Humidity Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

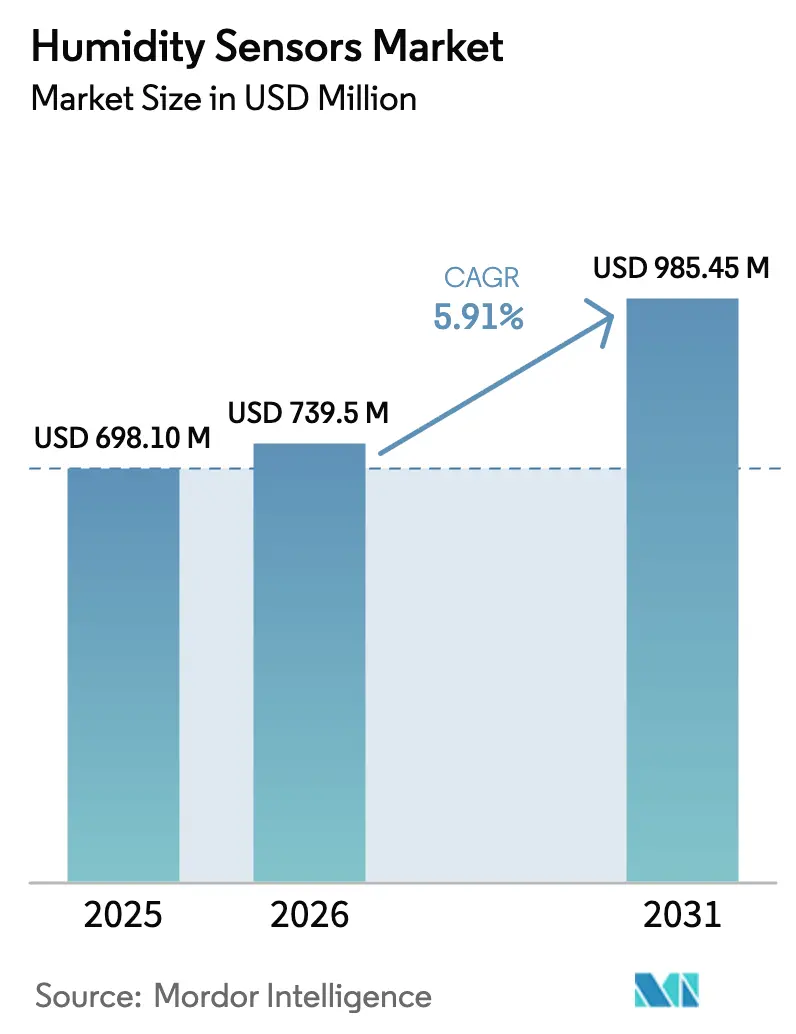

| Market Size (2026) | USD 739.5 Million |

| Market Size (2031) | USD 985.45 Million |

| Growth Rate (2026 - 2031) | 5.91% CAGR |

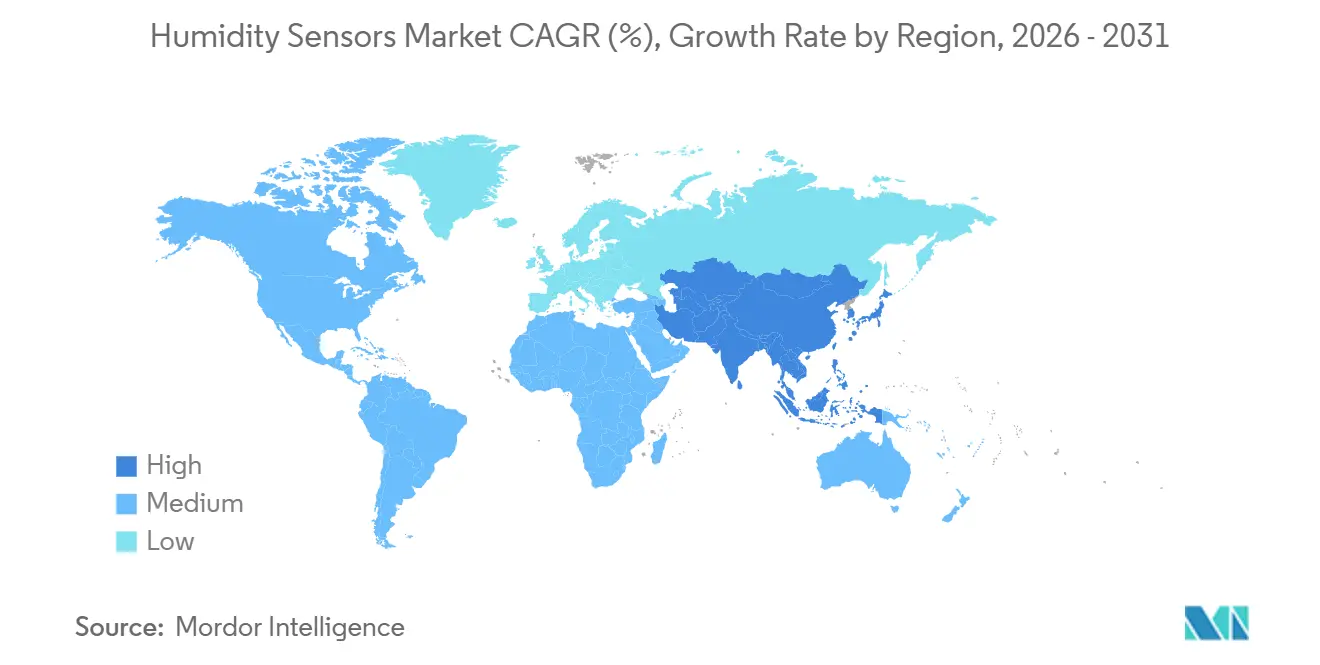

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Humidity Sensors Market Analysis by Mordor Intelligence

The Humidity Sensors Market size was valued at USD 698.10 million in 2025 and is estimated to grow from USD 739.5 million in 2026 to reach USD 985.45 million by 2031, at a CAGR of 5.91% during the forecast period (2026-2031).

Momentum stems from a global pivot to MEMS-based digital platforms that consolidate edge processing, a migration hastened by electric-vehicle battery safety mandates and stricter pharmaceutical cold-chain regulations. Semiconductor fabs in Taiwan and South Korea, as well as wide-scale HVAC retrofits across India, Indonesia, and Vietnam, collectively amplify unit demand, alongside rising greenhouse installations in North America. Vendors are also responding to a surge in aftermarket orders placed through e-commerce portals as operators retrofit legacy HVAC and industrial lines rather than replace full systems. Competitive dynamics are shifting as semiconductor majors harness wafer-scale integration to pressure discrete-module incumbents on cost, while still meeting the sub-1 % accuracy and sub-1 milliwatt standby-power thresholds required by wearables and IIoT nodes.[1]Sensirion AG, “Half-Year Report 2025,” sensirion.com

Key Report Takeaways

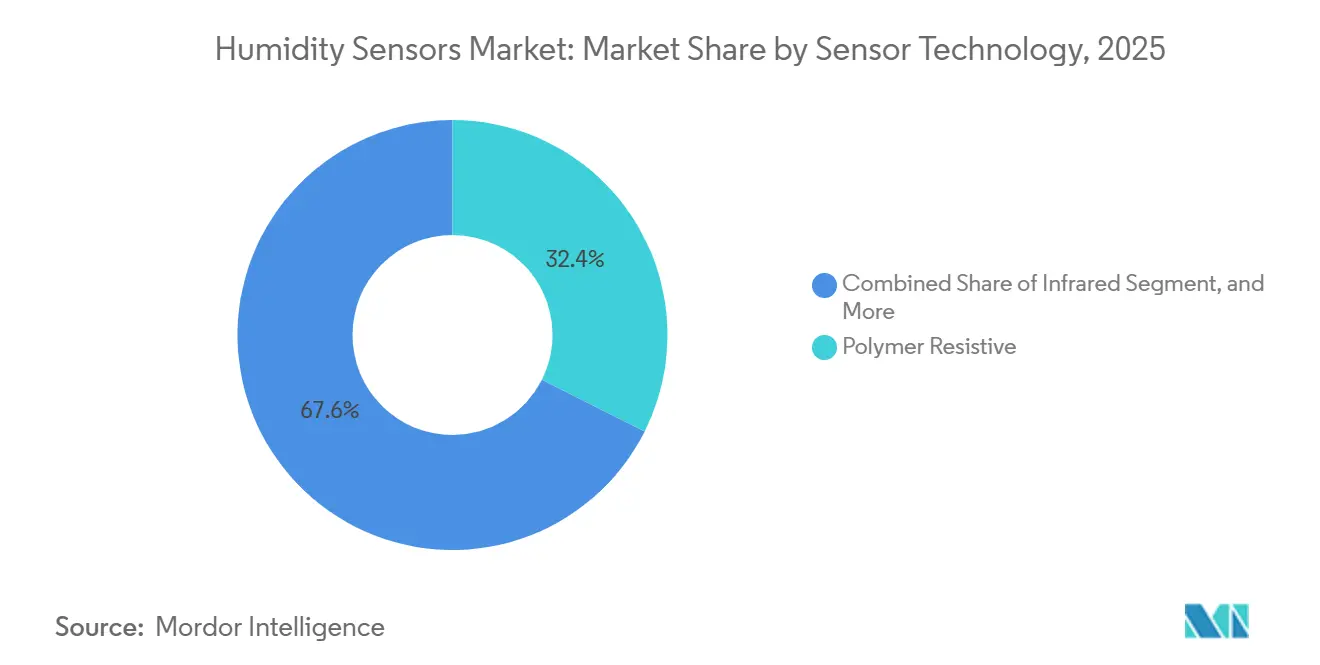

- By sensor technology, polymer resistive devices held 32.40% of the 2025 revenue pie, while MEMS-based digital sensors are advancing at a 6.40% CAGR through 2031.

- By measurement parameter, relative humidity commanded 46.00% share in 2025 and is on track to expand at a 7.70% CAGR to 2031.

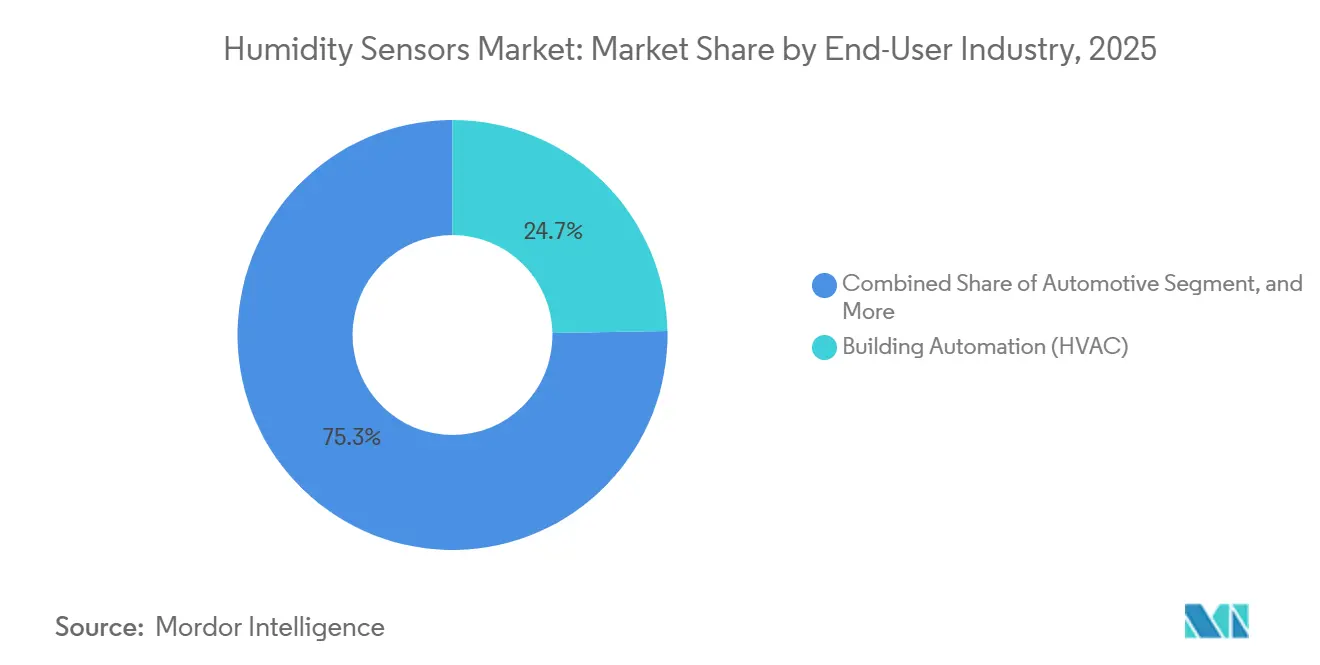

- By end-user industry, building automation and HVAC accounted for 24.70% of 2025 sales, whereas automotive applications post the fastest growth at a 6.00% CAGR.

- By distribution channel, OEM integration captured 52.20% of 2025 shipments, while the e-commerce route is scaling at a 7.20% CAGR.

- By geography, Asia-Pacific contributed 36.90% of global 2025 revenue and is projected to log a 6.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Humidity Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Miniaturization for Wearables | +1.2% | Asia-Pacific, North America | Medium term (2-4 years) |

| Rising HVAC Retrofit Projects in Emerging Economies | +1.0% | Asia-Pacific, Middle East, South America | Long term (≥ 4 years) |

| Stringent Pharmaceutical GMP Humidity Controls | +0.9% | North America, Europe | Short term (≤ 2 years) |

| Electric-Vehicle Battery Thermal Safety Needs | +0.8% | China, Europe, North America | Medium term (2-4 years) |

| Demand for Edge-Ready IIoT Environmental Nodes | +0.7% | North America, Europe | Medium term (2-4 years) |

| Carbon-Credit-Linked Greenhouse Monitoring | +0.5% | North America, Europe, Asia-Pacific, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Miniaturization for Wearables

Wearable brands are now integrating humidity sensing to differentiate themselves through sweat rate, skin hydration, and ambient condition data, rather than relying solely on step counts. Bosch Sensortec’s BME690, released in 2024, merges a MEMS humidity element and AI algorithm inside a 3 mm × 3 mm land-grid package that draws just 0.1 mA in low-power mode.[2]Bosch Sensortec, “BME690 Gas Sensor Datasheet,” bosch-sensortec.com Analog Devices followed with the MAX32672 microcontroller, which embeds sensor interfaces on-die to eliminate the need for discrete boards. Wafer-level chip-scale and fan-out packaging now reduces board real estate by up to 70%, enabling sub-2 mm² footprints. As component counts fall, device makers compress design cycles to match six-month model refreshes. Vertically integrated semiconductor houses gain a cost edge because they can co-optimize MEMS and logic on the same line, a hurdle for discrete-sensor specialists.

Rising HVAC Retrofit Projects in Emerging Economies

Cooling demand in Southeast Asia, the Middle East, and South America is increasing as urban populations expand and average temperatures rise. The International Energy Agency projects that ASEAN's space-cooling energy use will triple by 2040 compared to 2020. Variable-refrigerant-flow systems, coupled with humidity-responsive controls, cut energy consumption by 20-30%, encouraging building owners to replace stand-alone humidistats with networked arrays. Saudi Arabia’s 2024 green-building code mandates humidity sensing in new commercial HVAC and subsidizes retrofits. Electricity tariffs are rising faster than equipment costs, particularly in India, where commercial rates climbed 8% annually between 2020 and 2025, further strengthening retrofit economics. Suppliers benefit from steady demand for plug-and-play sensors that avoid lengthy plant shutdowns.

Stringent Pharmaceutical GMP Humidity Controls

The revised 2024 WHO guidance requires continuous monitoring with calibrated probes traceable to national metrology institutes and automated alerts outside 30%-70% relative humidity windows. The U.S. FDA’s concurrent update reinforces ICH Q1A protocols and requires ±2% RH accuracy during storage-zone mapping. Contract manufacturers and third-party logistics providers must now provide regulators with electronic audit trails, which is driving the adoption of cloud-linked sensor networks. Demand intensifies for NIST-traceable devices offering sub-1% drift over five years, as biologics and cell- and gene therapies are more moisture-sensitive than small-molecule drugs. Failure to meet the new thresholds risks warning letters and lost contracts, creating a compliance-driven replacement cycle.

Electric-Vehicle Battery Thermal Safety Needs

Humidity excursions within lithium-ion battery packs promote dendrite growth and electrolyte degradation, thereby increasing thermal runaway risks. Tesla’s 2024 patents outline dew-point sensors at module interfaces that flag moisture ingress before condensation forms. An IEEE 2025 white paper cites humidity intrusion as a leading driver of capacity fade, recommending MEMS sensors qualified for continuous operation at 85 °C. The migration to lithium-iron-phosphate chemistries, while safer thermally, heightens moisture sensitivity, and 800-volt powertrains further narrow allowable humidity bands. Automakers therefore place redundant sensors inside packs and cabins, leveraging shared supply chains to reduce bill-of-materials costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Calibration Drift in Polymer-Based Sensors | -0.8% | Tropical Asia and South America | Short term (≤ 2 years) |

| Limited Adoption in Extreme-Temperature Oilfields | -0.5% | Middle East, North America, Russia, offshore zones | Medium term (2-4 years) |

| High IP Barriers for MEMS-Level Packaging | -0.4% | Asia-Pacific, North America manufacturing hubs | Long term (≥ 4 years) |

| Supply-Chain Concentration of Specialty Dielectrics | -0.3% | Global dependence on East Asian suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Calibration Drift in Polymer-Based Sensors

Low-cost polymer resistive and capacitive devices experience an annual accuracy loss of 2-5% RH due to aging, contamination, and hysteresis. An IEEE Sensors Journal article from 2025 reported irreversible sensitivity shifts of over 10% RH within 12 months when exposed to volatile organic compounds. NIST’s 2024 calibration guide recommends yearly verification against saturated-salt standards, which can reduce five-year ownership costs by up to 40%. High-humidity tropical zones accelerate polymer swelling, shortening recalibration intervals. Because most polymer units require factory, not field, recalibration, HVAC and warehouse operators often delay replacements, which slows market penetration for higher-spec devices.

Limited Adoption in Extreme-Temperature Oilfields

Downhole and wellhead environments exceed 150 °C and 20,000 psi, conditions that overwhelm typical polymer or MEMS humidity sensors. Fiber-Bragg-grating optical alternatives withstand the heat but remain expensive, limiting deployment to offshore deepwater or unconventional wells. Operators in shale basins rely on periodic testing, rather than continuous monitoring, which suppresses sensor volumes. Corrosive hydrogen sulfide and hydrocarbon vapors can foul membranes within months, thereby increasing maintenance costs and expenses. Until vendors commercialize robust, economical high-temperature technology, uptake in oil and geothermal projects will lag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Technology: MEMS Digital Variants Outpace Legacy Platforms

The humidity sensors market size attributed to polymer resistive devices was significant in 2025, when the segment secured a 32.40% share of the overall humidity sensors market value. MEMS-based digital sensors, however, are pacing the gains with a 6.40% CAGR to 2031, reflecting their ability to integrate analog-to-digital conversion, temperature compensation, and serial communication onto a single die.

Infrared and cooled-mirror hygrometers retain their niche in the laboratory because they deliver reference-grade accuracy but command prices above USD 5,000 per unit. Aluminum-oxide capacitive elements remain relevant for compressed-air and oven applications where sub-zero dew points are a concern, although the risk of contamination limits their broader adoption. Optical-fiber sensors, immune to electromagnetic interference, win orders in MRI suites and high-voltage substations. Vendors such as Vaisala transitioned to modular designs with the Indigo 200 series, enabling probe head swaps to reduce inventory complexity.

By Measurement Parameter: Relative Humidity Dominates, Dew Point Gains in Process Industries

Relative humidity secured 46.00% of 2025 revenues and anchors the measurement landscape due to its inclusion in nearly every HVAC and consumer electronics control loop. With a 7.70% CAGR, the metric remains the fastest climber, underscoring its lock-in due to building codes and industrial standards.

Dew-point sensing, while smaller, is gaining traction in compressed-air, natural-gas, and pharmaceutical spray-drying lines where moisture must be quantified independently of temperature swings. Michell Instruments’ DMT152, which measures to −60 °C dew point, supports petrochemical dryers and industrial gas processors. Absolute humidity is favored in controlled-environment agriculture because vapor-pressure deficit calculations improve crop yields.

By End-User Industry: Automotive Electrification Outpaces Building Automation

Building automation and HVAC generated 24.70% of the 2025 turnover, benefiting from heat pump rollouts and smart thermostat retrofits. Yet, the automotive segment leads growth with a projected 6.00% CAGR, as battery packs and cabin systems embed redundant sensors to manage condensation and extend range.

Semiconductor fabs follow close behind; operators in Taiwan, South Korea, and the United States must hold cleanrooms to ±1% RH to avoid electrostatic discharge on sub-3 nm lines. Pharmaceutical producers expand demand through biologics, and food-and-beverage plants utilize sensors in fermentation, grain storage, and cold chains. Oil and gas, power generation, and pulp and paper each constitute smaller but stable end-markets.

By Distribution Channel: E-Commerce Disrupts OEM-Dominated Landscape

OEM integration represented 52.20% of 2025 shipments because appliance, automotive, and industrial manufacturers lock in multi-year contracts to secure their supply. Still, e-commerce posts the fastest momentum at a 7.20% CAGR as small and mid-sized enterprises order replacement sensors online. Component marketplaces, such as Digi-Key, Mouser, and regional peers, offer parametric search engines that reduce procurement lead times from weeks to days, eroding the OEM channel’s convenience advantage.

Aftermarket installers appreciate drop-in digital sensors that extend asset life without plant downtime, particularly in facilities where capital budgets are frozen. OEM channels will remain dominant for safety-critical sectors such as medical and automotive, where qualification and warranty coverage justify higher prices.

Geography Analysis

The Asia-Pacific region generated 36.90% of the global humidity sensors market revenue in 2025 and is projected to record a 6.90% CAGR from 2026 to 2031. Demand concentrates in semiconductor fabs across Taiwan and South Korea, electric-vehicle production in China, and government-incentivized HVAC retrofits in India and Southeast Asia. Japan is following the trend, exemplified by Hitachi High-Tech’s 2025 factory in Yamanashi, which manufactures cleanroom monitor systems featuring Vaisala probes.[3]Hitachi High-Tech, “Completion of Yamanashi Factory,” hitachi-hightech.com India’s Bureau of Energy Efficiency now requires humidity-sensing controls in higher-capacity air conditioners, lifting sensor content per unit.

North America ranks second, driven by pharmaceutical storage upgrades, data center construction, and electric vehicle assembly lines. The U.S. EPA’s 2024 semiconductor air-pollutant standards tightened humidity windows inside fabs, prompting sensor network retrofits. Canada’s federal heat-pump subsidies likewise seed residential demand.

Europe is experiencing solid expansion, driven by the installation of heat pumps, which surpassed 500,000 units in Germany by 2024. The Middle East pursues megaprojects such as NEOM and Masdar City, which incorporate integrated environmental monitoring. South America’s growth clusters in Brazil’s food processing and pulp-and-paper mills, while Africa remains nascent, with uptake limited to pharmaceutical cold-chain and Tier-III data centers.

Competitive Landscape

The top five suppliers, Sensirion, Honeywell, Bosch Sensortec, TE Connectivity, and Texas Instruments, control roughly 45-50% of the global revenue, resulting in a moderately fragmented humidity sensors market. Sensirion reported CHF 103.7 million (USD 117.3 million) in first-half 2025 sensor income, down 14.8% year over year because consumer-electronics inventories were flushed. TE Connectivity, by contrast, delivered 17% organic growth in its sensor segment during Q4 2025, aided by the April 2025 acquisition of Richards Manufacturing, which adds hermetic packaging for harsh environments.

Semiconductor giants STMicroelectronics, Infineon, and Renesas leverage wafer fabs to drive unit costs below USD 1 in high volume, capturing design wins in wearables and automotive modules. Patent filings for hermetic MEMS encapsulation, through-silicon vias, and wafer-level sealing rose 15% in 2024, surpassing 200 grants at the USPTO. Cross-licensing pacts guard freedom to operate, while litigation risk elevates the barriers for start-ups.

Partnerships and vertical integration accelerate: STMicroelectronics and Qualcomm teamed in October 2024 to co-develop Bluetooth-enabled IoT sensor modules that pair MEMS humidity elements with wireless radios. Smaller players differentiate themselves through application focus; ProGlove, for instance, embeds sensors in wearable barcode scanners to track warehouse comfort levels, although its aggregate revenue trails that of the majors.

Humidity Sensors Industry Leaders

Honeywell International Inc.

Sensirion AG

Bosch Sensortec GmbH

Texas Instruments Incorporated

TE Connectivity Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Sony and Internet Initiative Japan have formed a joint venture to market smart-agriculture nodes that combine soil moisture and humidity monitoring over cellular links, targeting the deployment of 10,000 devices by the end of 2026.

- July 2025: Hitachi High-Tech completed a semiconductor equipment plant in Yamanashi that fabricates cleanroom environmental monitoring systems outfitted with Vaisala probes.

- May 2025: Infineon Technologies has launched the XENSIV PAS CO₂ sensor, featuring an integrated MEMS humidity element for indoor air quality analytics.

- April 2025: TE Connectivity acquired Richards Manufacturing to enhance its hermetic packaging capability for harsh-environment sensors.

Global Humidity Sensors Market Report Scope

A humidity sensor is an electronic device that measures the humidity in its environment and converts its findings into a corresponding electrical signal. Humidity sensors are a part of environmental sensors. The Humidity Sensors Market Report is Segmented by Sensor Technology (Infrared, Bimetallic, Cooled Mirror, Aluminum Oxide Capacitive, Polymer Resistive, MEMS-Based Digital, Optical Fiber), Measurement Parameter (Relative Humidity, and More), End-User Industry (Chemical and Petrochemical, and More), Distribution Channel (OEM Integration, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Infrared |

| Bimetallic |

| Cooled Mirror |

| Aluminum Oxide Capacitive |

| Polymer Resistive |

| MEMS-Based Digital |

| Optical Fiber |

| Relative Humidity |

| Absolute Humidity |

| Dew Point |

| Chemical and Petrochemical |

| Building Automation (HVAC) |

| Automotive |

| Oil and Gas and Natural Gas |

| Pharmaceutical |

| Semiconductor |

| Power Generation |

| Food and Beverage |

| Paper and Pulp |

| Water, Wastewater, and Incineration |

| Consumer Electronics |

| Rest of End-User Industries |

| OEM Integration |

| Aftermarket / Retrofit |

| E-Commerce |

| North America | United States |

| Canada | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Sensor Technology | Infrared | |

| Bimetallic | ||

| Cooled Mirror | ||

| Aluminum Oxide Capacitive | ||

| Polymer Resistive | ||

| MEMS-Based Digital | ||

| Optical Fiber | ||

| By Measurement Parameter | Relative Humidity | |

| Absolute Humidity | ||

| Dew Point | ||

| By End-User Industry | Chemical and Petrochemical | |

| Building Automation (HVAC) | ||

| Automotive | ||

| Oil and Gas and Natural Gas | ||

| Pharmaceutical | ||

| Semiconductor | ||

| Power Generation | ||

| Food and Beverage | ||

| Paper and Pulp | ||

| Water, Wastewater, and Incineration | ||

| Consumer Electronics | ||

| Rest of End-User Industries | ||

| By Distribution Channel | OEM Integration | |

| Aftermarket / Retrofit | ||

| E-Commerce | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the global humidity sensors market in 2026?

The humidity sensors market size stands at USD 739.50 million in 2026 and is on course to reach USD 985.45 million by 2031.

Which sensor technology is growing fastest?

MEMS-based digital humidity sensors are expanding at a 6.40% CAGR through 2031 thanks to integrated signal conditioning and shrinking package footprints.

Why are humidity sensors critical in electric-vehicle batteries?

Continuous humidity monitoring inside battery packs helps automakers detect moisture ingress early, preventing short circuits and thermal runaway events.

What drives demand for sensors in emerging-market HVAC retrofits?

Rising electricity costs and policies that mandate humidity-responsive controls encourage building owners to add networked sensors to existing air-conditioning systems.

Which region contributes the highest revenue?

Asia-Pacific leads with 36.90% of global 2025 revenue and delivers the fastest regional CAGR at 6.90% through 2031.

How does e-commerce affect sensor distribution?

Online component marketplaces are posting a 7.20% CAGR as small and midsize enterprises purchase retrofit sensors directly, eroding OEM channel dominance.

Page last updated on: