Market Overview

| Study Period | 2021 - 2031 |

|---|---|

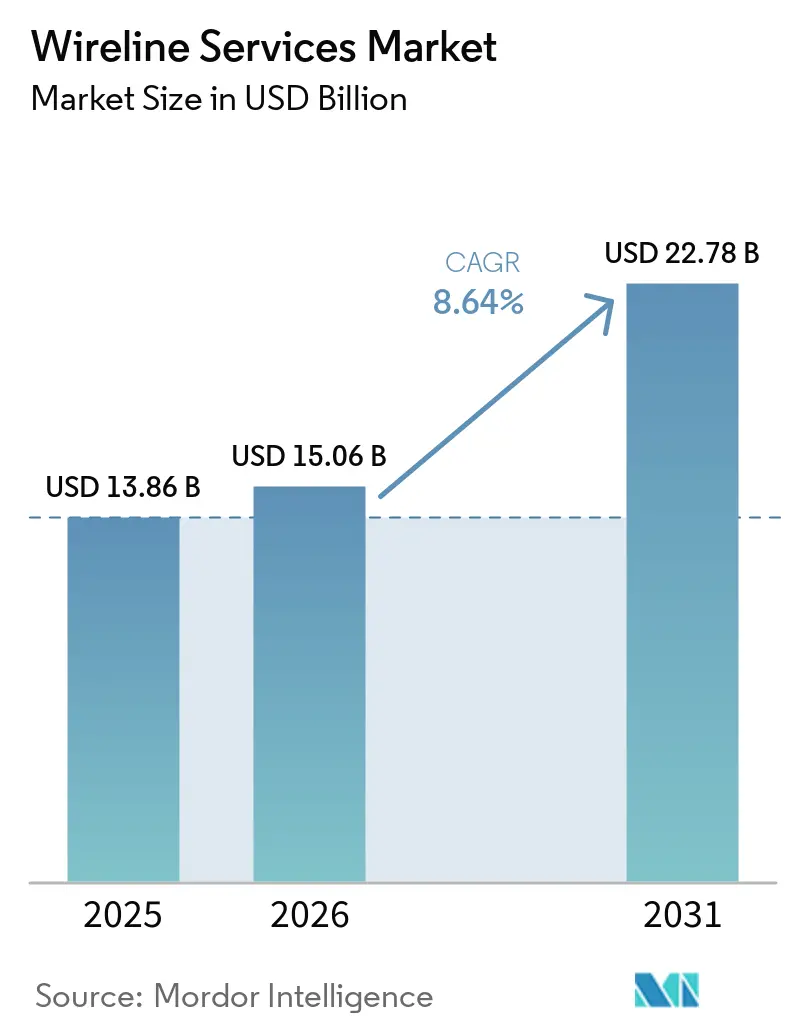

| Market Size (2026) | USD 15.06 Billion |

| Market Size (2031) | USD 22.78 Billion |

| Growth Rate (2026 - 2031) | 8.64% CAGR |

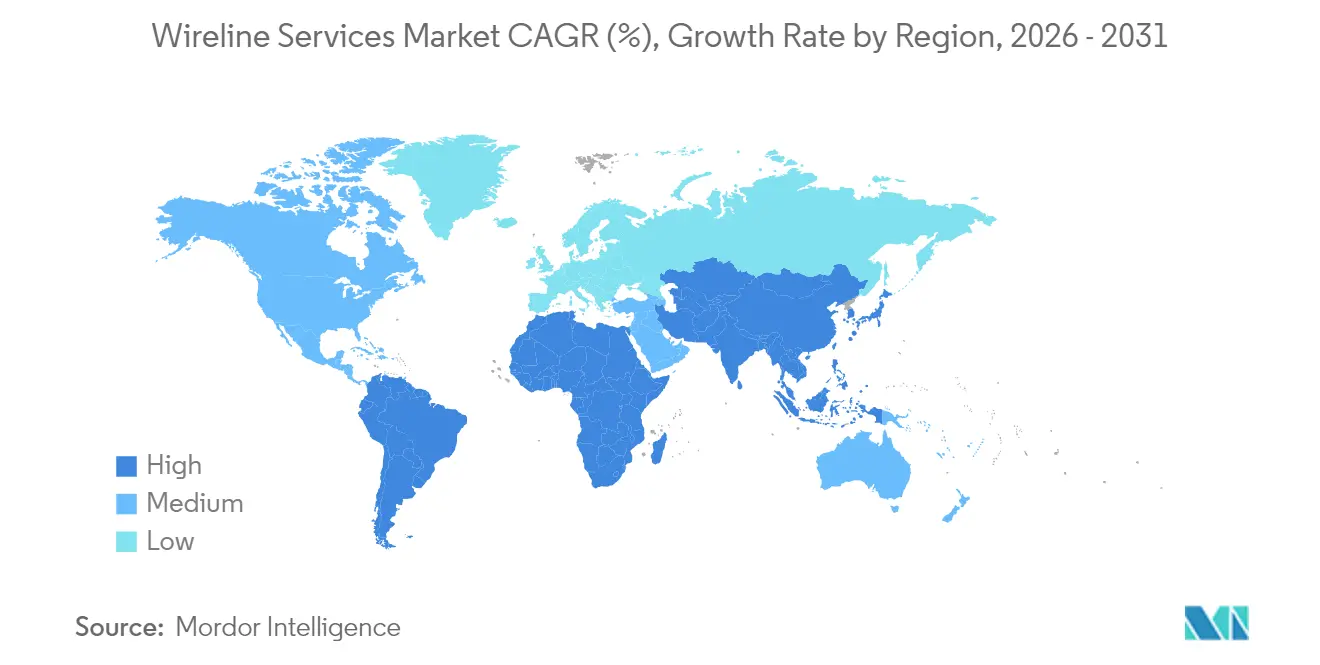

| Fastest Growing Market | South America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wireline Services Market Analysis by Mordor Intelligence

The Wireline Services Market size was valued at USD 13.86 billion in 2025 and estimated to grow from USD 15.06 billion in 2026 to reach USD 22.78 billion by 2031, at a CAGR of 8.64% during the forecast period (2026-2031).

Strong offshore deep-water investment, wider adoption of fiber-optic electric lines, and pervasive digital transformation projects are the core engines behind this growth. Operators are reallocating budgets from one-off completion work to repeatable intervention and surveillance programs that raise ultimate recovery without drilling new wells. Demand is especially high for high-precision logging and real-time data transmission tools that can deliver dependable measurements in extended-reach and high-pressure wells. Competitive advantage is increasingly resting on AI-enabled geosteering and autonomous down-hole control, allowing service companies to shorten decision-making loops and deliver higher production efficiency. The technology shift rewards vendors with robust intellectual property and a global logistics footprint, while intensifying cost pressures on regional specialists.

Key Report Takeaways

- By type, electric line led with 64.60% revenue share in 2025, while slickline remained cost-favoured in niche mechanical tasks.

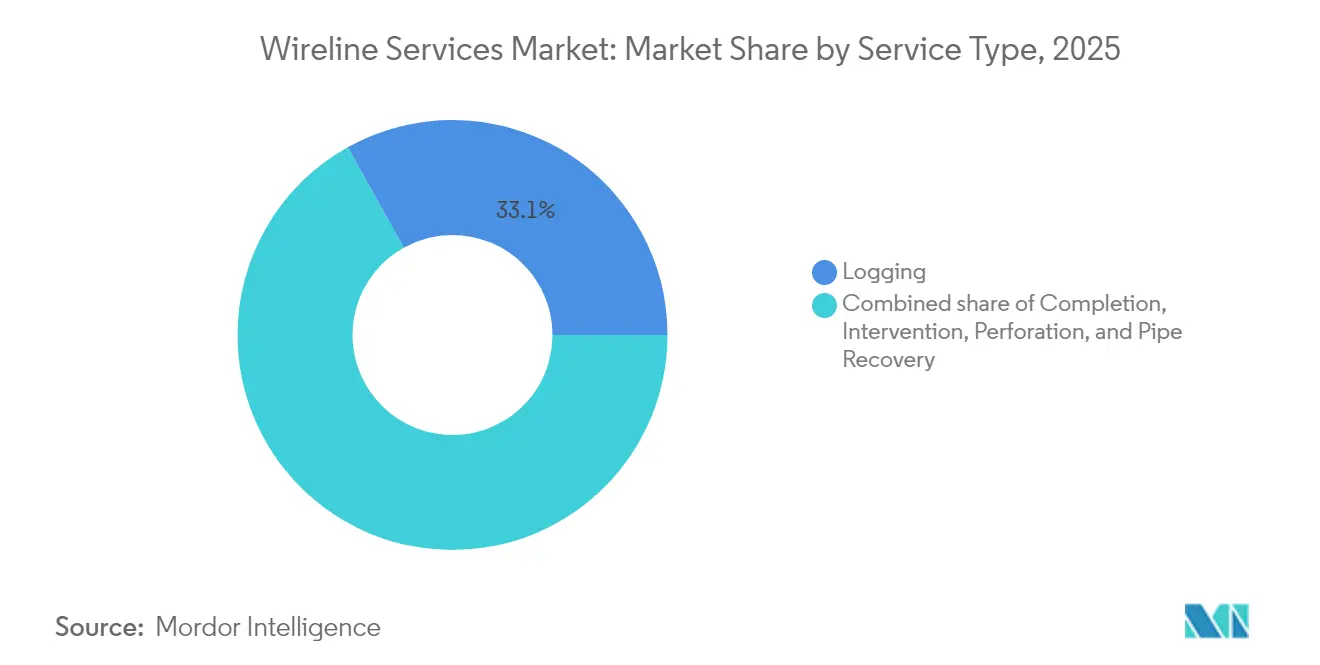

- By service, intervention outpaced all other categories, with a 9.60% CAGR through 2031, logging a retained 33.10% of the wireline services market share in 2025.

- By hole condition, cased-hole applications held a 59.30% share of the wireline services market in 2025 and are projected to grow at a 8.84% CAGR through 2031.

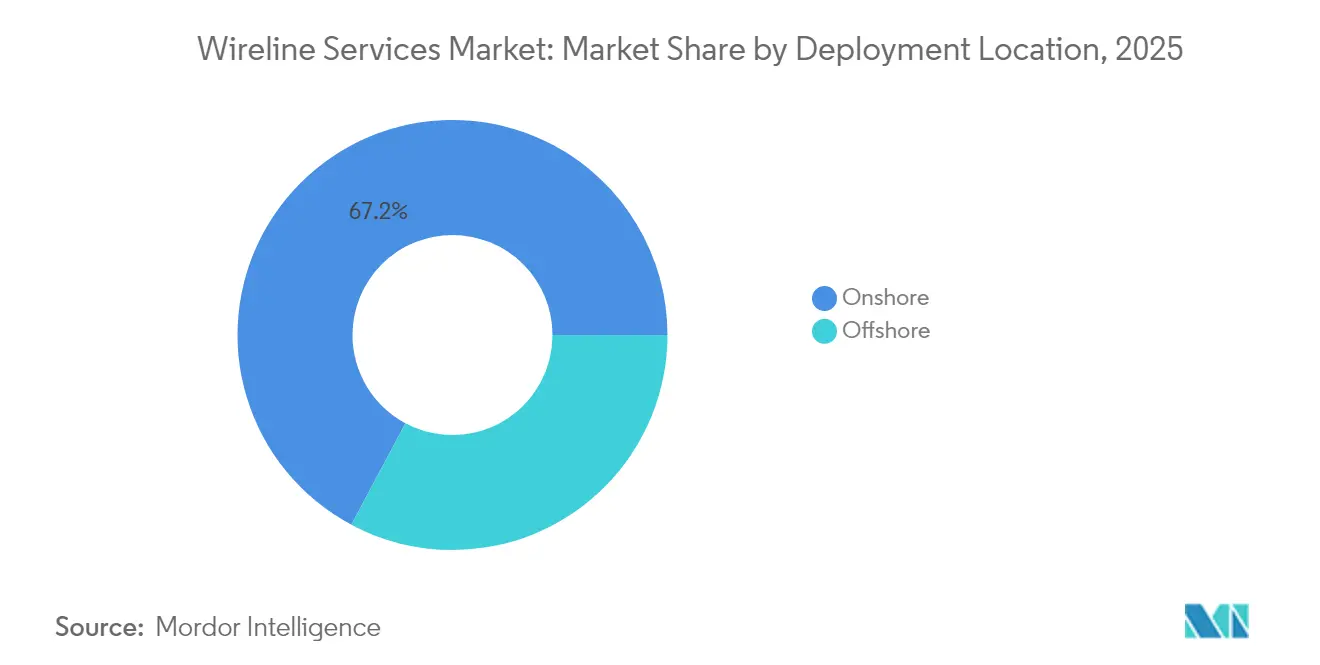

- By deployment location, offshore activity is forecast to rise at a 10.05% CAGR, even as onshore activity still accounts for 67.20% of 2025 spending.

- By region, South America tops the growth table at 9.72% CAGR, while North America accounted for 36.20% of 2025 revenue.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wireline Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising well complexity & demand for high-precision logging | 2.10% | Global, with concentration in North America & MENA | Medium term (2-4 years) |

| Offshore deep-/ultra-deepwater CAPEX rebound | 1.80% | Global offshore regions, led by South America & Africa | Long term (≥ 4 years) |

| Enhanced reservoir surveillance needs in mature fields | 1.40% | North America, MENA, North Sea | Short term (≤ 2 years) |

| Digital slickline adoption enabling real-time data | 1.20% | Global, early adoption in North America & Europe | Medium term (2-4 years) |

| NOC-led brownfield rejuvenation programs (MENA) | 0.90% | MENA region, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Miniaturised down-hole sensor integration (micro-wireline) | 0.60% | Global, technology leaders in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising well complexity & demand for high-precision logging

Shale laterals beyond 3 km and high-angle offshore wells require sub-meter accuracy in formation evaluation. AI-based geosteering platforms, such as SLB’s Neuro, can complete as many as 25 autonomous trajectory changes per well, keeping the bit in sweet spots that conventional steering would miss. Machine-learning algorithms now classify lithology with 92.7% balanced accuracy, shaving hours from interpretation cycles. Enhanced precision directly lifts recovery factors in heterogeneous formations, making wireline data indispensable for field development planning. Service companies with proprietary analytics suites are therefore winning premium contracts.

Offshore deep-/ultra-deepwater CAPEX rebound

Pre-salt Brazil and Guyana’s Stabroek block anchor the new offshore cycle. Petrobras awarded a USD 800 million integrated services package that includes complex HPHT wireline, underscoring the technical entry barriers. United States regulators now require third-party verification for novel HPHT tools, which raises compliance costs but improves safety. Deep-water day-rates for wireline crews and assets are 40–60% higher than their onshore equivalents, thereby boosting margins for providers with certified equipment. Training demands are steep because pressure envelopes surpass 20,000 psi, narrowing the field to a handful of global suppliers.[1]United States Bureau of Safety and Environmental Enforcement, “Final Rule: High-Pressure High-Temperature Well Control,” federalregister.gov

Enhanced reservoir surveillance needs in mature fields

North American shale and Middle East carbonate assets are in mid-life, prompting operators to focus on steady production gains rather than greenfield exploration. Fiber-optic distributed sensing installed during cased-hole runs now gives real-time temperature and pressure curves across the entire wellbore. ADNOC reported 15–25% output uplift after coupling continuous surveillance with targeted interventions. Generative-AI routines harvest decades of well files in minutes, cutting engineering time by 70% and supporting right-sized remediation plans. Such results transform wireline contracts from sporadic jobs into multi-year performance partnerships.[2]ADNOC, “Enhanced Oil Recovery Program Update,” adnoc.ae

Digital slickline adoption enabling real-time data

Fiber-optic slickline eliminates the one-way data gap of mechanical cable. Halliburton’s ExpressFiber and Baker Hughes’ SureCONNECT FE stream high-resolution down-hole information to remote operations centres, trimming on-site personnel by up to 50%. Completion crews now execute perforation and pressure-build-up diagnostics in a single run, saving 30–50% of tower time. Operators in unconventional basins credit these systems for sharper cluster efficiency during hydraulic fracturing stages. The business case is strongest where rig rates and non-productive time penalties are highest.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price volatility curbing E&P budgets | -1.50% | Global, particularly impacting North America shale operations | Short term (≤ 2 years) |

| Stringent decarbonisation / ESG regulations | -0.80% | Europe, North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Shortage of skilled high-pressure wireline crews | -0.60% | Global, acute in offshore and HPHT operations | Long term (≥ 4 years) |

| Limited supply of corrosion-resistant ultra-HPHT wire | -0.40% | Global, affecting deepwater and geothermal projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Crude-price volatility curbing E&P budgets

When Brent dips under USD 65 per barrel, small E&P companies trim discretionary spending almost immediately. Wireline intervention is among the first items deferred because its production impact is less visible than that of drilling. Although performance-based contracts and variable pricing models mitigate the impact, service demand can still fluctuate by 20–30% within a quarter. Larger integrated oil companies now prioritise free cash flow, leading to leaner completion schedules that compress baseline wireline volumes during downturns.[3]United States Energy Information Administration, “Short-Term Energy Outlook,” eia.gov

Stringent decarbonisation / ESG regulations

New methane rules in the United States require quarterly leak detection, which adds inspection runs but also increases compliance paperwork and equipment certification expenses. Canada is moving toward a 35% reduction in emissions below 2019 levels, a policy that could cap future oil sands production. Europe is tightening flaring limits and carbon intensity thresholds, making some offshore projects uneconomic. These pressures may redirect capital toward lower-carbon opportunities, dampening overall wireline utilisation in more mature basins.[4]United States Environmental Protection Agency, “Standards of Performance for Crude Oil and Natural Gas Facilities,” epa.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Electric Line Widens the Digital Gap

The electric-line segment captured 64.60% of 2025 revenue and is growing at a 9.12% CAGR. That leadership stems from real-time telemetry, high-bandwidth fiber-optic cores, and compatibility with multi-physics logging packages. By contrast, slickline holds value for simple mechanical tasks and low-cost brownfield work but struggles to meet precision data needs in complex wells. Digital electric systems now carry DAS and DTS modules that produce terabytes of continuous wellbore information. Coupled with AI-driven analytics, operators can adjust the perforation depth or fluid mix while the tool is still downhole, thereby reducing non-productive time and enhancing stimulation effectiveness. Over the forecast period, workflow automation and autonomous down-hole control are expected to tilt additional jobs toward electric line, reinforcing its central place in the wireline services market.

Electric-line providers also benefit from standardised tool strings that accelerate rig-up and reduce headcount. Cloud-based data pipelines ship logs to remote asset teams within minutes, shrinking analysis cycles and cutting travelling staff costs. Many national oil companies now incorporate real-time data clauses in tender documents, making electric capability a minimum entry requirement. Slickline will persist in low-pressure land wells and for gauge retrieval, yet its share is projected to erode incrementally as fibre-optic costs fall and digital slickline gains traction.

By Service Type: Intervention Takes the Growth Crown

Intervention services are set to climb at a 9.60% CAGR, outperforming all other categories even though logging still commanded 33.10% of the wireline services market share in 2025. Operators are shifting funds toward production maintenance, cement squeeze, and zonal isolation work that lengthen field life. In mature shale, a successful plug-and-perf refrac can increase output by 15–30% at a fraction of the cost of drilling a new well. Intervention campaigns increasingly use live-data decision engines that optimize treatment in real-time, further strengthening the value proposition.

Logging remains critical at spud and during reservoir management, but the volume of new drills is moderating in several basins. Completion runs face margin pressure as plug-and-perf designs become standardised. Pipe recovery and fishing remain niche yet essential when collapsed casing or stuck pipe threatens abandonment. Taken together, the pivot towards continuous optimisation underpins the intervention’s superior expansion outlook within the broader wireline services market.

By Hole Type: Cased-Hole Programs Rule Recurring Revenue

Cased-hole work held 59.30% of 2025 revenue, expanding at a robust 8.84% CAGR. Mature wells demand frequent production logging, saturation profiling, and cement evaluation, all of which rely on cased-hole instruments. Reservoir engineers value the ability to correlate time-lapse data sets and quickly pinpoint water breakthrough or gas coning events. Permanent fibre systems installed behind pipe deliver 24/7 surveillance, transforming wellsites into automated data generators.

Open-hole services remain indispensable for formation evaluation and fluid sampling on new wells. Yet because each new drill creates multiple follow-up cased-hole jobs across its economic life, the recurring opportunity heavily favours the latter. Advances in cross-casing porosity and density tools now allow accurate reads even with multiple casing strings, preserving open-hole-grade log quality after completion. These technological gains underpin the long-term strength of cased-hole solutions within the wireline services market.

By Deployment Location: Offshore Earns the Growth Premium

Offshore spending is predicted to rise at a 10.05% CAGR against a 67.20% onshore share baseline. Deep-water projects above 1,500 m water depth rely on specialised winch systems, dual-redundant safety valves, and corrosion-resistant wire rated to 200 °C. The Bureau of Safety and Environmental Enforcement now mandates independent validation of any novel HPHT tool for US waters, reinforcing the high entry hurdles. High mobilization costs and limited vessel availability push service margins higher than those of land operations.

Onshore campaigns continue to standardise through remote control and batch drilling, compressing cycle times. AI-driven planning reduces rig uptime by up to 30%, while trimming service hours and improving operational predictability. Consequently, while onshore volumes dwarf offshore, pricing power and technical differentiation remain strongest in deep-water, sustaining its growth premium within the wireline services market.

Geography Analysis

North America’s dominant 36.20% share in 2025 reflects its unmatched rig count and high uptake of digital logging services. Operators continue to run AI-assisted geosteering and remote operations centres that squeeze 30% more efficiency from each crew. The United States Gulf of Mexico seeks deeper reservoirs, but tight labour availability and stringent methane controls raise operating costs. Canada’s proposed 35% emissions cap may constrain oil sands expansion, tilting service demand toward integrity inspection rather than new well deployment.

South America offers the most compelling growth story. Brazil’s pre-salt carbonate columns can exceed 8,000 m measured depth and 20,000 psi bottom-hole pressure, making each wireline run both technically demanding and highly remunerative. Petrobras now bundles logging, intervention, and surveillance under long-term alliances that favour vendors with proven ultra-HPHT track records. Argentina’s Vaca Muerta shale mirrors North American pad drilling yet still lags in well count, leaving significant runway for wireline uptake as infrastructure matures.

Europe and Asia-Pacific grow at a mid-single-digit pace under the shadow of net-zero targets. Norway’s North Sea optimises mature assets via 4D seismic-calibrated cased-hole saturation logs, while China’s Bohai and deep-water South China Sea basins invest in domestic energy security, opening tenders for advanced logging fleets. The Middle East remains a volume stronghold, driven by ADNOC’s brownfield renewals and Kuwait’s new offshore push. Africa is mixed: Namibia’s discoveries brighten the outlook, whereas security issues curb activity in parts of West Africa.

Competitive Landscape

The wireline services market exhibits moderate consolidation, with SLB, Halliburton, and Baker Hughes collectively holding a 60–65% global market share. Their edge rests on proprietary digital ecosystems, worldwide maintenance hubs, and an installed base of certified ultra-high-pressure, high-temperature (HPHT) equipment. SLB’s Neuro™ system logged 25 automated trajectory corrections in Ecuador without real-time human input, signalling a shift toward autonomous operations. Halliburton’s ExpressFiber and Baker Hughes’ SureCONNECT FE each embed fiber-optic sensors directly into the cable, enabling millisecond-level data streaming and hands-off tool control.

Regional specialists still capture local work where national content rules apply, yet capital hurdles for deep-water and high-temperature gear are rising. Market share battles now hinge on analytics, cloud connectivity, and service integration rather than brute asset count. The acquisition of Datagration by Weatherford demonstrates how incumbents are acquiring software talent to remain relevant in the evolving wireline services industry. Continued M&A activity aimed at enhancing digital capabilities is expected as service firms fortify their data-driven value propositions.

Wireline Services Industry Leaders

Schlumberger Limited

Baker Hughes Company

Weatherford International PLC

Halliburton Company

NOV Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SLB secured an AI-enabled deep-water drilling contract that expands autonomous wireline deployment in complex reservoirs.

- April 2025: Halliburton won a multi-well construction award from Rhino Resources in Namibia’s Orange Basin, covering exploration and appraisal wireline scopes.

- December 2024: SLB introduced Neuro™ autonomous geosteering after 25 successful trajectory shifts in an Ecuador pilot.

- September 2024: Weatherford acquired Datagration, strengthening its real-time data and analytics suite.

Global Wireline Services Market Report Scope

The wireline services market report include:

By Type

| Electric Line |

| Slick Line |

By Service Type

| Completion |

| Intervention |

| Logging |

| Perforation |

| Pipe Recovery |

By Hole Type

| Open Hole |

| Cased Hole |

By Deployment Location

| Onshore |

| Offshore |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Norway | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Electric Line | |

| Slick Line | ||

| By Service Type | Completion | |

| Intervention | ||

| Logging | ||

| Perforation | ||

| Pipe Recovery | ||

| By Hole Type | Open Hole | |

| Cased Hole | ||

| By Deployment Location | Onshore | |

| Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Norway | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the wireline services market?

The industry was valued at USD 15.06 billion in 2026 and is projected to reach USD 22.78 billion by 2031.

Which segment is growing fastest within the wireline services market?

Intervention services are leading growth with a 9.60% CAGR through 2031.

Why are electric-line tools preferred over slickline in new projects?

Electric lines provide real-time data transmission and support AI-enabled logging, capabilities that mechanical slickline lacks.

Which region offers the highest growth opportunity?

South America, driven by Brazil’s pre-salt and Argentina’s Vaca Muerta, is expected to grow at 9.72% CAGR to 2031.

How are ESG regulations affecting wireline demand?

More stringent methane and carbon rules increase compliance costs and may restrict drilling activity, moderating service volume in some mature basins.

Who are the leading players in the wireline services market?

SLB, Halliburton, and Baker Hughes jointly control about two-thirds of global revenue, leveraging proprietary digital platforms and certified HPHT equipment.

Page last updated on: