Horticulture Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

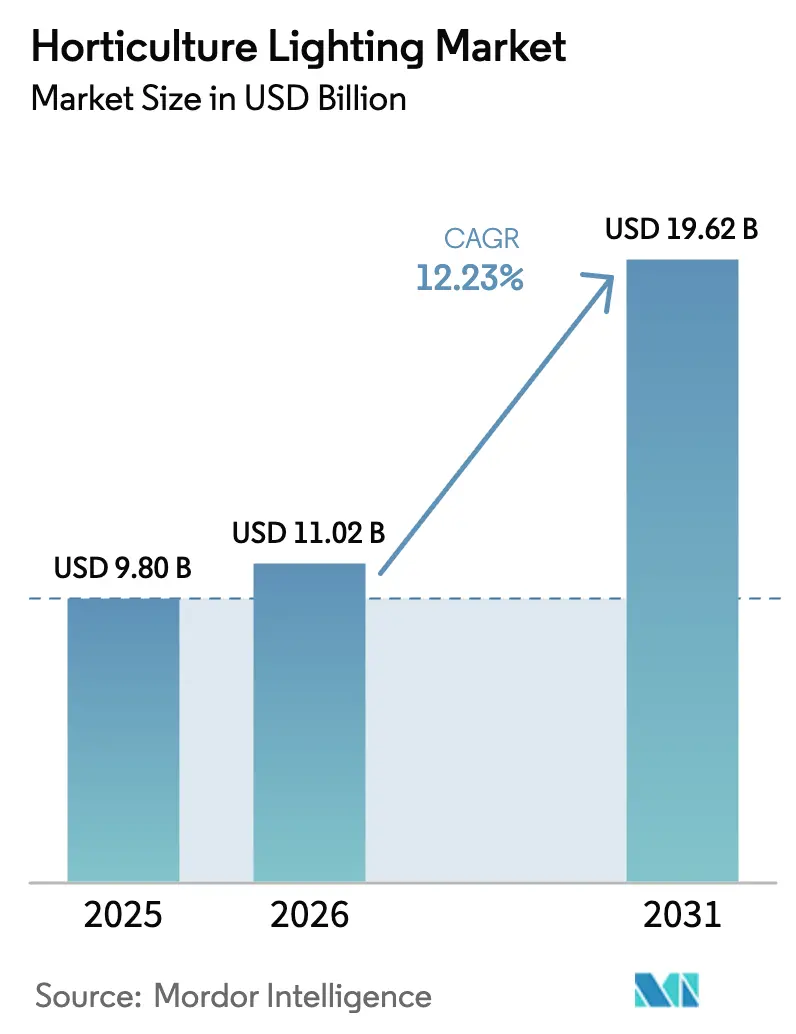

| Market Size (2026) | USD 11.02 Billion |

| Market Size (2031) | USD 19.62 Billion |

| Growth Rate (2026 - 2031) | 12.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Horticulture Lighting Market Analysis by Mordor Intelligence

The horticultural lighting market size is projected to expand from USD 9.80 billion in 2025 and USD 11.02 billion in 2026 to USD 19.62 billion by 2031, registering a 12.23% CAGR between 2026 and 2031. Precision-tuned LED spectra are lifting cannabinoid yields in legalized North American cannabis cultivation, while urban food-security mandates in Asian megacities and the European Union’s Fit-for-55 energy program are triggering rapid retrofits of legacy high-intensity discharge fixtures. Fixture prices have fallen 15-20% since 2024 as Samsung and LG scale semiconductor production, yet plasma and other alternative light sources are re-emerging in research environments that need continuous spectra. Hardware commoditization is steering vendors toward cloud-based spectral analytics, and corporate ESG-linked green bonds are unlocking capital for large retrofit programs.

Key Report Takeaways

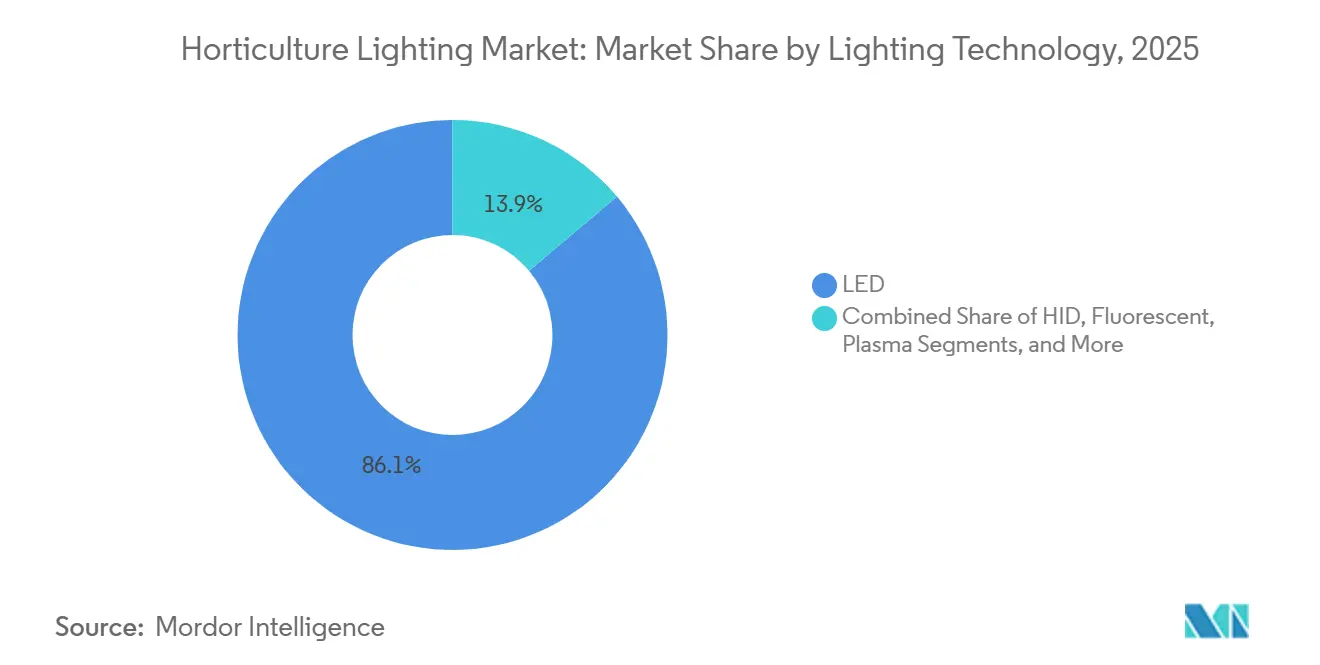

- By lighting technology, LED systems held 86.13% of horticultural lighting market share in 2025, while plasma and other alternatives are advancing at a 12.41% CAGR through 2031.

- By offering, hardware captured 71.52% of revenue in 2025; software and services are forecast to grow at a 12.53% CAGR through 2031.

- By installation type, new builds controlled 58.36% of revenue in 2025, whereas retrofits are projected to expand at a 13.46% CAGR.

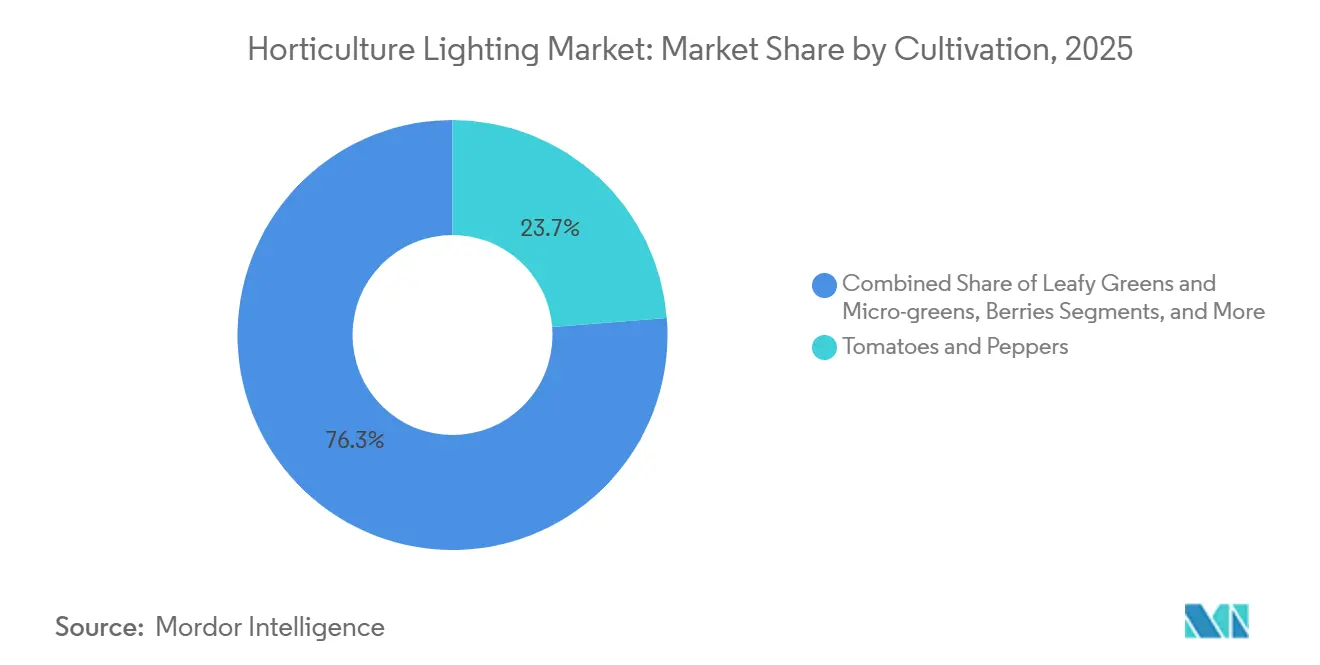

- By cultivation, tomatoes and peppers led with 23.74% of horticultural lighting market size in 2025, and berries are poised for a 15.22% CAGR through 2031.

- By application, greenhouses commanded 49.21% revenue in 2025; vertical farms are expected to post the highest 15.21% CAGR to 2031.

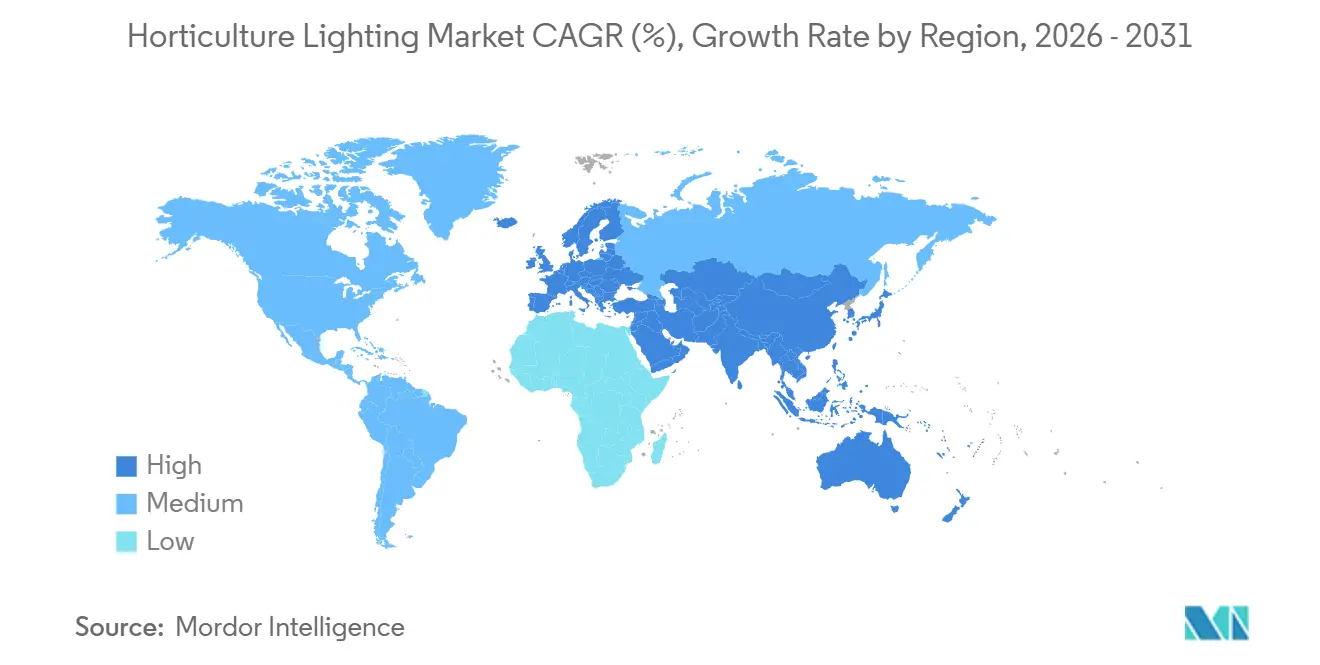

- By geography, Europe dominated with 32.94% share in 2025, and Asia-Pacific is forecast for a 13.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Horticulture Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-tuned LED spectra raising cannabinoid yield in North American cannabis grows | +2.1% | North America, with spillover to Europe and Australia | Medium term (2-4 years) |

| Urban food-security programs accelerating vertical-farm lighting demand across Asian megacities | +2.3% | Asia-Pacific core (Singapore, Tokyo, Seoul, Shanghai), spillover to Middle East | Long term (≥4 years) |

| EU "Fit-for-55" energy directives incentivising LED retrofits in heated glass greenhouses | +1.8% | Europe (Netherlands, Germany, Spain, France) | Short term (≤2 years) |

| Surge in off-grid micro-powered CEA solutions for desert farming in GCC countries | +1.2% | Middle East (Saudi Arabia, UAE, Qatar) | Medium term (2-4 years) |

| Corporate ESG-linked green bonds funding large-scale horticultural greenhouse LED roll-outs | +1.5% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Cloud-based spectral analytics optimising photosynthetic photon efficacy in controlled-environment facilities | +1.4% | Global, early adoption in North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Precision-Tuned LED Spectra Raising Cannabinoid Yield In North American Cannabis Grows

Cannabis growers are shifting from broad-spectrum metal-halide lamps to LED fixtures emitting 680-730 nm far-red wavelengths, boosting THC and CBD concentrations by 12-18 percent and cutting waste heat by 40-50 percent. The segment, valued at USD 1.5 billion in 2025, is growing at 15% annually as additional U.S. states legalize medical and adult-use sales. Fixture vendors Fluence and California LightWorks dominate large facilities, while modular systems from Black Dog LED are winning budget-sensitive craft operators. Federal rescheduling could accelerate multi-state expansion beyond 2028.

Urban Food-Security Programs Accelerating Vertical-Farm Lighting Demand Across Asian Megacities

Under its "30 by 30" plan, Singapore allocated SGD 200 million (USD 148 million) in 2024 to enhance its food security and reduce reliance on imports. Meanwhile, in 2025, Tokyo set aside JPY 5 billion (USD 33 million) to subsidize urban agriculture initiatives, aiming to promote sustainable farming practices within the city. Seoul's Smart Farm Innovation Center rolled out 12 hectares of fully enclosed farms, utilizing Samsung's LM301H LEDs, which boast an impressive efficacy of 3.1 µmol J⁻¹.[1]Samsung Electronics, “Samsung Newsroom,” SAMSUNG.COM These advanced farming systems, equipped with lighting fixtures priced between USD 150-250 m², achieve 10-15 harvests annually. This high productivity ensures a lighting payback period of under four years, making the investment in such technology economically viable and efficient.

EU Fit-for-55 Energy Directives Incentivising LED Retrofits In Heated Glass Greenhouses

Under the Fit-for-55 package, growers are required to reduce greenhouse gas emissions by 55% by 2030. This initiative is driving the replacement of traditional 1,000 W HPS lamps with more energy-efficient 400-600 W LED arrays. In 2025, Germany allocated grants totaling EUR 120 million (approximately USD 130 million) to support this transition. Dutch pilot programs demonstrated significant success, achieving a 40-50% reduction in lighting energy consumption while maintaining a light intensity of over 200 µmol m⁻² s⁻¹ PPFD, which is essential for cultivating crops like tomatoes and peppers.[2]International Electrotechnical Commission, “IEC Standards,” IEC.CH However, the process of obtaining CE-mark certification under IEC 62471 standards imposes additional costs, ranging from EUR 8,000 to 15,000 per model. These expenses create challenges for smaller vendors, slowing down their ability to launch new products in the market.

Surge In Off-Grid Micro-Powered CEA Solutions For Desert Farming In GCC Countries

In 2024-2025, Saudi Arabia's Vision 2030 allocated SAR 1.2 billion (USD 320 million) to controlled-environment projects, aiming to enhance agricultural sustainability and food security in the region. Solar-powered LED farms in the UAE and Qatar have successfully achieved water-use efficiency targets under 5 L kg⁻¹, representing a significant ten-fold improvement compared to traditional field crops. However, challenges persist, as dust accumulation has been reported to reduce photovoltaic output by 15-25 percent monthly. These advancements highlight the region's commitment to leveraging innovative technologies while addressing environmental constraints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute aluminium and rare-earth cost inflation squeezing high-power LED fixture margins | -1.9% | Global, with acute impact in Asia-Pacific manufacturing hubs | Short term (≤2 years) |

| Fragmented regional import tariffs complicating fixture price parity for Asia-Pacific growers | -1.3% | Asia-Pacific (India, ASEAN, Australia), spillover to Africa | Medium term (2-4 years) |

| Photobiological safety compliance costs delaying spectrum-tuning product launches in EU | -0.8% | Europe, with secondary effects in North America | Short term (≤2 years) |

| Limited DALI/KNX interoperability curbing smart-lighting adoption in legacy greenhouses | -0.7% | Global, concentrated in Europe and North America, legacy facilities | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Acute Aluminium And Rare-Earth Cost Inflation Squeezing High-Power LED Fixture Margins

In 2025, average aluminium prices climbed to USD 2,580 per tonne, marking a significant increase that led to a rise of USD 6-10 in fixture bills of materials per unit. This surge in costs resulted in a notable compression of manufacturers' gross margins, reducing them by as much as 12 percentage points.[3]U.S. Geological Survey, “Mineral Commodity Summaries 2025,” USGS.GOV Furthermore, the implementation of stringent export quotas by China significantly impacted the market for rare earth elements. These restrictions drove prices of europium and terbium oxides up by 30 percent, thereby exerting additional pressure on suppliers of LED phosphors and further complicating their operational dynamics.

Fragmented Regional Import Tariffs Complicating Fixture Price Parity For Asia-Pacific Growers

India's 25% import duty, Australia's anti-dumping levies, which range from 15% to 58%, and Pakistan's 20% regulatory duty collectively drive landed costs to increase by 35-40% above ex-factory prices. These elevated costs significantly impact the pricing structure and profitability of multinational companies operating in these regions. To navigate these challenges, multinationals are compelled to maintain country-specific inventories tailored to meet the unique regulatory requirements and market conditions of each country. This approach, while necessary, results in an approximate 8-12% inflation in their working capital. The increased working capital requirements not only add financial strain but also introduce additional complexities in managing supply chain operations effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lighting Technology: LED Dominance With A Resurgent Plasma Niche

LED systems held 86.13% of horticultural lighting market share in 2025, reflecting sustained 40-50 percent energy savings versus HID lamps. The horticultural lighting market size for plasma and other alternatives is projected to advance at a 12.41% CAGR as research facilities value their continuous 380-780 nm spectra. LED fixture costs have declined to USD 80-150 m⁻², and gallium-nitride-on-silicon roadmaps suggest further price drops by 2028.

LED innovation is shifting toward 10-channel tunable arrays, typified by Heliospectra’s MITRA X platform released in 2024, which recreates sunrise-to-sunset transitions with 1 percent spectral granularity. Plasma systems priced at USD 800-1 200 per unit are penetrating high-margin cannabis and cut-flower operations despite higher capex. HID lamps, still clinging to 8-10 percent share in older greenhouses, are falling out of favor as bulb supply tightens under EU Ecodesign rules.

By Offering: Hardware Commoditization Fuels Software Value Capture

Hardware contributed 71.52% of 2025 revenue, yet falling LED package prices are shrinking average selling prices by 6-8 percent yearly. Software and services are expanding at 12.53% CAGR as platforms such as LumiGrow smartPAR Cloud charge USD 2-5 m⁻² yr⁻¹ for photon efficacy optimization. These SaaS fees already represent 12-18 percent of total project value in new vertical farms.

Driver electronics now embed Bluetooth LE and Zigbee radios, eliminating hard-wired DALI infrastructure and reducing installation labor USD 8-12 per linear meter. Energy-savings-as-a-service models pioneered by Deere Infinite Vertical keep fixtures off growers’ balance sheets, although legal complexities around measurement and verification confine adoption to operators above USD 10 million annual revenue.

By Installation Type: Retrofit Momentum Builds On Payback Certainty

New facilities accounted for 58.36% of 2025 spending, largely purpose-built vertical farms that integrate lighting, HVAC, fertigation, and robotics from day one. Retrofits, however, will outrun at a 13.46% CAGR as growers secure 18-36 month paybacks by swapping 1 000 W HPS for 600 W LED arrays. Netherlands’ Wageningen University trials demonstrated 42 percent power savings and an 8 percent tomato yield uplift.

Older glasshouses face higher capex because 480 V distribution upgrades can add USD 15-25 m⁻², stretching paybacks beyond four years. Germany’s 40 percent capital grants shorten this window, whereas Spanish plastic-house operators still defer upgrades amid milder climates. Leasing at 8-12 percent interest over seven years inflates lifecycle costs 25-35 percent versus construction loans available to green-field projects.

By Cultivation: Berries Overtake Growth Rates Of Traditional Glasshouse Staples

Tomatoes and peppers led revenue with 23.74 percent share in 2025, yet berries will grow fastest at 15.22% CAGR as far-red LEDs extend strawberry and blueberry seasons and lift anthocyanin content 15-22 percent. Premium berry programs at Driscoll’s and Naturipe Farms retrofitted 180 ha of interlighting during 2024-2025, raising yields 18-25 percent and enhancing shelf life by 12 days.

Leafy greens fill vertical farms near high-price urban markets, accounting for 18-20 percent of spend, whereas cannabis and specialty botanicals hold 15-18 percent share. Cut flowers command 12-14 percent thanks to strict stem-length grading in Dutch auctions. Remaining crops — from cucumbers to propagation seedlings — absorb hybrid HPS-LED deployments where radiant heat is still desirable.

By Application: Vertical Farms Gain Traction Despite Capital Intensity

Greenhouses still represent 49.21 percent of horticultural lighting market size, but indoor and vertical farms will post a 15.21% CAGR through 2031 as cities chase local food security. Vertical facilities can achieve 10-15 crop cycles annually at 400-600 µmol m⁻² s⁻¹ PPFD, but capex runs USD 1 200-2 000 m⁻², with lighting making up 35-40 percent.

Research institutes, aquaponics, and container farms share 14-18 percent of spending. More than 320 container units were installed worldwide in 2025, predominantly in Middle Eastern sites where water scarcity and high heat favor modular deployment. Power costs above USD 0.12 kWh⁻¹ remain the tipping point for economic viability.

Geography Analysis

Europe dominated with 32.94 percent share in 2025 as Fit-for-55 subsidies cover 40 percent of LED retrofit capex in countries such as Germany and France. Netherlands’ 10 000 ha of heated glasshouses consumed 4.5 TWh in 2024, making energy savings of 40-50 percent through LEDs financially compelling. Spain’s Almería plastics sector is less aggressive because natural light suffices most of the year, but pilot LED-climate algorithms delivered 18-month paybacks.

Asia-Pacific will be the fastest-growing region at 13.42% CAGR. China’s 1.2 million ha of protected horticulture is scaling LEDs to offset land limits, while Singapore pumped SGD 200 million (USD 148 million) into vertical farms since 2024. Japanese urban farms receive JPY 5 billion (USD 33 million) in annual subsidies, and India’s 25 percent tariff raises costs versus ASEAN neighbors with 0-5 percent duties. Australia’s anti-dumping tariffs on Chinese drivers divert orders to Korean suppliers at 12-18 percent mark-ups.

North America accounted for roughly 30 percent share in 2025. United States cannabis lighting reached USD 1.5 billion that year, and Canada’s 2 800 ha of glasshouses are rapidly retrofitting LEDs under volatile natural-gas prices. Mexico’s 1 800 ha of tomato greenhouses fitted interlighting in 2024-2025, gaining 18-25 percent yield bumps. Saudi Arabia, UAE, and Qatar together invested USD 320 million in solar-powered LED farms to cut 85-90 percent import dependence.

Competitive Landscape

The horticultural lighting market registers moderate fragmentation: the top five players, Signify, ams OSRAM, Fluence, Samsung, and LG Innotek, held about 45-50 percent combined revenue in 2025. Samsung and LG use semiconductor scale to underprice fixtures by 15-20 percent, a move that forced Heliospectra to raise SEK 25.6 million (USD 2.8 million) in fresh equity to sustain R&D in spectral tuning.

Signify absorbed Fluence in 2022 to consolidate cannabis and vertical-farm channels. Ams OSRAM, by contrast, divested non-core fixtures to focus on upstream LED dies. Patent filings surged: Signify lodged 18 horticulture patents in 2024-2025, and Samsung targeted gallium-nitride-on-silicon processes that omit rare-earth phosphors. Plug-and-play wireless systems for old glasshouses and IP65 dust-proof enclosures for desert use are emerging white-space arenas.

Nationstar Optoelectronics and Everlight are flooding markets with sub-USD 80 m⁻² LED kits, compressing gross margins across Europe and South America. Deere Infinite Vertical is piloting savings-as-a-service contracts, retaining fixture ownership and billing growers per kilowatt-hour saved. Standards groups such as LightingEurope and the DesignLights Consortium are steering interoperability rules that will further lower entry barriers for price-aggressive challengers.

Horticulture Lighting Industry Leaders

Signify Holding

ams OSRAM AG

Fluence Bioengineering (Scotts Miracle-Gro)

Heliospectra AB

Hortilux Schréder

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Signify announced a EUR 85 million (USD 92 million) expansion at its Piła, Poland plant to add 40 percent capacity for GreenPower modules, with commissioning in Q3 2026.

- October 2025: Samsung partnered with Bowery Farming, investing USD 15 million to deploy LM301H LEDs across 12 ha of Texas and Georgia vertical farms.

- September 2025: California LightWorks closed USD 22 million Series C to build a 28 000 ft² plant in Sacramento dedicated to SolarSystem fixtures.

- August 2025: Gavita International integrated its plasma and LED products with Priva Connext climate controls, targeting 12-18 percent energy cuts.

Global Horticulture Lighting Market Report Scope

Horticulture lighting increase, support, and enable the growth of plants by illuminating them with artificial light. The horticulture lighting supplements natural daylight and raises growth light levels to enhance photosynthesis, thereby improving plants' growth and quality. This also replaces daylight with artificial light for ultimate climate control.

The Horticultural Lighting Market Report is Segmented by Lighting Technology (LED, HID, Fluorescent, Plasma, and More), Offering (Hardware, Software and Services), Installation Type (New, and Retrofit), Cultivation (Vegetables and Fruits, Leafy Greens, Berries, Tomatoes and Peppers, Flowers, Cannabis, and More), Application (Greenhouses, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

| LED |

| HID |

| Fluorescent |

| Plasma and Others |

| Hardware (Fixtures, Drivers, Controls) |

| Software and Services |

| New Installations |

| Retrofit Installations |

| Vegetables and Fruits |

| Leafy Greens and Micro-Greens |

| Berries |

| Tomatoes and Peppers |

| Flowers and Ornamentals |

| Cannabis and Specialty Crops |

| Other Crops |

| Greenhouses |

| Indoor and Vertical Farms |

| Research/Academic Facilities |

| Aquaponics and Container Farms |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Lighting Technology | LED | ||

| HID | |||

| Fluorescent | |||

| Plasma and Others | |||

| By Offering | Hardware (Fixtures, Drivers, Controls) | ||

| Software and Services | |||

| By Installation Type | New Installations | ||

| Retrofit Installations | |||

| By Cultivation | Vegetables and Fruits | ||

| Leafy Greens and Micro-Greens | |||

| Berries | |||

| Tomatoes and Peppers | |||

| Flowers and Ornamentals | |||

| Cannabis and Specialty Crops | |||

| Other Crops | |||

| By Application | Greenhouses | ||

| Indoor and Vertical Farms | |||

| Research/Academic Facilities | |||

| Aquaponics and Container Farms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will global horticultural lighting revenue be by 2031?

The sector is forecast to reach USD 19.62 billion by 2031 under a 12.23% CAGR.

Which crop segment is expanding fastest under LEDs?

Berries lead with a 15.22% CAGR as far-red spectra extend harvest windows and enhance anthocyanin content.

What drives retrofits in European glasshouses?

EU Fit-for-55 rules and 40 percent subsidy rates slash payback periods to 18-36 months.

How do vertical-farm power costs impact viability?

Facilities need electricity below USD 0.12 kWh⁻¹ because lighting can account for 35-40 percent of capex.

Page last updated on: