Air Conditioner Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

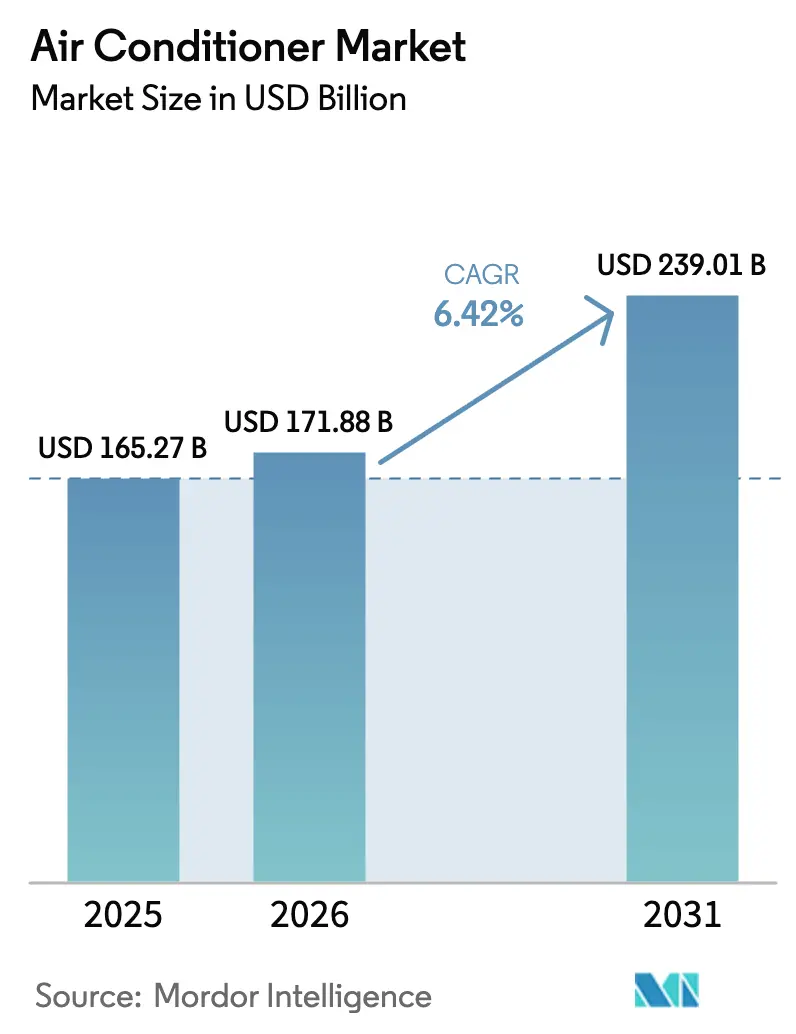

| Market Size (2026) | USD 171.88 Billion |

| Market Size (2031) | USD 239.01 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

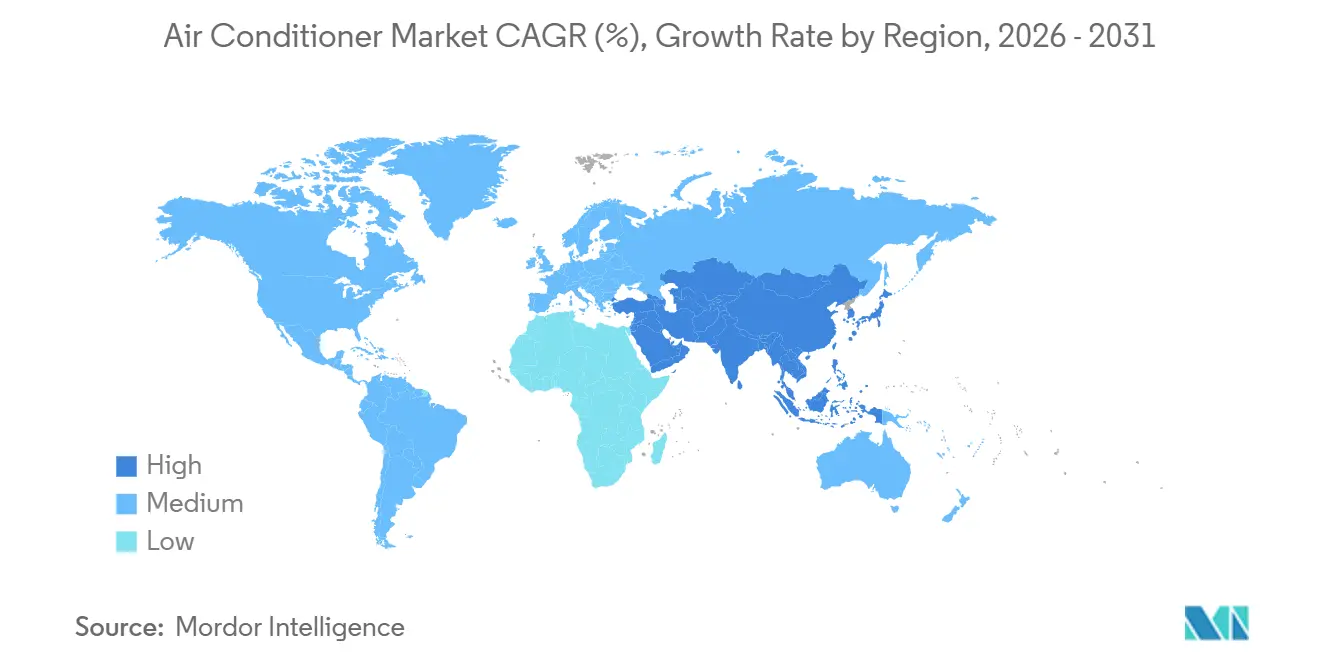

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Conditioner Market Analysis by Mordor Intelligence

The Air Conditioner Market size is projected to be USD 165.27 billion in 2025, USD 171.88 billion in 2026, and reach USD 239.01 billion by 2031, growing at a CAGR of 6.42% from 2026 to 2031.

Rising urban temperatures and longer heat seasons are structurally increasing cooling demand worldwide. Cooling degree-days in major cities have increased by 15–20% since 2020, lifting baseline appliance usage. Air conditioning is now widely regarded as essential infrastructure in dense urban environments rather than a discretionary purchase. The adoption of inverter-based air conditioners has accelerated as price gaps with conventional systems narrow. Consumers increasingly recover higher upfront costs within two years through lower electricity bills. Policy incentives and tighter energy-efficiency standards are further encouraging the shift toward high-efficiency products. Split air-conditioning systems remain the dominant product category due to performance and energy advantages. Meanwhile, portable and compact air conditioners are gaining popularity among renters and remote workers. Together, climate pressure, regulatory support, and improving technology economics are underpinning sustained market expansion.

Key Report Takeaways

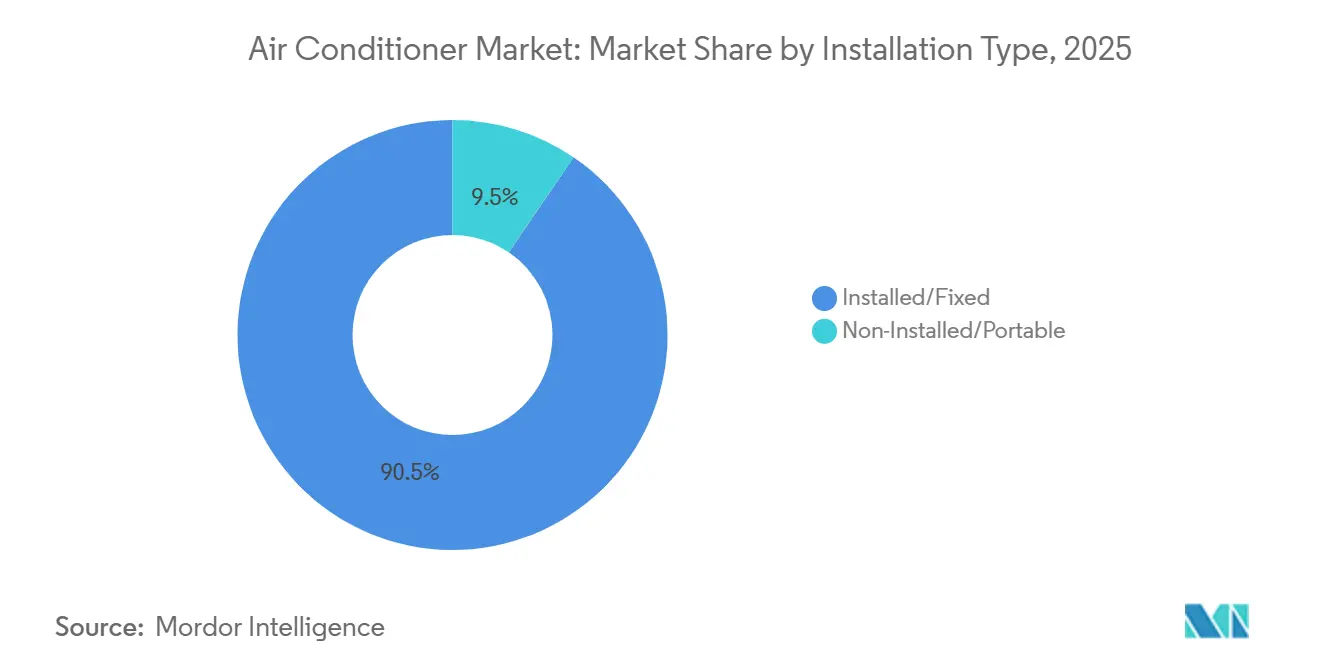

- By installation type, installed or fixed units held 90.48% of the air conditioner market size in 2025, while portable units are forecast to grow at a 7.53% CAGR through 2031.

- By product type, split systems commanded 68.67% of the air conditioner market size in 2025, whereas portable ACs will post the fastest 7.53% CAGR to 2031.

- By end user, the residential segment captured 71.49% of the air-conditioner market share in 2025, while commercial applications are projected to expand at a 7.21% CAGR through 2031.

- By technology, inverter products contributed 71.85% of the air conditioner market size in 2025 and are expected to grow at a 7.57% CAGR, outpacing non-inverter models.

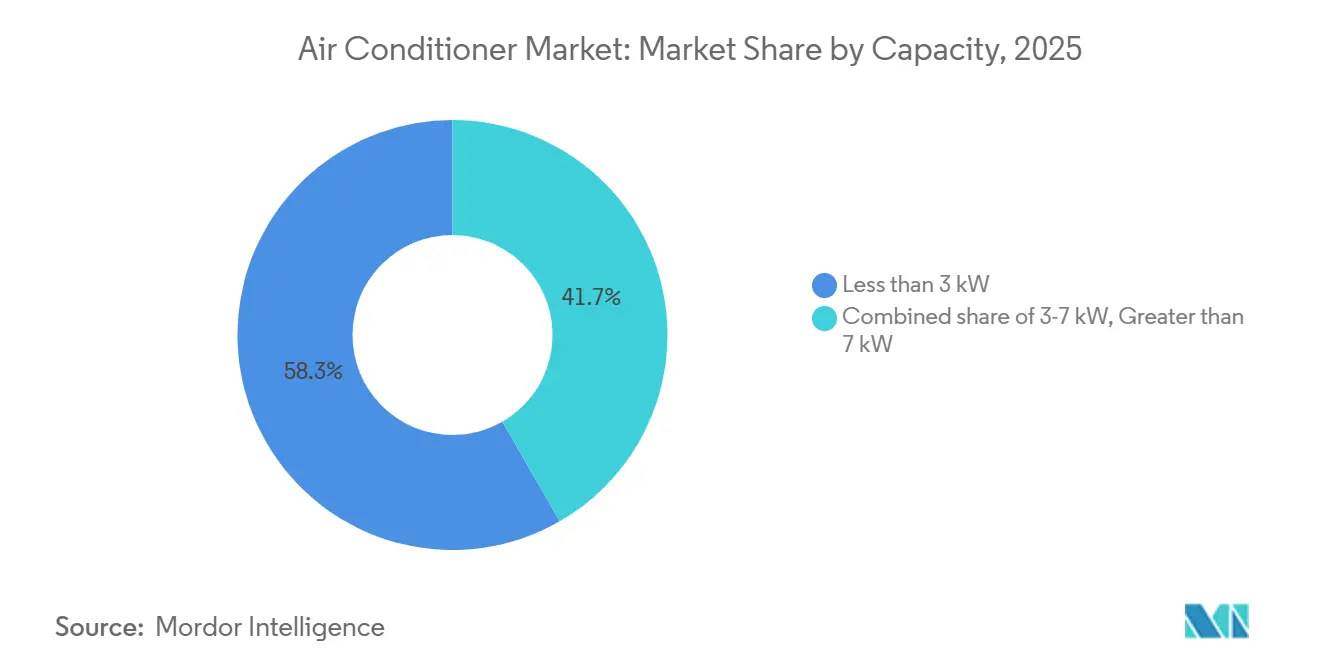

- By capacity, air conditioners with <3 kW accounted for 58.32% of the air conditioner market size in 2025, while units in the 3–7 kW range represented 9.08%, reflecting strong demand for lower-capacity systems.

- By distribution channel, B2C retail controlled 74.84% of the air conditioner market share in 2025, yet B2B direct deals are advancing at a 5.64% CAGR as cooling-as-a-service gains traction.

- By geography, Asia-Pacific generated 47.01% of the air conditioner market size in 2025, and the Middle East and Africa region is forecast to grow at a 7.52% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Air Conditioner Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying urban heat-island effects and rising temperature anomalies | +1.2% | APAC megacities, Middle East, United States Sun Belt | Long term (≥ 4 years) |

| Rising disposable income among the emerging middle class | +1.5% | India, Southeast Asia, Indonesia, MEA | Medium term (2-4 years) |

| Accelerated adoption of energy-efficient inverter AC technology | +1.1% | North America, the EU, Japan, and South Korea | Medium term (2-4 years) |

| Government incentives and subsidies promoting high-star-rated air conditioners | +0.9% | India, China, EU | Short term (≤ 2 years) |

| Commercial lease mandates emphasizing workplace comfort and wellness | +0.6% | North America, EU, APAC corporate hubs | Medium term (2-4 years) |

| AI-enabled predictive maintenance reduces the total cost of ownership | +0.5% | North America, EU, APAC early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Urban Heat-Island Effects and Rising Temperature Anomalies

Urban cores such as Delhi, Phoenix, and Dubai now record cooling degree-day increases of 15–20% compared to previous years, which strengthens year-round demand for residential and commercial cooling. Higher night-time temperatures keep AC systems running for longer hours, lengthening daily load profiles by three to four hours. Dense building materials trap daytime heat, so municipalities like Singapore and Abu Dhabi impose indoor temperature standards that effectively require constant air-conditioner operation. As regulations solidify these requirements, replacement cycles shorten because equipment experiences greater annual run-time. Customers respond by choosing premium, energy-efficient units to avoid high electricity bills. Manufacturers with efficient split systems, therefore, benefit from accelerated replacement demand.

Rising Disposable Income Among the Emerging Middle Class

Households in India, Indonesia, Vietnam, and the Philippines are moving past the USD 5,000-7,000 annual income threshold, which is when AC ownership becomes attainable. India’s Production-Linked Incentive (PLI) scheme triggered USD 1.2 billion of fresh investment in local AC manufacturing and helped cut inverter split prices by 12–15% since 2022 [1]Source: Ministry of Heavy Industries, “Production Linked Incentive Scheme for Air Conditioners,” DHI.nic.in. Similar income gains in Indonesia reveal a latent pool of 40–50 million potential buyers. Because the income elasticity of AC demand exceeds 1.8, even modest wage growth generates strong incremental sales. More accessible retail prices and finance options speed first-time adoption, creating a broad base for the air-conditioner market.

Accelerated Adoption of Energy-Efficient Inverter AC Technology

The cost gap between inverter and fixed-speed compressors has narrowed, and new United States efficiency rules require a seasonal energy-efficiency ratio above 15.0 for split systems. Japan’s Top Runner Programme sets energy-efficiency standards by using the most efficient products as benchmarks, pushing all manufacturers to improve. It has driven the adoption of high-efficiency appliances and vehicles, reducing energy use and emissions while promoting sustainable technology. [2]Source: United Nations SDG Partnerships, “Top Runner Programme,” sdgs.un.org. Utilities in California complement legislation with rebates that shave 15–20% from the installed cost of smart inverter systems. Buyers also value faster cooling and quieter operation, benefits that encourage hospitality and healthcare clients to pay an 8–10% price premium. As production volumes climb, economies of scale will continue to reduce retail prices, helping inverter technology dominate.

Government Incentives and Subsidies Promoting High-Star-Rated Air Conditioners

Globally, governments are promoting high-efficiency air conditioners through labeling programs, rebates, and tax incentives to reduce electricity consumption and carbon emissions. For instance, Bureau of Energy Efficiency (BEE) star ratings are a grading system widely used in India to indicate the energy efficiency of electrical appliances. This system employs a simple five-star scale, making it easy for consumers to gauge the energy consumption of a product and its potential impact on electricity bills.[3]Source: Bureau of Energy Efficiency (BEE), “Star Labeling Program for Appliances,” beeindia.gov.in. Programs like India’s BEE star ratings exist in Japan, the United States, and Europe, where energy labels help consumers identify top-performing AC units. Many countries link financial benefits, such as subsidies or rebates, to ACs that meet high efficiency criteria, making energy-saving models more affordable. These initiatives help curb peak electricity demand, lower household energy costs, and support national climate and energy efficiency goals. They also drive manufacturers to innovate, introducing inverter technology, smart controls, and eco-friendly refrigerants to improve performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial cost compared with room coolers, limiting adoption in low-income regions | -0.8% | South Asia, Sub-Saharan Africa | Short term (≤ 2 years) |

| Strict refrigerant phase-out regulations are increasing compliance costs | -0.6% | EU, North America, Japan, South Korea | Medium term (2-4 years) |

| Grid instability and peak-load penalties restrict AC usage in vulnerable regions | -0.5% | South Asia, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| ESG-linked financing discourages investment in non-green HVAC solutions | -0.4% | Global financial hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High initial Cost Compared with Room Coolers, Limiting Adoption in Low-Income Regions

In low-income households earning under USD 3,000 annually, air conditioner ownership remains limited due to the high upfront cost of entry-level inverter split ACs, which range from USD 350 to 450, compared to evaporative or room coolers priced at USD 50 to 100. Limited access to formal financing and credit facilities further restricts purchases, as many consumers work in the informal economy. Rural and semi-urban areas face additional barriers from unreliable electricity supply, making consistent use of AC units challenging. Consequently, premium air conditioners are concentrated in urban and high-income pockets, leaving potential demand in smaller towns and villages largely untapped. Even with subsidies or government incentives, adoption is slow until household incomes increase and financing options expand. This cost barrier also influences consumer preferences, with many opting for energy-efficient but lower-cost alternatives that meet basic cooling needs.

Stringent Refrigerant Phase-Out Regulations are Increasing Compliance Costs

The air conditioner market faces increasing regulatory pressure as governments worldwide phase out high-global-warming-potential (GWP) refrigerants. In the European Union, for example, the revised F-Gas Regulation prohibits new AC units using refrigerants with a GWP above 750 from January 1, 2025, forcing manufacturers to transition to low-GWP alternatives. [4]Source: Refrigerants Center, “When Was R 410A Banned,” refrigerantscenter.com. Compliance requires re-engineering product designs, investing in new manufacturing lines, and conducting extensive testing to meet safety and efficiency standards. These shifts can increase production costs, which are often passed on to consumers, limiting affordability in price-sensitive markets. Additionally, supply chain disruptions for approved low-GWP refrigerants may cause delays in product availability and price volatility. Overall, stringent refrigerant regulations act as a significant barrier for market expansion, particularly in emerging economies where cost and infrastructure constraints are more pronounced.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Installation Type: Fixed Units Anchor Revenue

Installed units accounted for 90.5% of 2025 revenue, underlining a long-standing preference for permanent cooling in homes and commercial properties. Builders integrate AC piping during construction, and code requirements in hot climates reinforce this habit. Rental growth and remote work, however, generate fresh demand for portable models, which are forecast to expand at a 7.53% CAGR through 2031.

Although efficiency is lower, innovative dual-inverter portables are closing the performance gap. Retailers position these products as an entry point for price-sensitive renters, broadening the customer pool for the air-conditioner market. Portable units serve seasonal needs in temperate Europe, where heat waves last several weeks rather than months. Manufacturers now add Wi-Fi controls and smart-home compatibility, which raises perceived value.

Over time, owners of portable units often upgrade to fixed splits when they buy a home, supporting a steady replacement pipeline. The installed segment, therefore, retains dominance, yet portables inject incremental growth and help brands establish early relationships with new customers.

By Product Type: Split Systems Dominate

Split systems generated 68.67% of 2025 revenue due to their superior noise profile, energy efficiency, and flexible installation. Portable ACs will grow at a 7.53% CAGR, but their base is smaller, so they will not displace splits in the forecast period. Window units still attract buyers in retrofit projects with limited wall space, especially in North America.

Cassette and rooftop systems cater to offices, hotels, and retail, where ceiling-mount installations free floor space. Product boundaries are converging. New split systems add multi-zone capability once reserved for ducted HVAC, while premium window units now ship with inverter compressors. Daikin’s Emura line features air-purification inserts to combat urban pollution.

Mitsubishi Electric links up to eight indoor heads to one outdoor unit, optimizing capacity in large apartments. Such innovation sustains strong interest in splits and solidifies their majority position in the air-conditioner market.

By End-User: Residential Leads

Households represented 71.49% of demand in 2025 because the purchase decision is often made at the family level. Rising income and smaller urban apartments drive the adoption of compact 1–1.5-ton splits. Commercial demand is accelerating at a 7.21% CAGR, led by offices, healthcare, and hospitality.

Hotels in hot climates must deliver 24/7 comfort, and hospitals need strict temperature and air-quality control. Office developers choose variable-refrigerant-flow systems that adjust output to measured occupancy, cutting energy use by up to 30%. Retailers design micro-climate zones to extend customer dwell time. Education ministries in emerging markets fund AC units in classrooms because cooler environments improve test scores. The commercial share therefore widens gradually, although residential volume remains the backbone of the air-conditioner market size projection.

By Technology: Inverter Ascendancy

Inverter models captured 71.85% of 2025 shipments and will expand at a 7.57% CAGR through 2031. Regulatory minimums require SEER ratings that fixed-speed units cannot economically achieve. Variable-speed compressors cut electricity use by up to 40% and reach set points faster, advantages that customers recognize even in first-time purchases.

Production scale has lowered the price premium to 15–20% compared with 40–50% in 2020. Non-inverter units persist in markets where electricity costs less than USD 0.08 per kWh. Yet as grids modernize and tariffs rise, running costs will push more buyers toward inverters. China’s new efficiency labels restrict the top rating tiers to inverter models, giving them better shelf placement. The technological transition is therefore a central pillar of expected growth in the air-conditioner market.

By Capacity: Mid-Range Expansion

Sub-3 kW systems held 58.32% of sales in 2025 because single-room cooling remains common. Mid-range 3–7 kW units represented 9.08% of sales in 2025 because multiple-room apartments, small clinics, and boutique hotels fit neatly into this band. Building information modeling software now guides right-sizing, discouraging the traditional practice of oversizing.

Accurate sizing improves comfort and trims costs, nudging consumers toward the mid-range. Suppliers answer with modular outdoor compressors that connect different indoor capacities, enabling room-by-room customization. This flexibility appeals to households upgrading from single-room units as their income improves. The segment’s strong forecast makes it a focus for component standardization and scale economies that underpin profit growth in the air-conditioner market.

By Distribution Channel: Retail Dominance

B2C retail accounted for 74.84% of 2025 volume because households value in-store demonstrations and immediate installation scheduling. Multi-brand outlets facilitate price comparisons, while exclusive brand stores maintain premium service standards. E-commerce grows quickly because platforms bundle financing, installation, and extended warranties in a single checkout flow. B2B channels will narrow the gap, rising 5.64% CAGR, as large property owners sign cooling-as-a-service contracts that transfer maintenance responsibility to manufacturers. Digital procurement hubs let hotel chains aggregate orders and negotiate lower prices. These developments widen the sales toolbox for suppliers and enhance channel resilience across the air-conditioner market.

Geography Analysis

The Asia-Pacific region accounted for 47.01% of global air conditioner revenue in 2025 and is expected to grow at over 7.17% CAGR. China drives much of the demand through rapid replacement in coastal cities and rising adoption inland. India’s production-linked incentives have lowered retail prices and attracted significant factory investment, boosting local supply. Emerging markets such as Indonesia, Vietnam, and the Philippines represent tens of millions of potential first-time buyers due to low penetration rates.

Japan and South Korea are mature markets, but steady replacement cycles and premium pricing continue to support revenue growth. Strict energy-efficiency regulations in both countries maintain inverter systems as the dominant technology.

North America represents about a quarter of global revenue, with the United States Sun Belt concentrating most demand due to population growth and longer summers. Federal efficiency standards are accelerating the shift to inverter air conditioners. Urban centers in Canada are seeing rapid adoption as traditional passive cooling becomes insufficient. Mexico presents a mixed picture, with high penetration in border regions but slower uptake in the south due to grid limitations. Replacement cycles and rising incomes continue to support revenue growth in mature markets. Manufacturers offering high-efficiency solutions are well-positioned to capture the evolving demand.

Competitive Landscape

The global air conditioner market remains moderately competitive, with leading players such as Daikin, Gree, Midea, Carrier, and LG capturing a significant share of shipments while still leaving opportunities for smaller firms to compete. Each of these leading firms invests heavily in research and development, focusing on low-GWP refrigerants and AI-enabled control systems. For instance, Daikin allocated substantial funds in 2024 toward next-generation refrigerant solutions, signaling a strong commitment to innovation. Gree and Midea maintain cost advantages through vertical integration, producing the majority of their components in-house. This strategy allows them to offer aggressive pricing in the value-oriented segment while protecting margins.

Digital and IoT-enabled services have become key differentiators for premium brands in commercial and industrial applications. Carrier’s Abound and Trane’s Tracer SC+ platforms help reduce downtime significantly for clients while enabling new business models such as cooling-as-a-service. These platforms have attracted a notable number of corporate customers in North America within months of launch. Firms without strong IoT capabilities risk losing contracts for large office buildings or data-center projects. As a result, digital innovation is increasingly shaping competitive positioning in the air-conditioner market.

Regulatory frameworks also play an important role in shaping market rivalry and product strategies. Global brands with flexible refrigerant portfolios can serve multiple markets despite differing national rules. For example, Gree secured approval for environmentally friendly refrigerants in the United States, strengthening its market position. Smaller companies often struggle with repeated certification costs and technician training, which may accelerate consolidation. Meanwhile, patent activity remains concentrated in areas such as compressor efficiency, where Japanese and South Korean manufacturers continue to hold a technological edge.

Air Conditioner Industry Leaders

Haier Group

Daikin Industries

Gree Electric Appliances

Midea Group

Carrier Global

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Samsung India launched its BESPOKE AI WindFree™ AC range with 19 new models featuring advanced AI‑driven cooling, WindFree™ technology for gentle airflow, and SmartThings connectivity. The series offers features such as AI Energy Mode for up to 30% savings, rapid cooling, remote app control, and voice assistant support.

- January 2025: LG Electronics unveiled its latest DUALCOOL™ AI Air conditioner, featuring enhanced AI technologies designed to optimize comfort, energy efficiency, and air quality. The unit uses AI Core Tech and a Human Detecting Sensor to intelligently adjust temperature, airflow direction, and speed based on room conditions and user behavior.

- July 2025: Panasonic Malaysia launched its next-generation X Premium Inverter Series of air conditioners that combine powerful cooling with advanced air purification using proprietary nanoe™ X technology for cleaner, healthier indoor air. The smart 2-in-1 system features real-time air quality monitoring, dust and odour sensors, and enhanced purification that targets pollen, bacteria, and odours.

- July 2025: Xiaomi has launched the new Mijia Central Air Conditioner Pro Dual Air Wheel series, its most advanced central AC system, available in standard and dual outlet versions with capacities from 5 HP to 8 HP. The model features robust performance in extreme temperatures, rapid cooling, and high airflow with a 556 mm dual air wheel delivering strong circulation.

Global Air Conditioner Market Report Scope

An air conditioning unit is a device or system designed for the purpose of regulating temperature, humidity, and air quality in an open area, usually such as a room or building. It is capable of cooling the indoor air to a comfortable level by removing the heat from the air in the room and transferring it outside.

Air conditioner market is segmented by installation type, product type, end-user, technology, capacity, distribution channel, and geography. By installation type, the market is segmented into installed/fixed, non-installed/portable. By product type, the market is segmented into window air conditioner (AC), split air conditioner (AC), portable air conditioner (AC), cassette air conditioner (AC), packaged & rooftop air conditioner (AC). By technology, the market is segmented into inverter and non-inverter. By end user, the market is segmented into residential and commercial. By capacity, the market is segmented into <3 kW, 3-7 kW, and >7 kW. By distribution channel, the market is segmented into B2B/direct from the manufacturers, B2C/retail consumers. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Installed/Fixed |

| Non-Installed/Portable |

| Window Air Conditioner (AC) |

| Split Air Conditioner (AC) |

| Portable Air Conditioner (AC) |

| Cassette Air Conditioner (AC) |

| Packaged & Rooftop Air Conditioner (AC) |

| Residential |

| Commercial |

| Inverter |

| Non-Inverter |

| <3 kW |

| 3-7 kW |

| >7 kW |

| B2B/Direct from the Manufacturers | |

| B2C/Retail Consumers | Multi-Brand Stores |

| Exclusive Brand Stores (EBOs) | |

| Online | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia | |

| Rest of APAC | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Installation Type | Installed/Fixed | |

| Non-Installed/Portable | ||

| By Product Type | Window Air Conditioner (AC) | |

| Split Air Conditioner (AC) | ||

| Portable Air Conditioner (AC) | ||

| Cassette Air Conditioner (AC) | ||

| Packaged & Rooftop Air Conditioner (AC) | ||

| By End-User | Residential | |

| Commercial | ||

| By Technology | Inverter | |

| Non-Inverter | ||

| By Capacity | <3 kW | |

| 3-7 kW | ||

| >7 kW | ||

| By Distribution Channel | B2B/Direct from the Manufacturers | |

| B2C/Retail Consumers | Multi-Brand Stores | |

| Exclusive Brand Stores (EBOs) | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia | ||

| Rest of APAC | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How large is the global air-conditioner market in 2026?

The air-conditioner market size is USD 171.88 billion in 2026 and is projected to reach USD 239.01 billion by 2031, growing at a 6.42% CAGR.

Which region contributes the most to global sales?

Asia-Pacific generates 47.01% of total revenue, and the Middle East and Africa region is the fastest-growing at a 7.52% CAGR.

What technology is gaining the quickest share?

Inverter compressors already make up 71.85% of shipments and are expanding faster than non-inverter models because of efficiency rules and rising electricity costs.

Why are portable AC sales rising?

Remote work and rental housing favor plug-and-play units that avoid permanent wall changes, so portable models are expected to grow at a 7.53% CAGR.

How are regulations influencing product design?

The EU and United States restrict high-GWP refrigerants and set higher efficiency minimums, so manufacturers redesign systems for R-32 or R-454B and adopt inverter technology.

What business model changes are emerging?

Cooling-as-a-service subscriptions, supported by AI predictive maintenance, let customers pay per cooling hour and shift maintenance risk to manufacturers.

Page last updated on: