High Pressure Protective Packaging Film Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

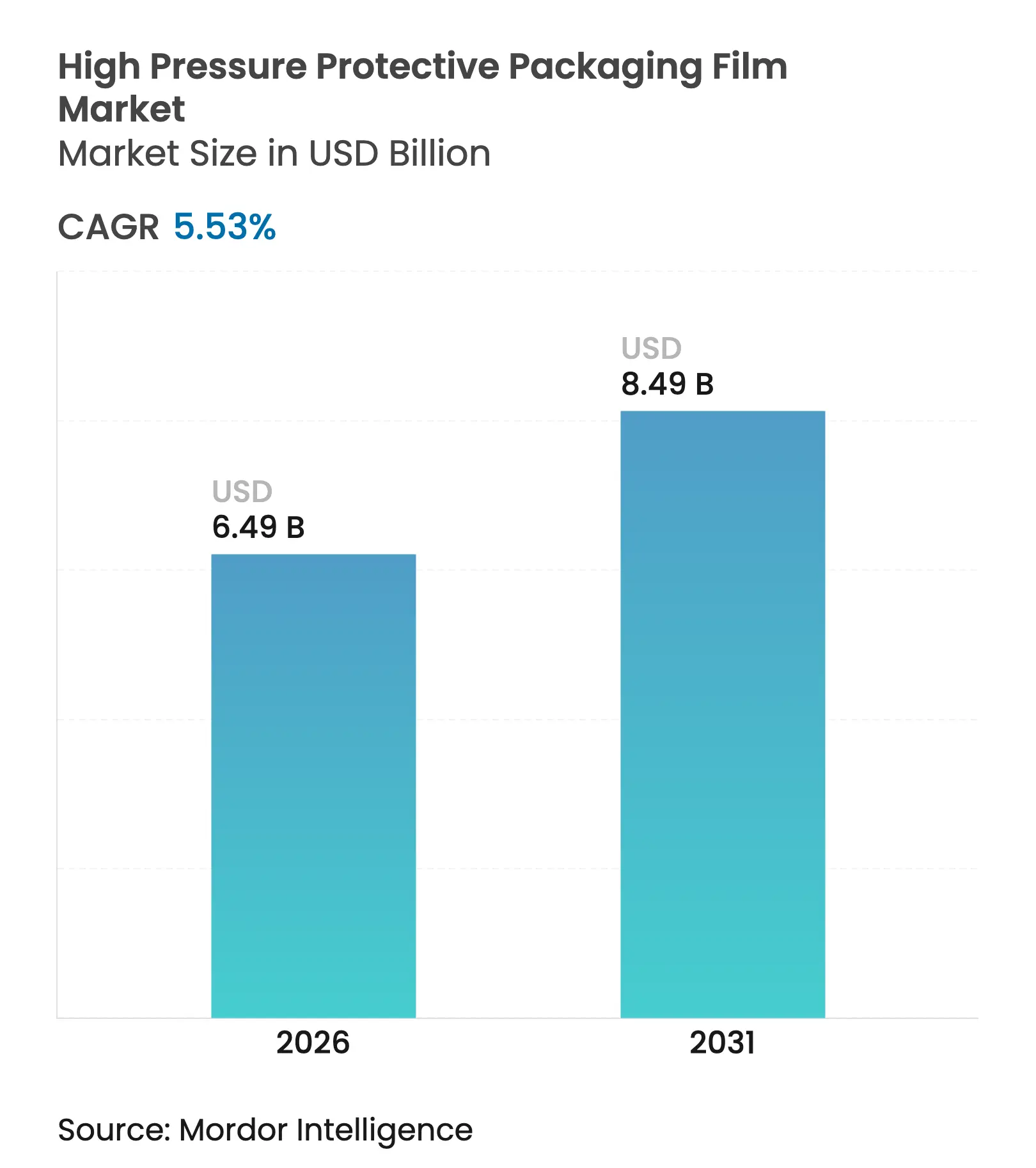

| Market Size (2026) | USD 6.49 Billion |

| Market Size (2031) | USD 8.49 Billion |

| Growth Rate (2026 - 2031) | 5.53 % CAGR |

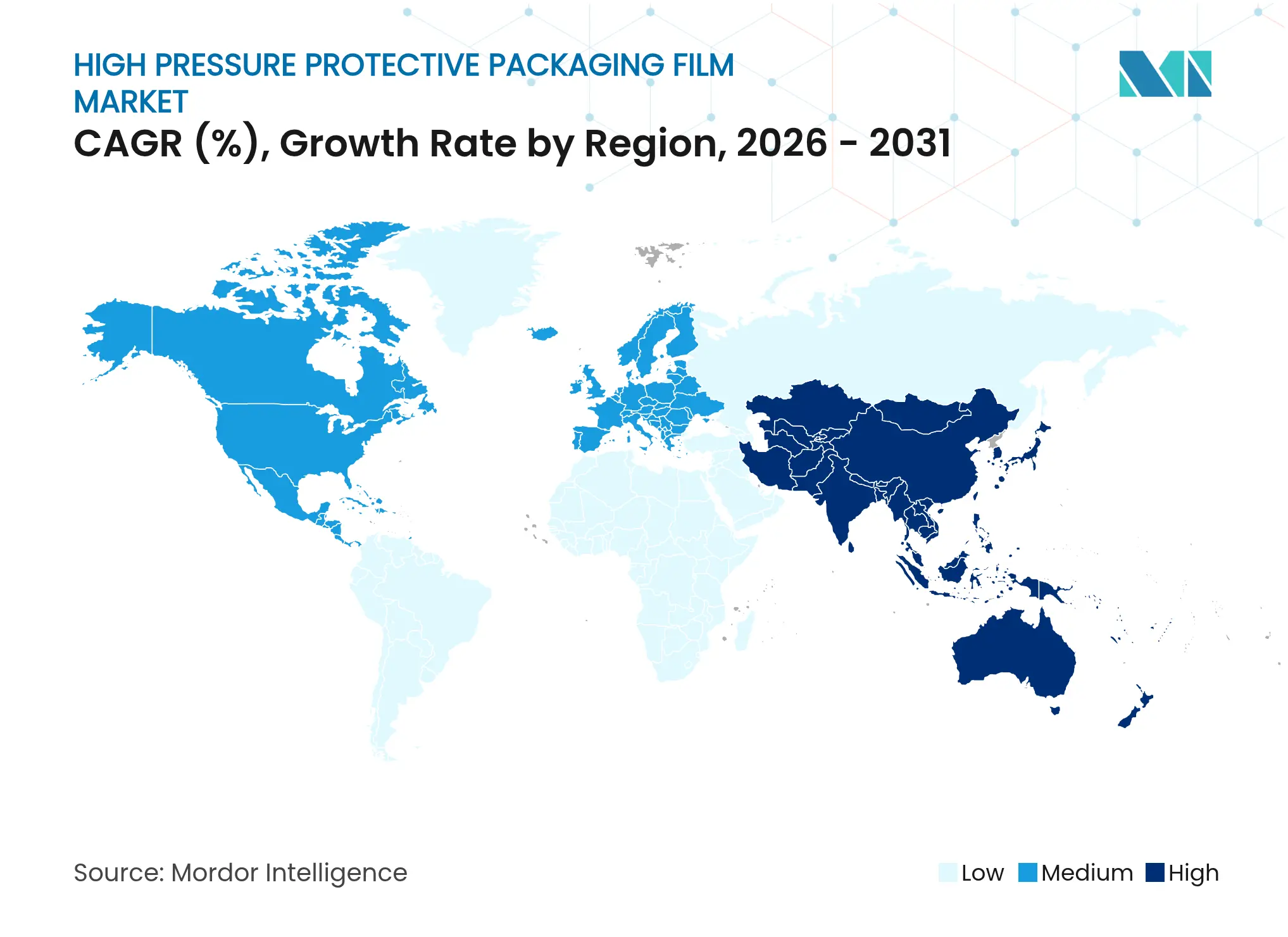

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

High Pressure Protective Packaging Film Market Analysis by Mordor Intelligence

The high-pressure protective packaging film market size was valued at USD 6.15 billion in 2025 and estimated to grow from USD 6.49 billion in 2026 to reach USD 8.49 billion by 2031, at a CAGR of 5.53% during the forecast period (2026-2031). Demand is reinforced by the rapid adoption of e-commerce in the Asia-Pacific region, increasing electronics export volumes, and pharmaceutical cold-chain compliance, which favors shock-absorbing, tamper-evident films.[1]China Internet Network Information Center, “Statistical Report on China’s Internet Development,” cnnic.net.cnBubble wrap retained the largest share in 2024, yet reusable inflatable dunnage bags and on-demand inflation systems are penetrating automotive and fulfillment centers, respectively, thereby trimming in-warehouse storage costs and freight surcharges. The material mix is tilting toward biodegradable and recycled-content polymers in response to European rules that set recyclability grades and a 30% recycled-content floor by 2030, while polyethylene continues to benefit from low feedstock prices in the United States. Pharmaceutical distributors, motivated by the United States Drug Supply Chain Security Act serialization deadline, are switching to serialized air cushions with QR codes and holographic seals that authenticate pack integrity. Mergers such as the Amcor-Berry tie-up and the pending Sealed Air buy-out point to a moderate but tightening industry concentration that emphasizes scale efficiencies and vertical integration into inflation equipment.

Key Report Takeaways

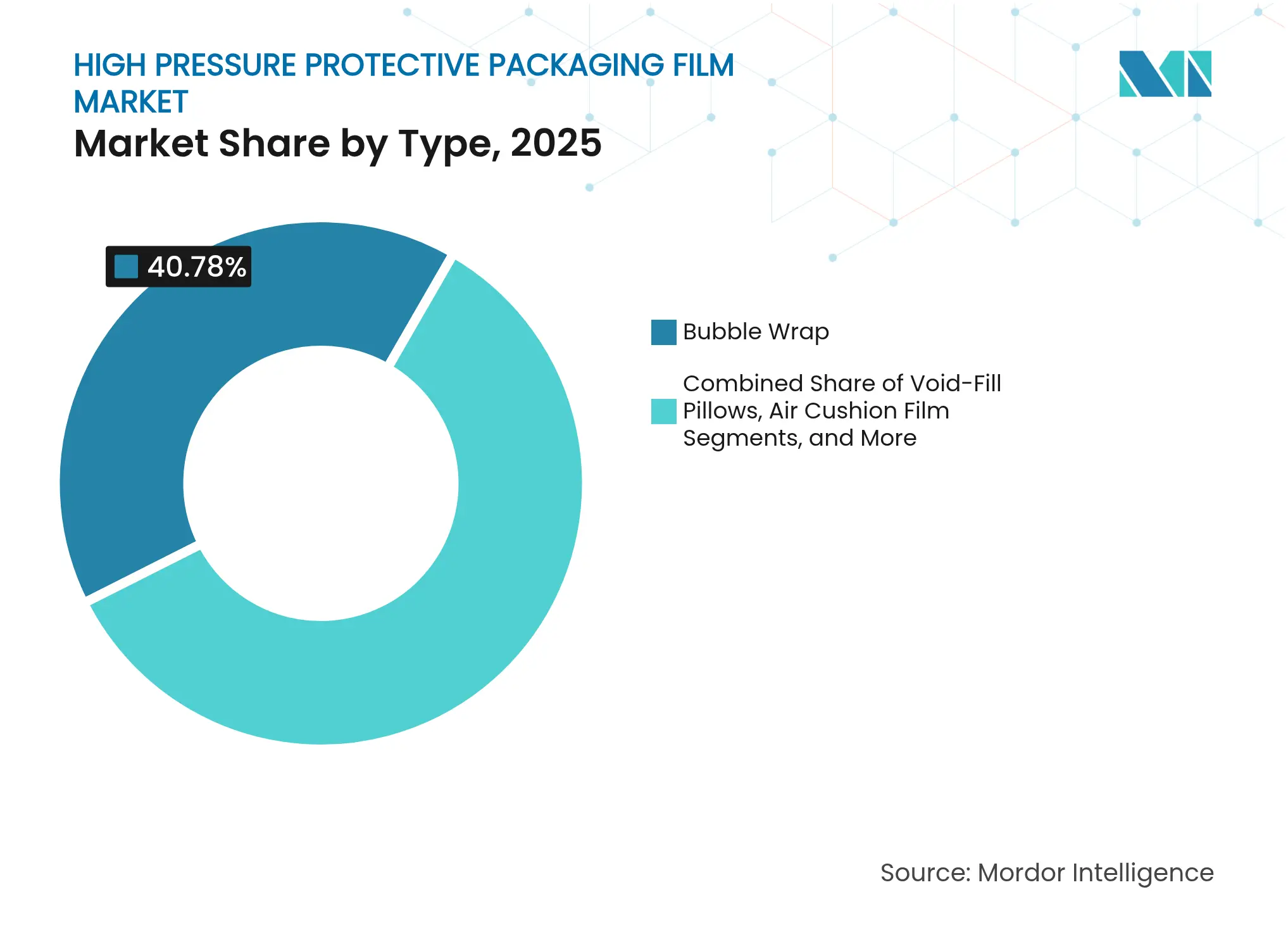

- By type, bubble wrap led with a 40.78% share of the high-pressure protective packaging film market in 2025, whereas inflatable dunnage bags are forecast to record a 6.08% CAGR through 2031.

- By material, polyethylene held a 55.74% share in 2025, while biodegradable polymers are projected to advance at a 6.95% CAGR through 2031.

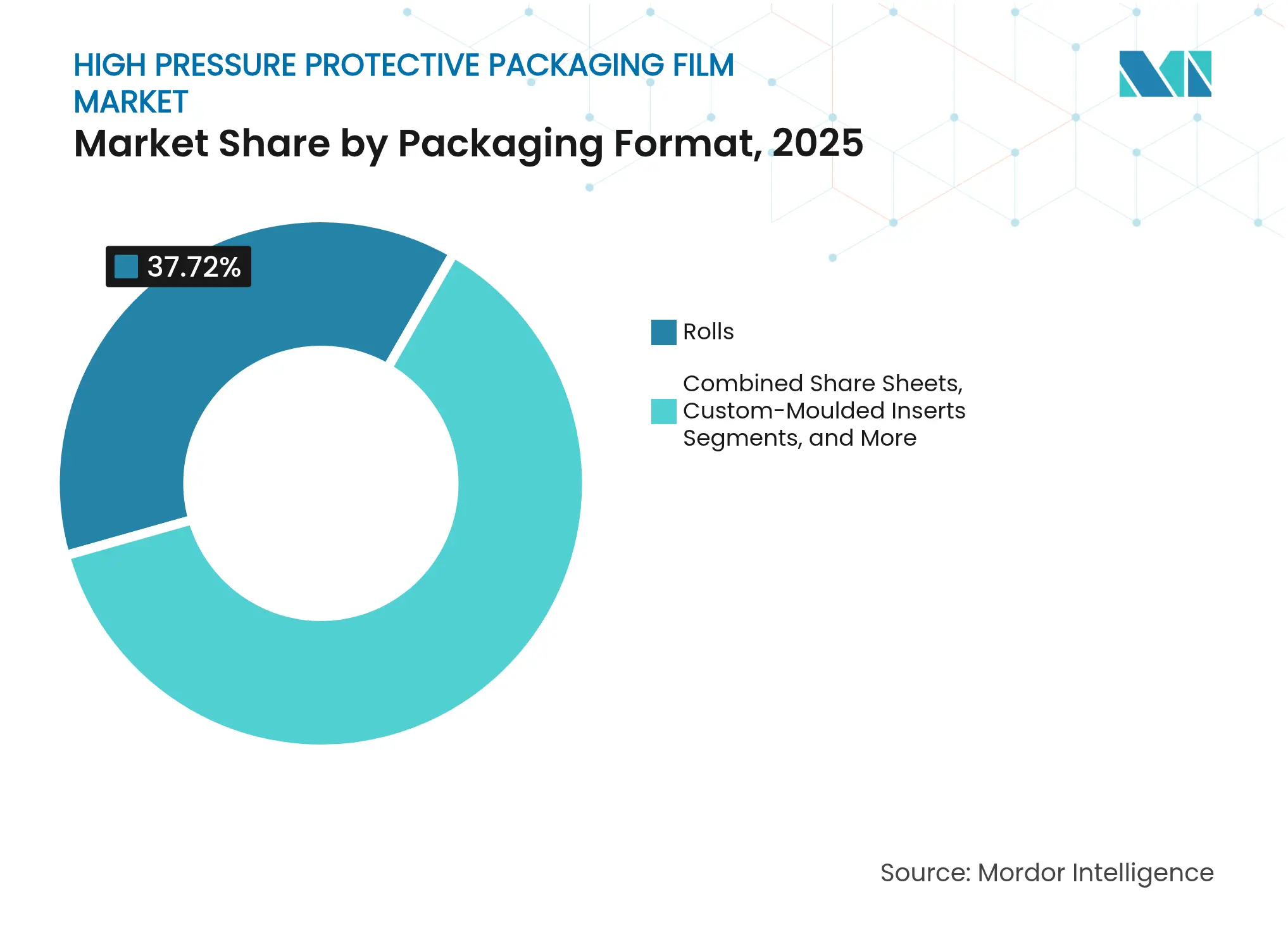

- By packaging format, rolls accounted for 37.72% of the high-pressure protective packaging film market size in 2025, but custom-molded inserts are expected to expand at a 6.18% CAGR over the same horizon.

- By end user, electronics captured a 34.10% share in 2025, whereas pharmaceutical applications are expected to post a 7.45% CAGR from 2025 to 2031.

- By geography, North America dominated with a 39.10% share in 2025; however, the Asia-Pacific region is poised to grow at a 7.60% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High Pressure Protective Packaging Film Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expansion of E-Commerce and Last-Mile Logistics

Expansion of E-Commerce and Last-Mile Logistics

| +1.8% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

Global, strongest in Asia-Pacific and North America

|

Impact Timeline

:

Medium term (2-4 years)

|

Growth in Electronics Exports Requiring Shock-Resistant

Packaging

Growth in Electronics Exports Requiring Shock-Resistant

Packaging

| +1.2% | Asia-Pacific core, spillover to North America | Medium term (2-4 years) | |||

Stringent Product-Safety Regulations in Pharmaceutical

Cold Chains

Stringent Product-Safety Regulations in Pharmaceutical

Cold Chains

| +0.9% | North America and EU | Short term (≤ 2 years) | |||

Rising Sustainability Mandates Driving Shift to

Lightweight Recyclable Films

Rising Sustainability Mandates Driving Shift to

Lightweight Recyclable Films

| +1.1% | EU and UK, expanding globally | Long term (≥ 4 years) | |||

Integration of On-Demand Inflation Systems in Automated

Fulfilment Centers

Integration of On-Demand Inflation Systems in Automated

Fulfilment Centers

| +0.7% | North America and Western Europe | Medium term (2-4 years) | |||

Adoption of AI-Designed Multi-Layer Structures for

Pressure-Optimized Cushioning

Adoption of AI-Designed Multi-Layer Structures for

Pressure-Optimized Cushioning

| +0.5% | Global | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Expansion of E-Commerce and Last-Mile Logistics

Global online sales climbed to USD 6.3 trillion in 2024 and are tracking toward USD 8.1 trillion by 2028, making parcel density and damage prevention critical for retailers that face last-mile costs representing 41% of total logistics spend.[2]United Nations Conference on Trade and Development, “Global E-Commerce Sales,” unctad.orgSame-day delivery commitments in China, India, and the United States increase the number of handling steps, thereby increasing the risk of breakage for electronics, ceramics, and glassware. On-demand systems, such as Pregis AirSpeed HC Versa, inflate up to 45 feet of film each minute, allowing warehouses to tailor cushioning volume to real-time order mixes and cut inventory space requirements by up to 40%.[3]Pregis LLC, “AirSpeed HC Versa Product Sheet,” pregis.comThe ability to right-size packages aligns with European Union rules that cap space at 50%, reducing dimensional-weight surcharges. As parcel networks scale, e-commerce players are gravitating towards films that balance low basis weight with high burst pressure, supporting growth in the high-pressure protective film packaging market.

Growth in Electronics Exports Requiring Shock-Resistant Packaging

India produced USD 115 billion in electronics during fiscal 2024 and targets USD 300 billion by 2026 under its Production Linked Incentive program. Apple plans to move 14% of iPhone assembly to India by December 2024, which is expected to increase demand for multi-layer cushions that meet ASTM D6653 shock benchmarks. Vietnam’s electronics exports increased 15% year-over-year in 2024; however, local converters cannot fully meet the protective film needs, resulting in imports from Thailand and China that inflate lead times and freight bills. Semiconductor wafers, foldable OLED screens, and ultra-thin glass panels are 40% more fragile than legacy components, prompting suppliers like Corning to deploy custom air-cushioned carriers that cut damage claims from 2.3% to 0.7%. Robust Asian export pipelines, therefore, underpin a steady rise in the high-pressure protective packaging film market.

Stringent Product-Safety Regulations in Pharmaceutical Cold Chains

The U.S. Drug Supply Chain Security Act required serialized, tamper-evident packaging by November 2024, prompting distributors to adopt air cushions embedded with QR codes and holographic seals. Amcor’s AmPrima Plus film reveals color changes after breach, while Huhtamaki’s irreversible time-temperature labels warn of excursions beyond 2-8 °C storage windows. United States Pharmacopeia Chapter 1079 requires validation across an ambient temperature range of –20 °C to 40 °C, favoring reflective metallized cushions that reduce radiant heat transfer by 35%.[4]United States Pharmacopeia, “USP Chapter 1079,” usp.org Sealed Air’s TempGuard solution maintains payloads within ±2 °C for 96 hours without active refrigeration, solving ultra-cold mRNA vaccine distribution hurdles. Compliance imperatives anchor sustained film demand in North America and Europe, with early adoption in Japan.

Rising Sustainability Mandates Driving Shift to Lightweight Recyclable Films

European Union Regulation 2025/40 stipulates recyclability grades and a 30% recycled-content minimum by 2030, while banning perfluoroalkyl substances in food-contact packaging from August 2026. The United Kingdom imposes a GBP 200 per metric ton plastic tax (USD 254) and Spain levies EUR 0.45 per kilogram (USD 0.51) on non-reusable plastics, narrowing virgin-resin margins. Dow’s ECOLIBRIUM resins enable five recycling loops without performance loss, and BASF’s Ecovio PS 1606 biodegradable film meets EN 13432 standards, but commands a 15-25% price premium. Mondi’s PerFORMing Cushion replaces polyethylene bubble wrap with curbside-recyclable honeycomb paper, retaining 85% of its cushioning capability. These developments accelerate a shift toward circular materials across the high-pressure protective packaging film industry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile Petrochemical Feedstock Prices

Volatile Petrochemical Feedstock Prices

| -0.9% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

Global, acute in Asia-Pacific and Europe

|

Impact Timeline

:

Short term (≤ 2 years)

|

Availability of Paper-Based and Foam Alternatives

Availability of Paper-Based and Foam Alternatives

| -0.6% | North America and EU | Medium term (2-4 years) | |||

Capital Intensity of High-Pressure Inflation Equipment for

SMEs

Capital Intensity of High-Pressure Inflation Equipment for

SMEs

| -0.4% | Global | Medium term (2-4 years) | |||

Emerging Plastic-Tax Policies Targeting Air-Filled Films

Emerging Plastic-Tax Policies Targeting Air-Filled Films

| -0.5% | EU and UK | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Petrochemical Feedstock Prices

Low-density polyethylene prices oscillated between USD 1,200 and USD 1,650 per metric ton in 2024, mirroring the swings in Brent crude from USD 70 to USD 95 per barrel and squeezing film converter margins by up to five percentage points. Polypropylene averaged USD 1,100-1,250 per metric ton, but a Middle East outage in September 2024 triggered a 12% spot spike within three weeks. European producers, reliant on higher-priced liquefied natural gas, face a 20-25% feedstock disadvantage compared to their United States peers, whose natural gas traded at USD 2.50-3.50 per million Btu in 2024. Small and mid-sized converters without long-term supply contracts often face working-capital strain during price surges, which can delay equipment upgrades and jeopardize capacity additions.

Availability of Paper-Based and Foam Alternatives

Ranpak’s paper void-fill systems generated USD 1.1 billion in sales in 2024 by appealing to retailers that have committed to phasing out single-use plastics. Automated Packaging Systems’ FillPak TT Tornado produces 60 feet of crumpled paper per minute, matching mid-range air cushion throughput without incurring plastic tax liability. Pregis EverTec paper cushioning and molded pulp inserts, adopted by Apple and Samsung, reduce reliance on polyethylene foam by about 18%. Paper solutions cost 15-25% more per cubic foot than polyethylene but bypass European plastic levies and align with corporate ESG metrics, gradually capping upside for the high-pressure protective packaging film market.

Segment Analysis

By Type: Dunnage Bags Gain Ground in Automotive and Industrial Shipments

Bubble wrap commanded a 40.78% share of the high-pressure protective packaging film market in 2025, driven by its low unit cost and broad adoption in e-commerce. Void-fill pillows followed with around 22.18%, prized for their ability to conform to irregular geometries and minimize empty space penalties under European Union packaging rules. Inflatable dunnage bags, with a projected 6.08% CAGR of roughly 18.94%, are expected to post the fastest growth, buoyed by the shift in electric vehicle battery logistics from rigid foam to reusable air-filled systems, which reduce packaging weight by 30%. Sheets and corner protectors comprised the remaining 18.10%, serving as protection for glassware and ceramics where breakage sensitivity is high.

As Amazon and DHL automate their fulfillment centers, operators prefer roll-fed films that are compatible with multiple machines to avoid vendor lock-in, indirectly channeling volume toward bubble wrap and pillow formats. Nevertheless, automotive tier-ones are drafting returnable packaging standards that prioritize dunnage reusability over one-way cushioning, promising a stable order flow for multi-chamber air bags. Paper-laminated dunnage, such as Storopack PAPERbubble, meets both Automotive Industry Action Group guidelines and growing sustainability targets, putting competitive pressure on commodity polyethylene films. This dual emphasis on cost efficiency and recyclability anchors long-term value creation in the high-pressure protective packaging film market segment.

Note: Segment shares of all individual segments available upon report purchase

By Material: Biodegradable Polymers Accelerate Amid Recycled-Content Mandates

Polyethylene maintained a 55.74% foothold in 2025, underpinned by abundant United States shale gas feedstock and converter familiarity; however, its high-pressure protective packaging film market size edge will narrow as policy mandates escalate. Polypropylene held close to 24.18%, finding favor in industrial applications that require heat resistance and higher tensile strength during ocean transit. Biodegradable polymers, currently accounting for less than 10%, are forecast to rise at a 6.95% CAGR, driven by European recyclability targets and corporate zero-waste pledges. Polyvinyl chloride (PVC) slipped to about 7.76% amid health-based phase-out pressures, leaving ethylene vinyl acetate (EVA) and TPU blends to fill specialty niches, such as electrostatic discharge protection.

Dow’s ECOLIBRIUM resin platform permits five mechanical recycling loops without yield loss, boosting the circular appeal of polyethylene. BASF’s Ecovio PS 1606, certified to EN 13432, secures trial volumes in Western Europe but faces challenges with infrastructure gaps in North America and the Asia-Pacific region, where industrial composting capacity is limited. Converter margins are therefore pulled between stable, low-cost PE and premium, policy-compliant biopolymers. Feedstock volatility, coupled with plastic taxes on virgin content, will ultimately accelerate material substitution; however, polyethylene is expected to remain the anchor of the high-pressure protective packaging film market through 2031.

By Packaging Format: Custom-Molded Inserts Expand in Precision Machinery Logistics

Rolls occupied 37.72% share in 2025, their high-pressure protective packaging film market size advantage stemming from compatibility with on-demand inflation equipment that slashes warehouse space. Bags and pouches followed with roughly 28.10%, gaining traction among pharmaceutical distributors that must serialize every package under the United States Drug Supply Chain Security Act. Sheets accounted for about 20.66%, favored by glassware shippers that require flat-pack options for automated wrapping lines. Custom-molded inserts stood at ~13.52% but will climb at a 6.18% CAGR through 2031 as aerospace and precision machinery exporters seek contour-specific cushioning that meets ASTM and United Nations transport standards.

Pregis committed USD 50 million to boost North American molding capacity, signaling longer-term confidence in inserts for electric vehicle battery modules. Rolls are evolving with machine-readable perforations, allowing robotic pick-and-pack lines to dispense exact strip lengths and reduce material waste by 10-12%. Bags with tamper-evident seals now embed QR codes for end-to-end traceability, aligning with pharmaceutical anti-counterfeiting rules. Sheets will retain relevance where dimensional-weight surcharges demand flat, lightweight substrates, but the greatest value upside resides in custom formats engineered for high-value payloads.

Note: Segment shares of all individual segments available upon report purchase

By End User: Pharmaceutical Segment Surges on Cold-Chain Compliance

Electronics contributed 34.10% of the revenue in 2025, yet pharmaceuticals are expected to outpace others with a 7.45% CAGR, increasing their share of the high-pressure protective packaging film market size by 2031. E-commerce and retail accounted for approximately 26.18%, reflecting the growth of direct-to-consumer fulfillment, which prioritizes lightweight cushioning to reduce volumetric freight charges. The automotive sector controlled nearly 13.86%, bolstered by reusable dunnage for EV battery logistics that adheres to Automotive Industry Action Group protocols. Glass and ceramics, industrial components, and food and beverages collectively accounted for 18.12%, while furniture and appliances filled the remaining 7.74%.

Ultra-cold mRNA vaccines require payloads to be kept within a temperature range of ±2 °C for up to four days, prompting the development of Sealed Air’s TempGuard and similar hybrid solutions that combine air cushions with phase-change materials. Electronics distributors require cushions that pass ASTM D4169 drop tests, prompting converters to adopt AI-driven finite-element design, which reduces film gauge by 15% without compromising burst strength. Automotive tier-ones value reusable air bags because they return modules to assembly plants, slashing packaging spend over multiple cycles. Collectively, stricter validation protocols and rising cold-chain volumes position pharmaceuticals as the fastest-growing end-user slice of the high-pressure protective packaging film market.

Geography Analysis

North America held 39.10% of the 2025 revenue, buoyed by mature e-commerce logistics and pharmaceutical serialization mandates; however, the Asia-Pacific region is forecast to register a 7.60% CAGR from 2025 to 2031. China’s flexible packaging segment reached USD 52.3 billion in 2024, supported by a 52.1% online shopping penetration that intensifies parcel throughput and demand for cushioning. India’s packaging spending reached USD 73 billion, expanding at a rate of 26-28% annually, as Apple and TSMC scale up local manufacturing. Vietnam experienced a 15% increase in exports in 2024; however, it still relies on imported protective films, presenting near-term opportunities for greenfield investments.

Europe accounted for approximately 27.84%, constrained by plastic taxes of EUR 0.80 per kilogram (USD 0.90) on non-recycled content and recyclability mandates that increase compliance costs. South America’s 6.05% share is concentrated in Brazil, where packaging spending stood at BRL 92 billion (USD 18.4 billion) in 2024.

The Middle East and Africa combined account for roughly 7.02%, driven by the United Arab Emirates' logistics infrastructure and Saudi Arabia's pharmaceutical imports; however, sub-Saharan uptake is tempered by tariffs and cold-chain gaps. As electronics manufacturing migrates from China to India and Vietnam, the region’s share of the high-pressure protective packaging film market is set to expand more than any other geography.

Competitive Landscape

Market Concentration

Market concentration is moderate, with the top five companies controlling 45% of revenue in 2024. Clayton Dublier and Rice’s USD 10.3 billion bid for Sealed Air, expected to close in mid-2025, and Amcor’s USD 8.43 billion acquisition of Berry, completed in June 2025, intensify the consolidation momentum. Sealed Air’s protective segment booked USD 450 million in Q4 2024 sales, 7% below 2023, as volumes slipped 5.4% and EBITDA margin narrowed to 14.8% from 18.7%, highlighting pricing fragility in North America. Amcor-Berry now commands more than USD 24 billion in flexible packaging revenue and a global footprint that strengthens bargaining power with resin suppliers.

Strategic thrusts revolve around integrating inflation equipment and digital services. Pregis and Automated Packaging Systems generate 30-40% higher margins by bundling proprietary machines with consumable films, locking customers into captive cartridge ecosystems. Dow and BASF invest in AI-aided design that simulates ASTM drop tests, enabling converters to trim gauge without compromising performance, thereby lowering resin intensity. Ranpak wins share through paper-based void fill, helping retailers sidestep plastic taxes, with 12% revenue growth to USD 1.1 billion in 2024.

White-space openings exist in pharmaceutical ultra-cold chains, where specialized cushions capable of maintaining –70 °C are still a niche product. Regional converters with ISO-certified cleanrooms can tap this gap, provided they secure a medical-grade resin supply. As consolidation accelerates, mid-tier players may pursue partnerships with equipment OEMs or biotech packagers to avoid margin compression and defend their slice of the high-pressure protective packaging film market.

High Pressure Protective Packaging Film Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amcor closed its USD 8.43 billion acquisition of Berry Global, creating a flexible packaging entity with more than USD 24 billion in sales.

- April 2025: Storopack added two biodegradable air-cushion extrusion lines in Wrocław, Poland, boosting annual capacity by 12,000 metric tons.

- January 2024: Sealed Air introduced TempGuard temperature-controlled pharmaceutical packaging, which maintains payloads within ±2 °C for 96 hours without requiring active refrigeration.

- November 2024: Industry forums 4evergreen and the Sustainable Packaging Summit, along with this year's ALL4PACK fair, have honored Mondi and Amazon with three prestigious packaging awards. These accolades underscore the duo's enduring collaboration in crafting innovative paper-based packaging, emphasizing ease of packing, user-friendly opening, and recyclability.

Table of Contents for High Pressure Protective Packaging Film Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Expansion of E-Commerce and Last-Mile Logistics

- 4.2.2Growth in Electronics Exports Requiring Shock-Resistant Packaging

- 4.2.3Stringent Product-Safety Regulations in Pharmaceutical Cold Chains

- 4.2.4Rising Sustainability Mandates Driving Shift to Lightweight Recyclable Films

- 4.2.5Integration of On-Demand Inflation Systems in Automated Fulfilment Centers

- 4.2.6Adoption of Ai-Designed Multi-Layer Structures for Pressure-Optimized Cushioning

- 4.3Market Restraints

- 4.3.1Volatile Petrochemical Feedstock Prices

- 4.3.2Availability of Paper-Based and Foam Alternatives

- 4.3.3Capital Intensity of High-Pressure Inflation Equipment for SMEs

- 4.3.4Emerging Plastic-Tax Policies Targeting Air-Filled Films

- 4.4Industry Value Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Impact of Macroeconomic Factors on the Market

- 4.8Porter's Five Forces Analysis

- 4.8.1Threat of New Entrants

- 4.8.2Bargaining Power of Buyers

- 4.8.3Bargaining Power of Suppliers

- 4.8.4Threat of Substitutes

- 4.8.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Type

- 5.1.1Bubble Wrap

- 5.1.2Void-Fill Pillows

- 5.1.3Air Cushion Film

- 5.1.4Inflatable Dunnage Bags

- 5.1.5Other Types

- 5.2By Material

- 5.2.1Polyethylene

- 5.2.2Polypropylene

- 5.2.3Polyvinyl Chloride

- 5.2.4Biodegradable Polymers

- 5.2.5Other Materials

- 5.3By Packaging Format

- 5.3.1Rolls

- 5.3.2Bags / Pouches

- 5.3.3Sheets

- 5.3.4Custom-Moulded Inserts

- 5.3.5Other Packaging Formats

- 5.4By End User

- 5.4.1Electronics

- 5.4.2E-Commerce and Retail

- 5.4.3Automotive

- 5.4.4Glassand Ceramics

- 5.4.5Pharmaceutical

- 5.4.6Industrial Components

- 5.4.7Foodand Beverages

- 5.4.8Other End Users

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2South America

- 5.5.2.1Brazil

- 5.5.2.2Argentina

- 5.5.2.3Chile

- 5.5.2.4Rest of South America

- 5.5.3Europe

- 5.5.3.1United Kingdom

- 5.5.3.2Germany

- 5.5.3.3France

- 5.5.3.4Italy

- 5.5.3.5Spain

- 5.5.3.6Rest of Europe

- 5.5.4Asia-Pacific

- 5.5.4.1China

- 5.5.4.2Japan

- 5.5.4.3India

- 5.5.4.4South Korea

- 5.5.4.5Australia and New Zealand

- 5.5.4.6Rest of Asia-Pacific

- 5.5.5Middle East and Africa

- 5.5.5.1Middle East

- 5.5.5.1.1United Arab Emirates

- 5.5.5.1.2Saudi Arabia

- 5.5.5.1.3Turkey

- 5.5.5.1.4Rest of Middle East

- 5.5.5.2Africa

- 5.5.5.2.1South Africa

- 5.5.5.2.2Kenya

- 5.5.5.2.3Nigeria

- 5.5.5.2.4Rest of Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Productsand Services, Recent Developments)

- 6.4.1Sealed Air Corporation

- 6.4.2Amcor plc

- 6.4.3Pregis LLC

- 6.4.4Mondi plc

- 6.4.5Huhtamaki Oyj

- 6.4.6Coveris Holdings S.A.

- 6.4.7Winpak Ltd.

- 6.4.8Sonoco Products Company

- 6.4.9Smurfit WestRock

- 6.4.10Storopack Hans Reichenecker GmbH

- 6.4.11Intertape Polymer Group Inc.

- 6.4.12Uflex Limited

- 6.4.13Rajapack SAS

- 6.4.14Dow Packaging and Specialty Plastics (Dow Inc.)

- 6.4.15Supreme Industries Limited

- 6.4.16Fruth Custom Plastics Inc.

- 6.4.17iVEX Protective Packaging Inc.

- 6.4.18Abco Kovex Ltd.

- 6.4.19Tarheel Paper and Supply Company

- 6.4.20CDF Corporation

- 6.4.21Automated Packaging Systems Inc.

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-Space and Unmet-Need Assessment

Global High Pressure Protective Packaging Film Market Report Scope

High-pressure protective packaging films are specially designed for packaging a product that requires high-pressure cushioning and protection. It includes bubble packaging and Void-fill pillows.

The High Pressure Protective Packaging Film Report is Segmented by Type (Bubble Wrap, Void-Fill Pillows, Air Cushion Film, Inflatable Dunnage Bags, Other Types), Material (Polyethylene, Polypropylene, Polyvinyl Chloride, Biodegradable Polymers, Other Materials), Packaging Format (Rolls, Bags or Pouches, Sheets, Custom-Moulded Inserts, Other Packaging Formats), End User (Electronics, E-Commerce and Retail, Automotive, Glass and Ceramics, Pharmaceutical, Industrial Components, Food and Beverages, Other End Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).