Hydroponics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

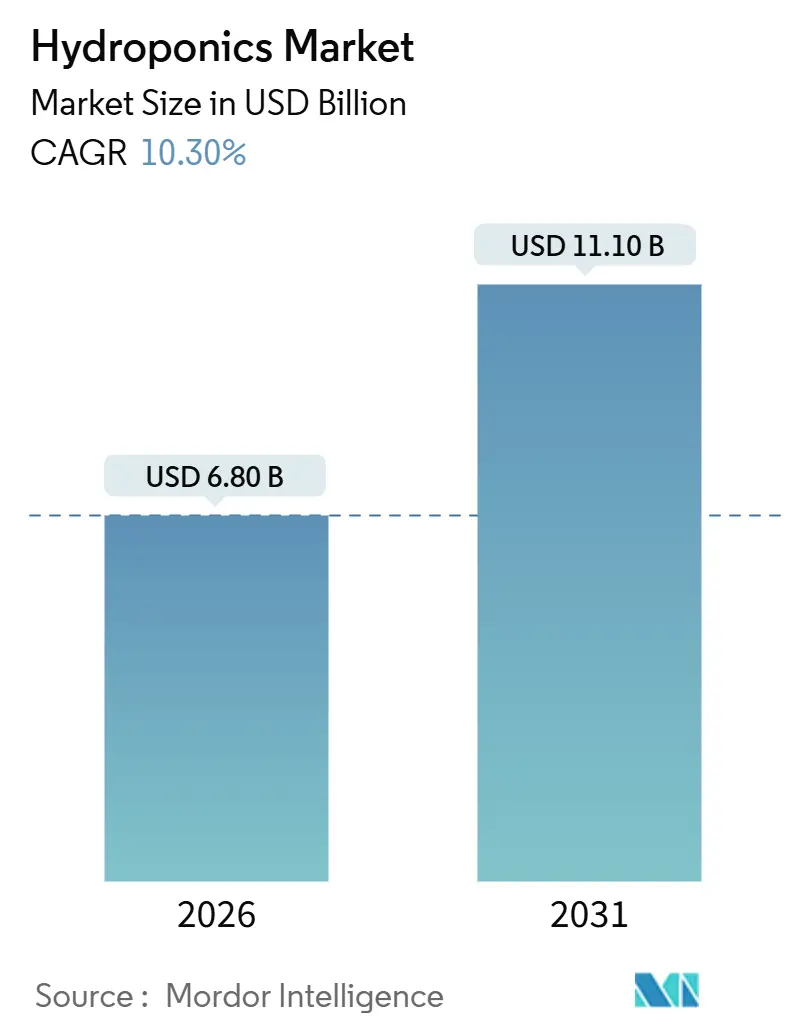

| Market Size (2026) | USD 6.80 Billion |

| Market Size (2031) | USD 11.10 Billion |

| Growth Rate (2026 - 2031) | 10.30% CAGR |

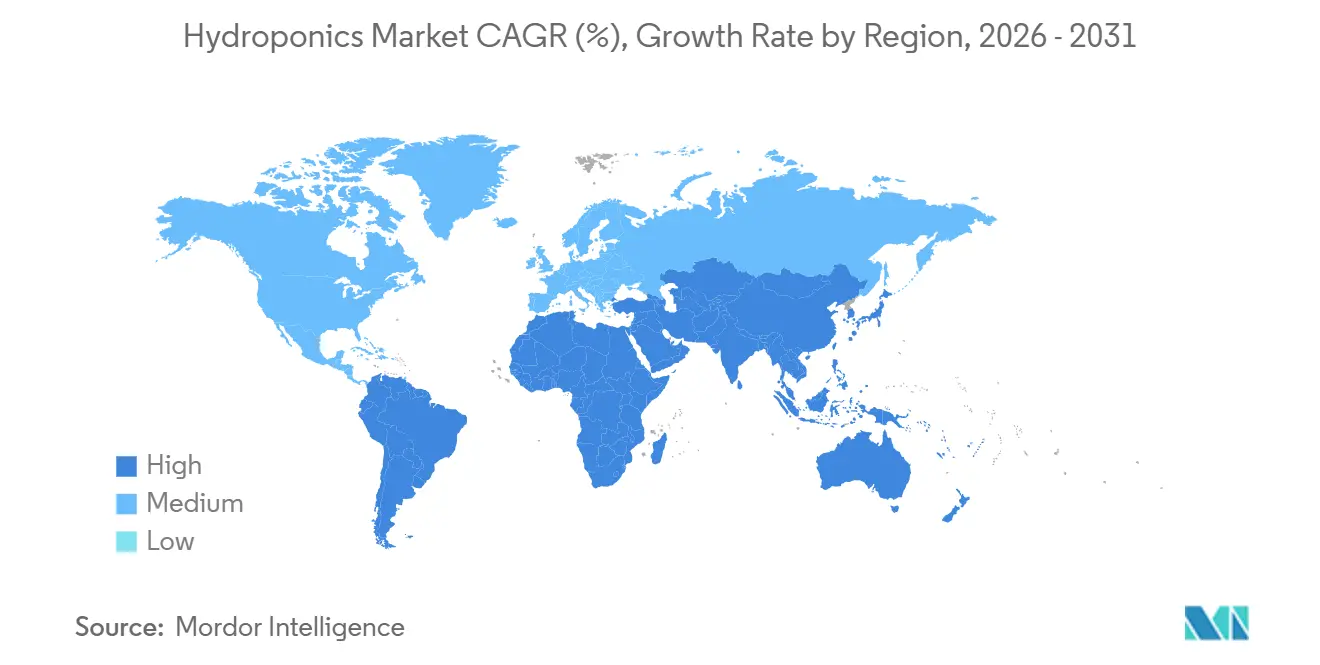

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydroponics Market Analysis by Mordor Intelligence

The hydroponics market size is estimated to be USD 6.80 billion in 2026 and is projected to reach USD 11.10 billion by 2031, supported by a 10.30% CAGR through the forecast period. Structural pressure on land availability, climate volatility, and rising water costs underpin demand as growers pivot from soil cultivation to closed-loop systems. While the greenhouse hydroponics dominate value creation, the indoor vertical farms segment is accelerating in response to an urban food security agenda that prioritizes year-round supply and short delivery radii. Government research grants, notably the United States Department of Agriculture (USDA) program, which allocates USD 10 million annually to controlled-environment studies, position hydroponic technologies as a mainstream food-security lever rather than an experimental niche[1]Source: U.S. Department of Agriculture National Institute of Food and Agriculture, “7 USC 5925g – Specialty Crop Research Initiative,” NIFA.usda.gov. Retailers prefer pesticide-free produce that meets strict traceability standards, thereby bolstering the adoption of leafy greens while biopharma buyers pull herbs into a higher-margin trajectory. Competitive fragmentation persists because automation specialists and lighting innovators can still enter at different points in the value chain, even as larger operators expand their footprints to secure purchasing power. Carbon-credit monetization for low-emission produce adds a parallel revenue stream for growers who invest in renewable energy, creating additional momentum behind the technology.

Key Report Takeaways

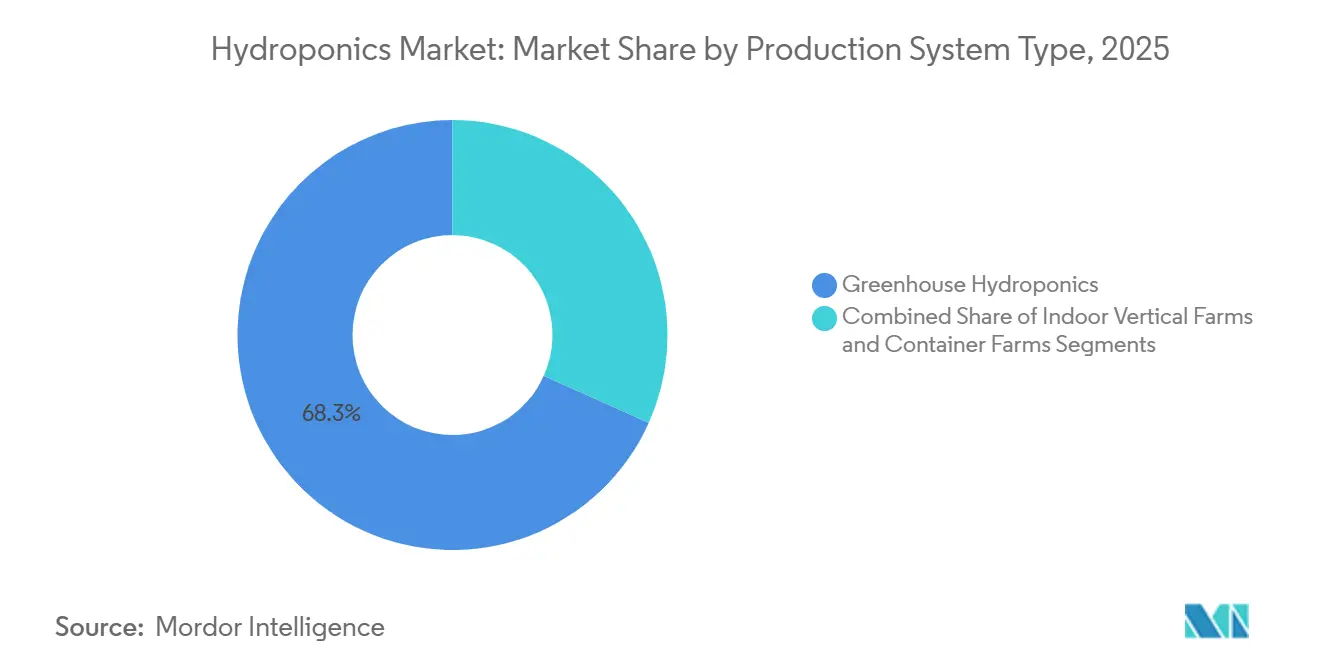

- By production system type, greenhouse hydroponics led with 68.3% of the hydroponics market size in 2025, while indoor vertical farms are forecast to expand at a 13.4% CAGR through 2031.

- By crop type, leafy greens captured 47.2% of value in 2025, and herbs and microgreens are projected to advance at a 12.6% CAGR to 2031.

- By production scale, large commercial operations held 55.8% of the hydroponics market share in 2025, whereas small systems are projected to grow at a 13.3% CAGR between 2026 and 2031.

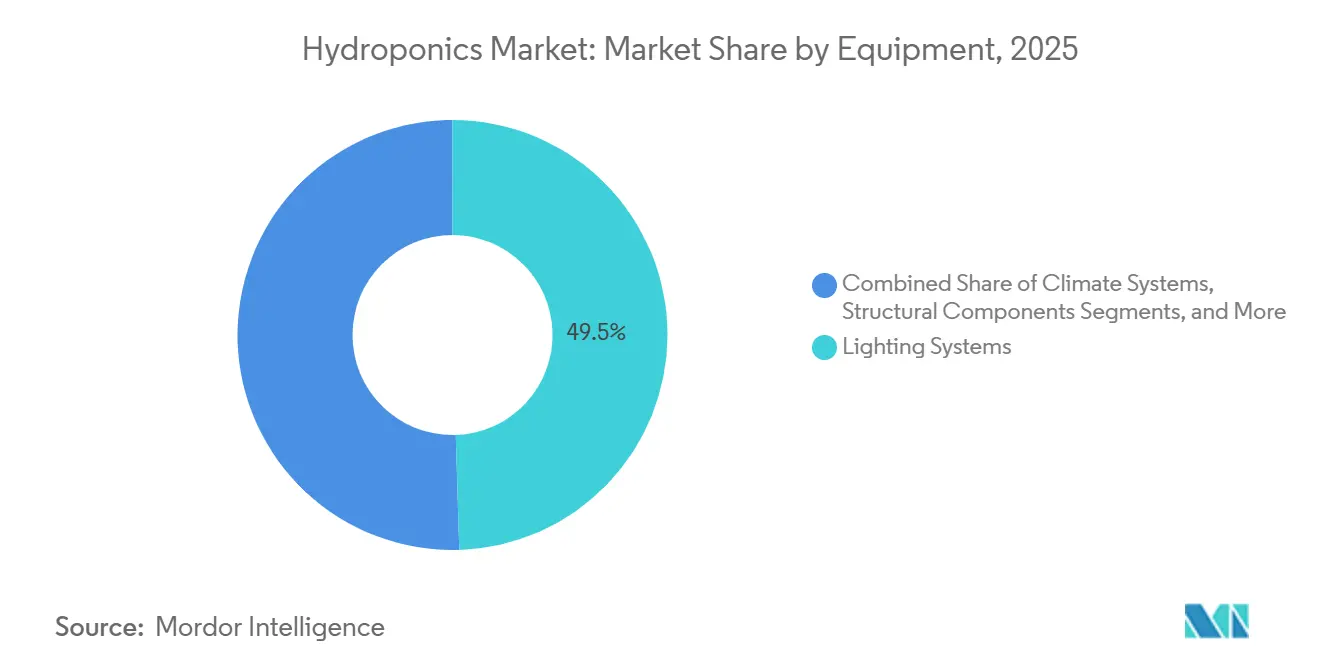

- By equipment, lighting systems accounted for 49.5% of the hydroponics market in 2025, with climate systems projected to register a 12.8% CAGR through 2031.

- By geography, Europe accounted for 34.3% of the 2025 hydroponics market revenue, while the Asia-Pacific region is positioned for the fastest regional expansion at a 12.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hydroponics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Controlled-environment food-security initiatives | +2.1% | Asia-Pacific, Middle East, and North America | Medium term (2-4 years) |

| Declining arable land per capita | +1.8% | Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Year-round output advantages | +1.6% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Carbon-credit revenue stacking | +0.9% | Europe, North America, emerging Asia-Pacific | Long term (≥ 4 years) |

| Pharmaceutical-grade ingredient demand | +0.7% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Urban wastewater-reuse regulations | +0.6% | Europe, Middle East, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Controlled-Environment Food-Security Initiatives

National programs now position hydroponics within critical-infrastructure strategies that mitigate climate shocks. The United States Department of Agriculture (USDA) funds urban and indoor agriculture under 7 USC 5925g, turning research grants into pilot facilities that demonstrate commercial viability. Japan’s Ministry of Agriculture, Forestry and Fisheries (MAFF) targets 50% smart-agriculture adoption by 2030, prioritizing controlled environments that stabilize output during typhoon seasons. China’s National Smart Agriculture Action Plan mandates the use of the Internet of Things (IoT) and artificial intelligence in facility agriculture pilots, thereby accelerating domestic investment in this sector[2]Source: Ministry of Agriculture and Rural Affairs, “National Smart Agriculture Action Plan,” Moa.gov.cn. India’s Digital Agriculture Mission earmarked Rs 2,817 crore (USD 338 million) for precision-farming infrastructure, while the Clean Plant Programme channels Rs 1,765.67 crore (USD 212 million) into disease-free nursery material[3]Source: Ministry of Agriculture and Farmers Welfare, “Digital Agriculture Mission,” Agricoop.nic.in. These policies compress financing costs and standardize regulatory pathways, speeding adoption among commercial growers who once viewed hydroponics as capital-prohibitive.

Declining Arable Land per Capita

Land scarcity intensifies the economic rationale for soilless cultivation. The Food and Agriculture Organization (FAO) recorded a 20% drop in global arable land per person, from 0.24 to 0.20 hectares between 2000 and 2024. Urban sprawl in the Asia-Pacific and water constraints in the Middle East leave limited expansion room for soil farming. Hydroponics multiplies usable growing area up to 80 times by stacking production vertically or fitting systems onto non-arable sites, such as rooftops and warehouses. The Netherlands utilizes greenhouse clusters to export high-yield vegetables, despite having scarce farmland, illustrating the potential leverage when land is no longer the limiting factor. As per-capita arable acreage becomes increasingly scarce, the cost-benefit of vertical infrastructure outweighs land acquisition, especially near high-density cities.

Year-Round Output Advantages

Reliability attracts retailers seeking a consistent supply on the shelf. Village Farms International Inc. ships tomatoes and cucumbers year-round from its greenhouses in Texas and Canada, operating under multi-year contracts that buffer the supply chain against weather-related shortages. Plenty Unlimited Inc. signed a deal with 7-Eleven to serve 1,300 stores in 2024, utilizing indoor farms to mitigate seasonal variability. Controlled environments cut crop loss from frost, drought, and pests, with programmable lighting and nutrient delivery, and trim harvest cycles to as few as 30 days for leafy greens. Retailers thus prefer hydroponic suppliers for predictable volume, which in turn supports premium pricing and long-term demand.

Pharmaceutical-Grade Ingredient Demand

Biopharmaceutical firms value contaminant-free biomass for the extraction of recombinant proteins and nutraceuticals. Peer-reviewed work in Public Library of Science (PLOS) Biology validates plant molecular farming as a significant biomanufacturing pillar that relies on sterile, tightly controlled facilities. AeroFarms Inc. operates an AgX site focused on speed breeding and phytochemical production in indoor environments, highlighting how high-margin pharmaceutical contracts justify vertical-farm capital expenditures. Health Canada’s 2024 guidance officially frames hydroponics as a containment strategy that prevents gene flow, positioning the segment as a supplier to vaccine and antibody pipelines. Premium pricing, often 10-50 times the value of food-grade products, offsets operating expenses and insulates margins from fluctuations in fresh-produce prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for large systems | −1.4% | Global, strongest in emerging markets | Short term (≤ 2 years) |

| Energy-cost sensitivity for artificial lighting | −1.1% | Global, acute in Europe and Middle East | Short term (≤ 2 years) |

| Tightening micronutrient-discharge regulations | −0.6% | North America, Europe, and Middle East urban centers | Medium term (2-4 years) |

| Limited seed genetics for hydroponic inputs | −0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Large Systems

Turnkey vertical farming systems can exceed USD 1,000 per square meter, often extending payback periods beyond seven years for smaller investors. While several large-scale operators historically relied on substantial venture funding to finance automated facilities, capital intensity has proven challenging for highly leveraged expansion strategies, as evidenced by the Chapter 11 filing of Kalera PLC. Village Farms International Inc. opted to privatize its fresh-produce unit for USD 40 million and a 37.9% equity stake in 2025, illustrating structural pressure to streamline its balance sheet. To mitigate upfront investment risk, smaller growers are increasingly favoring modular or leased cultivation formats that shift capital expenditures toward operating expenses, thereby improving flexibility and reducing financial exposure.

Energy-Cost Sensitivity for Artificial Lighting

Indoor farms using light-emitting diode (LED) arrays face volatile power prices that can exceed the revenue from producing at USD 12 cents per kilowatt-hour. The United States Energy Information Administration (EIA) pegs industrial averages at USD 7.5 cents, but California and the Northeast run higher, thereby shrinking margins[4]Source: United States Energy Information Administration, “Electric Power Monthly,” EIA.gov. Signify’s 2023 GreenPower LED Toplighting Compact 2.0 boosts photosynthetic-photon efficiency, cutting kilowatt-hours per kilogram, yet adoption demands capital outlays that squeeze smaller operators. Middle-Eastern utilities impose higher industrial tariffs, so joint ventures such as Plenty Unlimited Inc. and Mawarid include on-site solar generation to stabilize cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production System Type: Vertical Farms Capture Urban Density Premium

Greenhouse hydroponics generated 68.3% of 2025 revenue, supported by the 5.5 million-square-foot Village Farms International Inc. complex in Texas and extensive Dutch clusters that combine sunlight with waste-heat capture. Indoor vertical farms are projected to grow at a 13.4% CAGR through 2031, as municipalities pursue resilient last-mile supply chains while minimizing refrigerated freight. Container-based hydroponic systems, although representing a niche market, continue to address remote and decentralized demand through modular, rapidly deployable units suited for institutional, research, and emergency-response settings.

Automation compresses labor costs, narrowing the historical cost gap between vertical structures and greenhouses. Signify’s newest LEDs reduce energy draw, making high-rise grow towers more viable in power-intensive regions. Plenty Unlimited Inc.’s USD 680 million joint venture with Mawarid signals that Middle Eastern capital is gravitating toward vertical platforms where conventional greenhouse cooling is cost-prohibitive. As lighting and robotics mature, the hydroponics market will shift further toward multi-tier formats that capitalize on scarce urban land.

By Crop Type: Herbs Surge on Biopharma Contracts

Leafy greens accounted for 47.2% of the hydroponics market size in 2025, driven by 30-45 day harvest cycles that maximize turns and cash flow for hydroponic growers. Herbs and microgreens are anticipated to post a 12.6% CAGR through 2031, as pharmaceutical and nutraceutical buyers demand pesticide-free biomass with traceable phytochemical profiles. Tomatoes, cucumbers, and peppers collectively form the second-largest value block, utilizing high-wire greenhouse systems to produce year-round volumes in line with supermarket contracts.

Pharmaceutical uptake redefines revenue potential. AeroFarms Inc. partners with drug developers to produce specialty extracts, illustrating how growers can pivot from commodity produce to active-ingredient supply. Leaf-crop dominance will continue near large consumer bases because rapid cycles offset operating expenses, yet the margin upside in high-value herbs acts as a buffer against energy volatility. Over time, carbon-pricing schemes that reward lower water and energy footprints may further shift production toward crops with superior efficiency metrics.

By Production Scale: Small Urban Installations Disrupt Last-Mile Logistics

Large facilities captured 55.8% of the hydroponics market share in 2025, driven by increasing purchasing power for energy and nutrients, as well as multi-year contracts with national retailers. Small sites are expanding at a 13.3% CAGR as container farms and rooftop greenhouses cut delivery miles and cold-chain loss, meeting city sustainability mandates. Medium-scale operators serve regional grocery networks but feel margin pressure from both larger rivals and premium urban boutiques.

BrightFarms (Cox Enterprises) opened a greenhouse in Yorkville in December 2024, marking the first of three planned hubs. This initiative showcases the utilization of large-scale facilities for decentralized hydroponics production, while maintaining economies of scale and integrating with national retail networks. Medium-scale urban hydroponics models, such as those managed by Gotham Greens, utilize rooftop spaces to overcome land constraints. These facilities supply regional grocery partners within hours of harvest, ensuring product freshness. At the small-scale level, modular and turnkey container-based hydroponic systems are increasingly adopted by restaurants, educational institutions, and community operators, enabling hyper-local sourcing without the capital burden of purpose-built facilities.

By Equipment: Lighting Dominates While Climate Control Accelerates

Lighting systems accounted for 49.5% of the hydroponics market in 2025, confirming that light-emitting diode arrays remain the largest single purchase for growers. Signify’s GreenPower LED Toplighting Compact 2.0 enhances photosynthetic-photon efficiency, enabling hydroponics farm operators to reduce kilowatt-hour usage per kilogram of produce and protect margins from power price fluctuations. Hydroponics greenhouse producers utilize hybrid lighting to supplement sunlight during low-radiance hours, while indoor vertical farms rely on full-spectrum fixtures to achieve consistent yields, albeit at higher costs. Structural frames, irrigation components, and pumps follow in spending but have longer replacement cycles than lamps and drivers, keeping lighting the top budget priority across hydroponics production models.

Climate systems remain the fastest-growing, projected to grow at a 12.8% CAGR from 2026 to 2031, as operators adopt advanced heating, ventilation, and cooling systems to stabilize growing conditions in their grow rooms. Modern systems integrate temperature, humidity, and carbon dioxide management with lighting schedules, boosting biomass output without requiring additional floor space. Container farms and rooftop greenhouses install modular chillers and heat-recovery ventilators to meet urban energy codes, while large sites retrofit sensor networks to comply with stricter nutrient-discharge rules. As renewable energy and water-recirculation mandates increase, growers invest in intelligent climate platforms that synchronize pumps, fans, and dosing valves, optimizing controlled-environment facilities.

Geography Analysis

Europe accounted for 34.3% of the hydroponics market revenue in 2025, driven by Dutch greenhouse exports and stringent European Union (EU) discharge regulations that have spurred innovations in water reuse. While regional growth is evident, it's tempered by already high capacities and rising electricity costs. Instead of expanding acreage, Germany, the United Kingdom, France, and Spain focus on retrofitting with LEDs and automating processes to enhance efficiency. Russia faces technological access challenges, whereas Scandinavian nations experiment with carbon-neutral greenhouses, harnessing geothermal and hydropower.

Asia-Pacific is set to lead with a 12.2% CAGR, outpacing other major regions. China's "Smart Agriculture Action Plan" for November 2024 allocates state funds to IoT-driven controlled environments, with a particular focus on hydroponics. India’s Digital Agriculture Mission has allocated Rs 2,817 crore (approximately USD 338 million) to precision and controlled-environment systems, fostering the adoption of hydroponics to enhance water efficiency and yield stability. Japan aims for a 50% adoption rate of smart agriculture by 2030, with a focus on hydroponics for typhoon-resilient and climate-controlled production. In Australia, hydroponic greenhouse sites are being expanded near coastal cities to ensure a steady supply of fresh produce to urban areas. Meanwhile, Southeast Asian urban centers are experimenting with vertical hydroponics to reduce their dependence on imported produce.

In North America, the market growth is driven by funding from the United States Department of Agriculture, as well as investments from companies such as Village Farms International Inc. and Plenty Unlimited Inc., which are advancing large-scale, controlled-environment farming. In the Middle East, countries such as the United Arab Emirates and Saudi Arabia are investing in hydroponic systems to reduce import costs and conserve groundwater, as demonstrated by Abu Dhabi’s 10-hectare AgTech Park initiative. In South America, urban hydroponic projects in Brazil and Argentina are driving progress. Meanwhile, in Africa, targeted deployments in South Africa and Kenya are leveraging hydroponics to address post-harvest losses, despite challenges related to power grid reliability.

Competitive Landscape

The hydroponics market remains fragmented, allowing regional specialists and niche operators to thrive alongside larger players. Village Farms International Inc. leverages its 5.5 million-square-foot greenhouse footprint to lock in high-volume contracts across North America and Europe. Plenty Unlimited Inc. raised its profile through a USD 680 million partnership with Mawarid to build vertical farms across the Middle East. Gotham Greens Inc. and BrightFarms emphasize proximity production and automation to capture freshness premiums while trimming labor overhead.

Strategies in the hydroponics market primarily focus on three areas, including achieving cost leadership through scaled, controlled-environment systems, leveraging urban proximity with water-efficient hydroponic setups, and specializing in high-value crops through precise nutrient control. AeroFarms Inc. exemplifies the third strategy by utilizing hydroponic precision to produce pharmaceutical-grade biomass, adopting an R&D-driven model that positions the company upstream of traditional commodity produce. Equipment providers like Signify are addressing niche opportunities, focusing on the increasing efficiency of hydroponics-specific LED technology. Additionally, stricter regulations on nutrient discharge and carbon reporting are driving the adoption of closed-loop hydroponic systems. This trend is accelerating the integration of IoT sensors, AI-driven climate control, and recirculating water treatment technologies, while simultaneously increasing entry barriers for new players.

In the current hydroponics market, technology adoption has become a fundamental requirement rather than a competitive advantage. Operators failing to meet increasing standards for efficiency, traceability, and regulatory compliance risk losing retailer contracts. Meanwhile, well-capitalized companies are consolidating hydroponic capacity through mergers, joint ventures, and privatization efforts. This trend is exemplified by Village Farms International Inc.’s restructuring plans for 2025, which reflect the ongoing consolidation within the industry.

Hydroponics Industry Leaders

Gotham Greens

BrightFarms (COX Enterprises, Inc)

Village Farms International Inc.

AeroFarms Inc.

Plenty Unlimited Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: City officials in Hartford, Connecticut, United States, approved a special permit for Levo International's hydroponic urban farm. This approval enables the development of year-round greenhouses, hydroponics education programs, and projected annual production of over 23.0 metric tons.

- August 2025: Sun Capital acquired GrowUp Farms in the United Kingdom, indicating financial restructuring and potential growth in its hydroponic lettuce and salad leaf production capacity. This acquisition is anticipated to provide GrowUp Farms with the necessary resources to enhance its operational efficiency and expand its market presence.

- January 2025: Aerospring Hydroponics initiated its second commercial hydroponic farming pilot project at Themar Al Emarat in Sharjah, United Arab Emirates. The project focuses on vertical aeroponic systems, designed to increase yield per square meter by approximately 400% while significantly reducing water usage. This initiative aims to enhance regional food security and promote scalable, sustainable production.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hydroponics market as the sale of inputs, systems, and produce revenue generated when plants are grown without soil, instead receiving mineral-rich nutrient solutions in inert media or circulating water.

Production carried out in aquaponic, soil-based greenhouse, or traditional open-field environments is not included.

Segmentation Overview

- By Production System

- Greenhouse Hydroponics

- Indoor Vertical Farms

- Container Farms

- By Crop Type

- Leafy Greens

- Tomatoes

- Cucumbers

- Peppers

- Herbs and Microgreens

- By Equipment

- Lighting Systems

- Irrigation Components and Pumps

- Climate Systems

- Automation and Control Systems

- Structural Components

- By Production Scale

- Large

- Medium

- Small

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- Netherlands

- United Kingdom

- France

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed commercial growers across the United States, the Netherlands, Japan, and the UAE, alongside equipment integrators and input formulators. The conversations clarified installed acreage, typical yield-per-square-meter, current average selling prices (ASP) for tomatoes and leafy greens, and payback expectations, allowing us to adjust model drivers that were only partially visible in public data.

Desk Research

We built the first layer of evidence from openly accessible authorities such as FAO crop yield series, USDA-ERS vegetable price files, Eurostat structural greenhouse data, UN Comtrade shipment codes for substrate and nutrient salts, and white papers issued by the International Greenhouse Vegetable Production Association. Company 10-Ks, investor decks, and mainstream business press add detail on system costs and capacity announcements, while D&B Hoovers and Factiva supply hard-to-find financial line items that anchor producer revenue. These references illustrate the mix of statistical, trade, and corporate signals we screened; many other secondary sources were consulted during data validation.

Market-Sizing & Forecasting

A top-down "cultivated area × average yield × ASP" reconstruction pulls 2024 greenhouse floor space and adoption ratios from national statistics, which are then checked against sampled distributor shipment volumes; our sole bottom-up touchpoint. Key variables in the model include substrate replacement cycles, water-use reduction premiums, energy-price pass-through, average LED intensity per square meter, and seasonality of retail tomato prices. We employ multivariate regression to project each driver through 2030, and scenario analytics stress-test water-scarcity shocks before publishing the midpoint outlook.

Data Validation & Update Cycle

Outputs pass three gates: automated variance scans against prior editions, peer review by a senior analyst, and, when deviations exceed set thresholds, rapid re-contacts with primary respondents. Reports refresh annually, while material events, policy shifts, or technology cost breaks trigger interim revisions, ensuring buyers always access the most current baseline.

Why Mordor's Hydroponics Baseline Commands Reliability

Published figures often differ because firms select dissimilar crop mixes, monetize equipment separately, or lock exchange rates at outdated levels. According to Mordor Intelligence, careful alignment of scope, live currency conversion, and annual refresh cadence minimizes such drift.

Key gap drivers versus other studies center on whether hardware revenue is bundled, the breadth of crop basket beyond tomatoes and lettuce, and how producer-level ASP escalation is treated.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.95 B (2025) | Mordor Intelligence | - |

| USD 5.20 B (2023) | Global Consultancy A | Older base year and excludes hydroponic equipment revenue |

| USD 5.00 B (2023) | Industry Journal B | Uses static ASPs and limits scope to vegetables grown under glass |

Taken together, the comparison shows that Mordor's disciplined variable selection and annual data refresh deliver a balanced, transparent baseline that decision-makers can retrace and replicate with confidence.

Key Questions Answered in the Report

How large is the hydroponics market in 2026?

The hydroponics market size is USD 6.80 billion in 2026 and is set to hit USD 11.10 billion by 2031 on a 10.30% CAGR.

Which production system leads revenue?

Greenhouse hydroponics contributes 68.3% of 2025 global sales, though indoor vertical farms are growing faster at a 13.4% CAGR.

Why are herbs and microgreens the fastest-growing crop group?

Pharmaceutical and nutraceutical companies pay premiums for traceable, contaminant-free herbs and microgreens, fueling a 12.6% CAGR to 2031.

Which region will grow the fastest through 2031?

Asia-Pacific leads with a 12.2% CAGR, driven by state investment in smart-agriculture programs across China, India, and Japan.

Page last updated on: