Personal-Use Glucometer Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

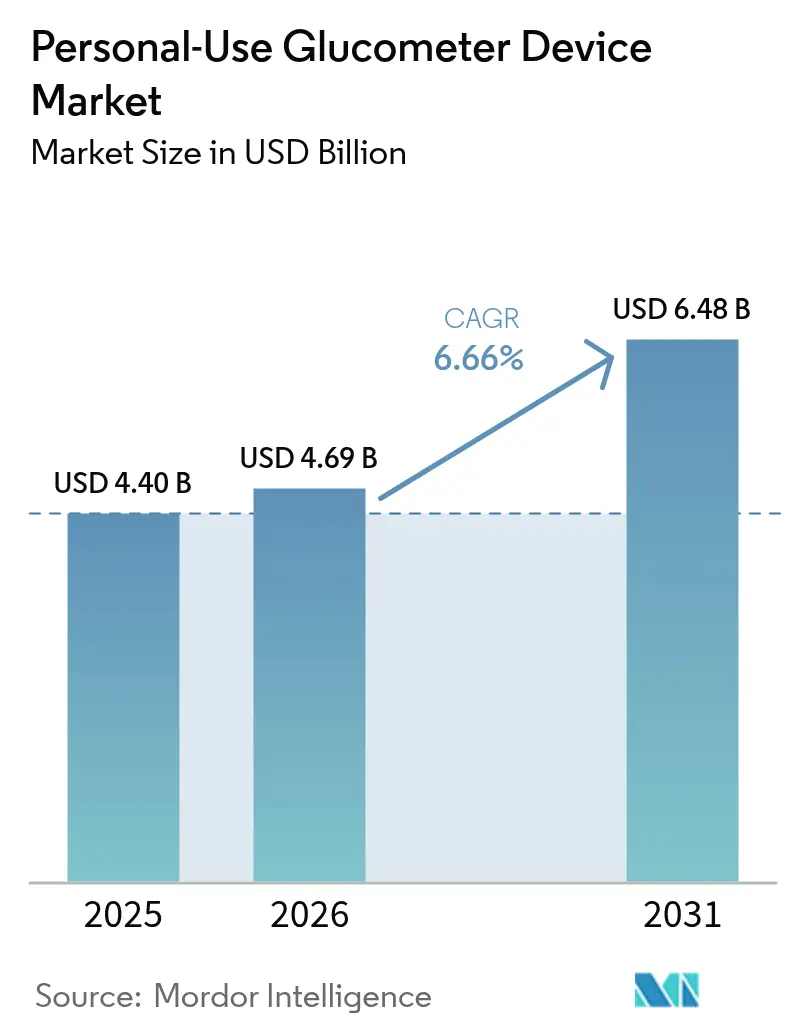

| Market Size (2026) | USD 4.69 Billion |

| Market Size (2031) | USD 6.48 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

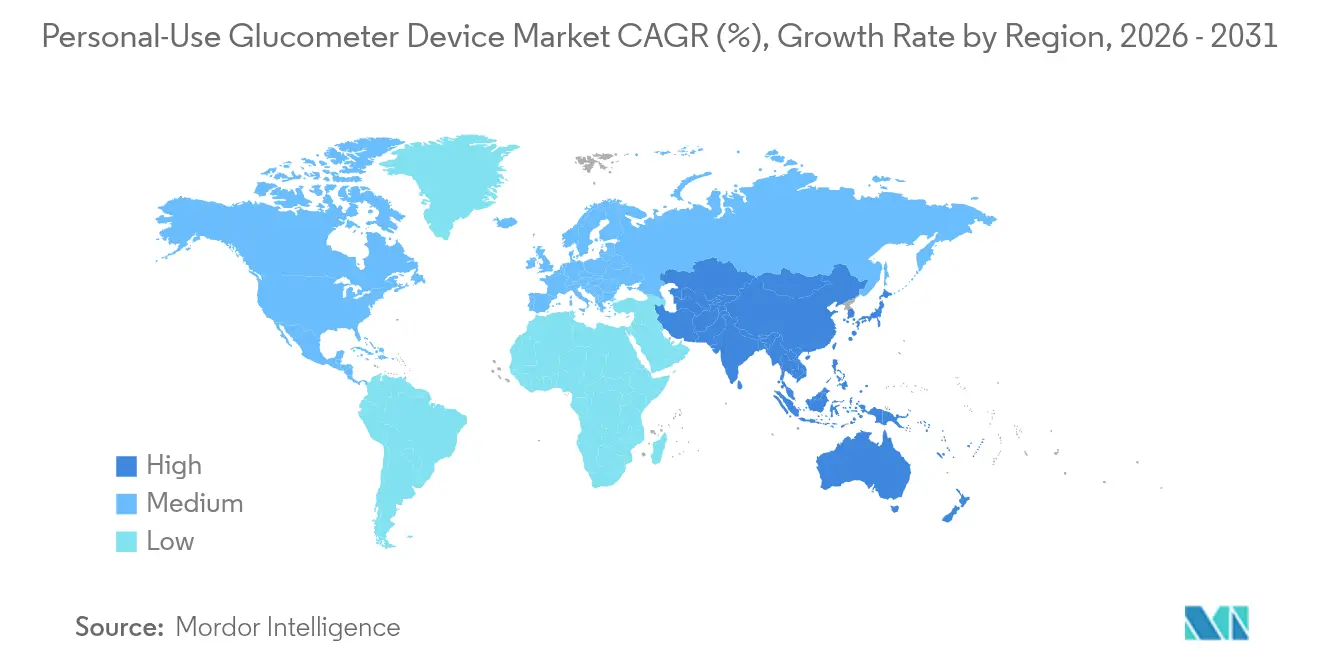

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal-Use Glucometer Device Market Analysis by Mordor Intelligence

The personal-use glucometer devices market size in 2026 is estimated at USD 4.69 billion, growing from 2025 value of USD 4.40 billion with 2031 projections showing USD 6.48 billion, growing at 6.66% CAGR over 2026-2031. The expansion reflects the compound effect of rising diabetes prevalence, population aging, and steady reimbursement gains for connected meters. Continuous sensor innovation, smartphone integration, and over-the-counter (OTC) clearances broaden the addressable base beyond insulin-dependent patients, while real-time analytics improve therapeutic decision-making. Growth also benefits from expanding wellness adoption among non-diabetic consumers and sustained venture funding that accelerates miniaturized, low-power designs. Competitive intensity remains moderate but is sharpening as scale players link glucose data with automated insulin delivery, digital coaching, and generative AI platforms.

Key Report Takeaways

- By component, test strips led with 64.62% of personal-use glucometer devices market share in 2025, whereas glucometer devices are set to post the fastest 8.96% CAGR to 2031.

- By technology, self-monitoring blood glucose accounted for 34.98% revenue share in 2025, while continuous glucose monitoring is poised to rise at a 12.06% CAGR.

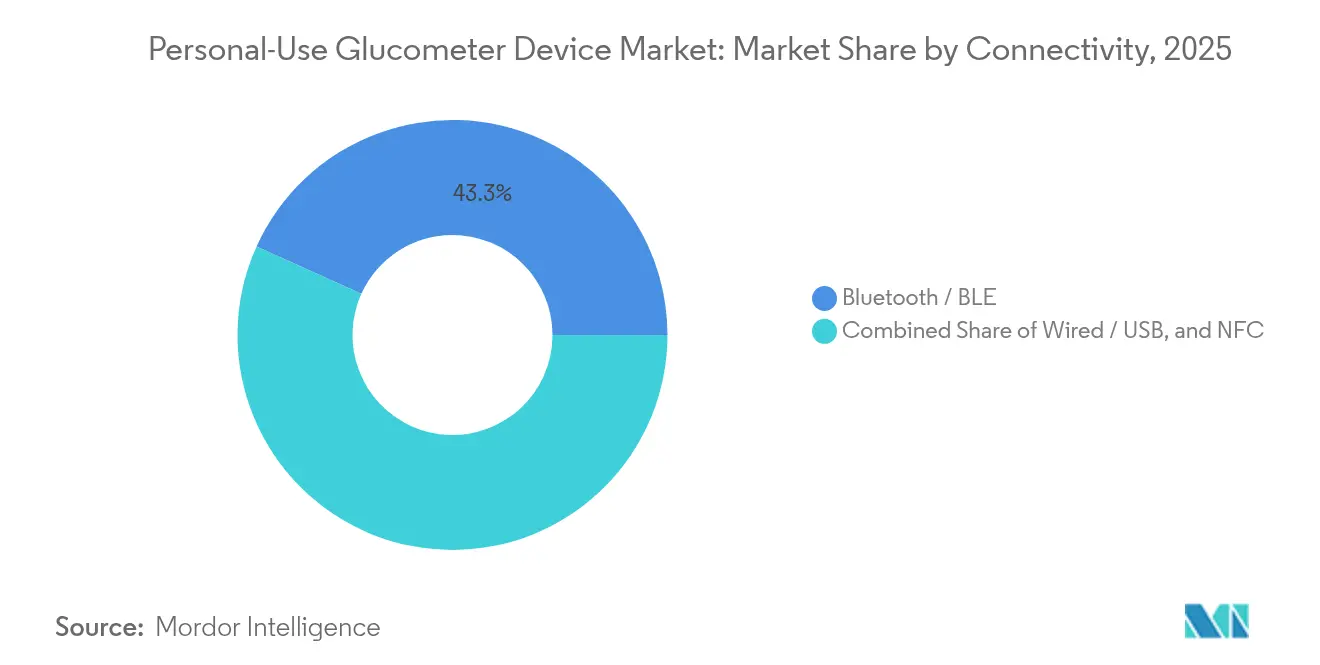

- By connectivity, Bluetooth commanded 43.25% revenue share in 2025; near-field communication is projected to climb at an 10.98% CAGR through 2031.

- By end-user, the home-care segment represented 88.15% of industry revenue in 2025, while sports and wellness users are forecast to expand at 11.31% CAGR.

- By geography, North America held 42.10% revenue share in 2025, yet Asia-Pacific is on track for the quickest 12.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal-Use Glucometer Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes Prevalence & Ageing Population | +1.8% | Global, with highest impact in APAC and MEA | Long term (≥ 4 years) |

| Smartphone-Linked Smart Meters Gain Reimbursement Traction | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Expansion Of Continuous & Flash GM Into Type-2 Pre-Diabetes | +1.5% | Global, led by developed markets | Medium term (2-4 years) |

| OTC Approval Of Non-Invasive Optical Meters | +0.9% | North America & EU regulatory frameworks | Short term (≤ 2 years) |

| Wellness Wearables Drive Adoption By Non-Diabetics | +0.8% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence & Ageing Population

Global diabetes prevalence could exceed 783.2 million by 2045, creating sustained demand for easy-to-use monitors[3]Centers for Disease Control and Prevention, “IDF Diabetes Atlas: Global, regional and country-level diabetes prevalence estimates for 2021 and projections for 2045,” stacks.cdc.gov. The burden is pronounced in Asia-Pacific, where China already records a 13.67% prevalence and faces a projected 29.1% rate by 2050. Older adults need simplified interfaces, larger displays, and dependable connectivity, prompting manufacturers to refine ergonomy and voice-guided prompts. Combined demographic and disease pressures ensure that the personal-use glucometer devices marketcontinues expanding even in reimbursement-constrained settings. The sheer volume of potential users underpins long-run volume growth that can absorb price erosion.

Smartphone-Linked Smart Meters Gain Reimbursement Traction

Medicare aligned coverage rules with ADA guidance in 2023, waiving finger-stick confirmation and adding basal-only Type 2 patients, thereby subsidizing 80% of approved CGM system costs[2]Sean M. Oser & Tamara K. Oser, “Medicare Coverage of Continuous Glucose Monitoring — 2023 Updates,” aafp.org. Commercial payers quickly followed, citing documented A1c reductions and reduced hypoglycemia events. In Europe, Norway and Belgium introduced national funding for sensor-based monitors, while additional markets evaluate similar moves. Reimbursement cuts out-of-pocket cost, fostering mainstream adoption and enabling vendors to bundle smartphones, apps, and cloud portals. As insurers link sensor data with population-health analytics, reimbursement remains a decisive pull factor for the personal-use glucometer devices market.

Expansion of Continuous & Flash GM Into Type-2 Pre-Diabetes

Clinical trials show continuous monitoring reduces HbA1c even in non-insulin Type 2 cohorts, supporting coverage expansion and primary-care uptake. Public health authorities now study cost-effectiveness findings that place CGM within accepted willingness-to-pay thresholds for basal-only users. Pre-diabetic and wellness users number near 720 million globally, representing an untapped market for early metabolic feedback. Consumer platforms such as Ultrahuman demonstrate how lifestyle analytics motivate dietary adjustments among healthy individuals. These dynamics pull continuous sensors deeper into primary prevention, broadening the commercial base for the personal-use glucometer devices market.

OTC Approval of Non-Invasive Optical Meters

The FDA cleared Dexcom’s Stelo and Abbott’s Lingo as the first OTC CGMs in 2024, erasing prescription barriers[1]U.S. Food and Drug Administration, “FDA Clears First Over-the-Counter Continuous Glucose Monitor,” fda.gov. Device makers now sell directly through pharmacies and e-commerce, reaching early stage diabetics and wellness consumers. Optical sensing studies show Raman-based prototypes hitting 12.8% MARD, approaching clinical-grade accuracy. OTC access reshapes marketing, emphasizes intuitive apps, and supports subscription revenue. Rapid consumer uptake accelerates data volumes, enabling personalized coaching and fueling competitive pressure across the personal-use glucometer devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Lifetime Cost Of Consumables (Strips / Sensors) | -1.4% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Accuracy Gaps Vs. Lab Reference In Tropical Climates | -0.8% | Tropical regions, APAC, MEA, South America | Medium term (2-4 years) |

| Cyber-Security & Data-Privacy Regulations Tighten | -0.6% | Global, led by North America & EU enforcement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Lifetime Cost of Consumables (Strips / Sensors)

Annual CGM ownership ranges between USD 1,200 and USD 3,600, while 100-count strip boxes retail from USD 35 to USD 170, squeezing uninsured and low-income users. Even Dexcom’s value-priced Stelo still averages USD 100 per month. Surveys across six developing countries confirm affordability gaps that dampen sustained monitoring adherence. Manufacturers respond with longer-life sensors and bundle discounts, yet volume-driven cost declines remain gradual. Without broader subsidies, consumable burden continues to temper uptake in price-sensitive segments of the personal-use glucometer devices market.

Accuracy Gaps vs. Lab Reference in Tropical Climates

Heat and humidity can induce up to 30.1% error within minutes, undermining clinical confidence in warm regions. Hospital studies in Thailand and the Philippines report systematic variance during monsoon months, forcing labor-intensive stress testing. Strip enzymes degrade under oscillating temperature cycles, while sensor membranes suffer moisture intrusion. Vendors are redesigning packaging and electronic shielding, yet field reliability lags lab benchmarks. Persistent accuracy concerns slow guideline endorsement and constrain the personal-use glucometer devices market in equatorial economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Consumables Continue to Anchor Revenue

Test strips captured 64.62% of the personal-use glucometer devices market in 2025, preserving a high-margin replenishment stream that underwrites manufacturer cash flows. Devices, however, are registering the quickest 8.96% CAGR as users pivot to integrated, sensor-rich platforms that lower per-reading cost over time. Longer wear sensors such as Dexcom G7 15-Day demonstrate how hardware upgrades decrease monthly spend and improve convenience. Accessories—from lancet drums to smartphone cradles—command modest but rising revenue as connectivity and comfort influence brand choice.

Glucometer innovation now targets single-platform ecosystems that pair proprietary sensors with AI-driven apps. Abbott’s FreeStyle Libre 2 Plus, the first U.S. CGM to link directly with automated insulin delivery, illustrates the hardware-software convergence reshaping the personal-use glucometer devices market. Vendors also trial reusable optical readers designed to leverage strip-free photonics, potentially compressing consumable demand. While strips remain dominant, incremental sensor advances steadily shift revenue weight toward durable equipment and cloud subscriptions.

By Technology: Continuous Monitoring Disrupts SMBG Hegemony

Self-monitoring blood glucose still holds 34.98% share, anchored by affordability and clinician familiarity. Nevertheless, continuous sensors are outpacing at 12.06% CAGR because real-time trend data reduce hypoglycemia risk and support dose titration. Randomized studies in primary care show CGM users achieving HbA1c drops of 1.3 percentage points versus 0.8 points for finger-stick cohorts. Non-invasive optical prototypes demonstrate accelerating accuracy gains, aided by machine-learning spectroscopic algorithms.

Technology suppliers bundle sensors with telehealth dashboards, broadening clinical oversight and unlocking insurer value-based payments. Medtronic’s Simplera disposable CGM, half the size of its predecessor, shows how form-factor reductions drive comfort and adoption. As reimbursement spreads and component costs fall, CGM looks set to erode SMBG leadership across the personal-use glucometer devices market.

By Connectivity: Bluetooth Reigns While NFC Accelerates

Bluetooth retained 43.25% revenue share in 2025, benefitting from universal smartphone support and established pairing stacks. Near-field communication, however, is projected to grow 10.98% annually because it permits tap-to-scan uploads without user configuration. NFC chips also consume less power, extending sensor life and fostering fully disposable designs. USB and proprietary cables linger for clinical download stations but fade in consumer channels.

Connectivity now underpins analytics differentiation. Dexcom recently launched the first glucose biosensing generative-AI platform on Google Vertex AI, a move that demands stable, low-latency data links. NFC’s simplicity supports elderly users and emerging-market customers who rely on entry-level Android phones, expanding penetration of the personal-use glucometer devices market.

By End-User: Home-Care Dominates Yet Wellness Surges

Home-care applications represented 88.15% of revenue in 2025, reflecting the day-to-day nature of diabetes self-management. Retail OTC approvals now allow walk-in purchase, bolstering household adoption. Simultaneously, sports and wellness users are forecast for an 11.31% CAGR as athletes and weight-loss seekers adopt CGMs to fine-tune diet and training. A multi-armed study on non-diabetic Indians using Ultrahuman’s platform illustrated how real-time glucose curves encourage healthier meal choices.

Mainstream media coverage has normalized CGM for metabolic awareness, though data literacy gaps persist. Manufacturers counter by embedding color-coded insights and automated food logging. Wellness adoption thus diversifies revenue and creates a preventive front door for the personal-use glucometer devices market.

Geography Analysis

North America led the personal-use glucometer devices market with 42.10% revenue share in 2025 on the back of payer funding, early tech uptake, and robust distribution networks. Medicare’s expanded coverage and successive private-payer updates have widened eligibility for continuous sensors, spurring double-digit unit growth. The U.S. FDA’s friendly stance toward OTC clearances further enlarges the consumer funnel and shortens go-to-market cycles. Canada mirrors these trends, advancing national reimbursement pilots for flash sensors.

Asia-Pacific is projected to log a 12.28% CAGR through 2031 as high prevalence converges with rising middle-class disposable income. China’s digital health programs demonstrate that integrated platforms can trim fasting glucose by 1.68% and HbA1c by 0.45 points among engaged users. India’s uptake of point-of-care HbA1c screening, with an ICUR of just USD 185.10/QALY in rural settings, underscores economic viability. Government initiatives to localize sensor assembly are also likely to shrink end-user prices, fuelling further expansion of the personal-use glucometer devices market.

Europe maintains stable mid-single-digit growth, underpinned by national funding steps such as Norway’s 2023 decision to reimburse sensor-based monitors. The EU’s Medical Device Regulation harmonizes safety benchmarks, favoring firms with rigorous quality systems. Meanwhile, Latin America and Middle East-Africa show rising incidence but adoption lags due to cost and limited payer coverage. Nevertheless, philanthropic procurement and telehealth pilots in Gulf Cooperation Council states foreshadow incremental upside.

Competitive Landscape

Competition centers on technology leadership, integrated ecosystems, and regulatory agility. Abbott, Dexcom, and Roche collectively anchor the top tier, each leveraging data platforms to lock in users. Abbott’s August 2024 agreement with Medtronic links FreeStyle Libre sensors with automated insulin pumps, broadening closed-loop care. Dexcom counters through AI-driven insight engines that personalize coaching and flag glycemic excursions in real time.

Mid-cap players pursue white-space. Glucotrack advanced an implantable monitor through first-in-human trials, potentially eliminating external wearables. Tandem Diabetes Care signed a June 2025 pact with Abbott to incorporate dual glucose-ketone sensing into its automated delivery portfolio. Such alliances consolidate data streams, complicate entrant differentiation, and heighten switching costs in the personal-use glucometer devices market.

Regulatory standards raise technical hurdles. The May 2025 FDA rule (21 CFR 862.1355) codified accuracy and cybersecurity criteria for integrated systems, prompting heavy investment in quality assurance. Vendors that meet these bars gain first-mover market access, while laggards risk reimbursement exclusion. As platform convergence intensifies, channel leverage and data-analytics capability are expected to determine share shifts over the next five years.

Personal-Use Glucometer Device Industry Leaders

LifeScan Inc.

Arkray Inc.

Ascensia Diabetes Care Holdings AG

F. Hoffmann-La Roche AG

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: PT Diagnostics introduced the A1CNow SELF CHECK in the UK, enabling individuals to monitor diabetes in just five minutes at home.

- June 2024: Abbott secured FDA clearance for Lingo, an OTC CGM aimed at both diabetes and general wellness audiences.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the personal-use glucometer market as all handheld self-monitoring blood-glucose meters sold to consumers, together with their disposable test strips, lancets, and simple app-linked accessories used for capillary finger-stick testing at home. It tracks retail and online sales across every region and covers insulin as well as non-insulin diabetic cohorts.

Scope Exclusions: Professional point-of-care analyzers, flash or continuous glucose monitors, and any hospital procurement fall outside this scope.

Segmentation Overview

- By Component

- Glucometer Devices

- Test Strips

- Lancets

- Accessories

- By Technology

- SMBG (Capillary)

- Continuous Glucose Monitoring (Personal)

- Non-Invasive Optical Monitoring

- By Connectivity

- Wired / USB

- Bluetooth / BLE

- NFC

- By End-User

- Home-Care / Personal

- Sports & Wellness Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed endocrinologists, diabetes educators, retail pharmacy buyers, and meter R&D leads in North America, Europe, Asia-Pacific, and Latin America. Their feedback refined strip-usage frequencies, device replacement cycles, and reimbursement nuances, closing gaps left by desk work and grounding key assumptions.

Desk Research

Mordor analysts gathered foundational data from tier-1 public sources such as the International Diabetes Federation, World Health Organization, CDC National Diabetes Statistics, European device registries, and UN Comtrade shipment records. They then enriched insights with peer-reviewed journals like Diabetes Care. Company filings retrieved via D & B Hoovers and patent pulses from Questel informed price curves and innovation intensity. The sources cited are illustrative; many others aided data collection, verification, and clarification.

Market-Sizing & Forecasting

A top-down prevalence pool of diagnosed diabetics is filtered through SMBG adoption, monthly strip consumption, and meter life cycles. Selective supplier roll-ups and channel checks provide bottom-up cross-checks that adjust totals. Core variables, diabetes prevalence trends, smartphone penetration, reimbursement caps, average selling prices, and regulatory approvals feed a multivariate regression that extends demand to 2030. Moving averages bridge occasional shipment lags while analyst judgment resolves outliers.

Data Validation & Update Cycle

Outputs undergo variance scans versus IDF prevalence paths and historic strip-to-meter ratios, followed by a peer review before sign-off. Mordor refreshes each model annually and issues interim updates whenever material policy, recall, or technology shifts arise. Every client delivery is preceded by a fresh validation sweep.

Why Mordor's Personal-Use Self-monitoring Blood Glucose Devices Baseline Earns Decision-Makers' Trust

Published estimates often diverge because some publishers merge SMBG with CGM devices, apply uniform strip-use rates, or rely on aging base years. By restricting scope to true personal-use meters, refreshing data yearly, and triangulating assumptions through direct user input, Mordor provides a figure that mirrors real-world consumption.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.40 B (2025) | Mordor Intelligence | |

| USD 6.72 B (2024) | Regional Consultancy A | Includes CGM units and professional channels inflating value |

| USD 13.43 B (2023) | Global Consultancy B | Bundles all blood-glucose devices, uses older prevalence and unadjusted price data |

The comparison shows that careful scope selection, live variables, and an annual refresh let Mordor deliver a balanced, transparent baseline that managers can trace to clear inputs and reproducible steps.

Key Questions Answered in the Report

What is the current size of the personal-use glucometer device market?

The market stands at USD 4.69 billion in 2026 and is projected to reach USD 6.48 billion by 2031.

Which component category generates the most revenue?

Test strips lead with 64.62% market share in 2025, anchoring recurring revenue.

How fast is continuous glucose monitoring (CGM) growing?

CGM is advancing at a 12.06% CAGR through 2031, the quickest pace among technology segments.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at a 12.28% CAGR on the back of rising diabetes prevalence and healthcare investments.

What recent regulatory move is boosting consumer adoption?

The FDA’s 2024 OTC clearance of devices like Dexcom’s Stelo and Abbott’s Lingo removed prescription barriers and widened access.

Page last updated on: