Humidifier Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.14 Billion |

| Market Size (2031) | USD 7.11 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Humidifier Market Analysis by Mordor Intelligence

The Humidifier Market size is expected to increase from USD 4.84 billion in 2025 to USD 5.14 billion in 2026 and reach USD 7.11 billion by 2031, growing at a CAGR of 6.72% over 2026-2031.

Demand continues to shift from low-cost ultrasonic units toward cleaner evaporative designs in select high-growth markets, while connected features and hygiene-focused materials influence premium price points in developed regions. Installation preferences remain split between portable convenience and whole-home systems that pair well with HVAC retrofits, supported by innovations that reduce water waste and improve ease of ownership. Digital retail strengthens routes to first-time buyers, yet specification-grade opportunities expand in commercial buildings, data centers, and controlled environments where humidity control supports uptime, comfort, and safety standards. Asia-Pacific remains the growth outlier with the highest projected regional expansion, which redirects competitive focus toward feature sets that balance energy efficiency, cleanability, and smart-home interoperability.

Key Report Takeaways

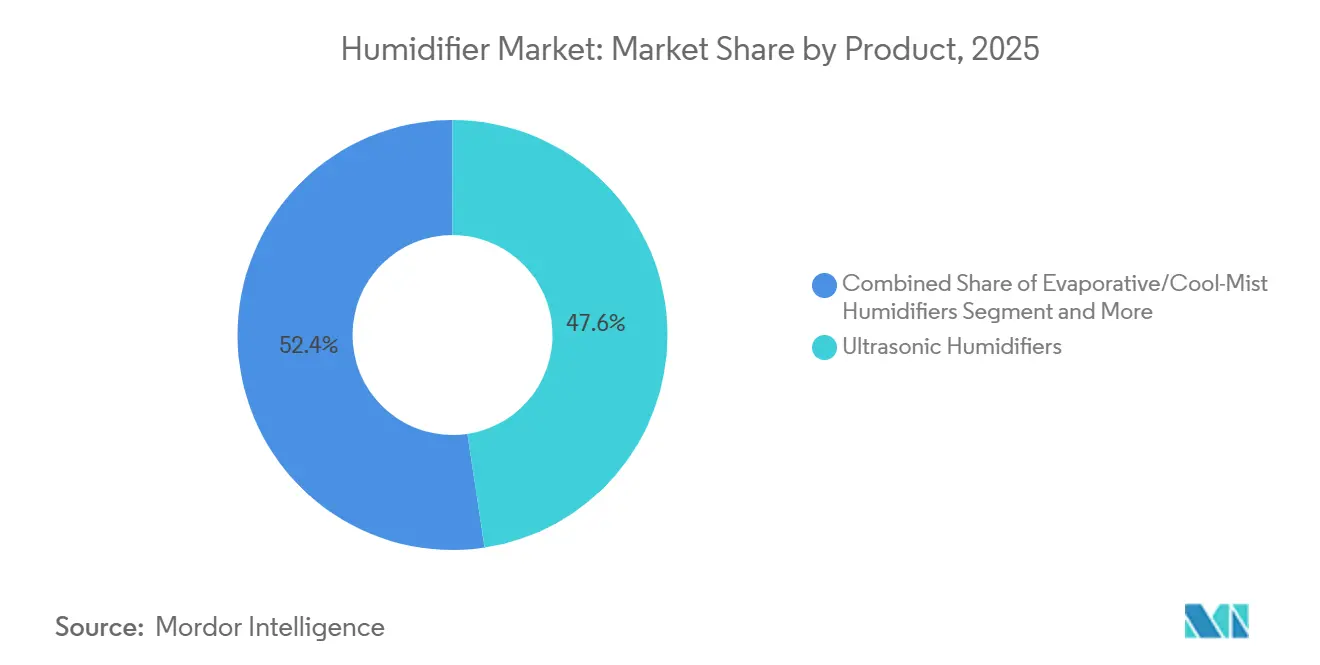

- By product, ultrasonic models led with a 47.62% revenue share in 2025; evaporative designs are gaining momentum in health-focused segments, while ultrasonic retained the highest projected product-segment growth at a 7.62% CAGR through 2031.

- By installation type, portable units accounted for a 61.37% share in 2025, and whole-house systems are forecast to expand at an 8.27% CAGR through 2031 as HVAC retrofits scale.

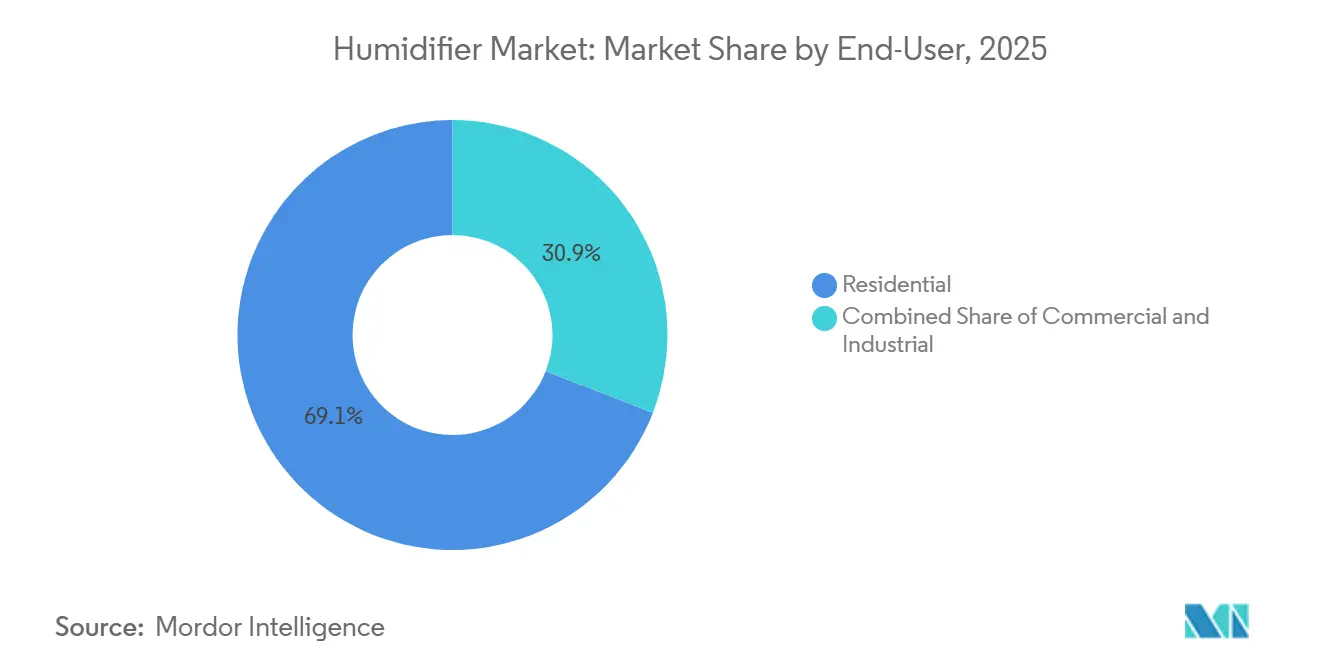

- By end user, residential held 69.11% of 2025 revenue, while commercial is advancing at a 7.14% CAGR through 2031 on IAQ and productivity-led upgrades.

- By distribution channel, B2C represented 73.81% of revenue in 2025, and online retail is the fastest-growing channel at a 9.81% CAGR through 2031.

- By geography, Asia-Pacific commanded 41.53% of revenue in 2025 and is projected to deliver the highest regional expansion at an 8.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Humidifier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing awareness of indoor air quality & respiratory health | +1.8% | Global, with early gains in North America, Europe, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Proliferation of smart / IoT-enabled small appliances | +1.5% | Global, strongest in North America, Japan, South Korea, and urban China | Short term (≤ 2 years) |

| Expansion of e-commerce & omnichannel retailing for small appliances | +1.3% | Global, with disproportionate impact in Asia-Pacific and LATAM | Short term (≤ 2 years) |

| Humidity compliance mandates in data-centers & semiconductor fabs | +0.9% | North America, Asia-Pacific core geographies, and spillover to Europe | Long term (≥ 4 years) |

| Rising prevalence of dry indoor environments due to HVAC-intensive buildings | +1.1% | North America, Europe, Middle East, high-density urban Asia-Pacific | Medium term (2-4 years) |

| Adoption of adiabatic humidification in vertical farming & greenhouse automation | +0.6% | Global, early adoption in the Netherlands, Japan, California, and the Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Indoor Air Quality (IAQ) Awareness Reshaping Residential Purchase Criteria Beyond Baseline Humidification

Indoor air can contain higher concentrations of pollutants than outdoor environments, which has heightened consumer attention on humidity control as part of broader indoor air quality strategies [1]Source: U.S. Environmental Protection Agency, “Indoor Air Quality,” U.S. EPA, epa.gov . A growing public health focus is visible as a large share of the United States population lives in counties with unhealthy ozone or particulate levels, which aligns with more active risk management within homes and workplaces. Guidance on maintaining relative humidity in the 40-60% range continues to influence building operations and consumer device settings, which supports steady demand for consistent moisture control through the year [2]Source: Raritan, “ASHRAE Best Practices for Environmental Monitoring of Humidity and Temperature,” Raritan, raritan.com . Climate-related events such as wildfire smoke and moisture intrusions increase indoor environmental variability, which pushes occupants and facility managers to adopt more precise humidity control as part of IAQ plans. As this awareness spreads across urban centers in North America, Europe, and parts of Asia-Pacific, device selection increasingly rewards products that maintain stable humidity while minimizing microbial risk and maintenance burden.

Smart Connectivity Commoditized, Hygiene Emerges as Premium Differentiator

Connected controls are now common across home climate devices, so premium performance is shifting toward material science and sanitation features that cut biofilm and mineral residue inside water pathways. Premium vendors emphasize tank materials and sterilization features that reduce pathogen counts in standing water, which helps close compliance gaps with cleaning guidance and supports higher uptime in daily use. Products that combine stainless steel reservoirs with ultraviolet treatments have become anchor offerings at the high end because they address user concerns about hygiene without adding frequent maintenance steps. In practice, connectivity serves convenience while hygiene drives the willingness to pay for top-tier models, especially among parents, allergy sufferers, and heavy users who run devices continuously in dry seasons. As a result, product roadmaps increasingly balance app control, voice integration, and self-cleaning designs that align with public health guidance on device maintenance.

Data Centers and Semiconductor Fabs Driving Specification-Grade Adoption

Data centers must maintain stringent humidity ranges to protect electronics from electrostatic discharge and corrosion, which drives the need for specification-grade humidification integrated with facility controls. Operators increasingly prioritize systems that operate efficiently alongside modern cooling architectures, which favors solutions that deliver moisture control while minimizing energy draw. Manufacturers are expanding production and service footprints near hyperscale corridors to support fast commissioning and rapid spare parts availability for mission-critical clients. Semiconductor cleanrooms and pharmaceutical facilities apply even tighter tolerance bands, which sustains demand for humidity systems capable of precise control under variable loads. This need for reliability and integration with building management systems supports long-term contracts and repeat upgrades as process requirements evolve.

Controlled-Environment Agriculture Favoring Energy-Efficient Evaporative Approaches

Greenhouses and vertical farms rely on specific humidity ranges during germination, vegetative growth, and flowering to manage plant stress and support optimal transpiration, which drives demand for precise control across seasons. Evaporative and adiabatic approaches use ambient heat to add moisture, which helps lower total energy use during conditioning compared with steam-based systems in many configurations. Integrated controls that link lighting, temperature, and humidity enable growers to hold tighter vapor-pressure deficits, which can support improved consistency and yield. Growers in water- and energy-constrained regions add humidification for both moisture and cooling benefits within closed environments, which eases stress during peak heat periods. As horticulture automation scales, vendors with proven agricultural references and easy-to-service systems are positioned to capture repeat deployments in new facilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High maintenance burden & risk of microbial contamination | -1.2% | Global, acute in healthcare facilities, less constraining in price-sensitive markets | Medium term (2-4 years) |

| Seasonal demand fluctuations are limiting capacity utilization | -0.7% | North America, Northern Europe, temperate zones with winter heating seasons | Short term (≤ 2 years) |

| Import-tariff volatility on piezo-ceramic ultrasonic transducers | -0.5% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Rising consumer concerns over mold growth, white dust, and indoor air hygiene | -0.6% | North America, Europe, urban Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Microbial-Contamination Liability Restricts Healthcare Adoption and Elevates Cleaning Burden

Health authorities advise regular emptying and cleaning of humidifier reservoirs to reduce the risk of Legionella growth, which raises user time costs and complicates care in sensitive settings [3]Source: Centers for Disease Control and Prevention, “Control Legionella: Other Devices Module,” CDC, cdc.gov . Hospitals and long-term care facilities reference stringent infection control guidance that limits the use of reservoir-type devices or requires special handling steps, which narrows product choices in clinical spaces. In homes, over-humidification can promote mold and dust mites, which undercuts the perceived health benefit when users run devices without monitoring room humidity. Mineral content in tap water can disperse as white dust when atomized, which is why manufacturers often recommend distilled water or demineralization to mitigate residue. Premium designs that combine UV treatments and materials that resist scratching help, yet users still need to follow care steps to meet hygiene goals.

Concentrated Winter Demand Creates Inventory and Pricing Friction

Humidifier sales cluster in colder months when indoor heating dries the air, which puts pressure on inventories and creates off-season discounting that can compress margins for consumer brands. Short demand windows complicate factory scheduling and retailer allocation, since a warm winter or a sudden surge can leave stock misaligned with local conditions. Whole-house in-duct systems installed during HVAC replacements or upgrades can smooth sales across the year, which helps vendors and contractors reduce seasonality exposure. Portable devices remain popular but produce a faster replacement cycle as new features arrive, which introduces churn risk when convenience or aesthetics improve at similar price points. As smart-home adoption continues, vendors are incentivized to offer accessory bundles and service plans that support replacement filters and cleaning guidance, which may reduce seasonal peaks by encouraging continuous usage on moderate settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Ultrasonic scale holds leadership while evaporative performance gains favor in hygiene-sensitive use cases

Ultrasonic models led the product mix with 47.62% of the 2025 market size and are projected to record the fastest product-segment expansion at a 7.62% CAGR through 2031, reflecting ongoing affordability and wide retail availability in the humidifier market. This leadership aligns with entry prices that draw first-time buyers, along with compact footprints that fit bedrooms and workspaces. However, the visible mist and ease of use now compete with concerns over mineral residue and standing-water hygiene, which pushes some buyers toward evaporative systems that avoid aerosolizing dissolved solids. Premium brands focus on hygienic engineering, such as UV treatment and durable tanks, to reduce biofilm risk, which improves the value proposition for long-run usage [4]Source: Dyson, “Dyson HushJet Purifier Compact,” Dyson, dyson.com. Warm-mist units retain appeal for relief during cold seasons, while evaporative products resonate in spaces that need quiet, low-energy operation and even moisture distribution. Industrial buyers continue to specify designs that integrate with building management systems and deliver precise settings for uptime and process safety, which sustains a multilayered product landscape across consumer and commercial channels.

The humidifier industry has shifted attention to materials and maintenance cycles as points of differentiation within similar form factors. Evaporative designs align with use cases where users want to avoid white dust and prefer natural moisture release through wicking and airflow. Ultrasonic models remain the workhorse of budget segments and gift seasons, yet growth in premium tiers is more closely tied to hygiene and energy features than to connectivity alone. In practice, households often operate multiple device types across rooms based on runtime, noise tolerance, and capacity needs, which sustains parallel demand within brands. As health awareness extends beyond winter, multi-function devices with purification or integrated sensors may capture a larger share of the humidifier market in urban and allergy-prone communities.

By Installation Type: Portable convenience dominates while whole-house retrofits accelerate with HVAC upgrades

Portable table-top devices accounted for a 61.37% installation market share in 2025, supported by renters, students, and households seeking instant setup, while whole-house installations are forecast to expand at an 8.27% CAGR through 2031 as retrofits and replacements gain traction in the humidifier market. Portables benefit from online retail discovery, easy shipping, and a broad assortment, which helps brands reach first-time buyers quickly. Console units serve large rooms and multi-room coverage, yet they face pressure from both compact portables and whole-home systems that integrate into existing HVAC. Whole-house solutions deliver uniform moisture across living areas and reduce the number of units needed, which simplifies filter logistics and daily use. Homeowners often schedule these installs with furnace replacements or efficiency upgrades, which reduces incremental labor and encourages control through existing thermostats. As energy and water use gain visibility, installation decisions favor designs that balance runtime, waste reduction, and serviceability over time.

In the humidifier industry, mini-split and heat-pump retrofits open opportunities for add-ons that condition air at the room or zone level. Portable devices will remain the on-ramp for many households, while whole-house units gain adoption in single-family homes where integration and one-time setup offer long-term convenience. High-performance products that reduce water waste and automate humidity targets can relieve maintenance concerns and improve user satisfaction, which supports sustained usage across seasons. As smart-home platforms mature, installers bundle sensors and services that keep relative humidity in check without constant manual adjustments. This combined approach helps each installation type retain its role, with portable devices capturing entry demand and in-duct systems anchoring long-term households in the humidifier market.

By End User: Residential volume leads while commercial projects grow on IAQ and productivity goals

Residential customers represented 69.11% of 2025 revenue, reflecting the importance of comfort and health awareness in daily routines, while commercial buyers are projected to grow at a 7.14% CAGR through 2031 as offices, hospitality, and public venues formalize IAQ programs in the humidifier market. At home, consumers value compact designs, quiet operation, and ease of cleaning, which steers premium choices toward materials that resist microbial growth. In commercial spaces, humidity control supports occupant comfort, helps reduce absenteeism linked to dry indoor air, and aligns with wellness certifications sought by employers and landlords. Healthcare and clean industries apply stricter standards that emphasize device sanitation, sterile water use, and precise control, which influences vendor selection and service agreements. Data centers and semiconductor lines remain focused on reliability and integration with automation systems to protect equipment and yields, creating a steady pipeline for specification-grade projects.

Residential purchases often occur during dry seasons or life-stage changes such as moving, expecting a child, or building a home office. Commercial projects involve longer cycles with site surveys, commissioning, and ongoing maintenance, which grow service revenue and support replacement intervals that differ from consumer cycles. As building owners retrofit HVAC systems for efficiency and wellness, bundled scopes that include humidification can accelerate adoption, especially when products deliver measurable water and energy benefits. The humidifier industry continues to diversify across home and professional applications, and vendors that address hygiene, monitoring, and integration can meet expectations for both sets of buyers. Over time, education on correct use and maintenance remains central to sustaining results in homes and workplaces.

By Distribution Channel: B2C leads by reach, while online growth outpaces legacy retail formats

B2C channels captured 73.81% of revenue in 2025, with online retail projected to be the fastest-growing route at a 9.81% CAGR through 2031 in the humidifier market. E-commerce search and reviews surface hygiene and reliability features that may be hard to convey in brief in-store interactions. Digital-first assortments also enable rapid testing of new bundles that pair humidifiers with filters, sensors, or compatible purifiers. In parallel, brand-operated sites and targeted advertising help vendors reach niche needs such as nursery use, winter skin care, or static control for home offices. For buyers who value in-person evaluation, brand showrooms and select retail partners act as experience centers before final online or offline purchase.

B2B routes serve projects that require sizing, engineered drawings, and commissioning, which favors manufacturers that maintain local service presence and fast parts logistics. As commercial projects add monitoring and building-automation integration, value migrates toward solution packages rather than standalone devices. The humidifier industry continues to balance open e-commerce access for consumers with consultative sales for industrial and healthcare applications. Over time, data insights from connected fleets can support preventative maintenance and filter programs, which improve reliability and build customer lifetime value. This dual-channel model enables brands to meet both immediate household needs and multi-year professional requirements in the humidifier market.

Geography Analysis

Asia-Pacific held 41.53% of global revenue in 2025 and is projected to post the fastest regional expansion at an 8.03% CAGR through 2031, reflecting a deep base of first-time buyers and growing IAQ awareness in urban corridors of key countries within the humidifier market. Urbanization and rising disposable incomes widen the installed base for home climate devices, which improves scale for regional brands and encourages multinational entrants to localize lineups. In Japan and parts of East Asia, strong winter dryness patterns encourage steady seasonal usage, while households in tropical climates adopt humidifiers in air-conditioned spaces that lower indoor relative humidity during long runtime periods. The breadth of housing formats across the region opens demand for small portables in apartments and higher-capacity devices in larger dwellings, which support diverse product mixes. As commercial construction accelerates in select metros, building projects incorporate humidity control into broader HVAC scopes, which will continue to favor specification-grade vendors alongside consumer channel leaders.

North America remains a high-value region with a mature installed base; winter severity, home renovations, and ongoing smart-home adoption shape replacement cycles. Retailers rotate assortments that emphasize quiet operation, all-day runtime, and self-cleaning features that address common user pain points tied to tank hygiene. Commercial adoption follows employer and landlord wellness initiatives, where humidity control supports comfort and helps maintain productive indoor environments. The region’s data center footprint also creates steady industrial demand for humidity systems that protect high-value electronics, which supports manufacturers that offer commissioning and local service teams. Over time, the humidifier market will see more whole-house integrations tied to furnace or heat pump upgrades, especially as owners look for water- and energy-saving features that reduce operating costs.

Europe blends high-penetration northern markets with developing opportunities in warmer climates where heating seasons are shorter, and humidity control is a newer category within home upgrades. Buyers in colder countries often adopt higher-end systems that pair with radiant heating and central ventilation, which positions integrated humidification as part of comfort packages. Indoor air quality standards in commercial buildings support stable project activity for offices, healthcare spaces, and preservation settings such as museums and libraries. Industrial customers continue to prioritize reliability, energy performance, and water management, which favors solutions with proven track records and service networks across major economies. Across the region, the humidifier market share for premium devices tends to be highest where consumers value low-noise operation, hygienic materials, and seamless integration with other building systems.

Regulatory Landscape

Humidifiers sold for household and similar use commonly align to IEC 60335-2-98:2023, which defines safety requirements for electric humidifiers (including battery-operated and DC-supplied units) and shapes test and certification needs for global product launches. Correct product classification matters, because adjacent categories follow different standards (for example, medical humidifiers under IEC 60601 and certain HVAC-integrated equipment under IEC 60335-2-88), affecting both compliance pathways and labeling.

In the European Union, environmental compliance is a parallel gatekeeper to market access for consumer humidifiers, notably through Directive 2011/65/EU (RoHS), which restricts 10 substances including lead, mercury, and cadmium, and through REACH (EC) 1907/2006 for chemical registration and restrictions. These regimes influence component selection (electronics, plastics, coatings) and supplier documentation across the bill of materials, particularly for premium designs that differentiate via hygiene-focused materials and water-path treatments.

Value Chain Analysis

The humidifier value chain starts with raw materials (plastics, stainless steel, packaging) and electronics inputs, then moves through specialized components such as motors/fans, ultrasonic atomizers (piezoelectric transducers), sensors, PCBs, and filters and wicks for evaporative designs. Assembly is split between brand-owned manufacturing and OEM/ODM production, with quality systems and safety testing aligned to household-appliance standards (for example, IEC 60335-2-98:2023) acting as a key go/no-go step before shipment.

Downstream, consumer volumes move through B2C retail and fast-growing online channels, while specification-grade humidification for commercial and industrial sites relies more on B2B/direct sales, engineering support, and commissioning, supported by spares availability. Supply-chain resilience is shaped by component availability and cost volatility for electronics and ultrasonic transducers, and by trade and tariff variability that changes landed cost and sourcing decisions. This reinforces the need for multi-sourcing, modular design, and regional inventory buffers for seasonal demand peaks.

Competitive Landscape

The humidifier market spans consumer, commercial, and industrial use cases, which creates a mix of high-volume retail brands and specification-led manufacturers. Consumer leaders focus on quiet operation, compact footprints, and ease of cleaning to win everyday use, while premium offerings add UV treatment and durable materials that resist biofilm formation within tanks and water paths. In contrast, industrial vendors compete on integration with building automation, commissioning speed, and lifecycle support, which includes local warehouses for spare parts and trained service teams that reduce downtime risks for mission-critical clients. This split supports healthy competition across tiers, with brands differentiating on both initial features and after-sales experiences that sustain performance and compliance with hygiene guidance.

Strategic moves emphasize proximity to customers, product innovation, and sustainability. One leading industrial supplier expanded its United States presence with a new facility that targets hyperscale corridors, which shortens lead times and strengthens commissioning resources for large projects. At the consumer end, a top premium brand launched a quiet compact purifier-humidifier in 2025, aiming at small urban apartments and noise-sensitive contexts where continuous operation matters to users. HVAC-integrated players continue to invest in designs that reduce water waste and support cleaner reservoirs, leveraging component improvements that ease maintenance and raise satisfaction in whole-house deployments. Together, these moves suggest a measured pivot toward solutions that keep maintenance simple while aligning with health guidance and energy goals across the humidifier market.

Regional manufacturing and distribution investments also shape competitive outcomes. A Canadian equipment maker expanded its European footprint in 2025 to cut delivery times and support local service standards, which is a common way to align with commercial client expectations on uptime guarantees. The same company launched reverse-osmosis support systems and high-pressure solutions with monitoring features, which reflects how industrial clients value reliability, predictive maintenance, and water quality protections that extend system life. In the United States residential channel, whole-house vendors lean on contractor networks and compatibility with modern thermostats to win replacement cycles, which anchors their share in single-family homes that plan HVAC investments years. These strategies align with a broader shift toward serviceable, integrated designs that deliver consistent humidity with fewer manual interventions across the humidifier market.

Humidifier Industry Leaders

Honeywell International Inc.

Dyson Ltd.

Vicks / Kaz (Procter & Gamble)

Crane USA

Boneco AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product innovation is concentrating on reducing cleaning and maintenance friction, which addresses a core restraint in the category and supports premium pricing as connectivity features commoditize. Levoit’s 2026 humidifier lines provide a clear indicator of this shift, including dishwasher-safe water-contact components in its NeoClassic series and a long-life, washable wick filter design in its Superior Studio smart evaporative humidifier.

Brand expansion and ecosystem bundling also open growth avenues beyond standalone seasonal appliances. Partnerships and multi-device app control position humidifiers within broader home-environment portfolios, with May 2026 bringing Kenmore’s licensing partnership with Airdog to develop and distribute Kenmore-branded humidifiers and related home-environment products. Molekule, meanwhile, positioned its Mo line to integrate humidification into its existing air-treatment app ecosystem. These moves broaden shelf presence and cross-selling opportunities (humidification plus purification and sensing) while raising expectations around interoperability, consumables attachment (filters and wicks), and after-sales support.

Recent Industry Developments

- June 2026: Levoit expanded its humidifier lineup with the launch of the Superior Studio Smart Evaporative Humidifier, emphasizing a washable, long-life wick filter and antimicrobial materials aimed at reducing recurring maintenance. The release reinforces the market shift toward ownership-cost and hygiene differentiators alongside smart controls.

- September 2025: Dyson expanded its air-treatment platform with integrated humidification and sensing capabilities, strengthening its multi-function device strategy. The development signals a move towards more comprehensive room-air management devices.

- October 2024: No additional major, in-scope 2024 corporate developments were evidenced in the provided source pack beyond the report context and 2025-2026 announcements. The 2025 cycle of product launches and distribution expansions remains the closest reference point for market-shaping actions carried into the 2026 base year.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the sales value of humidifier equipment used to add moisture to indoor air across residential, commercial, and industrial settings, including portable units and whole-house or in-duct systems. Revenues are counted at the point where products are sold into the market, and then aggregated by geography.

Scope exclusions: We exclude consumables and routine replacement items such as wicks, filters, and other standalone accessories when they are not sold as part of the humidifier unit.

Segmentation Overview

- By Product

- Ultrasonic Humidifiers

- Evaporative / Cool-Mist Humidifiers

- Warm-Mist / Steam Vaporizers

- Others

- By Installation Type

- Portable / Table-top

- Console / Room

- Whole-House / In-Duct Systems

- By End User

- Residential

- Commercial

- Industrial

- By Distribution Channel

- B2B/Directly from Manufacturers

- B2C/Retail Channels

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map humidifier demand drivers and set practical boundaries for what should be counted as humidifier revenue before the model was finalized. We referenced public sources such as the US Census Bureau trade and manufacturing tables, UN Comtrade for cross-border movement patterns, the International Energy Agency for building and energy context, and standards and guidance from ASHRAE that describe indoor humidity requirements in HVAC settings.

We also reviewed company filings and investor presentations to understand product mix shifts, for example portable versus whole-house units, and how pricing moved across bands. Credible press, retailer category pages, and published regulatory updates were checked for adoption triggers in schools, healthcare, and offices. Where extra confirmation was needed, we used paid subscriptions for company financials and intelligence, plus shipment-level import and export data to sanity-check flow volumes. The sources listed here are illustrative, and other public and paid references were used during data collection, validation, and clarification steps.

Primary Interviews and Surveys

Primary work was used to test assumptions on unit volumes, changes in average selling prices, and the split between portable and whole-house installations, which can be harder to observe from secondary data. We spoke with a mix of manufacturers, distributors, installers, and large buyers so the demand picture is checked from more than one angle across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | APAC: 40% |

| Mid tier: 49% | Functional/Unit leaders: 39% | EMEA: 36% |

| Smaller Players: 21% | Managers: 45% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where population, urban households, commercial floor space growth, and HVAC penetration are converted into an addressable installed base. This base is then filtered through humidifier adoption rates and replacement cycles. To keep the totals realistic, the value is derived using average selling prices by installation type and channel, then adjusted for regional mix and currency timing.

After the top-line view is formed, we corroborate it with selective bottom-up approximations such as supplier and distributor roll-ups for sampled countries, plus channel checks that link units sold to price bands. When gaps show up, such as limited visibility in smaller markets or informal channels, the model uses proxy indicators like import patterns and climate-driven seasonality to avoid overstating demand. For forecasting, scenario analysis is used so the outlook reflects different paths for housing completions, commercial retrofits, and consumer spending, and these scenarios are screened against what interviewees expect for pricing and mix over the next few years.

Data Validation & Update Cycle

Outputs are validated through multiple cross-checks so the final numbers do not rely on one data stream. We compare modeled demand against independent signals such as trade movement consistency, reported category revenue trends, and region-level adoption patterns tied to climate and building activity.

Variance checks flag unusual changes in units, pricing, or regional shares, and any outliers are reviewed before internal sign-off. If a mismatch stays unresolved, analysts re-contact select respondents to re-test the assumption that caused the swing. Reports are refreshed annually, and interim updates are done when material events can change volumes or pricing. Before delivery, a final pass is completed so clients receive the most current view that fits the same scope and rules.

Mordor Intelligence's Humidifier Market Size Compared With Other Published Estimates

Published market sizes for humidifiers often differ because teams do not count the same product basket, they anchor on different base years, and they convert units to dollars using different pricing logic. Timing also matters since some estimates are updated more frequently, which changes what each publisher treats as current.

Replacement items like standalone filters and wicks sit outside Mordor Intelligence's humidifier market scope, which can lower the reported value versus estimates that include ongoing consumables, accessories, or broader indoor air product lines. Gaps can also come from how prices are projected, where one model assumes faster smart-feature premiumization, and another keeps pricing flatter by region. The size can shift when a publisher uses a more aggressive demand curve for new builds and whole-house adoption without confirming it through installer and distributor checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.14 B (2026) | |

| Global Consultancy A | USD 4.73 B (2024) | Uses an earlier base year and may emphasize reported revenues in mature regions, which can understate faster adoption in newer APAC demand pockets and delay price mix shifts into the forecast. |

| Industry Publisher B | USD 10.90 B (2024) | Likely applies a wider inclusion set across related indoor air and broader humidification value streams, which can pull in adjacent categories and inflate totals compared with a device-only revenue view. |

The spread across the table is mainly explained by what gets counted as humidifier revenue and how current-year pricing and mix are treated. By tying volumes to adoption, replacement cycles, and region-level price bands, the model stays traceable to clear inputs that can be rechecked as market conditions change.

Key Questions Answered in the Report

What is the current size and growth outlook for the humidifier market?

The humidifier market size is USD 5.14 billion in 2026 and is projected to reach USD 7.11 billion by 2031 at a 6.72% CAGR, supported by hygiene innovation, HVAC integrations, and steady adoption in homes and critical facilities.

Which region is expanding the fastest within this space?

North America holds the largest regional position, while Asia-Pacific is projected to post the fastest growth through 2031, driven by first-time buyers and increased IAQ awareness in major urban centers.

Which product types are leading to demand today?

Ultrasonic models lead based on price and availability, while evaporative designs are gaining preference among buyers focused on reduced mineral residue and easier maintenance in the humidifier market.

What segments are driving commercial and industrial demand?

Offices, healthcare spaces, data centers, and cleanrooms require tight humidity control for comfort and equipment protection, which sustains specification-grade demand and service contracts.

How are maintenance and hygiene concerns being addressed?

Premium devices adopt UV treatment and durable tank materials, while guidance from public health agencies emphasizes regular cleaning and appropriate water use to lower microbial risks.

What drives the choice between portable and whole-house systems?

Portables offer immediate setup for renters and smaller rooms, while whole-house systems integrate with HVAC for uniform coverage and lower water waste, an approach favored during renovations and replacements in the humidifier market.

Page last updated on: