Hydraulic Workover Unit Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 10.15 Billion |

| Market Size (2030) | USD 13.09 Billion |

| Growth Rate (2025 - 2030) | 5.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

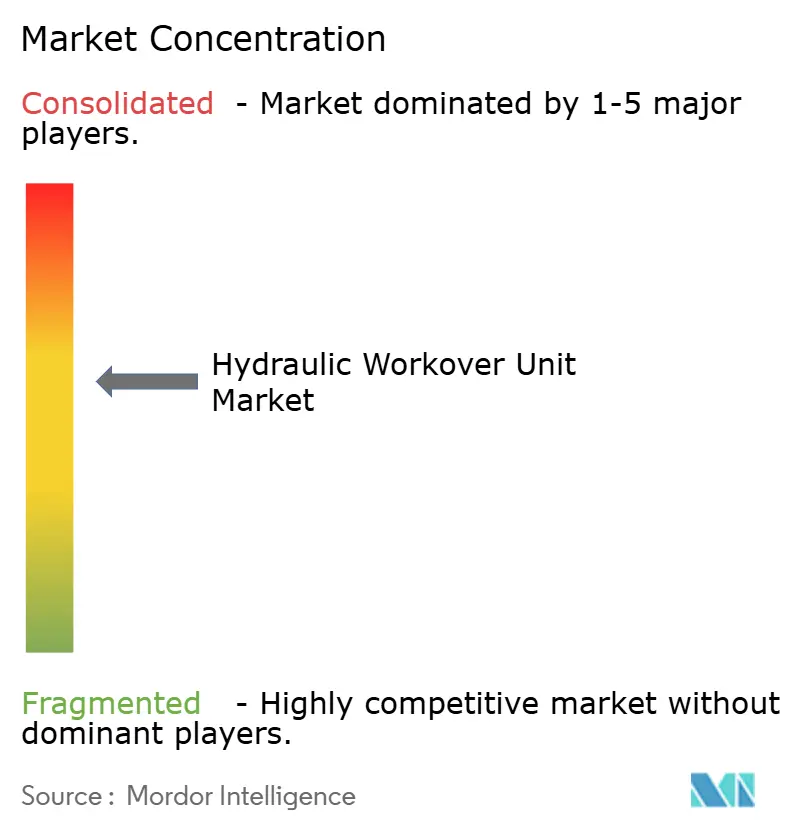

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydraulic Workover Unit Market Analysis by Mordor Intelligence

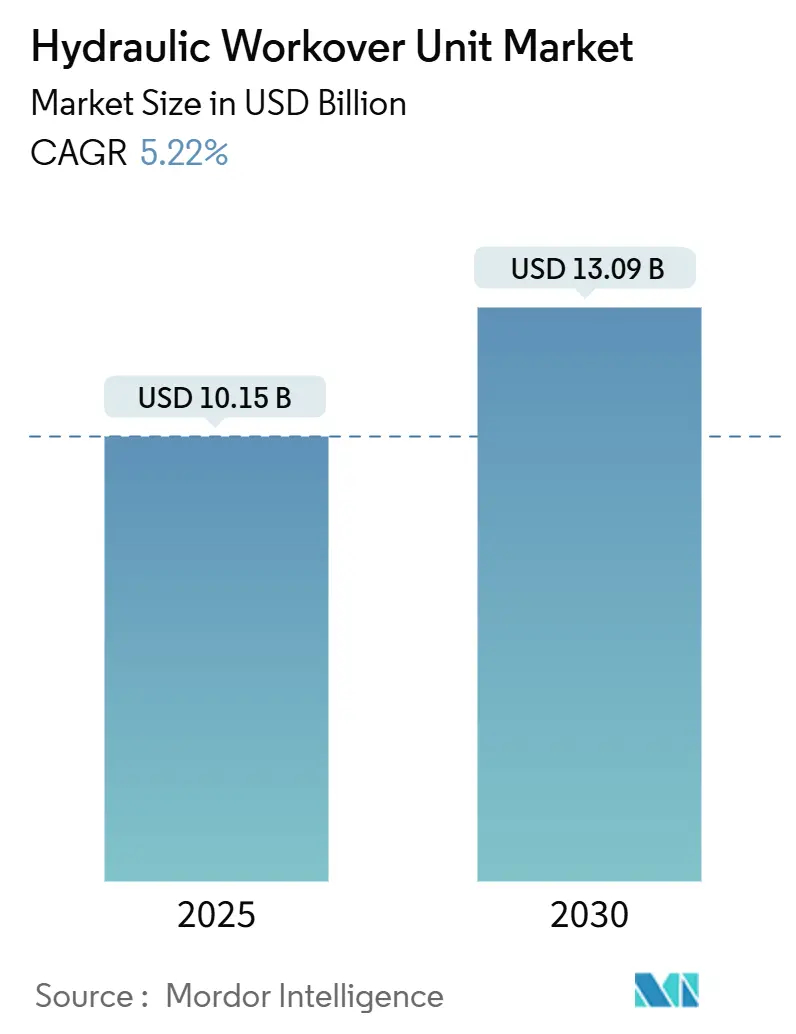

The Hydraulic Workover Unit Market size is estimated at USD 10.15 billion in 2025, and is expected to reach USD 13.09 billion by 2030, at a CAGR of 5.22% during the forecast period (2025-2030).

Robust demand for live-well interventions, operators’ need to lift production from aging reservoirs, and the compelling economics of hydraulic workovers over jack-up rigs underpin this growth trajectory. Lower mobilization costs, smaller crew requirements, and the ability to avoid kill-fluid damage keep workover economics attractive even in volatile price environments. Competitive differentiation is shifting toward digital control systems that mitigate crew shortages and enhance operational safety, while corporate consolidation delivers broader service portfolios and regional scale advantages. Asia-Pacific’s offshore modernization drive, MENA’s mature-field activity, and European life-extension projects collectively supply a steady pipeline of intervention candidates, sustaining a healthy utilization outlook for suppliers in the hydraulic workover unit market.

Key Report Takeaways

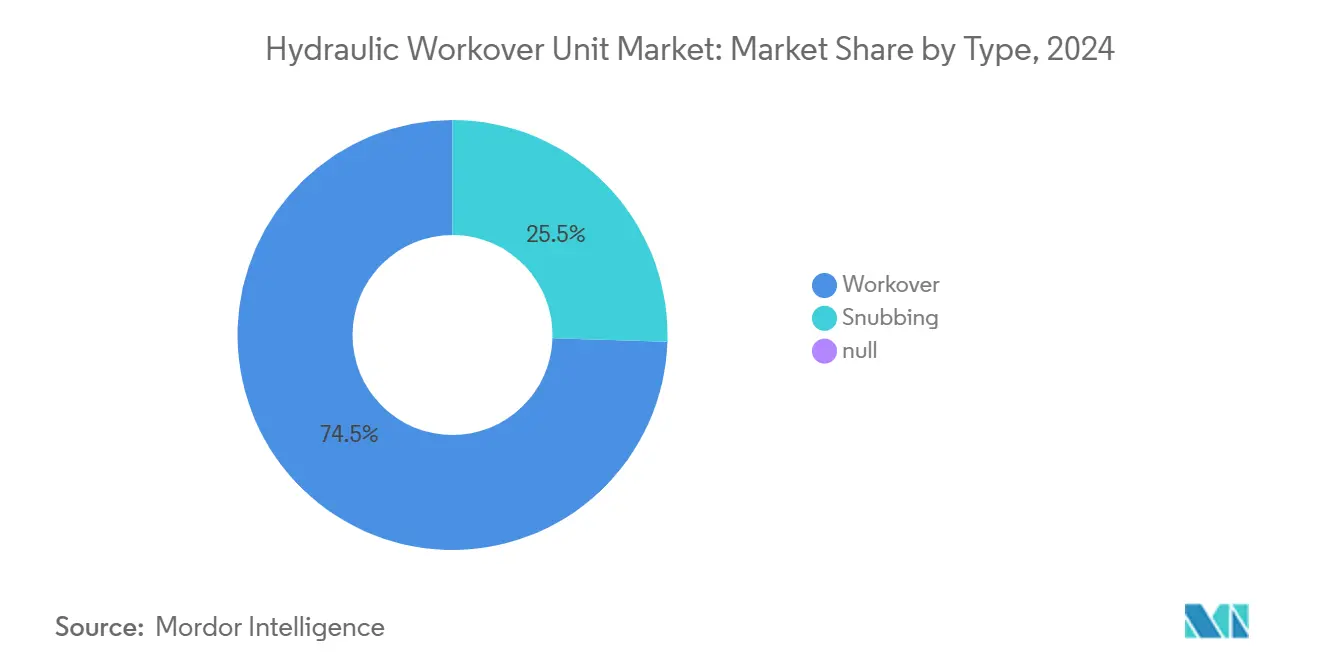

- By type, workover units held 74.5% of the hydraulic workover unit market share in 2024, whereas snubbing units are projected to advance at a 6.4% CAGR through 2030.

- By installation, skid-mounted systems captured 58.3% of the hydraulic workover unit market size in 2024; trailer-mounted units record the highest forecast CAGR at 5.7% to 2030.

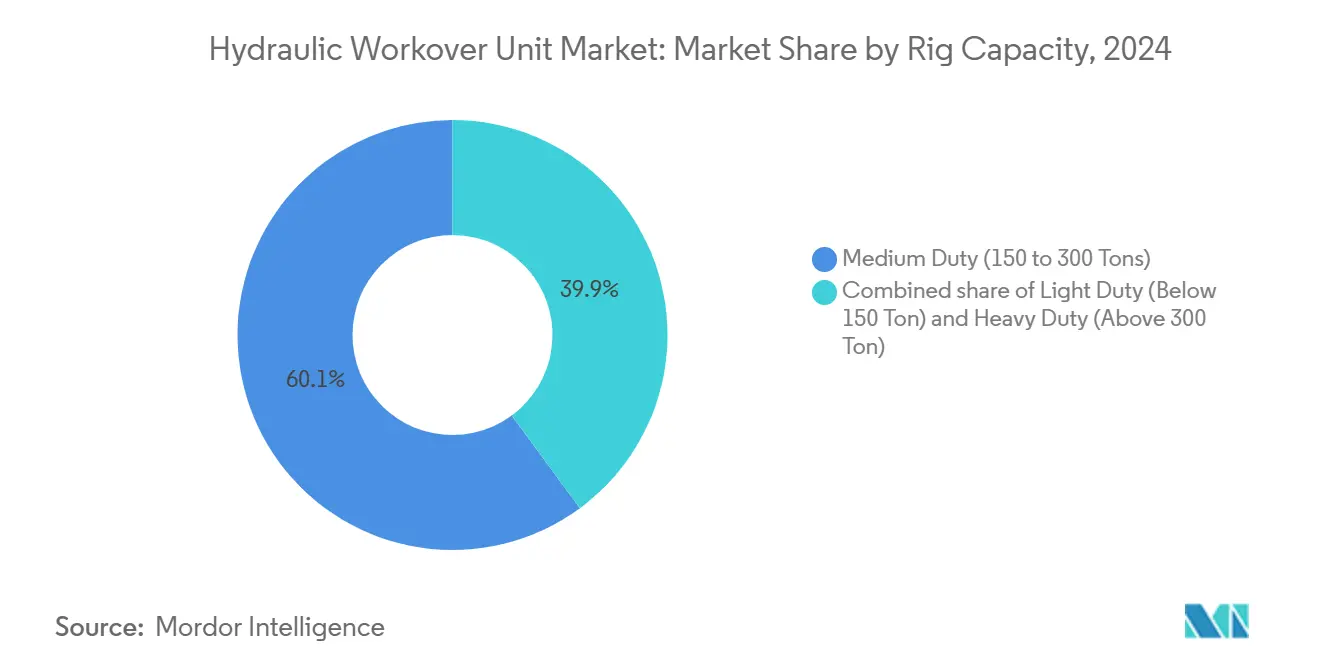

- By rig capacity, medium-duty units accounted for 60.1% of the hydraulic workover unit market size in 2024, while heavy-duty units are expected to register a 5.9% CAGR through 2030.

- By well status, dead-well operations represented 73.8% of 2024 revenues; live-well work is expanding at the fastest rate, with a 5.4% CAGR to 2030.

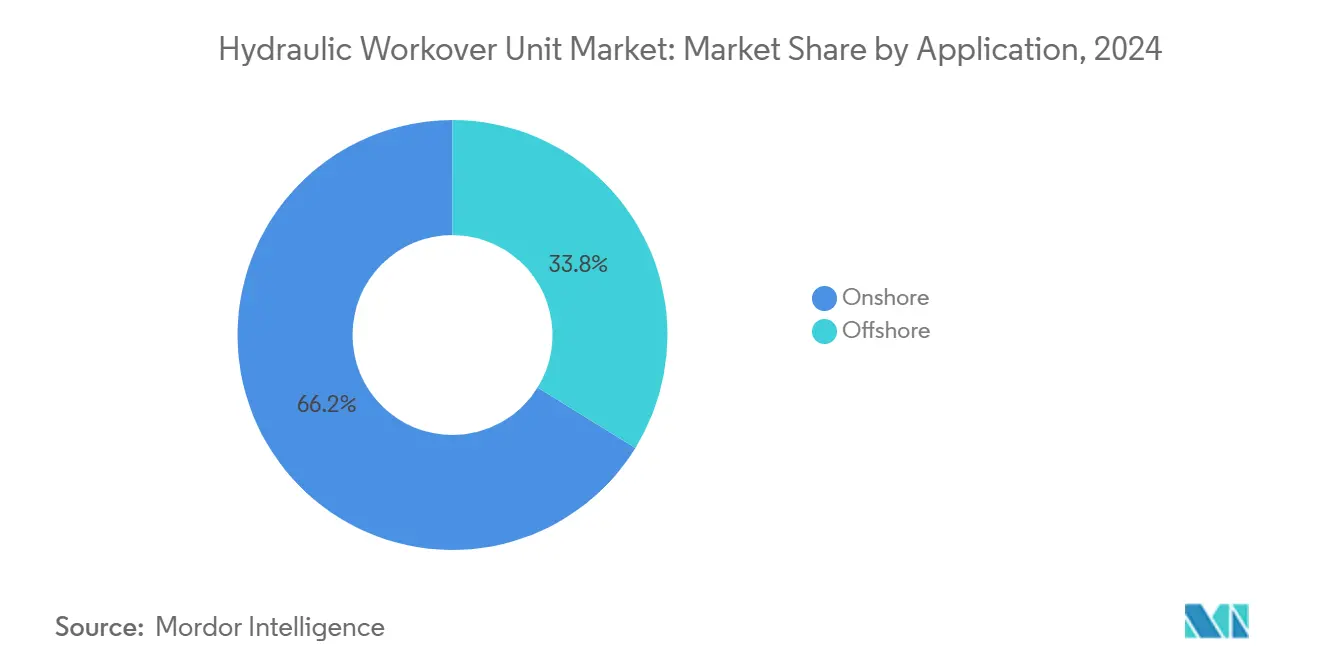

- By application, onshore activity retained 66.2% of revenue in 2024, whereas offshore campaigns are set to grow at a 5.5% CAGR to 2030.

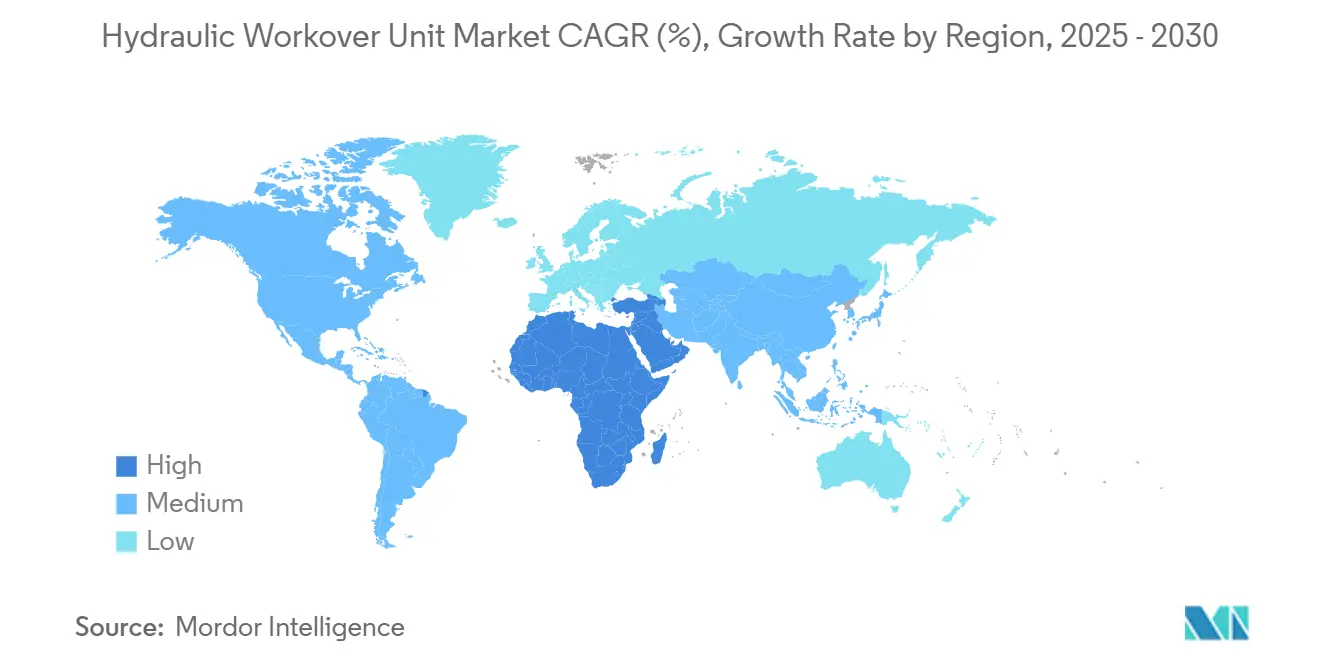

- By geography, North America led with a 32.7% share in 2024; the Asia-Pacific region is the fastest-growing at a 6.3% CAGR through 2030.

Global Hydraulic Workover Unit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing inventory of mature wells in MENA & Europe | +1.8% | MENA, Europe, spillover North America | Medium term (2-4 years) |

| Lower OPEX versus conventional workover rigs | +1.2% | Global, with offshore emphasis | Short term (≤ 2 years) |

| Surge in shallow-water life-of-field interventions | +0.9% | Gulf of Mexico, North Sea, coastal APAC | Medium term (2-4 years) |

| Autonomous & remote-operated HWOU control systems | +0.7% | North America, Europe, mature APAC | Long term (≥ 4 years) |

| Geothermal re-entry projects needing HWO units | +0.4% | North America, Europe, select APAC | Long term (≥ 4 years) |

| Hydrogen pilot wells requiring live-well snubbing | +0.2% | Europe, North America, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Inventory of Mature Wells in MENA & Europe Drives Intervention Demand

More than two-thirds of wells in the MENA and European regions will exceed 10 years of age by 2030, intensifying the need for production optimization.[1]SLB, “Middle East Mature Fields Outlook,” slb.com Saudi Aramco’s USD 25 billion award package for Jafurah and the Master Gas System underscores the region’s shift toward enhanced recovery rather than new drilling.[2]Journal of Petroleum Technology, “Jafurah Awards Mark Largest Shale Development Outside U.S.,” jpt.spe.org In Europe, North Sea operators prioritize velocity strings and advanced completions to stretch field life. Regular maintenance programs using hydraulic workover units lift production by roughly 10% at USD 12 per barrel gained, embedding these rigs as core assets for mature basins. This baseline activity secures long-term utilization for suppliers in the hydraulic workover unit market.

Lower OPEX Versus Conventional Workover Rigs Accelerates Adoption

In deepwater environments, hydraulic workover interventions cost approximately USD 0.50 per barrel of oil equivalent, compared with USD 3–4 for jack-ups, a differential of nearly 85%. Compact units require fewer personnel, minimize kill-fluid use, and expedite rig-up, sharply lowering direct and indirect expenses. Shallow-water case studies in the Gulf of Thailand have revealed successful barge-assisted hydraulic workovers on weight-constrained platforms, resulting in sustained uptime gains. These economics remain compelling during commodity downturns, ensuring that capital-disciplined producers continue to allocate funds to the hydraulic workover unit market.

Surge in Shallow-Water Life-of-Field Interventions Expands Market Scope

Chevron’s Tahiti campaign delivered an 8,500 BOPD uplift through acid stimulation executed by multi-service vessels, validating the model for rig-less shallow-water workovers. In the Asia-Pacific region, PETRONAS maintains steady hydraulic workover utilization for recompletions and plug-and-abandonment tasks across aging platforms. Modular equipment, real-time monitoring, and vessel-based deployment cut logistics costs and protect fragile installations. These innovations broaden the addressable client base for the hydraulic workover unit market, particularly for marginal fields that cannot support conventional rig day-rates.

Autonomous & Remote-Operated HWOU Control Systems Transform Operations

NOV’s KAIZEN platform utilizes machine learning to optimize operating parameters, thereby reducing risk and standardizing performance. Subsea applications, such as the Liberty E-ROV trim support vessel, spend USD 1 million per deployment and reduce exposure during high-pressure manipulation. Automation helps offset a shrinking skilled labor pool, as retiring personnel outpace new entrants in well control disciplines. The resulting safety and efficiency gains anchor a technology arms race that elevates service differentiation within the hydraulic workover unit market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-price volatility curbing intervention budgets | -1.1% | Global, especially North America shale | Short term (≤ 2 years) |

| Shortage of certified snubbing crews | -0.8% | North America, Europe, mature APAC | Medium term (2-4 years) |

| Platform deck-load constraints for heavy HWOU | -0.6% | Offshore markets worldwide | Medium term (2-4 years) |

| Regulatory delays on live-well operations | -0.3% | Europe—UK, Norway | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Oil-Price Volatility Curbing Intervention Budgets Constrains Market Growth

The EIA expects Brent to ease from USD 81 in 2024 to USD 74 in 2025 and USD 66 in 2026, forcing operators to trim discretionary spending. North American shale producers, in particular, prioritize free cash flow over production acceleration, dampening short-cycle workover demand. Halliburton’s Q1 2025 results reflected lower stimulation revenues as price uncertainty prompted deferrals.[3]Halliburton, “First-Quarter 2025 Results,” halliburton.comIn mature offshore fields, intervention economics turn marginal at sub-USD 70 pricing, stretching payback periods and limiting capital approvals. Volatility, therefore, injects cyclical softness into the hydraulic workover unit market.

Shortage of Certified Snubbing Crews Limits Operational Capacity

Live-well snubbing demands specialized pressure-control competence, yet the talent pipeline is thinning as veteran crews retire.[4]Rigzone, “Snubbing Crew Shortages Hamper Live-Well Programs,” rigzone.com Certification cycles can exceed 18 months, delaying capacity expansions even when equipment availability is adequate. Operators respond by adopting automated control systems that compress learning curves; however, technology adoption lags behind the immediate need. Consequently, crew scarcity caps near-term growth potential for the hydraulic workover unit market, especially in high-pressure, high-temperature applications where experience is irreplaceable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Snubbing Units Gain Momentum Despite Workover Dominance

Workover units maintained a 74.5% share of the hydraulic workover unit market in 2024, underpinned by their versatility in conventional interventions and broad global fleet presence. Snubbing units, however, are predicted to grow at a 6.4% CAGR to 2030 as operators embrace live-well techniques to protect reservoir pressure and eliminate costly kill-fluid programs.

Snubbing uptake is most pronounced in unconventional plays and sour reservoirs where pressure management preserves productivity and mitigates formation damage. Oman field trials restored wells in under 12 months at 40% lower cost than conventional approaches. Capability advances now enable safe operations at wellhead pressures of up to 15,000 psi, broadening the applicability. As confidence builds, the hydraulic workover unit market will see snubbing emerge as a mainstream option rather than a niche solution.

By Installation: Trailer-Mounted Systems Drive Mobility Advantages

Skid-mounted packages commanded 58.3% of the hydraulic workover unit market size in 2024, thanks to stability and payload capacity on fixed platforms and established onshore facilities. Trailer-mounted systems, advancing ata 5.7% CAGR, offer portable solutions that align with pad drilling and multi-well relocation schedules.

Recent designs feature quick-rig-up substructures, hydraulic mast deployment, and barge-assist options that allow operators to mobilize between wells within 24 hours. Regulatory standardization eases cross-border transfers, boosting asset utilization rates. As fleet owners seek higher returns and operators seek lower standby fees, trailer-mounted offerings expand their footprint in the hydraulic workover unit market.

By Rig Capacity: Heavy-Duty Units Emerge for Complex Operations

Medium-duty rigs (150–300 tons) account for 60.1% of installations across the hydraulic workover unit market, striking a balance between lifting capacity and a manageable footprint. Yet, complex deepwater and high-pressure tasks propel heavy-duty units (>300 tons) at a 5.9% CAGR as field depth and completion loads increase.

Newly released 600,000-pound units deliver weather-tolerant operations on floating installations while remaining smaller than comparable jack-ups. Operators exploit this capacity to mill long-reach liners and install 10,000-foot velocity strings without removing subsea trees. Upgrading to heavy-duty fleets, therefore, positions contractors to win premium scopes in the hydraulic workover unit market.

By Well Status: Dead-Well Operations Maintain Dominance

Dead-well work comprised 73.8% of revenue in 2024 in the hydraulic workover unit market, reflecting legacy practices and regulatory mandates that still require well killing for numerous repairs. Even so, demand for new wells grows at a 5.4% CAGR through 2030 as maturing fields require more extensive mechanical repairs and recompletions.

Live-well projects expand steadily as improved BOP technologies, real-time pressure monitoring, and snubbing proficiency alleviate historical safety concerns. Retaining reservoir pressure reduces clean-up time and environmental discharge volumes, compelling producers to trial live-well approaches where regulations permit. Blending both methods offers operational flexibility, reinforcing the hydraulic workover unit market’s resilience to shifting field needs.

By Application: Onshore Segment Drives Consistent Growth

Onshore projects captured 66.2% of 2024 turnover in the hydraulic workover unit market owing to robust unconventional development in North America and sustained remedial work in mature onshore basins worldwide. Annual growth of 5.5% through 2030 is supported by lower complexity versus offshore and a large backlog of wells requiring stimulation, re-perforation, and integrity repairs.

Offshore demand, while smaller, commands premium pricing. Recent 4,200-foot water-depth interventions off Brazil confirmed heavy-duty hydraulic workover units as cost-effective alternatives to rig-based solutions. Hybrid liftboat campaigns in the Gulf of Mexico further illustrate the flexibility of modular equipment packages. Together, these trends ensure balanced expansion across use cases in the hydraulic workover unit market.

Geography Analysis

North America accounted for 32.7% of the hydraulic workover unit market in 2024, driven by prolific shale production, deepwater Gulf of Mexico activity, and an established service ecosystem. Operators leverage hydraulic workovers for frac-hit mitigation, tubing change-outs, and live-well refracs, sustaining equipment utilization despite commodity volatility. Rising federal-lease scrutiny and methane intensity goals incentivize rig-less interventions that reduce flaring and well downtime.

Asia-Pacific is forecast to log a 6.3% CAGR to 2030, the fastest among all regions, as China’s Bohai Bay redevelopment, India’s mature-field service programs, and Southeast Asia’s shallow-water recompletions drive tool demand. National oil companies invest in platform upgrades to accommodate higher-capacity hydraulic workover units, while Australia’s basins pilot live-well hydrogen production tests that further diversify local scopes. Supply-chain localization and regional training partnerships ensure crew availability, solidifying long-term growth prospects.

Europe’s hydraulic workover activity primarily focuses on North Sea life-extension campaigns, geothermal reentries, and carbon-storage well conversions. Stringent safety regulations slow permitting for live-well snubbing, but collaborative programs with regulators progressively open new market niches. As energy transition projects accelerate, hydraulic workover units provide versatile solutions for repurposing hydrocarbon infrastructure, embedding continued relevance across European basins.

Competitive Landscape

Competitive intensity in the hydraulic workover unit market has intensified as major service providers strive for scale and technological depth. SLB’s USD 7.1 billion ChampionX purchase adds production chemistry and artificial lift capabilities, worth an estimated USD 400 million in annual pretax synergies. Nabors Industries’ acquisition of Parker Wellbore expands tubular-rental and high-spec drilling assets, enhancing integrated well-construction packages.

Technology differentiation now hinges on autonomous control software, remote-operated hydraulic power packs, and digital twin models that simulate intervention scenarios. Halliburton, Weatherford, and NOV each showcase AI-enabled platforms that optimize stroke efficiency, manage swab loads, and predict critical events before they escalate. Clients are increasingly demanding these digital layers to mitigate crew-availability risks and satisfy ESG reporting requirements, thereby reinforcing a premium tier within the hydraulic workover unit industry.

Regional specialists retain share by focusing on niche strengths such as ultra-light units for weight-restricted platforms or bespoke geothermal packages. However, capital requirements for next-generation control systems and heavy-duty upgrades may pressure smaller contractors, prompting them to form alliances or consider tuck-in acquisitions. Overall, the hydraulic workover unit market exhibits moderate consolidation, with the top five suppliers accounting for roughly 55% of combined revenue.

Hydraulic Workover Unit Industry Leaders

Halliburton

Schlumberger

Weatherford

Archer

Superior Energy Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SLB completed its acquisition of ChampionX, projecting USD 400 million in annual synergies, and cementing a broader production-asset management portfolio.

- July 2025: Aramco has awarded USD 25 billion in contracts for the Jafurah shale gas project and the Master Gas System expansion, accelerating its mature-asset production uplift goals.

- March 2025: SLB secured a multi-year contract with Woodside Energy for 18 ultra-deepwater wells on the Trion project offshore Mexico, commencing in 2026.

- October 2024: Axis and Brigade merged to form the largest U.S. well-servicing contractor, consolidating fleets under one brand.

Global Hydraulic Workover Unit Market Report Scope

| Workover |

| Snubbing |

| Skid Mounted |

| Trailer Mounted |

| Light Duty (Below 150 Tons) |

| Medium Duty (150 to 300 Tons) |

| Heavy Duty (Above 300 Tons) |

| Live Well |

| Dead Well |

| Onshore | Conventional Reservoirs |

| Unconventional/Shale | |

| Offshore | Fixed Platform |

| Jack-Up/Liftboat |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Workover | |

| Snubbing | ||

| By Installation | Skid Mounted | |

| Trailer Mounted | ||

| By Rig Capacity | Light Duty (Below 150 Tons) | |

| Medium Duty (150 to 300 Tons) | ||

| Heavy Duty (Above 300 Tons) | ||

| By Well Status | Live Well | |

| Dead Well | ||

| By Application | Onshore | Conventional Reservoirs |

| Unconventional/Shale | ||

| Offshore | Fixed Platform | |

| Jack-Up/Liftboat | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the hydraulic workover unit market?

The hydraulic workover unit market size stands at USD 10.15 billion in 2025.

How fast is demand for hydraulic workover units growing?

Global revenue is projected to rise at a 5.22% CAGR between 2025 and 2030.

Which region is expanding the quickest in hydraulic workovers?

Asia-Pacific posts the fastest growth at 6.3% CAGR through 2030 on strong offshore activity.

Why are snubbing units gaining popularity?

They allow live-well work that avoids kill-fluid costs and preserves reservoir pressure, driving a 6.4% CAGR.

What technology trends are shaping the sector?

Autonomous control systems and remote-operated hardware improve safety, offset crew shortages, and enhance efficiency.

How does oil-price volatility influence workover activity?

Lower prices can delay discretionary interventions, trimming near-term budgets but not eliminating the need for asset maintenance.

Page last updated on: