Heat Meter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

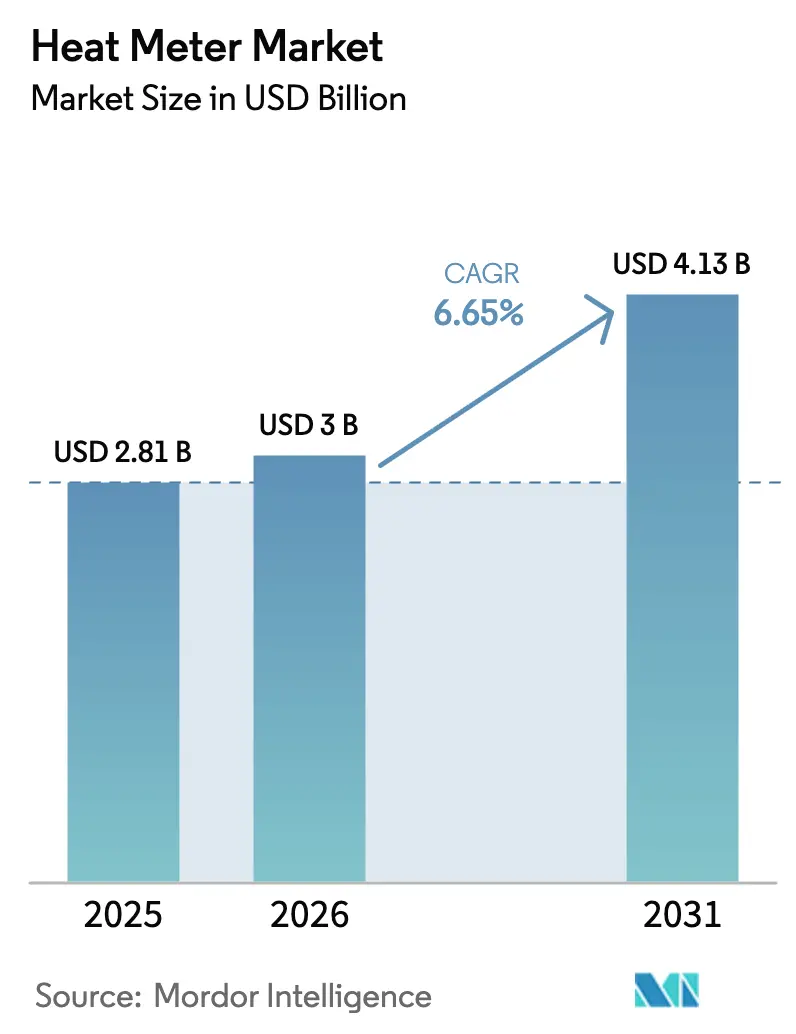

| Market Size (2026) | USD 3 Billion |

| Market Size (2031) | USD 4.13 Billion |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heat Meter Market Analysis by Mordor Intelligence

Heat meter market size in 2026 is estimated at USD 3 billion, growing from 2025 value of USD 2.81 billion with 2031 projections showing USD 4.13 billion, growing at 6.65% CAGR over 2026-2031. Growing demand for energy-efficient billing, modernization of district heating networks, and a clear shift toward ultrasonic and electromagnetic static meters underpin this trajectory. Regulatory mandates in Europe require consumption-based cost allocation, while North America’s aging infrastructure replacement programs and Asia-Pacific’s smart city projects widen the adoption base. Utilities increasingly favor wireless connectivity to reduce installation costs and enable real-time monitoring, and fourth-generation district heating systems operating at lower temperatures encourage integration of renewable heat sources. Market opportunities are further amplified by carbon-credit monetization for sub-metering and by predictive maintenance platforms that cut operational expenses in dense urban distribution networks.

Key Report Takeaways

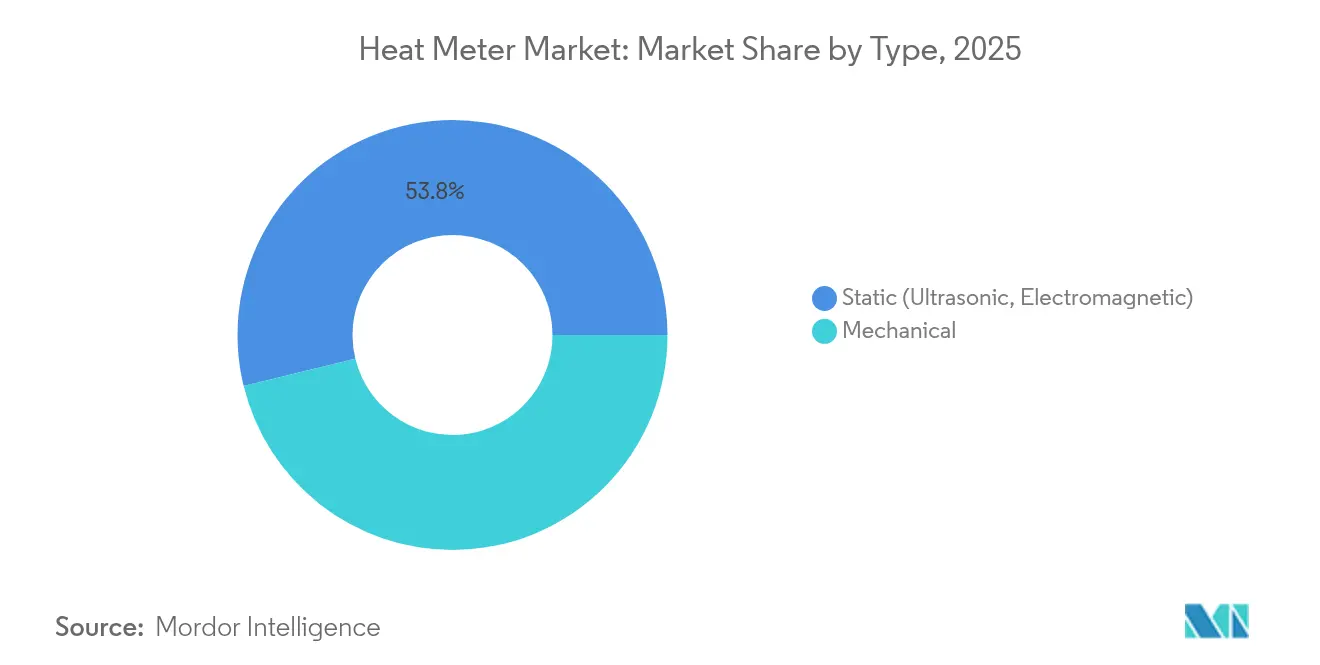

- By type, static meters led with 53.82% heat meter market share in 2025; mechanical alternatives are forecast to trail as static meters expand at an 8.03% CAGR to 2031.

- By connectivity, wireless solutions captured 62.85% of the heat meter market size in 2025 and are poised to grow at a 6.83% CAGR through 2031.

- By measurement principle, electromagnetic meters accounted for 58.62% heat meter market share in 2025, while ultrasonic technology records the fastest 8.47% CAGR to 2031.

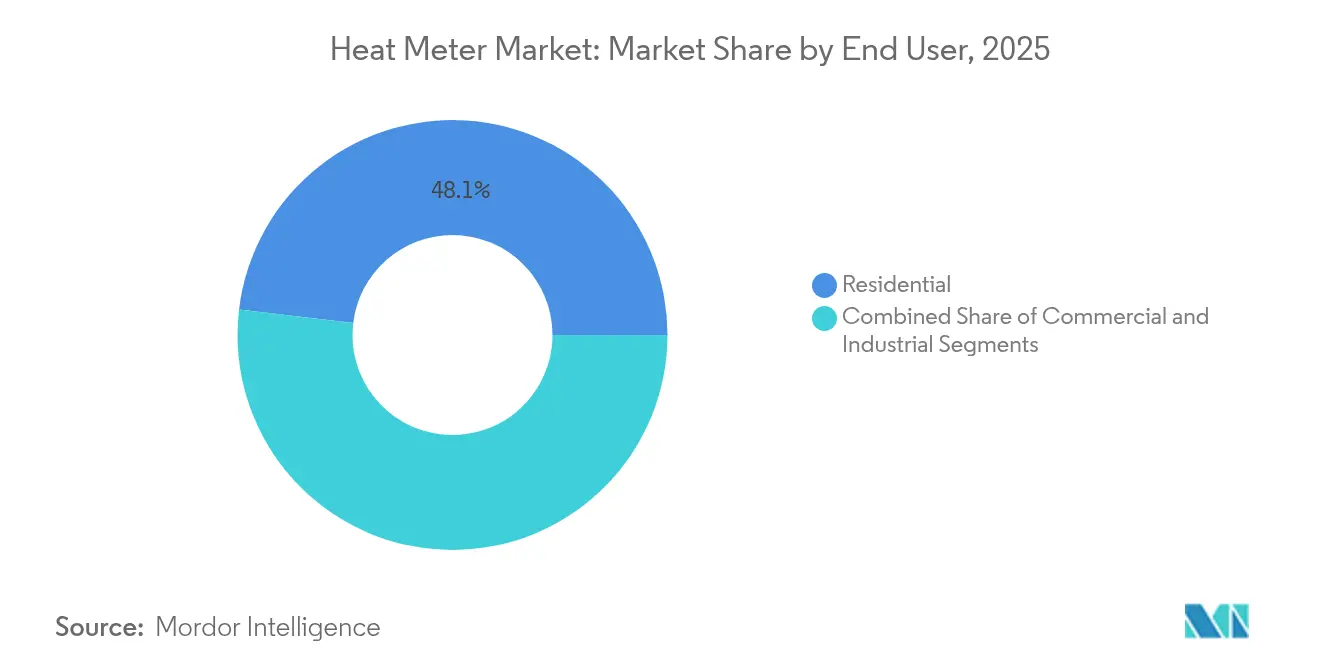

- By end-user, the residential segment held 48.10% of the heat meter market size in 2025; the industrial segment is projected to expand at 8.55% CAGR between 2026-2031.

- By application, process heat monitoring represented 39.88% of demand in 2025; HVAC sub-metering is advancing at a 7.31% CAGR to 2031.

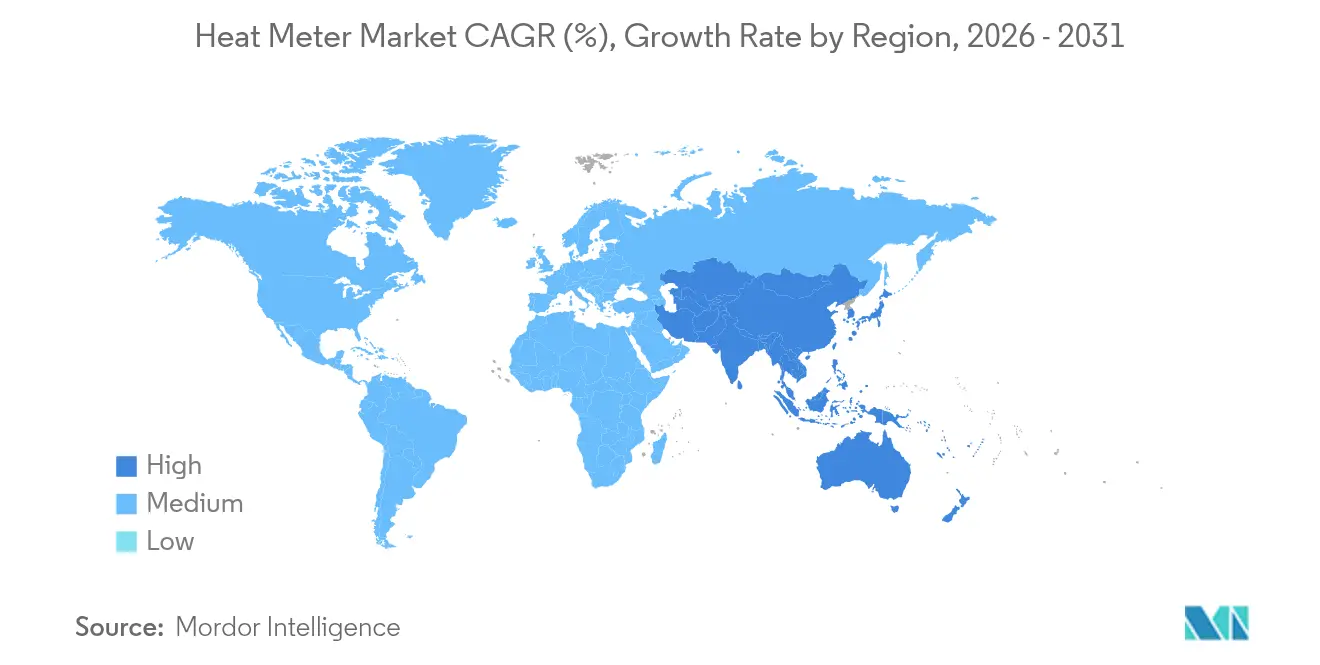

- By geography, North America dominated with 38.74% revenue share in 2025; Asia-Pacific delivers the fastest 8.12% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Heat Meter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for energy-efficient billing in district heating | +1.8% | Europe, North America | Medium term (2-4 years) |

| Government mandates for consumption-based cost allocation | +1.5% | Global (strongest in EU) | Short term (≤ 2 years) |

| Retro-fit smart meter roll-outs in Europe | +1.2% | Europe, spill-over to North America | Medium term (2-4 years) |

| AI-based anomaly detection lowering OPEX | +0.9% | Global, developed markets | Long term (≥ 4 years) |

| Carbon-credit monetization for sub-metering projects | +0.7% | EU, North America, select APAC | Long term (≥ 4 years) |

| Waste-heat recovery in EU industrial clusters | +0.6% | Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for Energy-Efficient Billing in District Heating

Fourth-generation district heating networks require precise household-level billing to optimize low-temperature, renewable-integrated systems. Stadtwerke Flensburg, for example, installed more than 19,000 ultrasonic meters coupled with Heat Intelligence analytics and achieved a 24.52% average consumption reduction across buildings. [1]Kamstrup, “Heat Intelligence Case Studies,” kamstrup.com Utilities leverage this data to fine-tune return temperatures, lower pumping costs, and introduce dynamic tariffs that flatten peak loads. High penetration of district heating in Scandinavia, where household coverage exceeds 50%, sets an influential benchmark that other European cities now emulate. The operational data stream also creates a foundation for predictive maintenance, preventing unplanned outages and elevating customer satisfaction.

Government Mandates for Consumption-Based Cost Allocation

The revised Energy Performance of Buildings Directive compels EU member states to achieve deep energy renovations in the worst-performing building stock by 2030, effectively obligating the installation of smart heat metering devices capable of granular usage tracking. [2]European Parliament and Council, “Recast EPBD,” europarl.europa.eu Germany’s Heat Planning Act and Poland’s large-scale smart meter tenders underscore the political urgency. Utilities now face compressed deployment windows, driving record procurement volumes and pressuring manufacturers to scale production without sacrificing 15- to 20-year warranty requirements. Compliance costs for building owners initially inflate project budgets, yet payback periods shrink as optimized billing cuts unbilled consumption and improves renovation economics.

Retro-fit Smart Meter Roll-outs in Europe

European cities substitute mechanical meters ahead of their natural replacement cycle because wireless retro-fit solutions avoid costly excavation. The UK’s extended partnership between Landis+Gyr and Horizon Energy Infrastructure provides continuity for smart meter deployments beyond 2026, ensuring utilities can meet Ofgem’s advanced metering targets.[3]Landis+Gyr, “UK Smart Meter Roll-out Extension,” landisgyr.com In Denmark, Aalborg District Heating achieved 95% automated reading within three years by prioritizing plug-and-play ultrasonic retrofits. Declining battery prices and 15-year life expectancy now tilt the total cost-of-ownership calculus in favor of wireless retro-fits even in smaller municipalities, accelerating knowledge transfer to emerging regional markets such as Eastern Europe.

AI-based Anomaly Detection Lowering OPEX

Utilities adopt machine-learning models—such as Long Short-Term Memory auto-encoders—to detect sensor drift and flow anomalies with 91% accuracy up to 40 hours before failure, decreasing maintenance costs by roughly 25%. Cisco’s IoT Control Center flagged meter glitches that conventional systems missed during winter peaks, resolving billing disputes and avoiding emergency dispatches.[4]Cisco Systems, “IoT Control Center for Utilities,” cisco.com Cloud platforms now deliver these analytics as a service, enabling mid-sized district-heating firms to benefit without heavy infrastructure investments. OPEX savings elevate internal rates of return, offsetting the higher capex of ultrasonic units and pushing utilities toward full-stack digital solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX of ultrasonic static meters | -1.4% | Global, price-sensitive markets | Short term (≤ 2 years) |

| Limited interoperability of wireless protocols | -0.8% | Global, fragmented regions | Medium term (2-4 years) |

| Scarcity of calibrated testing benches in APAC | -0.6% | Asia-Pacific | Medium term (2-4 years) |

| Cyber-security compliance costs (IEC 62443) | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX of Ultrasonic Static Meters

Ultrasonic devices cost 40–60% more than mechanical counterparts, and ancillary expenses for specialized install crews lift project totals by a further 15–20%. Mexico’s hybrid roll-out for 1 million meters highlights how utilities stagger replacements, dedicating ultrasonic units to high-value accounts while retaining mechanical meters elsewhere. Component prices are trending downward, yet the short-term sticker shock still deters budget-constrained utilities in Asia-Pacific and Latin America. Financing innovations such as meter-as-a-service are emerging, but uptake remains patchy outside developed markets.

Limited Interoperability of Wireless Protocols

The coexistence of Wireless M-Bus, LoRaWAN, NB-IoT, and proprietary stacks forces utilities to manage multiple data backbones. Quectel and STACKFORCE’s new dual-mode LoRa/W-Mbus module tries to bridge the gap, but adds cost and complexity. Data silos curb the potential of big-data analytics and oblige operators to maintain parallel firmware lines, delaying return on investment for advanced analytics. National standardization efforts are underway, yet industry consensus is unlikely before 2027, prolonging the restraint’s impact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Static Meters Drive Precision Revolution

Static meters held 53.82% of the heat meter market in 2025 and are forecast to expand at an 8.03% CAGR, displacing mechanical units as utilities emphasize longevity and low maintenance. Kamstrup’s flowIQ range illustrates the transition, using ultrasonic transducers and acoustic leak detection to maintain ±0.5% accuracy over 20 years. Electromagnetic variants within the static family allow accurate bi-directional measurement in industrial loops with varying conductivity, while mechanical meters persist in subsidy-constrained retro-fits. The heat meter market benefits when overall service calls drop, freeing utility budgets for network optimization software.

Cost parity between mechanical and static designs is narrowing due to volume production, and predictive analytics heighten the value proposition. As static devices integrate NB-IoT chips, they also support real-time network balancing, a feature that mechanical meters cannot offer. Emerging best-practice guidelines position static units as the default for new district heating grids, signaling continued dominance through 2031.

By Connectivity: Wireless Solutions Dominate Infrastructure Evolution

Wireless solutions accounted for 62.85% of the heat meter market in 2025, a lead set to widen as LoRaWAN and NB-IoT networks proliferate. NB-IoT enjoys nationwide coverage in China, enabling utilities to roll out millions of meters without building private gateways LoRaWAN remains the protocol of choice for private deployments across Europe and North America, offering ownership of data flow and flexibility in dense urban cores. Battery chemistries now support 15-year lifespans, mitigating earlier concerns about service visits.

Wired protocols such as M-Bus and BACnet retain a niche where high data density or on-site power make cabling cost-effective, for example in large commercial campuses. However, trenching costs of USD 1,000 per meter in congested districts strongly favor wireless retro-fits. Honeywell’s 5G-ready platform built with Verizon exemplifies the push toward higher-bandwidth applications such as real-time demand response.

By Measurement Principle: Electromagnetic Precision Meets Ultrasonic Innovation

Electromagnetic meters led with 58.62% heat meter market share in 2025, praised for stable accuracy across conductive mediums and bidirectional loops common in industrial clusters. Ultrasonic designs, growing at 8.47% CAGR, shine in residential and commercial districts where maintenance resources are scarce. Hybrid meters featuring dual principles are entering pilot projects to ensure redundancy in mission-critical applications such as petrochemical steam networks.

The interplay of principles is less about price and more about matching performance envelopes. Electromagnetic coils tolerate particle-rich flows, while ultrasonic transducers excel in clean water glycol mixes typical of modern heat pumps. Combined, they allow utilities to optimize portfolios without sacrificing accuracy thresholds mandated in Europe (Class 2 or better).

By End-User: Residential Dominance Challenged by Industrial Growth

Residential installations captured 48.10% of the heat meter market in 2025 but face rising competition from industrial applications where waste-heat capture is central to net-zero road-maps. Corporate ESG reporting increasingly requires sub-metering of process heat, propelling double-digit installation growth in chemicals and food and beverage plants. Commercial real estate adds another layer of demand as international green-building certifications require room-level consumption data.

Individual apartment metering in Europe fuels residential adoption, but strict payback criteria in social housing keep mechanical meters alive for a time. Emirates District Cooling integrated Kamstrup meters into Dubai towers to withstand 45 °C ambient temperatures, demonstrating the geographic reach of high-spec devices. Meanwhile, industrial users link meters to MES platforms, converting thermal data into predictive maintenance triggers for rotating equipment.

By Application: Process Monitoring Leads Digital Transformation

Process heat monitoring remained the largest application with 39.88% of 2025 revenue, underscoring its critical role in steam cycle efficiency and product quality. Predictive models built on meter data trimmed unplanned downtime in pulp mills by 12% on average, saving energy and lost production. HVAC sub-metering, the fastest-growing application at 7.31% CAGR, benefits from tighter building codes and occupant comfort objectives. Aars District Heating cut bypass valves from 200 to 16 and lowered average network loss by 7.8 MWh per customer using Heat Intelligence, exemplifying HVAC efficiency gains .

District heating and cooling continues expanding geographically, yet its per-unit growth lags as buildings switch to heat pumps. Even so, district schemes anchor thermal storage integration, and meter data facilitates peak-shaving strategies essential for renewable penetration.

Geography Analysis

North America commanded 38.74% of 2025 revenue, supported by federal infrastructure grants and state-level decarbonization statutes. Xcel Energy’s 200,000-meter program across the Dakotas typifies large utility investments in advanced metering infrastructure . U.S. cities such as Minneapolis and Vancouver pursue district-thermal expansions requiring high-accuracy billing. Canada invests in district heating for mixed-use urban cores, pairing geothermal boreholes with low-temperature distribution and demanding meters that function at variable flow rates. Mexico’s million-unit water-meter initiative illustrates broader Latin American modernization, foreshadowing heat metering opportunity as climate-adaptive cooling loops emerge.

Asia-Pacific registers the fastest 8.12% CAGR through 2031. China’s nationwide NB-IoT network underpins rapid wireless uptake, while Japan accelerates investment to enhance energy security. India’s Smart Meter National Program that channels USD 2.5 million into SAT Private Limited signals robust long-term demand for connected metering. South Korea leverages heat meters for hydrogen-ready district heating pilots, whereas Australia deploys precinct-scale systems in growing urban corridors. Constraints remain: a shortage of accredited calibration benches delays large tenders, and divergent national standards complicate cross-border equipment trade.

Competitive Landscape

The heat meter market shows moderate fragmentation. Kamstrup, Danfoss, and Itron combine hardware, analytics, and service layers to lock in recurring revenues. Kamstrup’s partnership with Avance Metering bundles SaaS analytics to elevate customer switching costs. Itron’s DLMS-based residential meter broadens its addressable base by lowering integration costs. Danfoss pursues open-protocol gateways, betting interoperability will win bids in data-centric municipalities.

Private-equity confidence rose after TPG and GIC acquired Techem for EUR 6.7 billion (USD 7.89 billion), underscoring digital revenue potential. Competitors respond with targeted M&A: Fidelix bought 40% of Lansen Systems to deepen sensor portfolios, and Landis+Gyr joined SPAN to develop circuit-level grid flexibility solutions. White-space entrants focus on AI and blockchain for carbon-credit verification. Cisco’s anomaly-detection module penetrates utility accounts where legacy OEMs cannot provide comparable analytics.

Overall, suppliers differentiate on cyber-security compliance (IEC 62443), battery lifespan, and ability to integrate heterogeneous data flows. Market entry barriers remain moderate; however, incumbents’ installed bases confer data scale that reinforces machine-learning models, making late entrants focus on niche innovations or regional specialization.

Heat Meter Industry Leaders

Apator S.A.

BMETERS Srl

Cosmic Technologies

Danfoss

Diehl Stiftung & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Itron and CHINT Global launched the first residential electric smart meter based on the DLMS Generic Companion Profile standard, boosting interoperability and cutting deployment cost.

- February 2025: Fidelix Holding Oy acquired 40% of Lansen Systems AB to enlarge its smart sensor footprint and deepen access to Nordic residential building owners.

- February 2025: Landis+Gyr and SPAN partnered to enhance electrification and grid flexibility through circuit-level billing-grade metering integration.

- January 2025: ConnectM Technology Solutions acquired MHz Invensys to expand its advanced RF mesh technology for next-gen AMI projects.

Global Heat Meter Market Report Scope

Heat meters, also known as thermal energy meters or energy meters, measure the thermal energy transferred from a source to a sink. They do this by gauging the flow rate of the heat transfer fluid and monitoring the temperature difference (ΔT) between the system's outflow and return legs. Commonly found in industrial plants, these meters assess boiler outputs and the heat utilized in processes. Additionally, in district heating systems, they quantify the heat supplied to consumers.

The heat meter market is segmented by type (mechanical, static), connectivity (wireless, wired), end-user (residential, commercial, industrial, others), geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Mechanical |

| Static (Ultrasonic, Electromagnetic) |

| Wired (M-Bus, Modbus, BACnet) |

| Wireless (NB-IoT, LoRaWAN, wM-Bus) |

| Ultrasonic |

| Electromagnetic |

| Superstatic |

| Residential |

| Commercial (Offices, Retail, Hospitals) |

| Industrial (Chemicals, Food and Bev., District Energy Plants) |

| District Heating and Cooling |

| HVAC Sub-Metering |

| Process Heat Monitoring |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Type | Mechanical | ||

| Static (Ultrasonic, Electromagnetic) | |||

| By Connectivity | Wired (M-Bus, Modbus, BACnet) | ||

| Wireless (NB-IoT, LoRaWAN, wM-Bus) | |||

| By Measurement Principle | Ultrasonic | ||

| Electromagnetic | |||

| Superstatic | |||

| By End-User | Residential | ||

| Commercial (Offices, Retail, Hospitals) | |||

| Industrial (Chemicals, Food and Bev., District Energy Plants) | |||

| By Application | District Heating and Cooling | ||

| HVAC Sub-Metering | |||

| Process Heat Monitoring | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the heat meter market?

The heat meter market size is USD 3 billion in 2026 and is forecast to grow to USD 4.13 billion by 2031, reflecting a 6.65% CAGR.

Which segment leads the heat meter market by type

Static meters, including ultrasonic and electromagnetic designs, hold 53.82% of 2025 revenue and are expanding at an 8.03% CAGR.

Why are wireless solutions gaining preference in heat metering?

Wireless connectivity avoids costly trenching, enables real-time data capture, and now offers 15-year battery lifespans, driving 62.85% market share in 2025.

How do government mandates influence heat meter adoption?

EU directives require consumption-based billing and deep renovations, compelling utilities to retrofit smart meters on tight timelines and boosting global demand.

Page last updated on: