Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 99.17 Billion |

| Market Size (2031) | USD 206.15 Billion |

| Growth Rate (2026 - 2031) | 15.74% CAGR |

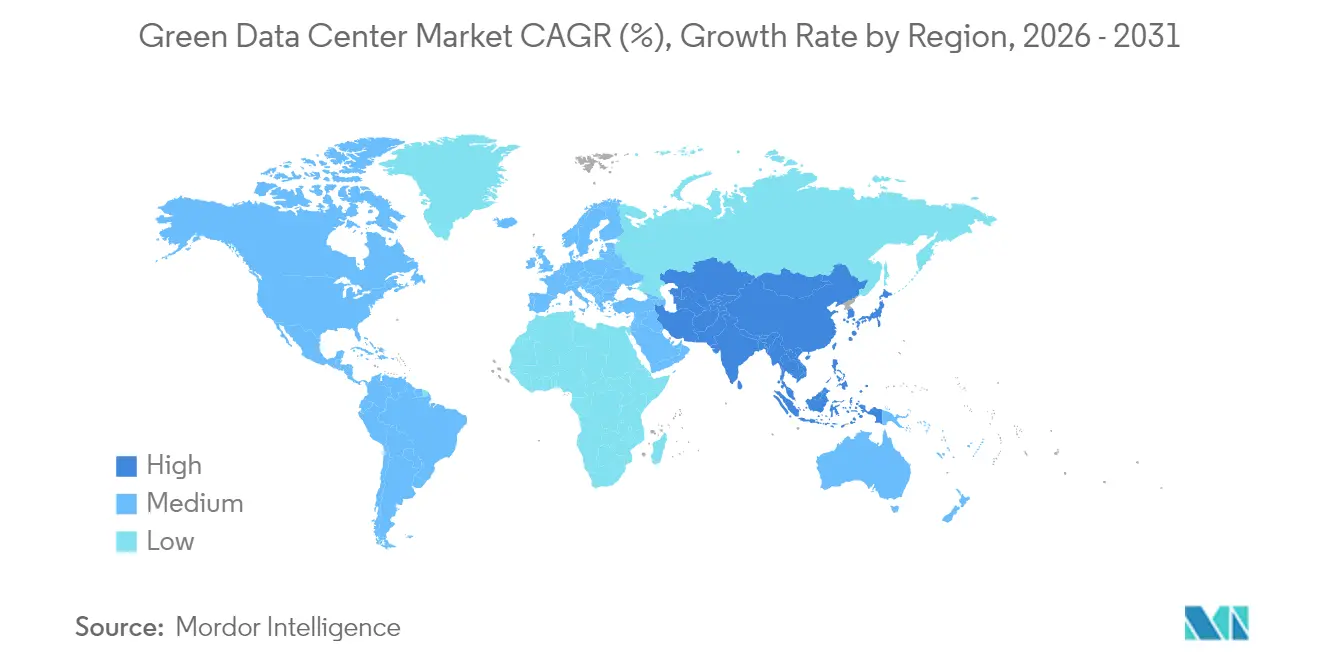

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

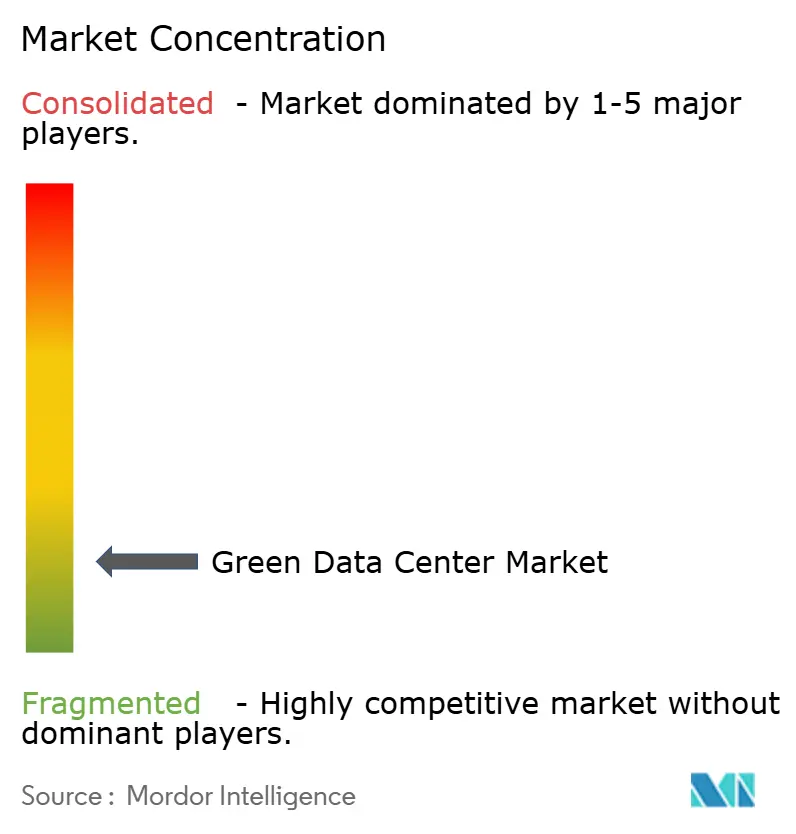

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Green Data Center Market Analysis by Mordor Intelligence

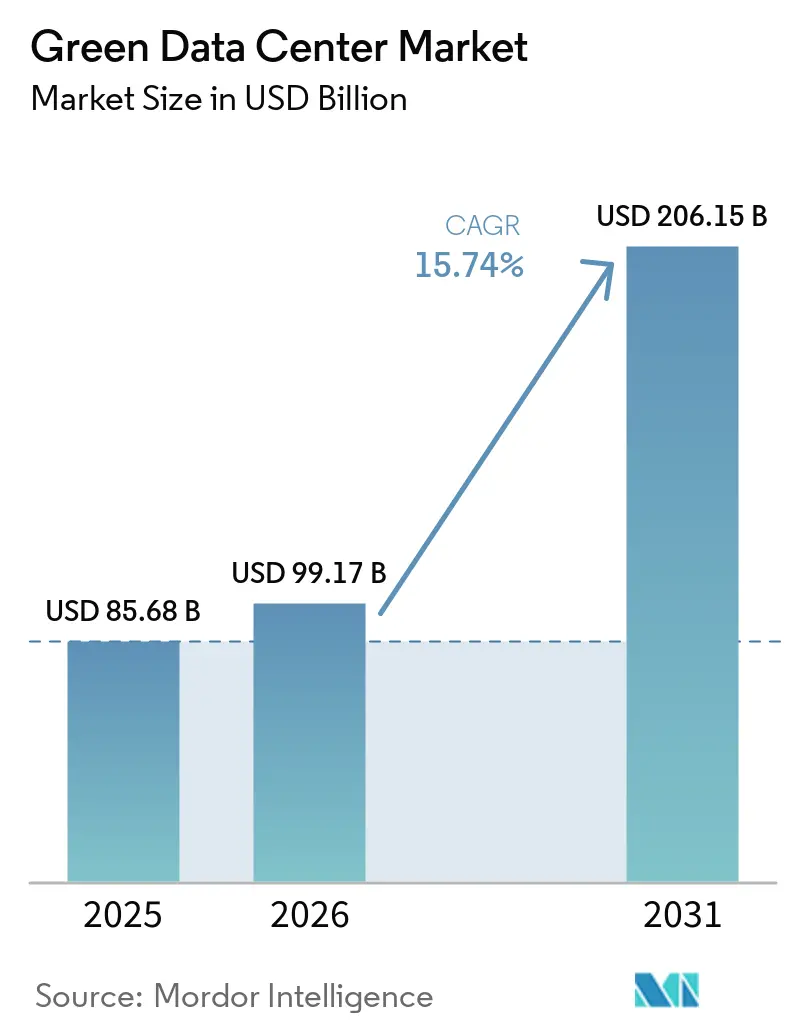

The Green Data Center Market size was valued at USD 85.68 billion in 2025 and is estimated to grow from USD 99.17 billion in 2026 to reach USD 206.15 billion by 2031, at a CAGR of 15.74% during the forecast period (2026-2031).

Operators are accelerating capital deployment into renewable power purchase agreements, liquid-to-chip cooling, and AI-enabled energy-management software to curb escalating electricity costs while meeting tightening ESG mandates. Hyperscale cloud providers influence technology standards by pre-booking multi-gigawatt renewable portfolios and publishing open-source liquid-cooling reference designs that colocation players later adopt. Regulatory bodies in OECD economies now benchmark facilities to a ≤1.3 PUE, prompting rapid retrofits and new-build designs that integrate waste-heat reuse and hydrogen-ready power systems. Investment appetite also benefits from premium pricing of location-based renewable-energy credits, which offsets a portion of up-front capital premiums for green builds, while AI workload growth sustains demand for high-density campuses equipped with low-GWP refrigerants.

Key Report Takeaways

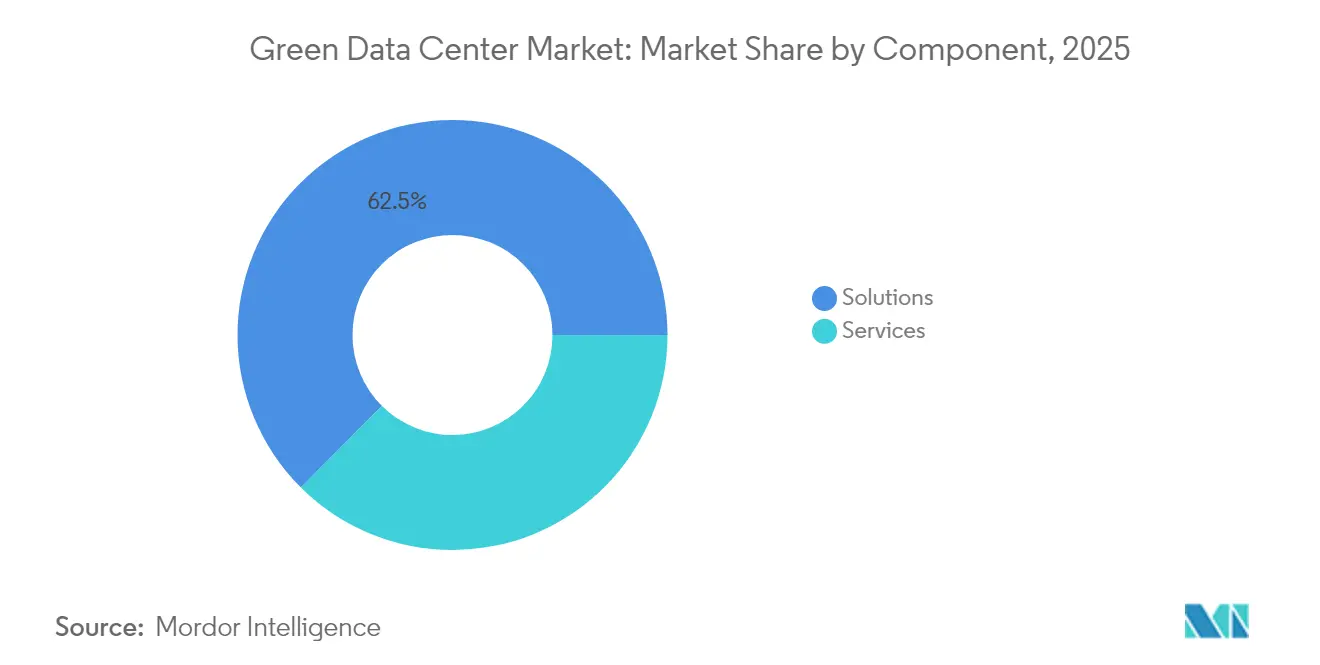

- By component, solutions captured 62.54% of the green data center market share in 2025; services are forecast to expand at a 15.38% CAGR to 2031.

- By data center type, colocation retained 36.62% revenue in 2025, whereas hyperscalers are advancing at a 16.21% CAGR through 2031.

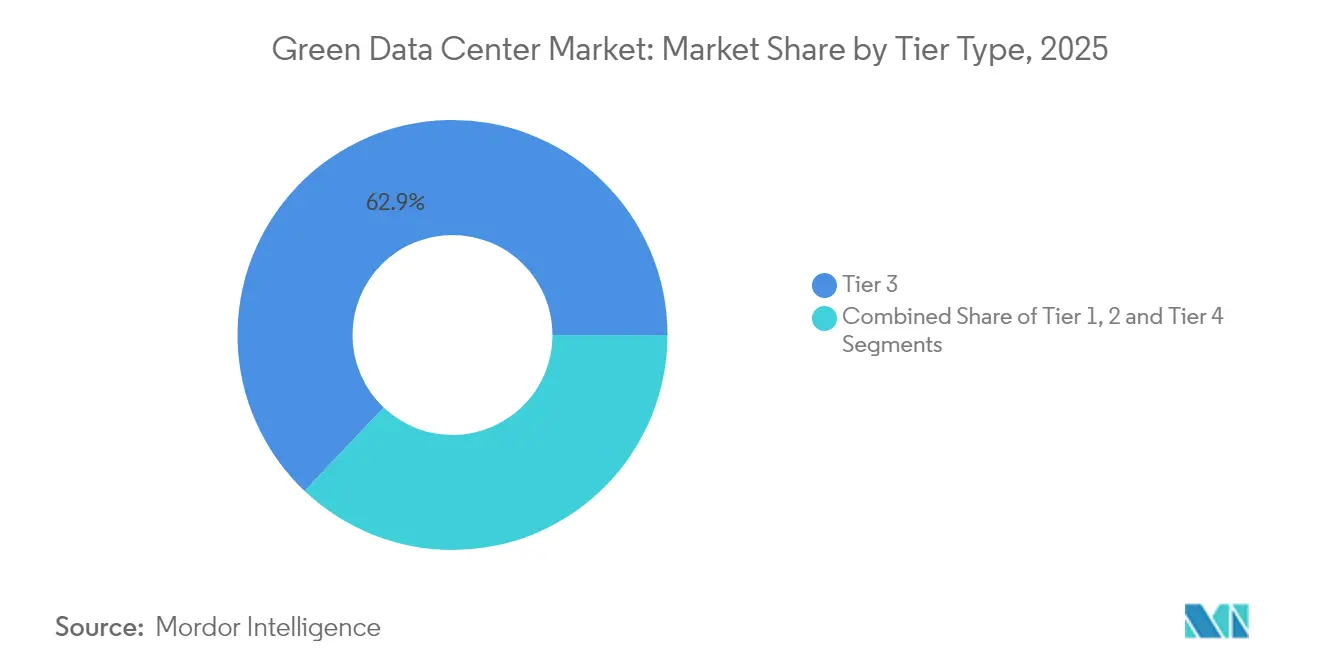

- By tier classification, Tier 3 represented 62.93% of 2025 revenue; Tier 4 is projected to post a 15.86% CAGR to 2031.

- By industry vertical, telecom and IT led with 26.88% of 2025 spending; government workloads are set to grow at 16.74% CAGR through 2031.

- By geography, North America accounted for 26.14% of 2025 revenue; Asia Pacific is expected to register the fastest 22.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Green Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale cloud build-outs shifting to 100% renewable power | +3.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Regulatory push for PUE ≤ 1.3 across OECD economies | +2.8% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| On-site hydrogen fuel-cell pilots in Greater than 10 MW campuses (2025–2028) | +1.9% | North America and EU core markets | Long term (≥ 4 years) |

| AI-workload waste-heat reuse for district heating networks | +2.1% | EU Nordic regions, expanding to North America | Medium term (2-4 years) |

| Location-based renewable-energy credits monetization | +1.7% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Liquid-cooling turnkey ecosystems from server-OEM alliances | + 2.5% | Global, led by hyperscale deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Cloud Build-outs Shifting to 100% Renewable Power

The green data center market is benefiting from hyperscale operators that now contract for wind, solar, and battery-hybrid projects sized well beyond their direct consumption. Amazon achieved company-wide 100% renewable energy in 2024, Microsoft has pledged carbon-negative operations by 2030, and Google channels surplus renewable power into municipal district-heating projects that further monetise waste heat.[1]Google Sustainability, “Finland Data Center Heat Re-use Project,” Google, google.com These strategies help operators lock in price-stable electricity, create hedging income through renewable-energy credit sales, and establish procurement templates that colocation landlords subsequently follow

Regulatory Push for PUE ≤ 1.3 Across OECD Economies

New directives in the EU and updated U.S. energy codes require transparent reporting of PUE, water-usage effectiveness, and carbon intensity in the green data center market. Germany’s Energy Efficiency Act mandates cooling-efficiency disclosures, while AWS reported a global PUE of 1.15 in 2024, proving compliance is feasible when AI-based workload scheduling and liquid cooling are combined. Operators that retrofit early capture cost savings from lower fan energy and reduced mechanical redundancy, improving competitiveness during colocation contract renewals. Penalties for non-compliance increase each fiscal year, creating a near-term rush to commission energy-efficient equipment.

On-site Hydrogen Fuel-Cell Pilots in Greater than 10 MW Campuses (2025–2028)

Microsoft, partnering with Caterpillar, and Bloom Energy are testing multi-megawatt proton-exchange-membrane systems that can displace diesel backup sets and feed grid-balancing markets during low-renewable output windows.[2]ECL, “Hydrogen Fuel-Cell Pilot Overview,” ECL, ecl.com Although current hydrogen fuel pricing inflates operational expenditure, incentives under clean-hydrogen production tax credits narrow the gap. Early pilots demonstrate ancillary-service income that partially offsets capital cost, positioning hydrogen as a credible long-term pathway to scope-1 emissions elimination.

AI-workload Waste-Heat Reuse for District Heating Networks

As rack densities exceed 80 kW, liquid cooling withdraws high-grade heat that Nordic utilities capture for municipal heating loops. Equinix expanded its heat-export program to multiple European metros, while HPE integrates heat-exchanger modules directly on board trays. Monetising waste heat transforms a cost centre into a revenue line, shortening payback periods for high-density retrofits. Urban stakeholders endorse these schemes as they decarbonise their own heating portfolios without investing in separate boilers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front CAPEX premium (30-40%) versus brownfield retrofits | -2.3% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Limited green-power grid capacity in emerging economies | -1.8% | APAC emerging markets, MEA, Latin America | Long term (≥ 4 years) |

| Scarcity of recycled-water rights near urban cores | -1.1% | North America Southwest, APAC urban centers | Medium term (2-4 years) |

| Supply-chain volatility for low-GWP refrigerants (R-718, R-1234yf) | -1.4% | Global, with concentration in advanced cooling deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Up-front CAPEX Premium (30–40%) Versus Brownfield Retrofits

High-performance insulation, structured cabling rated for immersion-cooled racks, and on-site solar plus storage systems inflate build costs by as much as 40% relative to conventional shells. Construction inputs such as low-carbon concrete and phase-change thermal walls remain supply-constrained in 2025, adding schedule risk to green data center market deployments. Smaller operators often pivot to incremental efficiency retrofits instead of full green builds, slowing overall capacity additions until component prices normalise.

Limited Green-Power Grid Capacity in Emerging Economies

Renewable resource potential across Southeast Asia, the Middle East, and parts of Latin America is high, yet transmission infrastructure lags behind power-purchase demand. Developers negotiate private-wire solar deals or deploy gas-peaking turbines as bridging solutions, both of which raise effective carbon intensity and slow hyperscaler site selection. Partnerships with utilities to co-fund grid renewables can mitigate the gap, but execution timelines stretch beyond standard campus delivery cycles, dragging on green data center market adoption rates.[3]African Data Center Association, “Renewable Grid Challenges in Emerging Markets,” africadca.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominate Despite Services Acceleration

Solutions generated 62.54% of 2025 revenue, underpinning the green data center market size leadership in capital intensity. Operators prioritised power-conditioning gear, heat-recovery chillers, and artificial-intelligence DCIM software to satisfy efficiency mandates, while liquid-to-chip cooling lines experienced double-digit unit shipment growth. Services, though smaller in absolute value, are forecast for 15.38% CAGR as facility owners engage specialists for lifecycle sustainability audits, AI-driven workload orchestration, and ESG reporting.

Power-train upgrades, including 98%-efficient UPS modules and smart grid interfaces, strengthened resilience and trimmed operating costs. Cooling solutions shifted from raised-floor air handlers to rear-door heat exchangers coupled with warm-water loops. On the services side, integration partners now bundle carbon accounting dashboards and renewable-certificate trading platforms. This professionalisation of sustainability management marks a structural uplift in the green data center industry.

By Data Center Type: Hyperscalers Drive Transformation

Colocation firms held 36.62% of 2025 spending as enterprises continued outsourcing strategies, yet hyperscalers outpaced the field with a 16.21% CAGR, enlarging the overall green data center market size for self-owned capacity. Their billion-dollar renewable PPAs and custom-designed immersion systems set technology adoption curves that trickle down into retail colocation suites.

Enterprise operators remained steady, refreshing brownfield assets with containment pods and modular battery storage to meet board-level emissions targets. Edge micro-facilities, though nascent, adopted passive cooling and solar-powered UPS to support 5G cell-site processing. The procurement heft of cloud majors keeps component suppliers’ cost curves descending, indirectly lowering barriers for second-tier providers.

By Tier Type: Tier 4 Emerges Despite Tier 3 Dominance

Tier 3 accounted for 62.93% of 2025 turnover, reflecting its balanced uptime and cost profile within the green data center market. However, Tier 4 is projected to expand at 15.86% CAGR as AI-driven analytics, fintech clearing, and public-sector command centres require 99.995% availability aligned with net-zero targets.

Tier 4 campuses in the green data center market now integrate two independent renewable power feeds, redundant liquid-cooling loops, and AI-embedded predictive maintenance to squeeze idle energy. Tier 1-2 operators face upgrade pressure; many adopt modular flywheel UPS and direct evaporative cooling to narrow efficiency gaps. This migration path sustains equipment vendors’ order books, especially for control-software updates that harmonise cross-tier architectures.

By Industry Vertical: Government Accelerates Beyond Telecom Leadership

Telecom and IT services in the green data center market contributed 26.88% of 2025 revenue, anchored by network virtualisation and content-delivery nodes that require ultra-efficient hosting. Government workloads, while historically conservative, are forecast to grow 16.74% CAGR as agencies sign 10-year renewable contracts to comply with federal carbon budgets. This shift enlarges addressable demand for certified sustainable colocation.

Healthcare tightens focus on electronic health-record hosting within carbon-neutral facilities, and financial-service firms embed environmental criteria into third-party vendor audits. Manufacturing accelerates digital-twin deployment at the edge, leveraging low-latency, energy-optimised micro-sites. Media streaming leaders negotiate long-term renewable PPAs to offset rising transcode compute loads, collectively expanding the green data center market.

Geography Analysis

North America accounted for 26.14% revenue in 2025, buttressed by reliable renewable generation, robust tax incentives, and hyperscale activity clustering around Virginia, Oregon, and Texas. State regulators impose granular ESG disclosures, prompting early adoption of AI-based energy management that pushes the regional green data center market ahead in technology maturity.

Asia Pacific is forecast for a 22.86% CAGR through 2031 as Japan’s carbon-neutral data center initiative, India’s data-sovereignty policy, and Australia’s renewable energy zones catalyse new builds. Grid bottlenecks in Southeast Asia have spurred private-wire solar plus battery deals, positioning the region for leap-frog efficiency gains once interconnect upgrades materialise.

Europe maintains a central role through unified policy such as the Climate Neutral Data Centre Operator Pact. Nordic campuses leverage near-free cooling and ample hydropower, exporting heat into municipal networks and thereby lowering effective PUE to 1.1. Southern Europe accelerates solar-hybrid projects, and Germany’s corporate PPAs fuel multicloud adoption in Frankfurt. Collectively, regional policy coherence sustains investment momentum within the green data center market

Competitive Landscape

The vendor ecosystem in the green data center market shows moderate concentration as Schneider Electric, Vertiv, and Dell Technologies cross-license liquid-cooling patents and integrate AI-driven DCIM into end-to-end offerings. Schneider’s acquisition of Motivair extends vertical control over cold-plate manufacturing, while Vertiv partners with NVIDIA for rack-ready immersion kits that simplify AI cluster deployment.

Dell, HPE, and Cisco embed telemetry APIs facilitating dynamic thermal mapping, differentiating equipment through software rather than solely hardware efficiency. Colocation incumbents Equinix and Digital Realty issue green bonds and joint ventures to fund 1 GW-plus expansion phases that anchor the green data center market in mature regions.

Emerging disruptors drive niche innovation: Edged Energy commercialises waterless cooling for arid geographies, Green Edge Compute positions urban micro-sites that monetise waste heat, and Stack Infrastructure advances prefabricated hydrogen-ready modules. These challengers keep pricing disciplined and accelerate knowledge diffusion, balancing market power among incumbents.

Green Data Center Industry Leaders

Fujitsu Ltd

Cisco Systems Inc.

Hewlett Packard Enterprise Co.

Dell Technologies Inc.

Hitachi Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: NTT DATA announced USD 10 billion multi-year expansion featuring 370 MW of liquid-cooled capacity and a 26% emissions reduction.

- January 2025: Edged Data Centers opened an Irving, Texas site delivering 24 MW on a waterless platform, cutting annual water use by 95 million gallons.

- December 2025: CoreWeave partnered with Dell for liquid-cooled PowerEdge XE9712 servers, achieving rack-level 1.4 exaFLOPS performance.

- October 2025: Equinix formed a USD 15 billion xScale venture with GIC and CPP Investments, targeting 1.5 GW hyperscale builds.

Global Green Data Center Market Report Scope

A green data center is a repository for storing, managing, and distributing data, in which the mechanical, electrical, lighting, and computer systems are designed to provide maximum energy efficiency and minimum environmental impact. The construction and operation of a green data center include advanced technologies and strategies.

The green data center market is segmented by service (system integration, monitoring service, and professional service), solution (power, servers, management software, networking technologies, cooling, and other solutions), user (colocation providers, cloud service providers, and enterprises), industry vertical (healthcare, financial services, government, telecom & IT, and other industry verticals), and geography.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Component

| By Service | System Integration |

| Monitoring Services | |

| Professional Services | |

| Other Services | |

| By Solution | Power |

| Cooling | |

| Servers | |

| Networking Equipment | |

| Management Software | |

| Other Solutions |

By Data Center Type

| Colocation Providers |

| Hyperscalers/Cloud Service Providers |

| Enterprise and Edge |

By Tier Type

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

By Industry Vertical

| Healthcare |

| BFSI |

| Government |

| Telecom and IT |

| Manufacturing |

| Media and Entertainment |

| Other Verticals |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia_Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | By Service | System Integration | |

| Monitoring Services | |||

| Professional Services | |||

| Other Services | |||

| By Solution | Power | ||

| Cooling | |||

| Servers | |||

| Networking Equipment | |||

| Management Software | |||

| Other Solutions | |||

| By Data Center Type | Colocation Providers | ||

| Hyperscalers/Cloud Service Providers | |||

| Enterprise and Edge | |||

| By Tier Type | Tier 1 and 2 | ||

| Tier 3 | |||

| Tier 4 | |||

| By Industry Vertical | Healthcare | ||

| BFSI | |||

| Government | |||

| Telecom and IT | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Other Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia_Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the green data center market in 2031?

The market is forecast to reach USD 206.15 billion by 2031, expanding at a 15.74% CAGR.

Which region is expected to grow fastest?

Asia Pacific is projected to post a 22.86% CAGR, driven by renewable-energy build-outs and digital-transformation initiatives.

Why are hyperscalers critical to market growth?

Hyperscalers commit multibillion-dollar renewable PPAs and set technology standards—such as open liquid-cooling designs—that secondary providers later adopt, accelerating overall market uptake.

How do operators monetise sustainability investments?

In mature markets, facilities sell location-based renewable-energy credits and, in colder climates, convert waste heat into revenue by feeding local district-heating networks.

Page last updated on: