Hyaluronic Acid Raw Material Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

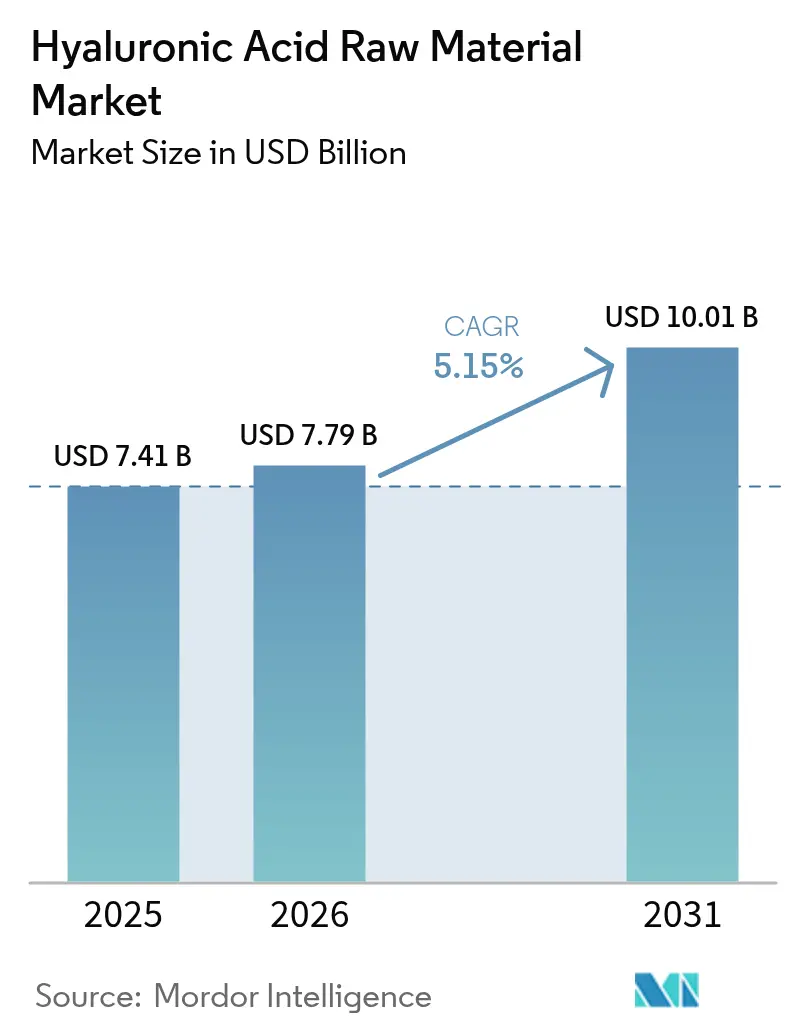

| Market Size (2026) | USD 7.79 Billion |

| Market Size (2031) | USD 10.01 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

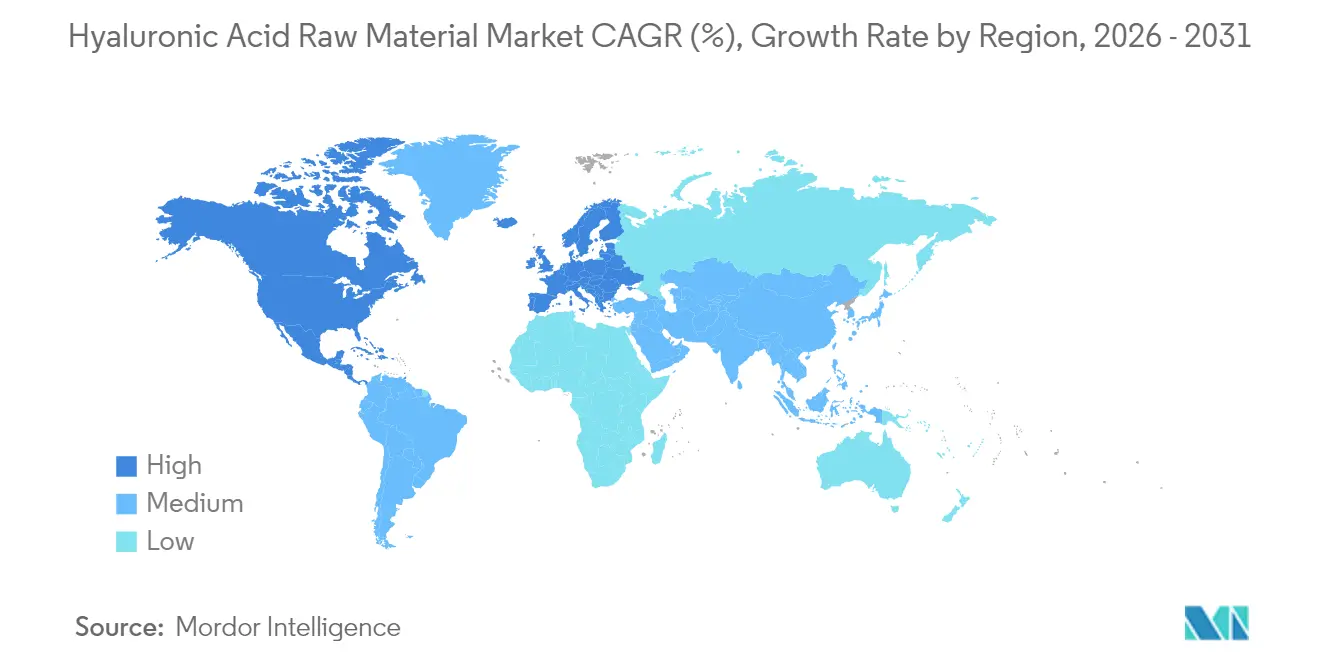

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

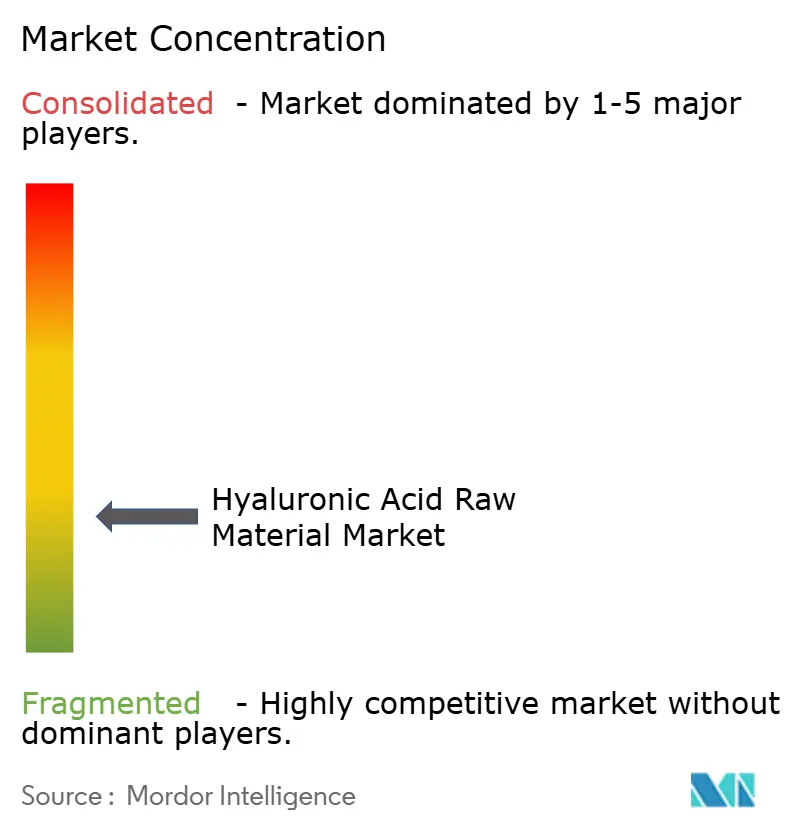

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hyaluronic Acid Raw Material Market Analysis by Mordor Intelligence

The hyaluronic acid raw material market size was valued at USD 7.41 billion in 2025 and estimated to grow from USD 7.79 billion in 2026 to reach USD 10.01 billion by 2031, at a CAGR of 5.15% during the forecast period (2026-2031). This consistent expansion is underpinned by maturing demand that now spans medical-grade viscosupplementation, ophthalmic devices, and advanced drug-delivery platforms alongside traditional dermal fillers. Regulatory validation of single-injection knee viscosupplementation, broadened anatomic indications for facial fillers, and insurance coverage expansions have collectively cushioned the market against the cyclicality typical of purely cosmetic products. Supply security initiatives adopted by vertically integrated manufacturers have reduced exposure to fermentation bottlenecks, while ongoing sustainability mandates spur investment in vegan-certified fermentation technologies. Strong clinical evidence supporting hyaluronic acid as a scaffold for tissue engineering further widens the addressable therapeutic base, positioning the hyaluronic acid raw material market for steady mid-single-digit growth through the decade.

Key Report Takeaways

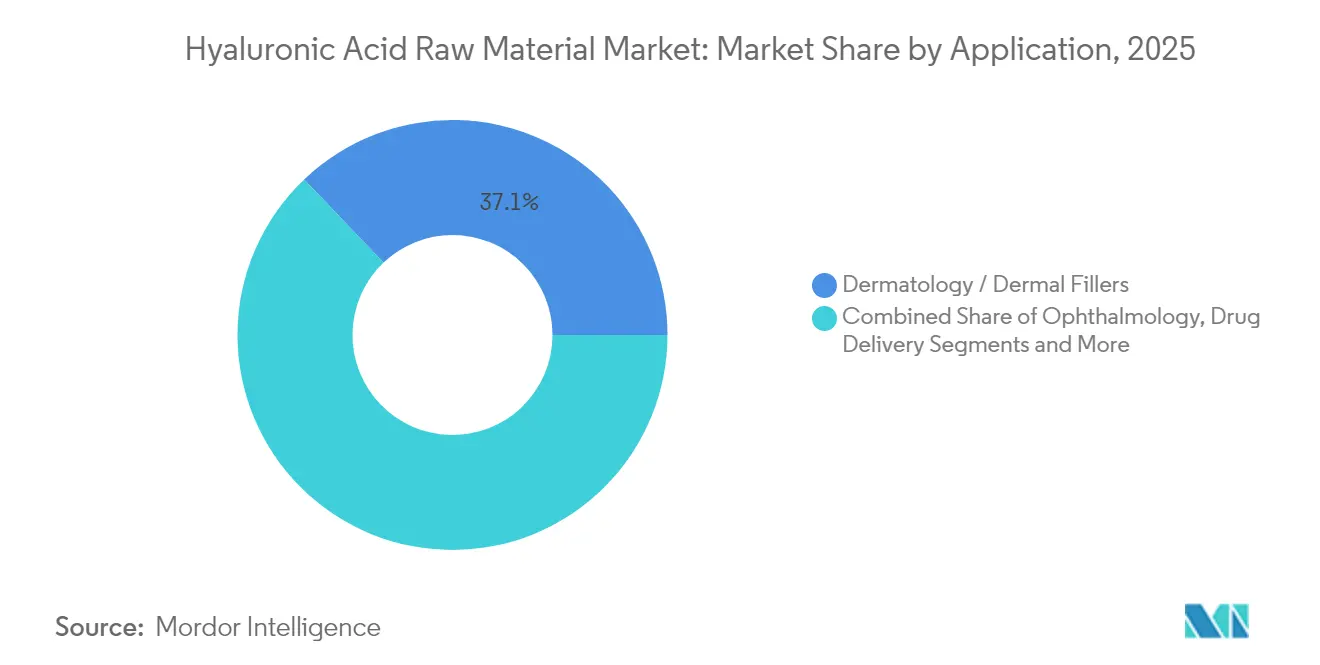

- By application, dermatology and dermal fillers accounted for 37.12% of hyaluronic acid raw material market share in 2025, while drug delivery is advancing at a 5.72% CAGR through 2031.

- By end user, hospitals held 42.38% share of the hyaluronic acid raw material market size in 2025, whereas cosmetic clinics are forecast to expand at a 6.08% CAGR over the same period.

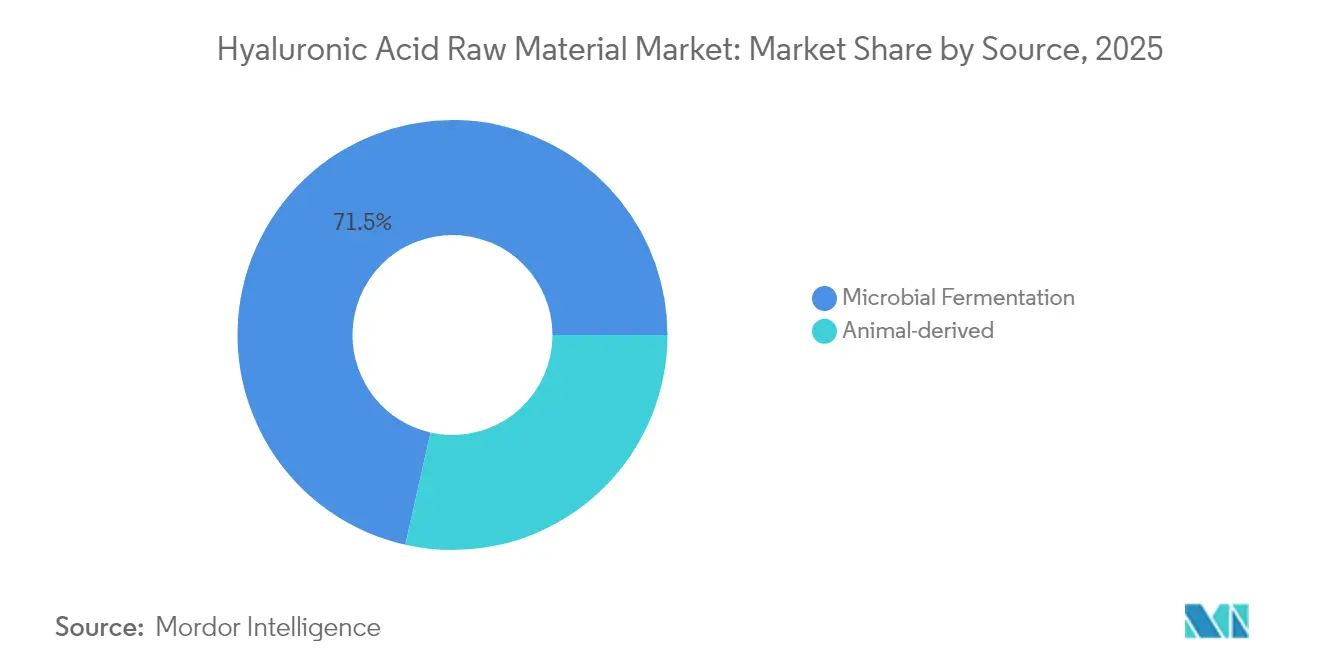

- By source, microbial fermentation commanded 71.48% of hyaluronic acid raw material market share in 2025, yet animal-derived material is registering a faster 5.85% CAGR to 2031.

- By geography, North America led with 43.10% revenue share in 2025; Asia-Pacific is set to grow at 6.28% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hyaluronic Acid Raw Material Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for anti-ageing & minimally invasive aesthetic solutions | +1.2% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Rapid growth of viscosupplementation in knee-osteoarthritis therapy | +0.9% | Global, strongest in Asia-Pacific | Long term (≥ 4 years) |

| Expanding ophthalmic applications | +0.7% | North America & EU leading; Asia-Pacific emerging | Medium term (2-4 years) |

| Shift toward fermentation-based, vegan-certified production | +0.5% | Global, driven by EU sustainability regulations | Long term (≥ 4 years) |

| Emergence of cross-linked dry-powder HA for improved shelf-life | +0.4% | Global manufacturing hubs, especially China & Europe | Short term (≤ 2 years) |

| Use of HA as bio-scaffold in 3-D bioprinting & tissue engineering | +0.3% | Research centers in North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Anti-Ageing and Minimally-Invasive Aesthetic Solutions

Preventative aesthetics have reshaped consumption patterns, with patients aged 25-35 accounting for one-third of new filler procedures in 2024, nearly double the 2019 level [1]Ioannis Peros, “Fibrotic Reaction to Hyaluronic Acid Fillers in the Face,” Journal of Cosmetic Dermatology, onlinelibrary.wiley.com. Broader anatomical approvals such as temple augmentation with JUVÉDERM VOLUMA XC increase treatment zones and elevate annual filler volumes per patient [2]AbbVie, “New Data Across Dermatology and Aesthetics Portfolios,” abbvie.com. Advanced cross-linking prolongs product residence time, permitting premium pricing that offsets reduced visit frequency. Social-media normalization of subtle refinements reduces stigma and drives procedural uptake among professionals in finance, technology, and healthcare. The net effect is a younger, recurring client base that lessens seasonal revenue swings, reinforcing a predictable growth foundation for the hyaluronic acid raw material market.

Rapid Growth of Viscosupplementation in Knee-Osteoarthritis Therapy

Viscosupplementation now serves as a cost-saving bridge delaying total knee arthroplasty by roughly 12 months, thereby lowering healthcare expenditures. Single high-molecular-weight injections have demonstrated non-inferiority to multiple low-dose regimens, cutting visit burden and boosting adherence. Expanded insurance coverage makes therapy accessible to seniors on fixed incomes, particularly in Asia-Pacific where aging demographics lift osteoarthritis prevalence. Novel formulations that combine hyaluronic acid with polynucleotides or niacinamide deliver superior pain relief, signaling a premium shift from commodity viscosupplements. Widespread adoption of ultrasound-guided protocols enhances placement precision and safety, enabling general orthopedists and rheumatologists to offer injections without referral to specialized centers.

Expanding Ophthalmic Applications

FDA clearance of Lacrifill Canalicular Gel in 2024 repositioned hyaluronic acid from symptomatic eyedrop ingredient to semi-permanent device that occludes tear drainage for up to six months. Cross-linked ocular gels demonstrate superior corneal healing post-surgery compared with unmodified tears. Riboflavin-conjugated drops mitigate UV-induced oxidative stress, broadening prophylactic applications. Combination products containing 0.001% hydrocortisone sodium phosphate target para-inflammation, addressing causal pathways rather than masking dryness. As reimbursement frameworks evolve, ophthalmologists increasingly view hyaluronic acid as a device-grade solution, supporting premium pricing strategies that enhance revenue per procedure.

Shift Toward Fermentation-Based, Vegan-Certified Production

Global cruelty-free mandates have accelerated the pivot from animal-derived inputs to microbial fermentation, with vegan badges becoming procurement prerequisites for European retailers. Engineered Streptococcus zooepidemicus strains now yield customizable molecular weights at higher volumetric productivity, lowering cost per kilogram despite stringent purity targets. ECOCERT and COSMOS certifications provide access to premium personal-care tiers, while marine by-product fermentation media underscores a circular-economy narrative attractive to investors. Photosynthetic production using engineered cyanobacteria offers a carbon-negative roadmap, but commercialization remains a mid-decade prospect.

Emergence of Cross-Linked Dry-Powder HA for Improved Shelf-Life

Dry-powder hyaluronic acid technology extends shelf stability from 18 to 36 months at ambient temperature, trimming cold-chain costs that can add 10-15% to landed product prices. Chinese and European manufacturing hubs have moved first, leveraging high-shear spray-drying to preserve molecular integrity. Clinics in emerging markets welcome room-temperature storage, which minimizes wastage associated with power outages. Powders reconstitute on-site into viscosupplements or filler gels, supporting decentralized compounding models that can customize concentration. Early-stage data suggest equivalent viscoelastic properties to pre-filled syringes, positioning dry-powder formats as a strategic hedge against logistic disruptions.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High product cost & price volatility of pharmaceutical-grade HA | -1.4% | Global, especially emerging markets | Medium term (2-4 years) |

| Adverse reactions and regulatory scrutiny on injectable fillers | -0.8% | North America & EU with strict oversight | Short term (≤ 2 years) |

| Supply-chain risk from limited fermentation capacity in China | -0.6% | Global, Asia-Pacific most vulnerable | Short term (≤ 2 years) |

| Environmental concerns over solvent-intensive cross-linking | -0.3% | EU & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Product Cost and Price Volatility of Pharmaceutical-Grade HA

Medical-grade hyaluronic acid commands raw-material prices ranging from USD 2,000 to USD 60,000 per kg, depending on molecular weight and endotoxin limits. Limited fermentation capacity for ultra-high-molecular-weight streams leads to supply–demand imbalances and spot price spikes exceeding 25% within a quarter. Quality-assurance testing—including endotoxin, protein, and nucleic-acid assays—adds 15-20% to production expenses relative to cosmetic grades. Dual sourcing from animal tissues remains necessary for certain therapies, but premium pricing elevates input cost for manufacturers that must maintain redundant supply chains. Small-to-mid-size firms often lack the purchasing power to secure long-term contracts, amplifying exposure to price swings that compress margins and inhibit R&D investment.

Adverse Reactions and Regulatory Scrutiny on Injectable Fillers

Post-market surveillance recorded nodules in 71.8% of delayed adverse filler reactions, prompting regulators to tighten labeling and training standards. The EU Medical Devices Regulation lengthened approval timelines, elevating compliance costs that disproportionately hit small innovators. Consensus guidelines now recommend extended patient monitoring, raising clinic overhead and malpractice premiums. Media amplification of rare granulomatous events undermines consumer confidence, particularly in first-time patients. Although hyaluronidase reversibility reassures practitioners, the requirement to stock reversal agents increases inventory burdens.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Medical Therapeutics Drive Premium Growth

Drug-delivery systems generated the fastest 5.72% CAGR through 2031 as formulators exploit CD44 receptor targeting to enhance chemotherapeutic payload concentration. This momentum steers the hyaluronic acid raw material market toward specialized therapeutics with longer product-development cycles and higher regulatory barriers. Dermatology and dermal fillers retained 37.12% of 2025 revenue, demonstrating the segment’s resilience amid broadening anatomic indications and safety upgrades.

Dermatology remains central to consumer awareness; however, sustained investments in oncologic, orthopedic, and ophthalmic indications diversify the revenue mix. Orthopedic viscosupplementation shifts toward single-injection formats, illustrating demand for convenience and reduced clinic visits. Ophthalmic pipelines add structural treatments that command premium reimbursement. Cross-therapeutic synergies—from drug-eluting gels to regenerative scaffolds—support pricing power and lengthen product life cycles, enabling manufacturers to amortize R&D costs across multiple indications.

By End User: Cosmetic Clinics Accelerate Market Democratization

Hospitals maintained 42.38% share of the hyaluronic acid raw material market size in 2025 due to their dominance in surgical and high-acuity interventions. Yet cosmetic clinics will expand at 6.08% CAGR to 2031, underscoring a democratized aesthetic ecosystem where nurse injectors, physician assistants, and qualified dentists offer advanced procedures. Portable ultrasound devices facilitate precise filler placement in non-hospital settings, improving outcomes and bolstering patient confidence.

Multi-modality treatment suites that combine radiofrequency microneedling with hyaluronic acid boosters attract clients seeking comprehensive rejuvenation. Medical spas deploy point-of-care diagnostics—such as skin hydration mapping—to personalize regimens, reinforcing client loyalty. Hospitals increasingly collaborate with outpatient partners, referring lower-acuity cases to clinics while focusing on complex surgeries, thus optimizing resource utilization across the care continuum.

By Source: Sustainability Drives Production Innovation

Microbial fermentation claimed 71.48% hyaluronic acid raw material market share in 2025, underlining its scalability and compliance with vegan labeling requirements. Engineered fermentation achieves precise molecular-weight tailoring, granting formulators flexibility without animal-origin concerns.

Animal-derived hyaluronic acid is growing at 5.85% CAGR, largely because niche orthopedic and ophthalmic applications value its reproducible bioactivity. High-purity rooster-comb extracts offer molecular-weight uniformity prized for single-injection viscosupplements. Firms hedge against ethical objections by maintaining dual supply lines, ensuring availability should fermentation capacity tighten. Emerging marine by-product substrates promise cost efficiency and circular-economy appeal, signalling that innovation will target both ecological credentials and functional performance.

Geography Analysis

North America led with 43.10% revenue in 2025, supported by entrenched reimbursement frameworks for viscosupplementation and high adoption of premium fillers. Favorable FDA pathways encourage quick scaling of novel ophthalmic and orthopedic devices.

Asia-Pacific will post the fastest 6.28% CAGR through 2031 as regulators harmonize standards and middle-class consumers embrace minimally invasive aesthetics. China’s NMPA approval of the Algeness VL filler in 2024 illustrates regulatory openness to differentiated formulations . Japan’s universal healthcare coverage of viscosupplementation further enlarges the therapeutic base.

Europe remains a sustainability vanguard, rewarding vegan-certified and solvent-free manufacturing. Strict MDR regimes favor incumbents with mature quality systems, reinforcing competitive moats. South America shows upticks linked to economic stabilization, while Middle Eastern markets leverage medical tourism. Africa’s nascent demand gains momentum as urban clinics adopt cost-effective dry-powder fillers that circumvent cold-chain gaps.

Competitive Landscape

The hyaluronic acid raw material market features moderate fragmentation, with top-tier producers leveraging multi-decade GMP expertise, broad regulatory dossiers, and global distribution. Bloomage Biotechnology capitalizes on scale, offering molecular-weight-specific portfolios and raw-material-to-finished-product integration. AbbVie’s Allergan Aesthetics division fortifies its franchise by expanding anatomical approvals, thus deepening clinical penetration.

Mid-size biotechnology firms pursue niche leadership through patents on cross-linking chemistries and hybrid high-/low-molecular-weight complexes. IBSA and Altergon’s ultrapure injectable formulation showcases university–industry collaboration that accelerates innovation cycles. Strategic partnerships allow pharma companies to tap fermentation specialists while sharing regulatory risk.

As key patents near expiration in 2026-2028, price competition will intensify in commodity dermal fillers, but differentiation via combination therapies and device-drug hybrids will protect margins. The looming transition toward carbon-negative fermentation may redraw cost curves, rewarding early movers who internalize sustainability as a core competency.

Hyaluronic Acid Raw Material Industry Leaders

Zimmer Biomet

Lifecore Biomedical, LLC

Anika Therapeutics, Inc

Sanofi

AbbVie, Inc. (Allergan)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Bloomage Biotech’s Hymagic-4D hyaluronic acid marked four years of sustained market momentum, spawning derivative 5D, 6D, and 7D products that shift the company toward turnkey solution provision.

- April 2023: IBSA and Altergon, in partnership with Luigi Vanvitelli University of Naples, unveiled an ultrapure biofermentative hyaluronic acid for injectable use, employing thermal processing to create hybrid molecular-weight complexes.

Global Hyaluronic Acid Raw Material Market Report Scope

As per the scope of the report, hyaluronic acid is naturally present in the human body and can be found in high concentrations in the eyes and joints. It acts as a cushion and lubricant in the joints and other tissues. Hyaluronic acid raw materials are the substances used for the manufacturing of the natural compound. Sodium hyaluronate raw material provides excellent performance in a wide range of products, including lotions, creams, shampoos, skin gels, and other products, due to which it is widely used in various cosmetic and medical procedures.

The hyaluronic acid raw material market is segmented by application (orthopedics, ophthalmology, drug delivery, dermatology, and other applications), end user (hospitals, cosmetic clinics, and Other End Users), and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Orthopedics (Viscosupplements) |

| Ophthalmology |

| Drug Delivery |

| Dermatology / Dermal Fillers |

| Other Applications |

| Hospitals |

| Cosmetic Clinics |

| Other End Users |

| Animal-derived |

| Microbial Fermentation |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Orthopedics (Viscosupplements) | |

| Ophthalmology | ||

| Drug Delivery | ||

| Dermatology / Dermal Fillers | ||

| Other Applications | ||

| By End User | Hospitals | |

| Cosmetic Clinics | ||

| Other End Users | ||

| By Source | Animal-derived | |

| Microbial Fermentation | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Hyaluronic Acid Raw Material Market size?

The hyaluronic acid raw material market size reached USD 7.79 billion in 2026 and is forecast to climb to USD 10.01 billion by 2031 at a 5.15% CAGR.

Which application is growing fastest?

Drug-delivery systems lead growth, expanding at a 5.72% CAGR as pharmaceutical firms harness hyaluronic acid’s receptor-targeting capability for precision therapeutics.

What drives Asia-Pacific demand?

Harmonized regulations, rising disposable income, and broader acceptance of minimally invasive aesthetics underpin a 6.28% CAGR in Asia-Pacific through 2031.

Why are cosmetic clinics gaining share?

Enhanced safety protocols and portable imaging technologies enable qualified non-physician injectors to offer advanced treatments, pushing clinic revenue up at 6.08% CAGR.

Page last updated on: