Social Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

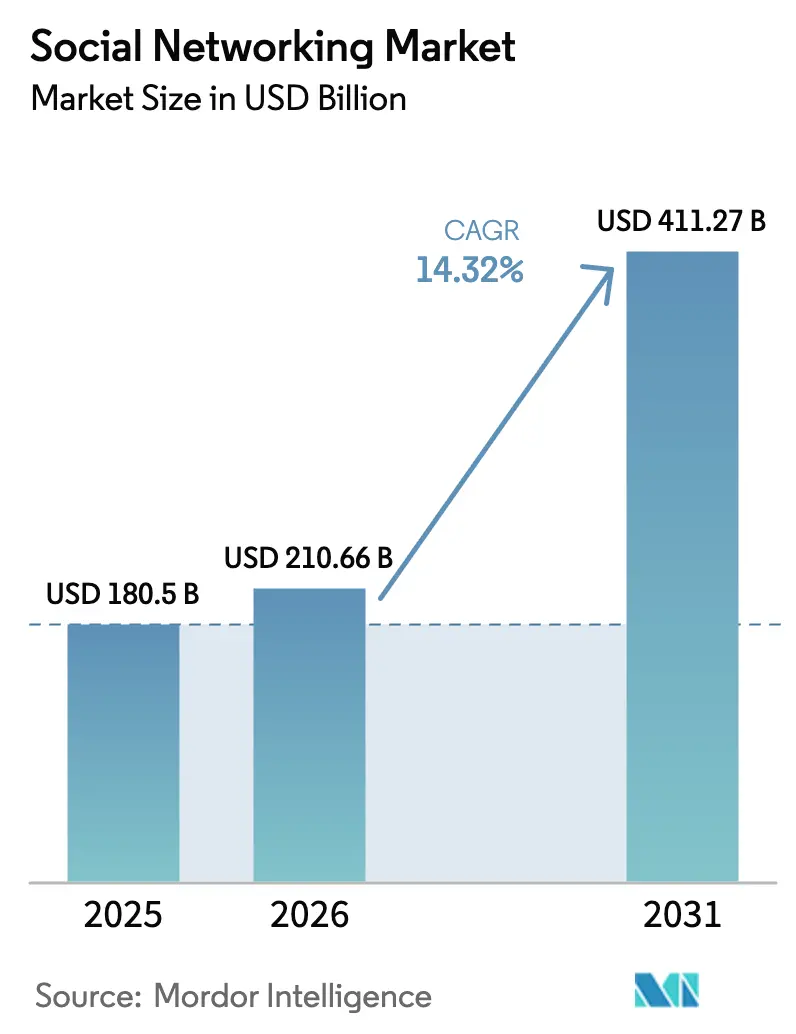

| Market Size (2026) | USD 210.66 Billion |

| Market Size (2031) | USD 411.27 Billion |

| Growth Rate (2026 - 2031) | 14.32% CAGR |

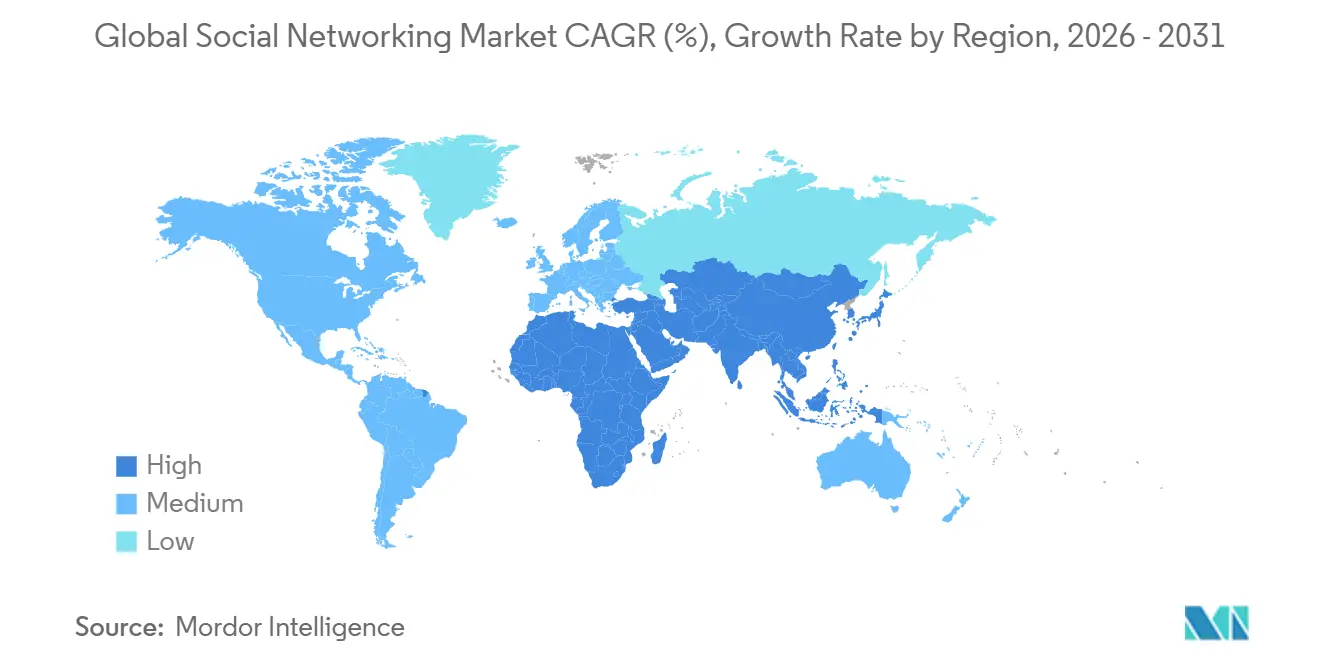

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Social Networking Market Analysis by Mordor Intelligence

The Social Networking Market size is expected to increase from USD 180.5 billion in 2025 to USD 210.66 billion in 2026 and reach USD 411.27 billion by 2031, growing at a CAGR of 14.32% over 2026-2031.

Advertising remains the primary revenue engine, but creator-oriented models such as virtual goods and tipping are scaling quickly as platforms diversify earnings streams. Smartphones account for the bulk of user sessions, yet head-worn displays and smartwatches are opening fresh surface areas for quick, low-friction interactions. Platform fragmentation is intensifying as decentralized networks win funding, while Gen Z engagement shifts toward short-form video and private group messaging. Asia Pacific leads by revenue, the Middle East and Africa posts the fastest growth, and regulatory rulings in Europe, Australia, and the United States are reshaping compliance costs and product design.

Key Report Takeaways

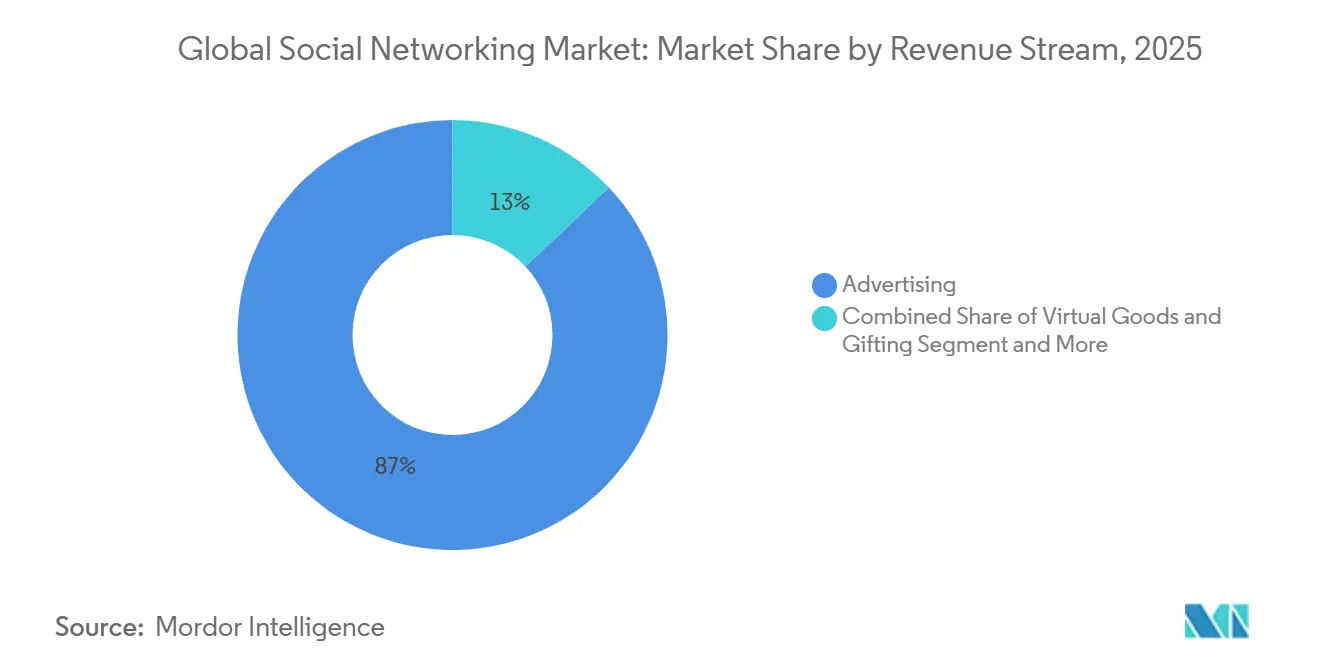

- By revenue stream, advertising commanded 87.03% of global social networking market share in 2025; virtual goods and gifting is advancing at a 14.89% CAGR through 2031.

- By device type, smartphones captured 78.21% of sessions in 2025, while wearables are forecast to expand at a 15.72% CAGR to 2031.

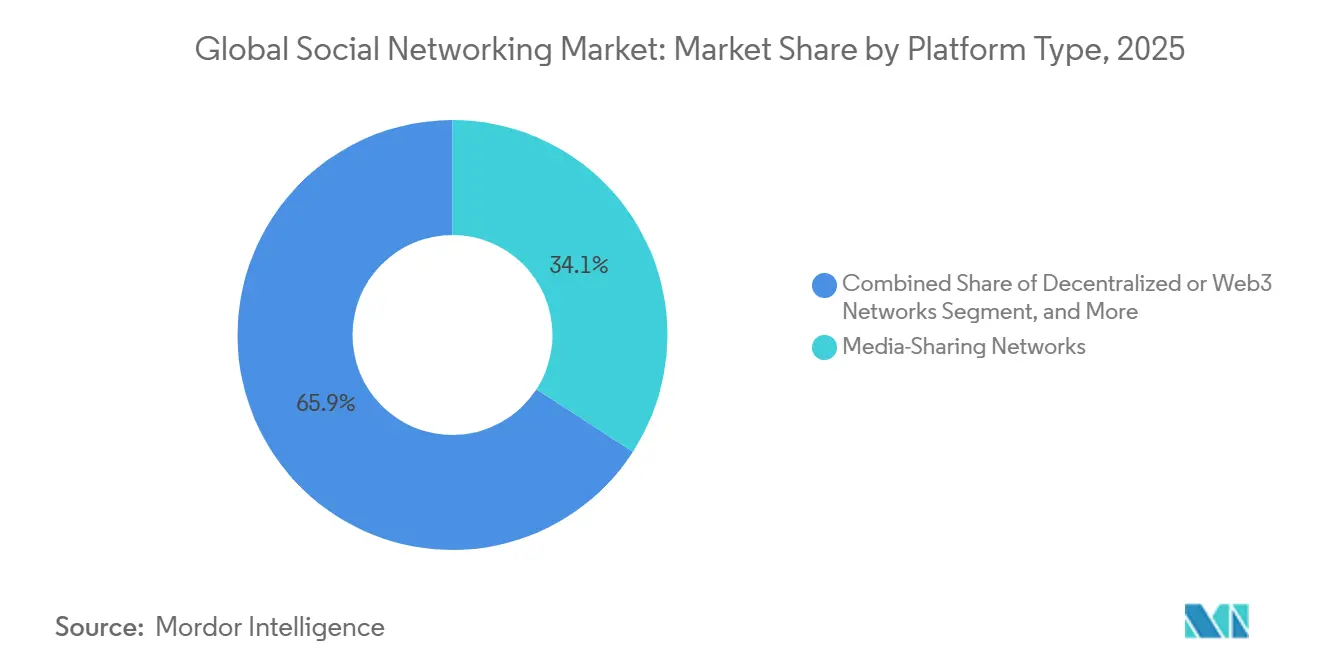

- By platform type, media-sharing networks held 34.14% of 2025 revenue; decentralized networks are projected to grow at a 15.23% CAGR during 2026-2031.

- By user demographic, the 25-34 cohort accounted for 31.44% of active users in 2025; the 13-24 segment is rising at a 16.01% CAGR through 2031.

- By geography, Asia Pacific generated 34.83% of global revenue in 2025, while the Middle East and Africa is on track for a 15.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Social Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Mobile-Internet Penetration | +2.30% | Global, with acceleration in South Asia and Sub-Saharan Africa | Medium term (2-4 years) |

| Surge in Digital Ad Spend on Social Media | +3.10% | North America, Europe, Asia Pacific | Short term (≤ 2 years) |

| Short-Form Video Adoption Across Regions | +2.80% | Global, led by Asia Pacific and Latin America | Short term (≤ 2 years) |

| Expansion of Social Commerce and Live Shopping Tools | +2.50% | Asia Pacific core, spill-over to Middle East and North America | Medium term (2-4 years) |

| Decentralized Social Protocols and Blockchain ID Adoption | +1.40% | North America and Europe early adopters, Asia Pacific following | Long term (≥ 4 years) |

| Synthetic-Media Influencers Unlocking New Engagement Models | +1.20% | Global, with brand partnerships concentrated in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Mobile-Internet Penetration

Global smartphone users reached 5.7 billion in 2025, and 5G subscriptions crossed 1.9 billion connections, lifting average monthly data use to 25 gigabytes in developed markets.[1]GSMA Intelligence, “Global Mobile Trends,” gsma.com First-time internet access now occurs primarily through budget Android handsets, with India alone adding 120 million smartphone users during 2023-2025.[2]McKinsey and Company, “Digital Trends in Emerging Markets,” mckinsey.com Platforms that bundle lite apps and 3G-fallback modes win share in bandwidth-constrained regions, as illustrated by the Philippines’ daily average of 3 hours 32 minutes on social media in 2025. These conditions reinforce the global social networking market’s ability to reach new users without desktop dependence.

Surge in Digital Ad Spend on Social Media

Instagram supplied more than half of Meta’s United States advertising revenue in 2025 as brands redirected budgets to Stories, Reels, and Shop tabs that merge content discovery with checkout.[3]“Meta Reports Third Quarter 2025 Results,” Meta Platforms, investor.fb.com Machine-learning models lowered cost-per-acquisition on Meta platforms by 18% year over year, validating performance-first budget allocations. Snap logged USD 1.5 billion in third-quarter 2025 revenue, with augmented-reality lenses driving 22% of impressions and 30% higher click-through rates than static units. Spending momentum supports sustained monetization across the global social networking market.

Short-Form Video Adoption Across Regions

TikTok users in Southeast Asia averaged 45 hours per month on the app in 2025, surpassing YouTube’s 38 hours and Instagram’s 29 hours. Algorithmic feeds give micro-creators with fewer than 10,000 followers outsized reach, fuelling a 79% jump in creator-economy payouts during 2025. Instagram Reels and YouTube Shorts together engaged 2.1 billion monthly users in 2025, compelling legacy platforms to prioritize vertical video. The format’s stickiness underpins robust user-time growth for the global social networking market.

Expansion of Social Commerce and Live Shopping Tools

United States social-commerce sales grew from USD 31.7 billion in 2023 to USD 67.8 billion in 2026, propelled by one-click checkout and influencer-led streams. China’s gross merchandise value reached CNY 4.9 trillion (USD 680 billion) in 2024, with Douyin and Kuaishou commanding 58% of activity. The United Arab Emirates recorded a 73% social-commerce conversion rate in 2025, the highest outside Asia. Live shopping strengthens the revenue depth of the global social networking market beyond ads.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Data-Privacy and Security Regulations | -2.10% | Europe and North America, with Asia Pacific adopting similar frameworks | Short term (≤ 2 years) |

| Global Antitrust Scrutiny of Dominant Platforms | -1.60% | North America and Europe, with spillover to Asia Pacific | Medium term (2-4 years) |

| User-Attention Saturation and Engagement Fatigue | -1.30% | Global, most pronounced in North America and Europe | Medium term (2-4 years) |

| Algorithmic Bias and Misinformation Hurting Brand Safety | -1.10% | Global, with heightened sensitivity in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Data-Privacy and Security Regulations

The European Union fined Meta EUR 251 million (USD 268 million) in 2024 for GDPR breaches, lifting cumulative penalties to EUR 1.2 billion (USD 1.28 billion) since 2018. Australia’s under-16 access ban, effective 10 December 2025, forces platforms to deploy age-verification layers and accept AUD 49.5 million (USD 32.7 million) breach risks. Compliance investments in data localization, consent management, and audits elevate cost structures across the global social networking market.

Global Antitrust Scrutiny of Dominant Platforms

A United States federal judge ruled in 2024 that Google maintained an illegal monopoly in online search and advertising. Parallel probes in the United Kingdom and European Union pressure Meta and ByteDance to open application programming interfaces and embrace data portability. These proceedings inject uncertainty into merger pipelines and could force structural remedies that dilute network effects in the global social networking market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Revenue Stream – Advertising Weight Faces Diversification Push

Advertising generated 87.03% of 2025 revenue, confirming its outsized influence on the global social networking market. Meta booked USD 50.1 billion in third-quarter 2025 ad sales after algorithmic tweaks cut cost-per-click, helping advertisers secure sub-USD 5 acquisition costs. The global social networking market size tied to ad spend still dwarfs other levers, but risk exposure is growing.

Virtual goods and gifting are the fastest-rising stream, advancing at a 14.89% CAGR through 2031. TikTok’s USD 2.5 billion creator payouts in 2024 illustrate how direct user-to-creator payments can scale without gatekeeper ad exchanges. Subscriptions are gaining relevance, with Snapchat+ delivering USD 150 million in quarterly revenue from 17 million users. The revenue remix reduces cyclicality in the global social networking industry and unlocks predictable cash flow.

By Device Type – Wearables Add Ambient Access Points

Smartphones retained 78.21% of user sessions in 2025, cementing their role as the dominant interface for the global social networking market. Tablets and desktops held modest shares linked to long-form video and professional networking.

Wearables and “other” form factors, however, are projected to post a 15.72% CAGR to 2031. Meta’s Messenger integration into Quest headsets and broader smartwatch notification ecosystems allow quick replies and voice-to-text input. For the global social networking market size attributed to wearables, cross-device sync and low-latency identity management remain gating factors, but adoption in high-income regions signals a shift toward always-on ambient networking.

By Platform Type – Decentralized Networks Break Walled Gardens

In 2025, media-sharing networks led by Instagram, TikTok, and YouTube accounted for 34.14% of total revenue. While messaging apps, professional networks, and niche communities maintain dedicated followings, decentralized Web3 protocols are projected to grow at a 15.23% CAGR through 2031.

In 2024, Lens Protocol and Farcaster collectively secured USD 77 million, supporting user-owned social graphs that challenge traditional lock-in models. Although Web3's slice of the global social networking market remains modest, its upward momentum is compelling established players to adapt, notably by opening APIs and enhancing portability.

By User Demographic – Gen Z Alters Engagement Metrics

In 2025, users aged 25-34 made up 31.44% of active users, significantly boosting premium subscriptions on platforms like LinkedIn and Snapchat+. This demographic's professional focus and purchasing power have made them a key target for platforms aiming to monetize through premium offerings. Meanwhile, the 13-24 age group, the fastest-growing segment, is expanding at a 16.01% CAGR.

Their strong preference for short-form videos and private messaging is driving platforms to adapt by prioritizing engagement metrics such as 'watch time' and 'message count' over traditional metrics like 'likes'. This shift reflects the evolving user behavior and the need for platforms to stay relevant in a competitive market. Additionally, with Gen Z increasingly normalizing AI-generated content, synthetic influencers are expected to gain a stronger foothold in the global social networking landscape, reshaping how brands and users interact within these platforms.

Geography Analysis

Asia Pacific produced 34.83% of 2025 revenue, powered by China’s super-app ecosystems and India’s 120 million new smartphone users added during 2023-2025. TikTok usage in Southeast Asia exceeded 45 hours per month, and Indonesia devoted 42.6% of online time to social media. The global social networking market size attributable to the region is poised for further upticks as vernacular interfaces and integrated payments deepen adoption.

The Middle East and Africa is forecast to register a 15.81% CAGR through 2031, the fastest globally. Saudi Arabia’s social-media penetration reached 111% in 2025, while the United Arab Emirates posted a 73% social-commerce conversion rate. Data-center buildouts under Vision 2030, worth USD 2.7 billion, reduce latency for live shopping and augmented reality, widening monetization capacity.

North America and Europe remain income leaders thanks to high average revenue per user, but their mature user bases mean single-digit growth. Regulatory expenses linked to GDPR, CCPA, and pending antitrust actions temper margins. South America and Africa boast faster user-base expansion; Brazil’s penetration crossed 70% in 2025, and Nigeria’s youthful demographics present large upside, yet monetization trails due to infrastructure gaps and lower disposable income. Australia’s under-16 ban illustrates how regional regulation can curtail reachable audiences in otherwise high-value markets.

Competitive Landscape

Meta Platforms dominates daily active people at 3.43 billion in third-quarter 2025 and leverages unified ad buying across Facebook, Instagram, WhatsApp, and Messenger. Alphabet’s YouTube remains the largest long-form video hub, while ByteDance’s TikTok paid USD 2.5 billion to creators in 2024 to secure supply. Together, the top three players capture the majority of ad spend flowing through the global social networking market.

Second-tier contenders focus on niche intensity rather than scale. Telegram turned its first profit in 2024 with USD 1 billion in revenue, validating a premium-feature subscription path. Discord filed confidentially for an initial public offering in December 2025, revealing 231 million monthly active users and USD 725 million in annual recurring revenue, 54% of which comes from non-gaming communities. Reddit, LinkedIn, and regional champions such as Kuaishou and Line add further fragmentation.

White-space innovation clusters around decentralized networks, professional micro-communities, and synthetic influencer tooling. Lens Protocol and Farcaster exemplify funding momentum behind user-owned graphs. Meanwhile, Meta’s 2024 launch of Meta Verified and Snap’s premium tier underscore the pivot to recurring revenue streams. Machine-learning investments, particularly in content recommendation and ad targeting, remain key competitive differentiators, though looming interoperability mandates could blunt proprietary data advantages.

Social Networking Industry Leaders

YouTube

ByteDance

Meta

Snap Inc.

Pinterest Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Federal Trade Commission began litigation seeking Meta’s divestiture of Instagram and WhatsApp.

- November 2024: The ITU confirmed global internet penetration hit 68% with 5.5 billion users, spotlighting expansion opportunities.

- March 2024: India’s digital-ad spend reached INR 40,800 crore (USD 4.9 billion), with social capturing 30%.

- February 2024: The GSMA reported 4.7 billion mobile-internet users and commercial 5G in 101 countries

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the social networking market as all revenue earned worldwide by online platforms that let people create profiles, build connections, share multimedia, and interact in real time. It counts advertising, premium features, in-app purchases, and virtual gifts delivered through mobile apps or browsers.

Scope exclusion: we do not track enterprise collaboration suites or standalone email services.

Segmentation Overview

- By Revenue Stream

- Advertising

- In-App Purchases

- Subscriptions

- Virtual Goods and Gifting

- By Device Type

- Smartphone

- Tablet

- Desktop or Laptop

- Wearable and Others

- By Platform Type

- Traditional Social Networks

- Media-Sharing Networks

- Messaging or Communication Apps

- Professional Networks

- Niche and Interest-Based Networks

- Decentralized or Web3 Networks

- By User Demographics (Age Group)

- 13-24 Years

- 25-34 Years

- 35-44 Years

- 45+ Years

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Southeast Asia

- Australia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with product leads at large networks, regional ad agencies, creator-economy tool vendors, and privacy counsel across North America, Europe, and fast-growing Asian markets. These conversations confirmed ARPU trajectories, ad-fill rates, and likely regulatory inflection points that secondary data alone could not reveal.

Desk Research

Public data anchors our desk work. Analysts review ITU connectivity tables, telecom regulator yearbooks, Interactive Advertising Bureau ad-spend trackers, and Form 10-K revenue splits. User-base disclosures from platform transparency centers, plus patents indexed on Questel, show how monetization may shift.

Dow Jones Factiva news wires and D&B Hoovers financials help cross-check emerging players and pricing moves, while statistics portals in China, India, and Brazil supply device-ownership and wage trends that shape affordability assumptions. Trade notes from GSMA and the World Federation of Advertisers round out the picture; many additional sources are consulted for validation.

Market-Sizing & Forecasting

We first reconstruct market value with a top-down approach that scales global digital-ad spend, in-app payments, and virtual-gift flows by disclosed platform splits, then adjusts for cross-device duplication. Select bottom-up checks, sampling regional monthly active users and blending them with surveyed ARPU, keep totals grounded. Key variables include smartphone penetration, social-ad CPM, average session time, privacy-penalty outlays, and creator-payout ratios; they feed a multivariate regression that produces the forecast. Adoption of emerging decentralized networks is bracketed through scenario analysis to bridge data gaps.

Data Validation & Update Cycle

Our team runs three layers of peer review, and any variance beyond five percent triggers fresh source checks. Outputs are compared with signals such as App Store grossing ranks and regulatory fee collections before sign-off. Reports refresh every twelve months, with interim updates whenever major policy changes or platform disclosures occur.

Why Our Social Networking Baseline Earns Decision-Makers' Trust

Published estimates often diverge because firms draw different lines around what counts as network revenue and which devices they total.

Key gaps arise when desktop usage is excluded or social-commerce gross merchandise value is folded into platform sales; slower refresh cycles and differing currency conversions amplify the spread.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 95.80 B (2025) | Mordor Intelligence | |

| USD 60.81 B (2023) | Global Consultancy A | App-only coverage, excludes browser revenue |

| USD 46.32 B (2024) | Industry Research B | Emerging-market focus, omits virtual-goods monetization |

| USD 98.37 B (2025) | Trade Journal C | Mobile-only ARPU uplift, no ad-fill cross-check |

The comparison shows that scope choices, not data scarcity, drive most variance. By anchoring our baseline on clearly stated revenue streams, transparent variables, and annual refreshes, Mordor Intelligence delivers a balanced, traceable benchmark clients can rely on.

Key Questions Answered in the Report

How large is the global social networking market in 2026?

The market generated USD 210.66 billion in revenue in 2026, on track for USD 411.27 billion by 2031 at a 14.32% CAGR.

Which revenue stream is growing fastest?

Virtual goods and gifting is forecast to expand at a 14.89% CAGR through 2031 as platforms embed tipping and digital collectibles.

What device category will see the highest growth?

Wearables, including smartwatches and head-worn displays, are expected to post a 15.72% CAGR during 2026-2031.

Which region leads market revenue?

Asia Pacific contributed 34.83% of global revenue in 2025, driven by China's super-app ecosystems and Indias rising smartphone base.

How are data-privacy regulations affecting the sector?

Cumulative GDPR and Digital Services Act fines exceeding USD 2 billion and Australia's under-16 access ban illustrate higher compliance costs and stricter user-age verification.

Who are the dominant players?

Meta Platforms, Alphabet, and ByteDance capture the majority of global ad spend, while Telegram, Discord, and emerging decentralized networks provide competitive pressure.

Page last updated on: