Online Racing Games Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

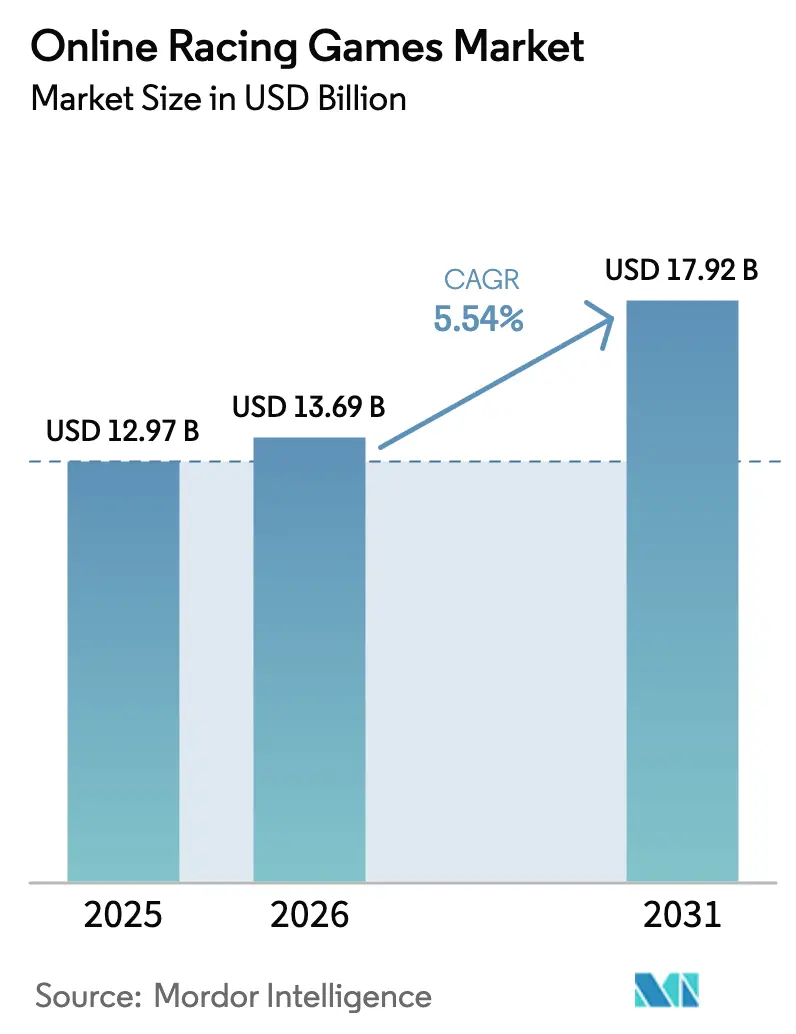

| Market Size (2026) | USD 13.69 Billion |

| Market Size (2031) | USD 17.92 Billion |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

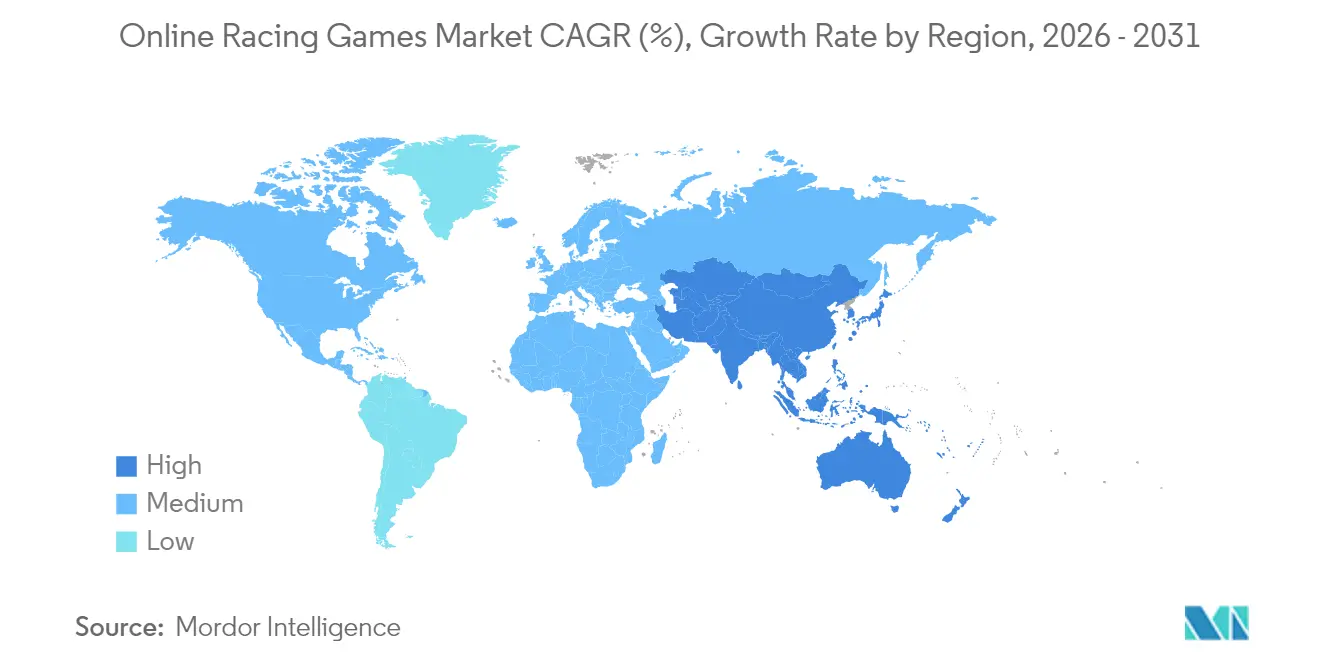

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Racing Games Market Analysis by Mordor Intelligence

The global online racing games market size was valued at USD 12.97 billion in 2025 and estimated to grow from USD 13.69 billion in 2026 to reach USD 17.92 billion by 2031, at a CAGR of 5.54% during the forecast period (2026-2031). Rising 5G penetration, cloud-native delivery, and AI-driven content generation continue to redraw competitive boundaries, shifting growth from console-centric ecosystems to cross-platform experiences optimized for smartphones and low-latency networks. Edge computing nodes hosted by more than 500 metropolitan points of presence shorten round-trip times to single-digit milliseconds, enabling console-grade visuals on mobile devices and widening the addressable base for the online racing games market.[1]Phil Spencer, “Expanding Cloud and Edge for Xbox Gaming,” Microsoft Blog, microsoft.com Esports tie-ins, premium hardware partnerships, and procedural track generation further diversify revenue streams and extend content lifecycles without proportionate development costs, while privacy-driven user-acquisition headwinds and escalating AAA budgets temper margins for mid-tier studios.

Key Report Takeaways

- By platform, mobile commanded 52.10% of the online racing games market share in 2025, whereas cloud-streaming clients are expanding at a 6.78% CAGR to 2031.

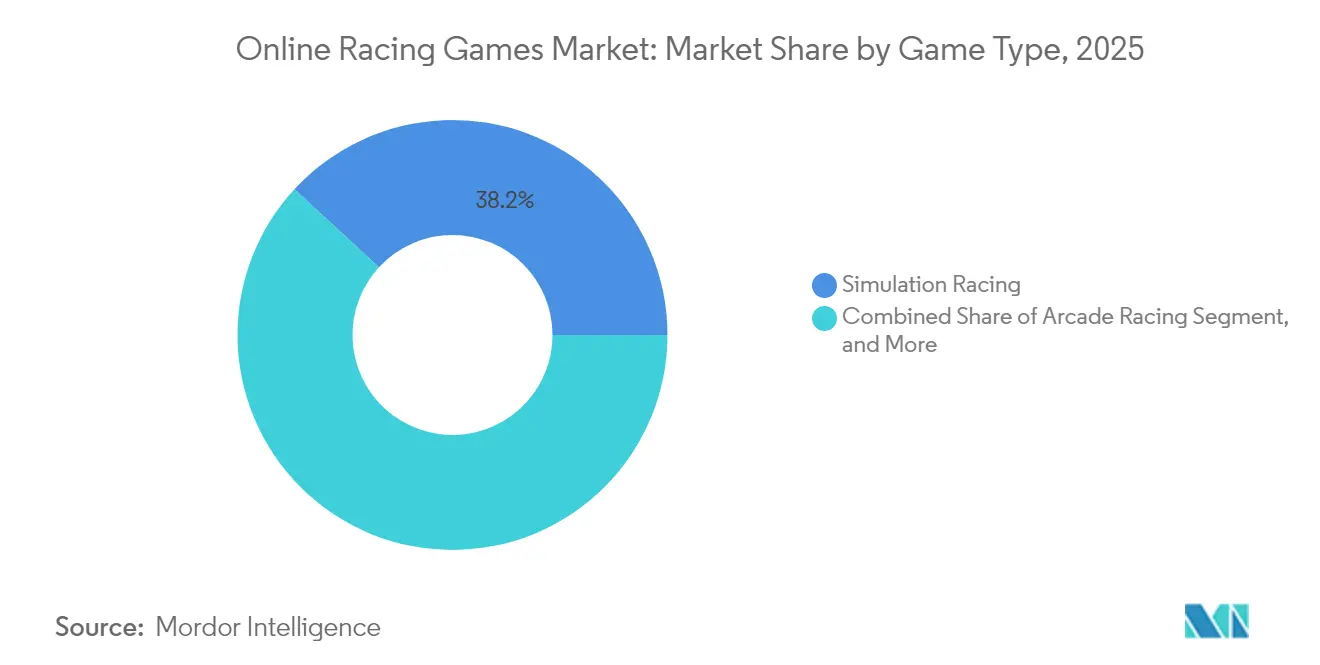

- By game type, simulation racing led with 38.15% revenue share in 2025 in the online racing games market; open-world street racing is forecast to grow at a 6.18% CAGR through 2031.

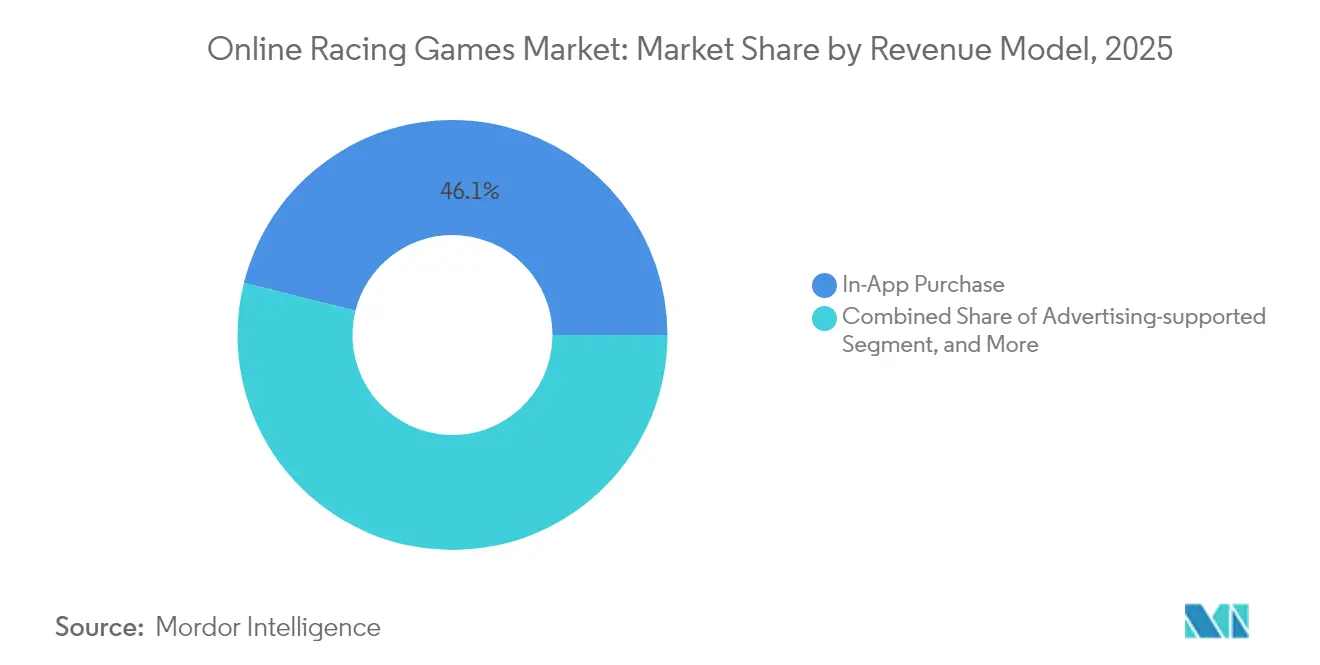

- By revenue model, in-app purchases accounted for 46.10% share of the online racing games market size in 2025, while subscriptions and season passes are advancing at a 6.64% CAGR to 2031.

- By player engagement level, mid-core competitive users held 42.30% share in 2025 in the online racing games market, whereas cloud-based engagement is rising at a 6.29% CAGR to 2031.

- By geography, North America retained 37.40% share in 2025 in the online racing games market; Asia-Pacific is on track to post a 6.18% CAGR through 2031 on the back of mobile-first gaming cultures and urban 5G rollouts

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Racing Games Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone and 5G penetration expands low-latency play | +1.5% | Global, with APAC and Middle East leading deployment | Medium term (2-4 years) |

| Cloud-gaming lowers hardware barriers | +1.2% | North America and EU early adoption, APAC mass market | Long term (≥ 4 years) |

| Esports integration boosts engagement and spend | +0.8% | Global, concentrated in urban gaming hubs | Short term (≤ 2 years) |

| AI-generated tracks cut content costs and refresh cycles | +0.9% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| VR haptics create premium immersion spend | +1.1% | North America and EU premium segments | Long term (≥ 4 years) |

| In-game OEM brand placements add revenue streams | +0.4% | Global automotive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smartphone and 5G Penetration Expands Low-Latency Play

Mobile-first racing titles now capitalize on sub-20 ms radio latencies that allow real-time multiplayer parity with console lobbies, eliminating the lag disadvantages that once discouraged cross-platform pools.[2]Corporate Communications, “5G Network Performance Update,” T-Mobile US, t-mobile.com T-Mobile’s L4S deployment cut perceived latency another 40%, while Microsoft’s 50 gaming data centers route compute within metropolitan reach, letting mobile drivers compete against rig-equipped PC users without physics desync. The resulting uplift in competitive integrity converts casual mobile users into repeat buyers of cosmetic items and battle-pass tiers, strengthening recurring revenue for the online racing games market. Publishers also bundle cloud-assisted rendering that off-loads physics to edge nodes, boosting frame stability on mid-range handsets and reducing hardware churn. Carriers reciprocate through zero-rating promotions that drop data fees for partnered titles, further lowering entry barriers across price-sensitive economies.

Cloud-Gaming Lowers Hardware Barriers

Streaming removes the USD 500-800 console outlay once prerequisite for authentic simulation experiences, broadening emerging-market demand and elevating lifetime value per gamer for the online racing games market.[3]Andrew Fear, “NVIDIA Demonstrates GeForce NOW for Game AI Inference,” NVIDIA Developer Blog, nvidia.comNVIDIA GeForce Now now pipes RTX 4080-level visuals to Chromebook users, while monthly infrastructure cost per active subscriber averages EUR 4.20, allowing gross margins to stay positive once adoption scales beyond 1 million users per region. Platform holders cement their reach by embedding cloud-play buttons inside digital storefronts, exemplified by Microsoft's Xbox store integration that transitions locally installed sessions to the cloud with a single click. License holders, in turn, repackage archival titles at subscription tiers, monetizing back catalogs without porting expenditures. Because rendering occurs server-side, developers decouple content updates from console generation cycles, shortening time-to-market for seasonal expansions and live-ops events.

Esports Integration Boosts Engagement and Spend

Prize pools topping USD 500,000 for flagship championships have repositioned racing from niche spectator sport to cornerstone of the broader esports economy. Event broadcasts embed real-time telemetry overlays that let viewers track tire wear and fuel burn, adding strategic depth that boosts minutes-viewed and thus sponsorship value. Fantasy competitions piggybacking on official leagues let casual fans form prediction brackets, an engagement loop that keeps the online racing games market top-of-mind during off-season lulls. Publishers record notable improvements in average revenue per paying user (ARPPU) once ranked-ladder resets coincide with esports majors, converting viewership spikes into in-game spending on commemorative liveries and driver cards. Retail brands cross-promote through limited-time bundles, cutting acquisition costs that rose sharply after iOS privacy reforms.

AI-Generated Tracks Cut Content Costs and Refresh Cycles

Machine-learning pipelines now synthesize photorealistic circuits in hours rather than the nine-to-twelve-month asset build common before 2024, trimming USD 2-5 million from per-track expenditures. Adaptive layouts scale complexity to player skill, boosting retention by delivering a fresh challenge curve without manual designer input. Neural rendering compresses texture payloads by 60%, keeping cloud egress fees flat even as map variety multiplies. Studios funnel those savings into marketing and community management, areas where spend efficiency shrank post-privacy changes. For the online racing games market, the upshot is faster patch cadence, continuous novelty, and steadier subscription revenue lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UA costs surge post-privacy changes | -0.7% | iOS-dominant markets (North America, EU, Japan) | Short term (≤ 2 years) |

| AAA racing development budgets escalate | -0.6% | Global, concentrated in premium market segments | Medium term (2-4 years) |

| Latency-sensitive gameplay raises regional server costs | -0.5% | APAC emerging markets, rural/suburban areas globally | Medium term (2-4 years) |

| Fragmented IP/licensing for cars and tracks | -0.4% | Global automotive markets, concentrated in premium racing segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

UA Costs Surge Post-Privacy Changes

Apple’s App Tracking Transparency policy stripped third-party identifiers that publishers relied on to model lifetime value, pushing iOS cost-per-install for sports and racing genres to USD 3.50, versus USD 2.50 on Android.[4]Developer Relations, “App Tracking Transparency Overview,” Apple Developer, apple.com In response, studios pivot to first-party telemetry and contextual ad buys, but ramp-up lead times inflate marketing overhead for new releases. Subscription models soften volatility yet demand continuous content drops to curb churn. GDPR compliance compounds complexity across Europe, as explicit consent gates throttle data-driven personalization that could offset UA inefficiencies, shaving 70-basis-points from the online racing games market CAGR projection through 2030.

AAA Racing Development Budgets Escalate

Photorealism, ray-traced reflections, and full trackside crowds push per-title budgets beyond USD 400 million, sums sustainable only for platforms with nine-figure annual live-service income. Codemasters’ USD 1.2 billion acquisition by Electronic Arts underscores consolidation pressures tied to cost inflation. Motion-capture rigs, tire-model physicists, and volumetric weather specialists extend dev cycles to four-plus years, delaying revenue realization and raising break-even thresholds. Mid-tier studios seek relief in cloud-native pipelines and procedural assets, but retraining and server fees erode initial savings. This capital squeeze subtracts 0.6 percentage points from the projected online racing games market CAGR during 2025-2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Revenue Model: Subscriptions Reshape Monetization Strategies

In 2025, in-app purchases held 46.10% share of the online racing games market size, driven by cosmetic skins and performance parts that preserve competitive balance while generating dependable microtransaction revenue. Subscriptions and season passes are rising 6.64% annually, supporting predictable cash flows that sustain live-ops content teams and analytics functions. Advertising-supported formats remain viable in regions with low card penetration, yet privacy limits dampen CPMs, nudging publishers toward brand partnerships and sponsored challenges.

Segment evolution shows how value shifts from one-off sales to recurrent access. Minecraft’s Marketplace Pass illustrates subscription value hinges on a steady cadence of user-generated tracks and vehicles. For simulation die-hards, premium outright purchases coexist with optional telemetry modules and coaching subscriptions, reflecting a hybrid stack of mon¬etization tailored to engagement depth. As churn sensitivities mount, studios invest in sentiment analysis bots monitoring Discord and Reddit for early churn predictors, refining content drops that stabilize recurring revenue within the online racing games market.

By Platform: Mobile Dominance Faces Cloud Disruption

Mobile accounted for 52.10% of 2025 revenue, cementing its primacy in the online racing games market. Improved SoC efficiency lets 120 fps arcade racers run on USD 200 handsets, while gyroscope steering eases onboarding for casual audiences. Concurrently, cloud-streaming clients are projected to grow at 6.78% CAGR, vaulting them from experimentation to mainstream by 2031. PC rigs preserve simulation loyalty because triple-screen cockpits and load-cell pedals remain unmatched in fidelity.

Console vendors counter attrition with cross-gen entitlements and 120 hz performance modes, yet increasingly pivot toward cloud APIs that extend their storefronts to smart TVs. VR and AR headsets add a premium strata; although volumes are nascent, attach-rate for high-ticket DLC doubles that of flatscreen cohorts. The cross-pollination of local rendering for UI and streamed physics calculations optimizes battery life on mobile, making performance parity credible and enlarging subscriber funnels for the online racing games market.

By Game Type: Open-World Racing Gains Momentum

Simulation titles captured 38.15% of 2025 revenue as esports endorsements and tactile wheel ecosystems deepened user investment. Open-world street racers, however, are forecast to rise 6.18% CAGR through 2031 on the back of procedural cityscapes, social hubs, and photo modes conducive to influencer sharing. Arcade racers hold mass appeal but rely on ad-monetization, a model hurt by ATT privacy shifts.

Content pipelines now rotate seasonal events synced with real-world motorsport calendars, galvanizing re-engagement like FIFA’s Team-of-the-Week drops. MILE-scale multiplayer events leverage cloud servers to field 500-car endurance races, producing viral clips that push organic installs. Kart subgenres use crossover IP to court family audiences and diversify the portfolio mix, whereas rally sims command passionate micro-communities who pay for laser-scanned stages and historical car packs, collectively sustaining revenue diversity inside the online racing games market.

By Player Engagement Level: Mid-Core Competitive Dominates

Mid-core competitors comprised 42.30% of user hours in 2025, blending accessible controls with ranked ladders that encourage skill progression and drive retention. AI tutors analyze corner-exit speeds and gift ghost replays, shortening the learning curve and boosting conversion to paying tiers. Hardcore sim racers invest in USD 1,000 pedal sets and telemetry dashboards, delivering ARPPU multiples of casual cohorts.

Meanwhile, cloud-based engagement is scaling 6.29% CAGR as device-agnostic accounts let players resume races on subway commutes and living-room TVs alike. Casual audiences still enter via ad-supported hyper-short sessions but face competition from culturally localized games, pushing racing studios to integrate regional festivals and vehicle skins. Cohort funnels increasingly merge; arcade newcomers migrate toward sim-lite playlists as skill grows, expanding lifetime value and fortifying the online racing games market against genre fatigue.

Geography Analysis

North America retained 37.40% share in 2025, buoyed by entrenched console culture and early 5G rollouts that underpin low-latency cross-play. Publishers leverage favorable ARPPU and live-service adoption as 83% of Electronic Arts’ USD 1.67 billion Q1 FY26 revenue flowed from recurring content. Canada’s e-hockey fandom overlaps with racing through cross-promotions, and Mexico’s mobile uptake accelerates through prepaid 5G bundles.

Asia-Pacific is the fastest-growing region at 6.18% CAGR to 2031, with China’s mobile games reaching USD 86.6 billion in 2024 and racing showing resilience amid overall download softness. Japan’s USD 21 ARPU motivates premium haptic-enabled releases, while South Korea’s PC-bang culture hosts licensed simulation leagues. India leads in volume with 8.45 billion downloads yet lags in monetization, spurring studios to add regionalized storylines and low-SKU cosmetic tiers tailored to local payment norms.

Europe balances privacy rigor with premium spending, as GDPR compliance bolsters user trust that supports subscription uptake. Automotive OEM density in Germany, Italy, and the U.K. fuels branded content alliances, while pan-EU esports circuits add broadcast value. The Middle East and Africa witness rapid mobile adoption; youth bulges and improving fintech rails unlock new payer cohorts, albeit with localization demands on livery design and event timing to respect cultural norms. These dynamics collectively shape regional revenue trajectories for the online racing games market.

Competitive Landscape

The online racing games market reflects moderate concentration. Electronic Arts leverages Need for Speed and the officially licensed F1 series to anchor cross-media partnerships, including 2025’s F1 movie integration that bundles exclusive story modes. Tencent exploits mobile platform dominance and robust backend tech to syndicate racing titles into super-apps like WeChat. Codemasters’ specialized physics engine remains a moat, and its EA ownership secures marketing reach.

Cloud-native challengers such as Velocima Games build server-side renderers that scale on Kubernetes, halving content deployment time versus traditional console pipelines. These start-ups benefit from lower capital intensity yet face hurdles in brand awareness and licensing access. Vertical integration is intensifying: Corsair’s USD 110 million Fanatec purchase merges hardware and software ecosystems, aiming to lock enthusiasts into proprietary peripherals that synergize with premium DLC.

M&A tallied USD 6.6 billion in Q1 2025, signaling ongoing consolidation as infrastructure demands and UA costs favor well-capitalized actors. Patent portfolios around adaptive AI and haptic telemetry further fortify incumbents; newcomers must navigate licensing minefields or embrace open-source stacks. Regulatory scrutiny focuses on loot-box mechanics, compelling publishers to pivot toward transparent season passes, but market leaders adapt swiftly, maintaining their advantage inside the online racing games market.

Online Racing Games Industry Leaders

Electronic Arts Inc.

Microsoft Corporation

Gameloft SE

Aquiris Game Studio SA

THQ Nordic GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Electronic Arts launched F1 25 with integrated movie tie-in content and enhanced My Team 2.0 features, demonstrating cross-media marketing strategies that expand audience reach beyond traditional gaming demographics while generating additional revenue through premium content packages.

- March 2025: NVIDIA demonstrated GeForce Now capabilities for game AI inference, enabling cloud-based machine learning that supports advanced opponent behavior and personalized racing experiences without requiring local high-end hardware investments.

- January 2025: Electronic Arts pre-announced preliminary Q3 FY25 results indicating continued strength in live-service revenue streams that support ongoing investment in racing franchise development and community features.

- October 2024: NVIDIA launched GDN (GeForce Developer Network) to advance cloud gaming and graphics rendering, providing developers with tools to optimize racing games for streaming environments while maintaining visual fidelity and reducing latency.

Global Online Racing Games Market Report Scope

The growing trend in the online racing games market, men playing racing games will create more growth for the racing games market. Advanced skills of game developers to offer real-like video games are creating a positive impact on the market. The adoption of advanced visual effects in these games is attracting many customers to the online racing games market. Racing game apps require players to drive their vehicles, usually against other drivers, along racetracks.

The Global Online Racing Games Market is segmented by Type (Advertising, In-App Purchase, Paid App) and Geography.

| Advertising-supported |

| In-App Purchase (Micro-transactions) |

| Premium Purchase (Paid App / Full Game) |

| Subscription / Season Pass |

| Mobile Smartphones and Tablets |

| PCs |

| Game Consoles |

| Cloud-Streaming Clients |

| VR / AR Headsets |

| Arcade Racing |

| Simulation Racing |

| Kart and Party Racing |

| Open-World / Street Racing |

| MILE-style Mass Events |

| Casual / Hyper-casual |

| Mid-core Competitive |

| Hardcore Simulation / Esports |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Revenue Model | Advertising-supported | ||

| In-App Purchase (Micro-transactions) | |||

| Premium Purchase (Paid App / Full Game) | |||

| Subscription / Season Pass | |||

| By Platform | Mobile Smartphones and Tablets | ||

| PCs | |||

| Game Consoles | |||

| Cloud-Streaming Clients | |||

| VR / AR Headsets | |||

| By Game Type | Arcade Racing | ||

| Simulation Racing | |||

| Kart and Party Racing | |||

| Open-World / Street Racing | |||

| MILE-style Mass Events | |||

| By Player Engagement Level | Casual / Hyper-casual | ||

| Mid-core Competitive | |||

| Hardcore Simulation / Esports | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected size of the global online racing games market by 2031?

The global market is forecast to hit USD 17.92 billion by 2031, growing at a 5.54% CAGR.

How fast is the cloud-streaming client segment expanding?

Cloud-streaming clients are on track for a 6.78% CAGR through 2031, the fastest among delivery platforms.

Which revenue model is gaining the most momentum?

Subscriptions and season passes are rising at a 6.64% CAGR as publishers pivot toward predictable, recurring income.

Why is Asia-Pacific considered the fastest-growing region?

Mobile-first gaming cultures and rapid 5G rollouts are pushing Asia-Pacific to a 6.18% CAGR through 2031.

What share do mobile platforms hold in online racing games?

Smartphones and tablets commanded 52.10% of global revenue in 2025, making them the dominant access point.

Page last updated on: