Slickline Logging Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

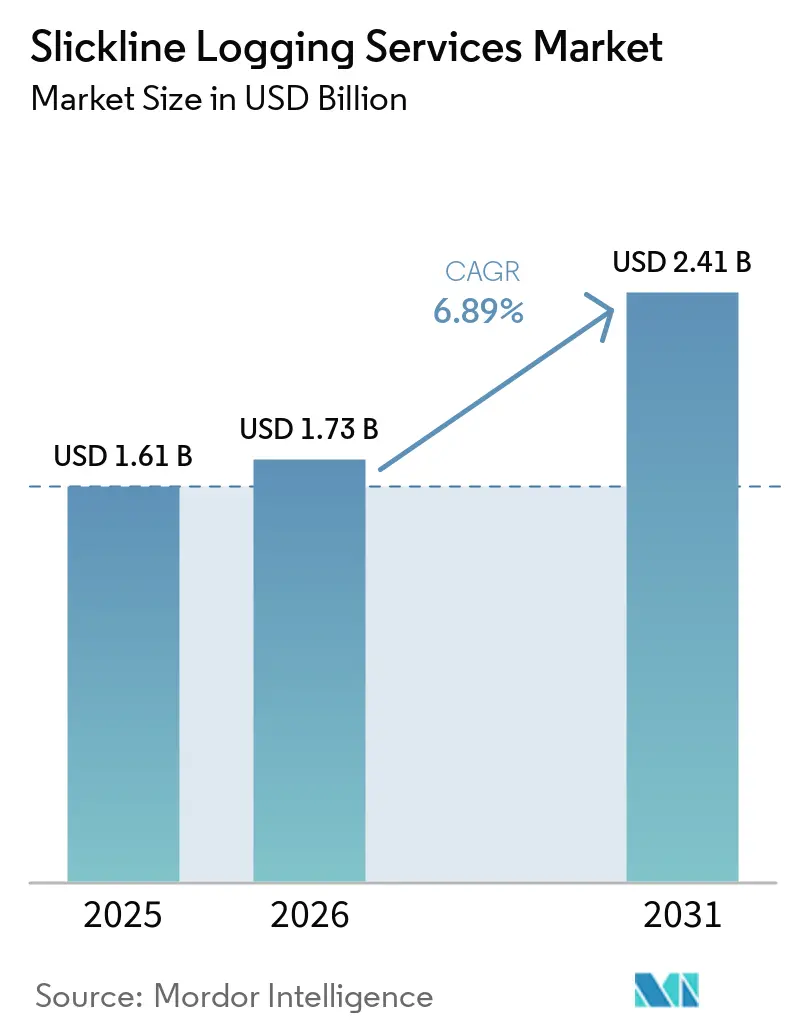

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 6.89% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Slickline Logging Services Market Analysis by Mordor Intelligence

The Slickline Logging Services Market size is projected to be USD 1.61 billion in 2025, USD 1.73 billion in 2026, and reach USD 2.41 billion by 2031, growing at a CAGR of 6.89% from 2026 to 2031.

Escalating deep- and ultra-deepwater projects are generating larger per-well budgets for high-specification slickline tools, while mature onshore basins continue to underpin recurring intervention volumes. National oil companies (NOCs) are bundling slickline into multi-service tenders that favor contractors with integrated portfolios, accelerating revenue visibility for the slickline logging services market. Digital telemetry is converting slickline from a batch-data service into a live reservoir-management backbone, compressing decision cycles and raising tool utilization.[1]ADNOC, “Well Digitalization Award,” adnoc.ae At the same time, workforce attrition and new methane-monitoring rules are elevating demand for autonomous systems that limit on-site personnel and streamline compliance reporting. Finally, landmark mergers completed in 2024 have shrunk the supplier base, tilting bargaining power toward a handful of integrated majors that can deploy slickline, coiled tubing, and wireline from a single mobilization.

Key Report Takeaways

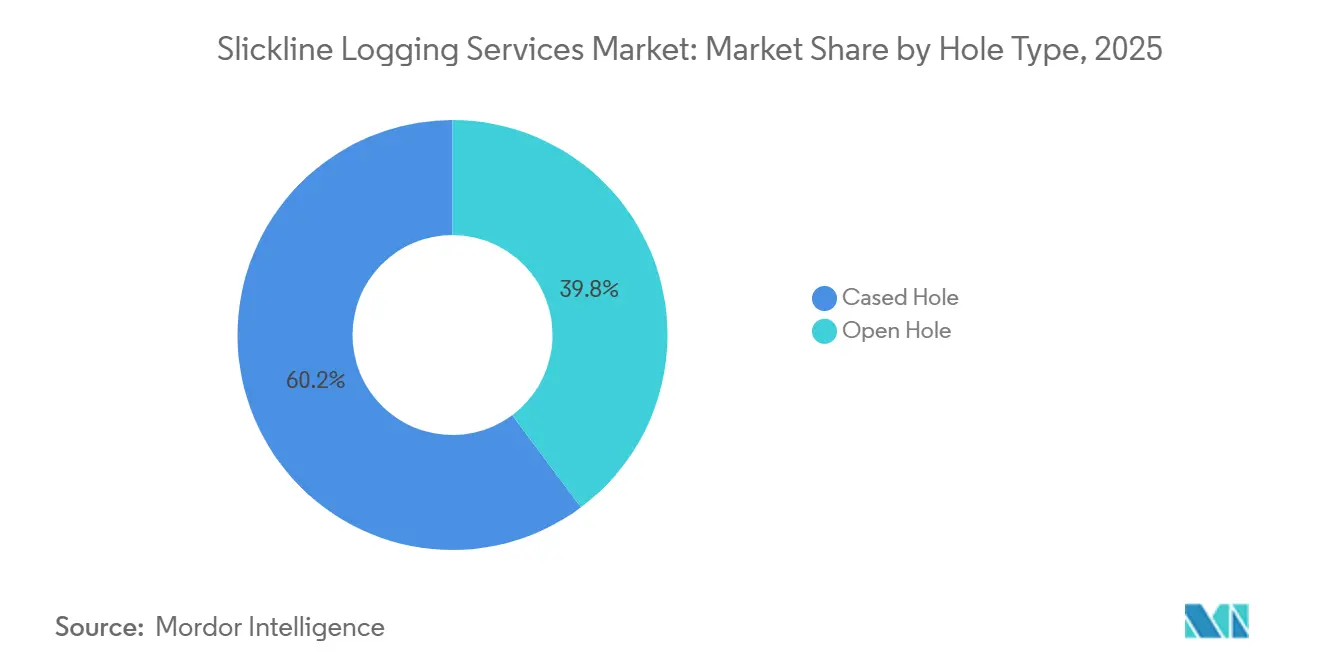

- By hole type, cased-hole operations led with 60.2% slickline logging services market share in 2025, and the same is expected to expand at a 7.1% CAGR through 2031.

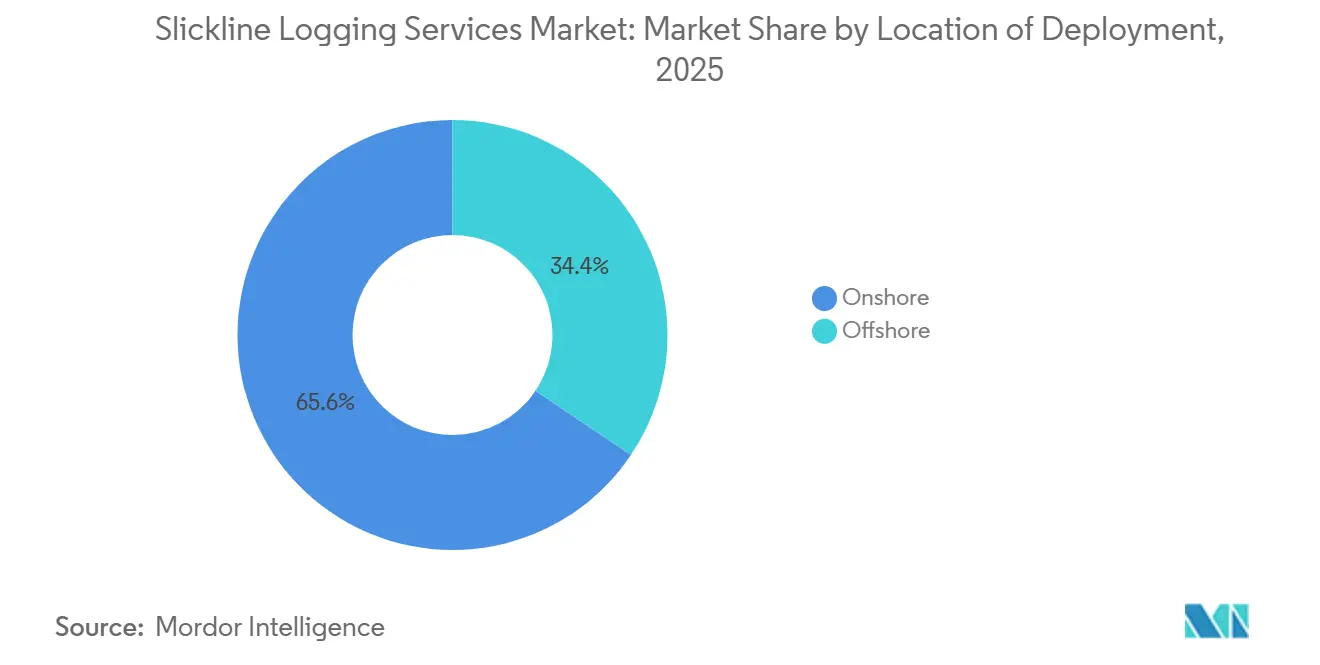

- By deployment location, onshore held 65.6% of the slickline logging services market size in 2025, while offshore is projected to grow at 7.5% CAGR through 2031.

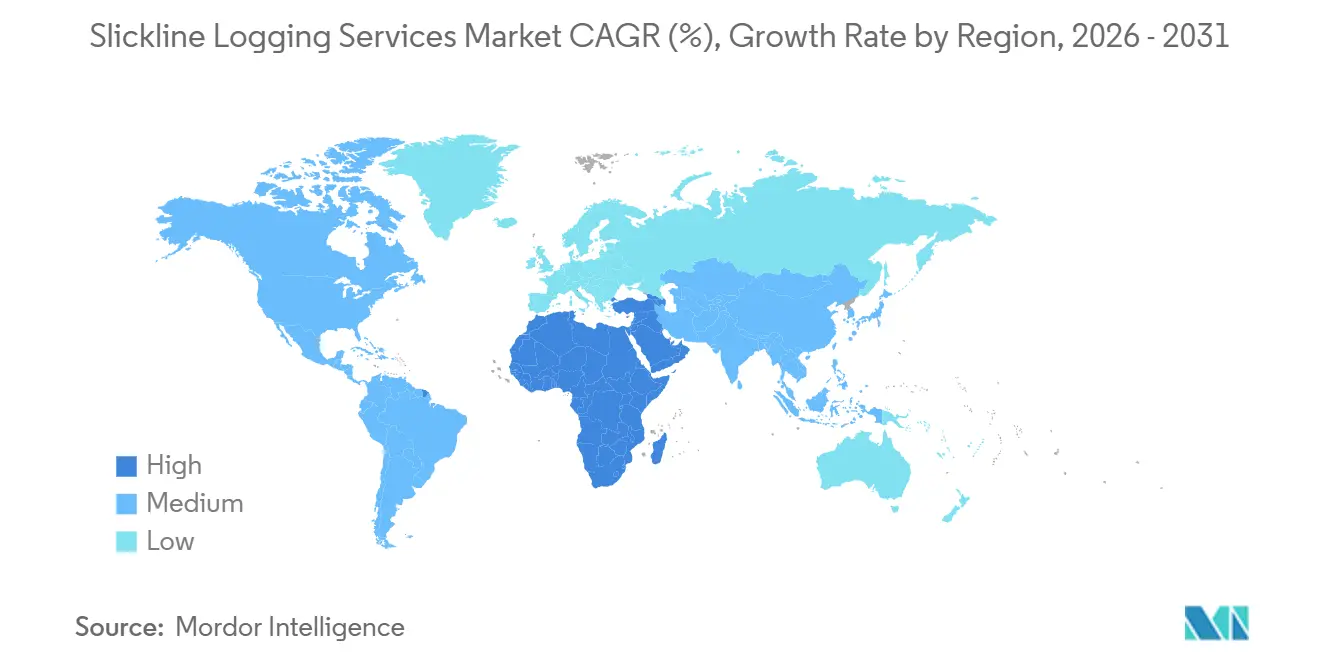

- By geography, North America commanded 38.5% revenue in 2025, while the Middle East and Africa region is expected to grow at a 7.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Slickline Logging Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained offshore deep- & ultra-deepwater drilling upcycle | 1.8% | Middle East & Africa, South America (Brazil pre-salt), Asia-Pacific (Indonesia, Malaysia, Australia) | Medium term (2-4 years) |

| Rising well-intervention spend on aging wells | 1.5% | Global, with concentration in North America (Gulf of Mexico, Permian), Middle East (Saudi Arabia, Kuwait, Oman) | Long term (≥ 4 years) |

| Rapid adoption of digital slickline platforms | 1.2% | Global, early adoption in North America, Europe (North Sea), Middle East NOCs | Short term (≤ 2 years) |

| Shale/tight-oil re-frac programs driving frequent interventions | 1.0% | North America (Permian Basin, Eagle Ford, Bakken), Argentina (Vaca Muerta) | Medium term (2-4 years) |

| NOCs bundling slickline into integrated service tenders | 1.0% | Middle East (Saudi Arabia, UAE, Kuwait, Oman), South America (Brazil, Colombia), Asia-Pacific | Medium term (2-4 years) |

| CCS pilot wells needing low-invasion logging solutions | 0.6% | North America (Alberta, Wyoming, Texas), Europe (North Sea), Middle East (UAE, Saudi Arabia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustained Offshore Deep- and Ultra-Deepwater Drilling Upcycle

Ultra-deepwater programs in Brazil, Indonesia, and the North Sea require extended well laterals and complex completions that drive multiple slickline runs per well.[2]Halliburton, “Petrobras Offshore Contract,” halliburton.com Petrobras awarded Halliburton a multi-year intervention contract in 2024 covering two-thirds of its offshore assets, embedding slickline for bridge-plug setting in pre-salt wells where depths exceed 6,000 ft and pressures surpass 15,000 psi.[3]Petrobras, “Pre-Salt Operations Update,” petrobras.com.br In Indonesia, SLB secured the Tangkulo deepwater scope in 2026 that couples slickline logging with subsea completion hardware for HP/HT environments.[4]SLB, “Stream Telemetry Launch,” slb.com Equinor’s renewed Transocean rig leases in the North Sea extend slickline demand on mature fields such as Troll to monitor water breakthrough and optimize lift. The International Energy Agency estimates that 35% of global upstream spending will be offshore by 2025, structurally favoring providers able to furnish deepwater-rated slickline assemblies.

Rising Well-Intervention Spend on Aging Wells

More than 70% of global oil now flows from fields discovered before 2000, where decline rates reach 8% annually in the absence of targeted interventions. Slickline’s low-cost mechanical isolation and production logging make it the first-line option for restoring output in mature assets. Saudi Aramco’s five-year Jafurah program pairs slickline with coiled tubing to evaluate fracture connectivity across 10,000-ft laterals. In the U.S. Gulf of Mexico, operators deploy slickline to retrofit gauges in aging subsea tiebacks, feeding real-time pressure data into reservoir simulators and postponing costly workovers. Kuwait Oil Company bundled slickline into its USD 1.5 billion Mutriba contract, targeting incremental barrels from fields onstream for over 40 years.

Rapid Adoption of Digital Slickline Platforms

Fiber-optic telemetry now streams downhole data at rates above 1 Mb/s, letting engineers adjust interventions in real time rather than after tool retrieval. SLB’s Stream platform, launched in 2024, identified fluid contacts on the fly in the North Sea, cutting decision cycles from two days to two hours. Baker Hughes’ iCruise system reduced stuck-tool incidents 25% during 2025 Permian trials, saving operators USD 30,000 per intervention on average. ADNOC is wiring 2,000 wells with permanent sensors that handshake with slickline telemetry to create full-field digital twins. Halliburton’s DecisionSpace 365 cloud now ingests slickline alongside drilling logs, letting asset teams triage intervention candidates based on predictive analytics instead of fixed schedules.

NOCs Bundling Slickline into Integrated Service Tenders

Petrobras structured its 2024 intervention tender so that bids must include slickline, coiled tubing, and P&A services in one package, effectively limiting competition to the integrated majors. Oman’s PDO granted NESR a USD 200 million five-year slickline award nested inside a broader framework that includes wireline and pressure pumping, unlocking volume discounts and streamlined logistics. Saudi Aramco expanded Baker Hughes’ coiled-tubing fleet from four to ten units in 2024, with contractual provisions for slickline support on unconventional gas wells, minimizing idle rig time. Such bundling compresses margins for standalone specialists and pushes them toward M&A or technology differentiation, as seen in Weatherford’s dual acquisitions of Expro and Altus.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price volatility curbing upstream CAPEX | -0.8% | Global, with acute sensitivity in North America shale, West Africa, UK North Sea | Short term (≤ 2 years) |

| Tightening HSE & emissions regulations on intervention fluids | -0.4% | North America (EPA jurisdiction), Europe (EU Methane Regulation), UK North Sea | Medium term (2-4 years) |

| Global shortage of certified slickline crews | -0.5% | Middle East (Saudi Arabia, UAE, Kuwait), North America (Permian, Gulf of Mexico), North Sea | Medium term (2-4 years) |

| Emergence of autonomous down-hole robots post-2030 | -0.3% | Global, with early commercial deployment in North Sea, Gulf of Mexico, Middle East offshore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Volatility Curbing Upstream CAPEX

WTI fluctuated between USD 70–90 per bbl during 2024-2025, pushing North American independents to defer non-core interventions and only fund wells with sub-12-month paybacks. Harbor Energy and EnQuest trimmed 2024 North Sea budgets after the UK preserved its 75% Energy Profits Levy, rendering many slickline jobs uneconomic below USD 80 Brent. Service companies are countering by offering production-linked pricing that shares commodity risk and stabilizes utilization during downturns.

Global Shortage of Certified Slickline Crews

The Society of Petroleum Engineers warns that 40% of petroleum professionals can retire this decade, while certification for slickline supervisors takes three-to-five years. Middle Eastern NOCs expanding unconventional portfolios now compete for the same labor pool, inflating daily crew rates by double digits. Welltec’s Autonomous Well Intervention System, proven in 2024 North Sea trials, trimmed crew size from five to three, but regulators have yet to sanction fully uncrewed operations in HP/HT wells. Until automation scales, crew shortages will cap deployment speed in the slickline logging services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hole Type: Cased-Hole Operations Sustain Mature-Field Economics

Cased-hole work accounted for 60.2% slickline logging services market share in 2025 and will expand at a 7.1% CAGR through 2031. This dominance reflects a pivot toward optimizing production from wells already lined with casing, where slickline executes production logging, perforating, bridge-plug placement, and mechanical isolation tasks critical for water-cut control and gas-lift tuning. The slickline logging services market size for cased-hole projects is expected to reach USD 1.46 billion by 2031, supported by Saudi Aramco’s multi-year Jafurah program and Kuwait’s Mutriba rejuvenation plan. Digital telemetry now delivers live casing-pressure and temperature data, letting engineers decide on subsequent runs without pulling the tool, which lifts asset uptime. Regulatory pressure boosts demand too, as the EPA’s 2024 methane rule mandates well-integrity checks that often rely on slickline-deployed gauges.

Open-hole slickline retains a vital role in ultra-deepwater appraisal, where operators collect formation-pressure points before cementing casing strings. Petrobras uses open-hole tools in Santos Basin wells drilled to 20,000 ft total depth with bottomhole temperatures of 300 °F, where traditional wireline tools risk failure. SLB’s Stream system now transmits both cased- and open-hole data in one string, blurring historic boundaries and allowing real-time decisions on casing design while the tool is still downhole. As CCS pilots multiply, open-hole slickline could gain share by verifying seal integrity before the injection tubing is landed.

By Location of Deployment: Offshore Growth Outpaces Onshore Scale

Onshore projects delivered 65.6% of the slickline logging services market size in 2025, anchored by high-volume shale re-fracturing in the Permian and mature Middle Eastern fields. Yet offshore interventions are expanding at the fastest 7.5% CAGR through 2031. Deepwater wells command two-to-three times higher slickline day rates because of stringent pressure ratings and rig logistics. Petrobras’s pre-salt contract covers 6,000-ft water depths and integrates slickline with plug-and-abandonment work, highlighting the premium offshore scope. SLB’s Tangkulo award in Indonesia bundles telemetry-enabled slickline within subsea completions for HP/HT reservoirs.

Onshore activity remains resilient in the Permian, Eagle Ford, and Bakken, where Baker Hughes reported a 25% uptick in 2025 re-frac slickline runs, each well requiring multiple isolations before new fracture stages. In Saudi Arabia, onshore wells with 80% water-cut still need slickline-deployed separation sleeves to prolong life. Offshore’s share is likely to accelerate if floating production systems take off in West Africa and Southeast Asia, where every new subsea tree demands intervention-ready wellheads that accommodate slickline without riser disconnects.

Geography Analysis

North America led with 38.5% revenue in 2025, but growth is moderating as shale producers pivot from output growth to cash-flow discipline. Upstream CAPEX in the U.S. dipped 8% during 2024 despite WTI averaging USD 78 per bbl, trimming discretionary slickline budgets. Canada’s emerging CCS fleets, such as Shell’s Quest project, are generating fresh slickline demand for pressure surveillance on injection wells. Mexico’s Pemex is preparing shallow-water tenders in the Bay of Campeche, yet faces funding uncertainty that may delay awards past 2026.

The Middle East and Africa region is the fastest grower at a 7.2% CAGR to 2031, lifted by ADNOC’s USD 920 million well-digitalization drive and Saudi Aramco’s Jafurah unconventional gas push. Kuwait’s USD 1.5 billion Mutriba package couples slickline with fracturing to recover incremental barrels from 40-year-old fields. Nigeria and Egypt are ramping up deepwater tiebacks that require high-pressure slickline assemblies compatible with subsea trees. Geopolitical volatility poses headline risk, but integrated multi-service awards give contractors a hedge against single-well cancellations.

Europe maintains steady demand anchored in the North Sea, where Equinor’s Troll and Johan Sverdrup programs rely on slickline to manage water ingress and optimize lift. The UK’s 75% Energy Profits Levy is constraining independent budgets, lowering run frequency when Brent prices sink below USD 80 bbl. Norway’s CO₂ storage licensing round could inject new volumes by mandating slickline monitoring of injection wells.

Asia-Pacific growth hinges on China’s Bozhong field, Australia’s Scarborough LNG, and Malaysia’s deepwater Kikeh extension. CNOOC uses slickline to measure pressure in 15,000-ft subsea wells, while Woodside deploys tools to regulate gas-lift valves in Scarborough’s dry-gas fields. South America’s upside remains centered in Brazil’s pre-salt, where each FPSO supports 20-30 subsea producers that need scheduled slickline runs for tubing retrieval and plug setting.

Competitive Landscape

The slickline logging services market is semi concentrated. SLB, Halliburton, and Baker Hughes collectively hold roughly 55% global revenue, while Weatherford vaulted into fourth place after buying Expro and Altus for a combined USD 2 billion in 2024. These integrated majors now offer slickline, coiled tubing, wireline, and P&A under unified commercial frameworks, an attractive proposition for NOCs issuing multi-service tenders.

Regional challengers such as NESR captured Oman’s USD 200 million award by pricing 15% below multinational averages and leveraging local content commitments. Technology remains the chief differentiator: SLB’s Stream platform enables live downhole visualization, and Baker Hughes’ iCruise introduces machine-learning tension control to cut non-productive time. Welltec’s autonomous system proved it could slash crew headcount 40% in North Sea trials, appealing to operators contending with labor shortages.

Emerging white space lies in carbon capture and storage. Shell’s Quest project logs CO₂ plume behavior via time-lapse slickline, and the U.S. DOE’s CarbonSAFE Sweetwater well will need similar surveillance once drilling completes. Smaller service firms such as Superior Energy Services and Nine Energy Service are building CCS-focused divisions, banking on regulatory tailwinds.

Slickline Logging Services Industry Leaders

Schlumberger Limited

Halliburton Company

Weatherford International Plc.

Baker Hughes Company

Expro Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Petro-Victory commenced drilling the SJ-12 well in Brazil’s São João Field. Halliburton was noted as the logging-services provider in earlier related campaigns, underscoring the continued reliance on wireline and slickline logging for reservoir evaluation, testing, and development planning in onshore Brazilian operations.

- July 2025: SLB launched the OnWave autonomous logging platform, which enables high-fidelity formation-evaluation measurements without the need for wireline units or cables. Although not a slickline tool, this platform disrupts conventional slickline and wireline logging by offering faster and safer deployment, along with automated downhole data acquisition across complex well trajectories.

- March 2025: Hunting PLC acquired Organic Oil Recovery technology to enhance the performance of mature fields. While not directly a slickline or logging acquisition, this technology's deployment often complements slickline and wireline diagnostics by verifying reservoir response. It integrates with intervention workflows in production-optimization programs.

- December 2024: Halliburton introduced its Intelli portfolio, a suite of wireline-conveyed diagnostic intervention services. This portfolio includes pulsed-neutron, production logging, casing inspection, and leak-diagnostic tools. These services aim to enhance downhole insights, streamline well-intervention workflows, and complement slickline and wireline operations by supporting precise logging-based diagnostics.

Global Slickline Logging Services Market Report Scope

The Slickline Logging Services Market encompasses the global industry that delivers slickline-based well intervention, measurement, and maintenance services for oil and gas wells. Slickline is a thin, single-strand wire utilized to deploy tools into a wellbore, enabling various downhole operations without the need for complex equipment.

The slickline logging services market is segmented into hole type, location of deployment, and geography. By hole type, the market is segmented into open hole and cased hole. By location of deployment, the market is segmented into onshore and offshore. By geography, the market is divided among North America, Europe, Asia-Pacific, South America, and the Middle East &Africa. The market sizes and forecasts are provided in terms of value (USD).

| Open Hole |

| Cased Hole |

| Onshore |

| Offshore |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Norway | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Hole Type | Open Hole | |

| Cased Hole | ||

| By Location of Deployment | Onshore | |

| Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Norway | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the slickline logging services market expected to grow through 2031?

It is projected to expand at a 6.89% CAGR between 2026 and 2031, reaching USD 2.41 billion by 2031.

Which segment currently leads by hole type?

Cased-hole operations dominated at 60.2% share in 2025 and are forecast to keep the lead through 2031.

Why is offshore deployment gaining traction despite smaller volume?

Deep- and ultra-deepwater wells demand higher-specification slickline tools, translating into faster revenue growth at a 7.5% CAGR.

What is driving adoption of digital slickline platforms?

Real-time telemetry compresses decision cycles, reduces non-productive time, and supports methane-monitoring compliance, delivering strong ROI in high-day-rate offshore environments.

Which regions are forecast to post the strongest slickline growth?

The Middle East and Africa region is the fastest, advancing at a 7.2% CAGR thanks to large NOC programs in Saudi Arabia, UAE, and Nigeria.

How are workforce shortages being addressed?

Vendors are investing in autonomous conveyance systems that lower crew requirements by up to 40% and enable remote supervision.

Page last updated on: