Glycol Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

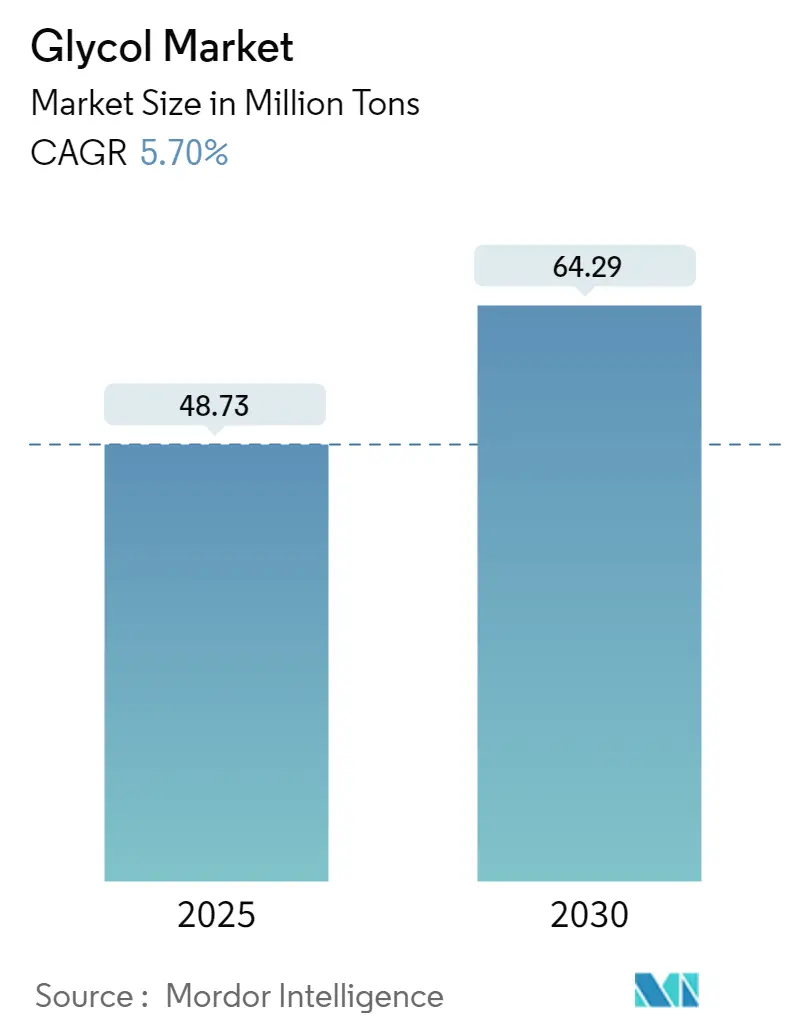

| Market Volume (2025) | 48.73 Million tons |

| Market Volume (2030) | 64.29 Million tons |

| Growth Rate (2025 - 2030) | 5.70% CAGR |

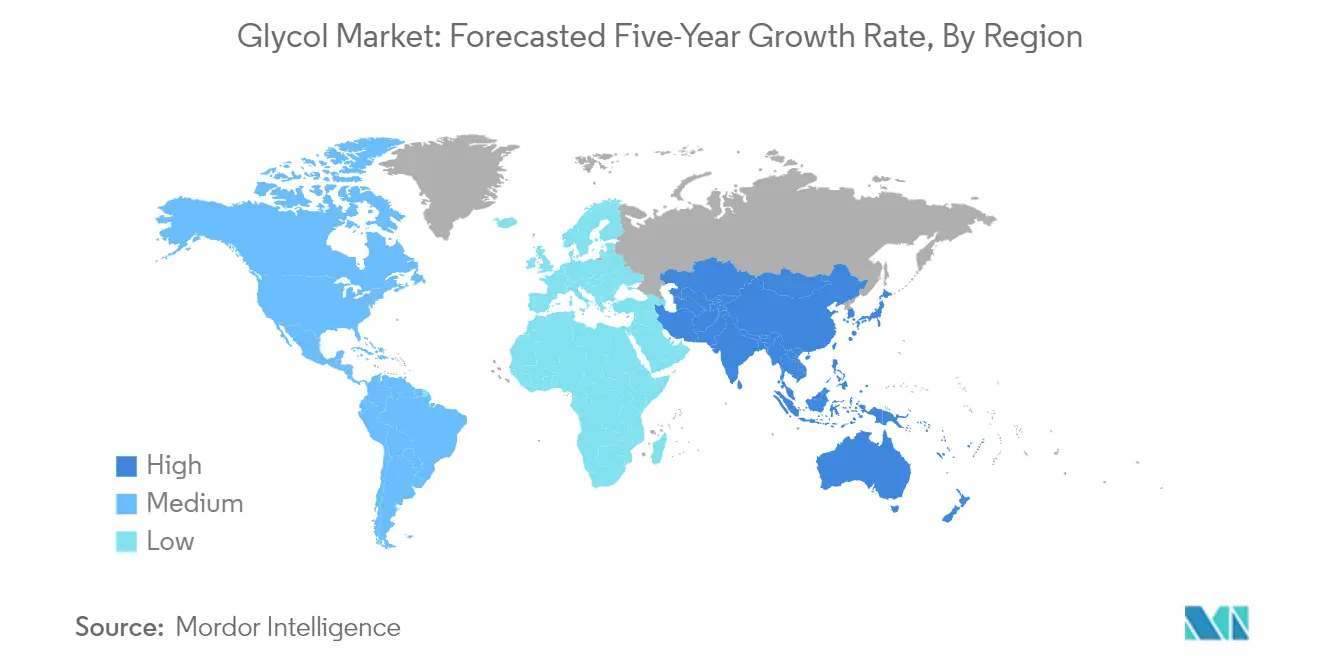

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

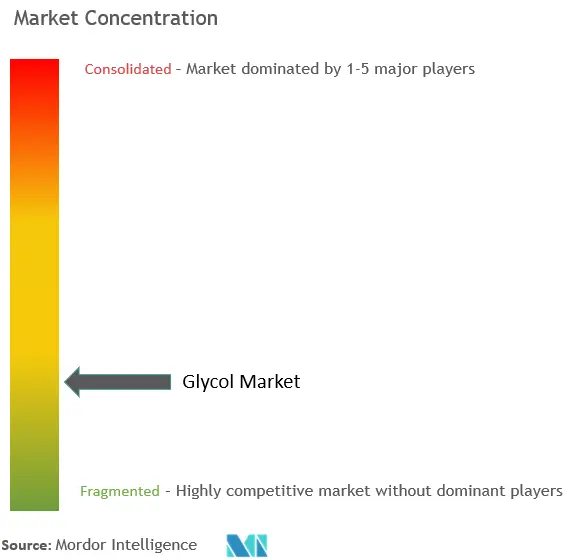

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glycol Market Analysis by Mordor Intelligence

The Glycol Market size is estimated at 48.73 million tons in 2025, and is expected to reach 64.29 million tons by 2030, at a CAGR of 5.7% during the forecast period (2025-2030).

The glycol industry is experiencing significant transformation driven by evolving end-user industries and changing consumer preferences. The automotive sector, particularly the electric vehicle segment, has emerged as a crucial growth catalyst with global EV sales reaching 675 million units in 2021. The increasing adoption of glycol-based products in EV battery thermal management systems and cooling solutions has created new avenues for market expansion. Additionally, the implementation of stringent environmental regulations across major economies has prompted manufacturers to invest in advanced production technologies and sustainable practices, leading to improved operational efficiency and reduced environmental impact.

The packaging industry continues to be a major consumer of glycol products, driven by the rapid expansion of e-commerce and changing consumer preferences. According to industry data, the food segment alone is estimated to reach USD 276.10 billion in 2022, necessitating innovative packaging solutions. The demand for PET packaging, which heavily relies on ethylene glycol as a raw material, has witnessed substantial growth due to its recyclability and versatile applications. Manufacturers are increasingly focusing on developing eco-friendly packaging solutions while maintaining the performance characteristics that glycol-based materials offer.

The textile manufacturing sector has undergone significant modernization with increased automation and technological integration. According to the Brazilian Food Industry Association (ABIA) survey, the food industry registered a growth of 3.2% in sales in 2021, indicating robust downstream demand across various sectors including textiles. The industry has witnessed substantial investments in research and development activities focused on improving production efficiency and developing innovative applications for glycol-based products in textile processing.

The market is witnessing a notable shift towards sustainable and bio-based alternatives, driven by increasing environmental awareness and regulatory pressures. According to L'Oréal, the global cosmetics market, worth nearly USD 240 billion, has been a significant driver of this trend with growing demand for sustainable ingredients. Industry players are investing in research and development of bio-based glycols, exploring alternative feedstocks, and implementing circular economy principles in their production processes. This transition is supported by collaborations between manufacturers, research institutions, and end-users to develop commercially viable sustainable solutions while maintaining product performance standards.

Global Glycol Market Trends and Insights

INCREASING DEMAND FOR POLYESTER FILMS AND PU ADHESIVES

The growing demand for polyester films and polyurethane (PU) adhesives across various industries is driving significant consumption of glycol products. The ethylene glycol market serves as a critical raw material in manufacturing poly(ethylene terephthalate) or PET, which is produced through the reaction of ethylene glycol with terephthalic acid. These polyester films find extensive applications in packaging foods and beverages, particularly for soft drinks, water, alcoholic drinks, edible oils, and juices. Beyond packaging, polyester films are increasingly utilized in printed electronics, optical displays, flexible electronics, medical films, tags and labels, electrical components, and printing applications, demonstrating the versatility and growing importance of glycol-based products.

The expansion of manufacturing capabilities by major industry players further validates the increasing demand for polyester films. For instance, in October 2021, Mitsubishi Chemical Corporation announced plans to expand its polyester film production capacity at its Wiesbaden, Germany site. Similarly, Dhanuka Group revealed plans to establish an INR 1,250 crore packaging film factory in West Bengal, India, with a total production capacity of 45,000 tons of Biaxially Oriented PET (BOPET). The demand for PU adhesives is particularly strong in the automotive and transportation industry, where these materials are extensively used for improving performance and developing lightweight designs. In 2021, Bostik launched a new line of PU sealants for the construction market, aiming to meet the growing demand for new constructions in developing countries.

INCREASING ETHYLENE GLYCOL CONSUMPTION FROM CHINA'S TEXTILE INDUSTRY

China's textile industry continues to demonstrate robust growth, driving substantial demand for ethylene glycol in the manufacturing of polyester fibers and textiles. According to recent data, China exported textiles, apparel, and clothing accessories worth USD 323.344 billion in 2022, registering a growth of 2.53% compared to the previous year. The export value of yarns and fabrics, which are the main raw materials for clothing, has shown significant growth, highlighting the increasing consumption of ethylene glycol in textile manufacturing processes. The Chinese government's strategic focus on developing Xinjiang as a major textile and apparel manufacturing hub, backed by an investment of USD 8 billion, further indicates the strong growth trajectory of ethylene glycol market demand in the region.

The textile industry's expansion is further supported by the establishment of new manufacturing facilities and increased production capabilities. According to the National Bureau of Statistics of China, the textile production volume in China reached 12.4 billion meters in the first four months of 2022, compared to 11.8 billion meters during the same period in the previous year. Furthermore, China's garment industry's revenue reached CNY 1.3 trillion in the first eleven months of 2021, with a growth of about 7.7% compared to the previous period. The government's plan to establish Xinjiang as the country's largest textile production base by 2030 is expected to significantly boost ethylene glycol consumption, as the region develops into a major manufacturing hub for textile and apparel products. This aligns with the monoethylene glycol market trends and the ethylene glycol price trend, which are influenced by such industrial expansions.

Segment Analysis: By Type

Ethylene Glycol Segment in Global Glycol Market

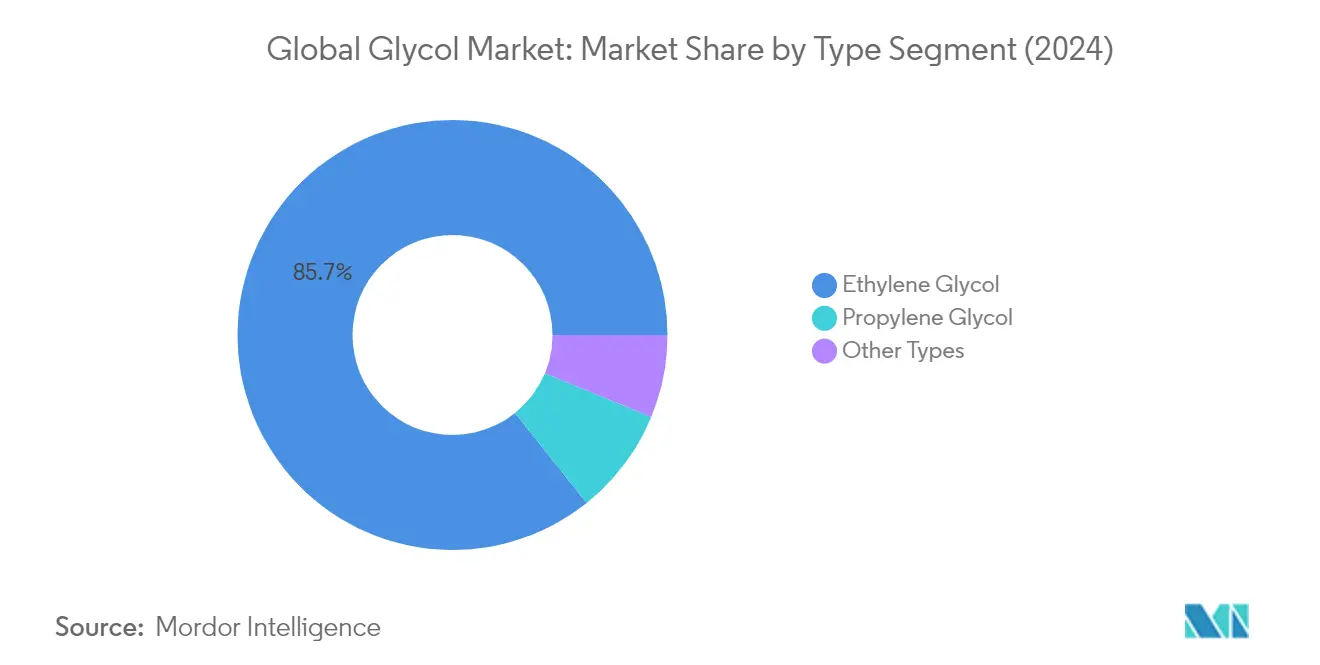

Ethylene Glycol continues to dominate the global glycol market, commanding approximately 86% of the total market share in 2024. This substantial market presence is primarily driven by the segment's extensive application in the production of polyester fibers and PET (polyethylene terephthalate) products. The segment's dominance is particularly evident in the textile industry, where Monoethylene Glycol (MEG) serves as a crucial raw material, with approximately 0.345 kg of MEG required for every 1 kg of polyester produced. The segment's robust performance is further supported by increasing demand from China's textile industry, which has shown significant growth in recent years. Additionally, the rising demand for polyester films and PU adhesives across various industrial applications, including packaging, automotive, and construction sectors, continues to fuel the segment's market leadership.

Propylene Glycol Segment in Global Glycol Market

The Propylene Glycol segment is emerging as the fastest-growing segment in the global glycol market, projected to grow at approximately 8% CAGR from 2024 to 2029. This remarkable growth trajectory is attributed to its increasing adoption in cosmetics, pharmaceuticals, and food and beverage industries, driven by its low toxicity profile compared to ethylene glycol. The segment's expansion is further supported by stringent regulations favoring safer alternatives in consumer products. The versatility of propylene glycol, particularly in applications such as personal care products, pharmaceutical formulations, and food preservatives, continues to drive its market growth. Additionally, the increasing focus on sustainable and bio-based alternatives has led to innovations in propylene glycol production methods, further accelerating its market penetration across various end-use industries.

Remaining Segments in Global Glycol Market by Type

The other types segment in the glycol market encompasses various specialized glycol products, including butylene glycol market and pentylene glycol, which serve specific niche applications across different industries. These glycols play crucial roles in specialized applications such as humectants in the tobacco industry, conditioning agents in personal care products, and as intermediates in the manufacturing of construction materials. The segment's significance is particularly notable in the cosmetics and personal care industry, where these specialized glycols are valued for their unique properties such as moisture-binding capabilities and antimicrobial properties. Their application in high-end cosmetic formulations and specialized industrial processes continues to maintain their relevance in the overall glycol market landscape.

Segment Analysis: End-User Industry

Textile Segment in Global Glycol Market

The textile industry dominates the global glycol market, commanding approximately 65% of the total market share in 2024. This substantial market presence is primarily driven by the extensive use of glycol in the production of polyester fibers, which are essential components in sportswear, carpets, and upholstery manufacturing. The segment's dominance is particularly evident in major textile manufacturing hubs like China and India, where glycol consumption in textile applications continues to grow rapidly. The segment is also experiencing the fastest growth rate in the glycol market, projected to expand at approximately 6% from 2024 to 2029, driven by increasing demand for polyester-based textiles, growing textile exports, and rapid industrialization in emerging economies.

Cosmetics Segment in Global Glycol Market

The cosmetics segment represents the second-largest application area in the glycol market, with significant growth potential driven by increasing consumer awareness and demand for personal care products. The segment's growth is supported by the rising adoption of glycol-based ingredients in skincare products, moisturizers, and other cosmetic formulations. Propylene glycol's role as a humectant and solvent in cosmetic applications continues to expand, particularly in premium and organic cosmetic products. The segment benefits from the growing trend toward natural and organic beauty products, where certain glycols serve as essential ingredients for product stability and effectiveness.

Remaining Segments in End-User Industry

The automotive and transportation, food and beverage, pharmaceuticals, and packaging segments collectively form a significant portion of the glycol market. The automotive sector utilizes glycols primarily in antifreeze and coolant applications, while the food and beverage industry employs them as food additives and in packaging materials. The pharmaceutical sector leverages glycols in drug formulations and as solvents, whereas the packaging industry uses them in the production of PET bottles and containers. Each of these segments contributes uniquely to the market's dynamics, with their demand patterns influenced by regional industrial development, regulatory frameworks, and technological advancements in their respective applications.

Glycol Market Geography Segment Analysis

Glycol Market in Asia-Pacific

The Asia-Pacific region dominates the global glycol market, driven by robust growth in key end-use industries such as textiles, automotive, and packaging. The region's market dynamics are shaped by China's massive manufacturing base, India's growing industrial sector, Japan's technological advancements, and South Korea's expanding chemical industry. The presence of major manufacturers and increasing investments in production capacity further strengthen the region's position. Rising demand from emerging economies and growing adoption of ethylene glycol in various applications continue to fuel market expansion across the region. The Asia-Pacific butyl glycol market is also witnessing significant growth due to these factors.

Glycol Market in China

China leads the Asia-Pacific glycol market, commanding approximately 55% of the regional market share in 2024. The country's dominance is attributed to its massive textile industry, which has become one of the main pillars of the economy. China's position as the largest textile-producing and exporting country globally drives substantial demand for ethylene glycol products. The nation's robust manufacturing infrastructure, government support for industrial development, and strategic initiatives like establishing Xinjiang as a textile manufacturing hub further consolidate its market leadership. The presence of numerous domestic and international manufacturers, coupled with continuous capacity expansions, reinforces China's position as the regional powerhouse.

Glycol Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 6% during 2024-2029. The country's market expansion is driven by rapid industrialization, growing textile exports, and increasing demand from the automotive sector. India's position as the largest provider of generic drugs and its expanding pharmaceutical industry create substantial demand for ethylene glycol products. The government's initiatives like 'Make in India' and 'Aatma Nirbhar Bharat' programs, coupled with 100% FDI allowance in the textile sector, are catalyzing market growth. The country's focus on developing its manufacturing capabilities and increasing investments in key end-use industries positions it as a crucial growth market in the region.

Glycol Market in North America

The North American glycol market demonstrates strong market fundamentals, supported by advanced manufacturing capabilities and technological innovation across the United States, Canada, and Mexico. The region's market is characterized by the presence of major manufacturers, robust research and development activities, and stringent quality standards. The automotive, aerospace, and pharmaceutical industries serve as key demand drivers, while increasing focus on sustainable and bio-based glycols shapes market development. The region's well-established distribution networks and strong integration across the value chain contribute to market stability and growth.

Glycol Market in United States

The United States dominates the North American glycol market, holding approximately 70% of the regional market share in 2024. As the second-largest automotive market globally after China, the country's substantial manufacturing base drives significant ethylene glycol consumption. The nation's leadership in aerospace manufacturing, coupled with its advanced pharmaceutical and personal care sectors, creates diverse demand streams. The presence of major manufacturers and continuous technological advancements in production processes reinforces the country's market position. The strong focus on research and development, along with increasing adoption of sustainable practices, shapes market dynamics.

Glycol Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 4% during 2024-2029. The country's market growth is driven by its expanding aerospace industry, where it ranks first globally in civil flight simulation and third in civil engine production. The strong presence of automotive manufacturing facilities and increasing focus on electric vehicle production contribute to market expansion. Canada's strategic position in the global aerospace industry, with over 70% of its products exported to more than 190 countries, creates sustained demand for ethylene glycol products. The country's commitment to environmental sustainability and technological innovation further supports market development.

Glycol Market in Europe

The European glycol market demonstrates sophisticated market dynamics, supported by advanced manufacturing capabilities across Germany, the United Kingdom, Italy, and France. The region's focus on sustainable production practices and stringent environmental regulations shapes market development. Strong presence in automotive, aerospace, and pharmaceutical industries drives consistent demand, while increasing focus on bio-based alternatives influences market trends. The region's well-developed infrastructure and emphasis on technological innovation contribute to market stability.

Glycol Market in Germany

Germany maintains its position as the largest glycol market in Europe, leveraging its strong industrial base and technological leadership. The country's dominant position in the European automotive market, with 41 assembly and engine production plants, drives substantial ethylene glycol consumption. Germany's leadership in textile exports and imports, coupled with its strong chemical manufacturing sector, creates diverse demand streams. The presence of numerous small and medium-sized businesses in the textile industry, along with continuous technological advancements, reinforces the country's market leadership.

Glycol Market in United Kingdom

The United Kingdom demonstrates the fastest growth trajectory in the European glycol market. The country's position as the second-largest aerospace sector in Europe and third-largest globally drives market expansion. The strong presence of aviation component suppliers and expertise in maintenance, repair, and overhauling operations create sustained demand. The UK's leadership in beauty and personal care products, coupled with its position among the top three cosmetic consumers in Western Europe, further supports market growth. The country's focus on research and development and increasing investments in manufacturing capabilities contribute to market development.

Glycol Market in South America

The South American glycol market demonstrates growing potential, with Brazil and Argentina emerging as key markets in the region. Brazil leads the regional market, benefiting from its position as the largest electric vehicle market in Latin America and strong presence in aircraft manufacturing. Argentina shows promising growth potential, supported by its expanding automotive and pharmaceutical sectors. The region's market development is influenced by increasing industrialization, growing automotive production, and rising demand from the pharmaceutical and personal care sectors. The presence of major manufacturers and continuous investments in production capabilities contribute to market expansion.

Glycol Market in Middle East & Africa

The Middle East & Africa glycol market showcases dynamic growth potential, with Saudi Arabia and South Africa emerging as significant markets. Saudi Arabia leads the regional market, leveraging its strong petrochemical industry and strategic location. South Africa demonstrates promising growth potential, supported by its expanding automotive sector and growing pharmaceutical industry. The region's market development is driven by increasing investments in manufacturing capabilities, growing demand from end-use industries, and rising focus on diversification of economies. The presence of major manufacturers and continuous capacity expansions contribute to market growth.

Competitive Landscape

Top Companies in Glycol Market

The global glycol market features prominent players like Shell PLC, MEGlobal, Indorama Ventures, Reliance Industries, and PETRONAS Chemicals Group leading the industry. These companies are increasingly focusing on sustainable production methods and bio-based alternatives to address growing environmental concerns. Strategic capacity expansions, particularly in Asia-Pacific regions, demonstrate the industry's commitment to meeting rising demand from end-user industries. Companies are strengthening their vertical integration capabilities across the value chain to ensure a stable raw material supply and optimize production costs. Research and development initiatives are centered on improving production efficiency and developing specialized grades for emerging applications. The industry is witnessing a shift towards collaborative approaches through joint ventures and partnerships to enhance market presence and technological capabilities.

Fragmented Market with Strong Regional Players

The monoethylene glycol industry exhibits a fragmented structure with Chinese manufacturers controlling a significant portion of global production capacity. Major petrochemical conglomerates maintain their market positions through extensive distribution networks and backward integration capabilities, while regional specialists focus on serving specific geographic markets or applications. The industry has witnessed notable consolidation through strategic acquisitions and joint ventures, particularly in developing markets, as companies seek to strengthen their market presence and expand their product portfolios.

The competitive dynamics are characterized by a mix of global chemical giants and regional players, each leveraging their respective strengths in technology, distribution, or local market knowledge. Market consolidation trends indicate a strategic shift towards creating integrated manufacturing facilities that can serve multiple end-user industries efficiently. Companies are increasingly focusing on establishing production facilities in proximity to their key markets to reduce logistics costs and improve supply chain efficiency. The industry structure promotes healthy competition while maintaining barriers to entry through capital-intensive requirements and technical expertise needs.

Innovation and Sustainability Drive Future Success

Success in the MEG industry increasingly depends on companies' ability to develop sustainable production processes and eco-friendly products. Incumbent players are strengthening their market positions by investing in advanced manufacturing technologies and expanding their product portfolios to serve emerging applications. The development of bio-based alternatives and circular economy initiatives has become crucial for maintaining a competitive advantage. Companies are also focusing on building strong relationships with end-users through customized solutions and technical support services.

Market participants must navigate challenges including raw material price volatility and evolving environmental regulations while maintaining operational efficiency. New entrants can gain market share in the monoethylene glycol sector by focusing on specialized applications or underserved geographic regions, while established players need to continuously innovate and optimize their operations. The industry's future success factors include the ability to maintain cost competitiveness while meeting stringent quality and environmental standards. Companies that can effectively balance sustainability initiatives with operational efficiency while maintaining strong customer relationships are likely to emerge as market leaders.

Glycol Industry Leaders

Shell PLC

Indorama Ventures Public Company Limited

Reliance Industries Limited

MEGlobal

PETRONAS Chemicals Group Berhad

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Dow commenced an expansion of its propylene glycol (PG) capacity at its integrated manufacturing facility in Map Ta Phut, Rayong, Thailand. This expansion boosts the facility's PG output by 80,000 tons annually, elevating the total production to 250,000 tons annually. This strategic move optimizes Dow's existing asset infrastructure at the Map Ta Phut site. It also solidifies its regional and global leadership position in the industry, enabling the company to serve its customers more effectively.

- March 2024: Dow introduced two new sustainable propylene glycol (PG) solutions in North America, utilizing bio-circular (REN) and circular feedstocks (CIR). The newly launched PG solutions, CIR and REN, aim to assist customers in achieving their circular and sustainability objectives. These solutions serve a wide range of applications spanning various industries, such as personal care, cosmetics, pharmaceuticals, food ingredients, flavorings, fragrances, agriculture, and industrial sectors.

Global Glycol Market Report Scope

Glycol, a member of the alcohol family, consists of chemical compounds characterized by two hydroxyl (OH) groups attached to separate carbon atoms. The term "glycol" often refers to its simplest form, ethylene glycol. This compound is a colorless, odorless, and flammable liquid with a sweet taste and viscous texture. While it finds extensive applications across diverse sectors, ranging from automotive and packaging to pharmaceuticals, food and beverage processing, textiles, etc., it is essential to note that high concentrations can be toxic to humans.

The glycol market is segmented by type, end-user industry, and geography. By type, the market is segmented into ethylene glycol (monoethylene glycol (MEG), diethylene glycol (DEG), triethylene glycol (TEG), and polyethylene glycol (PEG)), propylene glycol, and other types. By end-user industry, the market is segmented into automotive and transportation, packaging, food and beverage, cosmetics, pharmaceuticals, textiles, and other end-user industries. The report also covers the market sizes and forecasts for the global glycol market in 27 countries across major regions. For each segment, the market sizing and forecasts are based on volume in tons.

| Ethylene Glycol | Monoethylene Glycol (MEG) |

| Diethylene Glycol (DEG) | |

| Triethylene Glycol (TEG) | |

| Polyethylene Glycol (PEG) | |

| Propylene Glycol | |

| Other Types |

| Automotive and Transportation |

| Packaging |

| Food and Beverage |

| Cosmetics |

| Pharmaceuticals |

| Textile |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Ethylene Glycol | Monoethylene Glycol (MEG) |

| Diethylene Glycol (DEG) | ||

| Triethylene Glycol (TEG) | ||

| Polyethylene Glycol (PEG) | ||

| Propylene Glycol | ||

| Other Types | ||

| By End-user Industry | Automotive and Transportation | |

| Packaging | ||

| Food and Beverage | ||

| Cosmetics | ||

| Pharmaceuticals | ||

| Textile | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Glycol Market?

The Glycol Market size is expected to reach 48.73 million tons in 2025 and grow at a CAGR of 5.70% to reach 64.29 million tons by 2030.

What is the current Glycol Market size?

In 2025, the Glycol Market size is expected to reach 48.73 million tons.

Who are the key players in Glycol Market?

Shell PLC, Indorama Ventures Public Company Limited, Reliance Industries Limited, MEGlobal and PETRONAS Chemicals Group Berhad are the major companies operating in the Glycol Market.

Which is the fastest growing region in Glycol Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Glycol Market?

In 2025, the Asia Pacific accounts for the largest market share in Glycol Market.

What years does this Glycol Market cover, and what was the market size in 2024?

In 2024, the Glycol Market size was estimated at 45.95 million tons. The report covers the Glycol Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Glycol Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: