Market Overview

| Study Period | 2020 - 2030 |

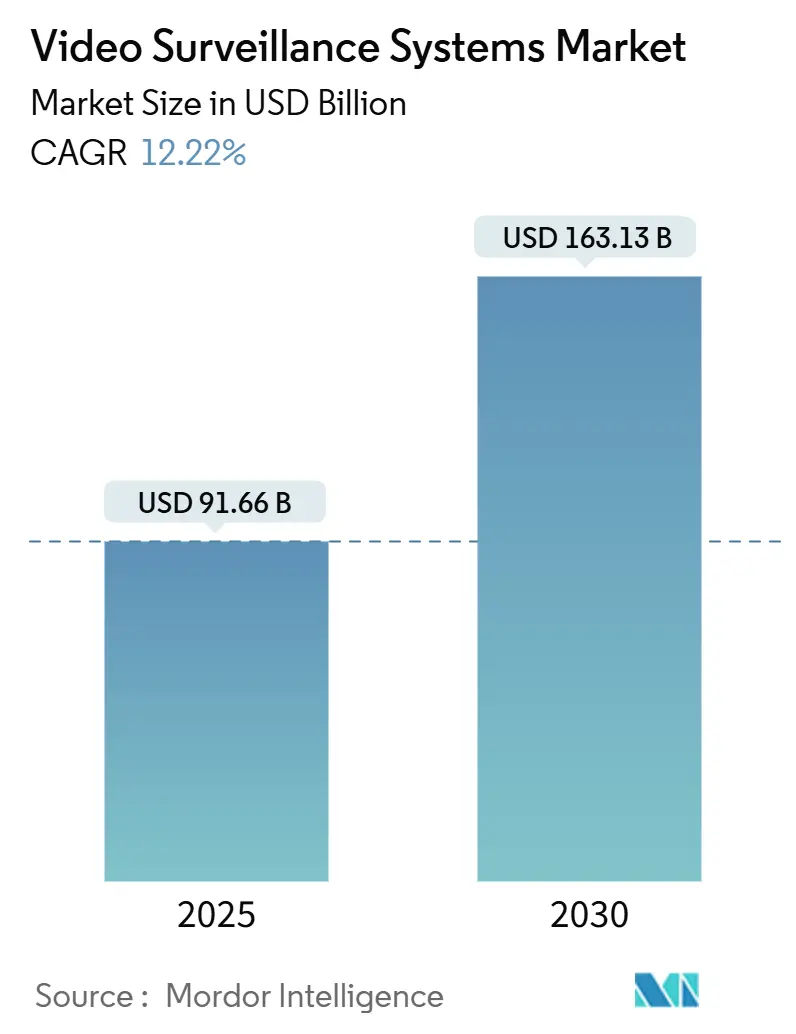

| Market Size (2025) | USD 91.66 Billion |

| Market Size (2030) | USD 163.13 Billion |

| Growth Rate (2025 - 2030) | 12.22% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Video Surveillance Systems Market Analysis by Mordor Intelligence

The video surveillance systems market size stands at USD 91.66 billion in 2025 and is on track to reach USD 163.13 billion by 2030, advancing at a 12.22% CAGR during the forecast period. This expansion is propelled by accelerated migration from analog to IP architectures, rapid integration of AI-powered edge analytics, and expanding public-safety budgets across emerging economies. Cloud-based video management platforms are reshaping cost structures, while NDAA-compliant product lines from Western vendors are gaining traction in response to tightened sourcing rules. Supply-chain realignments triggered by chiplet shortages and data-privacy mandates are moderating growth but have not derailed the underlying adoption curve. The video surveillance systems market size for IP-enabled devices is set to compound fastest, supported by 5G connectivity in transportation hubs and safe-city projects in the Middle East and Africa.

Key Report Takeaways

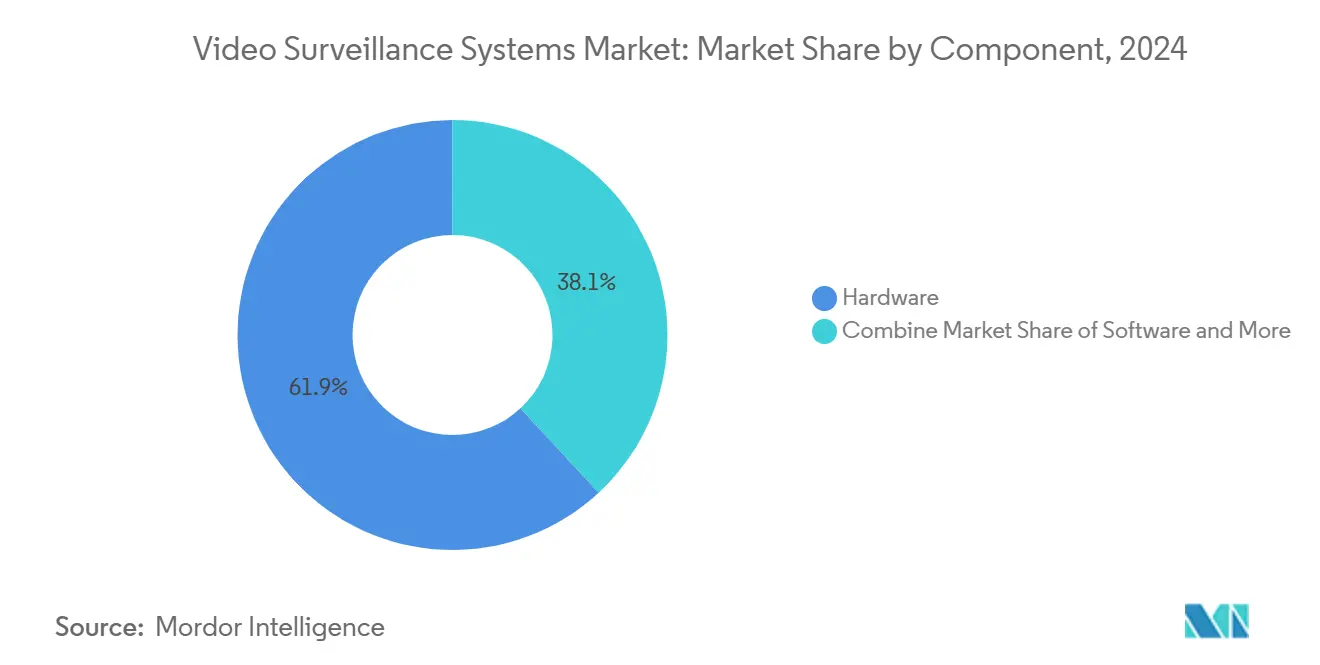

- By component, hardware led with 61.90% revenue share in 2024; services (VSaaS) are forecast to expand at a 14.37% CAGR to 2030.

- By system type, IP solutions held 71.23% of the video surveillance systems market share in 2024, while wireless 4G/5G platforms are projected to grow at 14.40% CAGR through 2030.

- By deployment mode, on-premise models retained a 66.65% share in 2024; cloud deployment is expected to deliver a 13.55% CAGR to 2030.

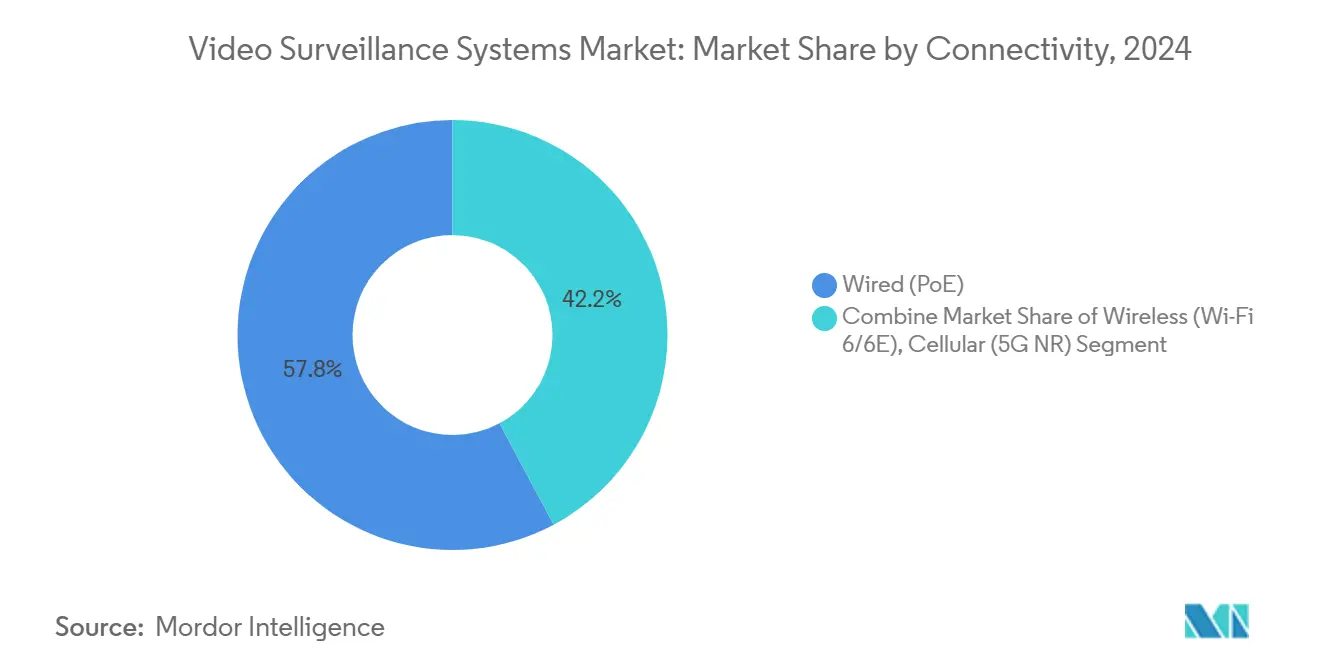

- By connectivity, wired PoE infrastructures commanded the majority share of 57.80% 2024 in 2024; 5G-enabled deployments are set to register 13.60% CAGR to 2030.

- By enterprise size, large enterprises captured 74.00% share in 2024; small and mid-sized enterprises are poised for a 12.60% CAGR through 2030.

- By application, city surveillance accounted for 28.70% of the video surveillance systems market size in 2024 and residential smart-home solutions are advancing at a 13.75% CAGR.

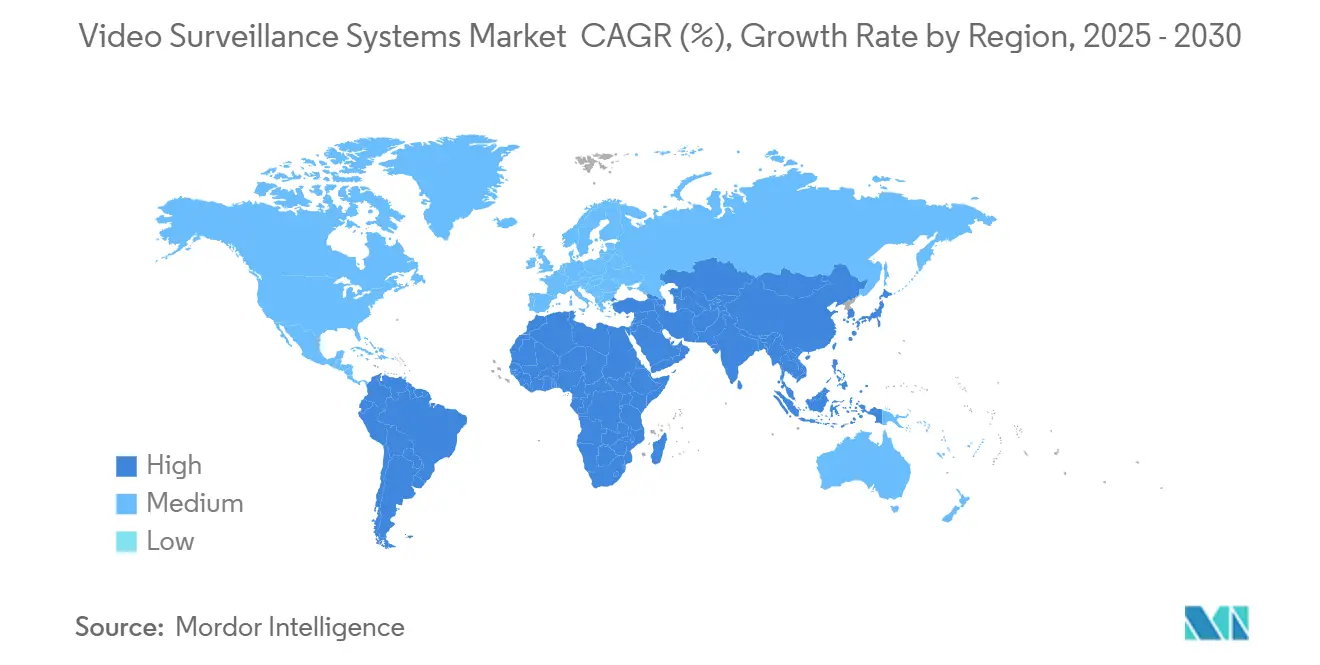

- By geography, Asia led with a 39.57% share in 2024; Africa is projected to post the fastest regional CAGR of 12.90% to 2030.

- Hikvision, Dahua, Axis Communications, and Motorola Solutions together controlled close to 50% of global revenues in 2024.

Global Video Surveillance Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid AI-powered edge analytics integration | +2.8% | Global; early uptake in North America and Europe | Medium term (2–4 years) |

| Mandatory migration from analog to IP in EU | +1.5% | European Union; spillover to Eastern Europe | Short term (≤ 2 years) |

| Tier-3 & Tier-4 data-center build-outs | +1.2% | North America; pattern emerging in Asia-Pacific | Medium term (2–4 years) |

| 5G-enabled ultra-HD streaming in Asia | +1.8% | China, Japan, South Korea, Southeast Asia | Medium term (2–4 years) |

| National safe-city grants across MEA | +2.1% | Saudi Arabia, United Arab Emirates, South Africa | Short term (≤ 2 years) |

| ESG-linked insurance incentives | +0.8% | Initially North America and Europe | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rapid AI-powered Edge Analytics Integration

Edge inference chips now enable real-time threat detection that trims false alarms by up to 90%, cutting response costs and widening use cases into operational intelligence. Multi-directional AI cameras consolidate coverage points, easing installation budgets and slashing bandwidth loads. Uptake is strongest in retail loss-prevention, industrial safety, and traffic-flow optimisation. Yet Axis Communications reports a gap between channel enthusiasm for AI and end-user priority on cybersecurity, suggesting vendors must better align messaging with risk-management goals

Mandatory Migration from Analog to IP in EU Smart-Cities

EU digital-transformation mandates are pushing municipalities to retire analog hardware, even as hybrid estates remain in service during transition. GDPR rules intensify encryption, anonymisation, and retention obligations, raising total cost of ownership but reinforcing data-sovereignty safeguards. The UN-Habitat Smart Cities Outlook underscores equitable access and transparent governance, themes that shape procurement criteria and vendor disclosures

Tier-3 & Tier-4 Data-Center Surveillance Build-outs across North America

Hyperscale investors have earmarked more than USD 500 billion for new facilities, with ANSI/TIA-942 clauses forcing tighter 24/7 surveillance, redundant feeds, and 180-day archives for Tier-4 halls. AI-enabled analytics at cabinet level guard intellectual property and meet SOC 2 audits, driving premium demand for NDAA-compliant cameras and edge storage.

5G-enabled Ultra-HD Streaming Demand in Asian Transportation Hubs

Private millimetre-wave 5G networks at Changi Airport and Hong Kong International Airport stream multi-megabit video from more than 120 cameras with sub-50 ms latency. [3]Civil Aviation Authority of Singapore, “5G Aviation Testbed Launched at Changi Airport Airside,” caas.gov.sgThe capacity uplift underpins autonomous ground-support vehicles and predictive maintenance models, cementing 5G as a keystone for smart-hub security.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-driven multi-terabyte retention costs | -1.7% | EU; multinationals with European assets | Medium term (2–4 years) |

| U.S. NDAA & FCC sourcing restrictions | -1.2% | North America; aligned allies | Short term (≤ 2 years) |

| Acute chiplet shortages for AI SoCs | -2.3% | Global; acute in emerging economies | Short term (≤ 2 years) |

| Rising cyber-insurability thresholds | -0.9% | Initially North America and Europe | Medium term (2–4 years) |

Source: Mordor Intelligence

GDPR-driven Multi-terabyte Data-Retention Costs

High-resolution video inflates storage footprints, forcing enterprises to build encryption-ready archives and manage privacy by design. IntechOpen research confirms mounting expenses tied to anonymisation engines that strip personally identifiable information while retaining evidentiary value . These outlays weigh on municipal budgets, slowing refresh cycles.

U.S. NDAA & FCC Black-List Sourcing Restrictions

Section 889 bans procurement of hardware from specific Chinese vendors, compelling rip-and-replace programs across federal estates. The FCC Covered List extends limitations to private utilities, boosting opportunities for Axis Communications, Avigilon, and Pelco to backfill demand.[2]Federal Communications Commission, “List of Equipment and Services Covered by Section 2,” fcc.gov Enterprises face higher acquisition prices and extended lead times as supply chains reorient.

Segment Analysis

Hardware generated 61.90% of 2024 revenues, anchored by IP cameras and network video recorders that underpin most installations. Cameras integrating AI inference engines now offload analytics from servers, raising unit prices but trimming bandwidth needs. Thermal and multispectral sensors are capturing niche demand in energy utilities and perimeter defence. The video surveillance systems market is witnessing hardware innovation in multi-sensor arrays that slash blind-spot risks and improve low-light fidelity. These gains encourage mission-critical sectors—airports, ports, and data centres—to budget for higher-spec devices despite economic volatility.

Services are expanding even faster. VSaaS subscriptions align with enterprise moves toward operational expenditure models and global access requirements. One-third of active surveillance capacity already sits in public-cloud buckets, and Wasabi forecasts storage exceeding 150 Exabytes in 2024. That volume validates the 14.37% CAGR for cloud services and is steadily recalibrating procurement between outright hardware purchase and bundled service contracts. Segment contributors anticipate the video surveillance systems market size for cloud-managed subscriptions to outpace on-premise appliance upgrades from 2026 onward.

Note: Segment shares of all individual segments available upon report purchase

By System Type: IP Dominance Accelerates with Wireless Growth

IP-based architectures owned 71.23% of market revenues in 2024, signalling the decisive pivot away from analog. High-definition sensors coupled with PoE simplify rollouts and feed directly into AI engines. Government tender documents increasingly specify NDAA compliance, cementing IP as the reference standard for security-grade installations. The video surveillance systems market share of wireless 4G/5G solutions remains smaller but is scaling fast on the back of transport-hub pilots and remote industrial deployments. A projected 14.40% CAGR reflects pent-up demand for rapid-install units where trenching fibre is impractical.

Hybrid deployments remain relevant during legacy transitions. Analog-to-IP encoders and coax-over-Ethernet bridges allow campuses to stagger upgrades without downtime. Vendors now bundle cloud gateways that expose analog feeds to AI analytics, smoothing adoption for budget-constrained municipalities. As 5G standalone cores mature, cellular cameras are expected to close cost gaps with Wi-Fi backhaul, particularly in disaster-response and temporary event security.

By Deployment Mode: On-Premise Legacy Yields to Cloud Momentum

On-premise video management software still anchors 66.65% of installed systems, driven by data-sovereignty rules in critical infrastructure. Financial institutions and government agencies maintain private networks and air-gapped storage arrays to meet audit mandates. However, cloud-native platforms are eroding this base. A 13.55% CAGR to 2030 mirrors enterprise IT’s broader shift to software-as-a-service. Edge gateways now compress and encrypt streams before transit, mitigating bandwidth fears and reducing total cost. The video surveillance systems market size for private-cloud architectures is projected to widen as security-conscious organisations seek control without foregoing scalability.

Hybrid models illustrate the transition path. They permit local recording for low-latency playback while offering cloud redundancy for disaster recovery. This mix is especially appealing to retail chains balancing thousands of sites with limited on-site IT skills. Vendors such as Synology and Milestone are adding policy-based routing that moves high-risk footage automatically to secure clusters, satisfying cyber-insurer thresholds that increasingly shape procurement guidelines.

By Connectivity: Wired Infrastructure Evolves with Wireless Innovation

Wired (PoE) cabling remains the backbone of enterprise and holds a 57.80% share in 2024, due to reliability and power delivery convenience. Multi-gigabit switches with extended temperature ratings now populate factory floors and parking structures, underscoring PoE’s endurance. Yet wireless innovations are expanding the perimeter. Wi-Fi 6/6E pushes gigabit speeds indoors, while true 5G cameras using licensed spectrum open up rail corridors, oil fields, and event venues where wires are untenable. The European Commission prioritises the 26 GHz band for such high-capacity uplinks that support uncompressed 4K streams in crowd-dense hotspots.

Whereas, cellular (4G/5G NR) is growing at the fastest CAGR by 2030. Also, end users often conflate 5G cellular with 5 GHz Wi-Fi, prompting vendors to clarify capabilities and range assumptions. As private 5G deployments proliferate in airports and seaports, expect growth in managed connectivity services bundled with surveillance hardware, adding a novel revenue layer for system integrators.

Note: Segment shares of all individual segments available upon report purchase

By Application: City Surveillance Leads While Residential Segment Surges

Municipal safe-city networks accounted for 28.70% of 2024 revenues. Integrated command centres ingest camera, license-plate, and sensor feeds to orchestrate traffic flow and emergency dispatch. China, Singapore, and Gulf states headline mega-projects, but EU cities are scaling similar platforms tied to urban mobility and climate-resilience goals. The video surveillance systems market size allocated to residential and smart-home use cases is expanding fastest, charting a 13.75% CAGR as doorbell cameras, indoor monitors, and interoperable home hubs proliferate.

Commercial settings remain the workhorse of demand. Retailers marry shopper-analytics with loss-prevention, banks integrate teller-position monitoring with fraud detection, and industrial sites track PPE compliance. Defence and homeland-security programmes continue to push the frontier in resolution, ruggedisation, and embedded AI, with downstream benefits filtering to civilian sectors as component costs drop.

Geography Analysis

Video Surveillance Systems Market in Middle East & Africa

Asia held 39.57% of global revenues in 2024, led by China’s scale but increasingly diversified as Indian smart-city tenders and Japanese infrastructure upgrades gain momentum. Beijing’s policy focus on public-safety AI fosters mass deployment of edge-intelligent cameras, even as export restrictions nudge local vendors toward ASEAN markets. Hong Kong International Airport’s private 5G roll-out underscores the region’s lead in integrating connectivity and surveillance.[3]GSMA, “How 5G is Transforming APAC,” gsma.com

North America remains a technological bellwether. NDAA and FCC rules catalyse replacement cycles, funneling share toward compliant suppliers. Cloud-connected camera counts rose by over 1 million units last year, highlighting the rapid VSaaS shift. Canadian transport authorities mirror this trajectory with multi-agency cloud roll-outs.

Africa, though smaller in absolute value, is the fastest-growing region at a 12.90% CAGR. Nigeria’s expanding urban footprint and rising crime statistics underpin state-level surveillance grants. Chinese concessional financing packages accelerate adoption but raise policy debates around data governance and vendor lock-in. Power intermittency and bandwidth constraints pose operational challenges, making hybrid solar-powered towers and low-bitrate codecs critical for sustained performance.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Innovation and Integration Drive Market Success

The top four suppliers—Hikvision, Dahua, Axis Communications, and Motorola Solutions—collectively hold nearly half of global hardware revenues, underscoring moderate concentration at manufacturing level. Chinese leaders maintain scale advantage in component integration and domestic demand, yet face curtailed access to North American and European government contracts due to security sanctions. Western incumbents are capitalising on these sanctions by pitching NDAA-compliant portfolios and transparent cybersecurity roadmaps.

Strategic M&A reshapes software and services layers. Triton’s acquisition of Bosch’s security business adds a EUR 1 billion revenue stream and 4,300 employees, strengthening European manufacturing capacity. GardaWorld’s purchase of Stealth Monitoring embeds AI-enabled remote monitoring into its guarding portfolio, illustrating convergence between physical and cyber services. Milestone Systems bought Brighter AI to integrate anonymisation engines that address stringent privacy regulations.

Alliances supplement outright deals. Bosch and Sony’s distribution pact leverages Bosch’s channel muscle while preserving Sony’s imaging R&D. Platform openness and SDK availability now differentiate vendors as integrators seek to orchestrate video, access-control, and building-automation under unified dashboards. Edge-to-cloud orchestration capabilities, zero-trust architectures, and data-residency assurances are emerging battlegrounds shaping future share.

Video Surveillance Systems Industry Leaders

-

Hangzhou Hikvision Digital Technology Co. Ltd

-

Zhejiang Dahua Technology Co. Ltd

-

Axis Communications AB

-

Bosch Security & Safety Systems

-

Hanwha Vision (Samsung)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Milestone Systems acquired Brighter AI to embed advanced anonymisation in its video-management suite.

- April 2025: Axis Communications published “The State of AI in Video Surveillance,” summarising feedback from 5,800 practitioners.

- April 2025: U.S. video surveillance revenue outlook lifted to USD 18.06 billion by 2030 on sustained cloud adoption.

- February 2025: Hikvision issued five AIoT predictions covering perception innovation and proactive cybersecurity.

Global Video Surveillance Systems Market Report Scope

Video surveillance systems refer to the use of security cameras to monitor and record activities in specific areas or locations for security, safety, or monitoring purposes. Such a system comprises cameras, monitors or display units, and recorders. These cameras can be analog or digital and come with various design features. These systems can be installed indoors and outdoors, operate 24/7, and can be set to record based on movement or specific times of the day.

The video surveillance market is segmented by type (hardware (camera (analog, IP cameras, and hybrid) and storage), software (video analytics and video management software), and services (VSaaS)), end-user vertical (commercial, infrastructure, institutional, industrial, defense, and residential), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa).

| By Component | Hardware | Cameras | Analog | |

| IP | ||||

| Thermal / Multispectral | ||||

| Storage | DVR/NVR | |||

| SAN / Edge-Storage | ||||

| Software | Video Management Software | |||

| Video Analytics | ||||

| Services (VSaaS) | Hosted | |||

| Managed | ||||

| Hybrid | ||||

| By System Type | Analog | |||

| IP | ||||

| Hybrid | ||||

| Wireless 4G/5G | ||||

| By Deployment Mode | On-premise | |||

| Cloud | Public | |||

| Private | ||||

| By Connectivity | Wired (PoE) | |||

| Wireless (Wi-Fi 6/6E) | ||||

| Cellular (5G NR) | ||||

| By Enterprise Size | Large Enterprises | |||

| SMEs | ||||

| By Application | City Surveillance and Safe-City | |||

| Commercial | Retail and Malls | |||

| BFSI and Fin-tech | ||||

| Critical Infrastructure | Energy and Utilities | |||

| Transportation (Airports, Rail, Ports) | ||||

| Industrial Manufacturing | ||||

| Residential and Smart-Home | ||||

| Defense and Homeland Security | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Nordics | ||||

| Benelux | ||||

| Rest of Europe | ||||

| APAC | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| ASEAN | ||||

| Australia and New Zealand | ||||

| Rest of APAC | ||||

| Middle East | Saudi Arabia | |||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Rest of Africa | ||||

By Component

| Hardware | Cameras | Analog | |

| IP | |||

| Thermal / Multispectral | |||

| Storage | DVR/NVR | ||

| SAN / Edge-Storage | |||

| Software | Video Management Software | ||

| Video Analytics | |||

| Services (VSaaS) | Hosted | ||

| Managed | |||

| Hybrid | |||

By System Type

| Analog |

| IP |

| Hybrid |

| Wireless 4G/5G |

By Deployment Mode

| On-premise | |

| Cloud | Public |

| Private |

By Connectivity

| Wired (PoE) |

| Wireless (Wi-Fi 6/6E) |

| Cellular (5G NR) |

By Enterprise Size

| Large Enterprises |

| SMEs |

By Application

| City Surveillance and Safe-City | |

| Commercial | Retail and Malls |

| BFSI and Fin-tech | |

| Critical Infrastructure | Energy and Utilities |

| Transportation (Airports, Rail, Ports) | |

| Industrial Manufacturing | |

| Residential and Smart-Home | |

| Defense and Homeland Security |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Benelux | |

| Rest of Europe | |

| APAC | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Australia and New Zealand | |

| Rest of APAC | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the video surveillance systems market?

The market is valued at USD 91.66 billion in 2025 and is forecast to reach USD 163.1 billion by 2030 at a 12.2% CAGR.

Which region holds the largest share of global revenues?

Asia leads with 39.57% of worldwide spending, supported by large-scale smart-city and transportation projects.

How fast are cloud-based surveillance services growing?

Cloud deployment is advancing at a 13.55% CAGR, reflecting rising VSaaS adoption and hybrid architecture roll-outs.

What impact do NDAA and FCC rules have on procurement?

The regulations restrict equipment from certain Chinese manufacturers, prompting U.S. enterprises to switch to NDAA-compliant suppliers and reshaping global supply chains.

Page last updated on: June 27, 2025