Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.26 Billion |

| Market Size (2026) | USD 10.79 Billion |

| Market Size (2031) | USD 13.92 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

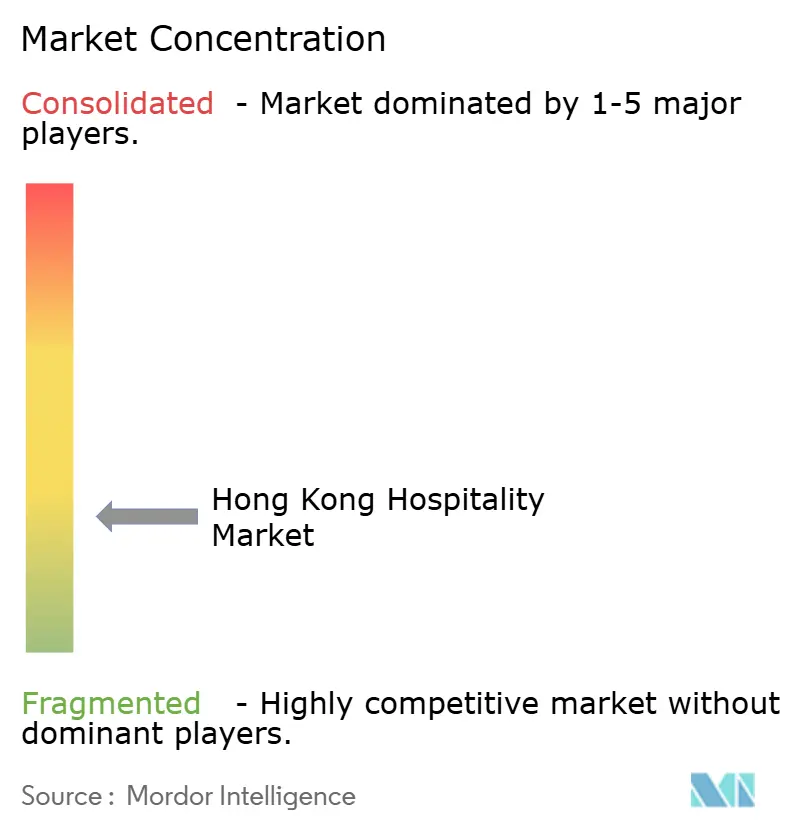

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Hospitality Market Analysis by Mordor Intelligence

The Hong Kong Hospitality Market size was valued at USD 10.26 billion in 2025 and estimated to grow from USD 10.79 billion in 2026 to reach USD 13.92 billion by 2031, at a CAGR of 5.22% during the forecast period (2026-2031).

The reopening of borders with mainland China facilitated a swift recovery in visitor arrivals, which approached 2019 levels by late 2024. This rebound drove premium hotel average daily rates to pre-pandemic levels during key holiday periods, such as the Lunar New Year in 2025. Government capital spending exceeding HKD 30 billion (USD 3.86 billion) on sport, culture, and transit nodes, most prominently Kai Tak Sports Park and the USD 13 billion Sky Topia airport precinct, adds fresh demand generators while easing geographic concentration risk[1]Government of Hong Kong, “Development Blueprint for Tourism Industry 2.0,” info.gov.hk . Hoteliers simultaneously accelerate mobile-first direct-booking engines, diversify toward halal-certified and pet-inclusive offerings, and embed smart-room technologies to manage wage inflation and labour shortages. These structural upgrades, coupled with resurgent international MICE activity and policy incentives such as the Tourism Industry 2.0 blueprint, anchor the next growth leg for the Hong Kong hospitality market.

Key Report Takeaways

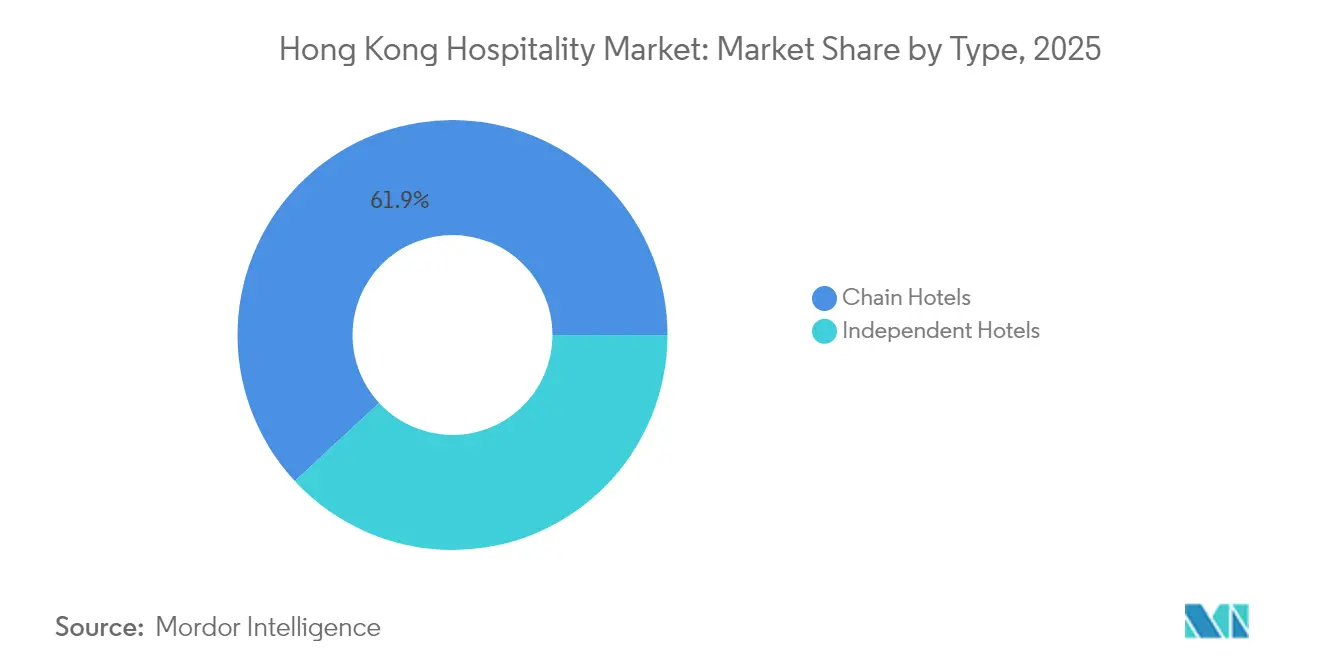

By type, chain hotels held 62.37% of the Hong Kong hospitality market share in 2024, whereas independent hotels are predicted to post a 6.21% CAGR through 2030.

By accommodation class, luxury properties accounted for 38.37% of the Hong Kong hospitality market size in 2024, while service apartments are forecast to grow fastest at a 6.98% CAGR to 2030.

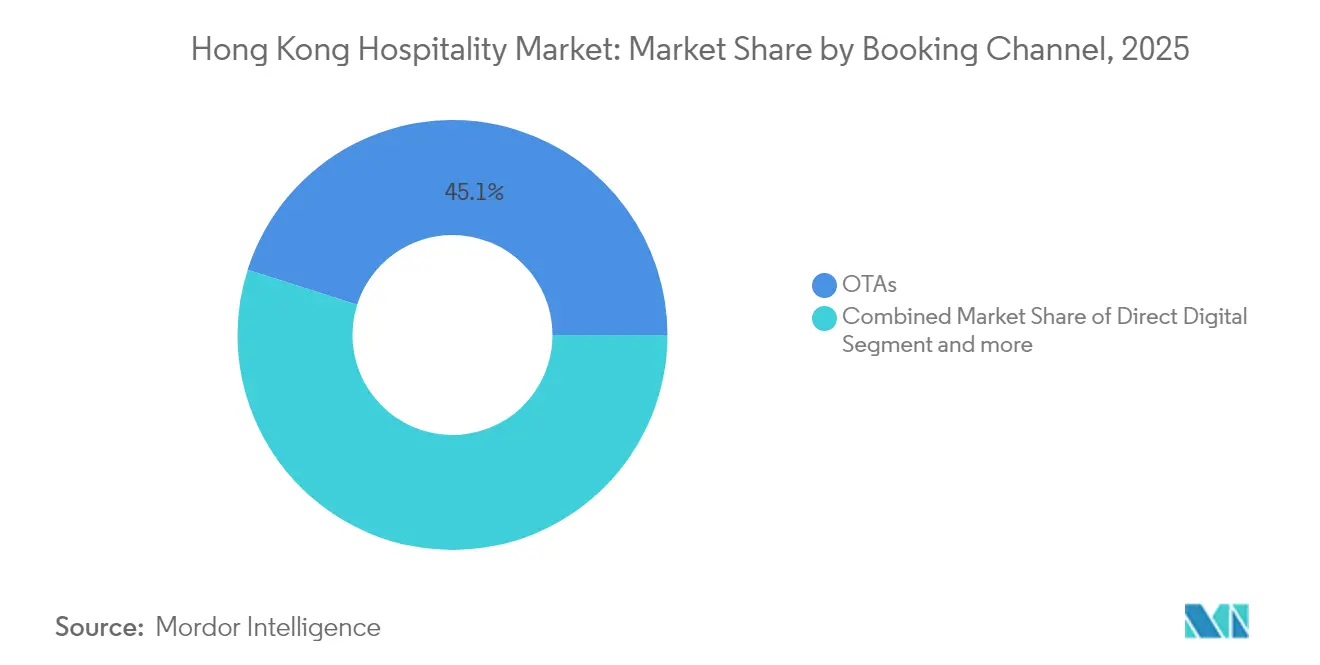

By booking channel, OTAs contributed 45.64% of the Hong Kong hospitality market share in 2024 value, yet direct digital channels are expected to accelerate at a 9.89% CAGR to 2030.

By geography, Kowloon controlled 35.74% of the Hong Kong hospitality market share in 2024, whereas Lantau Island is projected to record the highest 5.98% CAGR between 2025-2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hong Kong Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mainland Chinese leisure travel post-border reopening | +1.5% | Hong Kong Island, Kowloon core districts | Short term (≤ 2 years) |

| Recovery of international MICE events via HKTB subsidy schemes | +1.2% | Global, with a concentration in the Kowloon convention areas | Medium term (2-4 years) |

| Government investment in tourism infrastructure (Kai Tak Sports Park) | +0.8% | Lantau Island, New Territories, with spillover to Kowloon | Long term (≥ 4 years) |

| Expansion of direct mobile bookings | +0.9% | Global reach with Asia-Pacific concentration | Medium term (2-4 years) |

| Growing halal-certified room demand from ASEAN visitors | +0.6% | ASEAN markets, the Middle East, with Hong Kong with a wide impact | Long term (≥ 4 years) |

| Pet-friendly staycation trend among local millennials | +0.4% | Local Hong Kong market, regional spillover potential | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Mainland Chinese Leisure Travel Post-Border Reopening

Visitors' spend patterns now tilt toward premium room categories, enabling hotels to sustain 2019 ADR benchmarks even as total arrivals remain below historic peaks. Strategic alliances between the Hong Kong Tourism Board and mainland digital-travel platforms reinforce this momentum by embedding instant-payment options and dynamic content in Mandarin. The Hong Kong hospitality market benefits further from policy moves allowing multi-entry visas for tech entrepreneurs, encouraging repeat trips, and weekday demand bursts. Crucially, these travellers increasingly favour micro-cations, two to three-night itineraries stitched around shopping, gastronomy, and emerging cultural venues, creating predictable compression on prime-district inventory.

Recovery of International MICE Events via HKTB Subsidy Schemes

HKTB’s scheme underwriting venue rental and attendee-marketing costs helped secure more than 60 confirmed international conventions and exhibitions for 2025-2027[2]Laotian Times, “HKTB Drives Strong MICE Rebound Over 60 World-class MICE Events Secured, Solidifying World’s Meeting Place Appeal,” laotiantimes.com. The extension of delegate stays for leisure purposes has resulted in increased ancillary spending, thereby enhancing food and beverage (F&B) capture ratios at integrated convention hotels in Kowloon. Industry reports indicate that corporate MICE (Meetings, Incentives, Conferences, and Exhibitions) revenue now constitutes a substantial share of peak-season earnings. This trend, compared to pre-pandemic levels, reflects a structural transformation within Hong Kong's hospitality market, with a growing emphasis on higher-margin group business. This shift underscores the evolving dynamics of the sector, where integrated convention hotels are capitalizing on the rising demand for corporate and leisure hybrid travel experiences.

Government Investment in Tourism Infrastructure (Kai Tak Sports Park)

Kai Tak Sports Park, Hong Kong’s largest single tourism build at HKD 30 billion (USD 3.86 billion), features a 50,000-seat main stadium, indoor arenas, a vast retail promenade, and an omnichannel ticketing platform integrated with public-transport smart cards[3]South China Morning Post, “Hong Kong’s Kai Tak Sports Park ‘new stage’ for mega-events economy,” https://www.scmp.com/ . The MTR interchange in Hong Kong improves transfer efficiency between Central and Tsim Sha Tsui, facilitating a more balanced distribution of visitor traffic across the city. Findings from 2024 trial events highlight an increase in the average visitor stay duration, driven by heightened engagement with cultural clusters in Kowloon East. The implementation of advanced technologies, such as cashless payment systems within stadiums and real-time crowd-flow monitoring dashboards, strengthens Hong Kong's positioning as a tech-enabled destination for Gen-Z travellers, supporting the long-term growth of its hospitality market.

Expansion of Direct Mobile Bookings

AI-powered booking engines formulate real-time personalized offers based on browsing history, loyalty tier, and even weather forecasts, lifting ancillary revenue through upsold breakfasts and late-checkout bundles. Hotel ICON’s kiosk-enabled lobby check-in slashes front-desk staffing needs, demonstrating how digitalization offsets labour shortages while elevating guest satisfaction ratings. Independent properties benefit disproportionately because a sleek user interface levels the marketing playing field against global chains, gradually trimming heavy OTA commissions. As 5G coverage expands across mass-transit nodes, mobile bookings for same-day stays rise, softening occupancy volatility and underpinning stable yield management in the Hong Kong hospitality market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile inbound demand from geopolitical/health shocks | -0.8% | Global impact with Asia-Pacific concentration | Short term (≤ 2 years) |

| Labor shortages & rising wage costs | -0.6% | Hong Kong-wide, with service-intensive segments most affected | Medium term (2-4 years) |

| Competition from the Greater Bay Area hotel pipeline | -0.5% | Regional competition affecting Hong Kong market share | Long term (≥ 4 years) |

| Rising electricity tariffs are squeezing budget hotel margins | -0.3% | Local Hong Kong market, budget segment concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Inbound Demand from Geopolitical / Health Shocks

Hong Kong's position as a critical aviation hub renders its hotel booking trends highly susceptible to geopolitical developments and emerging health risks. The forward booking window, which spanned several days before the pandemic, has significantly contracted to just over a day by early 2025. This shift has necessitated the adoption of agile and data-driven pricing models by revenue management teams to address the shortened booking cycles. Hotels are mitigating market volatility by implementing tiered cancellation policies and diversifying their marketing efforts to attract a wider range of feeder markets. However, abrupt regulatory changes, such as unexpected visa restrictions or public health advisories, can lead to an immediate and substantial decline in weekend occupancy rates. To counter these challenges, the hospitality market in Hong Kong increasingly relies on robust liquidity reserves and localized staycation campaigns as strategic measures to sustain operations and drive revenue during periods of uncertainty.

Labor Shortages & Rising Wage Costs

The Hong Kong hospitality market is grappling with a projected cumulative shortfall of service employees by 2028, as evidenced by increasing vacancy rates in front-of-house positions. Wage inflation for specialized roles, such as executive chefs and revenue managers, continues to rise on a year-on-year basis, exerting pressure on gross operating profit margins, particularly for budget and boutique properties. To mitigate labour shortages, large hotel chains are adopting advanced technologies, including robotics for luggage handling and AI-driven chatbots to manage guest inquiries. These organizations are also strengthening their workforce pipelines by establishing apprenticeship programs in collaboration with vocational institutes. However, smaller independent operators face significant challenges in adapting to these trends. Limited financial resources hinder their ability to invest in automation technologies, which raises concerns about potential declines in service quality and competitiveness within the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chain Hotels Consolidate Leadership Through Scale Advantage

In 2025, chain-affiliated properties contributed 61.89% of room revenue in Hong Kong, with a projected CAGR of 6.16%. This performance underscores the competitive advantage of established brands within the hospitality market. International hotel chains leverage extensive loyalty programs and corporate-negotiated rates to secure higher occupancy levels and achieve a more diversified guest mix compared to independent operators. For example, JW Marriott Hong Kong consistently outperforms nearby unbranded competitors in weekday occupancy rates and generates higher food and beverage revenue through exclusive member-focused dining promotions.

Operational scale provides chain-affiliated properties with procurement advantages, enabling them to negotiate region-wide contracts for essentials such as linens and enterprise software, which enhances operating margins. Standardized digital solutions, including mobile keys, AI-driven guest preference systems, and cloud-based property management platforms, further accelerate innovation across chain portfolios. In contrast, independent hotels face rising customer acquisition costs as OTA algorithms increasingly favor established brands with strong performance histories. Many independents are affiliating with soft-brand collections to retain their unique identity while accessing global marketing resources. Asset-light management models continue to drive growth, with recent launches of lifestyle brands like Mondrian and Regent conversions reflecting property owners’ preference for chain alignment to mitigate risks exposed during the pandemic. Independent properties that remain competitive often occupy niche segments, such as heritage buildings, wellness retreats, or co-living spaces, where distinctive positioning supports premium pricing and shields them from market commoditization.

By Accommodation Class: Service Apartments Lead Extended-Stay Demand

Service-apartment inventory is on track for a 6.87% CAGR to 2031, the fastest among all classes in the Hong Kong hospitality market. Mainland tech firms second staff for multi-month stints during IPO roadshows, while global consulting teams prefer residential amenities such as in-unit laundry and kitchenettes that lower meal-per-diem costs. Shama and Oakwood demonstrate higher RevPAR spreads compared to similar four-star operators, driven by longer average guest stays and optimized housekeeping operations, which position them as attractive investments for private-equity firms.

Luxury hotels remain the largest revenue slice at 38.05% thanks to high-net-worth preferences from mainland China, Indonesia, and the Philippines for harbour-view suites, Michelin dining, and personal-luxury shopping access. The Four Seasons advanced refurbishment of its spa floors and rooftop infinity pool in 2024 to preserve ADR leadership. Budget and economy hotels struggle under twin pressures of soaring utilities and wage escalation, prompting some owners to pivot toward mid-scale renovations or co-living formats. The Hong Kong hospitality market, therefore, bifurcates upscale and extended-stay segments that thrive on experiential and functional differentiation, while undifferentiated low-end stock consolidates or exits.

By Booking Channel: Direct Digital Rises Despite OTA Dominance

Online Travel Agencies (OTAs) currently dominate 45.09% of the transaction value within the market. However, direct digital reservations are projected to expand at a CAGR of 9.76%, reflecting operators' focused strategies to enhance profitability and recover margins. Hotel chains are increasingly adopting advanced loyalty platforms that integrate features such as gamified point accrual systems, biometric authentication for secure access, and frictionless payment solutions like one-click Apple Pay. These technological advancements are driving a substantial increase in mobile app bookings, particularly among younger consumer segments, highlighting a shift in booking preferences and the growing importance of digital engagement strategies.

Corporate and MICE portals furnish stable mid-week occupancy, while wholesale and traditional agents maintain a beachhead in escorted-group niches, especially among Tier-3 mainland cities with lower digital penetration. Nevertheless, the gravitational pull toward mobile-driven user journeys is unmistakable, and algorithmic ancillary bundling, airport transfer upsells, and spa credits enrich unit economics. The Hong Kong hospitality market’s shifting channel mix compels continuous data-science investments to personalize price fences and loyalty perks.

Geography Analysis

Kowloon produced 35.33% of room revenue in 2025, defending primacy through the triad of shopping (Harbour City, K11 Musea), culture (West Kowloon Cultural District), and MTR connectivity linking five radial lines. Hotels along Canton Road routinely fill with cross-border shoppers, while convention-centre clusters near Hung Hom drive weekday business blocks. In 2024, as the aviation industry worked toward restoring capacity, five-star hotels in Tsim Sha Tsui demonstrated consistent occupancy levels. This performance underscores the robust and sustained demand within Hong Kong's hospitality sector, even amidst ongoing recovery efforts in the travel and tourism market.

Lantau Island is poised for a 5.89% CAGR as mega-projects redraw its visitor map. Skytopia’s opening phases in 2026-2027 pair a high-rise business district with an immersive entertainment boulevard adjacent to Hong Kong International Airport, elongating passenger stopovers and diverting MICE groups to new expo halls. Kai Tak Sports Park activates East Kowloon spillover demand too, but Lantau hotels capitalize on larger footprints, resort pools, and family-suite layouts unavailable in densely built core districts. Hong Kong Island retains a premium cachet owing to its financial-district adjacency; flagship properties in Central command the market’s highest ADRs. New Territories hotels leverage lower land rents to build expansive ballrooms targeted at association conferences, while Outlying Islands like Cheung Chau cater to wellness retreats and eco-tourism seeker groups. Together, the geographic mosaic diversifies exposure, underpinning the long-run sustainability of the Hong Kong hospitality market.

Competitive Landscape

The Hong Kong hospitality market is highly fragmented, with the top five operators holding more than one-fourth aggregate share, granting nimble independents room to experiment. Marriott International has strategically enhanced its market presence by introducing the 820-room Park Lane Hong Kong Autograph Collection. This development bolsters its luxury-lifestyle segment in Causeway Bay while leveraging the expansive reach of Bonvoy's membership network[4]Marriott International, “Press Release: Park Lane Hong Kong Autograph Collection Launch,” marriott.com . Shangri-La accelerates ESG investments—solar thermal rooftop arrays, AI-driven food-waste reducers, to appeal to corporate RFPs mandating science-based emission targets. The Peninsula brand upgrades its proprietary guest-experience app with carbon-footprint calculators and real-time local event tips, differentiating on service intimacy.

Emergent players carve micro-segments: Ovolo Hotels courts millennials through plant-based F&B, all-inclusive mini-bar policies, and pet-welcome packages that fuel social-media virality. ONYX leases repositioned Grade-A office floors for Shama-branded serviced apartments, capitalizing on hybrid work demand. Technology adoption becomes the arms race: AI revenue-management platforms automate demand forecasting and generate room-type-level dynamic price fences, while guest-facing robots deliver amenities, reducing labour exposure.

Access to capital will shape consolidation. Budget-hotel owners facing utilities and payroll pressure evaluate franchising or asset sales to chain flags that promise margin uplift via central procurement. Conversely, elevated land values constrain greenfield pipeline growth, increasing the allure of asset-light management deals for international chains. These crosscurrents maintain competitive dynamism and opportunity across the Hong Kong hospitality market.

Hong Kong Hospitality Industry Leaders

The Hongkong & Shanghai Hotels Ltd (Peninsula)

Shangri-La Hotels & Resorts

Mandarin Oriental International Ltd

Marriott International

Hilton Worldwide

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Park Lane Hong Kong Autograph Collection officially opened, adding 820 rooms, two specialty restaurants, and a sky-garden bar to the premium inventory on Hong Kong Island.

- January 2025: Miramar Hotel and Investment announced the acquisition of a unit from Henderson Land Development in Hong Kong for HKD 3.12 billion (USD 400.75 million). The company intends to develop a hotel and commercial complex on the acquired property. The transaction, involving Solution Right, strategically located in Hong Kong's Tsim Sha Tsui district, reflects a positive trajectory in the recovery of the local tourism industry post-pandemic.

- November 2024: ONYX Hospitality Group, a leading Southeast Asian hotel and serviced apartment management company, is expanding its Shama brand internationally. Recent openings include Shama Hub Qiantang in Hangzhou, China, Shama Hub Metro South in Hong Kong, and Shama Suasana in Johor Bahru, Malaysia. The company also plans further developments in Malaysia, Laos, and Thailand.

- November 2024: Emperor Entertainment Hotel completed the divestment of its serviced-apartment portfolio for USD 35.4 million, reflecting strategic portfolio optimization as the company focuses on core hotel operations.

Hong Kong Hospitality Market Report Scope

A complete background analysis of the Hospitality Industry in Hong Kong, which includes an assessment of the industry associations, overall economy, and emerging market trends by segments, significant changes in the market dynamics, and market overview is covered in the report.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| Hong Kong Island |

| Kowloon |

| New Territories |

| Lantau Island |

| Outlying Islands |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Hong Kong Island |

| Kowloon | |

| New Territories | |

| Lantau Island | |

| Outlying Islands |

Key Questions Answered in the Report

What is the Hong Kong hospitality market size in 2026?

It totals USD 10.79 billion in 2026 and is projected to reach USD 13.92 billion by 2031.

How fast will the market grow through 2031?

Revenue is expected to increase at a 5.22% CAGR over 2026-2031.

Which accommodation class is expanding fastest?

Service apartments lead with a forecast 6.87% CAGR tied to extended-stay demand from business travellers.

Which district generates the most hotel revenue?

Kowloon commands 35.33% share due to its retail, cultural, and convention assets.

How prominent are mobile direct bookings today?

Mobile channels already contribute more than 40% of online hotel sales and are growing quickly as apps integrate AI personalization.

What structural challenges face operators?

Key issues include labour shortages, rising wage and utility costs, and new competing supply across the Greater Bay Area.

Page last updated on: