Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

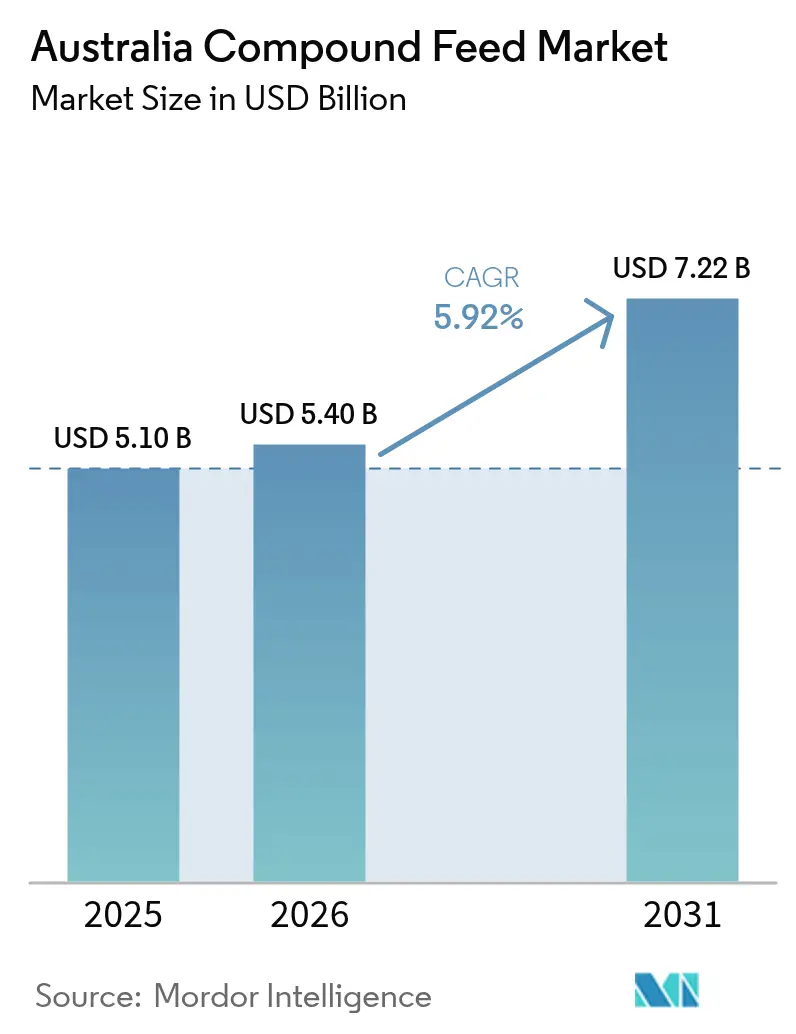

| Base Year Market Size (2025) | USD 5.10 Billion |

| Market Size (2026) | USD 5.4 Billion |

| Market Size (2031) | USD 7.22 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Compound Feed Market Analysis by Mordor Intelligence

The Australia compound feed market size is expected to grow from USD 5.10 billion in 2025 to USD 5.40 billion in 2026 and is forecast to reach USD 7.22 billion by 2031 at 5.92% CAGR over 2026-2031. This growth trajectory reflects the nation's intensifying livestock production demands and strategic pivot toward sustainable feed technologies. Rising domestic meat demand, particularly chicken, the swift uptake of precision-nutrition technologies, and federal incentives for methane-reducing additives collectively sustain the upward trajectory of the Australian compound feed market. According to OECD, for instance, in 2024, consumption of pork meat was 759.8 metric tons from 679.5 metric tons in 2023 [1]Source: Organisation for Economic Co-operation and Development, “Meat Consumption Statistics for Australia,” OECD Data, oecd.org. Cereals remain the dominant ingredient category, yet supplements post the fastest growth as livestock producers pursue lower emissions and higher feed efficiency. Vertical integration among major poultry and aquaculture operators secures captive feed offtake, while global agribusinesses accelerate local investments to capture emerging opportunities. Biosecurity regulation, grain-price swings, and a gradual consumer tilt toward plant-centric diets temper momentum but do not derail the positive outlook.

Key Report Takeaways

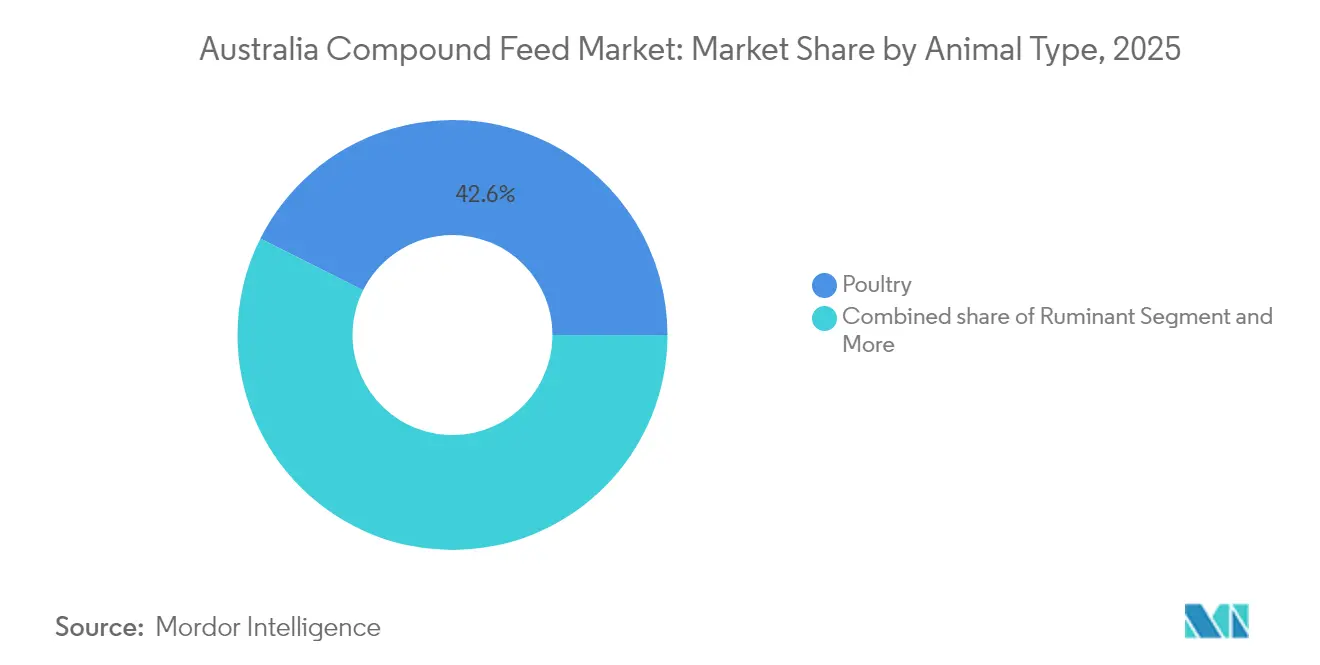

- By animal type, poultry accounted for 42.60% of the Australia compound feed market size in 2025, while aquaculture is projected to grow at a CAGR of 7.55% through 2031.

- By ingredient, cereals held 66.10% of the Australia compound feed market share in 2025, while supplements are predicted to grow at an 8.05% CAGR through 2031.

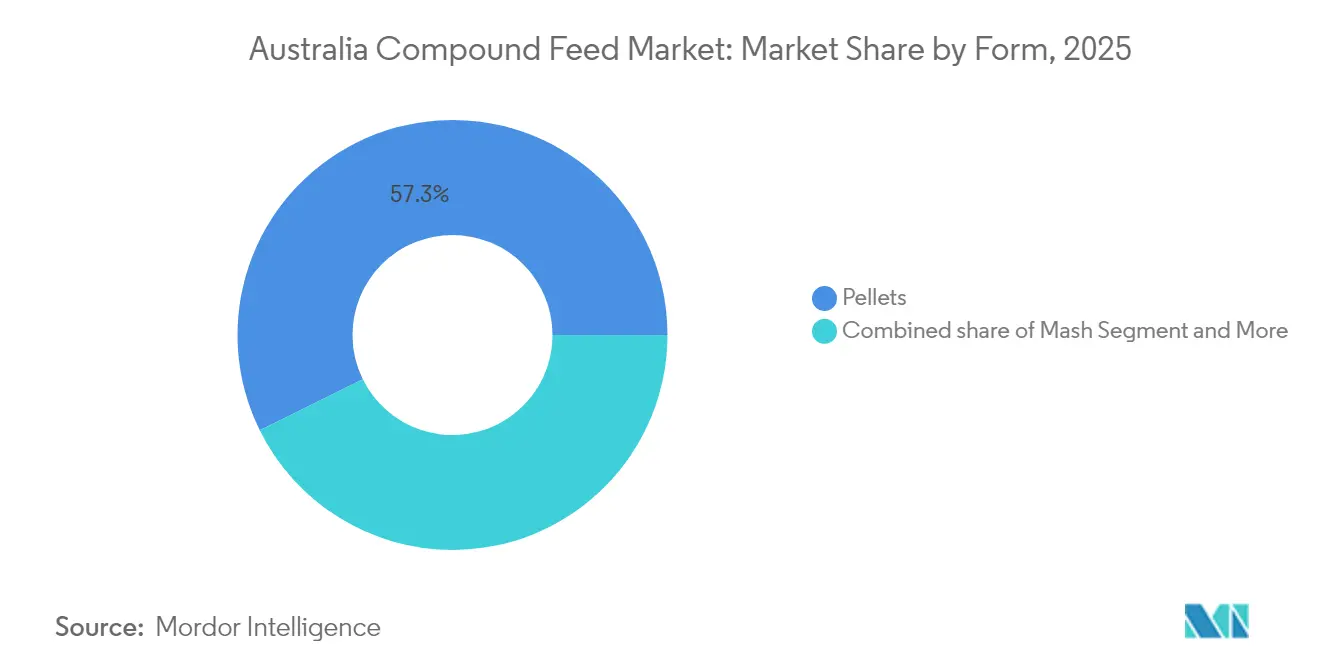

- By form, pellets dominated with a 57.30% share of the Australia compound feed market in 2025, while crumbles are predicted to grow at a 6.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Compound Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising poultry meat consumption | +1.2% | National, strongest in New South Wales and Queensland | Medium term (2-4 years) |

| Rapid expansion of integrated feed–protein conglomerates | +0.9% | National, most pronounced in eastern states | Long term (≥ 4 years) |

| Growth in aquaculture exports | +0.7% | Northern Territory and Queensland coastal zones | Long term (≥ 4 years) |

| Precision-nutrition adoption lowering feed conversion ratios | +0.6% | National, early uptake in intensive systems | Medium term (2-4 years) |

| Surge in alternative grain cultivation | +0.4% | Queensland and northern New South Wales grain belt | Medium term (2-4 years) |

| Government grants for methane-reducing feed additives | +0.3% | National, focus on grazing systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Poultry Meat Consumption

The rise in poultry meat consumption, from 1,376.6 metric tons in 2023 to 1,413.6 metric tons in 2024 (OECD), drives significant demand for compound feeds. In December 2023, poultry value surpassed sheep meat for the first time, reaching AUD 999.8 million (USD 667 million), reflecting a shift in protein preferences.[2]Source: Australian Bureau of Agricultural and Resource Economics and Sciences, “Agricultural Commodities and Trade Data,” Department of Agriculture Fisheries and Forestry, agriculture.gov.au This growth encourages feed millers to invest in enzyme complexes and improve pellet quality, maintaining poultry’s central role in the Australian compound feed market.

Rapid Expansion of Integrated Feed–Protein Conglomerates

Vertical integration strategies by major protein producers create captive feed demand that stabilizes market dynamics while intensifying competition for independent feed manufacturers. Inghams Group and Baiada Poultry's expansion of integrated operations guarantees feed offtake volumes, reducing market volatility but constraining growth opportunities for non-integrated players. Ridley Corporation's AUD 1.28 billion (USD 854 million) revenue in 2024 and strategic acquisition of Oceania Meat Processors demonstrate how feed companies pursue backward integration to secure protein value chains. This integration provides scale economies in feed production, buffers against grain-price volatility, and facilitates precision-nutrition programs across poultry and aquaculture. Independent feed manufacturers face tighter competition as integrated giants lock in volume and negotiate advantaged grain contracts.

Growth in Aquaculture Exports

Commercial aquaculture is shifting from boutique to industrial scale in the Northern Territory and Queensland, spurring demand for specialized high-protein aquafeeds. NSW (New South Wales) aquaculture generated AUD 90 million (USD 60 million) gross value in 2020 and is projected to represent 64% of national seafood output by 2029. Tassal’s USD 65 million Ocean Barramundi project targets 17,500 metric tons annual capacity, requiring feeds that optimize flesh quality and omega-3 profiles. Federal backing for seaweed cultivation supplies marine-derived ingredients for both livestock and aquafeeds, reinforcing a virtuous supply chain loop.

Precision-Nutrition Adoption Lowering Feed Conversion Ratios

Near-infrared sensor platforms technology and automated feeding systems enable real-time ration optimization that reduces feed waste while improving animal performance metrics. AB Vista's NIR technology processes approximately 15,000 spectra monthly, enabling rapid feed analysis and ration adjustments that traditional laboratory testing cannot match for speed and cost efficiency. Digital bunk scanners funded by Meat and Livestock Australia automate ration adjustments in feedlots, cutting waste and improving daily gain. University of Sydney trials confirm sorghum diets can reduce crude protein without sacrificing performance, trimming soybean meal import costs. These technologies collectively nudge the Australia compound feed market toward data-driven efficiency gains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating vegan and flexitarian trends | -0.8% | National, strongest in urban centers | Medium term (2-4 years) |

| Volatility in grain prices due to climactic swings | -0.6% | National, more acute in grain-dependent regions | Short term (≤ 2 years) |

| Biosecurity regulations raising compliance costs | -0.4% | National, greatest burden on small mills | Long term (≥ 4 years) |

| Heightened scrutiny of antibiotic growth promoters | -0.3% | National, concentrated in intensive systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Vegan And Flexitarian Trends

Plant-based protein adoption affects approximately 25% of Australian consumers who actively limit meat consumption, creating headwinds for livestock production and associated feed demand. This consumption pattern particularly impacts younger demographics concentrated in urban centers, where alternative protein adoption rates exceed rural areas by significant margins. Processing infrastructure gaps limit domestic plant protein development, with only one pulse fractionation factory operational through Australian Plant Proteins, constraining local alternative protein supply and maintaining import dependence. The trend creates bifurcated market dynamics where premium livestock products maintain demand while conventional production faces margin pressure from reduced per-capita consumption growth rates.

Volatility In Grain Prices Due to Climactic Swings

El Niño weather amplifies grain-price spikes that compress feed-miller margins. In 2024, GrainCorp’s 1H EBITDA slid to AUD 164 million (USD 109 million) from AUD 383 million (USD 255 million) a year earlier 2023, underscoring the profit risk associated with volume swings and weaker export opportunities. Smaller mills with limited hedging capacity feel the sharpest pinch, incentivizing ingredient diversification and contract farming. Feed manufacturers face margin compression when grain price spikes cannot be immediately passed through to livestock producers, particularly affecting smaller operators with limited hedging capabilities. Climate volatility creates strategic imperatives for supply diversification and alternative ingredient adoption to mitigate price risk exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Poultry Maintains Lead as Aquaculture Surges

Poultry accounted for 42.60% of the Australian compound feed market size in 2025, driven by consistent growth in domestic chicken demand. The poultry segment within the Australian compound feed market benefits from vertically integrated companies that ensure steady offtake and maintain control over feed formulation. During the forecast period, integrated operators are expected to adopt enzyme-rich pellets, optimize amino acid ratios, and refine precision feeding practices to sustain profitable operations.

Aquaculture is projected to post a 7.55% CAGR as barramundi and tuna farms scale up in the Northern Territory and coastal Queensland, necessitating marine-protein-rich diets with fine-tuned lipid ratios. Feed manufacturers are partnering with seaweed producers to improve digestibility and augment omega-3 profiles. Ruminant demand remains stable despite grain-price pressure, while swine demand slows due to subdued pork consumption and heightened disease vigilance.

By Ingredient: Cereals Dominate while Supplements Accelerate

Cereals contributed 66.10% of the Australia compound feed market size in 2025, reflecting entrenched reliance on wheat, barley, and corn. Alternative grain uptake, led by sorghum, mitigates drought risk and constrains raw-material costs. According to the United States Department of Agriculture (USDA), Australian wheat exports reached 24.0 million metric tons in 2024, up 26% year-over-year, creating domestic supply tightness that elevates alternative grain importance for feed manufacturers .

Supplements rise at an 8.05% CAGR owing to government-funded methane-reduction initiatives and precision-nutrition programs. FutureFeed’s Asparagopsis additive drives interest in novel functional ingredients that both lift feed efficiency and curb emissions. Cakes and meals remain vital protein sources, yet soybean meal price volatility drives exploration of local canola and pulses, gradually reshaping formulation economics within the Australia compound feed market.

By Form: Pellets Hold Sway as Crumbles Gain Ground

Pellets captured 57.30% share of the Australia compound feed market in 2025 because of superior handling, reduced wastage, and better feed-conversion performance. Investment in pelleting lines and conditioners by ANDRITZ underscores sustained demand for high-throughput processing equipment.

Crumbles expand at 6.86% CAGR as starter feeds for chicks and fingerlings emphasize digestibility and minimal feed fines. Mash continues to serve dairy and beef producers seeking rapid nutritional adjustments. The ongoing shift to automated feeding augments demand for uniform particle size distribution, reinforcing both pellet and crumble uptake in the Australia compound feed market.

Geography Analysis

Livestock production hubs in New South Wales and Queensland anchor the largest share of the Australia compound feed market, bolstered by proximity to grain origination zones and seaport infrastructure. Poultry complexes near Sydney and Brisbane absorb large volumes of high-density broiler rations.

Victoria’s dairy heartland sustains consistent ruminant feed demand, although margin pressure encourages the use of locally mixed rations that lower delivered cost. Western Australia operates a semi-independent supply chain because of geographic isolation, necessitating higher local grain inclusion and fostering small-scale feed mills.

Northern Territory emerges as the fastest-growing region, driven by state-backed aquaculture expansion and tropical livestock systems requiring heat-tolerant formulations. Tasmania’s premium positioning in free-range and organic production offers niche opportunities for specialized feeds with differentiated ingredient profiles. Diverse state-level biosecurity and transport rules influence sourcing choices and cost structures across the Australia compound feed market.

Regulatory Landscape

Australia's compound feed and feed-ingredient flows are governed by federal biosecurity and import controls administered by the Australian Department of Agriculture, Fisheries and Forestry (DAFF). The Biosecurity Act 2015 underpins import compliance, with importers using the Biosecurity Import Conditions (BICON) system to determine whether goods are permitted, what treatments or certifications apply, and whether a permit is required. Requirements vary by ingredient type and country of origin.

On-farm and mill-level safety is also shaped by species-specific restrictions, most notably the national Ruminant Feed Ban that prohibits feeding Restricted Animal Material (RAM) to ruminants to manage BSE risk. The framework is supported by Animal Health Australia guidance and state enforcement, including Western Australia's DPIRD ruminant feed safety requirements. These rules increase traceability, segregation, and documentation needs for mills handling multi-species rations, as well as for importers sourcing supplements and protein meals from overseas facilities that must meet DAFF facility and questionnaire requirements.

Competitive Landscape

The Australian compound feed market is consolidated with major players, including Ridley Corporation Limited, Inghams Group Limited, Baiada Poultry Pty Limited, Cargill Incorporated, and Riverina (Australia) Pty Limited. Mergers and acquisitions, expansion, product launches, and partnerships are the major business strategies adopted by companies. These top players round out the top tier, each emphasizing vertical integration, processing automation, and new ingredient adoption.

Global agribusinesses such as Cargill Incorporated and Archer Daniels Midland Company continue to invest in local crushing and blending plants to capture value from rising supplement demand. Regional specialists defend niches via tailored formulations and strong farm-gate relationships, focusing on equine nutrition, organic certification, or geographic proximity. Adoption of NIR real-time analytics and digital feeding platforms differentiates technologically advanced players, trimming formulation variance and improving customer margins.

Demand for emissions-reducing additives, antibiotic-free programs, and alternative grains creates white-space entries for innovators like FutureFeed and seaweed cultivators. Consolidation is likely as compliance costs rise and larger mills pursue throughput efficiencies, yet localized competition will persist given Australia’s vast geography and state-based regulatory nuances.

Australia Compound Feed Industry Leaders

Ridley Corporation Limited

Inghams Group Limited

Baiada Poultry Pty Limited

Cargill Incorporated

Riverina (Australia) Pty Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product-mix upgrading is a practical opportunity as intensive systems shift toward higher-value supplements and more differentiated formulations focused on feed efficiency and emissions management. Federal support for methane-reducing additives, including commercialization pathways around Asparagopsis via FutureFeed-linked initiatives, is expanding the addressable space for functional supplements and new ingredient supply chains. At the same time, precision tools such as AB Vista's NIR-driven rapid feed analysis and MLA-funded digital bunk scanning in feedlots are creating demand for consistent, spec-driven pellets and crumbles that can be adjusted in near real time.

Supply security and local substitution are also opening rooms in ingredient sourcing and processing. In March 2026, University of Queensland work on high-protein sorghum highlighted a route to reduce reliance on imported soybean meal in poultry and pig diets. Seasonal tightening in cottonseed availability reported in May 2026 also reinforced the commercial value of alternative grains, contract supply models, and formulation flexibility. Investment into adjacent, high-margin animal nutrition applications, including Symrise breaking ground in June 2026 on a Rutherford, New South Wales facility for pet food palatability and health ingredients, supports broader capacity build-out in premixes and specialty ingredients that can feed into compound feed innovation and procurement programs.

Recent Industry Developments

- June 2026: Symrise broke ground on a Rutherford, New South Wales facility for pet food palatability and health ingredients, enabling broader nutrition capability and potential spillover into premixes and specialty ingredients. The project advances Symrise's regional expansion and strengthens supply of health-oriented ingredients for companion and farm animal products.

- June 2025: Ridley Corporation finalized the divestment of its Wasleys feedmill to Baiada Poultry for AUD 22 million. The transaction strengthens Baiada's vertical integration and shifts a portion of South Australia feed capacity into integrated poultry supply, raising competitive pressure on independent millers serving similar customer segments.

- September 2024: The Australian Government Industry Growth Program awarded SeaStock Pty Ltd funding for a scaled prototype Asparagopsis growth facility feasibility study. This supported domestic capability-building for methane-reducing feed additives, reinforcing the pipeline for supplements adoption and creating procurement opportunities for mills that can incorporate novel functional ingredients.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of compound feed sold in Australia, where feed is formulated by mixing multiple ingredients and additives for livestock nutrition across farm and commercial feeding.

Scope exclusions: The sizing does not count on-farm use of single-ingredient raw materials that are not formulated and sold as compound feed.

Segmentation Overview

- By Animal Type

- Ruminant

- Beef Cattle

- Dairy Cattle

- Other

- Poultry

- Broilers

- Layers

- Turkeys

- Other

- Swine

- Aquaculture

- Fin-fish

- Crustaceans

- Other

- Other Animal Types

- Ruminant

- By Ingredient

- Cereals

- Corn

- Wheat

- Barley

- Sorghum

- Other

- Cakes and Meals

- Soybean Meal

- Canola Meal

- Other

- By-products

- Distillers Dried Grains (DDGS)

- Molasses

- Other

- Supplements

- Vitamins

- Amino Acids

- Enzymes

- Minerals

- Other

- Cereals

- By Form

- Pellets

- Mash

- Crumbles

- Other Forms

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the foundation for the model and to lock the definitions before any numbers were built. We used public statistics and reference material such as the Australian Bureau of Statistics, ABARES, DAFF publications, and feed and grain association websites to map livestock output trends and feed demand direction.

On top of this, import and export trade releases and customs-style datasets were reviewed to sense-check ingredient availability and price movement. Peer-reviewed animal nutrition journals were then used to validate typical inclusion rates and additive adoption timing. Company annual reports, investor presentations, and reputable press were used to cross-check capacity additions, mill utilization commentary, and pricing actions, and a paid subscription focused on company financials and news was referenced where a public split was not clear. The sources listed are illustrative only, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what is actually being sold as compound feed in Australia and how pricing and formulations are changing by species. We spoke with feed manufacturers, ingredient distributors, farm integrators, and large buyers, and the discussions helped close gaps around product form mix, average selling price movement, and demand shifts tied to herd and flock cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 39% |

| Mid tier: 48% | Functional/Unit leaders: 42% | EMEA: 34% |

| Smaller Players: 15% | Managers: 45% | Americas: 27% |

Market-Sizing & Forecasting

The core build starts from a top-down demand pool where livestock headcount and production, typical feed intake, and the share of diets met through commercially formulated feed are used to reconstruct consumption for Australia. Once that demand picture is in place, it is translated into value by applying segment-level pricing logic across major animal groups and common feed forms.

To keep totals realistic, selective bottom-up checks were used, including sampling manufacturer volumes where disclosed, channel feedback on tonnage movement, and spot-checks of price quotes multiplied by estimated volumes. When primary feedback showed gaps in public visibility, the model used ranges for utilization and commercial penetration, then narrowed them through repeat interview follow-ups. Inputs that were actively tracked include grain and oilseed meal price direction, additive inclusion trends (such as functional supplements), shifts in poultry and ruminant production, form preference (pellet versus mash), and drought-driven substitution patterns that impact buying behavior.

Forecasts were produced using scenario analysis because weather, herd rebuilding, and feed grain costs can swing demand quickly. The scenarios were anchored to the most consistent expert expectations gathered in calls. Final growth paths were adjusted only when multiple indicators moved together, such as livestock output signals alongside ingredient price normalization and confirmed buying intent.

Data Validation & Update Cycle

Validation is done in steps so the final number is not driven by a single assumption. We compare model outputs against independent signals like livestock production shifts, trade movement for key inputs, and stated pricing actions, then review variances until the drivers are understood.

If a major mismatch shows up, analysts re-check unit conversions, revisit penetration assumptions by animal type, and re-contact industry participants to confirm whether a real market change occurred. Each report is refreshed annually, with interim updates when material events happen, and a final pre-delivery review is completed so clients receive the most current view available at the time of release.

Mordor Intelligence's Australian Compound Feed Market Sizing Compared With Other Published Estimates

Published market sizes for Australian compound feed can differ even when the topic looks the same, since each publisher may use different base years, currencies, and what they count as compound feed sales. Differences also come from how demand is tied back to livestock cycles, ingredient cost swings, and whether values are reported at manufacturer selling price or closer to retail.

The main gap comes from scope choices around what qualifies as compound feed and when it is counted. Mordor Intelligence treats the market as commercially formulated feed sold for livestock nutrition in Australia, and avoids folding in broader animal feed categories or non-formulated raw inputs. In addition, some estimates lean more on a single base-year value and extend it forward, while others adjust for weather-linked demand, grain and protein meal price movement, and the pace of additive adoption, which can change the value trend year to year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.10 B (2025) | |

| Industry Publisher A | USD 4.95 B (2023) | Uses an earlier valuation year and a different forecast window, and its category treatment appears to mix broader feed coverage with compound feed, which can shift what gets counted and at what selling level. |

| Industry Publisher B | USD 5.20 B (2025) | Reports the market in AUD and converts to USD, so the number can move with exchange-rate timing, and it also presents a wider segmentation lens that can pull in adjacent feed items depending on definitions. |

Taken together, the spread is mainly explained by year selection, currency handling, and whether adjacent feed categories are included alongside compound feed. By keeping the demand build tied to livestock production and intake signals, and then pressure-testing value with pricing and mix checks, the estimate stays traceable to inputs that can be rechecked and repeated.

Key Questions Answered in the Report

What is the expected value of Australia compound feed by 2031?

The market is forecast to reach USD 7.22 billion by 2031, supported by rising poultry and aquaculture feed demand.

Which animal segment drives the largest share of national feed consumption?

Poultry leads with 42.60% share in 2025, underpinned by per-capita chicken intake climbing toward 52 kg.

Why are supplements the fastest-growing ingredient category?

Government incentives for methane-reducing additives and precision-nutrition practices drive an 8.05% CAGR for supplements.

How will biosecurity rules influence smaller feed mills?

Higher compliance fees and complex interstate regulations raise per-ton costs for small mills, accelerating consolidation toward larger operators.

Page last updated on: