Hybrid Memory Cube Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

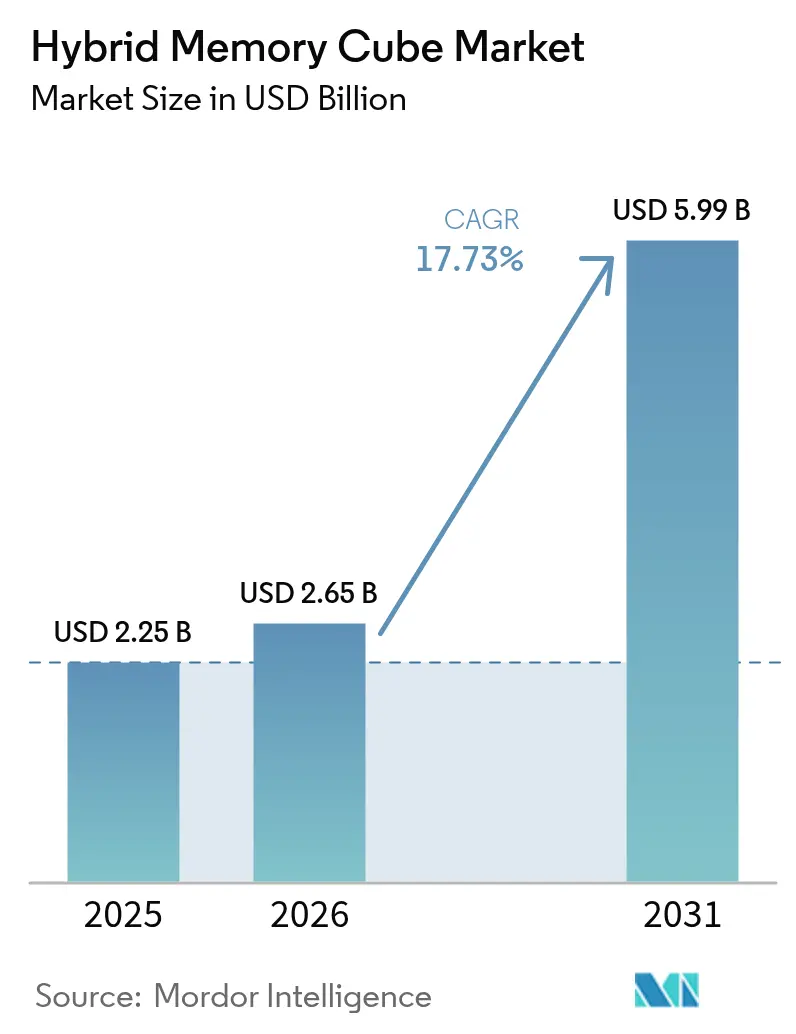

| Market Size (2026) | USD 2.65 Billion |

| Market Size (2031) | USD 5.99 Billion |

| Growth Rate (2026 - 2031) | 17.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Memory Cube Market Analysis by Mordor Intelligence

The Hybrid Memory Cube market size is expected to grow from USD 2.25 billion in 2025 to USD 2.65 billion in 2026 and is forecast to reach USD 5.99 billion by 2031 at 17.73% CAGR over 2026-2031. Enterprise storage upgrades, chiplet-based heterogeneous integration, and the rollout of exascale supercomputers are widening the total addressable opportunity, while the manufacturing scale in the Asia-Pacific positions the region at the center of supply and demand. Technology competition is intensifying as optical-interconnect prototypes and universal chiplet interconnect standards reduce vendor lock-in and expand the potential customer base. At the same time, yield headwinds in through-silicon-via (TSV) processes and thermal-management complexity threaten to restrain near-term unit cost improvements.

Key Report Takeaways

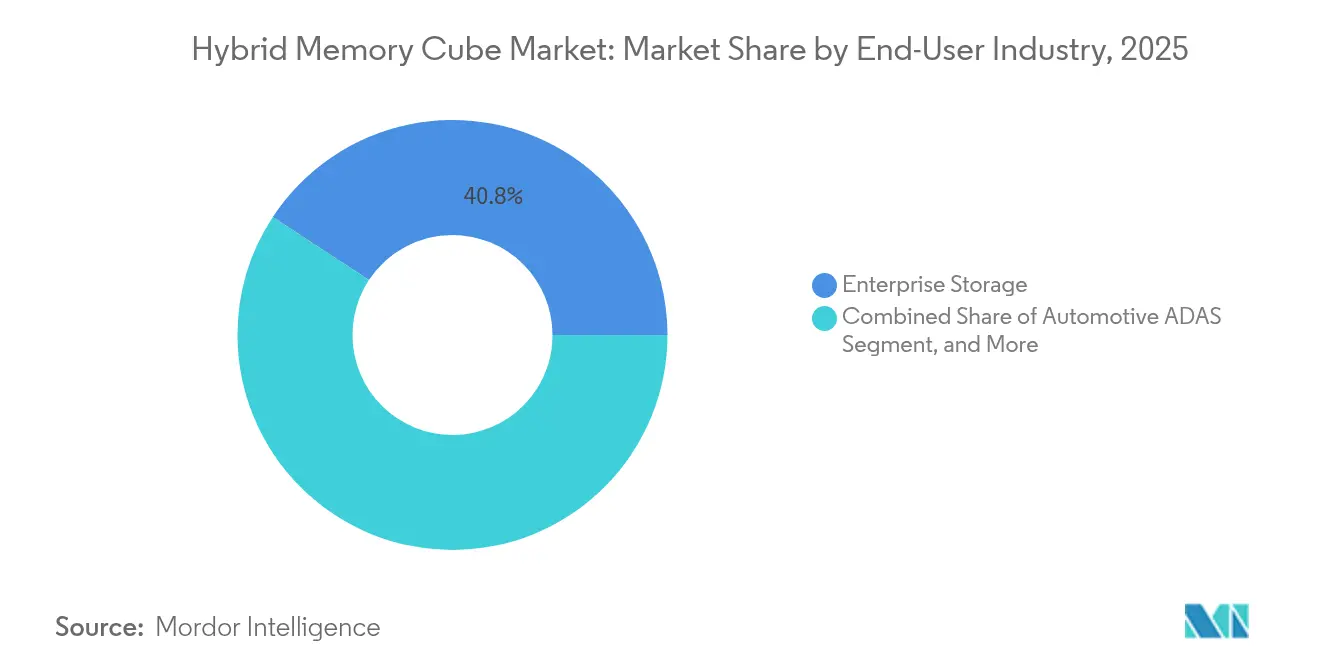

- By end-user industry, enterprise storage led with a 40.75% market share of the hybrid memory cube market in 2025, whereas automotive ADAS is forecast to expand at a 20.42% CAGR through 2031.

- By memory capacity, the 16 GB to 32 GB tier accounted for 37.15% of the hybrid memory cube market share in 2025. Modules larger than 32 GB are expected to grow at a 19.62% CAGR to 2031.

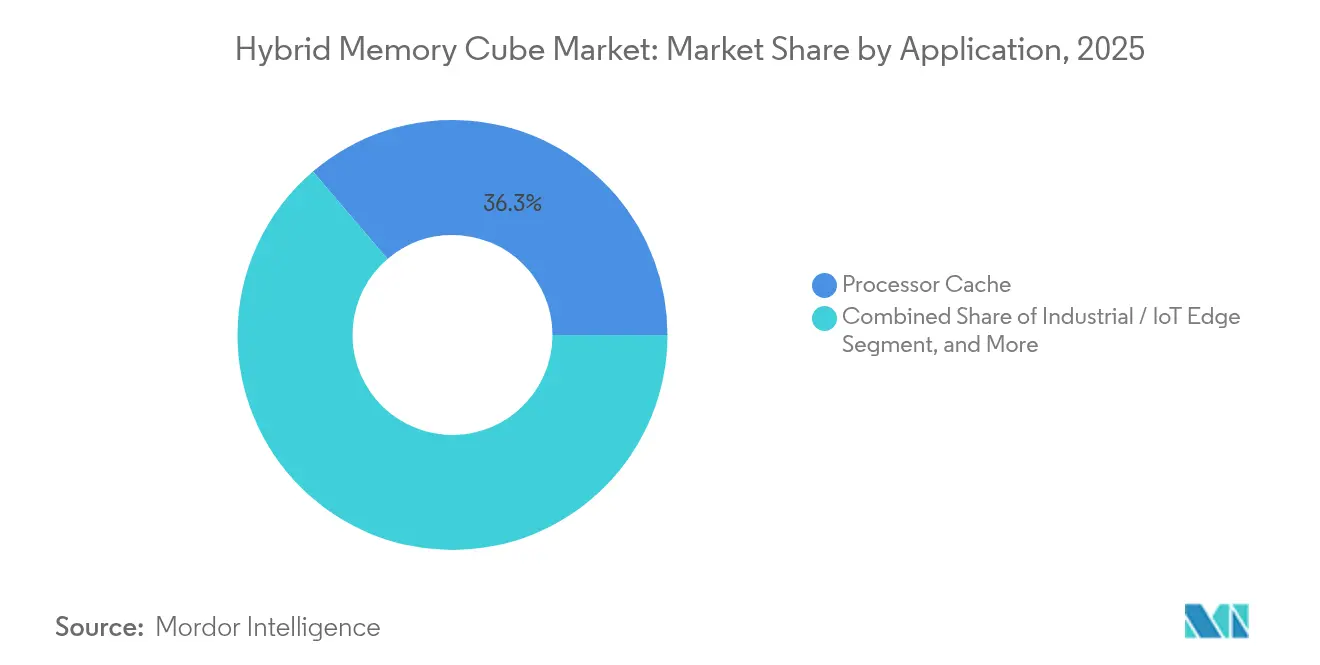

- By application, processor-cache deployments accounted for 36.25% of the hybrid memory cube market size in 2025, and industrial and IoT edge nodes are projected to advance at a 20.15% CAGR during 2026-2031.

- By technology node, TSV-based second-generation products commanded a 47.35% of the hybrid memory cube market share in 2025; however, optical-interconnect variants are projected to advance at a 19.28% CAGR over the forecast horizon.

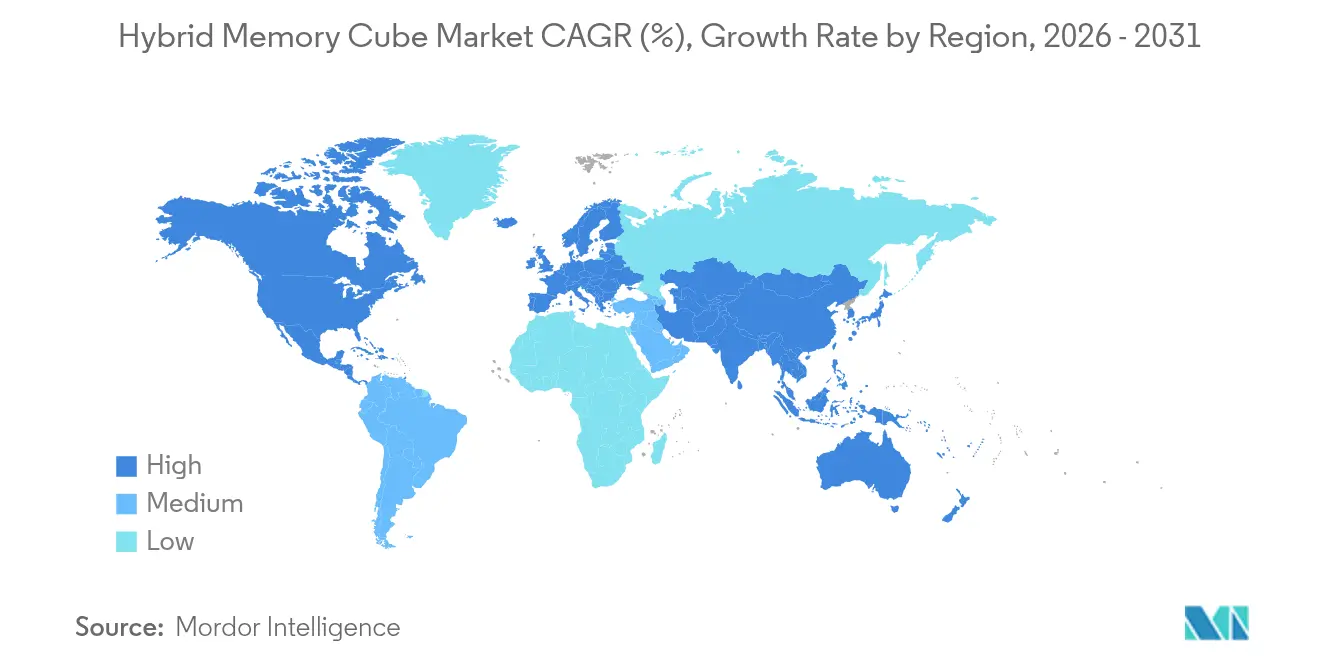

- By geography, the Asia-Pacific region contributed 41.05% of the hybrid memory cube market share in 2025 and is projected to grow at a 19.93% CAGR through 2031, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hybrid Memory Cube Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid uptake of AI / HPC workloads demanding high-bandwidth memory | +4.2% | Global, with concentration in North America and Asia Pacific | Medium term (2-4 years) |

| Growing enterprise storage and hyperscale datacenter refresh cycles | +3.8% | North America and Europe, spill-over to Asia Pacific | Short term (≤ 2 years) |

| Expanding 5G core and edge networking equipment deployments | +2.5% | Asia Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Government-backed exascale computing initiatives in the United States, China and Europe | +2.9% | United States, China, European Union | Long term (≥ 4 years) |

| Chiplet-based heterogeneous integration architectures gaining traction | +2.7% | Global, with early gains in Taiwan, South Korea, United States | Medium term (2-4 years) |

| Shift toward composable and disaggregated server architecture in cloud platforms | +2.1% | North America and Europe hyperscale operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of AI and HPC Workloads Demanding High-Bandwidth Memory

Large-language-model training has underscored the memory wall, where compute stalls before arithmetic units saturate, and Hybrid Memory Cube packages deliver up to 320 GB/s to keep GPUs and tensor cores fed.[1]Institute of Electrical and Electronics Engineers, “Energy Efficiency in 3-D Memory Interconnects,” ieee.org Edge inference for real-time language translation and autonomous perception now mandates low-latency DRAM alternatives, cementing demand for vertically stacked memory. Micron reported that AI server memory content doubled relative to traditional enterprise nodes in fiscal 2024, with high-bandwidth products capturing a rising percentage mix. IEEE research has found that 3-D interconnects lower energy per bit by 40% compared to DDR5, thereby reducing operating costs in megawatt-scale clusters. Continuous fine-tuning and retrieval-augmented generation extend memory footprints beyond terabyte levels, and modular scalability makes Hybrid Memory Cube attractive for such regimes. Early adopters also note latency determinism advantages, which improve quality-of-service metrics for conversational AI workloads.

Growing Enterprise Storage and Hyperscale Datacenter Refresh Cycles

Hyperscalers are replacing HDD arrays with all-flash nodes that integrate computational storage processors, and these chips demand bandwidth to manage parallel NAND channels with minimal queue depth.[2]Intel Corporation, “Investor Presentation 2024,” intc.com Intel highlighted that next-generation storage controllers rely on high-bandwidth memory to accelerate inline deduplication, erasure coding, and encryption. Enterprise refresh cycles are compressing as organizations adopt composable infrastructure, further emphasizing the need for packet-based memory interfaces that Hybrid Memory Cube supports. Samsung disclosed that enterprise SSD attach rates for stacked memory doubled year-over-year in 2024, reflecting this migration. Regulatory frameworks such as ISO 27001 intensify bandwidth needs by requiring always-on encryption and audit logging. Hyperscale operators also seek ways to reduce total rack count, and high-bandwidth memory reduces per-node latency, enabling denser deployments.

Government-Backed Exascale Computing Initiatives in the United States, China, and Europe

The U.S. Department of Energy’s Frontier and Aurora systems achieve sustained exaflop performance by utilizing 3D stacked memory, which provides consistent bandwidth to thousands of accelerators. China’s National Supercomputing Centers in Wuxi and Guangzhou deployed pilot systems with domestic stacked memory to sidestep import risks, backed by the National Integrated Circuit Fund’s CNY 15 billion allocation in 2024. The EuroHPC Joint Undertaking earmarked EUR 1.2 billion for pre-exascale projects, specifying high-bandwidth modules that support coherent interconnects and dynamic voltage scaling. These public investments offset non-recurring engineering costs, enabling commercial vendors to refine products before volume rollouts. Export-control regimes further accelerate domestic technology development in China, positioning Hybrid Memory Cube as a hedge against supply-chain shocks. Vendors that secure reference design wins now can establish long-cycle revenue streams once systems graduate from pilot to production.[3]Samsung Electronics, “Enterprise SSD Roadmap 2024,” samsung.com

Chiplet-Based Heterogeneous Integration Architectures Gaining Traction

Chiplet design splits complex SoCs into smaller dies, allowing economical node mixing and yield improvements. AMD’s EPYC roadmap features stacked memory dies connected through organic interposers, showcasing the advantages of TSV and chip-on-wafer-on-substrate technologies. TSMC expanded chip-on-wafer capacity in 2024, enabling customers to integrate Hybrid Memory Cube with logic or analog chiplets in a single package. The Universal Chiplet Interconnect Express (UCIe) standard, finalized in 2024, defines electrical, protocol, and mechanical specifications that the Hybrid Memory Cube serializer-deserializer already meets, lowering adoption friction. IEEE Spectrum estimated that chiplet segmentation reduces mask costs by 30% and localizes yield excursions, thereby improving the economic viability of mid-volume applications. Automotive and aerospace customers gain the flexibility to pair safety-certified compute chiplets with high-bandwidth memory modules, thereby speeding up platform certification cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong incumbency of conventional DDRx / LPDDR DRAM technology | -2.4% | Global | Short term (≤ 2 years) |

| High manufacturing cost and TSV yield constraints | -3.1% | Global, acute in leading-edge fabs | Medium term (2-4 years) |

| Thermal management complexity in 3-D stacked memory cubes | -1.8% | North America and Europe datacenter operators | Medium term (2-4 years) |

| Limited supplier ecosystem and IP licensing frictions | -1.5% | Global, with friction in Asia Pacific and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Manufacturing Cost and TSV Yield Constraints

Deep reactive-ion etching for TSVs introduces defect mechanisms not present in planar DRAM, increasing the per-gigabyte cost by up to 60% relative to DDR5, according to SK hynix’s 2024 earnings call. Yields under 85% create redundancy overhead and inflate die area, reducing gross margins. Copper-pumping failures during thermal cycling further damage bond integrity, worsening scrap rates in advanced packaging lines. Each TSV-capable cleanroom retrofit costs at least USD 500 million and needs nearly two years to qualify, limiting rapid capacity expansion. Environmental directives such as the EU’s RoHS add material-substitution requirements, complicating process chemistry and further delaying scale-up. Until yield climbs above 90%, vendors are likely to focus on premium niches rather than mass-market volumes.

Strong Incumbency of Conventional DDRx and LPDDR Technology

DDR5 module shipments surpassed 200 million units in 2023, driving per-gigabyte cost below USD 3 and reinforcing supply-chain economies of scale. Server OEMs need lengthy qualification cycles to introduce a non-DDR interface, and many enterprise customers maintain risk-averse purchasing policies. LPDDR5 already delivers adequate bandwidth for mobile and automotive use, reducing the urgency to shift to stacked solutions for cost-sensitive designs. JEDEC’s DDR6 and LPDDR6 roadmaps extend incumbent trajectories through 2027, delaying platform architects’ need for disruptive memory adoption. The comfort of a familiar ecosystem means many buyers will wait for stacked-memory prices to converge before committing to a design overhaul.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Enterprise Storage Holds Lead, Automotive ADAS Accelerates

Enterprise storage contributed 40.75% of 2025 revenue, underpinned by hyperscale operators refreshing all-flash arrays with memory-semantic storage controllers. These upgrades increase random-access throughput and use Hybrid Memory Cube packages to maintain low tail latency across parallel NAND channels. Automotive ADAS workloads, centered on Level 3 and Level 4 autonomy, are projected to rise at a 20.42% CAGR through 2031 as sensor fusion and in-vehicle AI become mainstream. Telecommunications, high-performance computing, and industrial automation each adopt the Hybrid Memory Cube to address deterministic latency needs that outstrip those of conventional DRAM. Regulatory requirements surrounding functional-safety certification and cybersecurity accelerate procurement in safety-critical domains.

Automotive growth highlights the shift of the hybrid memory cube market toward edge devices, which prioritize thermal efficiency and sustained bandwidth. The sensor count per vehicle is climbing, and real-time perception algorithms benefit directly from low-latency memory. Enterprise storage growth is now moderating as penetration reaches mature levels in North America and Europe, though ongoing capacity optimization ensures continued product cycles. Telecommunications operators are leveraging pooled-memory constructs in 5G core deployments. Government policies, such as the FCC’s Open RAN push and the EU Machinery Regulation, also champion modular memory architectures that Hybrid Memory Cube supports.

By Memory Capacity: Mid-Range Dominates, High-Capacity Surges

Modules in the 16 GB to 32 GB range captured 37.15% of 2025 deployments, aligning with expectations for dual-socket servers and providing the optimal sweet spot for cost-performance balance. The hybrid memory cube market size for capacities greater than 32 GB is forecast to expand at a 19.62% CAGR as large-language-model inference nodes and NUMA systems deploy multi-terabyte pools. The 8 GB-to-16 GB tier supports power-constrained edge servers, while devices with capacities below 8 GB remain common in embedded industrial controls, where radiation tolerance and extended temperature ratings take precedence over raw capacity.

The average memory per socket has doubled from 128 GB in 2020 to 256 GB in 2024, and the shift toward AI inference servers that store model weights in system memory has widened the addressable high-capacity segment. Network-slice orchestration functions in 5G cores further raise per-node capacity needs. Functional-safety and cybersecurity standards effectively double usable memory to accommodate redundancy and parity, reinforcing the case for moving up to larger HMC packages in control-plane equipment.

By Application: Processor Cache Leads, Industrial and IoT Edge Ramps Up

Processor cache usage accounted for 36.25% of 2025 deployments, providing near-memory acceleration for multi-chip server processors. Industrial and IoT edge adoption is forecast to grow at a 20.15% CAGR, as deterministic real-time workloads in factory automation and smart grid nodes require microsecond responses under harsh conditions. Data-buffer applications in storage controllers and network interface cards select Hybrid Memory Cube for queue-depth reduction, while graphics-driven systems in professional visualization leverage its bandwidth for detailed rendering.

As DDR5 narrows the bandwidth-per-pin gap, cache-oriented use cases will stabilize; however, edge-node deployment of AI analytics will sustain incremental volume growth. The advent of PCIe 5.0 and CXL 2.0 exposes memory-semantic interfaces where packetized protocols align neatly with HMC capability. Cybersecurity standards such as IEC 62443 consume extra bandwidth for secure boot and runtime attestation, indirectly boosting demand for high-bandwidth memory modules.

By Technology Node: TSV Gen 2 Leads, Optical Interconnect Gains Momentum

TSV-based Gen 2 designs held a 47.35% share in 2025 owing to supply maturity at Samsung, SK hynix, and Micron. Optical-interconnect variants are tracking a 19.28% CAGR as silicon photonics integrates more efficiently and lowers crosstalk in rack-scale disaggregated designs. Chiplet-oriented Hybrid Memory Cube devices offer a cost-efficient middle ground for mid-bandwidth applications that do not require full TSV throughput.

GPU accelerators have historically driven TSV growth; however, the emerging optical baseline may redefine package-level performance by reducing latency and lowering power per bit. Intel’s Falcon Shores integrates optical links to connect memory dies across a package boundary, signifying a production shift toward photonic methodologies. UCIe ratification reduces interface uncertainty and encourages multi-vendor chiplet ecosystems. Sustainability frameworks reward lower energy profiles, benefiting optical nodes that deliver and support regulatory compliance objectives across major regions.

Geography Analysis

The Asia Pacific delivered 41.05% of the hybrid memory cube market revenue in 2025 and is projected to grow at a 19.93% CAGR to 2031, driven by concentrated fabrication capacity at Samsung and SK hynix, as well as pro-semiconductor policies in China, Japan, South Korea, and India. The Chinese government's funds, totaling CNY 15 billion in 2024, target domestic stacked-memory innovation, while Japanese co-investment supports chiplet packaging through 2-nm nodes. Indian hyperscalers are drafting regional language AI models that require high-bandwidth memory, advancing in-country demand. Taiwan’s wafer-level packaging expansions further anchor the region as a hub for heterogeneous integration services.

North America represented 28.35% of 2025 revenue, driven by hyperscale cloud refresh cycles and the Department of Energy's exascale programs. Intel’s USD 20 billion Ohio expansion will house advanced packaging lines to embed Hybrid Memory Cube dies directly into Xeon and GPU assemblies. Amazon Web Services, Microsoft Azure, and Google Cloud all pilot disaggregated memory fabrics that pool high-bandwidth tiers across racks, a model that maximizes utilization while controlling per-server costs. Canada’s Vector and Mila institutes deploy HMC-based clusters to underpin national AI research goals. Export controls restricting advanced memory shipments reshape supply allocation patterns and drive onshore capacity investments.

Europe captured approximately 17.65% of the 2025 revenue, driven by the adoption of automotive ADAS and the installation of EuroHPC supercomputers. German tier-ones Bosch and Continental incorporated Hybrid Memory Cube into Level 3 perception platforms to meet stringent latency budgets. The region’s sovereign cloud push requires GDPR-compliant configurations, which in turn need encryption-friendly memory architectures. Arm expanded a coherent interconnect IP portfolio in 2024 to support European automotive and edge customers, underscoring local R&D momentum. The EU Chips Act funnels EUR 43 billion to double the regional semiconductor share, part of which finances advanced packaging for stacked memory lines.

Regulatory Landscape

Export controls and industrial policy are shaping the addressable supply base for stacked-memory products used in advanced computing programs. In the United States, the Bureau of Industry and Security (BIS) updated its license review policy on January 15, 2026 for advanced computing commodities, using technical performance parameters such as a 6,500 GB/s bandwidth threshold. This affects how high-bandwidth memory configurations are classified for restricted end uses and destinations.

In Europe, semiconductor capacity and advanced packaging for stacked memory are covered under the European Commission's 2026 Chips Act 2.0 proposal and related Council documentation. The framing emphasizes secure supply chains and scaling manufacturing capability. Alongside industrial policy, materials and process compliance obligations, including EU RoHS-related substance restrictions referenced in the report context as a process-chemistry constraint, add qualification complexity for TSV-based 3D integration and can extend time-to-volume for new package chemistries.

Value Chain Analysis

The value chain covers DRAM wafer fabrication, TSV formation and wafer thinning, die stacking and bonding, logic-base-die integration, advanced packaging and assembly, module test and qualification, and system-level integration by server, storage, and accelerator OEMs. Upstream, the ecosystem is concentrated in vertically integrated memory manufacturers and leading-edge packaging capacity, where yield and thermal-management constraints in TSV processes remain major cost and throughput bottlenecks.

Downstream demand is pulled by hyperscale datacenters, enterprise storage vendors, HPC programs, and automotive and industrial compute platforms that prioritize deterministic latency and bandwidth. A notable shift in the chain is the pivot from legacy HMC-specific roadmaps to broader high-bandwidth stacked-memory programs: Micron discontinued its HMC product line in 2018 and has since oriented high-performance memory toward alternatives such as HBM, concentrating investment and partner alignment on advanced packaging flows rather than reviving standalone HMC supply.

Competitive Landscape

Three vertically integrated suppliers, Samsung, SK hynix, and Micron, hold more than 70% of Hybrid Memory Cube capacity, yet new entrants leverage chiplet design and optical-interconnect IP to challenge legacy incumbents. Samsung leads in optical-interconnect prototypes that embed silicon photonics with stacked dies, reducing latency by 30% compared to electrical links. Micron secured a USD 6.1 billion CHIPS Act grant to expand U.S. production, improving supply diversity. SK hynix is investing USD 4 billion to add TSV capacity, signaling confidence in the rising demand for AI accelerators.

Intel’s acquisition of photonic IP and its integration into Falcon Shores GPUs introduces a new avenue of memory supply for accelerator products. Rambus licenses high-speed serializer-deserializer blocks to chiplet designers, enabling fabless firms to incorporate HMC interfaces without analog design overhead. Cadence tools accelerate time-to-market by simulating thermal and signal integrity in 3-D packages, lowering the engineering barrier for second-tier vendors. White-space opportunities lie in automotive ADAS and industrial IoT, domains that require functional safety certification, where established DRAM vendors have limited expertise.

Technology roadmaps reveal fast iteration cycles: Samsung is sampling 36 GB optical HMC modules, Intel is staging photonic Falcon Shores for 2026, and AMD plans EPYC chiplet processors with integrated high-bandwidth memory samples in late 2025. Standardization around UCIe and ongoing JEDEC HBM4 work is expected to blur lines between stacked DRAM families and packetized Hybrid Memory Cube, possibly expanding the overall high-bandwidth memory TAM. Suppliers that secure cross-licensing agreements and align with emerging automotive cybersecurity standards will gain meaningful differentiation.

Hybrid Memory Cube Industry Leaders

Micron Technology Inc.

Intel Corporation

Samsung Electronics Co., Ltd.

SK hynix Inc.

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace clusters around designs that reuse the packetized, stacked-memory concepts of Hybrid Memory Cube while fitting with current chiplet and disaggregated-server architectures. UCIe standardization, finalized in 2024 per the report context, reduces interface uncertainty for multi-vendor chiplet ecosystems and supports memory-semantic fabrics where HMC-like packet protocols align with PCIe 5.0 and CXL 2.0 platforms.

Public and corporate programs that subsidize advanced packaging and domestic capacity also create entry points for suppliers and ecosystem partners that can deliver qualified 3D-stacked memory at scale. Evidence in the report context includes the European Commission's 2026 Chips Act 2.0 proposal and the United States BIS January 2026 policy update, both of which use explicit performance thresholds for advanced computing commodities and raise the bar for compliance-grade product definition and traceability. At the same time, technical constraints highlighted in the report context, including sub-85% TSV yields and thermal complexity, leave room for process, test, and packaging improvements, such as enhanced redundancy schemes, thermal-aware design flows, and tighter integration between EDA simulation and package qualification, to broaden deployments beyond premium HPC and storage niches.

Recent Industry Developments

- July 2026: Intel-related disclosures around Cross-Batch Memory (XBM) surfaced via a patent publication, outlining an alternative high-performance memory approach aimed at bandwidth and cost constraints. The work points to continued architectural experimentation around stacked and near-memory concepts as vendors look for ways beyond conventional interfaces and packaging bottlenecks.

- October 2025: Samsung Electronics began mass production of 36 GB optical-interconnect memory packages at Pyeongtaek, citing 30% lower latency than electrical SerDes equivalents. This move takes optical links from prototype toward manufacturing and supports rack-scale disaggregated designs that prioritize power-per-bit and latency determinism.

- June 2024: The Universal Chiplet Interconnect Express (UCIe) standard was finalized, establishing common electrical, protocol, and mechanical specifications for die-to-die connectivity. A clearer interoperability baseline reduces vendor lock-in for heterogeneous integration programs and supports broader attachment of stacked-memory devices within multi-die packages.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the hybrid memory cube market is defined as the revenue earned from selling hybrid memory cube (HMC) devices and related modules that deliver high bandwidth, stacked-memory performance for computing and networking workloads.

Scope exclusions: We exclude conventional DRAM modules, standalone HBM products, and non-HMC advanced packaging services when they are not sold as part of an HMC offering.

Segmentation Overview

- By End-User Industry

- Enterprise Storage

- Telecommunications and Networking

- High-Performance Computing

- Automotive ADAS

- Other End-User Industry

- By Memory Capacity

- 2 GB–8 GB

- 8 GB–16 GB

- 16 GB–32 GB

- Above 32 GB

- By Application

- Processor Cache

- Data Buffer

- Graphics Memory

- Industrial / IoT Edge

- By Technology Node

- TSV-based Hybrid Memory Cube (Gen 2)

- Optical-interconnect HMC

- Chiplet-based HMC

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and to anchor a few measurable signals that can be tracked consistently year to year. We relied on public materials such as US SEC filings, annual reports, and investor presentations to understand product roadmaps, end-market exposure, and shipment timing.

To support the input assumptions, we also reviewed non-paywalled sources such as semiconductor trade statistics (where available through customs and trade portals), government industry datasets, standards and technical references from bodies such as JEDEC, and peer-reviewed papers that describe memory stacking, TSV yields, and bandwidth benchmarks. Patent databases were used to sense where active development is taking place and which architecture themes are getting more filings. A paid subscription for company financials and a separate paid patent database were also used as supporting references for cross-checking. These desk research sources are illustrative, and many other public documents and references were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured surveys with people involved in memory design, component sourcing, system integration, and demand planning across compute, networking, and storage use cases. Since this is a global market, we covered viewpoints from APAC, EMEA, and the Americas so assumptions on adoption timing and pricing direction were not driven by a single region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 21% | APAC: 45% |

| Mid tier: 46% | Functional/Unit leaders: 37% | EMEA: 34% |

| Smaller Players: 22% | Managers: 42% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where the addressable demand pool is reconstructed from compute and networking workloads that require very high memory bandwidth, and then filtered through expected HMC attach rates by platform type. To keep it grounded, the totals were then checked using selective bottom-up approximations, such as sampling typical ASP ranges and aligning them with plausible unit volumes by application.

The model used a small set of practical inputs, including expected HMC adoption by end-user industry (for example, high-performance computing and enterprise storage), average capacity mix shifts (2 to 8 GB, 8 to 16 GB, and higher), pricing progression as yields improve, technology shifts across TSV-based HMC variants, and regional demand weighting where APAC manufacturing and integration activity is stronger. When inputs were not directly observable, gaps were handled by using ranges from interviews and then stress-testing the impact on totals.

Forecasts were produced using scenario analysis supported by short time-series smoothing for pricing and adoption curves, and then the scenario weights were adjusted based on expert consensus on supply readiness and design-in cycles. This kept the forecast simple enough to be repeated each year with the same set of traceable assumptions.

Data Validation & Update Cycle

Validation was done by cross-checking model outputs against independent signals, including shipment timing cues from public product roadmaps, capacity and packaging constraints discussed in technical literature, and spend patterns inferred from company disclosures. Outliers were reviewed in multiple steps, and if a data point shifted the market materially, follow-up calls were triggered to confirm the underlying reason.

Reports are refreshed annually, and interim updates are made when major events change pricing, supply, or adoption timing. Before delivery, we perform a final pass to align the model with the latest public releases and to ensure the assumptions still match what participants are seeing in the field.

Mordor Intelligence's Hybrid Memory Cube Market Estimate Compared With Other Published Estimates

Published market sizes for hybrid memory cube can differ by a wide margin because firms do not always apply the same product boundary, base year, or pricing logic, and the forecast horizon can also change what looks like the current market. Differences also show up when one estimate leans on aggressive adoption curves while another waits for clearer design wins and supply readiness.

Key gap drivers in this market usually come from whether adjacent high bandwidth memory products are mixed into the count, how quickly ASPs are assumed to fall as yields improve, and whether demand is tied back to real workloads like HPC, networking, and enterprise storage. The spread is often amplified by currency timing, and then by refresh cadence, where older pages can miss recent capacity and integration signals captured in the latest checks applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.25 B (2025) | |

| Global Consultancy A | USD 5.71 B (2025) | A broader interpretation of the market is likely, where neighboring high bandwidth memory solutions and related stacked-memory revenue can be included alongside HMC, and adoption is extended faster across more end uses. |

| Industry Publisher B | USD 2.39 B (2025) | The number is close, but differences can come from using a narrower capacity or application mix, and from applying a different ASP path for 2025 based on alternate yield and supply assumptions. |

Overall, the table suggests that scope and pricing assumptions explain most of the variation, more than any single demand indicator does. By keeping the demand pool tied to HMC-specific use cases and by sanity-checking ASP and adoption timing with interviews, the resulting figure stays easier to trace and repeat when the model is updated.

Key Questions Answered in the Report

What is the projected value of the Hybrid Memory Cube market by 2031?

The market is forecast to reach USD 5.99 billion by 2031, reflecting a 17.73% CAGR from 2026.

Which end-user sector currently contributes the most revenue?

Enterprise storage led with 40.75% of 2025 revenue as hyperscalers refreshed all-flash arrays.

Which application segment is set to grow the fastest?

Industrial-and-IoT edge nodes are expected to expand at a 20.15% CAGR during 2026-2031.

Why is Asia Pacific the fastest-growing region?

Concentrated fabrication capacity, government incentives, and strong cloud buildouts drive a 19.93% regional CAGR.

What manufacturing challenge restricts near-term cost reductions?

TSV yield rates remain below 85%, elevating per-gigabyte cost by up to 60% over DDR5 modules.

How are chiplets influencing memory adoption?

UCIe-based chiplet standards let designers integrate Hybrid Memory Cube into multi-die packages without bespoke interfaces, speeding time-to-market.

Page last updated on: