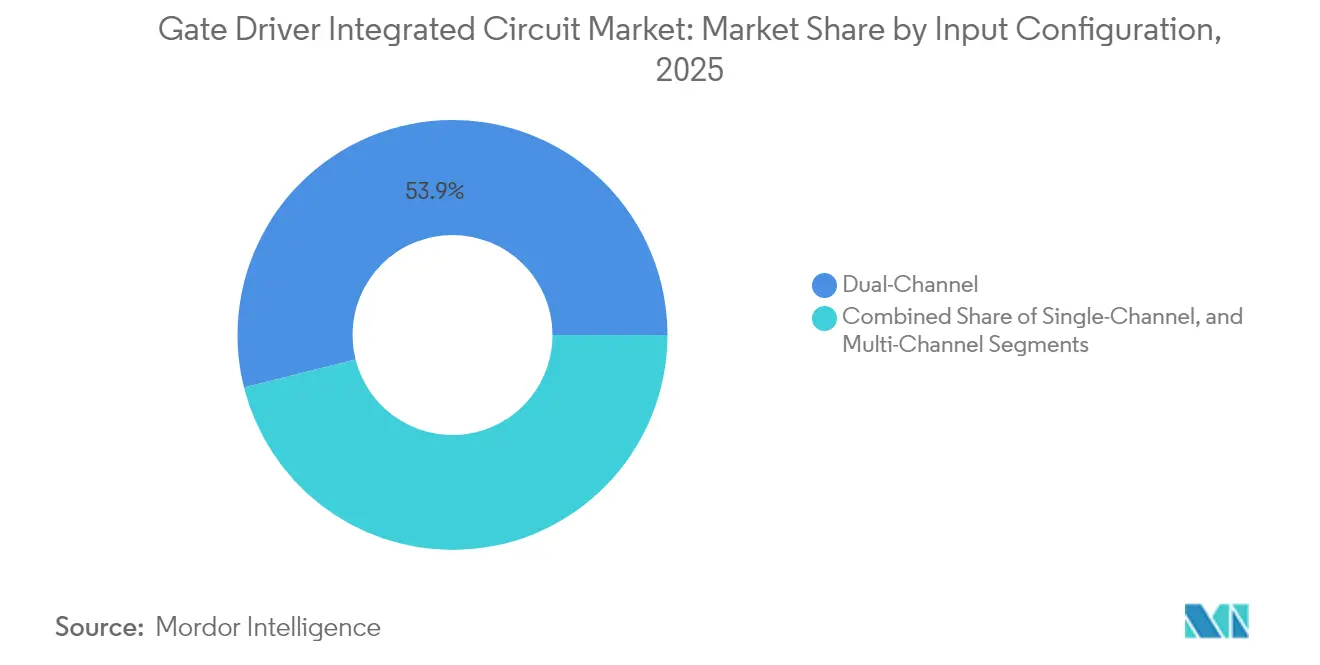

- By input configuration, dual-channel devices captured 53.92% revenue share in 2025; multi-channel solutions will record 5.82% CAGR through 2031.

- By application, industrial systems represented 41.85% share of the gate driver integrated circuit market size in 2025, and residential applications are growing at 6.12% CAGR to 2031.

- By end-user industry, automotive held 36.55% share in 2025, while energy and power shows the highest projected CAGR at 7.12% through 2031.

- By geography, Asia-Pacific commanded 48.05% share in 2025; Middle East and Africa is advancing at 7.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gate Driver Integrated Circuit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in SiC and GaN power-device adoption | +1.8% | North America, Europe, China | Medium term (2-4 years) |

| Rapid EV on-board-charger & traction inverters | +1.2% | China, Europe, North America | Short term (≤ 2 years) |

| Expansion of PV & battery-storage inverters | +0.9% | Asia-Pacific, Europe | Medium term (2-4 years) |

| High-frequency switching in hyperscale data centers | +0.7% | North America, Europe, select Asia-Pacific markets | Short term (≤ 2 years) |

| Proliferation of smart-appliance BLDC motors | +0.6% | China, Japan, South Korea | Long term (≥ 4 years) |

| Efficiency standards lifting driver content | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in SiC and GaN Power Device Adoption Requiring Advanced Gate Drivers

Wide-bandgap devices switch at tens of megahertz, forcing designers to specify driver ICs with sub-35 ns delay and >300 kV/µs common-mode immunity.[1]Texas Instruments, “TIDA-01605 reference design,” ti.com SiC MOSFETs also need bipolar gate voltages of +15 V/-4 V and robust short-circuit detection, which traditional silicon-focused drivers cannot supply. Infineon’s trench-based SiC super-junction devices released in 2025 lower on-resistance by 40%, yet they place tighter constraints on gate-voltage accuracy and thermal handling.[2]Infineon Technologies AG, “Infineon introduces trench-based SiC superjunction technology,” infineon.com Co-development programs between driver and device teams reduce ringing, minimize EMI, and shorten validation cycles. As carmakers and data-center operators migrate to 800 V rails, the gate driver integrated circuit market expands by capturing higher content per module.

Rapid EV On-Board Charger and Traction Inverter Deployment

Automotive platforms moving from 400 V to 800 V battery packs double insulation stress yet promise faster charging. Driver ICs must satisfy ISO 26262 ASIL C or D and AEC-Q100 Grade 0, extending design cycles to five years but creating entry barriers that protect incumbent suppliers. Volkswagen’s supply agreement with onsemi bundles SiC MOSFETs and drivers, illustrating customer demand for turnkey, qualified power stages. Content per vehicle rises as domain controllers, DCDC converters, and traction inverters each require dedicated isolated drivers with integrated de-saturation and soft-off. Automotive qualification premiums offset commodity price pressure and bolster overall gate driver integrated circuit market revenues

Expansion of Photovoltaic and Battery-Based Energy-Storage Inverters

Utility-scale battery storage in Europe rose 94% year-on-year to 17.2 GWh in 2023, with residential units providing the bulk of installations. Three-phase inverters now switch beyond 200 kHz, demanding drivers that can handle rapid bidirectional current flow while retaining reinforced isolation over 20 years. Designers favor devices offering digital telemetry and temperature sensing, which enable predictive maintenance and grid-support functions. As feed-in tariffs tighten, system owners chase incremental efficiency gains; driver ICs that minimize dead-time and reverse-recovery losses unlock 0.3-0.5 percentage-point improvements. These incremental gains translate into meaningful lifetime energy yield, sustaining demand for premium solutions in the gate driver integrated circuit market.

High-Frequency Switching Demand from Hyperscale Data-Centers

AI server racks often exceed 100 kW load, pushing operators toward 48 V distribution to cut copper losses. SiC MOSFET-based DC-DC bricks improve efficiency by 1 percentage point versus silicon alternatives. Yet higher dV/dt and faster slew rates amplify EMI and thermal stress. Driver ICs with programmable gate strength, active Miller clamps, and remote temperature monitors allow power shelves to meet stringent uptime targets. Cloud providers also mandate PMBus or I²C diagnostics for real-time monitoring, which vendors embed directly in the driver die. These requirements help defend pricing and ensure that the gate driver integrated circuit market continues to capture value despite rising silicon content elsewhere in the rack.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal-reliability limits above 1200 V & high dv/dt | -0.8% | Automotive, industrial globally | Medium term (2-4 years) |

| Wide-bandgap substrate supply constraints | -0.6% | Automotive, industrial worldwide | Short term (≤ 2 years) |

| Stringent ISO 26262 & AEC-Q100 compliance costs | -0.4% | North America, Europe, Asia automotive | Long term (≥ 4 years) |

| Multi-channel high-side isolated driver design complexity | -0.3% | Industrial motor drives worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Thermal-Reliability Challenges under Above 1200 V, High dv/dt Operation

Gate drivers in 1200 V traction inverters face temperature swings from -40 °C to 150 °C during harsh duty cycles. Power-cycling studies show accelerated gate-oxide degradation once swings exceed 120 °C, forcing designers to adopt thicker isolation layers and derate switching speed.[3]MDPI, “Review on Power Cycling Reliability of SiC Power Device,” mdpi.com These mitigations add cost and PCB area. In cost-sensitive markets, engineers delay wide-bandgap adoption or cap bus voltage at 800 V. The restraint dampens near-term revenue growth for high-end products in the gate driver integrated circuit market, even though long-term demand remains intact.

Wide-Bandgap Substrate Supply Constraints

SiC wafer yields remain below 50% for automotive-grade material, and only five producers supply more than 90% of global capacity.[4]Evertiq, “Five companies control the SiC power market,” evertiq.com Planned 200 mm ramp-ups will ease cost curves by late 2027, yet interim shortages delay power-device shipments and, by extension, driver IC rollouts. To safeguard supply, leading vendors sign multi-year substrate agreements or invest in captive crystal-growth lines. Smaller driver specialists without vertical integration face allocation risk and longer customer qualification cycles, tempering the headline CAGR of the gate driver integrated circuit market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transistor Type: IGBT Growth Accelerates Despite MOSFET Dominance

MOSFET-based drivers accounted for 61.12% of revenue in 2025 as consumer and low-to-medium-power industrial products favor cost and efficiency at switching frequencies below 200 kHz. However, IGBT-centric designs will register a 7.35% CAGR through 2031 as electric-vehicle traction inverters and heavy-industrial drives demand higher current handling and rugged short-circuit tolerance. The gate driver integrated circuit market benefits because IGBT modules need peak-current drive up to 20 A and configurable soft-shut-off, features that command premium pricing. SiC MOSFET adoption blurs the boundary between MOSFET and IGBT categories, yet each device family preserves distinct gate-drive nuance, ensuring parallel demand streams.

Next-generation traction inverters pair 1200 V SiC MOSFET half-bridges with 20 A isolated drivers offering <35 ns delay skew, while industrial UPS makers still select 1700 V IGBTs driven at 15 A peak. Designers thus maintain dual qualification paths and evaluate total cost rather than strictly device technology. This coexistence keeps both MOSFET and IGBT driver innovation healthy within the gate driver integrated circuit market.

By Isolation Type: Non-Isolated Drivers Gain Despite Isolated Dominance

Isolated solutions retained 69.05% share in 2025 because high-voltage automotive and solar applications mandate reinforced safety barriers. Digital transformer isolation now achieves 8 kV peak ratings and <45 ns propagation delay, narrowing performance gaps to capacitive links. Nonetheless, non-isolated drivers will climb at 9.18% CAGR as system-on-chip and low-voltage motor-control boards integrate isolation elsewhere and prize lower BOM cost.

Cost-optimized brushless-DC appliance controllers exemplify this shift: motor module designers embed system isolation at the power stage and attach non-isolated gate drivers directly to microcontrollers. Such architecture trims PCB layers and shrinks form factor, a decisive edge in high-volume appliances. Consequently, the gate driver integrated circuit market flexes to serve divergent safety philosophies without cannibalizing existing offerings.

By Semiconductor Material: Silicon Carbide Disrupts Silicon Leadership

Silicon maintained 78.15% share in 2025 thanks to low wafer cost and decades-long supply chain maturity. Yet designers of 800 V EV platforms and data-center power shelves value the 50% lower switching losses and higher temperature headroom offered by SiC. Silicon-carbide driver attach rates will grow at 10.92% CAGR, lifting overall gate driver integrated circuit market size for high-value sockets.

The rise of gallium-nitride further stretches driver requirements because e-mode GaN transistors switch at multi-MHz rates and demand accurate negative gate bias control. Cambridge GaN Devices claims gate compatibility with conventional MOSFET controllers, but reference designs still recommend programmable gate-strength drivers for EMI mitigation. Material-agnostic driver platforms that auto-configure gate voltage and dead-time give vendors broad appeal across silicon, SiC, and GaN ecosystems.

By Input Configuration: Multi-Channel Complexity Drives Innovation

Dual-channel drivers captured 53.92% share in 2025 because they cost-effectively manage half-bridge topologies common in motor drives and LLC converters. Multi-channel devices will rise at 5.82% CAGR as power-dense converters integrate six- or twelve-switch interleaved phases that need synchronized gate timing within ±2 ns. The gate driver integrated circuit market rewards suppliers that offer programmable dead-time, on-chip current sense, and I²C configurability.

Industrial servo drives illustrate this migration: integrating all six low-side channels into one reinforced-isolated package removes discrete optocouplers and shrinks cabinet volume. Meanwhile, single-channel drivers remain indispensable for high-voltage stacked topologies that isolate each switch separately. The configuration mix ensures diverse design wins across appliance, automotive, and renewable-energy fields

By Application: Residential Segment Accelerates Through Electrification

Industrial systems represented 41.85% of revenue in 2025, with motor drives, welders, and programmable-logic power supplies accounting for most shipments. Residential demand will outpace at 6.12% CAGR as solar-plus-storage kits and smart appliances adopt high-efficiency BLDC motors. Energy-aware consumers value programmable power stages that trim electricity use by up to 35%, a benefit underpinned by finely tuned gate-drive profiles.

Appliance makers integrate sensor-less control that modulates gate current on the fly, cutting audible noise and prolonging fan life. Inverter air-conditioners employ stacked MOSFET arrays switching at 60 kHz, a regime best served by low-delay, low-jitter drivers. This residential pull invites new entrants while expanding total addressable volume for the gate driver integrated circuit market.

By End-User Industry: Energy and Power Sector Leads Growth

Automotive retained 36.55% share in 2025 because every EV subsystem-from traction inverter to cabin compressor-needs isolated gate drivers that meet strict reliability metrics. Energy and power will climb fastest at 7.12% CAGR as utilities add photovoltaic inverters, grid-forming battery systems, and flexible AC transmission modules.

Policy-driven expansion, such as European Union Fit-for-55 emissions targets, compels utilities to squeeze extra efficiency from hardware. Gate drivers supporting GaN totem-pole topologies help reach >98% conversion efficiency, unlocking substantial lifecycle savings. Consequently, the gate driver integrated circuit market captures new long-tail opportunities across sub-station upgrades and community energy-storage installations.

Geography Analysis

Asia-Pacific remains the core manufacturing and consumption hub for gate-drive solutions. China’s dominance in smart-appliance output and Japan’s high-reliability electronics heritage drive a complex mix of cost-sensitive and premium specifications. Government incentives for energy-efficient products, along with aggressive EV uptake targets, keep design cycles brisk. South Korea and Taiwan provide crucial semiconductor process capacity, allowing regional firms to iterate quickly without global logistics delays. Toshiba’s TPD4165K intelligent power device, which cuts BLDC inverter footprints by 21% while raising voltage capability to 600 V, demonstrates how compact driver-device integration matches regional board-space constraints.

North America and Europe jointly account for a substantial share of high-value, safety-critical applications. Data-center expansions in the United States have pushed rack-level loads beyond 100 kW, requiring isolated drivers with remote telemetry for proactive thermal management. European regulators have updated electric motor efficiency standards effective June 2027, leading OEMs to retrofit motor drives that meet higher benchmark efficiency classes. onsemi’s USD 2 billion SiC investment in the Czech Republic underscores how supply-chain security resonates with European automotive brands looking to localize wide-bandgap sourcing. These factors foster a premium segment of the gate driver integrated circuit market where safety certification and traceability outweigh pure cost.

The Middle East and Africa, though still accounting for a single-digit revenue share, show the most rapid growth. Gulf Cooperation Council countries finance multi-gigawatt solar parks and battery hubs to diversify beyond hydrocarbons. These projects demand megawatt-scale inverters using SiC modules and multi-channel gate drivers that guarantee >25-year operational life. Local technical talent pools remain thin, so suppliers that bundle reference designs and remote diagnostics win early design-ins. Over the forecast horizon through 2031, these initiatives create a durable growth corridor that strengthens the global presence of the gate driver integrated circuit market

Competitive Landscape

The market is moderately concentrated, with the top five suppliers controlling well above half of revenue. STMicroelectronics commands 32.6% share of silicon-carbide power devices, giving it leverage to bundle proprietary EiceDRIVER™ chips into traction inverter reference designs. Infineon holds 14% of automotive semiconductor turnover and augments its gate-drive lineup with the 2025 acquisition of GaN Systems, reinforcing a multi-material portfolio able to span 12 V DC fans to 1500 V solar strings. onsemi’s integration of Qorvo’s SiC JFET business expands its EliteSiC stack and tightens vertical control from substrate to driver IC.

Renesas added GaN expertise by closing the Transphorm purchase, enabling a unified driver-device roadmap that addresses EV chargers, data-center PSUs, and industrial automation rigs. Smaller specialists carve niches in radiation-hard drivers for satellites or ultralow-leakage solutions for medical implants, yet volume remains with diversified conglomerates boasting AEC-Q100 and ISO 26262 labs. Competition centers on platform breadth, safety pre-certification, and embedded telemetry rather than per-unit price. As power-device margins compress, suppliers monetize software-defined features like field-upgradeable gate profiles and cloud-based predictive-maintenance analytics embedded in driver firmware.

Strategic consolidation continues. SkyWater Technology’s takeover of Infineon’s Austin fab in February 2025 opens 65 nm BCD capacity on US soil, which fabless driver startups can tap for secure supply. Infineon’s trademarked solution CoolGaN deal with SounDigital validated audio-amplifier efficiency gains, showcasing how niche application wins translate into broader mindshare. Looking ahead, competitive differentiation will rest on how seamlessly vendors integrate isolation, sensing, and digital communication in packages small enough for compact motor drives yet rugged enough for 1500 V solar combiner boxes.

Gate Driver Integrated Circuit Industry Leaders

-

Infineon Technologies AG

-

NXP Semiconductors

-

Renesas Electronics

-

STMicroelectronics

-

Toshiba Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: SkyWater Technology acquired Infineon’s 200 mm Austin fab, adding high-voltage BCD capacity and long-term supply collaboration.

- February 2025: Infineon unveiled trademarked CoolGaN transistors that helped SounDigital lift Class-D amplifier efficiency by 5% while halving heat-sink volume.

- January 2025: Infineon launched AEC-qualified EiceDRIVER™ ICs with 20 A output for EV traction inverters, featuring integrated self-test for de-saturation events.

- January 2025: FORVIA HELLA chose Infineon’s 1200 V CoolSiC™ MOSFETs with top-side cooling for 800 V DC-DC converters.

- January 2025: onsemi closed a USD 115 million deal to acquire Qorvo’s SiC JFET assets, broadening its AI data-center power portfolio

Global Gate Driver Integrated Circuit Market Report Scope

A gate driver is a power amplifier that carries low power input from a controller IC and produces a power device's suitable increased current gate drive. It is used when a PWM controller cannot deliver the output current needed to drive the gate capacitance of the associated power device. The Gate Driver Integrated Circuit Market is segmented by Transistor Types such as MOSFET and IGBT among various Commercial, Industrial, and Residential Applications.

The studied market is further segmented into different End-user Industries such as Automotive, Consumer Electronics, Energy & Power among multiple geographies. The impact of COVID-19 on the market and impacted segments are also covered under the scope of the study. Further, the disruption of the factors affecting the market's expansion in the near future has been covered in the study regarding drivers and restraints.

Gate Driver Integrated Circuit Market is segmented by transistor type (MOSFET, IGBT), by application (commercial, industrial, residential), by end-user industries (automotive, consumer electronics, energy & power), by geography (North America, Europe, Asia Pacific, Middle East Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| MOSFET |

| IGBT |

| Isolated Gate Driver ICs |

| Non-Isolated Gate Driver ICs |

| Silicon (Si) |

| Silicon Carbide (SiC) |

| Gallium Nitride (GaN) |

| Single-Channel |

| Dual-Channel |

| Multi-Channel |

| Commercial |

| Industrial |

| Residential |

| Automotive |

| Consumer Electronics |

| Energy and Power |

| Healthcare |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Transistor Type | MOSFET | ||

| IGBT | |||

| By Isolation Type | Isolated Gate Driver ICs | ||

| Non-Isolated Gate Driver ICs | |||

| By Semiconductor Material | Silicon (Si) | ||

| Silicon Carbide (SiC) | |||

| Gallium Nitride (GaN) | |||

| By Input Configuration | Single-Channel | ||

| Dual-Channel | |||

| Multi-Channel | |||

| By Application | Commercial | ||

| Industrial | |||

| Residential | |||

| By End-User Industry | Automotive | ||

| Consumer Electronics | |||

| Energy and Power | |||

| Healthcare | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the gate driver integrated circuit market?

The gate driver integrated circuit market is valued at USD 1.87 billion in 2026 and is forecast to reach USD 2.36 billion by 2031.

Which region leads the market today?

Asia-Pacific commands 48.05% of global revenue in 2025 due to its strong appliance manufacturing base and automotive electronics capabilities.

Which segment is expanding the fastest?

Silicon-carbide driver attach rates post the quickest growth, with the material segment projected to advance at an 10.92% CAGR between 2026 and 2031.

How are electric vehicles influencing demand?

EV traction inverters and onboard chargers require ISO 26262-qualified, high-current isolated drivers, lifting automotive share to 36.55% of 2025 revenue and supporting premium pricing.

What are the main challenges facing suppliers?

Thermal-reliability at >1200 V operation and limited SiC wafer supply constrain near-term growth and raise qualification costs for new entrants.

Which companies hold the largest shares?

STMicroelectronics leads silicon-carbide power devices with 32.6% share, while Infineon captures 14% of automotive semiconductor revenue through its diversified portfolio.

Page last updated on: