Graphics Processing Unit (GPU) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

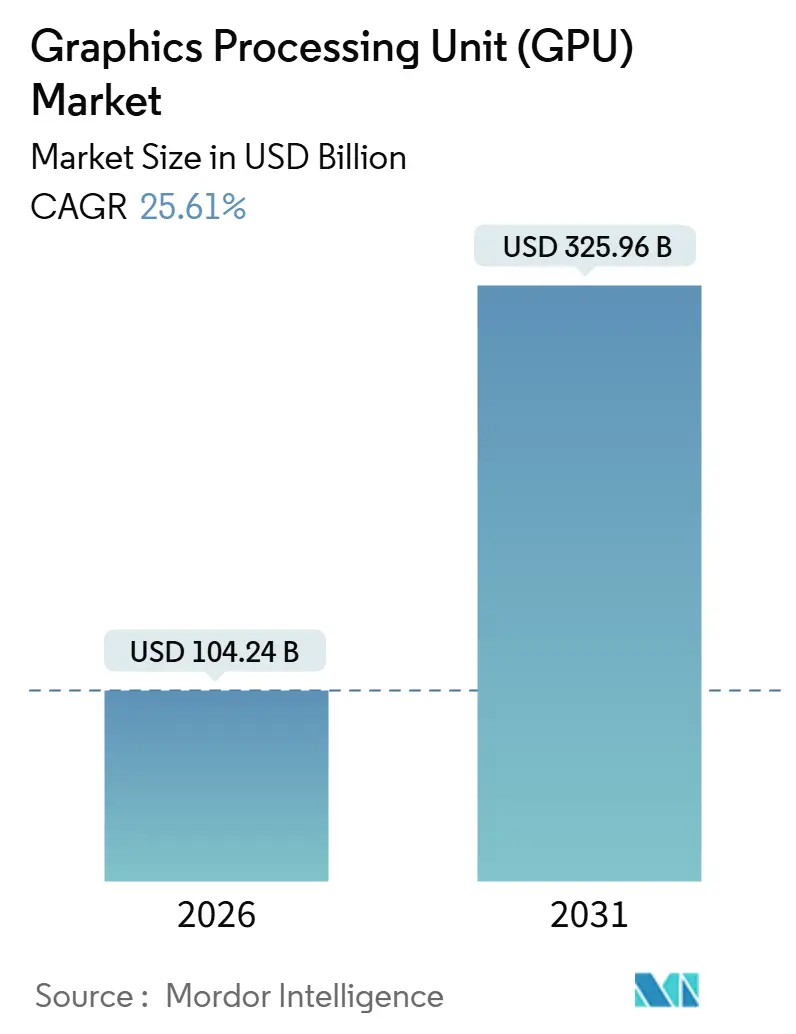

| Market Size (2026) | USD 104.24 Billion |

| Market Size (2031) | USD 325.96 Billion |

| Growth Rate (2026 - 2031) | 25.61% CAGR |

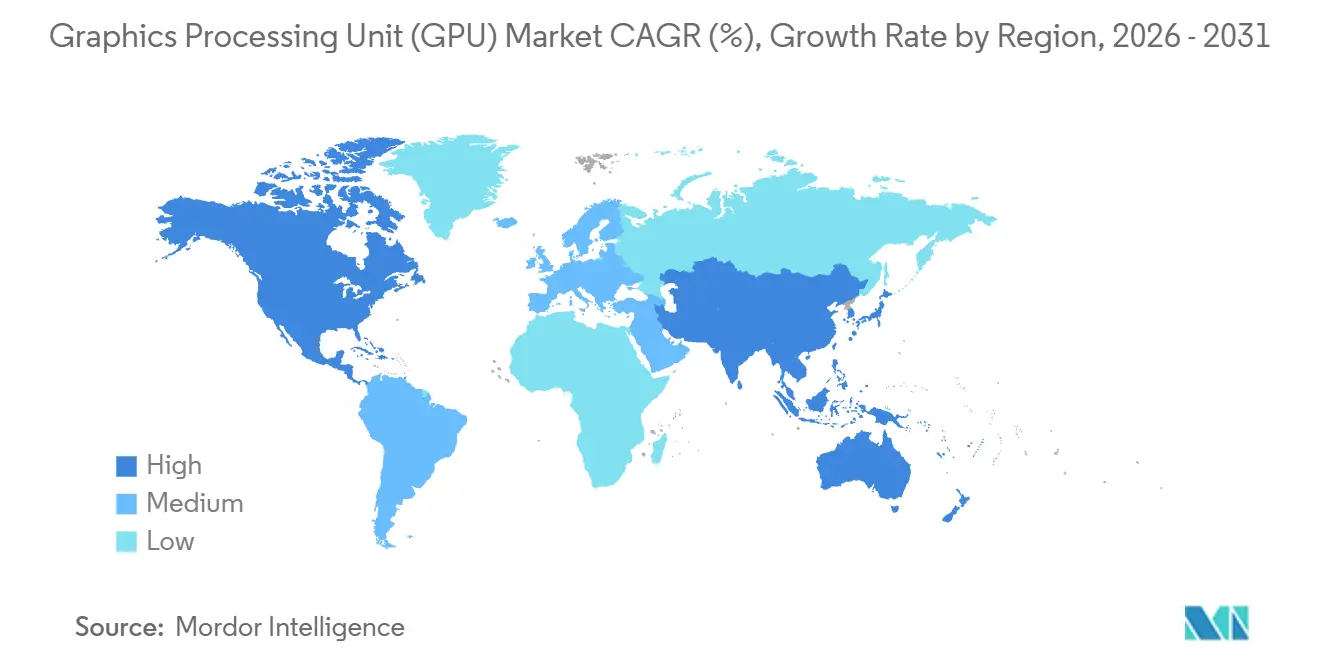

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

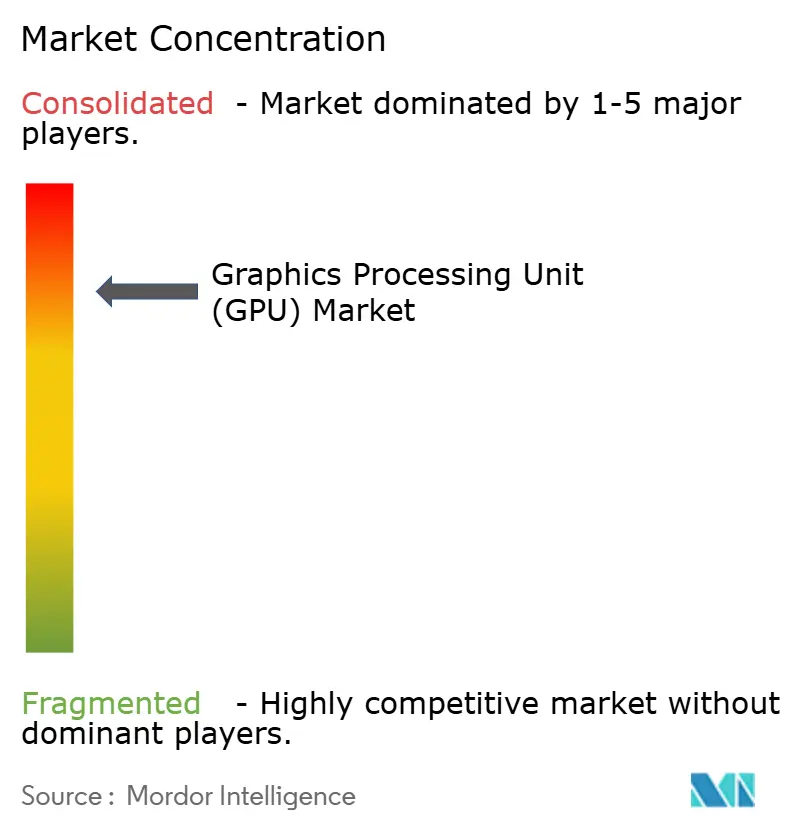

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Graphics Processing Unit (GPU) Market Analysis by Mordor Intelligence

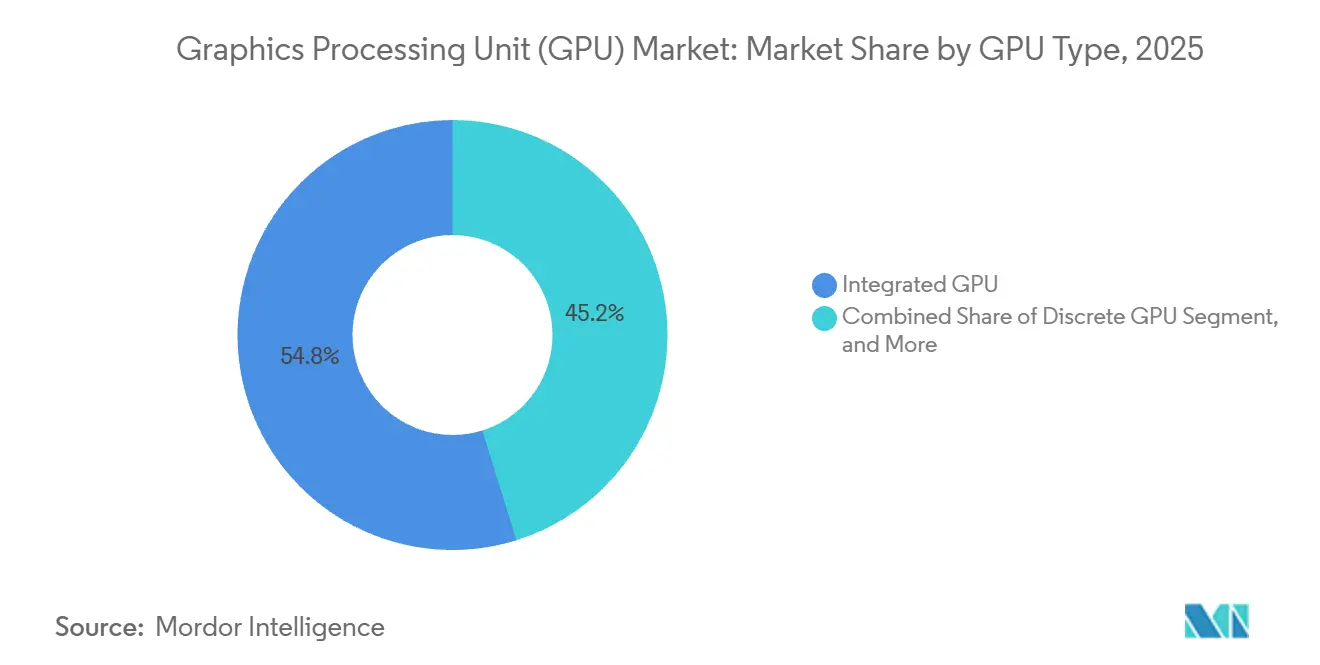

The GPU market size is USD 104.24 billion in 2026 and is projected to reach USD 325.96 billion by 2031, translating to a 25.61% CAGR. Growth drivers include surging generative-AI training intensity, a pivot toward heterogeneous compute architectures, and sustained datacenter build-outs that blend CPU and GPU resources. NVIDIA shipped more than 3 million H100 and H200 datacenter GPUs in 2025, enabling hyperscalers to order in excess of USD 150 billion of accelerator infrastructure as they scaled large-language-model deployments. Integrated GPUs retained 54.81% share in 2025 thanks to smartphone and tablet volumes, yet discrete accelerators are expanding at a 26.41% CAGR through 2031 as enterprises favor dedicated GPUs for inference and training tasks. Chiplet designs, liquid cooling adoption, and sovereign-AI initiatives are reshaping competitive strategies and reinforcing pricing power for vendors that hold long-term foundry allocations.

Key Report Takeaways

- By GPU type, integrated GPUs held 54.81% of GPU market share in 2025, while discrete GPUs are advancing at a 26.41% CAGR through 2031.

- By device application, mobile devices and tablets led with a 38.24% revenue share in 2025; servers and data center accelerators are forecast to expand at a 27.78% CAGR through 2031.

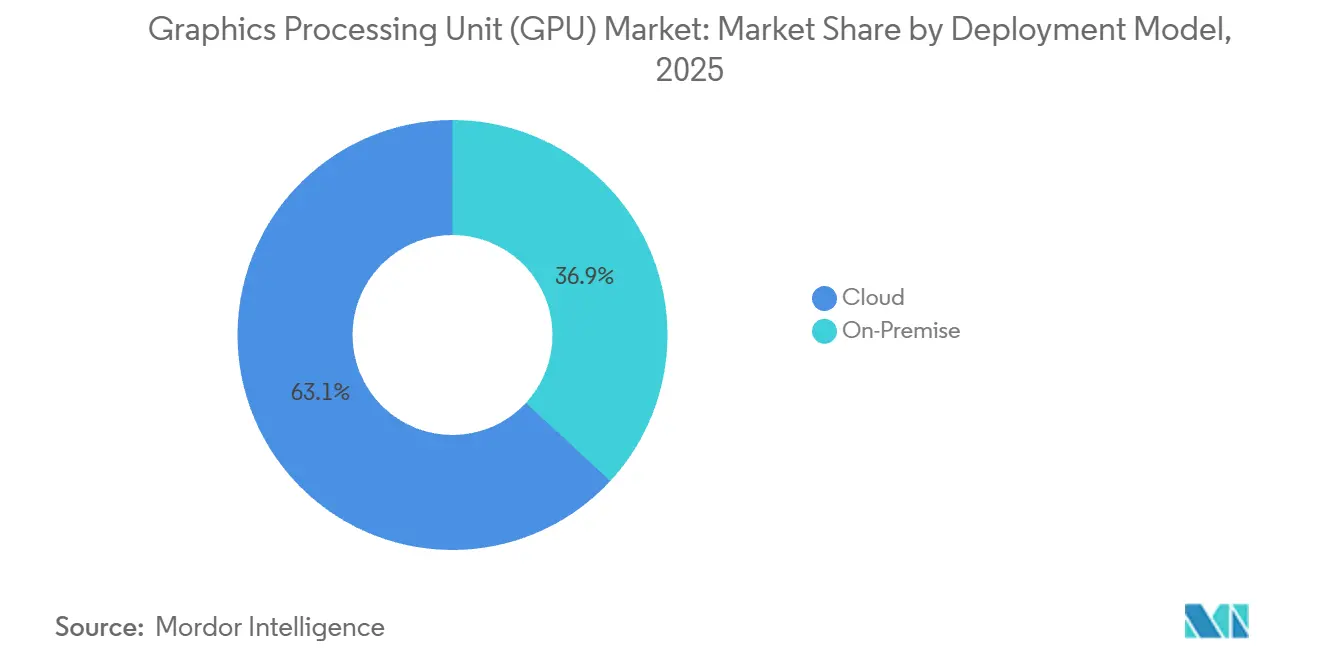

- By deployment model, the cloud segment accounted for 63.12% of the GPU market share in 2025 and is projected to grow at a 26.12% CAGR through 2031.

- By instruction-set architecture, Arm-based designs captured 46.37% of the GPU market share in 2025 and are projected to rise at a 26.15% CAGR through 2031.

- By geography, the Asia-Pacific region is advancing at a 37.4% CAGR, outpacing North America, which held 43.7% of the market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Graphics Processing Unit (GPU) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolving Graphics Realism in AAA Gaming | +3.2% | North America, Europe, East Asia | Medium term (2-4 years) |

| AR/VR and AI-Led Heterogeneous Computing Demand | +4.1% | North America, Asia Pacific | Medium term (2-4 years) |

| Cloud-Gaming Service Roll-outs | +2.8% | North America, Western Europe | Short term (≤2 years) |

| Generative-AI Model-Training GPU Intensity | +6.5% | Global hyperscalers | Long term (≥4 years) |

| Sovereign-AI Datacenter Build-outs | +4.9% | Middle East, Asia Pacific, Europe | Long term (≥4 years) |

| Chiplet-Based Custom GPU SKUs | +3.6% | North America, Taiwan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Evolving Graphics Realism in AAA Gaming

Ray-tracing, neural rendering, and path-tracing have lifted compute requirements for blockbuster titles. Cyberpunk 2077 Phantom Liberty and Alan Wake 2 now recommend discrete GPUs with at least 12 GB VRAM to sustain native 4K at 60 fps. NVIDIA’s RTX 5090, released in January 2025, integrates 24,576 CUDA cores and 24 GB GDDR7 memory for 120 teraflops of shader throughput.[1]NVIDIA Corp., “RTX 5090 Launch,” NVIDIA Newsroom, nvidianews.nvidia.com AMD’s RDNA 4 architecture, shipping in mid-2025, doubles floating-point throughput per clock and narrows the rasterization gap with NVIDIA. Console refresh cycles add momentum, as Sony’s PlayStation 5 Pro deploys a custom RDNA 3 GPU that sets new cross-platform baselines. Unreal Engine 5 features such as Nanite and Lumen further compress the lifespan of mid-range cards, accelerating replacement demand in the GPU market.

AR/VR and AI-Led Heterogeneous Computing Demand

Mixed-reality headsets combine CPU logic with dedicated GPU cores to maintain sub-12 ms motion-to-photon latency. Apple’s Vision Pro pairs an M2 chip with an R1 coprocessor to process 12 camera feeds and 5 LiDAR streams. Meta’s Quest 3 uses Snapdragon XR2 Gen 2 silicon to deliver 4K-per-eye rendering and has sold more than 15 million units through 2025. Enterprises extend these capabilities to surgical training and industrial maintenance, with Siemens deploying 10,000 VR workstations powered by NVIDIA RTX A6000 GPUs to reduce factory-layout prototyping costs by 30%. Cross-vendor frameworks such as oneAPI and ROCm simplify development, though API fragmentation still locks many creators into single-vendor ecosystems.

Generative-AI Model-Training GPU Intensity

Training models exceeding 100 billion parameters requires petaflop-scale clusters with multi-terabyte-per-second memory bandwidth. Meta’s 405-billion-parameter Llama 3.1 run trained on 16,384 H100 GPUs for 54 days. NVIDIA’s H200, shipping in late 2025, delivers 4.8 TB/s bandwidth and 141 GB HBM3e memory, cutting training time by 40% relative to H100. Hyperscalers also develop custom silicon, yet NVIDIA retains dominance in the GPU market because CUDA tools and FP8 precision remain unmatched. Efficiency gains from quantization and mixture-of-experts architectures are offset by multimodal model proliferation, sustaining demand for high-memory GPUs through 2031.

Sovereign-AI Datacenter Build-outs

Governments are pursuing domestic AI clusters to localize data and reduce their dependency on foreign clouds. Saudi Arabia allocated USD 40 billion in 2024 to build a 200,000-GPU complex supporting Arabic language models in the NEOM project. The UAE expanded its Falcon LLM program to 4,096 H100 GPUs in 2025. India, Japan, and others are launching similar initiatives that fragment global supply chains and accelerate domestic packaging capabilities.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capex and BOM Costs | -2.9% | Global | Short term (≤2 years) |

| Chronic Advanced-Node Supply Constraints | -3.4% | North America, Europe | Medium term (2-4 years) |

| Export-Control Limits on ≤7 nm GPU Sales | -2.1% | China, Russia | Long term (≥4 years) |

| Cooling and Power-Density Limits in Hyperscale Datacenters | -1.8% | Global hyperscale zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex and BOM Costs

Flagship datacenter GPUs exceed USD 3,000 bill-of-materials because HBM3 prices remain high and CoWoS interposer yields stay tight. Consumer cards feel similar inflation, NVIDIA’s RTX 5080 launched at USD 1,199 in January 2025, 20% above its predecessor. Many small enterprises postpone accelerator purchases or rent cloud GPUs, yet an 8-H100 cloud node still costs roughly USD 30,000 per month, making the economics unfavorable for long, continuous training runs.

Chronic Advanced-Node Supply Constraints

TSMC’s 3 nm and 5 nm fabs operated above 95% utilization in 2025, with Apple, NVIDIA, AMD, and Qualcomm signing multi-year allocations. Delivery times stretched to 12 months, forcing AIB partners to ration the issuance of discrete cards. Intel’s USD 43.5 billion fab build-out in Arizona and Ohio will not meaningfully ease the tightness until 2027, as Intel's 18A yields lag expectations.

Segment Analysis

By GPU Type: Discrete Accelerators Outpace Integrated Cores

Integrated GPUs commanded 54.81% of GPU market share in 2025, reflecting their inclusion in virtually every smartphone and entry-level laptop. Qualcomm’s Snapdragon 8 Gen 3 shipped in over 200 million devices, and Apple’s M4 chip improved performance-per-watt by 25% over M3.[2]Apple Inc., “M4 Chip Launch,” Apple Newsroom, apple.com Despite this dominance, discrete accelerators such as NVIDIA’s H200 and AMD’s MI300X are growing at a 26.41% CAGR, lifting the discrete slice of the GPU market size for datacenter workloads. NVIDIA’s discrete datacenter GPU revenue hit USD 47.5 billion in fiscal 2025.

Integrated designs minimize board cost and power draw, making them ideal for thin-and-light form factors. Intel’s Meteor Lake integrates Xe graphics for AV1 encoding, and Arm’s Immortalis-G720 brings variable-rate shading to mobile chips. Discrete GPUs dominate workloads that need sustained parallel throughput, including 8K video editing and AI model training, ensuring both segments grow in tandem within the broader GPU market.

Note: Segment shares of all individual segments available upon report purchase

By Device Application: Datacenters Eclipse Consumer Segments

Mobile devices and tablets held a 38.24% share of the GPU market in 2025 as smartphone shipments topped 1.2 billion. Qualcomm’s Snapdragon X Elite boosted Windows-on-Arm laptops, and Samsung’s Galaxy S25 featured RDNA-based graphics. Servers and data center accelerators, however, are the fastest-growing segment, expanding at a 27.78% CAGR as hyperscalers deployed more than 4 million GPUs in 2025.

PCs and workstations benefit from AI PC initiatives that integrate NPUs, while gaming consoles maintain a modest share, pending the release of Nintendo’s next-generation Switch. Automotive use cases grow quickly as autonomous platforms, such as NVIDIA Drive Thor, integrate 2,000 TOPS of GPU compute. Edge devices, such as smart cameras, adopt low-power GPUs, broadening the addressable demand across the GPU market.

By Deployment Model: Cloud Dominance Reflects Capex Aversion

Cloud deployments captured 63.12% of the GPU market share in 2025 and are projected to rise at a 26.12% CAGR as organizations increasingly prefer pay-as-you-go models. AWS P5e instances featuring H200 GPUs cost USD 98.32 per hour and underpin large-scale training jobs. Google Cloud, Microsoft Azure, and Oracle Cloud follow suit with H100- and MI300X-based offerings that cut start-up times for AI projects.

On-premise clusters remain vital where data residency or long training cycles result in a lower lifetime cost than cloud rental. JPMorgan installed a 1,024-GPU cluster to avoid egress fees. Hybrid orchestration enables firms to burst to the cloud during peaks, striking a balance between flexibility and budget within the GPU market.

By Instruction-Set Architecture: Arm Gains Ground in Power-Constrained Segments

Arm-based GPUs controlled 46.37% of the GPU market share in 2025 and are forecast to expand at a 26.15% CAGR through 2031. Smartphone dominance and Apple’s Mac transition fuel volume, while AWS Graviton4 servers pair Arm CPUs with discrete GPUs for inference tasks.

x86-64 CPUs still anchor training clusters given CUDA lock-in and AVX-512 support. AMD’s MI300A combines Zen 4 CPU cores with CDNA 3 GPUs on a single package, serving exascale systems. RISC-V remains a niche technology but is growing in academia, where open instruction sets enable customization.

Geography Analysis

Asia Pacific led the GPU market with 44.71% revenue share in 2025, supported by China’s 700 million smartphone output and Taiwan’s foundry dominance. TSMC fabricated more than 80% of advanced-node GPU dies, supplying NVIDIA, AMD, Apple, and Qualcomm. Japan’s automotive tier-1 suppliers have integrated Drive Orin and Snapdragon Ride chips into over 2 million vehicles, thereby enhancing ADAS penetration.

The Middle East is experiencing the fastest expansion, with a 27.61% CAGR, as Saudi Arabia, the UAE, and Qatar fund sovereign AI clusters. Saudi Arabia alone ordered 200,000 H200 GPUs for a 1.5 GW data center in NEOM. The UAE’s Technology Innovation Institute scaled its Falcon infrastructure to 4,096 H100 GPUs in 2025.

North America, with a mid-30s share, remains the innovation hub. Microsoft, Google, Meta, and Amazon spent over USD 100 billion on GPU infrastructure in 2025. Europe accelerates sovereign AI moves as France’s Mistral AI deploys 2,048 GPUs and Germany’s Aleph Alpha leverages A100 clusters for enterprise inference. South America and Africa remain nascent, though research institutes in Brazil and South Africa have started to add H100 and MI250X nodes, signaling early adoption trends in the global GPU market.

Competitive Landscape

NVIDIA controls 88% of datacenter accelerators and 82% of discrete gaming GPUs, maintaining the highest software lock-in through CUDA. AMD holds 10% datacenter share and undercuts NVIDIA on cost-per-FLOP with MI300X, winning Microsoft Azure and Meta workloads.[3]Advanced Micro Devices Inc., “AMD Investor Relations,” ir.amd.com Intel Gaudi 3 emphasizes inference efficiency, shipping 50,000 units to cloud providers and expanding choice for developers.

Strategic focus centers on chiplet modularity and vertical integration. NVIDIA’s Mellanox acquisition enables sub-5-microsecond intra-GPU latency, while AMD’s chiplet approach tailors memory-to-compute ratios. White-space entrants, such as Qualcomm, Graphcore, and Cerebras, address edge inference and wafer-scale AI, yet together hold under 2% share due to ecosystem limitations.

Regulation shapes roadmaps as the EU AI Act and ISO/IEC 23053 mandate transparency. Vendors integrate hardware attestation engines and secure boot to satisfy compliance, reinforcing barriers to entry in a GPU market that already favors scale, software depth, and access to foundries.

Graphics Processing Unit (GPU) Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Apple Inc.

Samsung Electronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: NVIDIA and Foxconn announced a partnership to co-develop AI factories that combine Blackwell GPUs with liquid-cooling racks.

- November 2025: AMD acquired Finland-based Silo AI for EUR 665 million to strengthen its European software ecosystem.

- October 2025: Intel launched Gaudi 3 into volume production, shipping 50,000 units to multiple clouds.

- September 2025: Qualcomm committed USD 1.2 billion to expand its Bangalore GPU design center.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the graphics processing unit (GPU) market as the worldwide revenue generated from the sale of discrete, integrated, and hybrid electronic circuits engineered to accelerate parallel-processing workloads across consumer devices, data-center servers, automotive ADAS, and edge systems.

Each unit must be a new, factory-shipped GPU that is either soldered on board or packed as an add-in card; refurbished boards, ASIC miners, and FPGA accelerators fall outside this definition. Scope exclusion: refurbished cards, pure AI application-specific ASICs, and FPGA-based accelerators are not covered.

Segmentation Overview

- By GPU Type

- Discrete GPU

- Integrated GPU

- Other GPU Types

- By Device Application

- Mobile Devices and Tablets

- PCs and Workstations

- Servers and Datacenter Accelerators

- Gaming Consoles and Handhelds

- Automotive / ADAS

- Other Embedded and Edge Devices

- By Deployment Model

- On-Premise

- Cloud

- By Instruction-Set Architecture

- x86-64

- Arm

- RISC-V and OpenGPU

- Other Instruction-Set Architectures (Power, MIPS)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview GPU designers, board manufacturers, cloud-infrastructure architects, gaming-OEM product managers, and regional distribution heads across North America, Asia-Pacific, and Europe. Their inputs on yield rates, channel inventory, cloud attach rates, and forward ASP roadmaps allow Mordor analysts to challenge desk assumptions and refine elasticity parameters before finalizing the model.

Desk Research

Our analysts begin with public datasets that map the supply chain, such as United States International Trade Commission HS-code exports, Eurostat COMEXT import flows, and China Customs electronics shipment files, which together reveal shipment volumes by device class. Semiconductor Industry Association wafer-capacity briefs, OECD ICT hardware price indices, and World Bank broadband penetration tables help us frame demand and pricing arcs. Company 10-Ks, investor decks, and earnings calls supplement these macro views, while D&B Hoovers and Dow Jones Factiva feed us firm-level revenue splits that sharpen estimated ASPs. This constellation of open and paid sources gives us the first pass at a balanced volume-value grid.

Patent landscapes from Questel, production statistics from IMTMA for board assembly lines, and traffic logs from open data-center registries further validate production ceilings and identify upcoming supply bottlenecks. Numerous additional secondary sources are reviewed; the titles above illustrate but do not exhaust our reference pool.

Market-Sizing & Forecasting

A top-down device-shipment reconstruction starts with shipments of PCs, servers, handsets, consoles, and vehicles, then applies segment-specific GPU attach ratios and average selling prices. Supplier roll-ups, selective channel checks, and sampled ASP × volume pairs act as bottom-up reasonableness tests. Key variables include gaming-PC replacement cycles, hyperscale server GPU density, memory-cost trajectories, cryptocurrency profitability indices, and regional disposable-income growth. Forecasts are generated through multivariate regression blended with scenario analysis, capturing volatility in AI server build-outs and consumer graphics demand. Data gaps, common in gray-channel console boards, are bridged by three-point estimates agreed upon during expert calls.

Data Validation & Update Cycle

Outputs pass anomaly scans, cross-metric variance checks, and a two-step peer review before sign-off. Reports refresh each year; interim re-checks trigger when material events (fab outages, new architecture launches, or steep tariff shifts) hit the market. A final analyst sweep is completed just prior to client delivery, ensuring clients receive an up-to-date baseline.

Why Mordor's Gpu Baseline Earns Trust

Published estimates often diverge because firms choose different device baskets, ASP assumptions, and forecast cadences.

Key gap drivers include whether mobile GPUs are booked at silicon or finished-device value, how aggressively AI-server demand ramps are modeled, and the currency conversion points used. Mordor publishes a unified 2025 base year and refreshes annually, whereas some publishers embed conservative GPU attach ratios or roll their forecasts forward only every two years, creating spread.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 82.68 B (2025) | Mordor Intelligence | - |

| USD 77.39 B (2024) | Global Consultancy A | mobile handset GPUs excluded; two-year currency average used |

| USD 101.54 B (2025) | Industry Publisher B | counts refurbished cards; assumes 45 % AI-server GPU attach by 2025 |

In sum, the disciplined scope selection, yearly refresh rhythm, and dual-path validation steps adopted by Mordor analysts deliver a transparent, repeatable baseline that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What is the current value of the GPU Market?

The GPU market size is USD 104.24 billion in 2026 and is forecast to hit USD 325.96 billion by 2031.

Which segment is growing fastest within the GPU market?

Servers and datacenter accelerators lead growth at a 27.78% CAGR through 2031 as AI model training scales.

Why are discrete GPUs gaining share despite integrated volume?

Enterprise AI workloads require high-memory bandwidth and sustained parallel throughput that only discrete accelerators provide, pushing discrete growth at 26.41% CAGR.

What factors limit GPU supply?

Advanced-node wafer shortages, high HBM3 prices, and U.S. export controls on ≤7 nm devices lengthen lead times and keep prices elevated.

Which geography will contribute the most new demand by 2031?

The Middle East shows the fastest regional CAGR at 27.61% as Saudi Arabia and the UAE deploy sovereign-AI clusters.

How concentrated is the vendor landscape?

NVIDIA, AMD, Intel, Qualcomm, and Arm together hold roughly 80% market share, yielding a high concentration score of 8.