Market Overview

| Study Period | 2021 - 2031 |

|---|---|

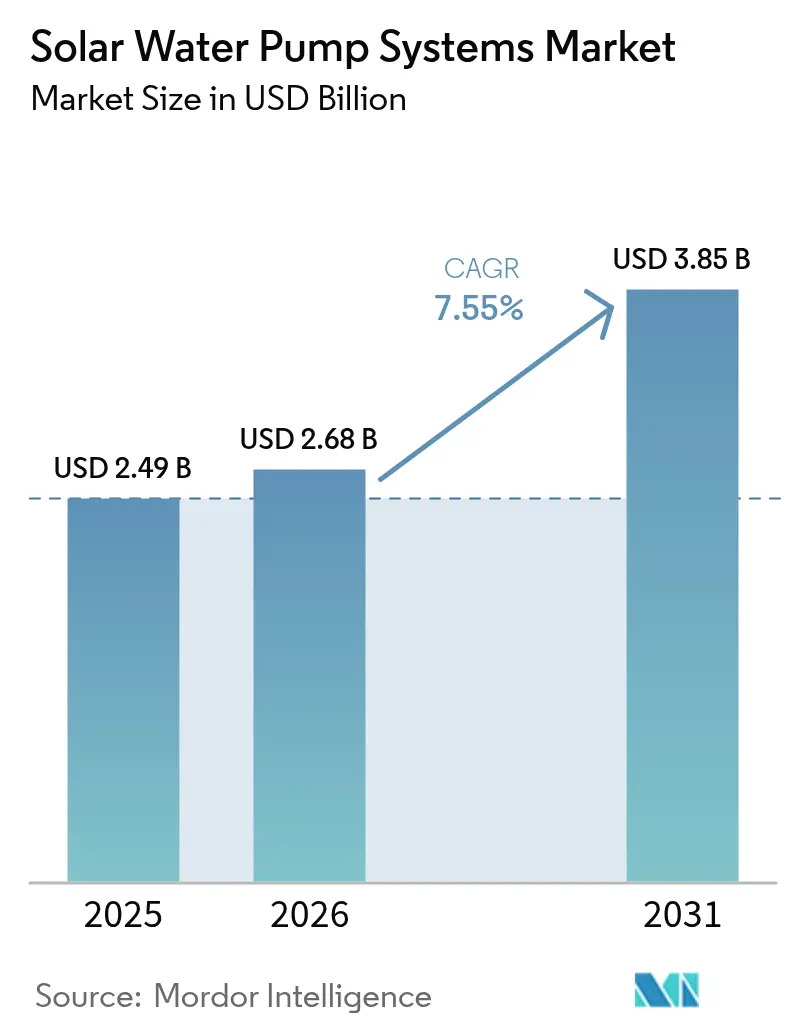

| Market Size (2026) | USD 2.68 Billion |

| Market Size (2031) | USD 3.85 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

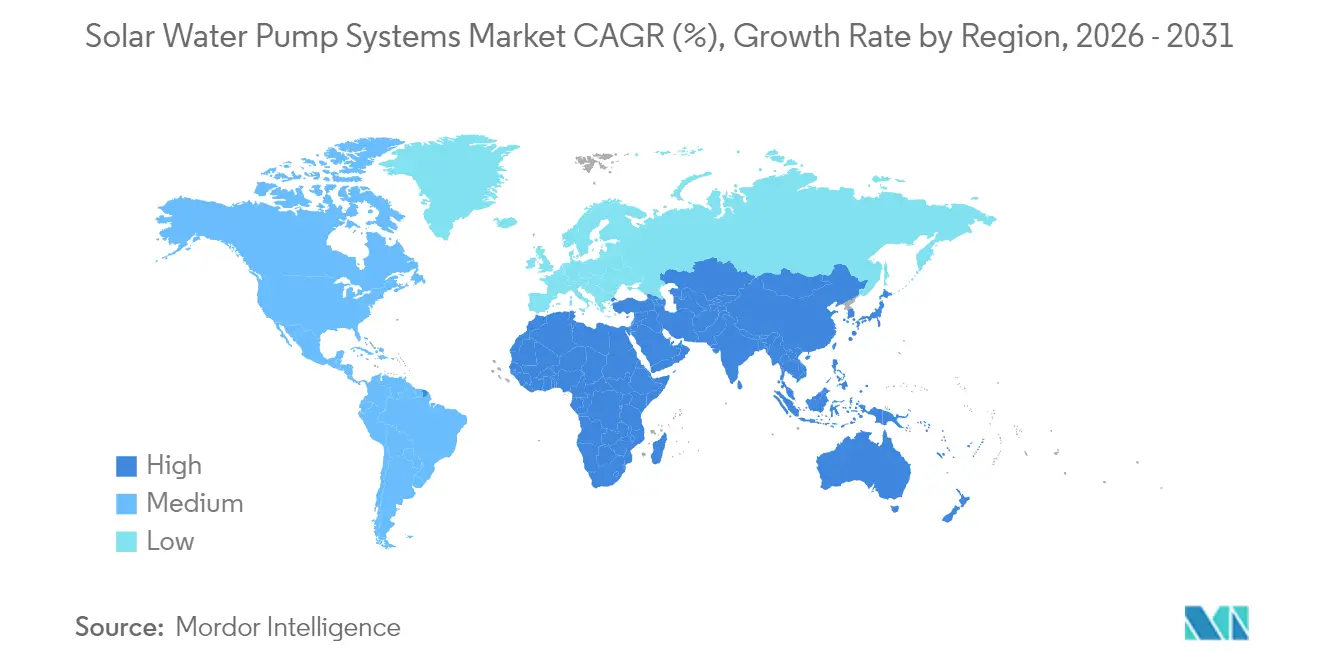

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solar Water Pump Systems Market Analysis by Mordor Intelligence

Solar Water Pump Systems market size in 2026 is estimated at USD 2.68 billion, growing from 2025 value of USD 2.49 billion with 2031 projections showing USD 3.85 billion, growing at 7.55% CAGR over 2026-2031.

Robust public-sector subsidies, an 85% fall in photovoltaic (PV) module prices since 2010, and widening irrigation deficits in water-stressed farming belts are lifting sales momentum. Surface pumps still dominate the installed base volumes, yet submersible variants are outpacing the overall solar water pump systems market, thanks to rising groundwater extraction needs and brushless DC motor upgrades that reduce maintenance downtime. Mid-range 3-10 kW units are scaling fast as commercial growers demand higher-capacity kits, while DC drives retain a cost edge in off-grid settings. Parallel digitization—encompassing satellite telemetry, IoT sensors, and predictive maintenance—now differentiates suppliers and enables utilities to monitor performance in remote communities. Investor confidence in pay-as-you-go (PAYG) leasing models is widening access for smallholders across Sub-Saharan Africa, easing the persistent up-front CAPEX hurdle.

Key Report Takeaways

- By pump type, surface pumps led with a 47.90% revenue share in 2025; submersible pumps are expected to expand at a 9.25% CAGR through 2031.

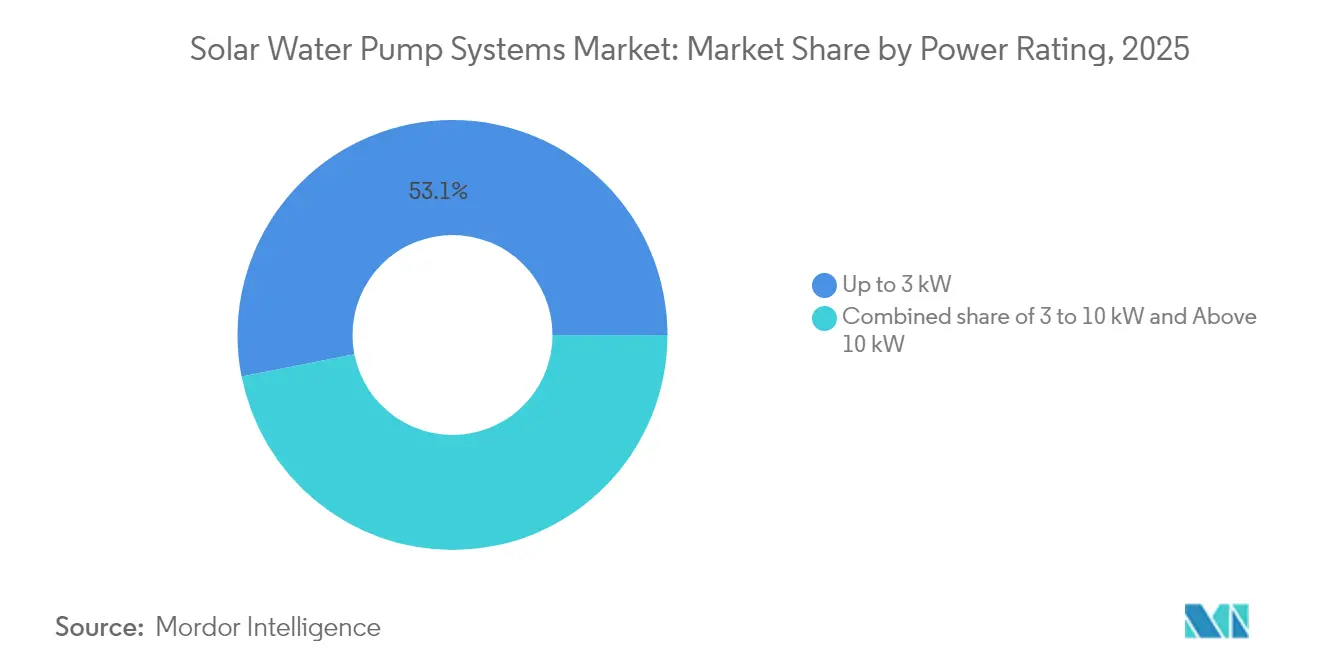

- By power rating, units with a capacity of up to 3 kW accounted for 53.10% of the solar water pump systems market share in 2025, while systems with a capacity of 3-10 kW posted the fastest 9.75% CAGR through 2031.

- By drive type, DC technology captured a 59.40% share of the solar water pump systems market size in 2025, and hybrid AC/DC drives are projected to rise at an 8.05% CAGR through 2031.

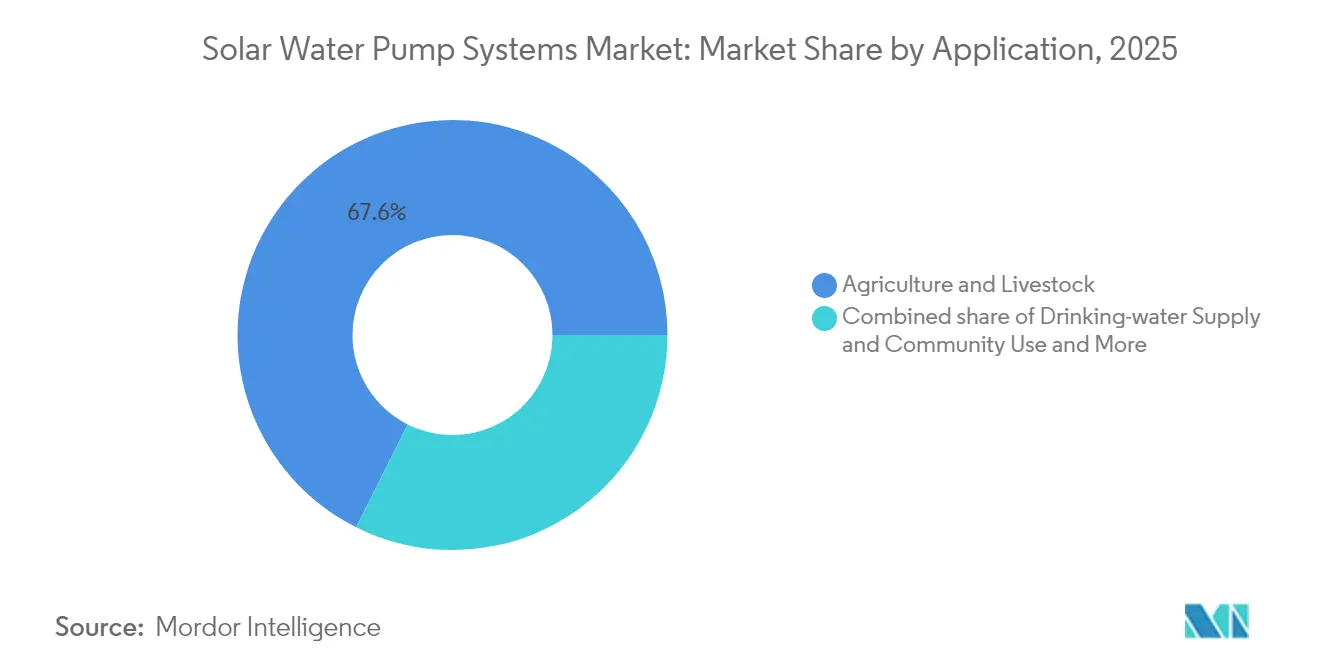

- By application, agriculture and livestock held a 67.60% share of the solar water pump systems market size in 2025; the drinking-water supply segment is projected to show an 8.55% CAGR between 2026 and 2031.

- By geography, the Asia-Pacific region commanded 63.10% of 2025 revenue, while the Middle East & Africa posted the fastest growth rate of 10.10% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Solar Water Pump Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining PV module prices | 2.50% | APAC, MEA | Medium term (2-4 years) |

| Government subsidies & rural-electrification schemes | 1.80% | APAC, MEA, South America | Long term (≥ 4 years) |

| Agricultural water-demand surge & shift to micro-irrigation | 1.20% | Water-stressed regions | Long term (≥ 4 years) |

| IoT-enabled remote monitoring & predictive maintenance | 0.90% | North America, EU, APAC | Medium term (2-4 years) |

| PAYG micro-financing models in SSA | 0.70% | Sub-Saharan Africa | Short term (≤ 2 years) |

| Hybrid AC/DC controller retrofits for legacy pumps | 0.60% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining PV Module Prices

PV module costs fell a further 12% in 2024, extending an 85% decline since 2010, as Chinese overcapacity and TOPCon cell efficiencies reached 23.1%(1)Source: Taiyang News, “Saatvik Solar’s ‘Made-In-India’ Product Offerings at REI 2024,” taiyangnews.info . Payback periods have tightened below two years in high-irradiance belts, pushing diesel pump retirements. Bifacial modules capture reflected light from water bodies, trimming array footprints and freeing farm land. Suppliers now prioritise durability—such as dual-glass laminates and anti-soiling coatings—over raw cost cuts, supporting lifetime energy yield gains.

Government Subsidies & Rural-Electrification Schemes

India’s PM-KUSUM Component-B supports 2 million standalone pumps with a 90% subsidy, reducing farm outlays to just 10% of the list price. Morocco’s NOOR and Egypt’s 250 MW irrigation corridors replicate blended-finance templates, combining upfront capital grants with skills training to curb post-installation failure rates. Fiscal prudence is vital; schemes that bundle technical support with subsidies avoid market distortions and keep private distributors engaged.

Agricultural Water-Demand Surge and Shift to Micro-Irrigation

Global farm water use is projected to increase by 15% by 2030, with drip systems replacing flood irrigation in the Kandi Belt and other semi-arid regions. Jain Irrigation’s AgroVoltaic pilots reveal conveyance efficiencies above 90% when solar pumps feed sensor-based drip lines(2)Source: The Energy and Resources Institute, “Learnings from Integrating Solar in Agriculture,” teriin.org . Soil-moisture probes, coupled with weather data, cut water draw by 28% without yield loss, which is critical as water tables drop 0.3-4 m annually across the Indo-Gangetic plains.

IoT-Enabled Remote Monitoring & Predictive Maintenance

Satellite narrowband links transmit pump vibration, flow, and irradiance files every 15 minutes, flagging anomalies before failure(3)Source: Grundfos, “Remote Monitoring Solar Water Pumps,” grundfos.com . Predictive algorithms reduce unplanned downtime by 40% and enable distributors to stock spares strategically. Field data is integrated into controller firmware updates that fine-tune duty cycles for local solar curves, increasing daily water yield by 6-9% on legacy arrays.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX despite falling PV costs | -1.1% | Global, particularly acute in low-income regions | Short term (≤ 2 years) |

| Intermittent solar irradiance leading to output variability | -0.8% | Global, with regional variations in impact severity | Medium term (2-4 years) |

| Limited end-user awareness & O&M skill gaps | -0.6% | APAC and MEA, concentrated in rural areas | Medium term (2-4 years) |

| Emerging groundwater-extraction caps in water-stressed regions | -0.4% | Global, with focus on India, California, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX Despite Falling PV Costs

Complete systems span USD 2,100-5,000 per hectare, equivalent to two-plus years of smallholder cash income in the Philippines, even when the ROI exceeds 315%(4)Source: ResearchGate, “Promoting Sustainable Agriculture Using Solar Irrigation,” researchgate.net . Controllers, structures, and labour now account for 60-70% of the project cost, mitigating further PV price gains. PAYG leases and equipment-as-a-service lift adoption yet strain provider working capital and demand robust collection tech.

Intermittent Solar Irradiance Leading to Output Variability

Cloud cover can reduce daily pumping capacity by 30-50% during the monsoon or winter months. Battery buffers add 40-60% cost and maintenance. Hybrid AC/DC units automatically switch to the grid where available, but weak rural lines limit their scope. World Bank modelling cautions that cheap pumping may encourage expansion into thirstier crops, offsetting CO₂ gains if governance fails(5)Source: World Bank, “Navigating the Opportunities and Risks of Solar Irrigation,” worldbank.org .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Submersible Systems Expand Reach

Sales of submersible units increased to 41.60% of 2025 shipments, while surface pumps maintained a 47.90% revenue lead. The segment’s 9.25% CAGR stems from deeper borehole drilling as surface water variability rises. Brushless DC motors and corrosion-resistant alloys simplify maintenance, while variable-frequency drives modulate speed to accommodate fluctuating irradiance, enhancing efficiency in the solar water pump systems market. In community schemes, low-flow positive-displacement pumps deliver steady head pressure, ideal for elevated storage tanks and day-night dispensing.

Embedded telemetry enables utilities to stagger pump starts, thereby flattening village load peaks. Suppliers bundle training so operators swap down-hole cartridges with basic tools, trimming service calls. Consistent flow also supports small aquaculture ponds, which diversify farmer income without requiring extra diesel consumption. With groundwater depth often exceeding 80 m in semi-arid APAC, submersibles prevail where suction limits hobble surface pumps.

By Power Rating: Mid-Range Systems Drive Commercial Uptake

Units of up to 3 kW dominate smallholder plots, yet the 3-10 kW slice registers the fastest 9.75% CAGR as cooperatives irrigate blocks of 8-20 ha. Declining per-kilowatt costs above 5 kW encourage growers to oversize arrays for morning and late-afternoon pumping windows, smoothing labour schedules in the solar water pump systems market. Modular designs allow owners to start with 5 kW and then add extra string inverters as acreage scales, avoiding stranded assets.

Industrial orchards and floriculture estates are piloting sets exceeding 10 kW to lift water from aquifers at depths of 150-200 m. Grid interconnection and protection relays inflate paperwork, but tariffs offset night-time top-ups when climate sensors trigger frost mitigation irrigation. Development banks in MEA now bundle concessional credit for 8-12 kW kits that serve shared pasture boreholes, cutting diesel haulage cost spikes after rainy-season road washouts.

By Drive Type: DC Retains Lead, Hybrids Gain Ground

Direct-current drives own 59.40% of 2025 revenue by bypassing inverters and associated losses, keeping the bill of materials lean for off-grid buyers. Fault diagnosis is simpler, with fewer electronic stages exposed to heat cycling. Yet grid-adjacent dairies favour hybrid controllers that toggle to AC during cloudbursts, keeping trough levels stable without the need for battery packs. Firmware updates enable remote parameter adjustments, such as increasing float switch thresholds in drought alerts.

Regulatory shifts in the EU impose power-quality limits on direct grid-tied systems, prompting installers to consider transformer-isolated hybrids. Commercial lenders also view bi-directional capability as collateral against output volatility, thereby increasing the odds of loan approval. The resulting traction tightens the supplier race to optimise MPPT algorithms for both PV and grid modes, fostering innovation in the solar water pump systems market.

By Application: Drinking-Water Supply Accelerates

Agriculture and livestock still absorb 67.60% of 2025 shipments, but community drinking-water systems grew 8.55% CAGR on donor funding and NGO roll-outs. Zero-fuel pumps reduce operational leakage, allowing village committees to redirect tariffs to filter cartridges and improve well sanitation. Remote sensors alert technicians to the risk of dry-running, extending pump life. Health clinics now integrate small solar pumps with rooftop PV and UV purification, cutting disease incidents tied to stagnant hand-dug wells.

Industrial dewatering at quarries and tunnels remains a niche yet lucrative market. Predictable duty cycles align with solar curves, and telemetry eliminates the need for daily site visits. Environmental regulators are increasingly mandating a diesel phase-out, positioning solar pumps as compliance tools that halve CO2 footprints compared to gensets in the solar water pump systems market.

Geography Analysis

Asia-Pacific generated 63.10% of 2025 revenue, underpinned by India’s target for 3 million pumps by 2026 and China’s integrated PV-pump packages that slash deployment times. State utilities in Maharashtra co-finance 3-7.5 HP submersibles, removing 90% of farmer CAPEX and fuelling bulk tender momentum. Concerns rise around groundwater overdraft, spurring pilots that pair metered pumps with prepaid smart cards to ration extraction sustainably.

The Middle East & Africa contributes a modest base today, yet logs the swiftest 10.10% CAGR to 2031. Morocco’s NOOR irrigation loans and AfDB lines of credit unlock 2-5 kW PAYG pumps for cereal growers, while Kenya’s distributors bundle mobile-money repayment plans that match harvest cashflows. Intense irradiance and erratic diesel supply chains accentuate the comparative advantage of the solar water pump systems market in this region. Capacity-building grants train local technicians, improving first-year service call resolution rates from 54% to 82%

North America and Europe mature steadily as they retrofit diesel backup wells and pursue net-zero farm mandates. California’s SGMA groundwater rules and EU nitrate directives pressure growers to couple smart irrigation with solar pumping, thereby tightening accountability for the water–energy nexus. OEMs headquartered in these regions pilot satellite-linked asset clouds that fuse pump, soil, and weather analytics, exporting software licences to APAC dealers after market validation.

Competitive Landscape

Competitive intensity is high, with no firm exceeding a 10% share, indicating a fragmented structure. Legacy pump majors—Grundfos, Xylem, and KSB—leverage their supply chains, while specialists such as Lorentz or Shakti Pumps pitch end-to-end solar kits. Strategic alliances dominate consolidation efforts; Xylem’s December 2024 majority stake in Idrica marries hydraulic hardware with digital analytics to deliver utility-scale smart-water suites. Grundfos partners with satellite IoT provider Myriota to embed nanoband links in controllers, providing distributors with data-driven service contracts and securing aftermarket revenue.

Regional OEMs deepen vertical integration. Saatvik Green Energy pivoted from module manufacturing to bundled pump sales after clinching a 250-unit tender in Maharashtra in February 2025. Shakti Pumps secured India’s largest single-state order for 12,537 units under PM-KUSUM, demonstrating its scale capability and narrowing the cost gap with multinational brands. IoT and hybrid-drive engineering remain key battlegrounds as clients demand continuous uptime and grid compatibility.

White-space opportunities sit in integrated storage, where lithium-iron-phosphate packs smooth evening loads for dairy and community taps. Entry barriers rise because certification, fire safety, and thermal management skills differ from those required for pump hydraulics. Firms that master both domains can prise premium margins in the solar water pump systems market.

Solar Water Pump Systems Industry Leaders

Shakti Pumps (India) Limited

Kirloskar Brothers Ltd.

Xylem Inc.

Grundfos Holding A/S

LORENTZ GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tata Power Renewable Energy and Andhra Pradesh signed an MoU to develop up to 7 GW renewable projects, earmarking a share for solar pumping clusters.

- February 2025: Saatvik Green Energy secured a contract to supply 250 solar submersible pumps in Maharashtra, marking its entry into the integrated pump solutions market.

- December 2024: Xylem acquired majority control of Idrica, strengthening smart-water analytics capabilities for pump fleets.

- November 2024: Saatvik Solar unveiled a dual-glass G12R TOPCon 625 W module aimed at solar pumping arrays during REI 2024.

Global Solar Water Pump Systems Market Report Scope

The solar water pump systems market report includes:

By Pump Type

| Surface (DC, AC/DC hybrid) |

| Submersible (DC, AC/DC hybrid) |

| Helical/Positive-displacement |

By Power Rating

| Up to 3 kW |

| 3 to 10 kW |

| Above 10 kW |

By Drive Type

| DC |

| AC/DC Hybrid |

By Application

| Agriculture and Livestock |

| Drinking-water Supply and Community Use |

| Industrial and Mining Dewatering |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Pump Type | Surface (DC, AC/DC hybrid) | |

| Submersible (DC, AC/DC hybrid) | ||

| Helical/Positive-displacement | ||

| By Power Rating | Up to 3 kW | |

| 3 to 10 kW | ||

| Above 10 kW | ||

| By Drive Type | DC | |

| AC/DC Hybrid | ||

| By Application | Agriculture and Livestock | |

| Drinking-water Supply and Community Use | ||

| Industrial and Mining Dewatering | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the solar water pump systems market?

The solar water pump systems market size reached USD 2.68 billion in 2026 and is forecast at USD 3.85 billion by 2031.

Which region leads global demand?

Asia-Pacific accounts for 63.10% of 2025 revenue, driven chiefly by India’s PM-KUSUM program.

What pump type is growing fastest?

Submersible units post the quickest 9.25% CAGR through 2031 as farmers tap deeper aquifers.

How are financing barriers being addressed?

Pay-as-you-go leasing and 90% capital subsidies under schemes like PM-KUSUM lower up-front costs for smallholders.

Which technological trend is differentiating suppliers?

IoT-enabled remote monitoring combined with predictive maintenance is emerging as a key competitive edge.

Why is MEA showing the highest growth rate?

Acute water scarcity, strong solar irradiance, and multilateral development financing propel a 10.10% CAGR in the region.

Page last updated on: