UHT Processing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

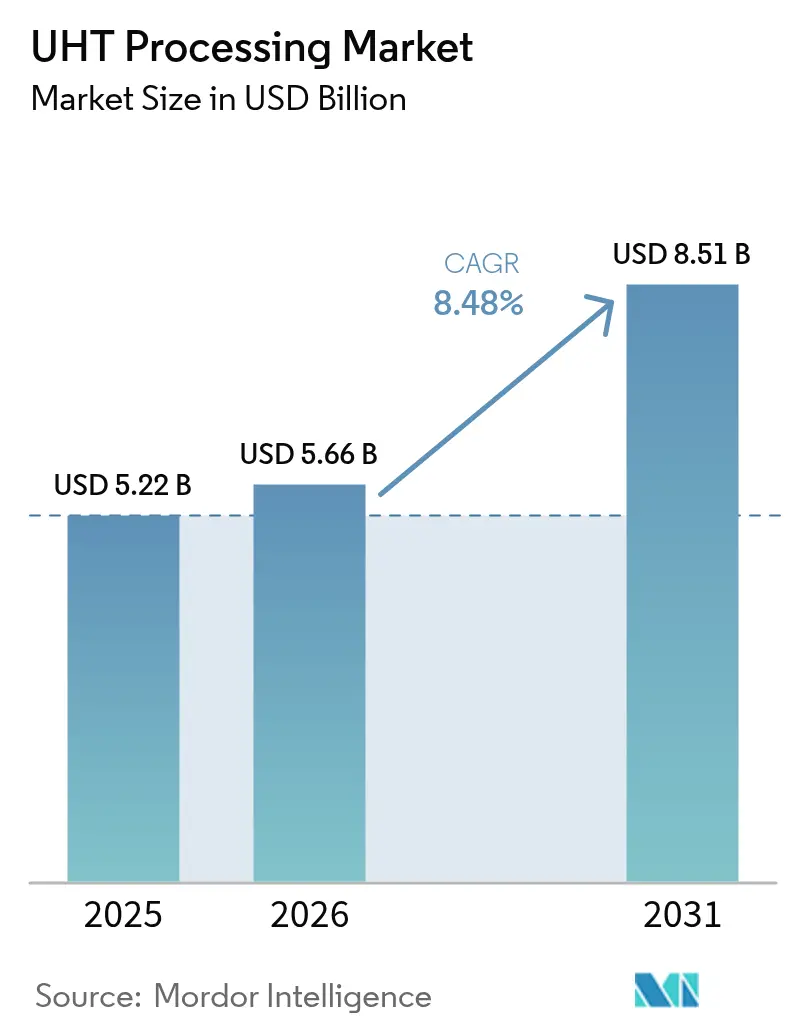

| Market Size (2026) | USD 5.66 Billion |

| Market Size (2031) | USD 8.51 Billion |

| Growth Rate (2026 - 2031) | 8.48% CAGR |

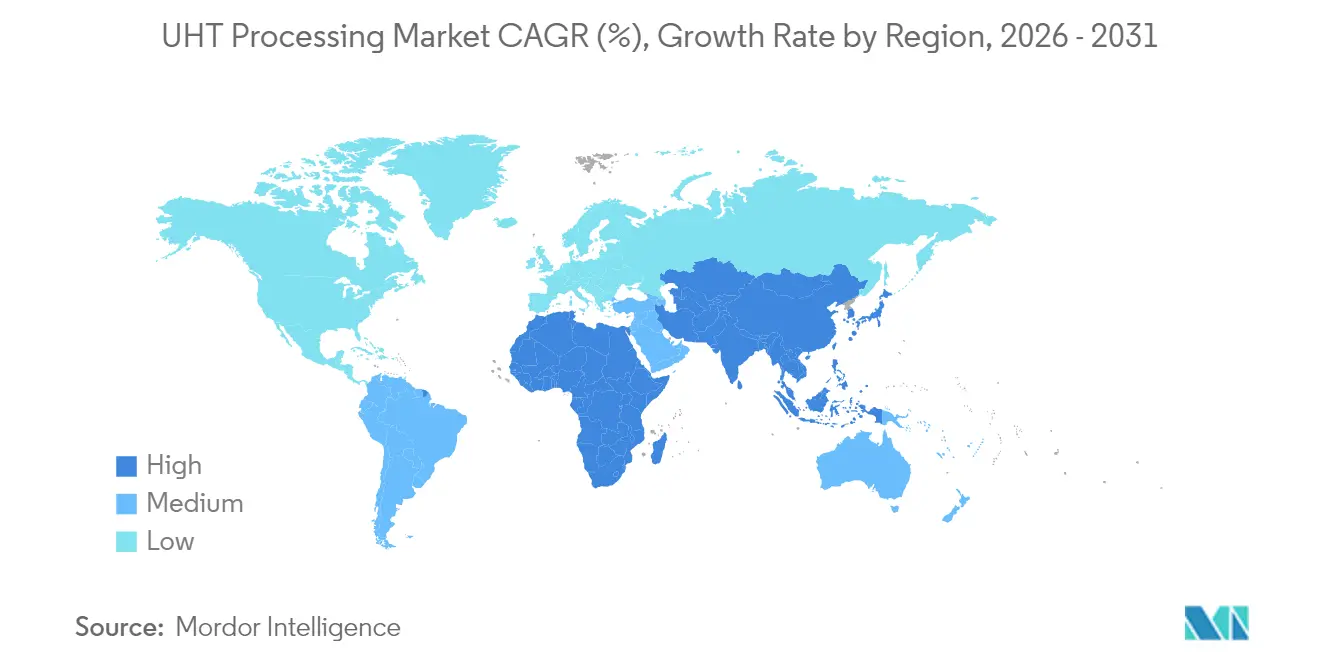

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UHT Processing Market Analysis by Mordor Intelligence

UHT processing market size in 2026 is estimated at USD 5.66 billion, growing from 2025 value of USD 5.22 billion with 2031 projections showing USD 8.51 billion, growing at 8.48% CAGR over 2026-2031. The market growth is driven by the increasing adoption of ambient distribution strategies, which reduce dependence on cold-chain infrastructure and enable broader shelf-stable product offerings. Advancements in direct steam-injection heaters and aseptic carton technology preserve protein integrity while providing up to 12 months of shelf life without refrigeration. The industry is shifting toward energy-efficient systems that recover 92% of process heat to meet sustainability requirements. Automated production lines reduce labor requirements and make UHT processing more accessible to medium-sized companies. While Europe maintains strong consumer acceptance, the Asia-Pacific region shows the highest growth potential due to infrastructure development and supportive policies. Market competition now focuses on packaging innovation and environmental performance metrics alongside traditional processing capabilities.

Key Report Takeaways

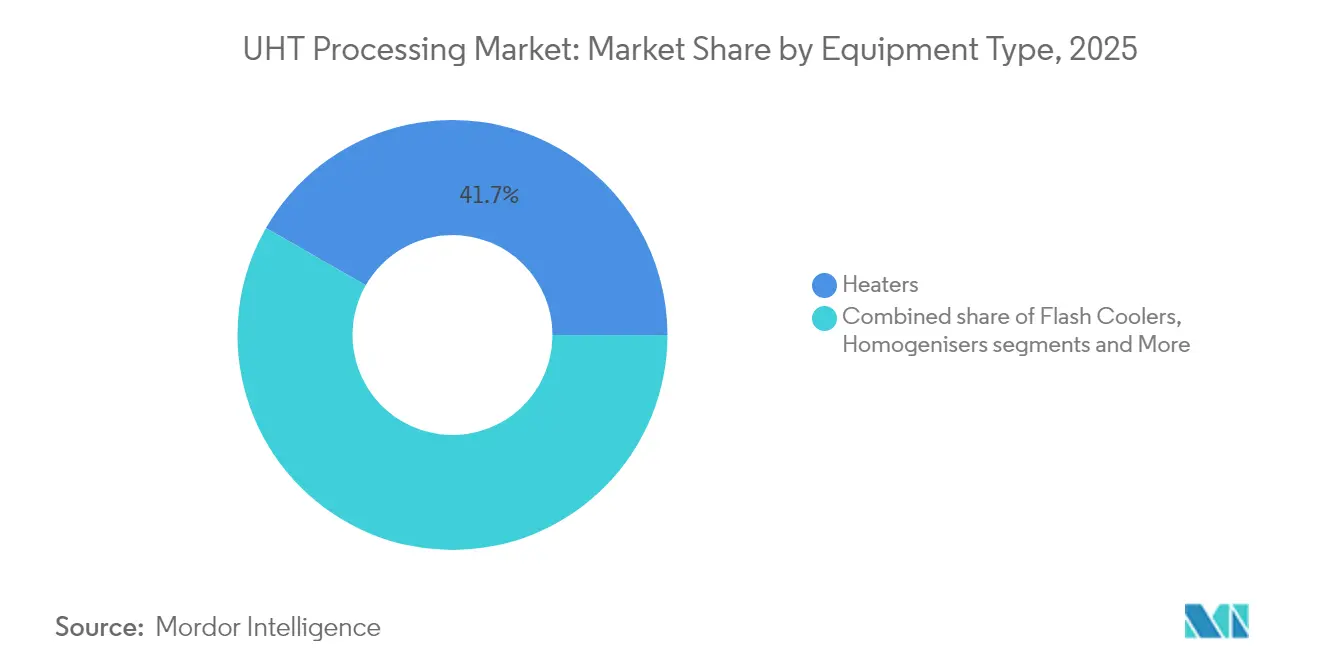

- By equipment type, heaters led with 41.72% of UHT processing market share in 2025; aseptic packaging is forecast to grow at 9.40% CAGR through 2031.

- By heating method, indirect UHT systems held 61.30% share of the UHT processing market size in 2025, while direct steam-injection systems are projected to expand at 10.95% CAGR over 2026-2031.

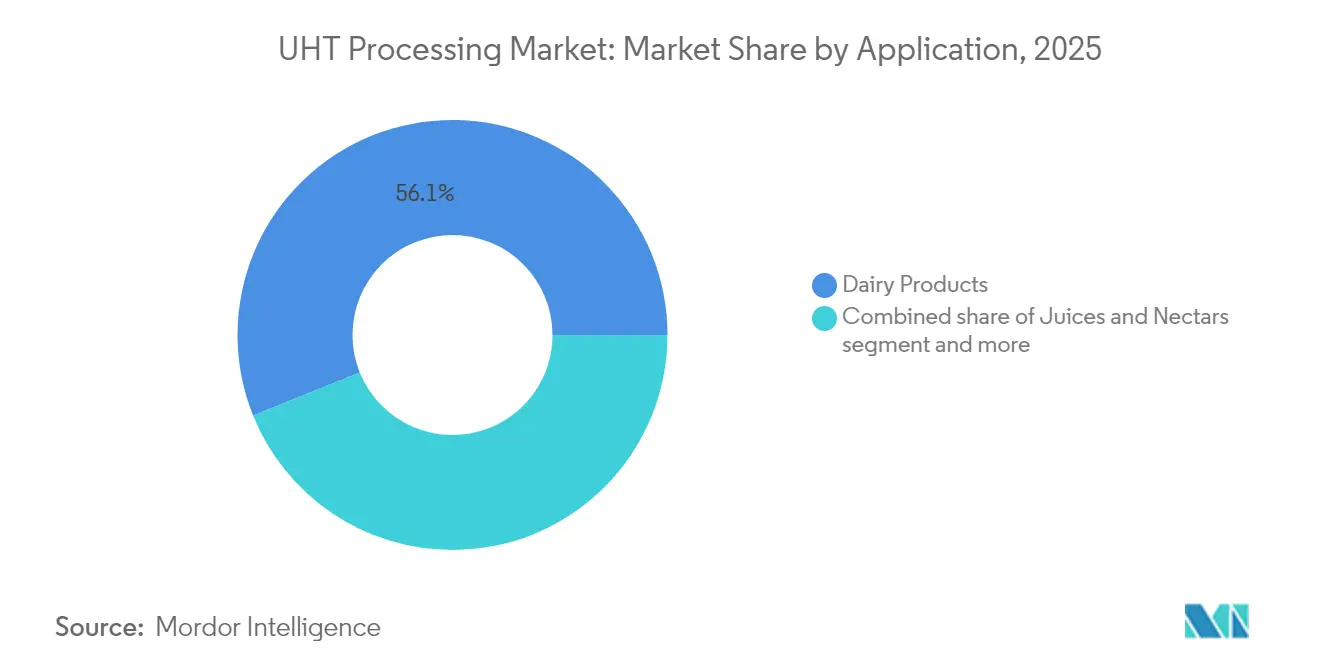

- By application, dairy products accounted for 56.10% share of the UHT processing market size in 2025, whereas juices and nectars are advancing at a 7.75% CAGR to 2031.

- By geography, Europe commanded 38.10% revenue share in 2025; Asia-Pacific is the fastest-growing region with an 8.55% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global UHT Processing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for shelf-stable dairy and beverage products | +2.1% | Global, with strongest impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Advancements in aseptic packaging technologies | +1.8% | Global, led by Europe and North America innovation centers | Short term (≤ 2 years) |

| Growing emphasis on ambient distribution to reduce cold-chain carbon footprints | +1.5% | Global, particularly relevant in regions with limited cold-chain infrastructure | Long term (≥ 4 years) |

| Technological advancements in UHT equipment | +1.4% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Increased adoption in non-dairy segments | +1.2% | North America and Europe leading, expanding to Asia-Pacific | Medium term (2-4 years) |

| Supportive government policies promoting food processing infrastructure | +0.8% | Asia-Pacific core, spill-over to Middle East and Africa and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for shelf-stable dairy and beverage products

The adoption of UHT technology extends beyond traditional dairy applications, driven by consumer preferences for bulk purchasing and improved remote distribution access. UHT milk has become essential in regions with limited milk production capabilities. For instance, the Philippines produces only 1% of its dairy demand and imports 99% of its requirements, according to USDA data.[1]United States Department of Agriculture, "Dairy and Products Annual", apps.fas.usda.gov The demand persists through imported ultra-heat-treated (UHT) milk, particularly in markets with developing cold-chain infrastructure, where traditional fresh milk distribution faces significant challenges and operational constraints. In 2024, Suntado's Idaho plant began processing 1 million lb of milk daily through UHT lines, eliminating refrigeration costs and providing a more efficient production model that reduces energy consumption and operational expenses. The technology now encompasses oat, almond, and soy beverages, addressing lactose-free requirements and sustainability concerns, while meeting the growing demand for plant-based alternatives and dietary preferences across different consumer segments. UHT processing has become integral to modern food distribution strategies by combining convenience, sustainability, and nutritional preservation, offering solutions for both manufacturers and consumers while maintaining product quality throughout the supply chain.

Advancements in aseptic packaging technologies

Packaging innovation drives UHT market differentiation through materials science breakthroughs that enhance sustainability while maintaining product integrity. The development of high-barrier, aluminum-free cartons represents a significant advancement in UHT packaging technology. SIG introduced a full-barrier package in May 2025 with 80% paper content, reducing carbon footprint by 61% while maintaining a 12-month shelf life on existing filling equipment. This innovation demonstrates the industry's commitment to environmental sustainability without compromising product quality. For instance, in September 2024, Tetra Pak launched its Prisma Aseptic 300 Edge carton, incorporating ergonomic design features to appeal to younger consumers. The design improvements focus on ease of handling and pouring, addressing specific consumer preferences in the beverage packaging segment. In Austria, Berglandmilch installed the first SIG SmileBig 24 filling system, which processes 24,000 packs per hour for both dairy and plant-based products. This installation showcases the versatility of modern UHT processing equipment in handling diverse product portfolios. Aluminium-free packaging is gaining traction. For instance, in June 2025, Hochwald implemented aluminum-free packaging formats, resulting in a 34% reduction in carton emissions.

Growing emphasis on ambient distribution to cut cold-chain carbon footprints

Environmental regulations and corporate sustainability commitments are driving UHT adoption as companies aim to reduce cold-chain energy consumption and carbon emissions. The implementation of stricter environmental policies worldwide has prompted food and beverage manufacturers to reassess their production methods and invest in sustainable technologies. The growing emphasis on environmental responsibility has made UHT processing an attractive option for companies seeking to minimize their ecological footprint. For instance, in May 2024, Tetra Pak's Factory Sustainable Solutions program achieves 92% heat recovery and 60% energy savings in Indirect UHT Unit D plants, showcasing the potential for substantial efficiency improvements in processing facilities and setting new industry standards for sustainable operations. Industrial heat pumps deliver 2-4 times the efficiency of traditional boilers, complementing UHT processing to reduce site energy consumption and operational costs while supporting environmental objectives. The expansion of carbon pricing across various regions makes ambient distribution increasingly important, supporting long-term growth in the UHT processing market and encouraging manufacturers to transition to more sustainable processing methods. This shift towards UHT technology represents a significant step in the industry's journey toward environmental sustainability and operational efficiency.

Technological progress in UHT equipment

Direct steam injection technology is the primary UHT method due to its higher heat transfer efficiency and lower capital costs compared to indirect heating systems. The technology enables precise temperature control and uniform heating distribution, ensuring consistent product quality and shelf life. SPX FLOW's Seamless Infusion Vessel, introduced in January 2024, minimizes product fouling and enhances operational efficiency through its improved design and control systems. Processing facilities with 12,000 liters per hour capacity require 30 fewer cleaning cycles annually, reducing energy consumption, water usage, and detergent requirements, which enhances sustainability and lowers operational costs. Krones' VarioAsept M UHT system processes 3,500 to 60,000 liters per hour and incorporates modular components, including aseptic storage, deaeration systems, and multiple heating options for flexible operations. The system enables processors to modify production capacity according to market demands while maintaining quality standards. Hydro-Thermal Corporation's A210 Sanitary Hydroheater delivers exact temperature control within milliseconds and reduces fouling, enhancing milk products and ice cream mixes flavor quality.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High initial capital investment for UHT systems | -1.9% | Global, particularly constraining for emerging market processors | Short term (≤ 2 years) |

| Higher energy consumption compared to traditional pasteurization | -1.3% | Global, with greater impact in regions with high energy costs | Medium term (2-4 years) |

| Shortage of skilled operators in emerging markets leading to operational inefficiencies | -0.8% | Asia-Pacific, Middle East and Africa, and Latin America primarily | Long term (≥ 4 years) |

| Nutritional degradation concerns due to high-temperature processing | -0.6% | Global, particularly relevant for health-conscious consumer segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High initial capital investment for UHT systems

High capital requirements create significant entry barriers in the market, especially for small-scale processors aiming to develop shelf-stable product lines. The substantial investments required for UHT processing infrastructure are demonstrated by Alfa Laval's SEK 350 million order in February 2025. This investment includes processing equipment, automation systems, and storage facilities necessary for UHT operations. The company's Indianapolis facility expansion shows how established companies increase production capacity to meet market demand through new processing lines and quality control systems. Major investments in dairy processing infrastructure, such as Chobani's USD 1.2 billion manufacturing plant in April 2025, indicate how extensive capital requirements benefit large-scale operators. The plant incorporates comprehensive processing capabilities, from raw material handling to packaging and distribution systems. Tetra Pak's USD 105 million Series D funding in May 2024 highlights the capital-intensive nature of UHT technology development and deployment, supporting research, development, and commercialization of new processing solutions.

Higher energy consumption compared to traditional pasteurization

Energy consumption remains a critical consideration as processors evaluate UHT benefits against operational costs, particularly in regions with high electricity prices or carbon pricing policies. The increasing focus on energy efficiency has prompted manufacturers to assess various pasteurization methods and their environmental impact. USDA research on pasteurization technologies shows HTST pasteurization has the lowest carbon footprint at 37.6 g CO2 equivalents/kg of processed raw milk, while UHT processing requires more energy, with consumption varying by system configuration.[2]United States Department of Agriculture, "Environmental assessment of alternative pasteurization technologies for fluid milk production using process simulation", ars.usda.gov UV pasteurization provides an energy-efficient alternative to thermal processing, though its use remains restricted to certain product types. The dairy industry has witnessed technological advancements in energy optimization, with Tetra Pak's UHT 2.0 heating system with OneStep technology reducing energy usage by up to 29% and water consumption by 35% compared to traditional UHT systems.[3]Tetra Pak International S.A., "Go nature. Go carton.", tetrapak.com Industrial heat pumps offer improved efficiency, operating 2-4 times more efficiently than conventional boilers while providing both heating and cooling functions needed for UHT operations. The implementation of these efficiency improvements helps processors maintain UHT benefits while controlling operational costs and meeting sustainability targets, making them increasingly important in modern dairy processing facilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Aseptic Innovation Drives Growth

Heaters hold a 41.72% market share in UHT processing equipment sales in 2025, due to their critical function in temperature control and product sterilization. The market prioritizes equipment that delivers effective heat transfer while maintaining sterile processing conditions to ensure product safety and quality. Direct steam-injection heaters offer superior fouling resistance compared to plate exchangers, reducing cycle times and operational downtime while improving production efficiency, driving the market growth.

Aseptic packaging equipment is expected to grow at a 9.40% CAGR through 2031, driven by increased manufacturer investments in contamination-prevention systems and sterile packaging solutions. KHS's systems demonstrate this advancement with a sterilization capacity of 36,000 bottles per hour, while Tech-Long's packaging equipment processes 70 packs per minute as of March 2024. Supporting equipment such as flash coolers, homogenizers, and clean-in-place systems enhances processing lines, with primary investment focusing on aseptic modules that offer product versatility, extended shelf life, and quality assurance.

By Heating Method: Direct Systems Gain Momentum

Indirect UHT Systems holds a dominant market share of 61.30% in 2025, supported by existing infrastructure and operational expertise. This dominance stems from their proven reliability, lower maintenance requirements, and widespread industry familiarity. Direct Steam-Injection Systems are experiencing significant growth with a CAGR of 10.95% during 2026-2031, driven by their rapid heating capabilities, enhanced product quality, and improved energy efficiency. Steam Infusion Systems serve a specific market segment, providing gentle heating for temperature-sensitive products, though they require more sophisticated equipment setups and specialized operator training.

Hydro-Thermal Corporation's A210 Sanitary Hydroheater exemplifies the benefits of direct steam injection, providing millisecond temperature control and minimizing fouling issues common in indirect systems. This technology delivers enhanced flavor profiles for milk and ice cream mixes, while also reducing processing time and energy consumption. The market shift toward direct systems presents growth opportunities for steam injection equipment manufacturers, particularly in regions with expanding dairy processing capabilities. In response, companies like Tetra Pak have adapted by offering both direct and indirect UHT options in their processing lines to meet diverse product specifications and customer needs, incorporating advanced automation features and digital monitoring capabilities.

By Application: Beyond Dairy Diversification

Dairy Products dominate with a 56.10% market share in 2025, leveraging established UHT technology infrastructure and processing capabilities. The Juices and Nectars segment shows robust growth at a 7.75% CAGR through 2031, attributed to rising consumer demand for plant-based beverages, health-focused options, and convenient consumption formats. Soups, Sauces, and Ready Meals offer growth potential as aseptic filling technologies enhance product durability, shelf stability, and consumer convenience. The Others segment includes plant-based milk alternatives and specialty beverages, showcasing UHT technology's adaptability across food categories.

Oat-based beverages show growth potential in non-dairy applications across developed markets like the US and Europe, and emerging markets such as Vietnam. This expansion stems from consumer preferences for environmental sustainability and the health benefits of plant-based alternatives. Research from the University of Copenhagen reveals that current UHT processing methods for plant-based drinks yield lower nutritional quality compared to cow's milk, indicating a need for processing improvements and new thermal treatment technologies. This diversification creates market growth opportunities while requiring manufacturers to develop expertise in managing product characteristics, including viscosity patterns and thermal sensitivity variations across food categories.

Geography Analysis

Europe holds 38.10% of the UHT processing market revenue in 2025. Belgium leads in UHT milk adoption, while the United Kingdom shows lower penetration rates, reflecting regional consumption preferences and traditional buying patterns. Germany, France, and Italy provide substantial processing infrastructure, with advanced manufacturing facilities and established distribution networks, while ongoing carton weight reduction initiatives align with EU carbon reduction goals and sustainability targets. The 2024 recycling partnership between Tetra Pak and Lactalis strengthens Europe's position in sustainable production methods through improved collection systems and processing capabilities.

Asia-Pacific emerges as the fastest-growing region with an 8.55% CAGR from 2026-2031. China and India drive regional market growth, with China's rapid urbanization and rising middle-class population increasing demand for packaged dairy products. The expansion of organized retail networks, including supermarkets, hypermarkets, and convenience stores, improves UHT product accessibility and consumer reach. India combines infrastructure development incentives with increasing consumer preference for convenience packaging and food safety assurance, while Japan adapts to its aging population through shelf-stable dairy products with enhanced nutritional profiles. Australia's variable climate conditions encourage processors to shift toward UHT milk production to reduce dependence on refrigeration and ensure consistent supply.

North America demonstrates steady growth supported by new processing facilities and technological investments. The Federal Milk Marketing Order (FMMO) reforms, implemented in June 2025, incorporate extended shelf-life (ESL) premiums to support regional demand for longer-lasting milk products and improve producer returns. These policy updates aim to align milk pricing with current market dynamics, production requirements, and changing consumer preferences while ensuring fair compensation for dairy farmers.

Regulatory Landscape

UHT processing is governed by national dairy safety and identity standards that cover heat treatment, aseptic processing controls, and product labeling for sterilized and long-life milk. In the United States, FDA regulations and the Grade A Pasteurized Milk Ordinance (PMO) underpin requirements for Grade A milk plants using aseptic processing and packaging systems. FDA standards also define ultra-pasteurized dairy products as processed at or above 280 degrees Fahrenheit for at least 2 seconds. In February 2026, a US Federal Register update referenced Grade A milk product processing requirements, reinforcing compliance expectations around sanitary design, process validation, and documentation for extended shelf-life and aseptic operations.

Several major dairy markets updated or proposed technical rules that affect UHT milk specifications and market access. Brazil moved to align identity and quality requirements through Portaria MAPA No 783 (April 2025), incorporating a Mercosur technical regulation for UHT milk to support harmonized trade and compliance across member markets. In Asia, China notified draft national food safety standards in June 2026 covering pasteurized and sterilized milk products. Vietnam promulgated Circular 09/2026/TT-BCT establishing QCVN 28:2026/BCT for fluid milk products, with implementation noted for September 1, 2026, increasing the emphasis on plant-side testing, traceability, and conformity assessment for UHT and other fluid milk categories.

Value Chain Analysis

The UHT processing value chain begins with raw milk or beverage base procurement and pre-treatment (standardization, separation, and filtration). It then moves through UHT heating (direct steam injection/infusion or indirect systems), homogenization, and aseptic holding prior to sterile filling and packaging. Equipment OEMs provide core processing modules, including UHT heaters, infusion vessels, homogenizers, aseptic tanks, and CIP/SIP systems, and they integrate controls, automation, and validation protocols. Packaging suppliers contribute cartons, bottles, caps, and barrier materials that are compatible with aseptic lines.

Downstream, ambient distribution and retail depend on sterility assurance and packaging integrity, shifting logistics from refrigerated transport to warehouse and shelf management for long-life formats. Service, testing, and local application support are increasingly important because aseptic validation and product development remain barriers for many processors. SPX FLOW expanded access to modular UHT testing by establishing pilot plant partnerships in southern California and Quebec in July 2025, helping shorten iteration cycles for formulation and process settings without committing to full-scale capex. Large dairy processors and co-packers continue to anchor demand for turnkey projects and upgrades, including SPX FLOWs over USD 30 million collaboration with Arla Foods (October 2025) to expand Lockerbie Creamery in Scotland into a UHT center of excellence. Regional capability builds also continue, including Shanghai EasyReal Machinery commissioning a UHT/HTST-DSI pilot plant for VILAC FOODS in Brazil (September 2025) to support R&D in dairy and functional beverages. Standards and analytical requirements shape upstream QA/QC inputs as well, including ISO/TS 27265:2026 (published May 2026) covering enumeration of thermoresistant spores in heat-processed products such as UHT milk.

Competitive Landscape

The UHT processing market demonstrates moderate concentration. Major global companies like The Tetra Laval Group, GEA Group AG, SPX FLOW Inc., SIG Group AG, and Krones AG dominate the market by providing comprehensive solutions, including heaters, homogenizers, filling lines, and digital twins. Smaller companies maintain market presence by focusing on specific components such as steam-injection nozzles, microwave-assisted modules, and carbon-neutral cartons.

Companies that combine thermal processing expertise with packaging innovation and automation capabilities hold competitive advantages in the market. These companies must also maintain adaptability to meet regional requirements and new food categories. SIG, GEA, and Krones implement machine-learning-based predictive maintenance systems to address operator shortages in emerging markets. Recent patent applications indicate industry focus on oxygen-blocking barrier layers without aluminum and robotic secondary packaging systems that reduce facility space requirements.

Regional companies maintain market positions through specialized offerings. Aftab Foods in India provides compact skid lines for contract packers, while China's Newamstar specializes in high-speed PET aseptic fillers for dairy and tea products. In Latin America, partnerships between local dairy companies and European equipment suppliers help distribute capital investment risks. The market remains dynamic as successful companies combine established thermal processing capabilities with advanced packaging technology and regional service networks.

UHT Processing Industry Leaders

-

The Tetra Laval Group

-

GEA Group AG

-

SPX FLOW lnc

-

SIG Group AG

-

Krones AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities center on lowering the cost and complexity of deploying aseptic lines while meeting sustainability and quality requirements. Modular, skid-mounted UHT line concepts from equipment suppliers are framed to reduce project timelines and enable capacity additions for mid-sized processors and co-packers that face long installation windows and specialist labor constraints. Energy and water intensity is also emerging as a key buying criterion: Tetra Pak describes OneStep technology that integrates pre-heating, separation, standardization, and homogenization into one step, with reductions of up to 35% in water use and up to 29% (and cited ranges up to 44%) in energy/heat energy versus traditional multi-step lines. This positioning aligns UHT investments with plant-level decarbonization targets.

Process and product innovation also creates scope beyond conventional dairy, particularly when processors target pasteurized-like sensory profiles with ambient shelf life. In April 2026, the Dairy Processing Task Force reported that indirect UHT milk processing lines can achieve up to 46% emissions reductions compared with 2019 standards, supporting retrofits and line redesigns tied to net-zero programs. Academic work published in 2026 highlights hybrid pathways such as microfiltration combined with microwave and indirect UHT heating (Customized Phase Treatment for whole milk), along with research into instantaneous UHT (INF) approaches aimed at sterilization with lower heat loads. Alongside broader adoption of digital twins, IoT monitoring, and predictive maintenance by major OEMs, these developments reinforce demand for integrated lines that combine sterility assurance, energy recovery, and faster changeovers across dairy, plant-based beverages, and ambient-ready foods.

Recent Industry Developments

- February 2026: ISO published ISO/TS 27265:2026, specifying methods to enumerate thermoresistant spores of thermophilic bacteria in heat-processed products, including UHT milk. The update strengthens a common QA/QC reference point for processors and OEMs, supporting validation and verification practices for aseptic operations across regions.

- November 2025: Tetra Pak launched an Integrated Heat Pump system for pasteurizers to electrify the process and recover waste heat, with claimed energy-use cuts of up to 77%. The launch reinforces the shift toward electrification and heat-recovery retrofits that complement UHT and ESL lines where processors are prioritizing operational decarbonization.

- October 2025: SPX FLOW introduced the APV Infusion UHT featuring SteamRecycle, positioned to recover and reuse 100% of steam used during the infusion UHT process and reduce CO2 emissions by up to 1,000 tons annually. This adds a differentiated sustainability feature to direct heating platforms, influencing equipment selection where energy and emissions metrics are tied to corporate targets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the UHT processing market covers equipment and systems used to sterilize liquid and semi-liquid food and beverage products at ultra-high temperatures, followed by aseptic handling so the product can be stored longer without spoilage.

Scope exclusions: The sizing excludes conventional pasteurization lines, retort canning, and non-food industrial sterilization uses.

Segmentation Overview

-

By Equipment Type

- Heaters

- Homogenisers

- Flash Coolers

- Aseptic Packaging

- Others

-

By Heating Method

- Indirect UHT Systems

- Direct Steam Injection Systems

- Steam Infusion Systems

-

By Application

- Dairy Products

- Juices and Nectars

- Soups, Sauces, and Ready Meals

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

We start by collecting public, repeatable inputs that explain where UHT demand is coming from and how equipment purchasing typically moves across regions. Common reference points include FAOSTAT for milk production, UN Comtrade for trade flows of dairy and juice categories, national agriculture and food processing statistics, and food safety guidance from bodies such as the FDA and the European Commission.

To link demand to equipment needs, we also review company filings and investor presentations from relevant equipment and packaging ecosystems, along with association publications and reputed press coverage on aseptic capacity additions. Patent databases are used selectively to understand heating method trends and packaging integration themes, and an import-export shipment level database helps sanity check cross-border equipment movements in key hubs. The desk sources listed are illustrative only, and additional public sources were also referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Next, we validate the desk-built picture using expert interviews and structured surveys across equipment suppliers, system integrators, packaging ecosystem participants, and end users such as dairy and beverage processors. Respondent input is used to confirm typical line configurations, adoption of direct versus indirect heating, replacement cycles, and regional purchasing patterns, so the final model does not rely on a single data series.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 18% | APAC: 44% |

| Mid tier: 48% | Functional/Unit leaders: 24% | EMEA: 32% |

| Smaller Players: 18% | Managers: 58% | Americas: 24% |

Market-Sizing & Forecasting

The core sizing is built using top-down logic where production and processing signals are translated into likely UHT line requirements, and then converted to spending using practical price and configuration assumptions. We focus on a defined demand pool by tracking indicators such as shelf-stable dairy output, ambient juice and nectar volumes, aseptic packaging adoption, the mix of direct steam injection versus indirect heating, and typical commissioning and replacement cycles at plants.

After the first total is formed, it is checked using selective bottom-up approximations, such as sampled line counts by region and typical line value ranges discussed in interviews, which are then used to adjust outliers. When a country has weaker visibility, gaps are handled by applying conservative penetration and utilization assumptions anchored to similar markets, followed by another review with experts.

For the forecast, scenario analysis is used because plant investments can shift quickly with dairy pricing, energy costs, and regulation changes. The scenarios are guided by expected capacity additions, modernization activity, and packaging availability, and then translated into yearly market values with consistent currency timing.

Data Validation & Update Cycle

We run multi-step checks before finalizing results, where model outputs are compared against independent signals such as reported capacity expansions, import patterns for processing equipment, and regional dairy and beverage processing growth. If a region shows an abnormal jump, the assumptions behind line count, average value, or timing are revisited, and the relevant experts are re-contacted for clarification.

Each report is refreshed annually, and interim updates are made when material events occur, including major capacity announcements or sharp changes in input costs that can delay projects. Before delivery, an analyst performs a fresh pass on the key inputs so clients receive an updated view aligned with the latest market direction.

Mordor Intelligence's Uht Processing Market Estimate Compared With Other Published Estimates

Published estimates for the UHT processing market can differ even when they appear similar on the surface, mainly because counted scope and year labeling are not always aligned. Differences also show up when one publisher ties demand to equipment and line additions, while another leans more heavily on broad industry growth rates.

Some external figures appear to include a wider set of adjacent aseptic and processing spending into the same number, or they use a different base year and currency timing across regions. In contrast, Mordor Intelligence counts UHT processing only when the equipment and systems are directly linked to UHT heating plus aseptic handling, and the totals are repeatedly checked against line configuration norms and replacement behavior gathered through interviews.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.66 B (2026) | |

| Global Consultancy A | USD 5.23 B (2025) | Uses a different base year and longer forecast window, and the disclosed breakout suggests broader treatment of applications and spend timing, which can shift the near-term level versus a 2026 stated size. |

| Industry Publisher B | USD 5.46 B (2025) | Reports a higher starting value with a base year anchored earlier in the cycle, and the scope presentation does not clearly separate UHT line spending from adjacent aseptic and packaging-linked investments in all regions. |

Looking across the table, the spread is largely explained by base year choice, what gets counted as UHT-only spending, and how equipment value is timed to project commissioning. Using clear inclusion rules and repeatable checks tied to production, packaging adoption, and line behavior helps keep the final number stable and easier to defend in planning discussions.

Key Questions Answered in the Report

What is the current UHT Processing Market size?

The UHT Processing Market is projected to register a CAGR of 8.48% during the forecast period (2026-2031).

Which is the fastest growing region in UHT Processing Market?

Asia-Pacific is estimated to grow at the highest CAGR of 8.55%over the forecast period (2026-2031).

Which region has the biggest share in UHT Processing Market?

In 2025, Europe accounted for the 38.10% market share in UHT Processing Market.

Which heating method has the biggest share in UHT Processing Market?

Indirect UHT Systems accounted for the 61.30% market share in UHT Processing Market.

Page last updated on: