Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

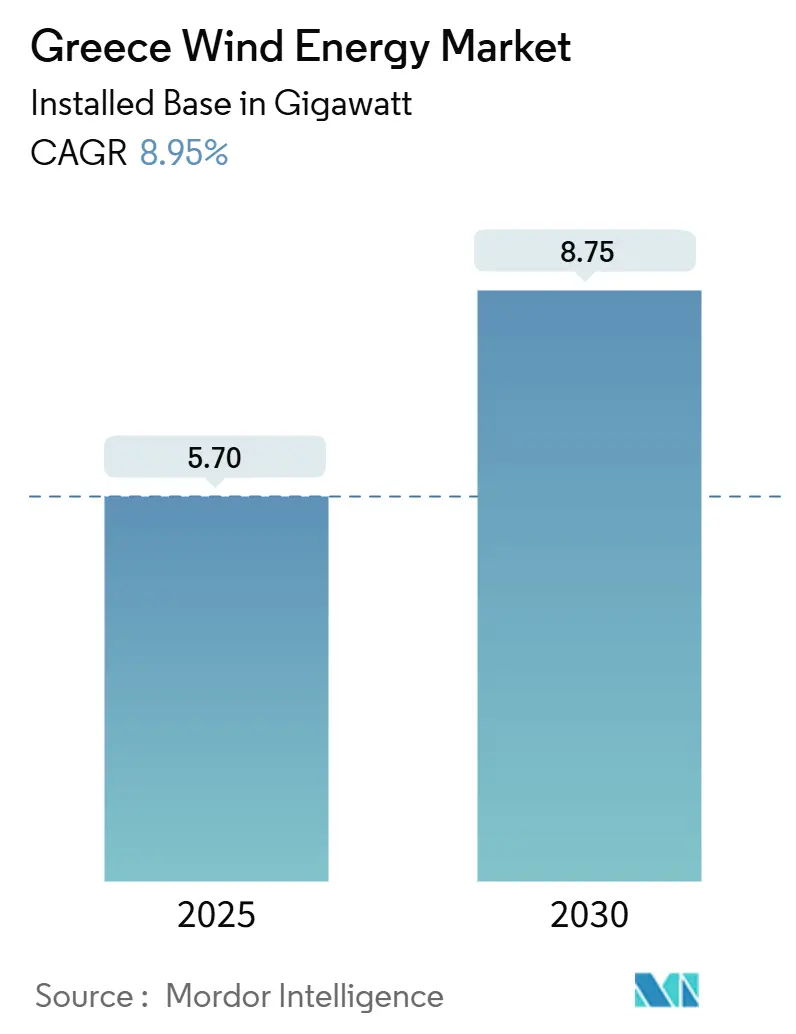

| Market Volume (2025) | 5.70 gigawatt |

| Market Volume (2030) | 8.75 gigawatt |

| Growth Rate (2025 - 2030) | 8.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Greece Wind Energy Market Analysis by Mordor Intelligence

The Greece Wind Energy Market size in terms of installed base is expected to grow from 5.70 gigawatt in 2025 to 8.75 gigawatt by 2030, at a CAGR of 8.95% during the forecast period (2025-2030).

In Greece, the current momentum is anchored in the National Energy and Climate Plan, which aims to achieve 9.2 GW of installed wind capacity by 2030 (but a shortfall is predicted), firmly positioning the country as a power exporter in the Eastern Mediterranean. Investor confidence is reinforced by wind and solar supplying nearly 50% of domestic electricity demand in 2024. A 100% onshore project mix today is gradually giving way to offshore pilots as floating‐foundation technology matures, while utility-scale projects dominate the build-out path due to economies of scale and favorable auction rules. Larger turbines above 5 MW are gaining share because they lower the levelized cost of energy in Greece’s mountainous and island terrains. Rising foreign capital, EU Recovery and Resilience Facility grants, and expanded grid interconnections combine to reinforce the long-term growth trajectory and to mitigate curtailment risks on the Aegean islands.

Key Report Takeaways

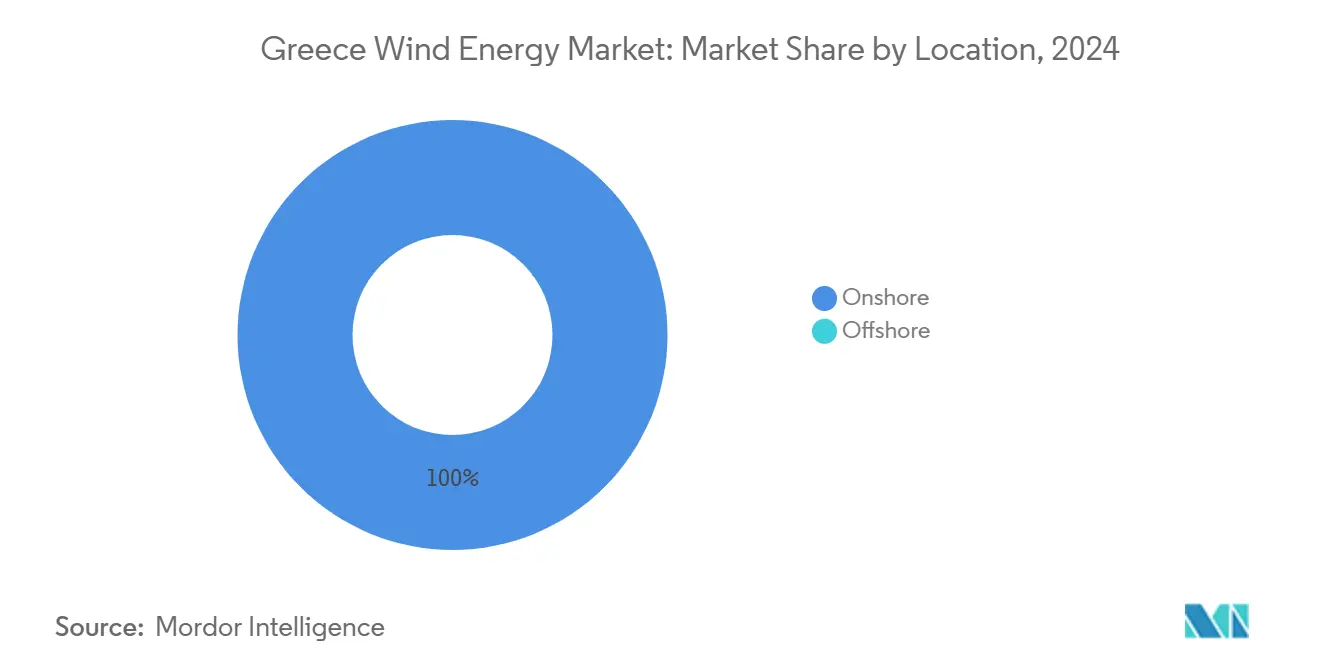

- By location, onshore installations held 100% of capacity in 2024, while offshore installations are projected to reach 1.5 GW by 2030.

- By turbine capacity, the 3-6 MW class commanded 47.5% of the Greek wind energy market share in 2024; turbines above 6 MW are projected to expand at a 15.8% CAGR during 2025-2030.

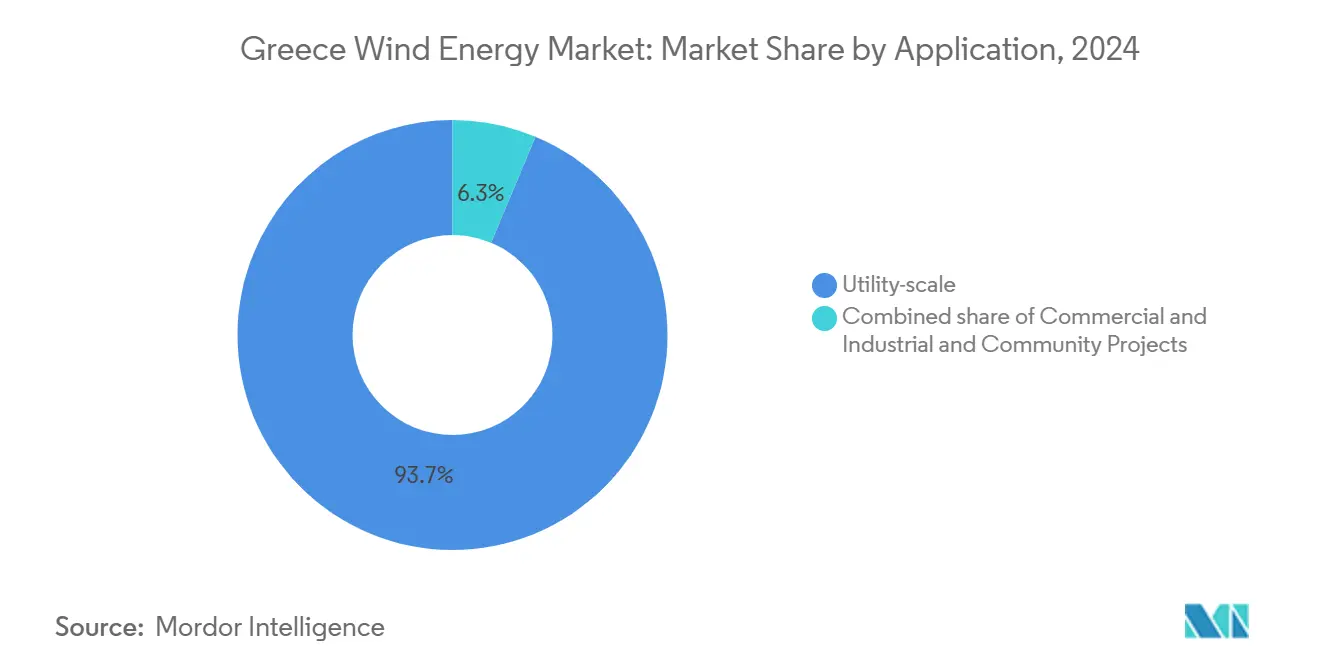

- By application, utility-scale projects accounted for 93.7% of the Greek wind energy market size in 2024, whereas commercial & industrial installations are advancing at a 12.5% CAGR to 2030.

- Masdar, GEK TERNA, and TERNA Energy collectively controlled 29% of the installed wind capacity in 2024, underscoring the ongoing consolidation among the top developers.

Greece Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive feed-in premiums and RES auctions | +2.1% | Mainland Macedonia, Thrace, Peloponnese | Medium term (2-4 years) |

| Raised NECP 2030 target to 9.2 GW | +1.8% | National | Long term (≥ 4 years) |

| Falling LCOE for ≥5 MW onshore turbines | +1.5% | High-wind zones on Aegean coast and in Evros | Short term (≤ 2 years) |

| RRF funding inflow | +1.3% | Priority to non-interconnected islands and offshore pilot areas | Medium term (2-4 years) |

| Military-base decarbonization tenders | +0.6% | Attica, Thessaloniki, Crete | Short term (≤ 2 years) |

| Green-hydrogen demand from Greek shipping | +1.2% | Offshore zones around Crete, Alexandroupolis, Dodecanese and mainland ports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supportive Feed-in Premiums & RES Auctions Under NECP

Greece’s sliding premium scheme guarantees a stable revenue floor, bridging the gap between reference and market prices while preserving spot-price signals.(1)European Commission, “State Aid SA.44666—Greece Renewable Energy Scheme,” ec.europa.eu This approach underpinned the country’s 57% renewable electricity share in 2023 and catalyzed competitive bidding that drove tariffs down. Predictable cash flows have attracted international capital, as illustrated by Masdar’s 2024 acquisition spree and Amazon’s corporate power-purchase commitments from 2024 to 2025. Auction discipline and premium degradation create a virtuous cycle: developers sharpen cost structures, the government limits subsidy outlays, and consumers gain from lower wholesale prices. Over time, premium volumes taper as merchant exposure rises, gradually integrating wind assets into Greece’s liberalized power market.

Raised NECP 2030 Target to 9.2 GW Wind Capacity

The revised target accelerates onshore additions to 8.9 GW and installs 1.9 GW offshore capacity by 2030.(2)Enerdata, “Greece Raises NECP Targets,” enerdata.net Implementation hinges on synchronized spending across generation, transmission, and storage. The Independent Power Transmission Operator (IPTO) is earmarking EUR 4.1 billion to reinforce the backbone grid, enabling 28 GW of renewable capacity to be integrated. Complementary legislation passed in 2024 established a dedicated offshore zoning and permitting pathway, aligned with floating technologies, suited to the Aegean’s deep waters. Smoother permitting and grid readiness raise investor confidence, ensuring the accrual of first-mover advantages in an increasingly crowded Mediterranean offshore arena.

Falling LCOE for More Than 5 MW Onshore Turbines

Cost curves continue to shift as hub heights increase and rotor diameters expand. Fraunhofer ISE pegs Greece’s onshore LCOE range at 4.3–9.2 EUR cents/kWh in 2024, down from previous estimates, and projects a further fall to 3.7–7.9 EUR cents/kWh by 2045.(3)Fraunhofer ISE, “Global Levelized Cost of Electricity Update 2025,” ise.fraunhofer.deDevelopers like TERNA Energy are front-loading larger machines in rugged sites such as Karystos, unlocking higher capacity factors while reducing pad counts and civil works outlays. The economics are even more compelling on islands, where fewer units mean fewer crane mobilizations and shorter construction windows between high-wind seasons.

EU Recovery & Resilience Facility Funding Inflow

Greece is channeling EUR 30.5 billion of RRF capital toward climate objectives, with grid interconnections and storage projects at the top of the list. The European Investment Bank’s EUR 5 billion line earmarks loans for private renewable investments exceeding EUR 20 million, blending low-cost finance with stringent green taxonomy criteria.(4)European Investment Bank, “InvestEU Energy Window,” eib.org Projects such as the Cyclades link and Amfilochia pumped hydro reduce curtailment and augment reserve margins, directly complementing new wind farms. By leveraging RRF grants for up to 50% of eligible costs, developers derisk construction budgets and retain skin in the game through the mandatory 30% private share.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy multi-agency permitting timelines | -1.4% | Forest-adjacent zones and archaeological buffer areas | Medium term (2-4 years) |

| Grid congestion and curtailment on islands | -0.9% | Crete, Rhodes, Lesbos, Cyclades | Short term (≤ 2 years) |

| Higher interest rates | -0.7% | Merchant projects that lack long-term PPAs | Short term (≤ 2 years) |

| Scarce heavy-lift vessels for offshore work | -0.5% | Aegean and Ionian Sea zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy Multi-Agency Permitting Timelines

Typical lead times exceed 3–5 years because approvals must be obtained from multiple ministries, environmental bodies, archaeological services, and the military. Digital one-stop shops, introduced in 2024, promise relief; however, field reports reveal an uneven rollout across prefectures. Projects in Natura 2000 zones are subject to heightened scrutiny: Skyros’ 300 MW plan has stalled due to concerns about bird habitats. For offshore arrays, marine spatial planning, fishing fleet negotiations, and defense radar assessments add extra complexity, prompting developers to front-load site screening and allocate larger contingency budgets.

Grid Congestion & Curtailment on Aegean Islands

Island grids face structural curtailment once wind penetration crosses 30% of demand, trimming plant revenues and blunting Greece's wind energy market growth. The EUR 1 billion Crete-Attica submarine cable, energized in 2025, and the multi-phase Cyclades links are critical milestones allowing surplus island output to flow into the mainland backbone. IPTO's EUR 6 billion 2034 plan and the national 4 GW battery goal provide medium-term relief, yet developers still model conservative revenue projections for assets coming online before 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Offshore Emerges Despite Onshore Dominance

Onshore wind capacity reached 5.70 GW in 2025, accounting for a 100% share of Greece's wind energy market. Long-established permitting routines, lower capital intensity, and well-trodden supply chains continue to make onshore sites attractive, particularly across mainland ridgelines and Northern Greece. Robust auction volumes in 2023-2024 signaled policy continuity and secured grid queue positions for at least 1.2 GW of fresh onshore projects by 2027. IPTO's substation upgrades in Thrace and Macedonia reduce lead times for connection agreements, enabling developers to capitalize on high-wind corridors without incurring excessive curtailment risk.

Offshore wind has no commissioned capacity, yet it is projected to outgrow onshore installations. Greece's wind energy market size for offshore projects is expected to breach 1 GW by 2029 as floating technology overcomes depth constraints. RF Energy's EUR 2 billion Limnos plan and Kopelouzos Group's Thracian Sea array headline the first wave of licensed projects. Regulatory clarity was introduced with the 2024 offshore law, which designates Aegean zones and outlines procedures for leasing, environmental management, and interconnection. Although heavy-lift vessel bottlenecks linger, the country's shipbuilding heritage offers a domestic content angle that could trim logistics costs over the long term.

By Turbine Capacity Range: Technology Shift Toward Higher-Capacity Units

The 3 to 5 MW class owned 47% of the installed turbines in 2024, becoming the workhorse of recent auction rounds because it strikes a balance between tower height, logistics, and cost per megawatt. Developers appreciate its bankability track record as turbines from Vestas, Siemens Gamesa, and Nordex operate across high-turbulence ridges without major gear failure incidents. Balance-of-plant providers maintain efficient spare parts warehousing because component standardization simplifies inventory management and reduces costs.

The above 5 MW tier is scaling fastest at a 15.8% CAGR through 2030, supported by Greece's rugged topography, which rewards higher hub heights and longer blades. Greece's wind energy market share for this category is on track to surpass 35% of new annual additions by 2028 because larger rotors push capacity factors above 42% in the best Aegean and Northern Greek sites. Greece's wind energy market size tied to machines above 5 MW could exceed 2.5 GW by 2030 if auction schedules stay on course. While turbines with capacities below 3 MW persist in island retrofits and land-constrained municipal parks, OEM roadmaps indicate that sub-3 MW platforms will be phased out after 2027.

By Application: Utility-Scale Dominance Reflects Grid Integration Focus

Utility-scale wind parks controlled 94% of the installed capacity in 2024, reinforcing a centralized build-out strategy that aligns with the NECP's export ambitions. Auction frameworks reward economies of scale, and IPTO prefers large feeders that help balance the synchronous system by reducing the number of metering points. Developers bundle wind, solar, and storage blocks into single gigawatt-scale tenders, accelerating grid code compliance and concentrating investment in strategic corridors, such as West Macedonia.

Commercial and industrial (C&I) demand for behind-the-meter wind rose from a negligible baseline to a projected 12.5% CAGR through 2030. Corporates leverage enhanced net-metering rules and virtual power purchase agreements to hedge power volatility and bolster their ESG narratives. Greece's wind energy industry is now courting port authorities and logistics clusters that can host mid-sized turbines near load centers, mitigating wheeling charges. Community energy schemes on islands like Tinos remain nascent, but they are receiving policy attention as grid interconnections reduce diesel reliance and enhance local acceptance of renewables.

Geography Analysis

Northern Greece, spanning Macedonia and Thrace, contributes most of the operating capacity and enjoys streamlined access to cross-border high-voltage links into the Balkans. Average hub-height wind speeds exceed 7 m/s, and brownfield substation availability reduces network-reinforcement chargIPTO'sTO’s 400 kV corridor between Nea Santa and Filippi raised transfer capacity in 2024, unlocking headroom for an extra 600 MW of new wind. This region also hosts industrial off-takers pursuing green-power purchase agreements, further diversifying revenue structures.

The Aegean islands boast superior wind resources, but they have historically suffered from grid isolation, which has triggered curtailment when variable generation pushes frequency stability limits. The 2025 activation of the 1 GW Crete-Attica cable reduced local diesel generator runtimes by 70%, freeing up carbon budgets and increasing appetite for new wind tenders. Cyclades Phase IV will link Naxos, Santorini, and Milos by 2026, reducing curtailment risk across smaller island clusters. Greece's wind energy market now counts these interconnections as key enablers that unlock latent island capacity for export to mainland demand centers.

Central Greece has emerged as a logistics and service hub, leveraging proximity to the port of Piraeus and the new high-speed highway network. OEMs stage nacelles and blades here before final lift to mountain sites, compressing transport windows to under three days. Central Greek authorities fast-tracked environmental clearances for 480 MW of onshore wind in 2024, signaling local political buy-in as communities benefit from municipal lease payments. Prospective offshore developers also gravitate toward Central Greece because fabrication yards can host floating substructures before towing them out to Aegean mooring fields.

Competitive Landscape

Domestic champion TERNA Energy dominated the market until its EUR 3.2 billion buyout by Masdar and GEK TERNA in mid-2024, creating a vertically integrated vehicle with finance, construction, and operations under one roof. Foreign utilities EDF-Renouvelables and Iberdrola Renewables maintain sizable pipelines but have slowed auction participation, preferring to partner with local firms to navigate permitting. Nordex and Vestas continue to share the blade-supply duopoly status; Nordex confirmed 359 MW of Greek orders in 2025 alone, reflecting its competitive pricing for high-turbulence sites.

Corporate buyers are reshaping demand patterns. Amazon's 2024 commitment to three Greek wind farms exemplifies the technology sector's entry, while Google and Meta reportedly screen similar PPAs to decarbonize their regional data center footprints. Shipping conglomerates like Angelicoussis explore floating offshore wind to fuel future green-hydrogen bunkering, presenting novel offtake structures that appeal to bank syndicates wary of wholesale-price risk.

Strategic alliances center on hybridization. Mytilineos is packaging wind with solar and 100 MWh battery clusters to maximize merchant exposure during peak spread windows. Once a thermal incumbent, Public Power Corporation (PPC) has pivoted into renewables by tendering 550 MW of wind and solar under a joint development arrangement with RWE. Project finance innovation flourishes as Greek banks co-lend with multilateral agencies, leveraging RRF guarantees that compress senior-loan margins despite the European Central Bank's tighter base rates.

Greece Wind Energy Industry Leaders

Vestas Wind Systems A/S

Iberdrola SA

Siemens Gamesa Renewable Energy, S.A.

General Electric Company

Nordex SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: VALOREM, a French independent green energy operator, inaugurated its first wind farm in Greece in May. The 27 MW wind farm, named "Anatoliko Askio - Magoula", is located on Mount Askio near Kozani in northern Greece.

- January 2025: Nordex has won turbine supply orders totalling 359MW for projects in Spain and Greece. In Greece, PPC Renewables placed an order for 19 of Nordex's N149/5.X turbines for three projects with a combined capacity of 100MW. Nordex will also carry out service and maintenance on the turbines for over 20 years.

- January 2025: Nordex announced 359 MW of wind turbine orders in Greece and Spain, demonstrating sustained demand for advanced wind technologies in Southern European markets.

- November 2024: Amazon is investing in three new wind farms in Greece, marking its first utility-scale wind energy projects in the country. The company has signed power purchase agreements (PPAs) with Aer Soléir for these projects, which include Vermio North, Vermio South, and the Mesokorfi and Koukouras projects.

Greece Wind Energy Market Report Scope

The Greek wind energy market report includes:

By Location

| Onshore |

| Offshore |

By Turbine Capacity

| Up to 3 MW |

| 3 to 6 MW |

| Above 6 MW |

By Application

| Utility-scale |

| Commercial and Industrial |

| Community Projects |

By Component (Qualitative Analysis)

| Nacelle/Turbine |

| Blade |

| Tower |

| Generator and Gearbox |

| Balance-of-System |

| By Location | Onshore |

| Offshore | |

| By Turbine Capacity | Up to 3 MW |

| 3 to 6 MW | |

| Above 6 MW | |

| By Application | Utility-scale |

| Commercial and Industrial | |

| Community Projects | |

| By Component (Qualitative Analysis) | Nacelle/Turbine |

| Blade | |

| Tower | |

| Generator and Gearbox | |

| Balance-of-System |

Key Questions Answered in the Report

What is the projected installed capacity for Greek wind power by 2030?

The Greece wind energy market is forecast to reach 8.75 GW of installed capacity by 2030.

How fast is the offshore segment expected to grow?

Offshore wind capacity is projected to expand at an 18.6% CAGR between 2025 and 2030, the fastest growth among all location categories.

Why are turbines above 6 MW becoming popular in Greece?

Larger units deliver higher capacity factors and lower LCOE, helping developers maximize limited grid connection slots.

Which policy mechanism underpins revenue stability for new wind projects?

Technology-specific feed-in-premium auctions under the NECP link premiums to wholesale prices, cushioning revenue volatility.

What finance instruments support island decarbonization projects?

The Islands Decarbonisation Fund blends grants and low-interest loans to encourage hybrid wind-battery schemes on non-interconnected islands.

Which companies lead the offshore hydrogen strategy?

Terna Energy and Hellenic Petroleum Renewables plan more than 5 GW of offshore wind tied to electrolyzers for green maritime fuels.

Page last updated on: