Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

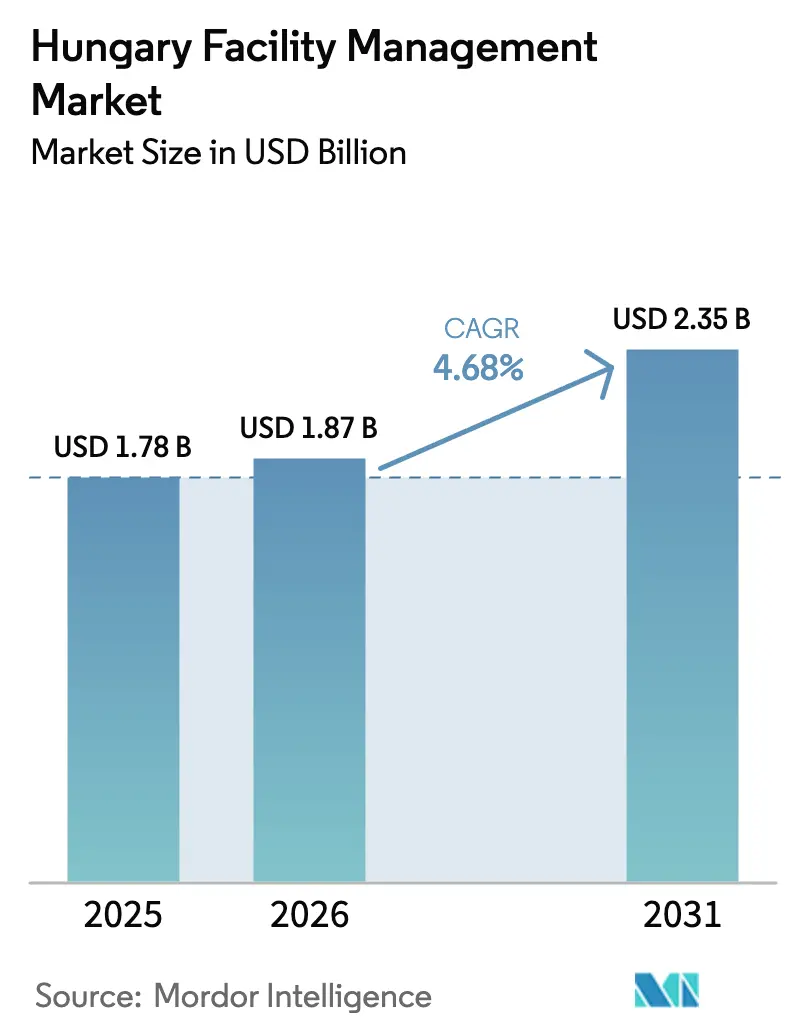

| Base Year Market Size (2025) | USD 1.78 Billion |

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.35 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

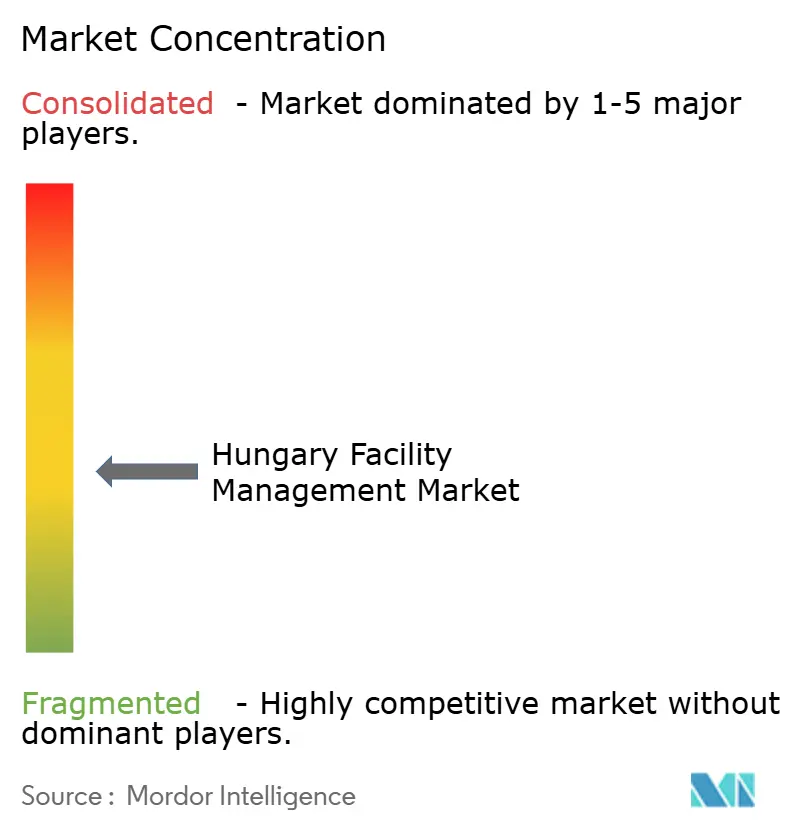

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hungary Facility Management Market Analysis by Mordor Intelligence

The Hungary facility management market size is expected to increase from USD 1.78 billion in 2025 to USD 1.87 billion in 2026 and reach USD 2.35 billion by 2031, growing at a CAGR of 4.68% over 2026-2031. Momentum stems from the country’s emergence as Central Europe’s logistics crossroads, the build-out of gigafactories, and a widening retrofit program that aligns with the European Union’s tighter energy-performance rules. Rising real wages, up 9.2% in 2024, are narrowing the historical cost gap with Western Europe, nudging providers toward automation and integrated contracts. Multinational occupiers now embed facility managers during design on 83% of Budapest’s new office projects, compressing bid cycles and lifting technical requirements. The revised Energy Performance of Buildings Directive is also channeling Recovery and Resilience Facility money into deep retrofits, anchoring multi-year pipelines that prize firms able to combine energy audits, HVAC optimization, and turnkey monitoring.

Key Report Takeaways

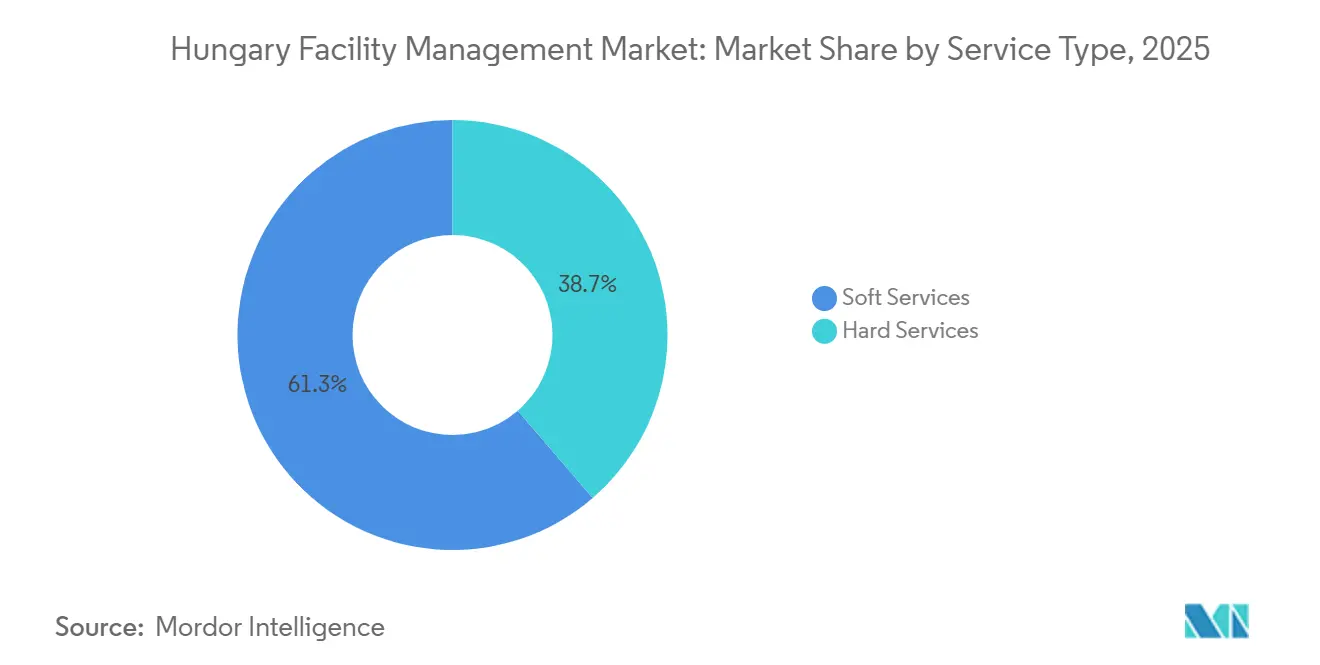

- By service type, soft services led with a 61.31% share of the Hungary facility management market size in 2025, while hard services are projected to expand at a 4.87% CAGR through 2031.

- By offering type, outsourced models commanded 57.41% of the Hungary facility management market share in 2025 and are forecast to grow at a 4.73% CAGR to 2031.

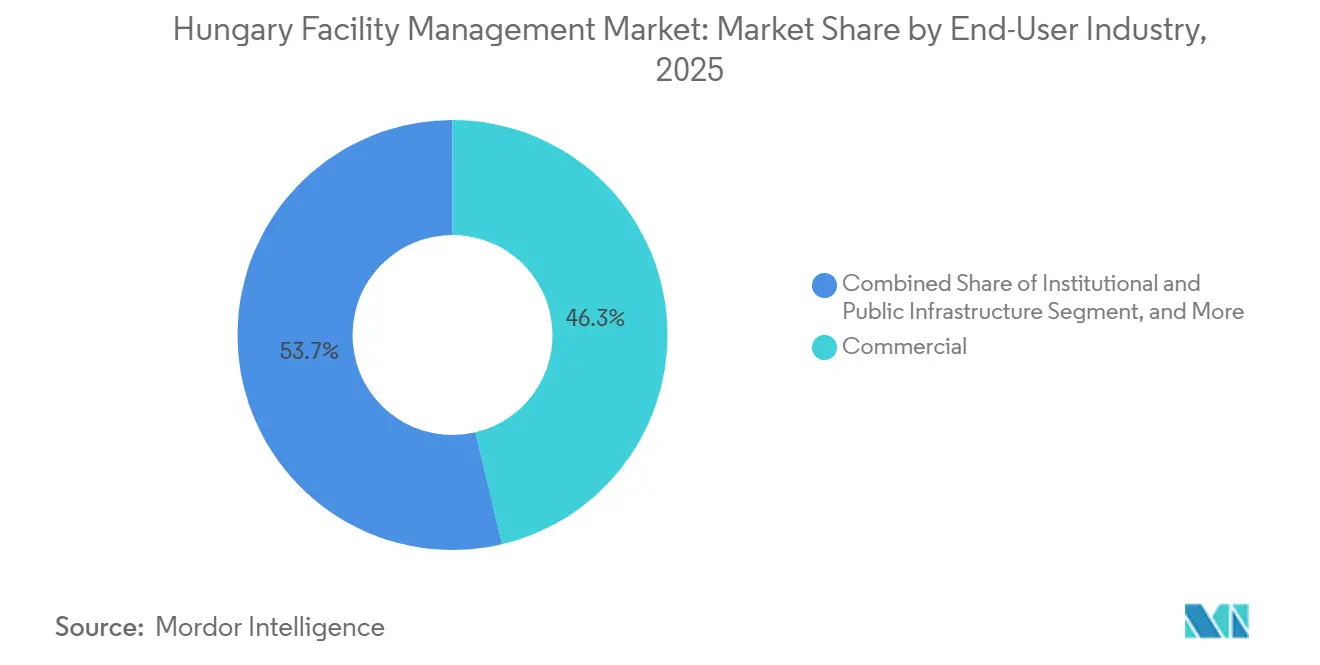

- By end-user vertical, commercial facilities captured 46.31% revenue share in 2025, whereas healthcare is advancing at a 5.06% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hungary Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and Population Growth in Budapest and Key Metros | +0.8% | Budapest, Debrecen, Győr, Szeged | Medium term (2-4 years) |

| EU-Funded Building Renovation Wave and Energy-Efficiency Mandates | +1.2% | National, concentrated in Budapest and regional capitals | Long term (≥ 4 years) |

| Corporate ESG Reporting Mandates Elevating Green KPI Services | +0.9% | National, early adoption in Budapest multinationals | Medium term (2-4 years) |

| Logistics and EV-Battery Investments Fueling Technical FM Demand | +1.5% | Debrecen, Győr, Kecskemét, Szeged industrial corridors | Short term (≤ 2 years) |

| Low Smart-Meter Penetration Creating Retrofit BEMS Opportunities | +0.6% | National, urban office and industrial clusters | Long term (≥ 4 years) |

| Build-to-Suit Leasing Surge Integrating FM Early in Project Cycles | +0.7% | Budapest, Pest County, logistics hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urbanization and Population Growth in Budapest and Key Metros

Budapest’s modern office stock stood at 4.46 million m² at end-2024, with vacancy falling to 14.13% as regional headquarters consolidate. This white-collar clustering stimulates scalable soft services, yet unemployment below 4.5% forces providers to compete with hospitality and retail for labor.[1]ESTON International, “Budapest Office Market Report H2 2024,” eston.hu Debrecen and Győr are rising as industrial magnets; BMW and CATL alone will employ thousands, lifting demand for on-site catering, shuttle logistics, and 24-hour technical standby. Tourism’s rebound could add another 23,000-49,000 jobs by 2030, further tightening staff availability. Wage differentials mean Budapest salaries run roughly 50% above the national average, incentivizing automation and digital work-order systems that favor large, capitalized FM firms.

EU-Funded Building Renovation Wave and Energy-Efficiency Mandates

The EPBD 2024/1275 obliges Hungary to renovate 16% of worst-performing non-residential space by 2030 and 26% by 2033. Facility managers that can package energy audits, HVAC redesign, and on-site renewables into single contracts stand to secure multi-year revenue streams. Upcoming digital logbooks and smart-readiness indicators will drive IoT sensor roll-outs; Siemens’ Desigo deployments have shown potential energy savings of up to 45% in lighting alone.[2]Siemens, “Smart Hungary 2025 - Building Management Systems Report,” siemens.com Smart-meter penetration below 10% keeps the retrofit addressable market wide, while EU grants de-risk client capex, making performance-based agreements more attractive.

Corporate ESG Reporting Mandates Elevating Green KPI Services

Roughly 500 Hungarian companies entered the CSRD regime in the 2024 cycle, requiring auditable Scope 1-3 metrics. That shift transforms FM into a data engine; clients now seek providers capable of sub-metering, waste tracking, and carbon accounting. Futureal’s Budapest assets already combine BREEAM, WELL, and Access4You certifications, signaling mainstream uptake of green standards. ISO 14001 and ISO 45001 are rapidly becoming tender prerequisites, pushing non-certified vendors out of high-value frameworks.

Low Smart-Meter Penetration Creating Retrofit BEMS Opportunities

With less than 10% of buildings equipped with advanced meters, most owners lack granular energy visibility.[3]Hungarian Energy and Public Utility Regulatory Authority, “Energy Market Statistics,” mekh.hu The EPBD’s smart-readiness metric and planned digital building logbooks will accelerate adoption of building energy-management systems. Reliable sub-metering also underpins ESG reporting, creating cross-sell potential between compliance services and hard-service maintenance. Early movers are packaging metering with cloud analytics and demand-response integration, positioning for annuity-style monitoring fees.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortage Escalating Wage Costs | -0.9% | National, acute in Budapest and industrial hubs | Short term (≤ 2 years) |

| Volatile Utility Prices Threatening Energy-Management Contracts | -0.7% | National, industrial users most exposed | Short term (≤ 2 years) |

| Concentrated Public Procurement Curtailing FM Market Entry | -0.5% | National, government and state-owned entities | Long term (≥ 4 years) |

| Rising State Ownership Preferring In-house Facility Operations | -0.4% | National, strategic sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortage Escalating Wage Costs

Unemployment hovered near 4.5% in 2025 and real wages climbed 9.2% the prior year, eroding Hungary’s labor-cost advantage.[4]Hungarian Central Statistical Office, “Labour Market Statistics 2024-2025,” ksh.hu Minimum-wage hikes of 13% in 2026 add further pressure, with labor comprising up to 70% of soft-service costs. Emigration removes roughly 71,000 workers annually, and foreign-born talent represents only 7% of the population. The squeeze pushes FM firms toward autonomous cleaning robots and predictive maintenance that lower headcount; B+N’s in-house robot line exemplifies the approach.

Rising State Ownership Preferring In-house Facility Operations

State entities in energy, transport, and healthcare continue to re-insource non-core services, citing security and data-sovereignty concerns. Hospital groups benefitting from HUF 500 billion (USD 1.3 billion) modernization funding have maintained internal maintenance departments to preserve job numbers, delaying outsourcing adoption. As state ownership widens, integrated FM penetration could stall outside the private sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Gain on Technical Complexity

Hard services are projected to grow faster than the overall Hungary facility management market at a 4.87% CAGR thanks to gigafactories, data centers, and hospital retrofits that require precise MEP, HVAC, and fire-safety regimes. BMW’s Debrecen plant will rely on lithium-ion fire-suppression, stringent humidity control, and predictive vibration monitoring to safeguard high-voltage battery lines. CATL’s added 60,000 m² hall houses solvent-intensive coating processes demanding continuous air-quality tracking. Within soft services, autonomous cleaning robots and UV disinfection units introduced by B+N help counter wage inflation, while catering contracts benefit from revived office occupancy. Security is pivoting toward integrated platforms combining video analytics and cyber-defense of building networks, shifting margin pools from guards to technology upkeep.

Soft services still held 61.31% of the Hungary facility management market in 2025, underpinned by daily cleaning, catering, and reception that scale with footfall. However, rising minimum wages and tight labor supply weigh on margins. Meanwhile, the hard-service share grows as predictive maintenance, digital twins, and condition-based asset management move from pilot to mainstream. Energy-audit demand also routes revenue toward technical teams capable of heat-pump retrofits and photovoltaic upkeep, reinforcing the segment’s upward trajectory.

By Offering Type: Integrated FM Captures ESG-Driven Demand

Outsourced contracts accounted for 57.41% of the Hungary facility management market in 2025 and should expand at a 4.73% CAGR, led by integrated FM models that bundle technical, cleaning, catering, and sustainability data services. Vodafone Hungary’s multi-year IFM award to ISS consolidated four formerly separate vendors, illustrating clients’ drive to simplify governance while securing a single ESG data stream. JLL already manages 1.5 million m² locally with energy dashboards embedded, offering tenants CSRD-ready reporting. Build-to-suit projects that integrate FM early boost IFM adoption by locking in life-cycle cost optimization from day one.

In-house operations still dominate state-controlled entities, reflecting security sensitivities and legacy staffing structures. Yet wage inflation and compliance complexity are nudging public bodies toward piecemeal outsourcing, often cleaning and landscaping first, with technical services following as capital renewal bills mount. Bundled FM, while a bridge solution, still forces clients to manage multiple SLAs and struggles to generate integrated sustainability metrics, hastening the shift to full IFM.

By End-User Industry: Healthcare Leads Growth Amid Aging Demographics

Healthcare is the fastest-growing end-user, advancing at a 5.06% CAGR through 2031 as HUF 500 billion (USD 1.3 billion) in hospital overhaul funds flow into modernizations such as Szent László Hospital’s EUR 140 million (USD 158 million) rebuild. An aging population, median age 43.9 years with 20% over 65, elevates demand for outsourced cleaning, sterilization, and energy-efficient HVAC that improve infection control and lower operating costs. Sodexo has already deepened its healthcare footprint by partnering with Medicover and Affidea on private clinics, signaling room for specialized providers.

Commercial real estate remained the largest slice at 46.31% in 2025, supported by Budapest’s 4.46 million m² office base and occupancy recovery. Multinationals request WELL and BREEAM certifications, embedding energy-dashboard reporting into FM scopes. Industrial and logistics demand is growing in parallel with battery and e-commerce expansions, necessitating 24-hour technical standby, chemical handling, and environmental compliance. Hospitality, though smaller, is rebounding as RevPAR rises; hotels require linen logistics, guest-facing maintenance, and green energy management, diversifying FM revenue streams.

Geography Analysis

Budapest and Pest County generated roughly 55-60% of Hungary facility management market revenues in 2025, mirroring the capital’s concentration of grade-A offices, hotels, and cultural venues. Build-to-suit projects that embed FM teams at design stage compress procurement and push service innovation. Labor scarcity, with wages 50% above national norms, drives early adoption of autonomous cleaning units and digital twins, giving scale players an efficiency edge.

Debrecen is crystallizing into an industrial FM nexus anchored by BMW’s EUR 2 billion (USD 2.26 billion) plant and CATL’s EUR 7.34 billion (USD 8.29 billion) gigafactory. These facilities impose cleanroom standards and hazardous-material protocols unseen in legacy automotive sites, raising technical-service intensity. Győr and Kecskemét similarly benefit from Audi and Mercedes supply parks, while Szeged’s geothermal heating rollout will necessitate FM expertise in renewable heat networks.

Regional cities offer lower wage bills but grapple with talent leakage to Budapest or abroad. FM firms operating outside the capital must blend cost competitiveness with upskilling programs to secure and retain technical staff. Digital building logbooks mandated by the EPBD could level the playing field by standardizing performance data, enabling remote monitoring centers to service dispersed portfolios across Hungary.

Competitive Landscape

Global brands, CBRE, ISS, JLL, Sodexo, Compass Group, and VINCI, dominate cross-border integrated contracts, yet local champions such as B+N Referencia, Future FM, and WING leverage cultural fluency and public-sector familiarity. B+N’s January 2025 purchase of ISS’s CEE units added EUR 70 million (USD 79 million) turnover and 4,000 staff, vaulting the firm into the region’s top tier and signaling consolidation pressure on mid-sized incumbents.

Technology is the new battleground. First Facility’s roll-out of APFM-Systems’ AHD platform across 80-90% of projects automates fault ticketing and KPI dashboards, underpinning CSRD-ready reporting. Futureal’s developments embed FM during design to hit BREEAM and WELL targets, illustrating demand for early-stage advisory. Framework procurement still favors incumbents; 70% of government awards are single-bid, creating high switching costs and regulatory hurdles for foreign newcomers.

White-space opportunities lie in retrofit automation where smart-meter penetration is low. Proptech start-ups offer cloud-based CAFM and energy analytics that commoditize administrative functions, letting smaller FM firms compete on service quality rather than headcount. However, capital requirements for ISO certifications and advanced IoT infrastructure remain barriers to scale.

Hungary Facility Management Industry Leaders

CBRE Group

B+N Referencia Zrt

ISS Global

Future FM Zrt

Apleona GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TRIBE Budapest Airport opened a 167-room hotel near Budapest Liszt Ferenc International Airport, integrating BREEAM-aligned facility systems.

- April 2025: Hungary’s Parliament raised annual energy-saving obligations to 1.4%, expanding opportunities for energy-management specialists.

- April 2025: Hungary’s hotel sector posted a 17% year-on-year jump in revenue per available room for February 2025, with occupancy reaching 58.3%, signaling stronger demand for hospitality-focused facility services.

- January 2025: B+N Referencia acquired ISS Group’s Central and Eastern European subsidiaries, adding EUR 70 million (USD 79 million) in annual turnover and nearly 4,000 employees, making it one of the region’s largest providers.

Hungary Facility Management Market Report Scope

Hungary's facility management market is defined as facilities management encompassing various disciplines and services that maintain the operation, comfort, safety, and efficiency of the built environment, including buildings, infrastructure, and property. Facilities management encompasses a number of parameters, including operations and maintenance. FM includes services such as building maintenance, maintenance operations, utilities, waste services, security, and others.

The Hungary Facility Management Market Report is Segmented by Service Type (Hard Services including Asset Management, MEP and HVAC Services, Fire Systems and Safety, Other Hard Facility Management Services; Soft Services including Office Support and Security, Cleaning Services, Catering Services, Other Soft Facility Management Services), Offering Type (In-house, Outsourced including Single Facility Management, Bundled Facility Management, Integrated Facility Management), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

By Offering Type

| In-house | |

| Outsourced | Single Facility Management |

| Bundled Facility Management | |

| Integrated Facility Management |

By End-User Industry

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process |

| Other End-User Industries |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By Offering Type | In-house | |

| Outsourced | Single Facility Management | |

| Bundled Facility Management | ||

| Integrated Facility Management | ||

| By End-User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How fast is the Hungary facility management market expected to grow between 2026 and 2031?

The sector is projected to expand at a 4.68% CAGR over 2026-2031, climbing from USD 1.87 billion in 2026 to USD 2.35 billion by 2031.

Which service type is gaining share most quickly?

Hard services, driven by gigafactory and hospital retrofits, are rising at a 4.87% CAGR, outpacing the overall market.

Why are integrated FM contracts becoming more popular in Hungary?

Corporate ESG rules under the CSRD require consolidated energy, waste, and carbon data, encouraging clients to bundle services under single providers that can supply audited metrics.

Which end-user segment shows the fastest growth?

Healthcare leads with a 5.06% CAGR through 2031, supported by a USD 1.3 billion hospital modernization program and an aging population that raises non-clinical outsourcing demand.

What is the main restraint facing facility managers in Hungary?

A skilled labor shortage is pushing wage costs higher, squeezing margins for labor-intensive cleaning and security services.

How concentrated is the competitive landscape?

The top five companies control roughly 40-45% of revenues, indicating a moderately concentrated market where both global and local players coexist.

Page last updated on: