Hydraulic Power Unit Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

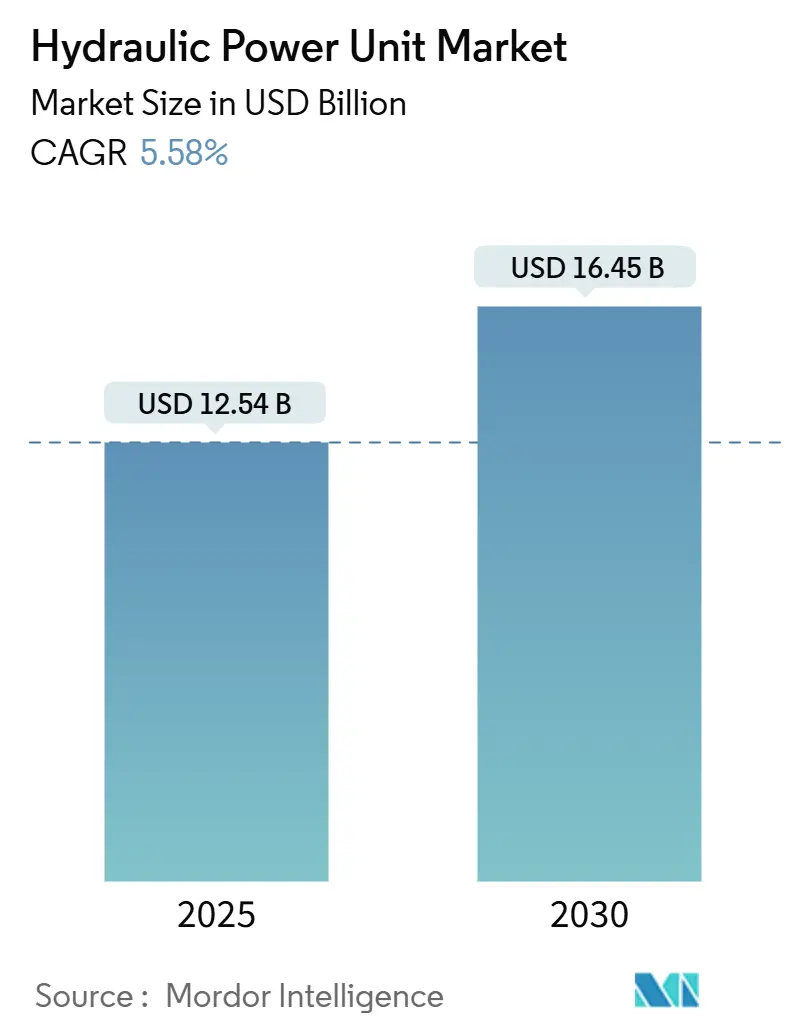

| Market Size (2025) | USD 12.54 Billion |

| Market Size (2030) | USD 16.45 Billion |

| Growth Rate (2025 - 2030) | 5.58% CAGR |

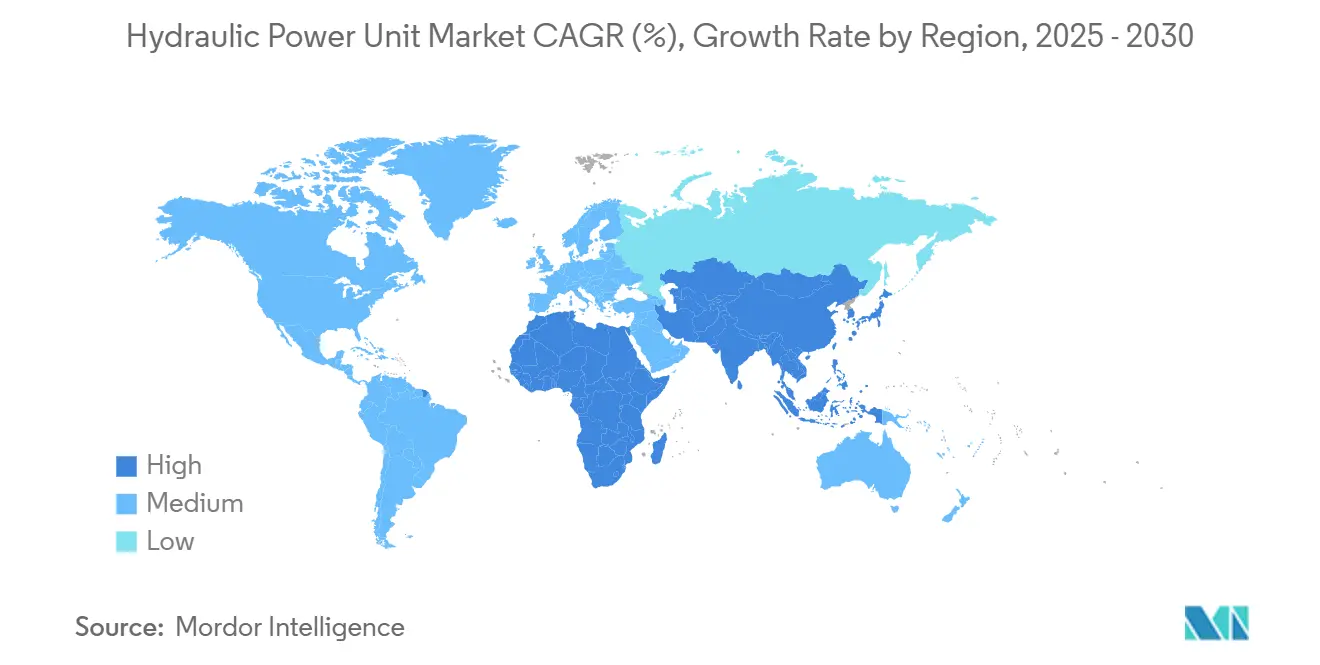

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

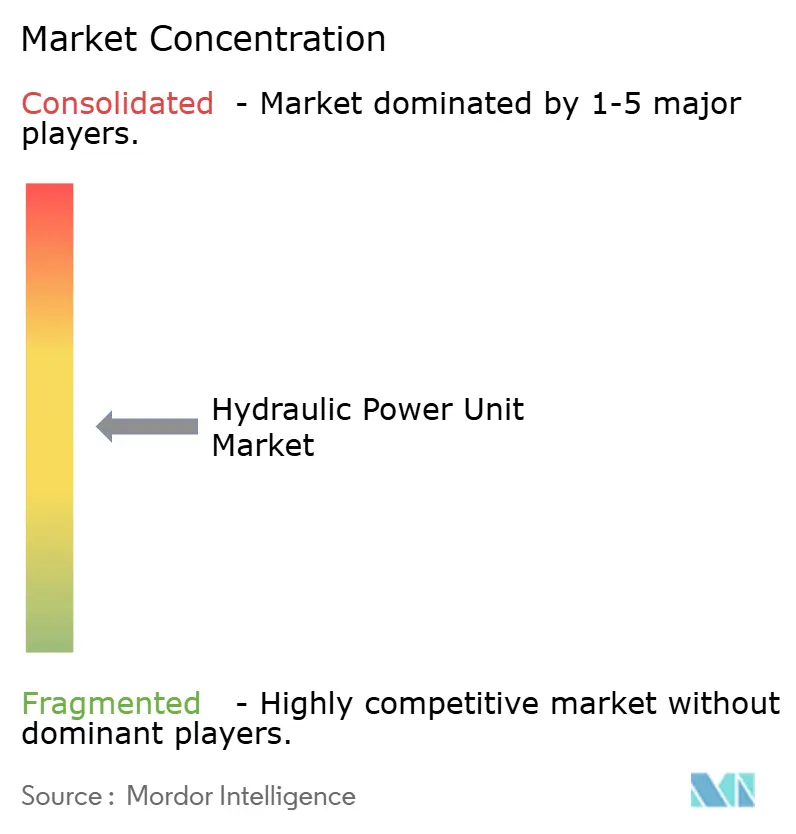

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydraulic Power Unit Market Analysis by Mordor Intelligence

The Hydraulic Power Unit Market size is estimated at USD 12.54 billion in 2025, and is expected to reach USD 16.45 billion by 2030, at a CAGR of 5.58% during the forecast period (2025-2030).

The sector maintains growth momentum as industrial automation advances, infrastructure modernizes, and hybrid electrification strategies preserve demand for high-force hydraulic actuation. Asia-Pacific remains the focus of capacity additions, while North America and Europe concentrate on energy-efficient upgrades and digital integration. Ongoing innovation in variable-speed pumps, servo-hydraulic drives, and IoT-enabled condition monitoring supports operational cost reduction and compliance with emissions regulations. Competitive dynamics are shaped by consolidation, with larger suppliers leveraging their scale to offset raw material volatility and finance R&D for compact electric-hydraulic systems.

Key Report Takeaways

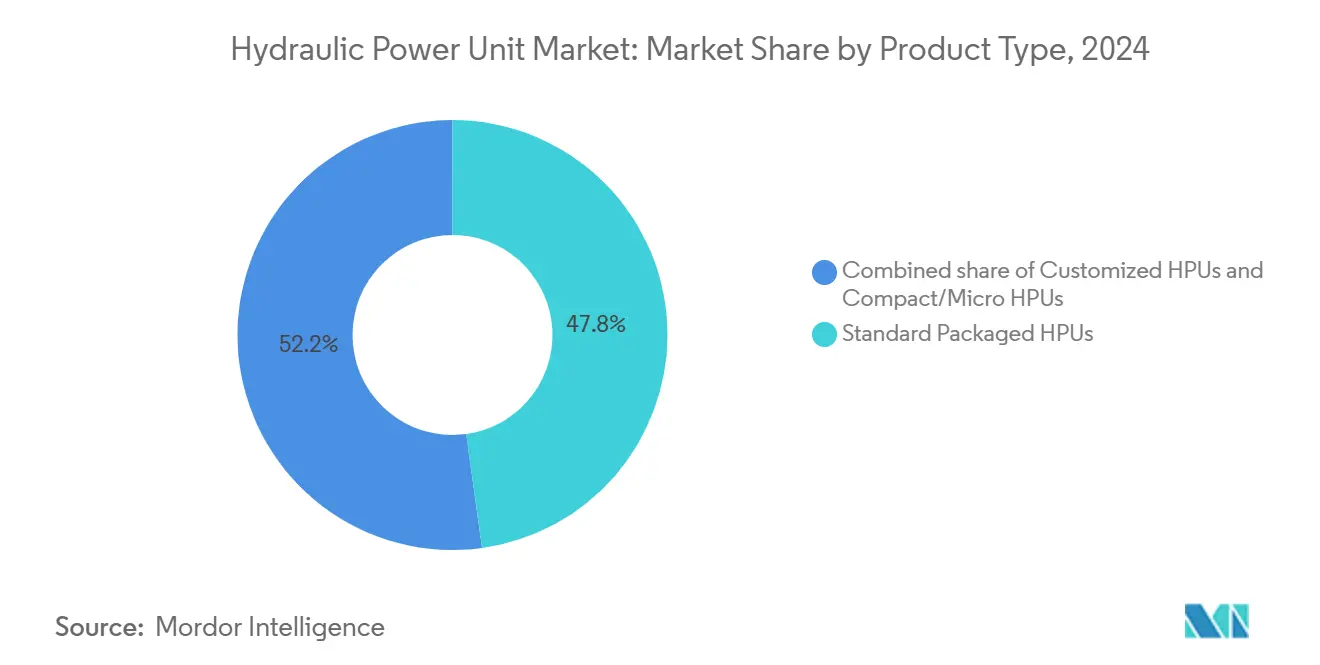

- By product type, standard packaged units accounted for 47.8% of the revenue share in 2024; customized solutions are projected to advance at a 6.5% CAGR through 2030.

- By power capacity, above-200 HP systems accounted for a 33.5% share of the hydraulic power unit market size in 2024, while units with a power capacity of up to 50 HP are projected to grow at a 6.8% CAGR between 2025 and 2030.

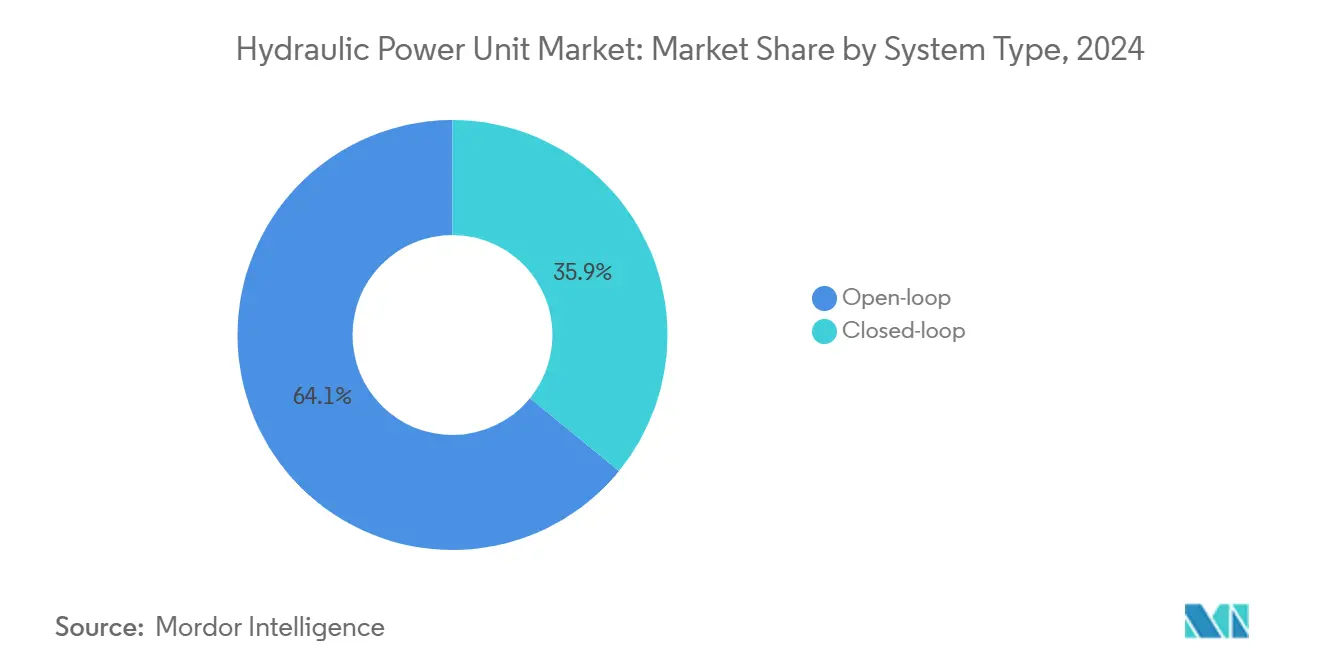

- By system type, open-loop accounted for 64.1% of the hydraulic power unit market size in 2024, whereas closed-loop is expanding at a 6% CAGR.

- By mobility, stationary installations retained a 62.9% share in 2024; mobile applications are expected to deliver the fastest CAGR at 6.3% through 2030.

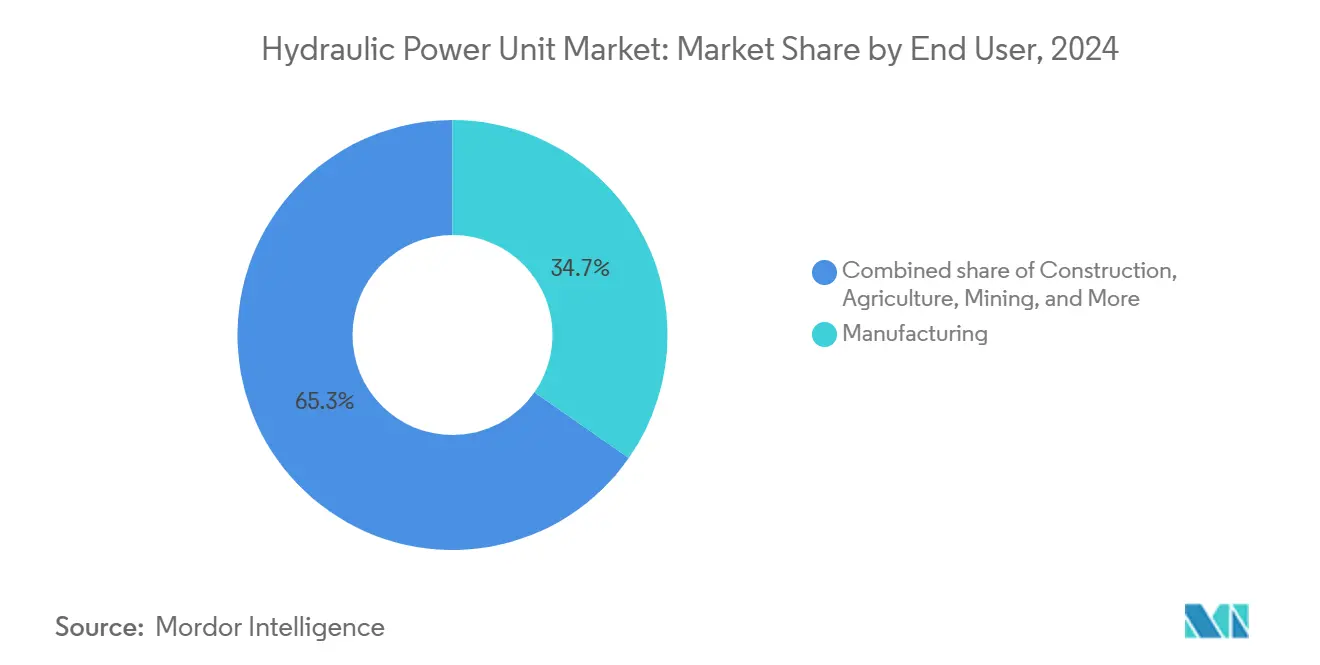

- By end user, manufacturing led with 34.7% of the hydraulic power unit market share in 2024, whereas construction is forecast to expand at a 7.1% CAGR through 2030 U.S.

- By geography, the Asia-Pacific region commanded a 39.4% revenue share in 2024 and is also forecasted to register the fastest CAGR of 5.9% from 2024 to 2030.

- Bosch Rexroth, Parker Hannifin, and Eaton collectively held a 23% slice of global revenues in 2024, underscoring a moderately fragmented competitive field.

Global Hydraulic Power Unit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification of off-highway machinery | +1.80% | Global; strongest in APAC & North America | Medium term (2-4 years) |

| Rising demand for energy-efficient hydraulics | +1.20% | EU & North America | Short term (≤ 2 years) |

| Expansion of renewable-energy EPC fleets | +0.90% | Wind- and solar-intensive regions | Long term (≥ 4 years) |

| Heavy-duty 5-axis CNC penetration | +0.70% | North America, Europe, advanced APAC | Medium term (2-4 years) |

| Micro-HPUs for collaborative robots | +0.60% | Germany, Japan, US | Short term (≤ 2 years) |

| Fast-growing African mining investments | +0.50% | Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification of Off-Highway Machinery

Hybrid equipment pairs battery-electric drivetrains with hydraulic actuation to retain superior force density in lifting, steering, and braking systems. Liebherr’s USD 2.8 billion agreement with Fortescue to supply 475 zero-emission mining trucks marks a significant shift, as the trucks retain hydraulically actuated components for critical functions. Parker Hannifin simultaneously markets sensor-rich “smarter hydraulics” that modulate flow based on load, reducing parasitic energy losses. Equipment OEMs, therefore, specify compact, efficient HPUs that integrate seamlessly with high-voltage battery architectures, opening revenue streams for suppliers that can deliver electric-hydraulic kits certified for mobile environments.

Rising Demand for Energy-Efficient Hydraulics

Variable-speed drives and servo-hydraulic packages reduce idle losses by matching pump output to instantaneous demand, a feature especially valued in 24/7 process industries that pay carbon levies. Field case studies report up to 80% electricity savings when upgrading fixed-speed systems.[1]SAE Media Group, “Servo-Hydraulic Energy Savings,” sae.org Baumüller’s audit calculator shows users tangible cost payback within two years for most duty cycles. IoT-enabled HPUs stream operating data that algorithms translate into predictive maintenance alerts, minimizing unplanned downtime and supporting service-as-a-subscription business models.

Expansion of Renewable-Energy EPC Fleets

Wind turbine erection and large-scale solar construction require rugged, trailer-mounted HPUs with capacities exceeding 200 HP to handle blades and tower sections. These fleets operate far from grid connections and require designs that tolerate intermittent generator power and airborne dust. EPC contractors prioritize standardized, easily serviced hydraulic packages to contain schedule risk. As turbine ratings exceed 15 MW, the associated lift capacities drive incremental demand for high-pressure, high-flow HPUs capable of simultaneous multi-circuit operation.

Heavy-Duty 5-Axis CNC Penetration

Aerospace and automotive machining cells increasingly rely on hydraulically clamped tombstones and rotary tables to maintain micron-level accuracy. Machines such as Hurco’s TMXMY series incorporate internal hydraulic networks governed by the CNC, ensuring repeatable positioning while suppressing thermal drift.[2]Hurco Companies, “TMXMY Series Overview,” hurco.com Demand favors closed-loop HPUs with low-ripple flow and active cooling to protect surface finish quality during lights-out shifts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in steel & copper prices | -0.80% | Global | Short term (≤ 2 years) |

| High maintenance versus electric drives | -0.60% | North America & Europe | Medium term (2-4 years) |

| Noise & leakage emission regulations | -0.40% | EU, North America, emerging APAC | Medium term (2-4 years) |

| Supply-chain exposure to rare pump alloys | -0.30% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Steel & Copper Prices

Spot steel surged 153.2% during pandemic-era disruptions, then receded 22.8% as inventories normalized[3]U.S. Bureau of Labor Statistics, “Producer Price Indexes,” bls.gov. Copper price swings exert parallel pressure on motor windings and heat exchangers. Smaller HPU assemblers often lack hedging capacity, prompting strategic stockpiles that inflate working capital and elevate breakeven points.

High Maintenance Versus Electric Drives

Fluid contamination, seal wear, and filter changes introduce service costs that purely electric actuators avoid. Where labor rates are high, end-users scrutinize the total cost of ownership and may opt for electromechanical systems with a capacity under 20 kN. Suppliers respond with contamination-tolerant pump designs, extended-life seals, and bundled maintenance contracts that guarantee uptime.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Customization Expands Value Creation

Standard packaged HPUs retained 47.8% of global revenues in 2024, primarily due to their off-the-shelf availability and attractive unit pricing. Customized assemblies, however, are growing at a 6.5% CAGR because OEMs seek performance differentiation through footprint reduction, sensor integration, and optimized cooling. The hydraulic power unit market size for customized solutions is expected to surpass USD 6 billion by 2030 as modular manifold platforms shorten engineering cycles. Moog’s EPU-G electro-hydrostatic unit exemplifies the demand for low-oil-volume architectures that fit tightly into machine envelopes while delivering closed-loop precision.

As industrial assets connect to plant MES and cloud services, end-users request HPUs with embedded edge controllers, thereby increasing average selling prices. Suppliers that develop configurable digital twins can quote more quickly and secure higher margins, whereas catalog products risk being commoditized.

By Power Capacity: Micro and Mega Polarization

Units above 200 HP dominated heavy-industry deployments, accounting for a 33.5% share in 2024, and powered steel mills, marine winches, and large excavators. Conversely, micro-systems with up to 50 HP posted the fastest growth at a 6.8% CAGR. Collaborative robots, semiconductor tools, and precision press brakes all specify micro-HPUs because they deliver 250-bar pressures in packages smaller than 30 liters. The hydraulic power unit market share for micro-capacity products is concentrated in Germany, Japan, and the United States, where factory automation adoption is highest.

Polarization forces manufacturers to maintain dual R&D roadmaps: one for ultra-compact, low-noise cartridges and another for high-flow, high-pressure pumps exceeding 500 l/min. Mid-sized ranges (51-200 HP) continue to serve the mainstream construction and agricultural equipment markets, but they lack the headline growth of the extremes.

By System Type: Closed-Loop Efficiency Gains

Open-loop architectures still account for 64.1% of usage because they are inexpensive and easy to troubleshoot. Yet, closed-loop systems are expanding at a 6.0% CAGR, thanks to energy-saving proportional valves and digital displacement pumps. Where utilities charge time-of-day tariffs, end users retrofit closed-loop HPUs to exploit power-on-demand logic that curtails off-cycle consumption. The hydraulic power unit market in Europe, in particular, rewards suppliers offering ready-certified IE5 motor packages and regenerative braking circuits that feed captured energy back to the grid.

By Mobility: Stationary Stability vs. Mobile Integration

Stationary installations accounted for 62.9% of the revenue in 2024, primarily from presses, injection-molding machines, and hydraulic powerpacks used in offshore rigs. Mobile units, though smaller in share, register a 6.3% CAGR as electrified construction and mining platforms incorporate onboard HPUs coupled to battery packs. Epiroc’s autonomous drilling rigs integrate closed-loop HPUs with digital pressure feedback to support operator-less shifts. Engineering priorities diverge: stationary gear emphasizes serviceability, while mobile design stresses vibration resistance, weight reduction, and CAN bus compatibility.

By End User: Construction Surges Ahead

Manufacturing accounted for 34.7% of revenues in 2024, driven by metal cutting, plastics forming, and general automation. Construction, however, is forecast to leapfrog other sectors with a 7.1% CAGR as governments channel stimulus into transportation, housing, and renewable energy. Hybrid excavators combine electric swing motors with hydraulic booms, maintaining demand for HPUs optimized for multi-circuit load-sensing control. Mining, agriculture, and utilities remain essential but mature niches where replacement cycles dominate order patterns.

Geography Analysis

Asia-Pacific contributed 39.4% of global revenue in 2024 and is projected to post a 5.9% CAGR through 2030. China’s leadership in electric vehicle battery plants and India’s highway expansion boost orders for both high-capacity stationary and mobile HPUs. ASEAN manufacturing diversification further amplifies consumption as companies relocate production to Vietnam and Indonesia for resilience.

North America represents a technologically advanced yet slower-growing arena where users purchase premium, digitally integrated systems. Parker Hannifin’s USD 19.9 billion fiscal 2024 revenue reflects sustained aftermarket demand for retrofit kits and service programs. Canadian investments in green hydrogen and carbon capture encourage specialty HPUs designed for hazardous locations.

Europe prioritizes energy efficiency and compliance with the circular economy. Bosch Rexroth’s EUR 7.6 billion 2023 turnover demonstrates regional appetite for smart hydraulics, with acquisitions such as HydraForce expanding modular valve offerings. OEMs utilize revisions to the EU Industrial Emissions Directive to justify the replacement of legacy open-loop powerpacks with closed-loop alternatives that meet stricter noise and leakage criteria.

Competitive Landscape

The hydraulic power unit market is moderately fragmented, with the top five suppliers accounting for approximately 38% of global billings. Bosch Rexroth, Parker Hannifin, and Eaton capitalize on broad portfolios spanning pumps, valves, filtration, and digital controllers. Mid-tier players differentiate via niche specialization—for instance, Sun Hydraulics in screw-in cartridges and HAWE in compact radial-piston pumps.

Consolidation accelerated in 2024-2025 as distributors and manufacturers sought economies of scale. Applied Industrial Technologies invested USD 260 million to acquire Hydradyne, strengthening fluid power coverage across 33 U.S. locations[4]Applied Industrial Technologies, “Hydradyne Acquisition,” applied.com. Ingersoll Rand added APSCO, Blutek, and UT Pumps for USD 135 million to broaden its mobile hydraulics and vacuum capabilities. Access to a larger installed base provides data that fuels predictive analytics platforms, reinforcing sticky service revenues.

Technology rivalry centers on servo-hydraulic drives, electro-hydrostatic actuators, and cloud-connected condition monitoring. Patent filings in smart valve timing and self-diagnosing pump swashplates suggest future competitive battles over intellectual property. Suppliers investing in open digital ecosystems may gain partner network effects that outpace proprietary architectures.

Hydraulic Power Unit Industry Leaders

Bosch Rexroth AG

Parker-Hannifin Corp.

Eaton Corporation plc

Danfoss Power Solutions

HYDAC International GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Applied Industrial Technologies acquired Hydradyne, LLC. Headquartered in Dallas, Texas, and with a presence throughout the Southeastern U.S., Hydradyne stands out as a leading provider of fluid power solutions.

- November 2024: Fortress Investment Group acquired TH Holdings, which includes Texas Hydraulics and Oilgear, to inject growth capital into the mobile and industrial segments.

- October 2024: Moog unveiled the EPU-G electrohydrostatic pump unit, cutting oil volume by 90%. The EPU-G, featuring a newly designed 4-quadrant internal gear pump and a high-dynamic servomotor, targets applications with flow rates of 20 to 85 l/min and pressure levels of up to 345 bar.

- June 2024: Wynnchurch Capital acquired Hydraulic Technologies from SPX Flow, with a pledge to expand services.

Global Hydraulic Power Unit Market Report Scope

The scope of the hydraulic power unit market report includes:

| Standard Packaged HPUs |

| Customized HPUs |

| Compact/Micro HPUs |

| Up to 50 HP |

| 51 to 100 HP |

| 101 to 200 HP |

| Above 200 HP |

| Open-loop |

| Closed-loop |

| Stationary |

| Mobile |

| Manufacturing |

| Construction |

| Agriculture |

| Mining |

| Energy and Utilities |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Standard Packaged HPUs | |

| Customized HPUs | ||

| Compact/Micro HPUs | ||

| By Power Capacity | Up to 50 HP | |

| 51 to 100 HP | ||

| 101 to 200 HP | ||

| Above 200 HP | ||

| By System Type | Open-loop | |

| Closed-loop | ||

| By Mobility | Stationary | |

| Mobile | ||

| By End User | Manufacturing | |

| Construction | ||

| Agriculture | ||

| Mining | ||

| Energy and Utilities | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the hydraulic power unit market?

The hydraulic power unit market size is valued at USD 12.54 billion in 2025 and is projected to reach USD 16.45 billion by 2030.

Which region leads demand for hydraulic power units?

Asia-Pacific holds 39.4% of global revenue, anchored by Chinese manufacturing and Indian infrastructure programs.

Which application segment is growing fastest?

Construction equipment applications are forecast to grow at 7.1% CAGR through 2030 as hybrid electrification boosts HPU content.

What technology trend most impacts market growth?

Energy-efficient servo-hydraulics and closed-loop systems that lower electricity consumption and support predictive maintenance are key growth drivers.

Who are the major players in the hydraulic power unit industry?

Bosch Rexroth, Parker Hannifin, Eaton, Moog, and Bosch-HydraForce rank among the leading global suppliers, together holding about 38% of sector revenues.

How are raw-material price swings affecting manufacturers?

Volatility in steel and copper prices can shift HPU production costs by up to 20%, pressuring margins and accelerating supply-chain consolidation.

Page last updated on: