Light Tank Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

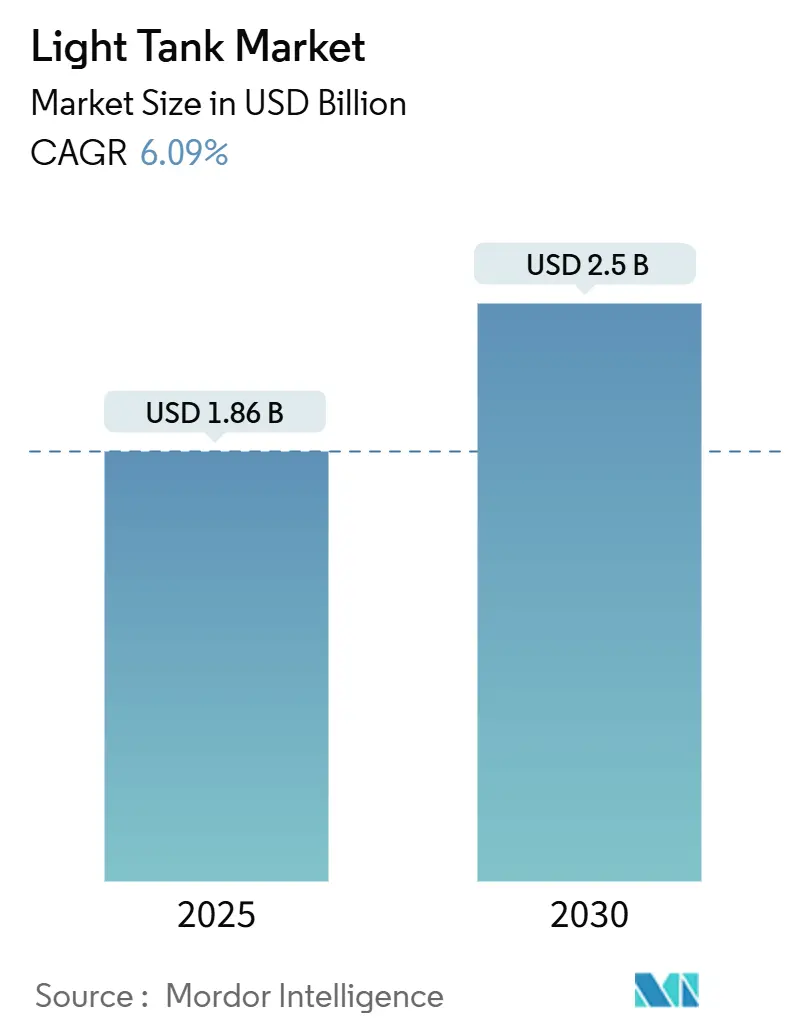

| Market Size (2025) | USD 1.86 Billion |

| Market Size (2030) | USD 2.5 Billion |

| Growth Rate (2025 - 2030) | 6.09% CAGR |

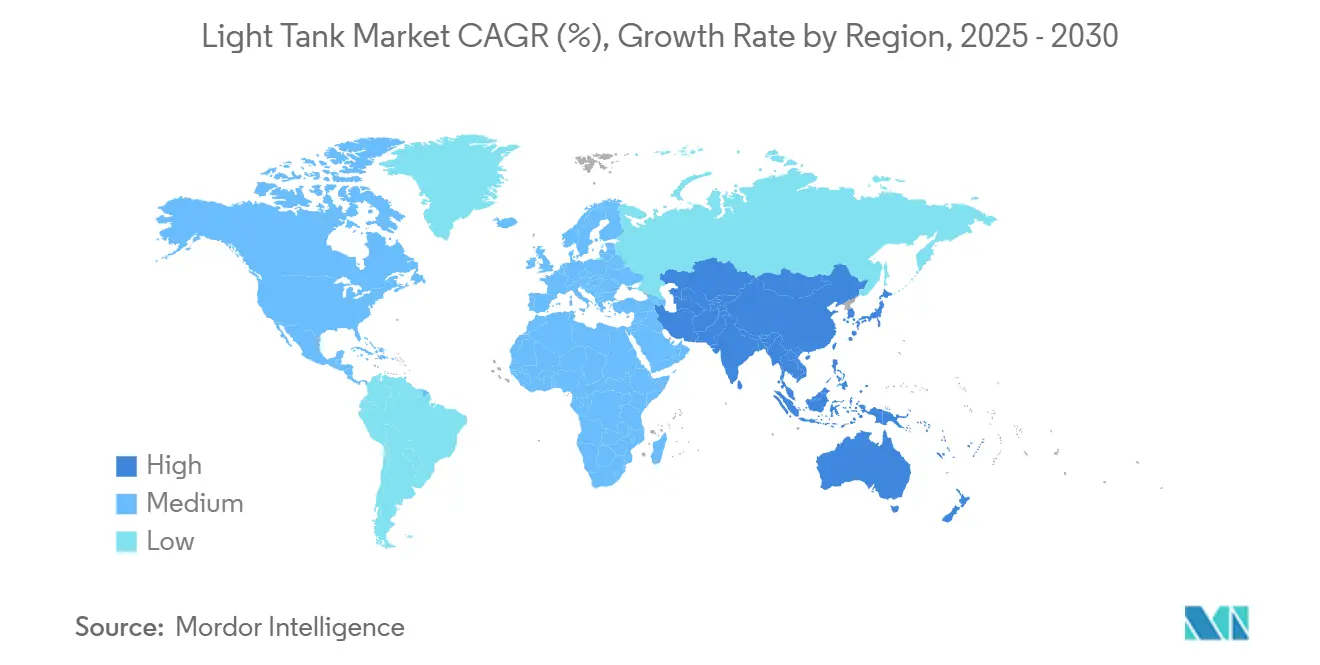

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

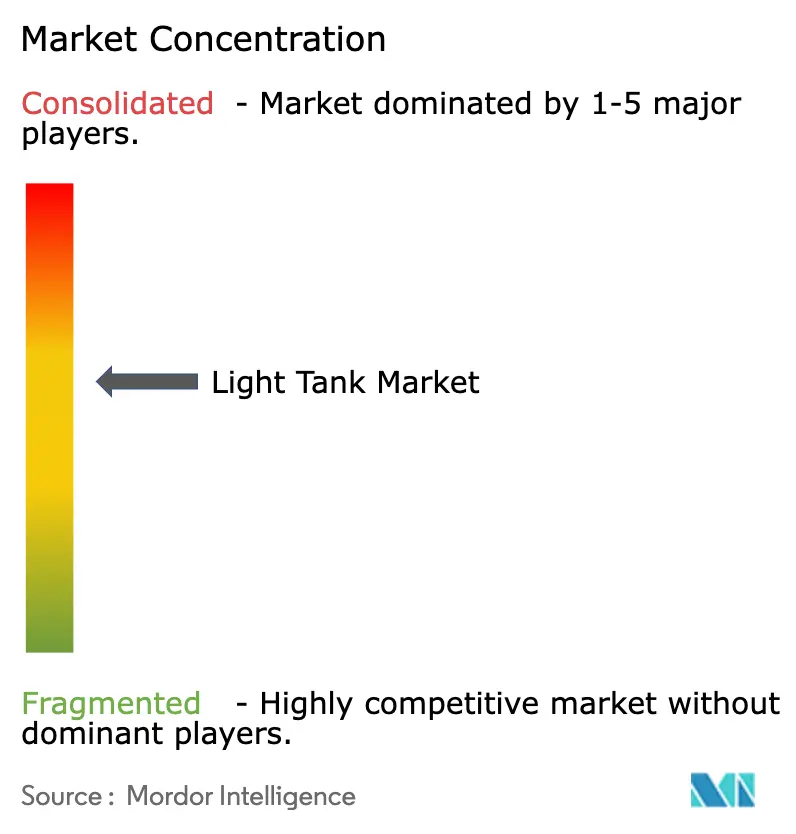

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Light Tank Market Analysis by Mordor Intelligence

The light tank market size reached USD 1.86 billion in 2025 and is projected to climb to USD 2.50 billion by 2030, translating to a 6.09% CAGR as militaries accelerate recapitalization programs worldwide. Mounting geopolitical tensions, lessons from recent high-intensity conflicts, and modular armor breakthroughs reinforce demand. At the same time, procurement frameworks that favor rapid deployment platforms sustain spending even as budgets tighten elsewhere. Diesel propulsion remains the incumbent technology because of global fuel logistics. However, hybrid- and full-electric concepts are advancing as forces seek silent mobility and lower thermal signatures for contested battlefields. High-altitude and expeditionary missions continue to influence design priorities toward lighter weight classes, with sub-10-ton platforms garnering interest from special operations units. Competitive intensity is growing as emerging suppliers in South Korea, Turkey, and India enter export markets, compelling established Western contractors to localize production and accelerate technology insertions into the light tank market. Supply-chain delays in advanced composites and electronic sub-systems threaten delivery schedules, underscoring the need for diversified sourcing and forward-order visibility.

Key Report Takeaways

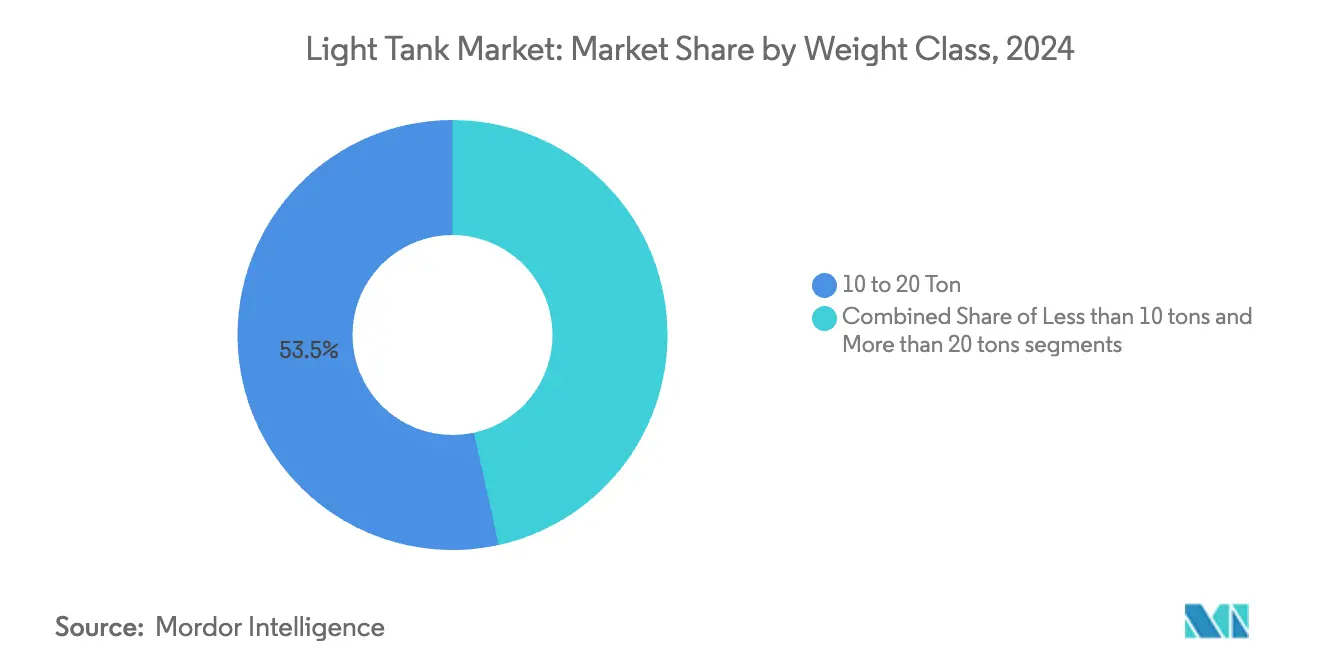

- By weight class, 10 to 20 ton platforms led with 53.45% of light tank market share in 2024, whereas the sub-10 ton segment is forecasted to expand at a 7.25% CAGR to 2030.

- By propulsion type, diesel systems held 91.25% of the light tank market size in 2024, while full-electric concepts record the fastest projected CAGR at 6.75% through 2030.

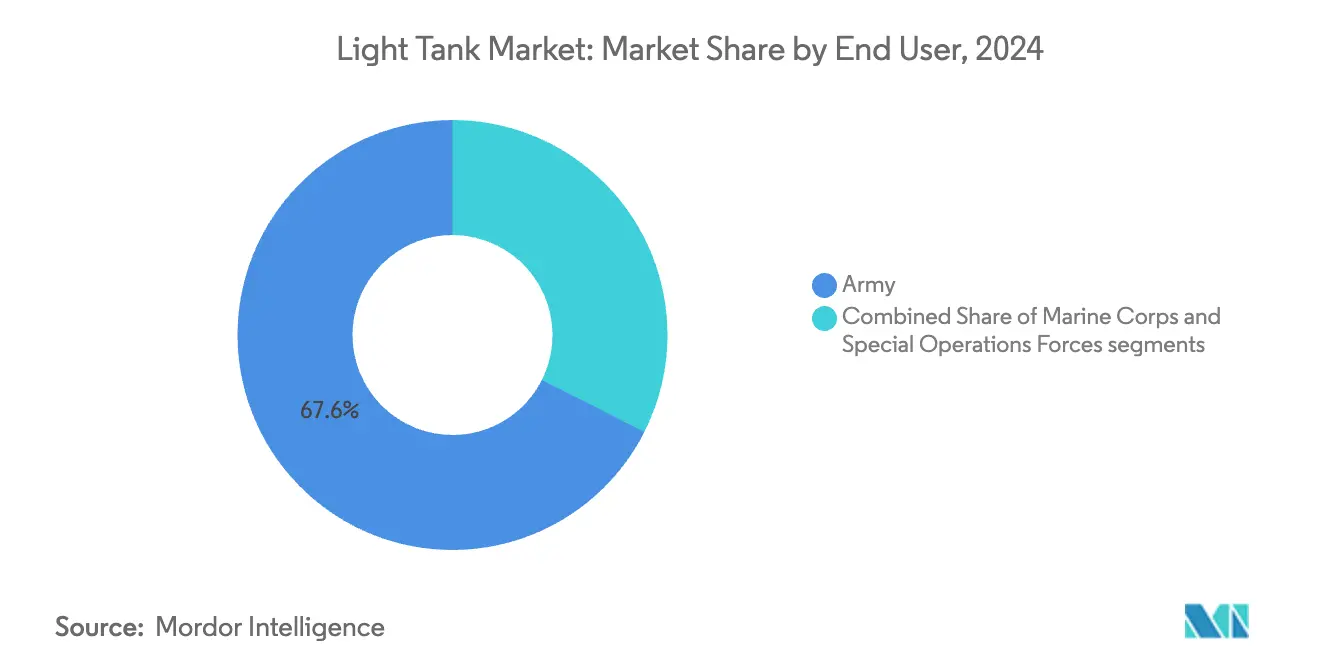

- By end-user, conventional armies accounted for 67.56% of the light tank market size in 2024; special operations forces display the highest anticipated CAGR at 7.23%.

- By caliber, 105–120 mm guns captured 77.67% of light tank market share in 2024, but sub-105 mm configurations are set to grow at 7.45% CAGR as weight reduction gains priority.

- By geography, North America commanded 29.87% of the light tank market in 2024, whereas Asia-Pacific is projected to register a 7.85% CAGR through 2030.

Global Light Tank Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing global defense modernization initiatives | +1.2% | NATO members; Asia-Pacific | Medium term (2-4 years) |

| Replacement of aging light armored vehicle fleets through procurement programs | +1.0% | North America; Europe | Short term (≤ 2 years) |

| Rising demand for highly mobile expeditionary and rapid-deployment forces | +0.8% | US, UK, France; regional powers | Medium term (2-4 years) |

| Technological advancements in modular armor and fire-control systems | +0.6% | Industrialized economies with R&D capacity | Long term (≥ 4 years) |

| Transition toward integrated manned-unmanned light tank formations | +0.4% | US, Israel, South Korea, select European nations | Long term (≥ 4 years) |

| Availability of export credit and financing incentives for international buyers | +0.3% | Emerging markets in Asia-Pacific, Middle East, Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Global Defense Modernization Initiatives

Rising top-line defense budgets have elevated armored vehicle procurement on spending agendas, with the US Army’s Mobile Protected Firepower contract positioning the 105 mm M10 Booker as a reference platform. In Europe, joint frameworks such as Germany’s Common Procurement Agreement enabled Lithuania to finalize a EUR 950 million (USD 1,119.75 million) Leopard 2A8 order that reinforces alliance interoperability targets. Asia-Pacific states match this pace: India’s Zorawar program and South Korea’s VT8 exports illustrate a pivot toward indigenous solutions that reduce import dependence while satisfying niche terrain requirements. Modernization efforts are also driven by rising expectations for open-architecture vetronics that can integrate AI-enabled situational-awareness suites. Altogether, these converging priorities sustain momentum in the light tank market as forces seek standardized yet upgradable platforms that align with joint operations doctrines.

Replacement of Aging Light Armored Vehicle Fleets

Cold-War inventories are approaching obsolescence, prompting accelerated replacement cycles across NATO and partner nations. The Czech Republic’s transition from legacy T-72 variants to Leopard 2A4/2A8 fleets exemplifies how end-of-life timelines translate into multi-year procurement pipelines. Poland similarly received 84 K2 Black Panther tanks by December 2024, highlighting a swift response to evolving regional security needs.[1]Administrator, “Poland has already received 84 K2 tanks from South Korea amid accelerated defense modernization,” Army Recognition, armyrecognition.com Such programs increasingly bundle active protection systems, digital backbones, and common weapon stations to address capability gaps rather than one-for-one swaps. US congressional funding tied to Ukrainian assistance has also augmented demand, as equipment donated abroad must be back-filled with modern equivalents. The result is a tangible near-term uplift to light tank market demand, reinforced by export-credit tools that enable middle-income buyers to engage in fleet renewal without straining budgets.

Rising Demand for Highly Mobile Expeditionary Forces

Doctrine is shifting toward rapid response formations capable of air-lift by C-130 or CH-47, creating performance thresholds that privilege weight discipline and compact profiles. The US Army’s requirement for air-transportable direct-fire support underpins the M10 Booker’s design, balancing 105 mm lethality with sub-20-ton weight. Special operations commands seek even lighter vehicles for helicopter internal-carriage, thereby accelerating development of less than 10-ton platforms with modular applique armor. NATO’s Article 5 readiness exercises underscore the need for units to redeploy across large distances on short notice, intensifying focus on self-deployability over rail or road. These operational imperatives feed directly into segmentation growth trajectories, with the sub-10 ton category forecast to log the fastest gains through 2030. The shift also influences supplier roadmaps, encouraging investment in lightweight composites and hybrid-electric drivetrains to protect mobility margins.

Technological Advancements in Modular Armor and Fire-Control Systems

Mission-tailorable protection packages now allow crews to trade armor weight against threat levels, a concept accelerated by adopting active protection systems such as Trophy on Leopard 2A8 derivatives. Fire-control upgrades are converging around AI-driven target classification and sensor fusion, as seen in the M1E3 Abrams development path expected to cascade technology to lighter classes. Panoramic sighting and assisted-engagement software improve first-round hit probabilities, making lighter platforms tactically significant despite inherent protection trade-offs. Compliance with emerging environmental directives also incentivizes research into recyclable armor ceramics and energy-efficient subsystems. These innovations elevate performance ceilings and lengthen refresh cycles, reinforcing steady adoption and upgrade revenues within the light tank market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Defense budget reallocation toward UAVs and precision-guided missile systems | -0.8% | Advanced military powers | Medium term (2-4 years) |

| Heightened vulnerability of light tanks to anti-tank guided missiles (ATGMs) and drones | -0.6% | Conflict zones; high-threat theaters | Short term (≤ 2 years) |

| Escalating R&D costs due to stricter global emission and environmental mandates | -0.4% | Developed nations with stringent environmental regulations | Long term (≥ 4 years) |

| Supply chain bottlenecks in advanced composite materials | -0.3% | Global, concentrated in high-tech manufacturing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Defense Budget Reallocation Toward UAVs and Precision-Guided Munitions

As unmanned systems and long-range fires deliver favorable cost-to-effect ratios, funding is migrating away from traditional armored fleets. The Pentagon’s prioritization of counter-drone weapons and hypersonic interceptors illustrates this internal competition for finite resources.[2]Dominik Minadeo, “Army awards BAE $656M for Bradley Fighting Vehicle,” InsideDefense.com, insidedefense.com European planners echo the trend, increasing missile inventories and ISR drone fleets at the expense of heavier ground systems. While existing recapitalization programs remain shielded, emerging budget cycles could defer additional light tank market acquisitions. Contractors respond by embedding swarm-defense suites and networked missile launchers into vehicle concepts to maintain relevance within future force structures. However, opportunity costs remain a tangible drag on long-term growth projections.

Heightened Vulnerability to ATGMs and Drones

Operational footage from contemporary conflicts shows even well-protected vehicles succumbing to man-portable missiles and loitering munitions, raising survivability concerns among procurement authorities. The cost imbalance between an inexpensive missile and a multi-million-dollar vehicle complicates return-on-investment analyses, particularly for lighter platforms with thinner base armor. The obligatory integration of active protection and hard-kill countermeasures inflates unit cost, potentially narrowing acquisition volumes. Moreover, sophisticated fire-control suites' electronic-warfare (EW) susceptibility introduces cyber and electromagnetic risks that must be mitigated through hardened architectures. These factors collectively temper enthusiasm and add complexity to capability justification processes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Weight Class: Strategic Mobility Takes Center Stage

The 10 to 20 ton category captured 53.45% of the light tank market share in 2024, making it the single largest contributor to the market size. Buyers favor this weight band because it combines survivability, 105 mm to 120 mm firepower, and cross-country agility without exceeding the load limits of standard military bridges, railcars, or C-17 airlifters. Vehicles in this range readily integrate active-protection suites and advanced panoramic fire-control sensors, capabilities that recent battlefield experience shows are essential against proliferating ATGMs. Its dominance also reflects a doctrinal shift toward balanced fleets that can confront peer adversaries yet still redeploy quickly across theaters. As a result, prime contractors prioritize upgrade packages and mid-life refresh kits for existing 10 to 20-ton fleets to preserve competitiveness through 2030.

Platforms exceeding 20 tons are projected to expand at a 7.25% CAGR through 2030, as armies operating in high-threat environments accept reduced strategic mobility in exchange for thicker composite armor and larger-caliber guns. Heavyweight designs attract customers, as they have observed the survivability advantage of up-armored vehicles in recent high-intensity conflicts. Conversely, sub-10-ton models retain niche relevance for airborne, special-operations, and peacekeeping missions where rapid insertion, low ground pressure, and political optics outweigh maximum protection. Manufacturers respond with modular architectures that allow operators to add or remove armor, sensors, and remote-weapon stations, effectively re-configuring a single chassis across weight classes to match evolving threat assessments and deployment constraints. This mission-tailorable approach sustains demand across the full weight spectrum while keeping lifecycle costs in check.

By Propulsion Type: Diesel Endures as Electrification Advances

Diesel engines retained a 91.25% share of the light tank market size in 2024, reflecting decades of field reliability and compatibility with established supply chains. Mature maintenance ecosystems and long-range endurance keep diesel the default choice for large-scale deployments. Nevertheless, environmental mandates and silent-watch requirements are reshaping future acquisition preferences. Hybrid-electric demonstrators now showcase fuel-burn cuts of up to 50%, extended silent-drive ranges, and lower infrared signatures, attributes attractive for reconnaissance and urban operations.

Full-electric solutions, projected to grow at a 6.75% CAGR, are progressing alongside military energy storage research. Lithium-iron-phosphate chemistries, scalable standard battery packs, and vehicle-to-grid concepts promise logistic simplification once the charging infrastructure matures. Interim hybrids are gaining favor as a transitional architecture, offering regenerative-brake energy capture without sacrificing rapid refuel options. Suppliers that can package electric drivetrains inside footprint-compatible housings stand to capture early mover advantage as defense ministries pilot clean-propulsion prototypes in the latter half of the decade.

By End-User: Conventional Forces Anchor Volumes, SOF Shapes Innovation

Conventional army formations dominated procurement with a 67.56% share in 2024, using light tanks to augment mechanized infantry and exploit gaps left by heavier main battle tanks in restrictive terrain. Volume orders from the US, India, and European allies ensure a stable baseline for production runs, facilitating cost amortization across supply networks. Marine Corps variants, optimized for littoral warfare and rapid amphibious landing, contribute to a specialized demand for corrosion-resistant coatings and buoyancy aids.

Special operations forces, while representing smaller absolute numbers, are poised for a 7.23% CAGR on account of mission-specific needs for air-portable fire support. Their propensity to field-test cutting-edge optics, lightweight armor, and advanced C4ISR suites accelerates technology maturation that subsequently migrates to regular units. Manufacturers respond with configurable mission kits, quick-detach armor plates, and modular sensor masts that can be tailored during deployment preparation, reflecting the broader shift toward plug-and-play architectures across the light tank market.

By Caliber Type: Lethality Mix Evolves with Mission Profiles

Systems armed with 105 to 120 mm cannons captured 77.67% of light tank market share in 2024, affirming military confidence in established ammunition stocks and target defeat tables. Their high-explosive and armor-piercing rounds allow engagement of entrenched positions and legacy armored threats at battlefield-relevant ranges. Recent trends, however, show growth in turret solutions below 105 mm, which are forecasted to expand at a 7.45% CAGR as forces pursue lighter turrets, higher elevation angles for urban combat, and compatibility with programmable airburst munitions that offset reduced kinetic energy.

Advancements in sabot-discarding projectiles and multi-mode fuzes permit smaller calibers to deliver near-MBT lethality against soft and semi-armored targets. Including coaxial anti-tank guided missile pods further augments firepower without increasing barrel diameter, supporting doctrinal moves toward precision rather than sheer gun caliber. Weapon-agnostic turret rings enable future caliber swaps should threat environments evolve, ensuring platform investments remain future-proof across diverse theaters.

Geography Analysis

North America accounted for 29.87% of the light tank market in 2024, supported by the US Army’s USD 6 billion Mobile Protected Firepower program to field 504 M10 Bookers through 2035. Robust budget allocations, mature industrial capacity, and a doctrine emphasizing combined-arms maneuver underpin sustained demand. Domestic suppliers benefit from multiyear contracts that de-risk R&D spending and fund innovations such as hybrid-electric drivetrains and AI-enabled decision aids. Canada’s NORAD modernization and Mexico’s border-security measures add incremental volume, yet US requirements remain the primary determinant of regional production schedules.

Asia-Pacific is the fastest-growing region, projected at 7.85% CAGR to 2030, fueled by China’s VT8 deployments, India’s high-altitude Zorawar initiative, and South Korea’s flourishing export campaigns. Indigenous programs respond to territorial disputes and a policy drive for defense self-sufficiency, elevating local value-added thresholds in procurement tenders. South Korea’s creation of manufacturing hubs in Australia and Romania exemplifies outward foreign direct investment (FDI) strategies that secure market access while propagating supply-chain resilience. Japan’s Type 10 upgrades and Australia’s Redback vehicle procurement further reinforce regional momentum for interoperable yet locally produced solutions.

Europe maintains a stable share anchored by collaborative frameworks like Germany’s Common Procurement Agreement, which enabled Lithuania’s Leopard 2A8 acquisition worth EUR 950 million (USD 1,119.75 million).[3]Halna du Fretay, “US Army selects BAE Systems to upgrade its Bradleys,” Army Recognition, armyrecognition.com Poland’s rapid intake of K2 tanks spotlights the region’s urgency to fortify NATO’s eastern flank and diversify beyond legacy suppliers. Simultaneously, European OEMs pursue US Foreign Military Sales (FMS) partnerships, reflecting a two-way exchange of technology and market access. In contrast, the Middle East and Africa offer episodic opportunities tied to security contingencies and commodity revenue cycles; Egypt’s procurement dialogues and Nigeria’s IDEX negotiations typify potential but volatile demand profiles.

Competitive Landscape

The light tank market is moderately concentrated, with heritage firms such as General Dynamics Corporation, BAE Systems plc, and FNSS Savunma Sistemleri A.Ş. retaining technology depth and global service networks. General Dynamics’ selection for the US MPF contract underscores the advantage of legacy combat-vehicle experience combined with digital-era upgrades. BAE Systems plc leverages Iron Fist active protection retrofits to defend installed platforms while eyeing next-generation hybrid proposals.

Emergent producers— Otokar, and India’s DRDO-L&T consortium—expand global footprints through cost-competitive offers and aggressive technology-transfer packages. Turkish and Indian platforms, priced below Western benchmarks yet equipped with export-compliant subsystems, now find traction among mid-income buyers balancing capability and affordability.

Strategically, OEMs emphasize open systems, additive manufacturing for spares, and lifecycle service contracts that assure operational readiness in contested supply contexts. Partnerships with domestic electronics firms allow bundling of sovereign C4ISR suites, satisfying defense-offset policies while differentiating bids. Competitive parity increasingly hinges on integrating defensive counter-UAS kits, predictive maintenance algorithms, and electric-drive retrofits, all of which define value propositions more sharply than pure armor thickness or main-gun caliber.

Light Tank Industry Leaders

General Dynamics Corporation

BAE Systems plc

FNSS Savunma Sistemleri A.Ş.

Elbit Systems Ltd.

Otokar Otomotiv ve Savunma Sanayi A.Ş

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Philippines received its third batch of Sabrah light tanks and an ASCOD-2 armored recovery vehicle from Israeli defense manufacturer Elbit Systems Ltd. via maritime transport as part of the Second Horizon phase of the Armed Forces of the Philippines modernization program.

- July 2024: The Defence Research and Development Organisation (DRDO) unveiled Zorawar, India's indigenous light tank prototype, for comprehensive testing. The tank incorporates air transport capabilities, high-angle firing systems, and auxiliary artillery functions, enhancing tactical and operational mobility.

Global Light Tank Market Report Scope

| Less than 10 Tons |

| 10 to 20 Tons |

| More than 20 Tons |

| Diesel |

| Hybrid-Electric |

| Full-Electric |

| Army |

| Marine Corps |

| Special Operations Forces |

| Less than 105 mm |

| 105 mm to 120 mm |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middile East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Weight Class | Less than 10 Tons | ||

| 10 to 20 Tons | |||

| More than 20 Tons | |||

| By Propulsion Type | Diesel | ||

| Hybrid-Electric | |||

| Full-Electric | |||

| By End User | Army | ||

| Marine Corps | |||

| Special Operations Forces | |||

| By Caliber Type | Less than 105 mm | ||

| 105 mm to 120 mm | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middile East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the light tank market today?

The light tank market size stood at USD 1.86 billion in 2025 and is forecasted to reach USD 2.50 billion by 2030 at a 6.09% CAGR.

Which region is growing the fastest for light tanks?

Asia-Pacific leads growth with a projected 7.85% CAGR, propelled by programs in China, India, and South Korea.

What weight class currently dominates procurement?

Platforms in the 10 to 20 tons range held 53.45% share in 2024, balancing air transportability with 105 mm firepower.

Why are militaries considering electric propulsion?

Hybrid- and full-electric drivetrains promise silent mobility, lower thermal signatures, and reduced fuel logistics while complying with emerging environmental mandates.

Which caliber is most common on modern light tanks?

Guns in the 105 to 120 mm bracket captured 77.67% market share in 2024 owing to established ammunition supply chains and versatile target-engagement profiles.

Page last updated on: