High Altitude Pseudo Satellites Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

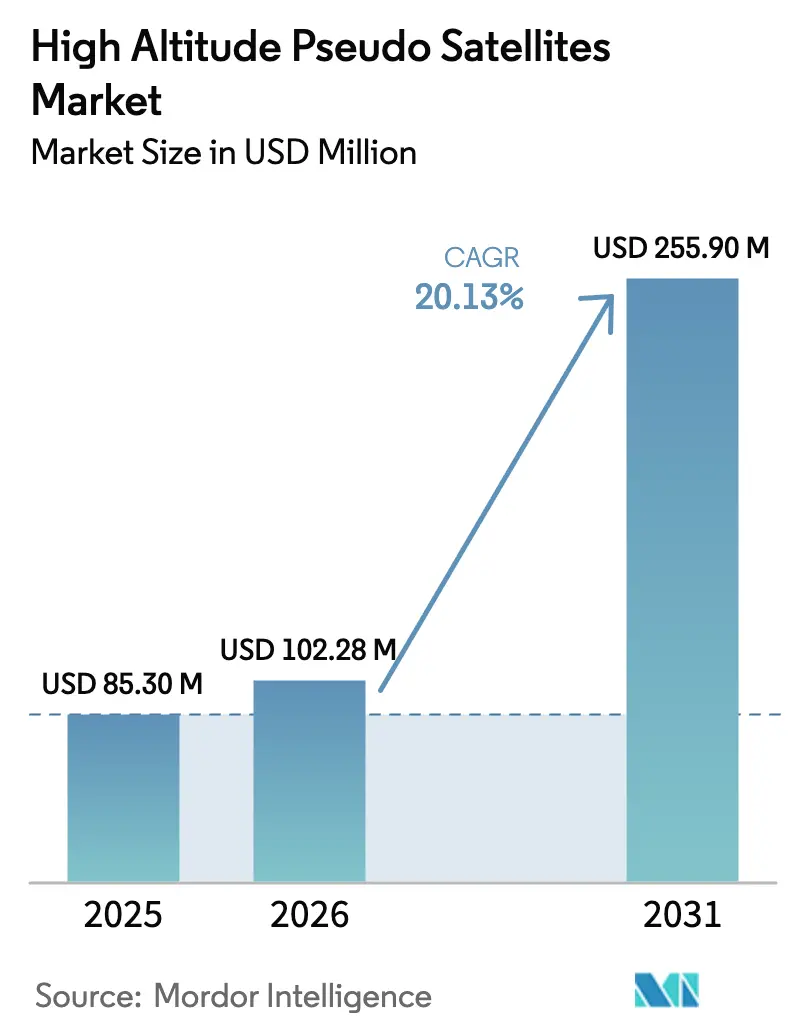

| Market Size (2026) | USD 102.28 Million |

| Market Size (2031) | USD 255.90 Million |

| Growth Rate (2026 - 2031) | 20.13% CAGR |

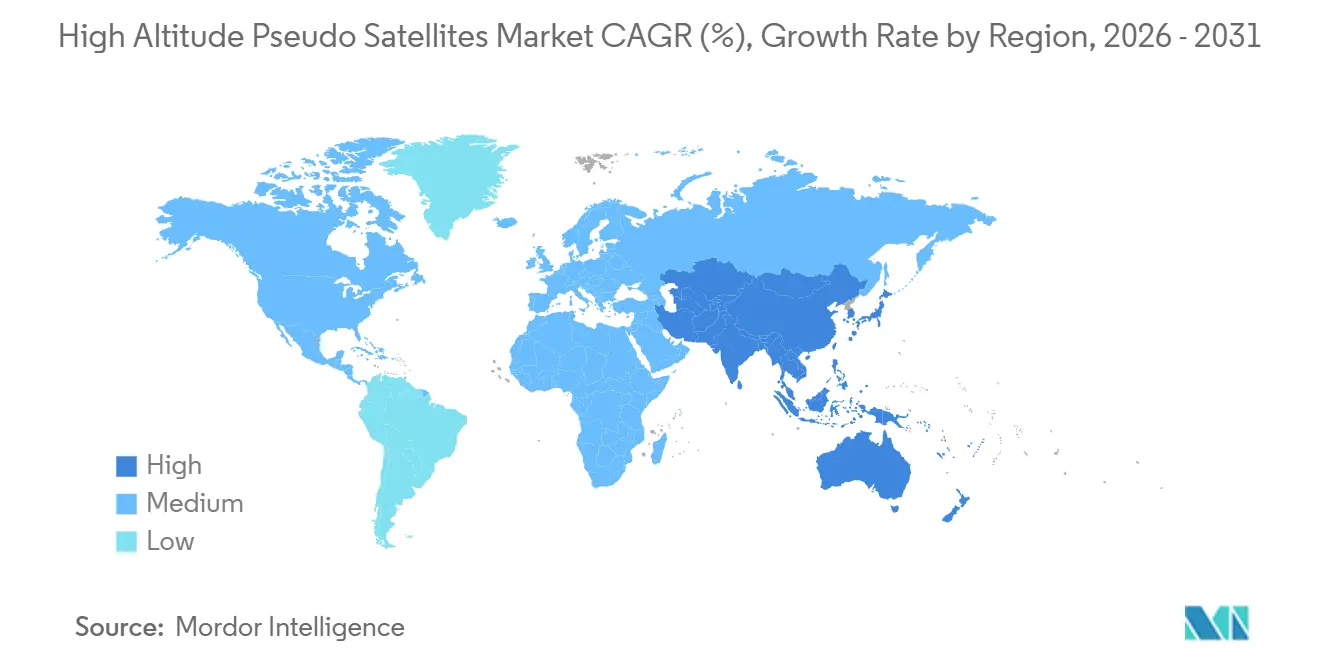

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

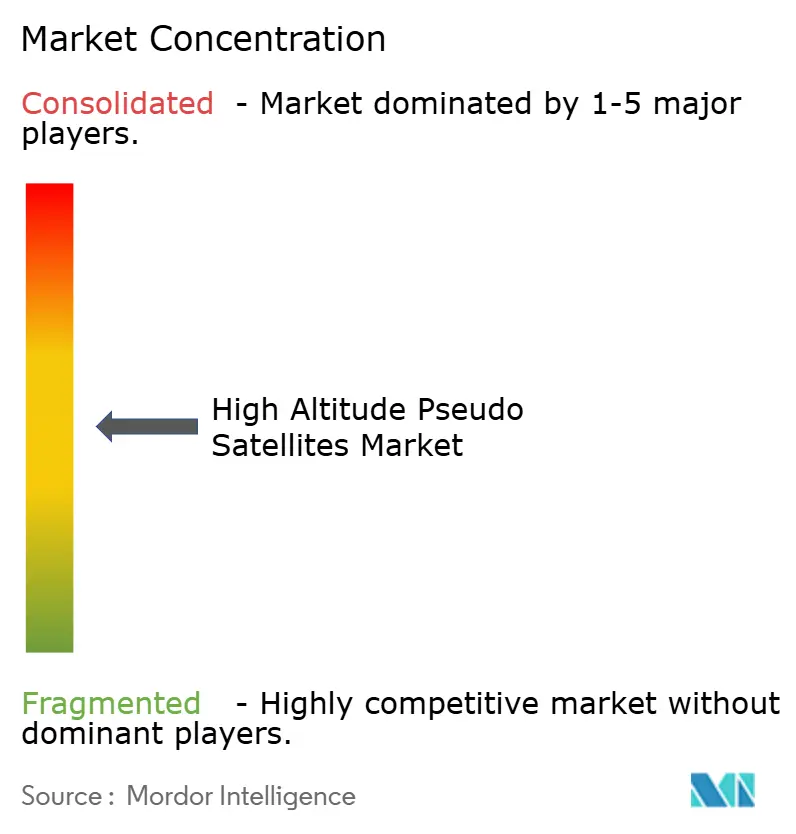

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Altitude Pseudo Satellites Market Analysis by Mordor Intelligence

The high-altitude pseudo-satellites market size is expected to grow from USD 85.30 million in 2025 to USD 102.28 million in 2026 and is forecasted to reach USD 247.56 million by 2031 at a 19.34% CAGR over 2026-2031. Demand stems from telecom operators racing to fill rural-connectivity gaps ahead of 6G standardization, defense ministries reallocating surveillance budgets toward stratospheric platforms, and regulators publishing airspace frameworks that shorten deployment cycles. Operators view the high-altitude pseudo-satellites market as an opportunity to deliver non-terrestrial 5G and early 6G services at a lower total cost of ownership than low-Earth-orbit constellations. Defense agencies favor year-round vigilance to avoid sortie-generation costs. Technological advancements in ultra-light solar modules, silicon-anode batteries, and hydrogen fuel cells extend mission endurance, while spectrum allocations in the 38 GHz and 47 GHz bands provide clear licensing paths. The sector’s momentum now hinges on proving multi-month stratospheric flights at costs that undercut satellite economics by an order of magnitude, a benchmark several pilots have neared since 2025.

Key Report Takeaways

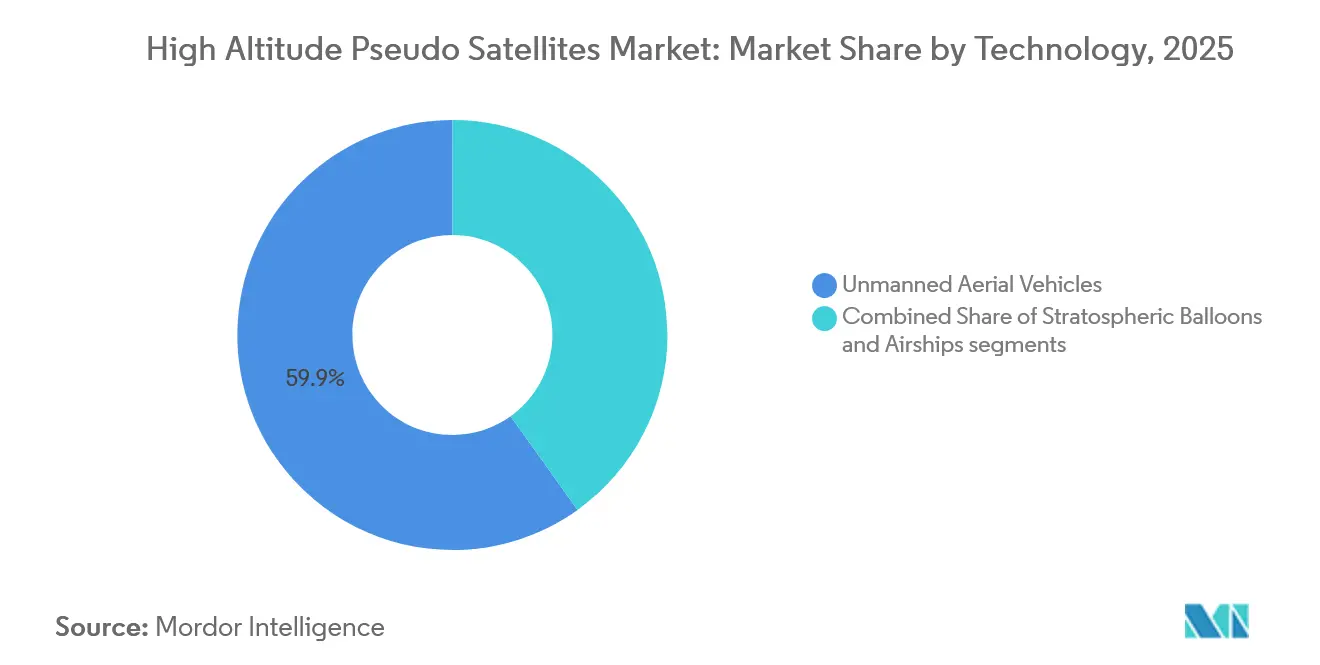

- By technology, unmanned aerial vehicles led with 59.85% of the high-altitude pseudo-satellites (HAPS) market share in 2025, while airships are forecast to expand at a 25.45% CAGR through 2031.

- By application, communication and connectivity captured 42.55% of 2025 revenue; the segment is projected to grow at a 24.40% CAGR to 2031.

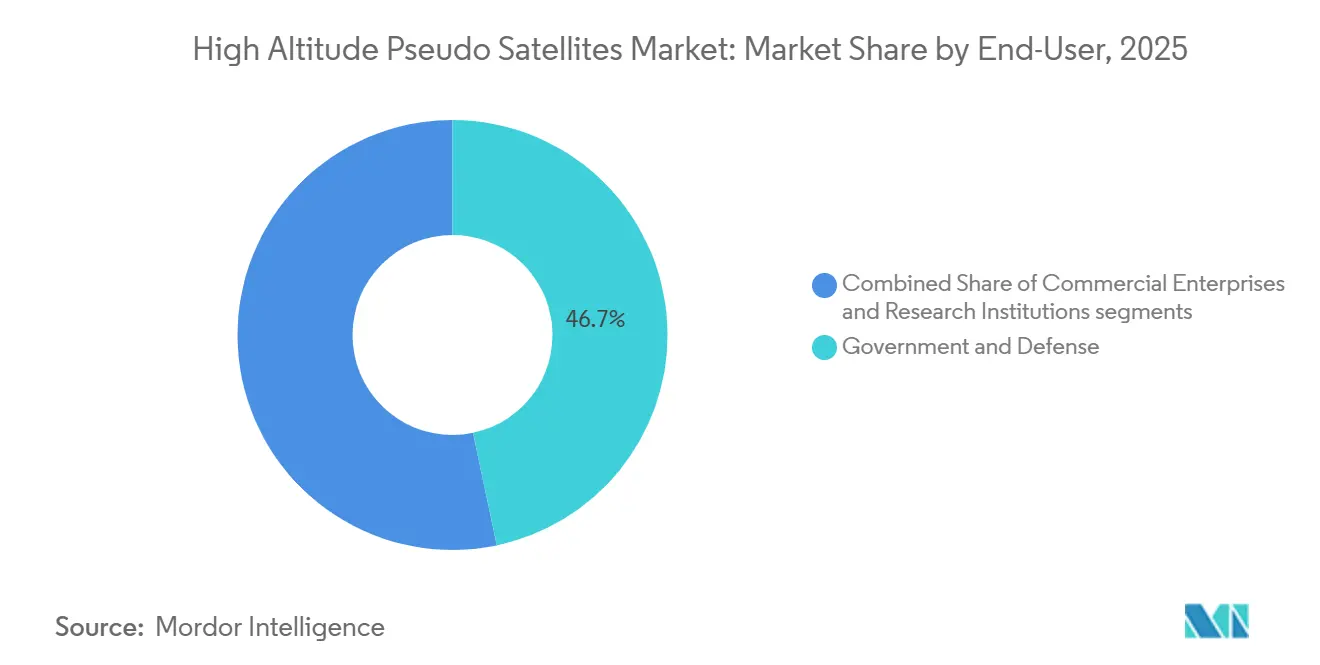

- By end-user, the government and defense sector held a 46.70% share of the high-altitude pseudo-satellites (HAPS) market size in 2025, while commercial enterprises recorded the fastest 25.50% CAGR through 2031.

- By power source, solar-electric systems accounted for 67.10% of 2025 installations, whereas hybrid hydrogen fuel cells advance at a 26.20% CAGR to 2031.

- By geography, North America led with 35.50% revenue in 2025, yet Asia-Pacific is the fastest region at a 25.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High Altitude Pseudo Satellites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G/6G NTN roll-outs | +4.5% | Global, early adoption in Japan, Kenya, EU test zones | Short term (≤ 2 years) |

| Growing ISR and persistent surveillance outlays | +3.2% | North America, Middle East, APAC border regions | Medium term (2-4 years) |

| Cost advantage over LEO constellations | +3.8% | Global rural and underserved markets | Medium term (2-4 years) |

| Advances in ultra-light solar/battery systems | +2.9% | Japan, Germany, United States | Long term (≥ 4 years) |

| Carbon-reduction mandates favoring low-emission rural backhaul | +2.1% | EU, North America, APAC spillover | Long term (≥ 4 years) |

| Stratospheric air-traffic corridors opened by regulators | +2.7% | North America, EU, ICAO guidance | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid 5G/6G NTN Roll-Outs

Telecom operators integrate stratospheric platforms into non-terrestrial networks to extend 5G coverage into areas where traditional tower economics are insufficient. Space Compass utilized an Aalto Zephyr to serve 1,000 users across a 140 km radius in Kenya in March 2025, confirming the commercial viability of its service. [1]Source: NTT DOCOMO, “Space Compass Completes Kenya HAPS Trial,” nttdocomo.co.jp HAPSMobile demonstrated 38 GHz millimeter-wave connectivity in May 2024 and targets commercial service in Japan by late 2026, positioning the high-altitude pseudo-satellite (HAPS) market for early 6G integration. 3GPP Release 18 treats HAPS as a network node, allowing vendors to ship dual-mode radios through established supply chains. [2]Source: 3GPP, “Release 18 Specifications,” 3gpp.org These moves reduce integration risk, accelerate equipment certification, and anchor revenue projections for operators that prioritize rural and maritime coverage.

Growing ISR and Persistent Surveillance Outlays

Defense ministries are redirecting surveillance budgets toward stratospheric platforms that can loiter for months and cost less than crewed aircraft. The United States Army evaluates unmanned alternatives because manned ISR flights exceed USD 10,000 per hour, while platforms like BAE Systems’ PHASA-35 demonstrated 24-hour stratospheric endurance in December 2024 with a doubled payload capacity. Sceye’s NASA partnership exemplifies civil-government adoption for wildfire tracking and methane detection, further broadening the high-altitude pseudo-satellite (HAPS) market's customer base. [3]Source: Sceye, “Partnership with NASA and USGS,” sceye.com Persistent presence without refueling underpins new concepts of operation where assets remain on-station year-round, improving situational awareness.

Cost Advantage over LEO Constellations

Capital expenditure per HAPS platform ranges from USD 10 million to USD 50 million, versus USD 500 million to USD 5 billion for a replenishable low-Earth-orbit satellite constellation. Operating costs between USD 1,000 and USD 5,000 per flight hour avoid the ground-station networks and launch cycles baked into satellite economics. Platforms shift 500 km within 24 hours by harnessing stratospheric winds, offering the agility that satellites cannot match. Retrieval enables refurbishment and payload refresh instead of total loss at end-of-life, reinforcing the high-altitude pseudo-satellites (HAPS) market value proposition for both telecom and defense users.

Advances in Ultra-Light Solar/Battery Systems

Endurance depends on power density. Amprius silicon-anode batteries delivered 450 Wh/kg during Zephyr’s 67-day flight in May 2025, a 40% leap over conventional lithium packs. SoftBank and Longi’s heterojunction modules weigh 665 g/m², achieving 22.2% conversion efficiency, which enables 1.5 kW of continuous power while preserving structural margins. Perovskite research published in 2024 shows potential for 44 W/g specific power, promising to double payload capacity if commercialized by 2028. These gains lengthen night-time reserves and narrow the gap between solar and emerging hydrogen solutions.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and maintenance cost per flight-hour | -3.5% | Global, acute in price-sensitive markets | Medium term (2-4 years) |

| Spectrum and airspace regulatory complexity | -2.8% | Global, fragmented ITU regions | Short term (≤ 2 years) |

| Stratospheric wind-shear unpredictability | -1.9% | Equatorial and polar latitudes | Long term (≥ 4 years) |

| Insurance and liability gaps for >30-day unmanned sorties | -1.6% | North America and EU underwriting | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Maintenance Cost per Flight-Hour

Acquiring a single platform demands USD 10 million–USD 50 million, a hurdle for operators without sovereign backing or deep capital pools. Multi-month missions consume USD 2.16 million to USD 10.8 million in direct OPEX, and each retrieval cycle can cost an additional USD 1 million for controlled descent, hull inspection, and gas replenishment. Limited secondary markets lock in depreciation, while rapid technology advances threaten obsolescence. These economics narrow the addressable high-altitude pseudo-satellites (HAPS) market to well-funded telecom carriers and defense agencies until modular designs drive down unit prices.

Spectrum and Airspace Regulatory Complexity

HAPS fly at altitudes of 20–50 km, a zone once unregulated for persistent aircraft. Operators must juggle ITU spectrum allocations, ICAO air traffic rules, and national approvals. The United States opened 47 GHz for HAPS in 2024, while many EU states await CEPT harmonization, due by 2027. Airworthiness remains a case-by-case process, creating multi-year backlogs. Each factor erodes deployment speed, delaying revenue conversion across the high-altitude pseudo-satellites (HAPS) market pipeline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: UAVs Lead, While Airships Accelerate

Unmanned aerial vehicles controlled 59.85% of the 2025 revenue within the high-altitude pseudo-satellite market, due to their proven solar-electric designs capable of carrying 150-lb payloads and multi-month flights. Airships emerge as the fastest-growing class at a 25.45% CAGR, propelled by hull fabrics that hold helium for year-long missions without retrieval. Balloons remain the low-cost choice for sub-30-day scientific campaigns. AeroVironment’s Horus A gained FAA certification in October 2024, demonstrating a clear path to commercial ISR contracting, whereas Sceye’s 270-ft airship targets telecom backhaul with a stationary footprint over 10,000 km².

Airships leverage buoyancy to hover almost motionless, consuming minimal propulsion energy, which is an advantage for video surveillance and backhaul applications that require stable pointing. UAVs utilize continuous propeller thrust, sacrificing higher energy needs for agile repositioning when disasters or seasonal events alter demand. Balloons serve universities needing rapid launches but lack station-keeping and controllability. Taken together, these trade-offs diversify revenue channels within the high-altitude pseudo-satellite (HAPS) market, with each technology catering to specific endurance, payload, and capital expenditure (Capex) tolerances.

By Application: Connectivity Dominates, Climate Monitoring Gains

Communication and connectivity platforms captured 42.55% of the 2025 revenue in the high-altitude pseudo-satellites (HAPS) market, and this portion is projected to grow at a 24.40% CAGR as mobile network operators embed HAPS nodes into rural 5G rollouts, reducing the need for expensive tower grids in sparsely populated areas. Intelligence, surveillance, and reconnaissance (ISR) capabilities follow, with militaries shifting from crewed patrol aircraft to persistent “eyes-in-the-sky” stratospheric assets that can loiter for weeks without refueling. Earth-observation and climate-monitoring demand is rising because NASA and USGS procure methane and wildfire data from stratospheric airships, creating a civilian revenue stream that diversifies operator income. Navigation and scientific missions remain niche but benefit from shared airtime, amortizing platform costs across multiple payload types to maintain high utilization.

The March 2025 Zephyr field trial demonstrated that one HAPS platform can cover the area typically served by approximately 50 macro towers, validating a compelling economic lever for rural telecom carriers. BAE Systems integrated a synthetic-aperture radar into its PHASA-35, demonstrating the ISR potential for border and maritime surveillance at a fraction of the cost of crewed aircraft. Sceye’s civil contracts demonstrate how environmental sensing revenues can subsidize connectivity payloads, creating blended business models. As dual-payload missions that pair broadband links with high-resolution imagery become common, operators increase flight utilization and shorten payback periods. This diversification reduces reliance on any single customer class, strengthens cash flows, and broadens the total addressable market for high-altitude pseudo-satellites (HAPS).

By End-User: Defense Anchors, Commercial Surges

Government and defense agencies controlled 46.70% of the 2025 revenue in the high-altitude pseudo-satellite (HAPS) market, as ISR budgets and border-monitoring mandates are well-funded despite fiscal pressure. The ability to hover for months without refueling lets commanders replace fleets of short-endurance drones and manned turboprops, generating significant life-cycle savings. Commercial enterprises, however, are posting the fastest growth rate of 25.50% CAGR as telecom carriers deploy rural broadband links and energy firms monitor pipelines and offshore assets. Research institutions secure smaller allocations aimed at atmospheric science, but they often collaborate with commercial operators to share airtime costs. This evolving mix signals a transition from defense-led pilots to broad commercial adoption, unlocking scalable manufacturing.

SoftBank’s plan to launch stratospheric service in Japan by 2026 marks a pivotal inflection point for commercial uptake. The project integrates HAPS relays into SoftBank’s terrestrial core, extending 5G coverage into mountainous regions where traditional tower economics are ineffective. Space Compass’s paying users in Kenya prove that rural customers will subscribe when pricing and reliability match terrestrial standards. As defense agencies validate multi-month endurance, commercial players inherit proven airframes, reducing technical risk. Insurance carriers also gain confidence, widening underwriting capacity. These dynamics accelerate cross-sector scale, making the high-altitude pseudo-satellites (HAPS) market attractive to infrastructure investors that previously focused on fiber and low-Earth-orbit constellations.

By Power Source: Solar Dominates, Hydrogen Advances

Solar-electric designs accounted for 67.10% of 2025 installations, driven by robust photovoltaic supply chains, declining panel prices, and steady efficiency gains that minimize the mass of energy storage. Hybrid hydrogen fuel-cell systems, although still emerging, are projected to post a 26.20% CAGR because they promise double the payload capacity and longer autonomous nights that can support multi-sensor ISR suites. Battery-only variants remain essential as redundancy, offering safe-mode power during cloud-shadow or fuel-cell maintenance events. Platform developers now design modular bays that can switch between solar, hydrogen, or hybrid stacks, depending on the mission length and power draw, ensuring procurement flexibility. This adaptability attracts telecom operators focused on cost, while militaries concentrate on performance, thereby enlarging the addressable high-altitude pseudo-satellite (HAPS) market.

Amprius silicon-anode batteries enhance nighttime endurance for solar platforms by delivering 450 Wh/kg, which extends loiter time without increasing wingspan or structural requirements. Concurrently, NASA is testing an approach of 1.5 kW/kg with fuel cells, edging toward the Department of Energy’s 2.0 kW/kg target and opening the door for high-power radar payloads. Solar, therefore, remains the preferred choice for telecom and earth-observation tasks with modest power requirements, while hydrogen solutions attract ISR programs that require kilowatt-class sensors. This bifurcation shapes corporate R&D roadmaps and procurement strategies, nudging suppliers to develop standard avionics that interoperate across both power architectures.

Geography Analysis

North America captured 35.50% of the 2025 revenue, buoyed by the Federal Aviation Administration's (FAA) high-altitude corridors, the Federal Communications Commission's 47 GHz spectrum allocations, and the Department of Defense's ISR budgets, which underwrite multi-year contracts. AeroVironment’s Horus A certification demonstrates that clear rules can shorten commercialization timelines, while partnerships with NASA and the USGS act as anchor tenants that de-risk cash flows. Venture capital and mature aerospace supply chains concentrate early production in the United States, fostering economies of scale that lower unit cost and expand the overall high-altitude pseudo-satellites (HAPS) market.

Asia-Pacific advances fastest at 25.70% CAGR through 2031, propelled by Japan’s scheduled commercial launches, India’s border-surveillance pilots, and China’s near-space vehicle programs. SoftBank’s late-2026 service will bridge significant coverage gaps and ensure seamless handoffs between terrestrial and stratospheric cells. Kenya’s proof-of-concept offers a template for emerging economies in Southeast Asia and Pacific islands, illustrating how HAPS enables mobile-money ecosystems and e-government services. Regional regulators in Australia and South Korea, as they evaluate spectrum releases, further widen the addressable high-altitude pseudo-satellite (HAPS) market.

Europe holds a mid-tier share but faces a regulatory lag until EASA's operational rules are finalized in 2026. BAE Systems’ PHASA-35 and DLR’s HAP-alpha flights demonstrate technical competence despite slower approvals. Middle Eastern operators deploy HAPS for oil-field connectivity under permissive airspace regimes, while Africa and South America remain embryonic, focusing on pilots in the Amazon and Sahel regions. Adoption is expected to accelerate once local regulators adopt ICAO templates, diversifying the global high-altitude pseudo-satellites (HAPS) market footprint.

Competitive Landscape

The high-altitude pseudo-satellites (HAPS) market exhibits moderate concentration, with aircraft integrators, telecom operators, and payload manufacturers forming cross-industry partnerships. Key differentiators include demonstrated endurance, payload capacity, production readiness, and regulatory approvals. AALTO's Zephyr achieved a 67-day endurance record in May 2025, highlighting the advantages of silicon-anode batteries and establishing the company as an early supplier to telecom carriers.

Sceye's 270-ft airship, supported by USD 525 million in Series C financing, aims to provide year-long stationary coverage for oil-and-gas and climate-monitoring customers. This diversification maintains high competitive intensity and distributes risk across workforce expertise, material supply chains, and regulatory compliance.

Technological approaches vary as solar UAVs focus on telecom payloads under 2 kW, hydrogen hybrids cater to ISR clients requiring 5 kW, and airships combine buoyancy with large platforms for multi-sensor arrays. Patent filings for station-keeping algorithms leveraging stratospheric winds indicate the development of stronger intellectual property protections. Early approvals from the FCC or FAA provide first-mover advantages, granting pioneers access to spectrum and airspace, enabling them to secure anchor customers ahead of competitors. As product portfolios grow, market consolidation is expected, with smaller European balloon vendors potentially merging or shifting toward research-focused niches. Ongoing design improvements, coupled with declining component costs, are driving the high-altitude pseudo-satellites (HAPS) market toward achieving greater endurance and reducing the cost per transmitted gigabyte.

High Altitude Pseudo Satellites Industry Leaders

AeroVironment, Inc.

Thales Group

BAE Systems plc

Airbus SE

Aurora Flight Sciences (The Boeing Company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Mira Aerospace, a subsidiary of UAE-based Space42, conducted the first civilian-approved high-altitude platform system (HAPS) flight in Europe. The solar-powered ApusNeo18, launched from Spain’s Fuerteventura Technology Park, gathered data for wildfire prevention under the ISSEC program, a collaboration between Telespazio Ibérica and Pegasus Aero Group. This event highlights the strategic importance of HAPS in enhancing disaster management capabilities, offering real-time data and operational efficiency. It highlights a growing market opportunity for governments and private entities to leverage aerial monitoring technologies to strengthen emergency response frameworks and optimize resource allocation.

- May 2025: Amprius Technologies announced its silicon anode batteries powered AALTO’s Zephyr high-altitude pseudo-satellite (HAPS) aircraft during a record-breaking 67-day stratospheric flight. This milestone highlights the critical role of advanced energy storage in supporting long-endurance HAPS operations, a key area of growth in aerospace. The collaboration between Amprius and AALTO demonstrates the increasing demand for reliable, high-performance battery technology to extend operational capabilities. This development validates Amprius’ position in the market and signals a broader industry trend toward sustainable, high-altitude platforms, likely driving further innovation and investment in energy solutions for aerospace applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the high-altitude pseudo-satellites market as solar- or hybrid-powered unmanned airships, balloons, and fixed-wing platforms that operate in the stratosphere between 18 km and 30 km, deliver persistent communication, intelligence, surveillance, reconnaissance, and earth-observation services, and are sold as new complete systems to defense, governmental, and commercial operators. According to Mordor Intelligence, the global market is valued at about USD 85.30 million in 2025 and is tracked through 2030.

Scope exclusion: After-sales spares, payload upgrades, and launch support services are not counted.

Segmentation Overview

- By Technology

- Stratospheric Balloons

- Unmanned Aerial Vehicles

- Airships

- By Application

- Communication and Connectivity

- Intelligence, Surveillance and Reconnaissance (ISR)

- Earth Observation and Climate Monitoring

- Navigation and Positioning

- Scientific and Research Missions

- By End-User

- Government and Defense

- Commercial Enterprises

- Research Institutions

- By Power Source

- Solar-Electric

- Hybrid Hydrogen-Fuel-Cell

- Battery

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed propulsion engineers, stratospheric test-range managers, spectrum regulators, and procurement officials across North America, Europe, and Asia. These discussions helped us validate endurance assumptions, typical platform pricing, and regional deployment hurdles, closing information gaps found during desk work.

Desk Research

We began with public datasets that report on stratospheric airspace usage and broadband-coverage gaps, such as NASA flight logs, the US Federal Aviation Administration unmanned aircraft registry, International Telecommunication Union connectivity statistics, and European Space Agency stratospheric flight test archives. Our team also pulled defense budget line items for persistent ISR programs, customs shipment codes for composite airframes, and patent filings on high-efficiency solar films via Questel to benchmark technology readiness.

Next, we tapped D&B Hoovers for company financials, Dow Jones Factiva for program announcements, World Bank rural-population trends, and respected trade associations like the Global Uncrewed Traffic Management Alliance to round out production and demand signals. These sources illustrate our approach and are not exhaustive; many additional references supported data checks and clarification.

Market-Sizing & Forecasting

We apply a top-down build that starts with known prototype counts, planned procurement budgets, and regional telecom-backhaul white spots, which are then translated into unit demand through platform endurance and service-life metrics. We corroborate the totals with selective bottom-up checks that roll up sampled average selling prices from supplier disclosures and channel insights. Key variables in our model include stratospheric flight hours logged, solar-cell efficiency gains, defense ISR allocation growth, 5G coverage deficit by population, and energy-storage density improvements. Multivariate regression forecasts each driver, and scenario analysis stress tests high-growth and restrained adoption cases before we lock the base case.

Data Validation & Update Cycle

Outputs are triangulated against historical HAPS crash statistics, manufacturer backlogs, and satellite-capacity lease prices. Any variance beyond preset thresholds triggers a senior review and a call back to high-priority respondents. Reports refresh once a year, and we issue interim revisions when material program awards or regulatory shifts occur. A last-mile analyst check is conducted before delivery.

Why Mordor's Pseudo-Satellite Baseline Commands Reliability

Published estimates seldom match because publishers pick different scopes, base years, and currency conversion points, and they refresh models at varied cadences. We recognize these factors upfront, and our disciplined inclusion criteria, driver selection, and annual update rhythm keep our baseline steady yet current.

Key gap drivers include broader "high-altitude platform" scopes used by some firms, older or more aggressive base-year exchange rates, and models that assume immediate mass production ramps without validating endurance test data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 85.30 m (2025) | Mordor Intelligence | - |

| USD 104.5 m (2024) | Regional Consultancy A | Includes tethered aerostats and service contracts |

| USD 99 m (2024) | Global Consultancy B | Uses single average platform price, omits regional weighting |

| USD 85 m (2023) | Trade Journal C | Older base year, does not adjust for inflation |

Taken together, the comparison shows that our carefully bounded scope, driver-led model, and timely updates produce a balanced, transparent foundation that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What is the projected value of the high-altitude pseudo-satellites (HAPS) market by 2031?

The market is forecast to reach USD 255.90 million by 2031, reflecting a 20.13% CAGR.

Which region will grow fastest in high-altitude pseudo-satellites deployment?

Asia-Pacific leads with a 25.70% forecast CAGR, driven by Japanese commercial launches and Indian border-monitoring projects.

Why do telecom operators prefer HAPS over terrestrial towers in rural zones?

A single platform can blanket a 140 km radius, equating to roughly 50 macro towers, lowering capex while meeting coverage mandates.

What technology currently dominates the power source mix?

Solar-electric systems account for 67.10% of installed platforms thanks to mature photovoltaic and battery supply chains.

How long can modern HAPS platforms remain aloft?

Endurance records reached 67 days in 2025, and year-long missions are expected once current airship programs enter service.

Page last updated on: