Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.93 Billion |

| Market Size (2026) | USD 2.06 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

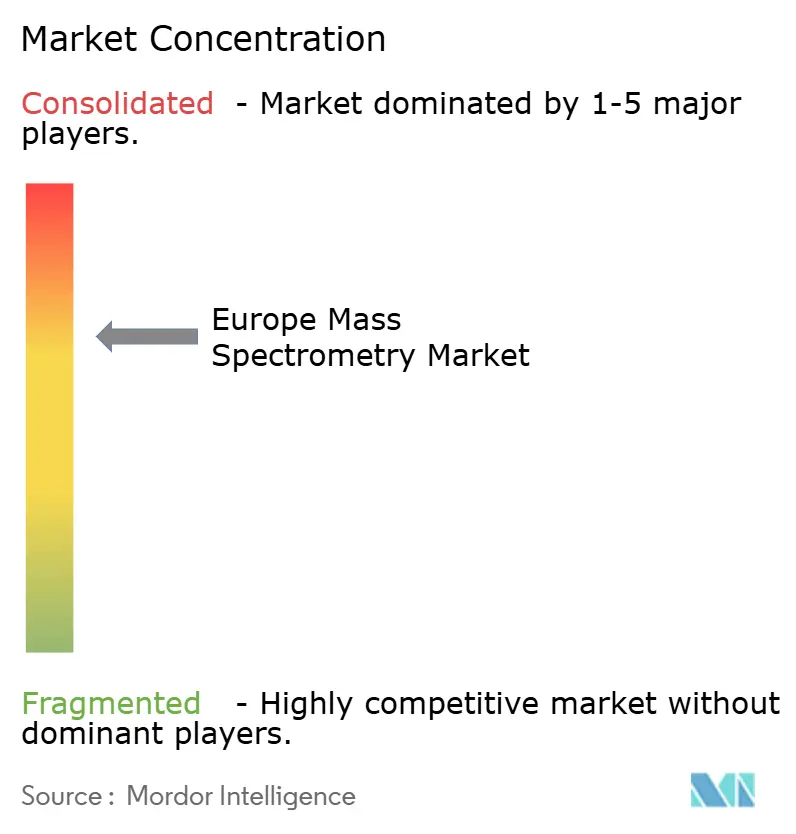

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Mass Spectrometry Market Analysis by Mordor Intelligence

The Europe Mass Spectrometry Market size is expected to increase from USD 1.93 billion in 2025 to USD 2.06 billion in 2026 and reach USD 2.87 billion by 2031, growing at a CAGR of 6.85% over 2026-2031.

Growing pharmaceutical and biotechnology pipelines that demand sub-nanogram-per-milliliter quantitation, tighter EU residue-monitoring rules for food and water, and the rapid turn-round advantages of tandem-mass-spectrometry clinical assays are expanding the installed base of high-resolution systems. Instrument vendors are embedding artificial-intelligence spectral deconvolution that lifts sample throughput by 30% to 40%, enabling midsize laboratories to process workloads that formerly required reference-lab outsourcing. Environmental agencies in Germany and the Netherlands are migrating from single-quadrupole to time-of-flight ICP-MS in response to new PFAS limits that sit below 1 ng/L, reinforcing the shift toward hybrid and triple-quadrupole architectures. Capital budgets across Spain’s science-park network and United Kingdom contract research organizations show a clear preference for cloud-connected data systems over incremental hardware upgrades, signaling that recurring software and services revenue will outpace instrument sales during the forecast window.

Key Report Takeaways

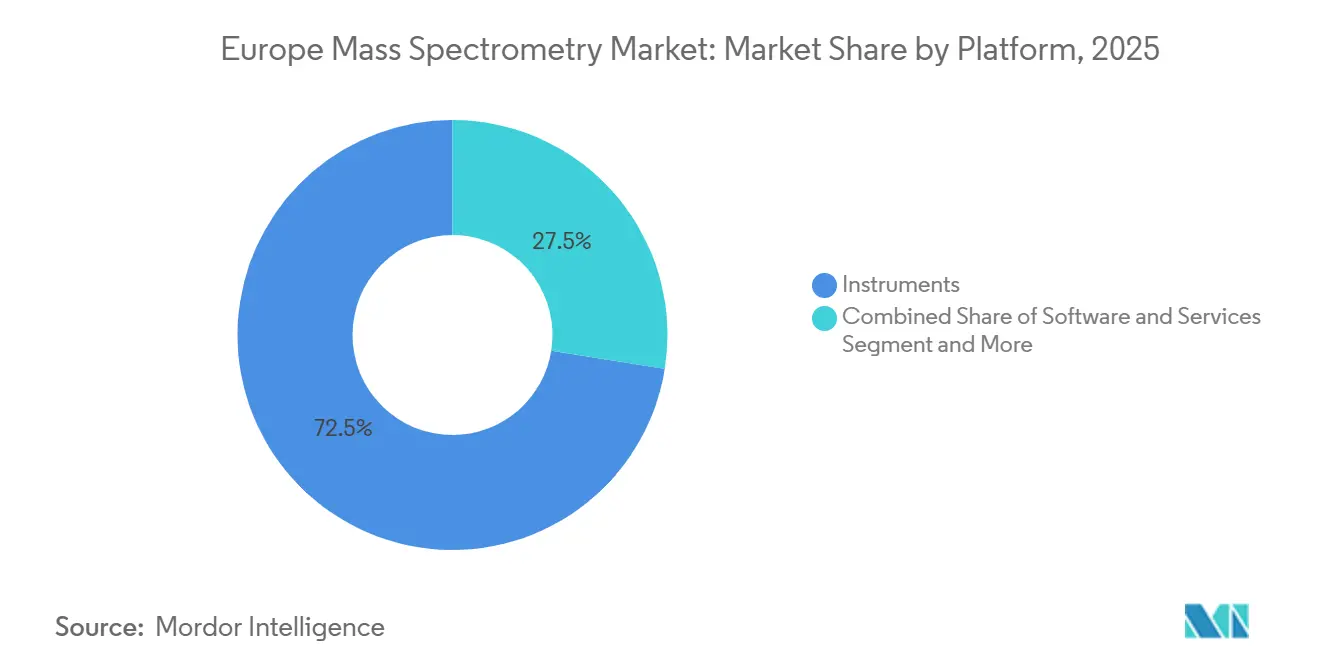

- By platform, instruments led with 72.55% revenue share in 2025, whereas software and services is set to record the highest CAGR at 9.85% through 2031.

- By technology, hybrid systems commanded 48.53% of 2025 revenue, while ICP-MS is forecast to grow the fastest at 8.75% CAGR to 2031.

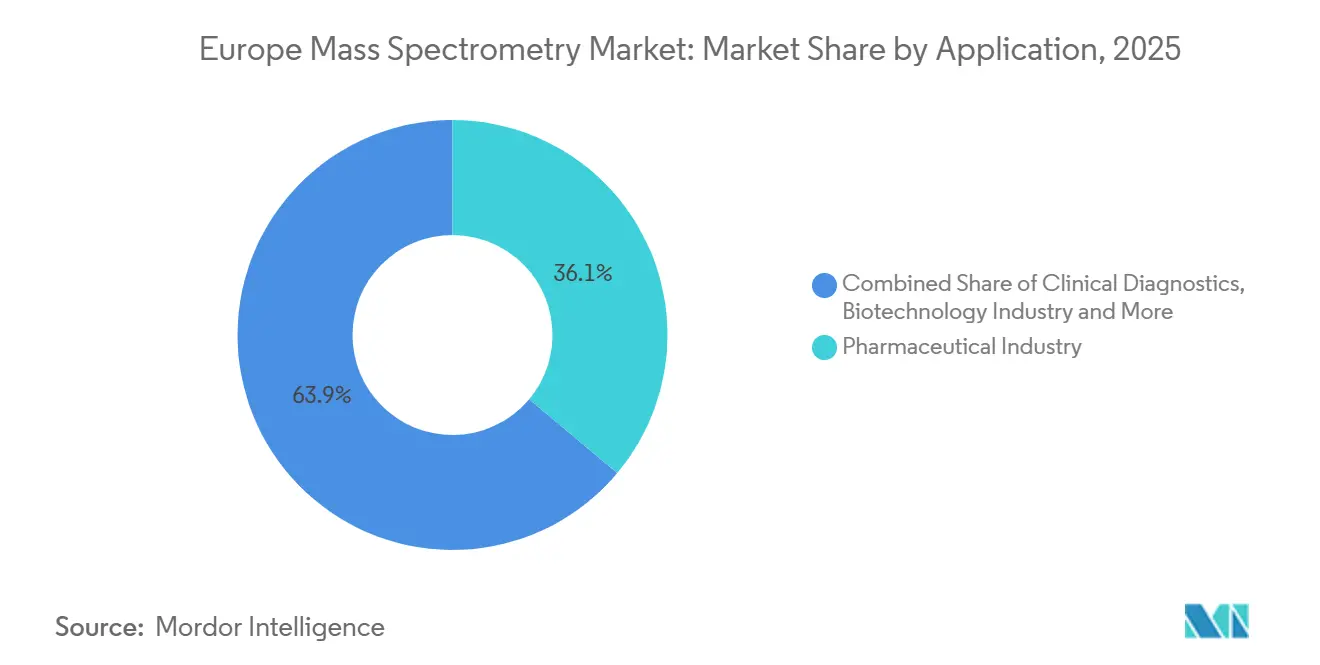

- By application, pharmaceutical analysis accounted for 36.15% share in 2025; clinical diagnostics is projected to expand at a 9.82% CAGR through 2031.

- By end user, pharmaceutical and biotechnology firms captured 42.32% of 2025 revenue, but hospitals and clinical laboratories are advancing at 9.29% CAGR to 2031.

- By geography, Germany held 39.52% of 2025 revenue, whereas Spain is expected to post the quickest growth at 8.32% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Mass Spectrometry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pharmaceutical & biotech R&D expenditure | +1.2% | Germany, France, United Kingdom, Switzerland | Medium term (2–4 years) |

| Stringent EU regulations for food safety & environmental monitoring | +1.5% | EU-wide, with early enforcement in Germany, Netherlands, Denmark | Short term (≤ 2 years) |

| Rapid adoption of hybrid & high-resolution MS technologies | +1.0% | Germany, United Kingdom, France, academic & pharma hubs | Medium term (2–4 years) |

| Expansion of clinical diagnostics & personalized medicine | +1.3% | Germany, Spain, United Kingdom, hospital networks | Long term (≥ 4 years) |

| AI-driven spectral interpretation enabling higher lab throughput | +0.8% | Global, with early gains in Germany, United Kingdom, Netherlands | Medium term (2–4 years) |

| Emergence of portable/benchtop MS unlocking decentralized testing | +0.7% | Spain, Italy, Rest of Europe, food & forensic sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pharmaceutical & Biotech R&D Expenditure

European pharmaceutical firms invested EUR 55 billion in R&D during 2024, driving sustained orders for liquid-chromatography–mass-spectrometry platforms that handle large molecule impurity profiling and biosimilar comparability under EMA guidelines. The European Biotech Act, proposed in December 2025, promises streamlined authorizations for cell and gene therapies, pushing research laboratories toward Orbitrap and quadrupole-time-of-flight systems that deliver sub-ppm accuracy needed for complex glycoform mapping. Contract research organizations such as Quotient Sciences have enlarged United Kingdom bioanalytical suites, adding triple-quadrupole lines to meet Good Laboratory Practice capacity commitments. Spain’s 974 biotech entities alone deployed more than 120 new high-resolution instruments across 80 science parks in 2025, a trend likely to extend as oncology pipelines mature. Because Phase I and Phase II studies increasingly demand 24-hour bioanalysis, procurement momentum is expected to persist through 2031.

Stringent EU Regulations for Food Safety & Environmental Monitoring

The European Food Safety Authority tightened maximum residue limits for 126 pesticides in 2024, obliging laboratories to validate multi-residue screens that quantify 500+ compounds in a single run—functionality delivered only by triple-quadrupole or accurate-mass platforms[1]European Food Safety Authority, “Pesticides Maximum Residue Levels – Revised Limits 2024,” efsa.europa.eu. The 2024 amendment to the EU Water Framework Directive added 24 PFAS to the priority list, requiring quarterly monitoring at levels below 1 ng/L and pushing environmental agencies to adopt triple-quadrupole ICP-MS for metal-free background and sub-ppt detection. Germany and the Netherlands have procured time-of-flight ICP-MS units that can track PFAS plumes around fluoropolymer facilities in real time. Food-testing labs across Denmark upgraded older single-quadrupole GC-MS to tandem configurations that meet ISO/IEC 17025 accreditation in under six months, shortening method-transfer cycles. This regulatory landscape is projected to lift the Europe mass spectrometry market CAGR by 1.5 percentage points through 2028, after which compliance-driven replacement demand levels off.

Rapid Adoption of Hybrid & High-Resolution MS Technologies

Hybrid designs that couple quadrupole mass filters with Orbitrap or time-of-flight analyzers delivered nearly half of Europe mass spectrometry market revenue in 2025 because they merge targeted quantitation with discovery-scale workflows. The Orbitrap Astral, introduced late-2024, captures 10,000 proteins per day from plasma by recording 200 spectra per second at 240,000 resolving power, transforming cohort-scale proteomics productivity. Academic alliances such as MSCoreSys in Germany operate shared quadrupole-time-of-flight libraries that harmonize quality-control metrics across four federal states. Fourier-transform ion-cyclotron-resonance remains a niche but is gaining recognition in complex petrochemical isomer resolution. As cloud-native algorithms automate deconvolution, hybrid platforms will consolidate dominance through 2031, blunting demand for legacy single-analyzer instruments.

Expansion of Clinical Diagnostics & Personalized Medicine

Hospitals across Germany, France, and the United Kingdom ran tandem-mass-spectrometry newborn-screening panels on more than 2 million infants in 2025, identifying metabolic disorders with specificity unmatched by immunoassays. Reimbursement reforms now cover vitamin D and testosterone quantitation via LC-MS/MS, removing a critical financial barrier to lab adoption in Germany. The MSTARS consortium is validating mass-spectrometry cardiovascular biomarker panels under EU in-vitro diagnostic regulation, targeting CE marking by 2027. Spain’s hospital networks funded 30 new triple-quadrupole installations during 2025 to support pharmacogenomic dosing workflows. These drivers position clinical diagnostics to be the fastest-growing application at 9.82% CAGR through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance costs of advanced instruments | -0.9% | EU-wide, acute in Southern & Eastern Europe | Short term (≤ 2 years) |

| Shortage of skilled mass spectrometrists | -0.6% | United Kingdom, Germany, France, hospital labs | Medium term (2–4 years) |

| Complex regulatory validation & method-standardization hurdles | -0.5% | Clinical diagnostics, EU-wide | Long term (≥ 4 years) |

| Helium & high-purity gas supply volatility post-Ukraine conflict | -0.4% | Germany, France, United Kingdom, GC-MS users | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs of Advanced Instruments

List prices for triple-quadrupole and Orbitrap systems range between EUR 300,000 and EUR 1.2 million, with annual service contracts adding up to 12% of purchase cost. Smaller clinical laboratories in Spain and Greece defer upgrades, relying on send-out testing despite turnaround delays. Reagent-rental and pay-per-sample models offered by vendors reduce upfront burden but lock customers into multi-year consumable commitments that can exceed original capital cost. Refurbished equipment remains scarce because high-resolution systems stay useful for a decade. This fiscal drag is expected to shave 0.9 percentage points from the Europe mass spectrometry market CAGR until component prices fall and secondary markets mature.

Shortage of Skilled Mass Spectrometrists

A Royal Society of Chemistry survey in 2024 found that 40% of analytical-chemistry employers struggle to hire LC-MS/MS-proficient staff, hampering method development and troubleshooting[2]Royal Society of Chemistry, “Chemistry Workforce Skills Gap Analysis 2024,” rsc.org. German newborn-screening labs expanding from 25 to 50 disorders require analysts trained in ion-suppression mechanics, yet only two universities added relevant modules in 2025. Vendors now bundle AI-guided tuning wizards, but root-cause analysis of failed runs still depends on human expertise. Contract research organizations such as Synexa Life Sciences report that hiring bottlenecks limit utilization of nine LC-MS/MS lines in Manchester to 80% capacity. This workforce gap will hold market growth back by roughly 0.6 percentage points through 2029.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Software & Services Gain Ground on Hardware

Instruments captured 72.55% of 2025 revenue, underscoring the capital-intensive nature of Orbitrap, triple-quadrupole, and ICP-MS purchases. Yet the software and services slice is projected to grow at 9.85% CAGR, outpacing hardware as laboratories prioritize data-integration, compliance documentation, and cloud pipelines. High-throughput contract labs that run 500 samples daily on a single triple-quadrupole consume EUR 70,000 in columns, calibration mixes, and ion-source spares each year, creating sticky recurring revenue. Subscription licensing models for enterprise chromatography data systems align vendor incentives with uptime, intensifying competition around analytics rather than detection limits.

Laboratories that already house multiple systems now view sample-to-report turnaround as the primary bottleneck. The Europe mass spectrometry market size for software tools that automate peak picking and audit trails rose sharply after Thermo Fisher introduced Chromeleon 7.3.2, which unites instrument control, LIMS connectivity, and AI-assisted method setup. Open-source alternatives such as MZmine 3 pressure commercial suites to prove tangible compliance benefits. As artificial-intelligence features mature, services tied to continuous algorithm upgrades are expected to offset slower instrument unit shipments, lifting overall market resilience.

By Technology: ICP-MS Surges on Environmental Mandates

Hybrid platforms contributed 48.53% of revenue in 2025, favored for their ability to toggle between discovery and targeted assays in a single run. Triple-quadrupole LC-MS/MS remains dominant in pharmaceutical bioanalysis because it pairs femtogram-level sensitivity with rugged uptime. Quadrupole-time-of-flight instruments excel in untargeted metabolomics, where mass accuracy below 3 ppm speeds unknown identifications. Orbitrap instruments, a subset of Fourier-transform technology, now extend to 200 Hz acquisition, opening doors for single-cell proteomics.

Environmental legislation is accelerating ICP-MS adoption; the Europe mass spectrometry market share for ICP-MS is projected to climb as triple-quadrupole configurations remove spectral interferences that once hampered arsenic or selenium quantitation below regulatory cut-offs. Germany alone commissioned 25 time-of-flight ICP-MS units in 2025 to monitor PFAS plumes, and Italy’s water authorities plan similar upgrades by 2027. Though magnetic-sector systems keep a toehold in isotope ratio studies, high-resolution Orbitraps are eroding that niche with comparable precision at a lower total cost of ownership.

By Application: Diagnostics Overtakes Discovery in Growth Pace

Pharmaceutical analysis dominated applications with 36.15% of 2025 revenue, fueled by EUR 55 billion in EU drug-development outlays that mandated impurity profiling and bioequivalence confirmation. Contract research labs in Verona and Manchester expanded triple-quadrupole lines to manage surging Phase I workloads, affirming hardware demand. However, clinical diagnostics is advancing at 9.82% CAGR and is on track to narrow the revenue gap by 2031.

Hospitals deploying LC-MS/MS assays for vitamin D, testosterone, and immunosuppressants report 25% declines in false-positive rates versus immunoassays, validating their economic case. Europe mass spectrometry market size for clinical assays will swell further once MSTARS gains CE marking for cardiovascular biomarker panels by 2027. Forensic toxicology, environmental surveillance, and food safety round out the application mix, but their collective growth lags diagnostics as reimbursement reforms reshape capital planning.

By End User: Hospitals & Clinical Labs Accelerate Procurement

Pharmaceutical and biotech companies retained 42.32% of 2025 spending, backed by multiyear pipeline funding that shields budgets from short-term volatility. Academic consortia such as MSCoreSys synchronized procurement across four German federal states, leveraging bulk discounts and shared spectral libraries to elevate Europe mass spectrometry market efficiency.

Hospitals and clinical laboratories are expected to add the most new systems, propelled by reimbursement shifts in Germany and the United Kingdom that now recognize LC-MS/MS for endocrine and therapeutic-drug tests. Charité–Universitätsmedizin Berlin alone processes 50,000 samples annually on a mixed triple-quadrupole and Orbitrap fleet, illustrating how clinical throughput needs reshape instrument specifications. As precision-medicine initiatives widen, the Europe mass spectrometry market size for hospital users will compound faster than any other end-user category through 2031.

Geography Analysis

Germany controlled 39.52% of Europe mass spectrometry market revenue in 2025, supported by MSCoreSys, which pools procurement and training across Berlin, Heidelberg, Mainz, and Munich. A Deutsche Forschungsgemeinschaft grant financed 12 new quadrupole-time-of-flight units for Hanover institutions, cementing academic demand. The country’s environmental agencies transitioned to time-of-flight ICP-MS for PFAS mapping, emphasizing Germany’s lead in high-resolution adoption.

The United Kingdom and France each hold robust installed bases across CROs and hospital networks. Synexa Life Sciences runs nine LC-MS/MS systems in Manchester for outsourced bioanalysis, while French labs accelerated hydrogen-carrier retrofits after helium prices tripled by 2025, illustrating how gas-supply shocks influence capital cycles. Clinical centers in both countries benefit from ISO 15189-validated platforms, encouraging in-house testing.

Spain represents the fastest-growing cluster at 8.32% CAGR. Its 974 biotech firms occupy 80 science parks and invested EUR 1.218 billion in R&D during 2023, channeling funds into Orbitrap and TOF platforms for proteomics and biosimilar analysis[3]AseBio, “AseBio Report 2023: Spanish Biotechnology Sector Analysis,” asebio.com. Hospital consortia leveraged national innovation grants to install 30 new triple-quadrupole instruments in 2025 alone. Italy mirrors this trend on a smaller scale, with Evotec’s Verona site expanding GLP-certified mass-spectrometry suites to serve EU and U.S. sponsors. Horizon-funded programs such as MSTARS and EU-OPENSCREEN distribute instrumentation to smaller member states, ensuring that Rest-of-Europe markets participate in method-standardization gains.

Competitive Landscape

Thermo Fisher Scientific, Waters, Agilent, Bruker, and other account for a dominant slice of Europe mass spectrometry market share, aided by ISO-accredited service networks that lower regulatory risk for clinical buyers. Thermo Fisher’s Orbitrap Astral targets single-cell proteomics with 200-Hz acquisition at 240,000 resolving power, while Waters’ Xevo TQ-XS consolidates pharmaceutical bioanalysis leadership by combining sub-pg/mL sensitivity with rugged pneumatic controls. Agilent’s 6546 Q-TOF and Bruker’s timsTOF Pro add ion-mobility separation that resolves co-eluting isomers in metabolomics.

Smaller entrants are exploiting whitespace in portable and benchtop formats. Microsaic Systems shipped compact quadrupoles to Italian pharma plants for real-time process monitoring, displacing bulky skid-mounted analyzers. TOFWERK’s cart-mounted TOF platforms support on-site VOC mapping for Austrian environmental agencies. Open-source software suites such as MZmine 3 and quantms erode proprietary data-analysis margins, prompting incumbents to add AI-driven compliance reporting.

Regulatory timelines shape switching costs; hospitals favor platforms already validated under ISO 15189, hindering late-stage challengers. The helium shortage accelerated R&D into hydrogen-compatible ion sources, an innovation race that could reorder vendor standings if operating-cost savings prove decisive. CRO expansions in Verona, Milan, and Manchester indicate enduring demand for multi-instrument, multi-vendor labs that can flex with sponsor requirements. Overall, competition revolves more around workflow integration and regulatory speed than raw resolving power.

Europe Mass Spectrometry Industry Leaders

Thermo Fisher Scientific Inc.

Bruker Corporation

Waters Corporation

Dani Instruments SpA

Agilent Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Frontage Europe consolidated its bioanalytical laboratory into a 2,500 m² facility near Milan, adding state-of-the-art quantitative mass-spectrometry, ligand-binding, and biomarker assay capacity.

- December 2025: Roche received CE-mark for its cobas Mass Spec Ionify reagent portfolio, enabling antibiotic therapeutic-drug monitoring and steroid-hormone and vitamin D testing on automated LC-MS/MS workstations.

Europe Mass Spectrometry Market Report Scope

As per the scope of the report, mass spectroscopy is an analytical chemistry technique used to identify the amount and type of chemical species present in a sample by measuring the mass-to-charge ratio and abundance of gas-phase ions. The scope of the report includes the details of different technology in terms of market importance and revenue share.

The Europe mass spectrometry market is segmented by platform into instruments, consumables, and software & services. By technology, the market is categorized into hybrid mass spectrometry, including triple quadrupole (tandem), quadrupole-TOF (Q-TOF), and FT-MS / orbitrap; single mass spectrometry, including ion trap, quadrupole, time-of-flight (TOF), and inductively-coupled plasma MS (ICP-MS) such as single quadrupole ICP-MS, triple quadrupole ICP-MS, and TOF-ICP-MS; magnetic-sector MS; and other specialized technologies. By application, the market is divided into the pharmaceuticals industry, biotechnology industry, clinical diagnostics, forensic & toxicology, and other applications. By end user, the segmentation includes pharmaceutical & biotechnology companies, academic & research institutes, contract research organizations, hospitals & clinical laboratories, and other end users. By country, the market is analyzed across Germany, the United Kingdom, France, Italy, Spain, and the rest of Europe. The report offers the value (in USD) for the above segments.

By Platform

| Instruments |

| Consumables |

| Software & Services |

By Technology

| Hybrid Mass Spectrometry | Triple Quadrupole (Tandem) |

| Quadrupole-TOF (Q-TOF) | |

| FT-MS / Orbitrap | |

| Single Mass Spectrometry | Ion Trap |

| Quadrupole | |

| Time-of-Flight (TOF) | |

| Inductively-Coupled Plasma MS (ICP-MS) | Single Quadrupole ICP-MS |

| Triple Quadrupole ICP-MS | |

| TOF-ICP-MS | |

| Magnetic-Sector MS | |

| Other Specialised Technologies |

By Application

| Pharmaceuticals Industry |

| Biotechnology Industry |

| Clinical Diagnostics |

| Forensic & Toxicology |

| Other Applications |

By End User

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Contract Research Organisations |

| Hospitals & Clinical Laboratories |

| Other End Users |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Platform | Instruments | |

| Consumables | ||

| Software & Services | ||

| By Technology | Hybrid Mass Spectrometry | Triple Quadrupole (Tandem) |

| Quadrupole-TOF (Q-TOF) | ||

| FT-MS / Orbitrap | ||

| Single Mass Spectrometry | Ion Trap | |

| Quadrupole | ||

| Time-of-Flight (TOF) | ||

| Inductively-Coupled Plasma MS (ICP-MS) | Single Quadrupole ICP-MS | |

| Triple Quadrupole ICP-MS | ||

| TOF-ICP-MS | ||

| Magnetic-Sector MS | ||

| Other Specialised Technologies | ||

| By Application | Pharmaceuticals Industry | |

| Biotechnology Industry | ||

| Clinical Diagnostics | ||

| Forensic & Toxicology | ||

| Other Applications | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| Contract Research Organisations | ||

| Hospitals & Clinical Laboratories | ||

| Other End Users | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How fast is demand for clinical LC-MS/MS assays growing across European hospitals?

Clinical diagnostics revenue is rising at a 9.82% CAGR through 2031 as hospitals replace immunoassays with high-specificity mass-spectrometry panels.

Which European country leads current mass-spectrometry sales?

Germany accounts for 39.52% of 2025 revenue, supported by coordinated public-research funding and nationwide core-facility networks.

What technology segment is expanding quickest under EU environmental rules?

ICP-MS, particularly triple-quadrupole configurations, is advancing at 8.75% CAGR on the back of PFAS and heavy-metal monitoring mandates.

Are portable mass spectrometers ready for regulatory-grade testing?

Field units now meet ISO 17025 in pilot programs, but broader EMA guidance is still pending, so adoption remains confined to early-stage food and forensic applications.

How are AI tools influencing laboratory productivity?

Machine-learning peak-integration and retention-time prediction cut manual review by up to 40%, enabling a single triple-quadrupole to process 700 samples per day.

Page last updated on: