High-density Polyethylene (HDPE) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

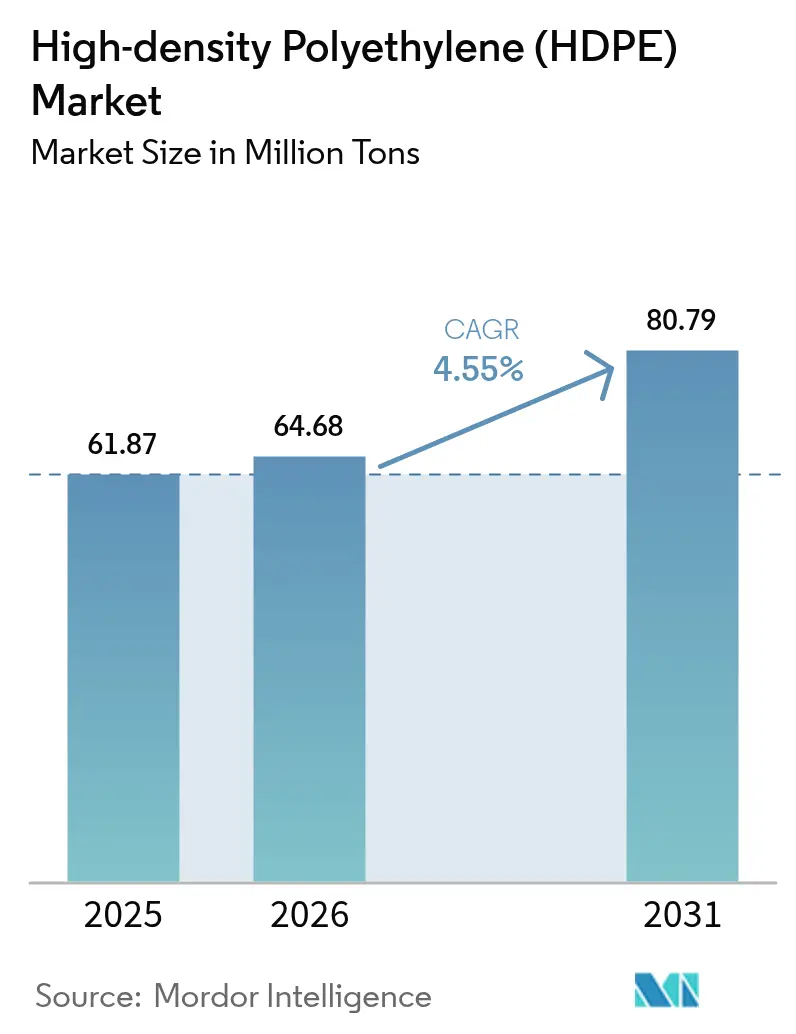

| Market Volume (2026) | 64.68 Million tons |

| Market Volume (2031) | 80.79 Million tons |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

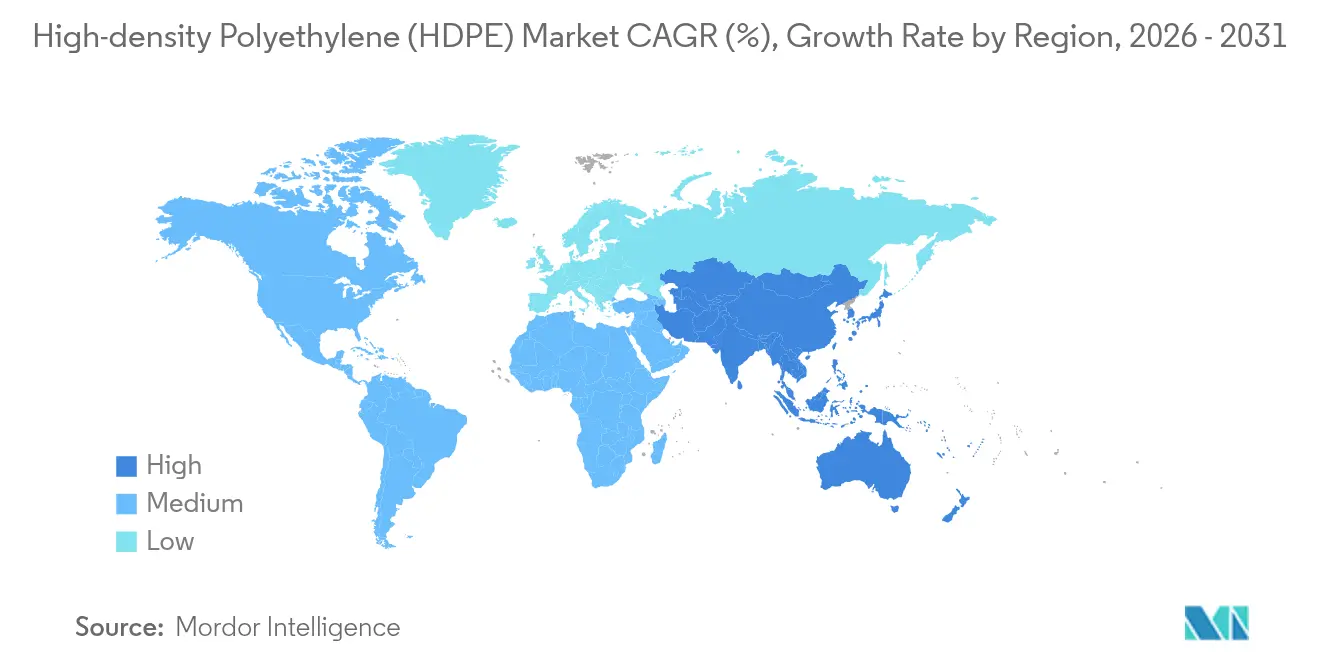

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

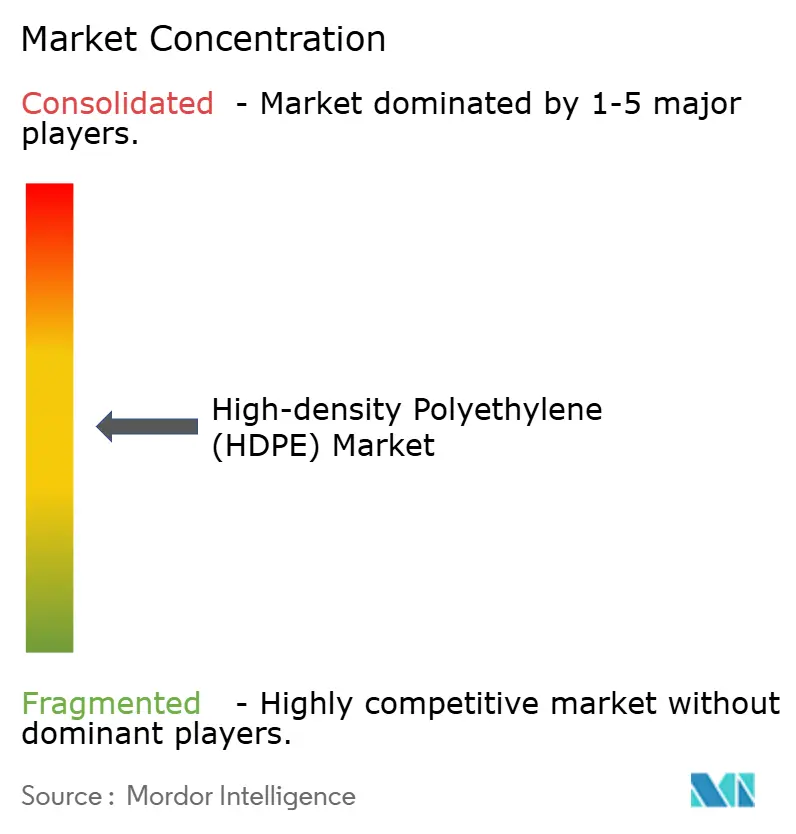

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-density Polyethylene (HDPE) Market Analysis by Mordor Intelligence

The High-density Polyethylene (HDPE) market size is expected to grow from 61.87 Million tons in 2025 to 64.68 Million tons in 2026 and is forecast to reach 80.79 Million tons by 2031 at 4.55% CAGR over 2026-2031. Strong infrastructure spending, widening chemical-recycling supply chains, and rising adoption of hydrogen-ready pipe systems anchor this trajectory, while the material’s intrinsic durability, chemical resistance, and recyclability keep end-users committed to high-density polyethylene solutions. Accelerated public-housing programs across India and ASEAN, expanding food-grade blow-molding in e-commerce distribution, and the rollout of PE-100-RC pipe networks for low-carbon gas grids collectively widen the HDPE market’s addressable demand. Chemical recyclers diverting mixed-waste streams into virgin-grade rHDPE strengthen supply security, temper feedstock volatility, and reinforce circular-economy mandates. Moderately fragmented competition persists, yet vertically integrated producers that pair cracker capacity with advanced recycling retain cost and sustainability advantages.

Key Report Takeaways

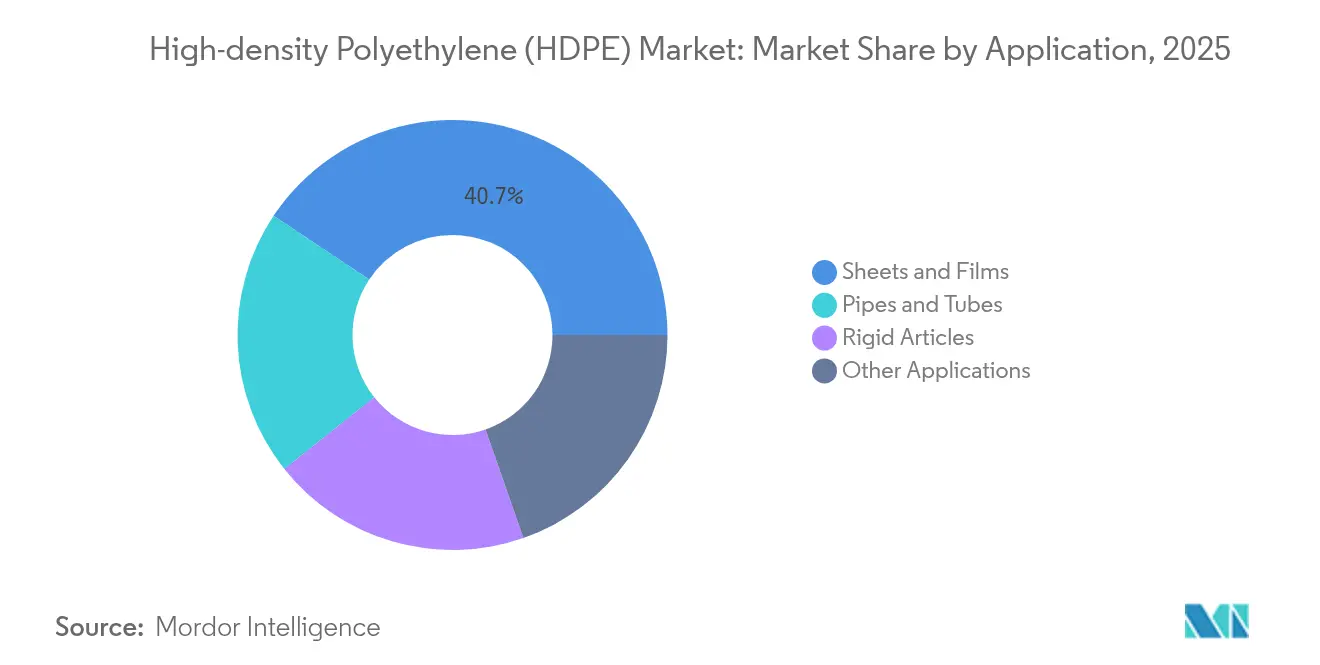

- By application, Sheets and Films captured 40.65% of the HDPE market share in 2025, while Pipes and Tubes registered the fastest 6.07% CAGR through 2031.

- By resin grade, PE-80 commanded 67.20% of the HDPE market size in 2025; Ultra-High-Molecular-Weight HDPE is progressing at a 9.10% CAGR through 2031.

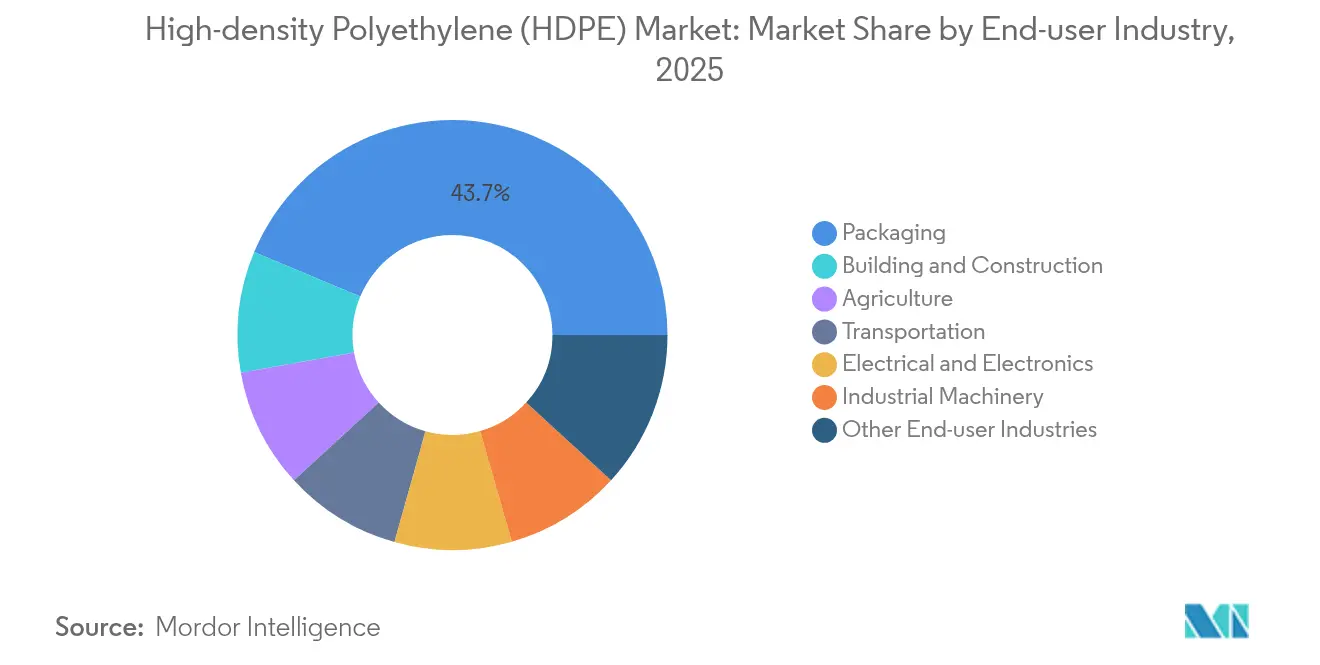

- By end-user industry, Packaging accounted for 43.70% of the HDPE market size in 2025; Building and Construction is expanding at a 5.41% CAGR through 2031.

- Asia-Pacific led with 42.30% HDPE market share in 2025 and is rising at a 5.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High-density Polyethylene (HDPE) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for pressure and non-pressure plastic pipes in water-infrastructure retrofit programmes | +1.2% | ASEAN and India core, spill-over to MEA | Medium term (2-4 years) |

| Expansion of food-grade blow-molded packaging in emerging e-commerce channels | +0.9% | Global, with a concentration in Asia-Pacific | Short term (≤ 2 years) |

| Sustained public-housing and mega-infrastructure spend across ASEAN and India | +1.0% | ASEAN and India, secondary impact in South Asia | Long term (≥ 4 years) |

| Roll-out of hydrogen-ready gas grids requiring PE-100-RC pipes | +0.7% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Chemical-recycling plants shifting mixed-waste streams into virgin-grade rHDPE | +0.6% | North America and Europe, pilot projects in Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Pressure and Non-Pressure Plastic Pipes in Water-Infrastructure Retrofit Programmes

Water-network modernisation projects prioritise HDPE pipes because they combine a 100-year service life with trenchless installation capability that cuts civil works costs by 30-40%. The American Society of Civil Engineers underscores HDPE’s corrosion resistance for ageing distribution lines[1]American Society of Civil Engineers, “HDPE and Aging Water Management Infrastructures,” asce.org. India’s 2024 quality-standard mandate for virgin polyethylene reinforces material integrity in critical water applications. Project designers favour HDPE because its flexibility accommodates ground movement, reducing leakage risk. Public-sector funding cycles spanning multiple five-year plans guarantee steady pipe volumes, ensuring predictable growth for the HDPE market. Integration of trenchless methods further differentiates HDPE from concrete and ductile-iron alternatives by lowering total installed costs.

Expansion of Food-Grade Blow-Molded Packaging in Emerging E-Commerce Channels

Rapid e-commerce penetration demands packaging that survives complex logistics while protecting food quality. Food-grade HDPE containers pass stringent migration tests and hold FDA clearance, making them default choices for dairy, condiments, and shelf-stable beverages. European Union regulations, effective March 2025, require extensive traceability for food-contact plastics, a standard that HDPE producers already meet[2]Foresight, “EU Introduces Stricter Regulations on Plastic Food Contact Materials,” useforesight.io . Weight-reduction via thin-wall blow-molding lowers resin usage, aligns with corporate emission targets, and sustains demand, reinforcing the HDPE market’s resilience.

Sustained Public-Housing and Mega-Infrastructure Spend Across ASEAN and India

Government-backed infrastructure pipelines in ASEAN and India secure multi-year offtake for HDPE geomembranes, cable conduits, and drainage systems. HDPE’s seismic-resistance credentials make it indispensable for metro rail, coastal defence, and landfill capping projects in geologically active zones. Public-private partnership models guarantee funding continuity, insulating HDPE suppliers from cyclical residential construction dips. Technical specifications that favour leak-proof joints, chemical inertness, and long life reinforce HDPE market penetration in construction utilities.

Roll-out of Hydrogen-Ready Gas Grids Requiring PE-100-RC Pipes

Hydrogen transmission introduces permeation and stress-crack challenges that PE-100-RC pipes are engineered to meet, enabling premium pricing within the HDPE market. GASCADE’s 400 km pipeline conversion demonstrates commercial feasibility ahead of Europe’s 2030 hydrogen-production target. Limited qualified suppliers and stringent certification hurdles create a defensible niche where leading HDPE producers capture higher margins. Future roll-outs across Asia-Pacific magnify volume potential and fortify long-term growth prospects for the HDPE market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating anti-single-use-plastic regulations and taxation | -0.8% | Europe and North America, expanding globally | Short term (≤ 2 years) |

| Volatile crude-oil-linked ethylene feedstock pricing | -0.6% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Accelerated materials switch to PP random copolymers in consumer rigid packaging | -0.4% | Global, concentrated in food and beverage packaging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Anti-Single-Use-Plastic Regulations and Taxation

Tighter packaging rules compress demand for disposable HDPE articles in Europe and parts of North America. However, HDPE’s recyclability mitigates policy risk in multi-use applications, and well-established collection streams preserve its appeal versus multi-layer films that lack mechanical-recycling pathways. Converters are redesigning closures and dispensing systems to remain within weight thresholds, limiting volume loss. Consequently, regulation restrains but does not reverse HDPE market growth.

Volatile Crude-Oil-Linked Ethylene Feedstock Pricing

Ethylene costs typically account for 60-70% of HDPE cash-cost curves, exposing producers to feedstock swings. Tariffs of 10-15% on polyethylene and feedstock imports imposed in 2025 compound cost inflation for U.S. converters. Integrated producers with captive crackers sustain higher utilisation, whereas merchant producers curtail operations, moderating HDPE market supply growth in tight-margin quarters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Films Drive Volume, Pipes Accelerate Growth

Sheets and Films held 40.65% of the 2025 HDPE market share, underpinned by steady packaging demand and downstream converter familiarity with blown-film processes. Sustainable packaging targets stimulate mono-material film designs that favour HDPE over mixed polymers.

Pipes and Tubes, although a smaller slice of the HDPE market size, posted the sharpest 6.07% CAGR for 2026-2031 on the back of water-infrastructure retrofits, hydrogen-ready gas grids, and trenchless renewals. Rising leak-loss penalties push utilities toward HDPE piping thanks to its homogenous fusion joints and 100-year service life. Industrial films, geomembranes, and carrier bags round out the portfolio, sustaining baseline resin offtake when construction spending softens.

By Resin Grade: PE-80 Dominates, UHMWPE Accelerates

PE-80 retained 67.20% share in 2025, balancing cost with 8-10 MPa hydrostatic pressure resistance ideal for municipal water and gas lines. PE-100 grades continue to replace legacy PE-80, where higher pressure ratings or thinner wall designs enhance system capacity. Ultra-High-Molecular-Weight HDPE posted a rapid 9.10% CAGR outlook, driven by orthopedic implants, battery separators, and ballistic inserts that demand extreme abrasion and impact resistance. Celanese’s GUR powders widen processing latitude, enabling compression-molded implant components that satisfy PFAS-free requirements.

PE-100-RC specifications aim to future-proof low-carbon gas grids; the grade’s enhanced stress-crack resistance and slow-crack-growth performance underpins hydrogen pipeline safety tests, leading to price premia versus commodity grades. As facility turnarounds integrate peroxide-ester catalysts and advanced bimodal reactors, the output of high-pressure grades rises, deepening their influence over the HDPE market.

By End-User Industry: Packaging Leads, Construction Accelerates

Packaging captured 43.70% of the HDPE market size in 2025, anchored by food-contact compliance, drop-impact resistance, and broad converter infrastructure. Lightweight, mono-material formats extend shelf life and lower freight emissions, prolonging HDPE’s packaging edge. Building and Construction volumes grow at 5.41% CAGR through 2031 as governments channel CAPEX into public housing, mega-rail, and coastal defences. HDPE geomembranes prevent seepage in landfill cappings, while conduit pipe and cable sheathing protect underground utilities.

Agriculture leverages HDPE drip-irrigation laterals that curb water usage by 40-60%, propelling steady resin demand in water-scarce regions. Transportation sector uses in fuel tanks and roof racks benefit from density reduction and corrosion resistance.

Geography Analysis

Asia-Pacific controlled 42.30% of the 2025 HDPE market share and is forecast to record a 5.55% CAGR to 2031, propelled by Chinese downstream film exports and India’s infrastructure boom. Integrated producers in the region benefit from coal-to-olefins and naphtha-cracker flexibility, buffering ethylene volatility. However, oversupply periods have compressed regional margins, prompting scheduled maintenance to balance inventories.

North America’s HDPE market benefits from ethane-advantaged feedstock and a wave of chemical-recycling investments that elevate circular-resin availability. While growth rates are lower than Asia-Pacific, value-added pipe, film, and medical-grade demand sustains profit pools.

Europe remains policy-driven; its hydrogen-network build-out channels HDPE into PE-100-RC pipe projects and chemical-recycling alliances that secure recycled feedstock. Anti-single-use-plastic mandates depress thin-wall rigid packaging volumes, yet high recyclability keeps HDPE firmly in multi-use, returnable crates and chemical drums.

Regulatory Landscape

HDPE demand and formulation choices increasingly track packaging and waste rules, recycled-content programs, and controls on resin loss across the supply chain. In the European Union, the Packaging and Packaging Waste Regulation (EU) 2025/40 entered into force on 11 February 2025 and applies generally from 12 August 2026, tightening recyclability requirements and documentation for plastic packaging (including HDPE formats used in food and household products). Complementing this, Regulation (EU) 2025/2365 targets plastic pellet losses and requires certification-based compliance for large enterprises handling over 1,500 tonnes of pellets per year by 17 December 2027, raising operational diligence expectations for HDPE producers, compounders, and logistics providers.

Outside Europe, regulators are also shaping HDPE supply options through plastics-waste governance and chemical-recycling oversight. India issued Plastic Waste Management (Amendment) Rules, 2026 (amending the 2016 rules under the Environment (Protection) Act, 1986), reinforcing compliance pressure on packaging value chains and accelerating design-for-recycling and traceability practices. In the United States, the EPA withdrew proposed TSCA Significant New Use Rules (SNURs) aimed at chemical recycling in July 2025, while an April 2026 EPA notice sought comment on reclassifying certain pyrolysis units from incineration standards to manufacturing standards under the Clean Air Act. That change can alter permitting pathways and compliance costs for facilities supplying circular feedstocks into HDPE applications.

Value Chain Analysis

The HDPE value chain starts with hydrocarbon feedstocks (ethane, naphtha) feeding ethylene production, followed by polymerization (including bimodal and specialty catalysts for PE-80, PE-100, PE-100-RC, and UHMWPE). After pellet handling and logistics, downstream conversion such as pipe extrusion, blow molding, film, and geomembranes supports distribution to packaging, infrastructure, agriculture, and industrial end users. Vertical integration remains a key cost lever because ethylene typically drives cash costs, while food-contact and pipe certifications, along with packaging traceability, increasingly shape which resin grades and suppliers are qualified at the converter level.

Recent supply-side events show how capacity additions and logistics shocks propagate through the chain. In July 2026, Tasnee completed a USD 500 million ethylene expansion at the Saudi Ethylene and Polyethylene Company (SEPC) in Al Jubail Industrial City, lifting ethylene output by 18% and improving upstream feedstock availability for polyethylene production in the region. By contrast, 2026 disruptions linked to Middle East conflict and shipping constraints, including chokepoints such as the Strait of Hormuz and Red Sea rerouting, increased lead times and freight costs for ethylene- and polymer-linked trade flows. Buyers responded by diversifying sourcing and holding more inventory. Downstream and regional moves also stand out, including L&T securing BPCLs EPCC contract in December 2025 for a dual-train LLDPE/HDPE unit in Bina (575,000 tpy each train), supporting local resin availability for high-growth pipe and packaging conversion hubs.

Competitive Landscape

The HDPE market is moderately fragmented yet tilting towards consolidation. Strategic differentiation increasingly revolves around circular-economy capabilities. LyondellBasell, SABIC, and Dow combine cracker capacity and proprietary catalyst systems to capture volume and margin leadership. Emerging players explore specialty niches. Competitive intensity, therefore, hinges on integrated cost positions, access to recycled feedstock, and agility in meeting end-use certification demands, all factors shaping the HDPE market’s medium-term structure.

High-density Polyethylene (HDPE) Industry Leaders

Dow

Exxon Mobil Corporation

INEOS

SABIC

LyondellBasell Industries Holdings B.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulation-driven packaging redesign and infrastructure-led pipe demand are creating specific whitespace for differentiated HDPE grades and circular feedstocks. The EU Packaging and Packaging Waste Regulation (EU) 2025/40 applies from 12 August 2026, pushing brand owners and converters toward recyclability-aligned structures and higher traceability. This favors HDPE formats that can be engineered into mono-material packaging streams and supported with certified pellet-handling and documentation. In Asia, new recycled-plastics standards also raise quality expectations, with Chinas SAC/TC 15 implementing nine national standards for recycled plastics on 1 February 2026. That move expands the addressable need for consistent rHDPE quality and converter-friendly specifications.

On the supply and investment side, multiple named capacity and integration projects create near-term avenues for producers and technology licensors serving faster-growing applications such as pipes, food-grade blow-molding, and premium pipe grades including PE-100-RC. Indian Oil Corporation Ltd selecting LyondellBasell Hostalen ACP technology for a 500,000 tpy HDPE unit at Paradip supports new regional production aligned with Indias infrastructure and packaging pull. BPCLs Bina project, executed as two 575,000 tpy LLDPE/HDPE trains under L&Ts December 2025 EPCC award, adds another locally anchored supply node for northern and central India. In China, Borouges April 2026 50:50 joint venture agreement with Wanrong New Materials to build an ethylene plant and polyethylene complex in Fujian points to continued investment in new PE capacity, and highlights the importance of product differentiation and circularity credentials as incremental volumes come online.

Recent Industry Developments

- April 2026: Infra Pipe Solutions acquired Atkore Inc.s HDPE business, adding five manufacturing sites across Texas, Oregon, South Carolina, New Mexico, and Missouri. The transaction deepens Infra Pipes downstream footprint in HDPE pipes and structures, tightening its control over supply, lead times, and customer service for infrastructure-related demand.

- August 2025: Aster Group completed the acquisition of Chevron Phillips Singapore Chemicals Pte Ltd, including a 400 kilotonnes per annum HDPE plant on Jurong Island, Singapore. The deal changes ownership of a strategic Asia hub asset and can influence regional supply allocation and customer relationships in packaging and industrial HDPE grades.

- May 2024: ISCO acquired Infinity Plastics, adding a facility in Mayville, Wisconsin, and lifting its total manufacturing footprint to 36 facilities across the United States and Canada. This expansion strengthens ISCOs fabrication and distribution capacity for HDPE piping and related products, supporting faster delivery and broader coverage in municipal and industrial projects.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the demand for high density polyethylene (HDPE) resin used across common converting routes. Volumes are tracked from polymer production through downstream consumption in end uses such as packaging and pipes, then consolidated at a global level.

Scope exclusions: Finished goods value added after conversion, such as the price of bottles, crates, or installed piping systems, is not counted beyond the resin volume consumed.

Segmentation Overview

- By Application

- Pipes and Tubes

- Sheets and Films

- Rigid Articles

- Other Applications

- By Resin Grade

- PE-80

- PE-100

- PE-100-RC

- Ultra-High-Molecular-Weight HDPE

- By End-User Industry

- Packaging

- Building and Construction

- Agriculture

- Transportation

- Electrical and Electronics

- Industrial Machinery

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and to anchor the model with signals that move HDPE demand. We relied on public and official sources such as UN Comtrade for polymer trade flows, the US International Trade Commission database for shipment codes and direction, and the US Energy Information Administration for feedstock and energy cues that influence operating rates and pricing.

We also reviewed materials and polymer references, including ASTM standards library documentation for common grade usage, plus publications from industry and chemistry journals and releases from relevant trade associations that discuss plastics use and recycling policies. To connect these signals to companies and assets, we used company annual reports, investor presentations, and reputable press coverage, and then applied selective paid subscriptions for company financials and intelligence, patent mapping, and shipment-level trade checks when needed. This list is not exhaustive, and we used additional sources throughout the research process to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work focused on interviews and survey inputs from resin producers, compounders, converters, distributors, and large end users that buy HDPE for packaging and pipe applications. These inputs were used to confirm how volume shifts across key applications, how pricing is typically quoted (contract vs spot), and which operating rate and trade assumptions are realistic across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 17% | APAC: 40% |

| Mid tier: 48% | Functional/Unit leaders: 40% | EMEA: 36% |

| Smaller Players: 17% | Managers: 43% | Americas: 24% |

Market-Sizing & Forecasting

The core sizing logic is built top-down. We use production, trade, and end-use demand indicators to reconstruct how much HDPE resin is consumed by region, then we consolidate to a global total. After the structure is in place, we cross-check totals with selective bottom-up approximations such as sampled supplier roll-ups, channel checks on converted product output, and volume times indicative price ranges, then adjust where the results show clear outliers.

Practical inputs in this market include cracker and polymer operating rates, net import and export balances for HDPE resins, application-level pull from packaging and pipe demand, substitution with other polyethylene grades, and typical price spreads linked to feedstock movements. For forecasting, we run scenario analysis so demand growth is stressed under different infrastructure spending, packaging demand, and trade flow conditions, then compare those outputs with what primary respondents report in order books and contracting behavior. Where a bottom-up view is thin for smaller countries or informal channels, we use proxy ratios from comparable markets, and then we validate those ratios against trade and production signals.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, followed by targeted variance checks at the region and application level so unusual movements are explained before sign-off. If a key assumption moves sharply, such as a sustained operating rate shift, a major trade restriction, or a large capacity start-up, follow-up calls are used to re-test the volume and pricing logic.

Each deliverable goes through a multi-step analyst review where model math, units, and conversion factors are rechecked, and narrative conclusions are compared against the quantified results. The report is refreshed annually, and material events can trigger interim updates, followed by a final pre-delivery pass so clients get the most current view at the time of access.

Mordor Intelligence's High Density Polyethylene Hdpe Market Size Versus Other Published Estimates

Published HDPE market numbers often differ because the unit of measure is not consistent, and because some estimates mix resin volumes with downstream finished product value. Variations also come from how trade is treated, which in-scope grades are included, and whether the year is updated after major capacity or operating rate changes.

The table highlights a split between volume-based sizing and value-based sizing, which can make totals appear far apart even when the underlying demand direction is similar. Some sources also rely on a single pricing curve or a fixed regional mix, while other approaches reflect that packaging and pipe demand grow at different speeds and pull different grade needs across regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 64.68 M (2026) | |

| Global Consultancy A | USD 107.80 B (2026) | This figure is presented in value terms, which depends heavily on assumed average selling prices and whether transfer pricing and services are included, so it is not directly comparable to a resin volume build. |

| Trade Publisher B | USD 108.69 B (2026) | This estimate reflects factory gate revenue style accounting with a different base year and price progression, which can lift the total when resin price cycles are strong even if underlying volumes are similar. |

The table indicates that the widest gap is mainly a unit and valuation question, and it can then widen due to the price and base-year assumptions used in each approach. In the Mordor Intelligence model, the core sizing is done in resin volume terms (million tons) and is kept aligned to application pull and net trade balance checks, which helps prevent price swings from being mistaken as demand growth.

Key Questions Answered in the Report

What is the current size of the High-density Polyethylene (HDPE) market and its growth outlook?

The High-density Polyethylene (HDPE) market size reached 64.68 million tons in 2026 and is projected to reach 80.79 million tons by 2031, reflecting a 4.55% CAGR.

Which application segment drives the largest HDPE demand?

Sheets and Films dominate, accounting for 40.65% of 2025 volumes due to sustained packaging requirements.

Why is the Pipes and Tubes segment growing fastest?

Infrastructure retrofits, hydrogen-ready gas grids and trenchless installation advantages push Pipes and Tubes to a 6.07% CAGR through 2031.

Which region leads the HDPE market?

Asia-Pacific holds 42.30% of 2025 volumes and is advancing at a 5.55% CAGR thanks to manufacturing scale and infrastructure spending.

How do anti-single-use-plastic regulations affect HDPE demand?

They curb growth in disposable packaging but simultaneously favour HDPE in regulated markets where recyclability and collection infrastructure are proven.

Page last updated on: