Emerging Non-Volatile Memory Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

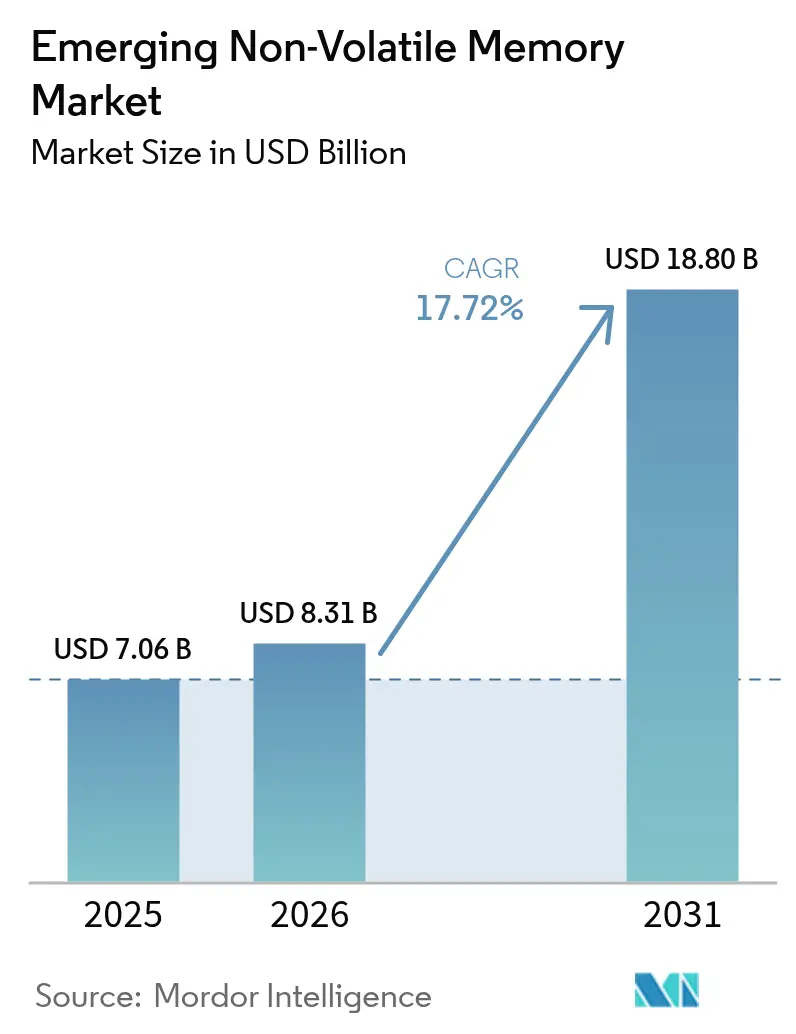

| Market Size (2026) | USD 8.31 Billion |

| Market Size (2031) | USD 18.8 Billion |

| Growth Rate (2026 - 2031) | 17.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

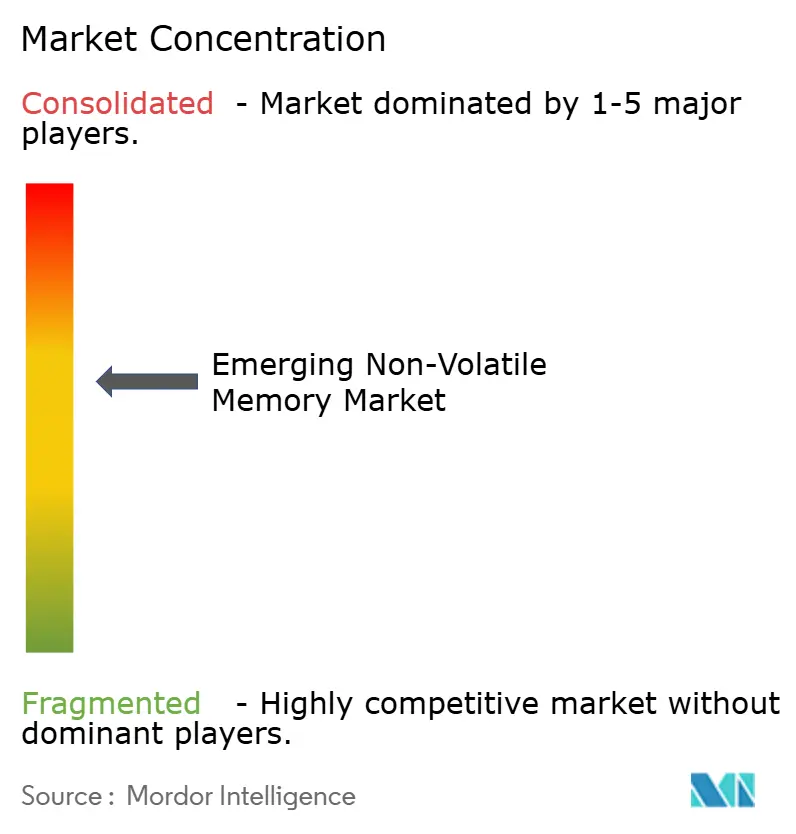

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Emerging Non-Volatile Memory Market Analysis by Mordor Intelligence

The emerging non-volatile memory market size was valued at USD 7.06 billion in 2025 and estimated to grow from USD 8.31 billion in 2026 to reach USD 18.8 billion by 2031, at a CAGR of 17.72% during the forecast period (2026-2031). Heightened demand for sub-microsecond latency in data-center AI training, the electrification of automobiles, and rising edge-AI inference workloads are accelerating the structural migration away from legacy flash toward magnetoresistive, resistive, phase-change, and ferroelectric technologies. Public-sector incentives under the U.S. CHIPS and Science Act, the European Union Chips Act, and comparable Chinese subsidies are redirecting capital into domestic memory fabs. Meanwhile, the foundry qualification of embedded MRAM at 22 nanometers and below enables designers to consolidate logic and storage on a single die. Automotive electrification is another catalyst, as high-temperature retention and instant-on capability meet the requirements of Advanced Driver Assistance Systems, battery management units, and domain controllers. Competitive strategies center on vertical integration, licensing, and portfolio diversification as incumbent NAND suppliers defend their position against pure-play startups offering drop-in flash replacements across industrial and automotive segments.

Key Report Takeaways

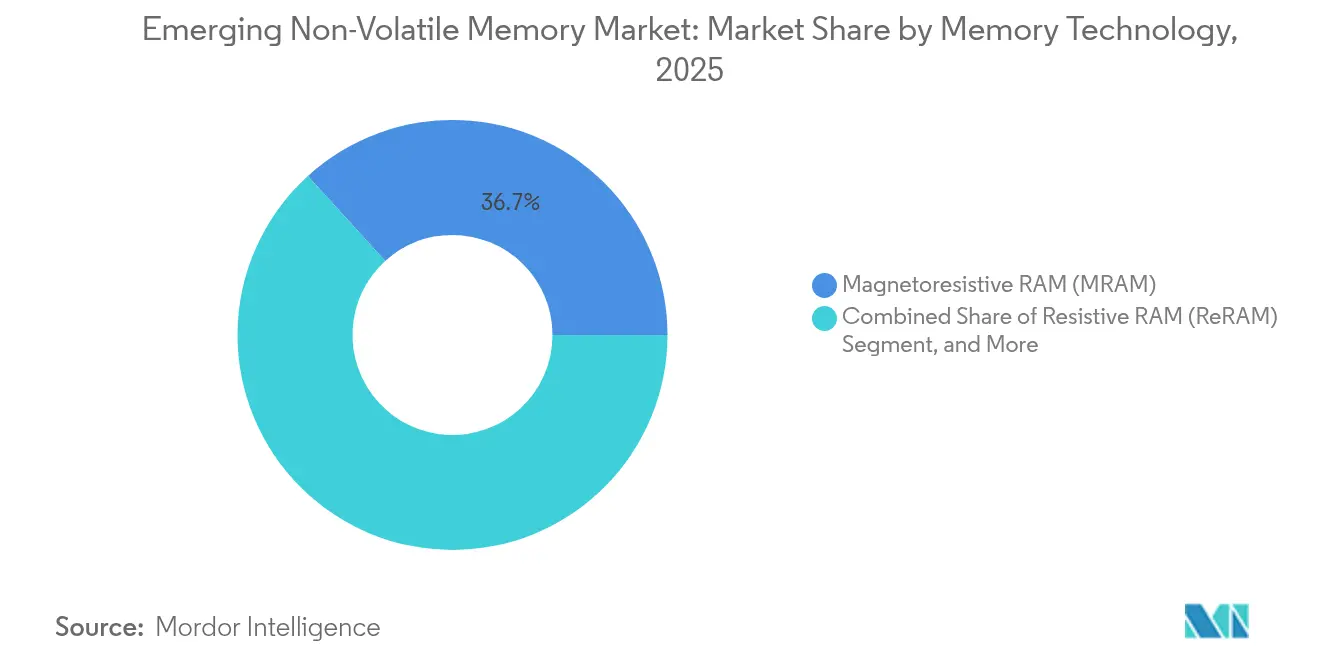

- By memory technology, magnetoresistive RAM led the emerging non-volatile memory market with a 36.74% revenue share in 2025; resistive RAM is forecast to expand at a 20.12% CAGR through 2031.

- By type, stand-alone modules accounted for 63.12% of the 2025 shipments in the emerging non-volatile memory market, while embedded variants are projected to grow at a 18.67% CAGR through 2031.

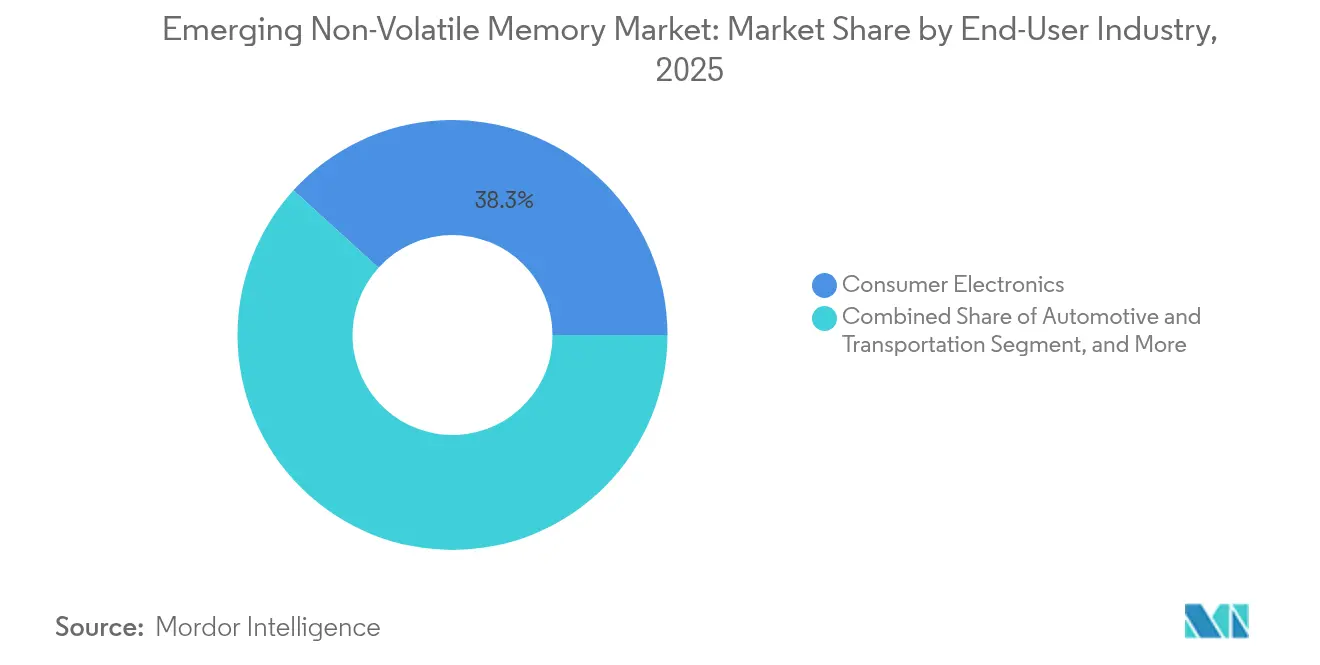

- By end-user industry, consumer electronics accounted for 38.25% of the demand in 2025 for the emerging non-volatile memory market; automotive and transportation are set to advance at a 21.05% CAGR between 2026 and 2031.

- By application, cache memory and enterprise storage captured 43.20% of the 2025 revenue of the emerging non-volatile memory market; mobile phones and wearables are expected to rise at a 21.10% CAGR through 2031.

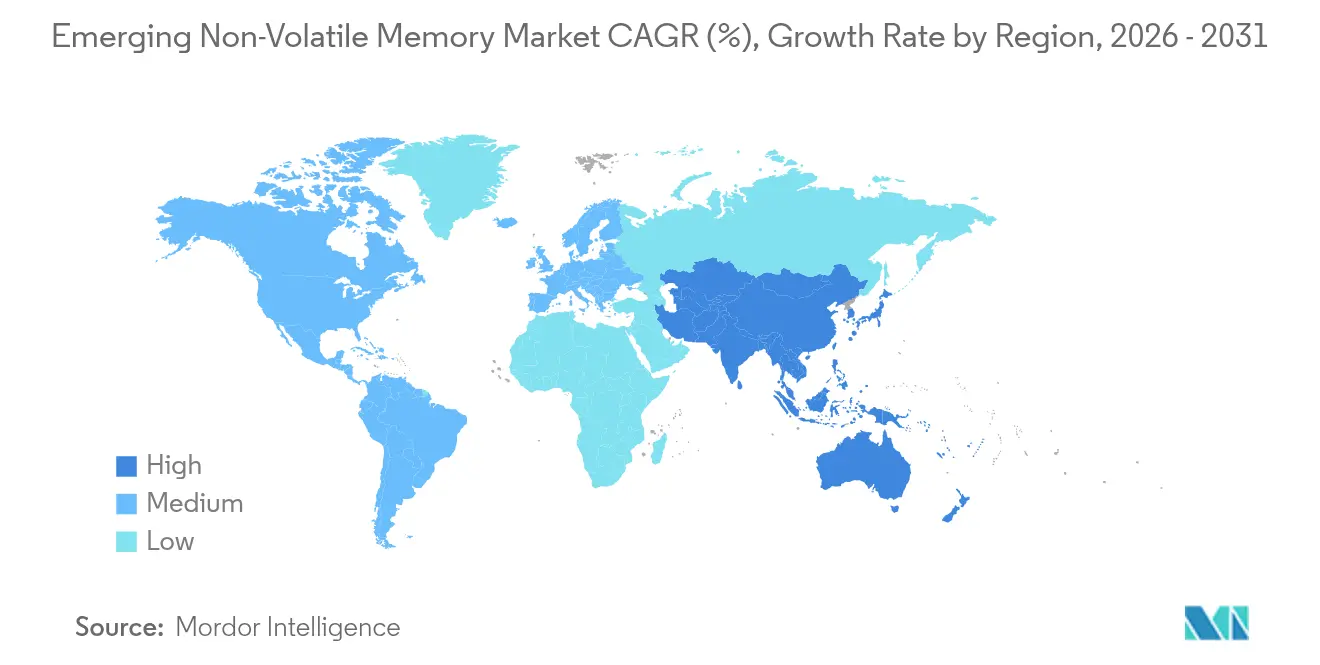

- By geography, the Asia Pacific region dominated the emerging non-volatile memory market with a 40.35% share in 2025 and is also the fastest-growing region, expanding at a 19.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Emerging Non-Volatile Memory Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding demand for low-latency, high-bandwidth storage in AI data centers | +3.2% | Global, strongest in North America and Asia Pacific | Medium term (2-4 years) |

| Shift toward energy-efficient memory for IoT and wearable devices | +2.8% | Global, led by Asia Pacific consumer-electronics hubs | Short term (≤ 2 years) |

| Automotive electrification and ADAS requiring high-temperature, high-endurance NVM | +3.5% | Europe, North America, Asia Pacific automotive corridors | Medium term (2-4 years) |

| Foundry qualification of embedded MRAM and ReRAM below 28 nm enables flash replacement | +3.1% | Asia Pacific fabs, spill-over to North America | Medium term (2-4 years) |

| Market pull for in-memory compute in edge-AI chips | +2.9% | Global, early adoption in North America and Asia Pacific | Long term (≥ 4 years) |

| Government semiconductor-sovereignty incentives expanding domestic fabs | +2.6% | United States, European Union, China, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding Demand for Low-Latency, High-Bandwidth Storage in AI Data Centers

Hyperscale operators running large language models are hitting the memory wall, where the energy used to shuttle data between DRAM and NAND exceeds the energy used for computation. Emerging non-volatile memory supplies sub-100-nanosecond access and byte-addressability, allowing training datasets to persist in place through power cycles and cutting reliance on costly DRAM tiers. Samsung’s 1-gigabit spin-transfer-torque MRAM prototype demonstrated 10-nanosecond writes in 2024, validating the latency advantage over NAND.[1]Samsung Electronics, “1 Gb STT-MRAM with 10 ns Write Speed,” samsung.com The discontinuation of Intel Optane in 2022 intensified the push toward MRAM and ReRAM tiers. As transformer models scale past one trillion parameters, persistent memory becomes essential for frequent checkpointing, boosting adoption across recommender systems and fraud-detection pipelines.

Shift Toward Energy-Efficient Memory for IoT and Wearable Devices

Battery-constrained devices are replacing serial NOR flash with ferroelectric RAM and MRAM to remove high write currents and erase-before-write overhead. STMicroelectronics disclosed in 2024 that embedded FRAM lowered system energy by 40% in ultra-low-power microcontrollers.[2]STMicroelectronics, “40% Energy Reduction with Embedded FRAM,” st.com Always-on voice assistants and continuous health monitors need instant wake-up and zero standby leakage, benefits that align with FRAM’s sub-microampere standby current. European Union Ecodesign rules, which mandate energy-efficiency labeling, are reinforcing adoption.

Automotive Electrification and ADAS Requiring High-Temperature, High-Endurance NVM

Advanced Driver Assistance Systems, battery-management units, and over-the-air firmware updates rely on memory that retains data at temperatures above 125 °C and withstands 10^9 write cycles. Everspin’s automotive-grade MRAM, qualified to AEC-Q100 Grade 1, demonstrates data retention at 150 °C. Infineon partnered with Everspin in 2024 to integrate 256-megabit MRAM into its AURIX microcontrollers, enabling Level 3 autonomy that requires instant boot and fail-operational redundancy. Compliance with ISO 26262 functional safety standards amplifies the demand for predictable failure modes.

Foundry Qualification of Embedded MRAM Below 28 nm Enables Flash Replacement

TSMC qualified a 22-nanometer embedded MRAM platform for volume production in 2024, letting designers co-integrate logic, SRAM, and non-volatile storage on a single die. GlobalFoundries followed with a 12-nanometer eMRAM process that spans −40 to 125 °C and features a 10-nanosecond write speed. Eliminating external serial flash reduces bill-of-materials costs, board area, and boot latency, especially in secure microcontrollers and edge AI accelerators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High fabrication cost and yield challenges at sub-20 nm nodes | -2.1% | Global, most acute where advanced-node capacity is scarce | Short term (≤ 2 years) |

| Lack of unified standards for controller interfaces and software stacks | -1.8% | Global, slowing adoption in enterprise and automotive segments | Medium term (2-4 years) |

| Device-level endurance variability limiting high-write workloads | -1.3% | Global, impacting data-center and industrial applications | Medium term (2-4 years) |

| Supply-chain dependence on critical magnetic and rare-earth materials | -1.5% | Global, heightened risk in single-source regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Fabrication Cost and Yield Challenges at Sub-20 nm Nodes

Emerging non-volatile memory stacks incorporate specialized mask layers and atomic-layer deposition steps, which increase wafer cost by 20%–30% over baseline CMOS. Extreme-ultraviolet scanners, which exceed USD 150 million each, concentrate capacity at a handful of fabs, limiting supply elasticity. Early pilot runs report defect densities two to three times higher than mature NAND processes, postponing cost parity in consumer devices and tempering near-term unit growth.

Lack of Unified Standards for Controller Interfaces and Software Stacks

JEDEC standards, such as NVDIMM-P, address persistent DRAM but omit byte-addressable non-volatile memory, forcing original equipment manufacturers to support proprietary drivers.[3]JEDEC, “JESD245 NVDIMM-P Specification,” jedec.org Fragmentation inflates qualification timelines in safety-critical sectors and hinders multi-sourcing, while only partial progress has been made toward NVMe extensions for persistent memory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Technology: MRAM Holds the Lead, ReRAM Gains Traction

Magnetoresistive RAM accounted for 36.74% of 2025 revenue, supported by qualification in automotive microcontrollers and industrial controllers that demand instant-on capability. Resistive RAM is forecast to grow at a 20.12% annual rate to 2031, as its two-terminal cell structure leverages existing high-k gate tooling. ReRAM’s cost trajectory appeals to fabless designers seeking drop-in flash replacements without the need for magnetic-deposition equipment. Phase-change memory remains a niche option in automotive black boxes and aerospace recorders, which value deterministic writes and radiation tolerance. Ferroelectric RAM retains a role in ultra-low-power microcontrollers and RFID tags, where unlimited endurance offsets density limitations. Cross-point architectures such as 3D XPoint are being repositioned for edge-AI accelerators that must preserve model weights across reboots. Samsung’s 1-gigabit prototype verifies that spin-transfer designs are narrowing the latency gap with spin-orbit-torque variants, reinforcing MRAM’s dominance.

ReRAM’s flexibility in switching materials, such as tantalum oxide, hafnium oxide, and titanium oxide, allows foundries to adapt to node-specific requirements. Weebit Nano’s 2024 partnership with SkyWater to qualify 130-nm ReRAM for radiation-hardened space applications shows suitability for specialty nodes. Ferroelectric RAM’s endurance, exceeding 10^14 cycles, keeps it relevant in smart-meter deployments, where it logs sensor data every few seconds over multi-decade lifetimes. Hybrid designs such as Samsung’s Z-NAND combine MRAM buffers with high-density NAND to extend endurance in write-intensive workloads.

By Type: Embedded Variants Accelerate as SoC Integration Deepens

Stand-alone modules contributed 63.12% of 2025 shipments, serving enterprise storage arrays and industrial controllers that value field-replaceable packages. Embedded non-volatile memory is projected to grow at a 18.67% annual rate through 2031, driven by system-on-chip designers eliminating external serial flash to reduce latency and lower power budgets. TSMC’s 22-nm eMRAM and GlobalFoundries’ 12-nm eMRAM platforms allow firmware, calibration data, and neural-network weights to reside on-die. The emerging non-volatile memory market size for embedded applications is projected to expand rapidly as consumer electronics adopt always-on sensing.

Stand-alone modules remain the preferred choice where capacity and serviceability are crucial, such as in storage-area networks and industrial PLCs. Everspin’s 256-megabit MRAM module targets cache tiers where power-fail protection and unlimited endurance outweigh cost premiums. Qualification cycles for embedded variants are longer because foundries must validate thermal stability across the entire process window; however, the savings in board area and assembly cost reinforce the migration trajectory.

By End-User Industry: Automotive Surpasses Consumer on ADAS Pull

Consumer electronics captured 38.25% of 2025 revenue, but automotive and transportation are on track for a 21.05% CAGR through 2031 as centralized domain controllers consolidate dozens of control units. The emerging non-volatile memory market supports instant-on, high-temperature retention, and fail-operational requirements inherent in Level 3 autonomy. Enterprise data-center demand, although smaller in revenue, is critical for storage-class memory tiers that bridge DRAM and NAND. Industrial segments favor FRAM and ReRAM for their unlimited endurance in harsh environments, while healthcare applications adopt non-volatile memory for implantable sensors that require data retention across battery changes. Aerospace and defense segments specify radiation-hardened variants, benefiting from ReRAM’s tolerance to single-event upsets.

Automotive demand is exemplified by Infineon’s integration of 256-megabit MRAM into AURIX microcontrollers, meeting instant boot and fail-operational redundancy mandates. Consumer electronics growth slows as smartphone penetration plateaus, but wearables sustain momentum by embedding always-on sensors and voice assistants that need a persistent state without flash latency.

By Application: Mobile and Wearables Register the Fastest Growth

Cache memory and enterprise storage represented 43.20% of 2025 revenue, leveraging MRAM and phase-change buffers that shield NAND from write-intensive workloads. Mobile phones and wearables are forecast to grow at a 21.10% annual rate due to the proliferation of always-on health monitoring and on-device AI inference.

The emerging non-volatile memory market size for mobile and wearables is expected to double as embedded FRAM replaces flash in ultra-low-power microcontrollers. Industrial control and automotive control applications rely on MRAM and FRAM for instant-on states over −40 to 125 °C ranges, while hybrid mass-storage architectures combine NAND with thin MRAM buffers to extend endurance. Secure microcontroller and smart-card deployments utilize ReRAM’s one-time programmable feature as a hardware root of trust.

Geography Analysis

The Asia Pacific region held 40.35% of 2025 revenue and is projected to grow at an annual rate of 19.82% through 2031. The region benefits from Samsung and SK Hynix pilot lines in South Korea, TSMC’s 22-nm eMRAM in Taiwan, and state-backed Chinese programs to localize resistive RAM production. Dense consumer-electronics and automotive supply chains reinforce a virtuous cycle of prototype and volume ramp. The emerging non-volatile memory market is further bolstered by the Asia-Pacific's growing adoption of battery-electric vehicles, which require high-temperature, high-endurance storage.

North America pursues radiation-hardened memory for aerospace and defense, with GlobalFoundries’ 12-nm eMRAM serving automotive and industrial microcontrollers. The U.S. CHIPS and Science Act allocates funds to domestic fabs, thereby enhancing supply security for defense contractors. Europe leverages the EUR 43 billion Chips Act to expand semiconductor capacity; Infineon and STMicroelectronics are piloting embedded MRAM for automotive electrification. The emerging non-volatile memory market share in Europe rises due to stringent functional-safety standards that favor MRAM.

South America, the Middle East, and Africa remain at early adoption stages, focusing on smart grid metering, oil and gas telemetry, and mobile payments. Saudi Arabia’s NEOM project is piloting MRAM-based data loggers for energy management, while African deployments focus on off-grid solar controllers that require low-power, high-endurance memory.

Competitive Landscape

Competition is moderate. Samsung, SK Hynix, Micron, and Kioxia collectively command a share of over 55% of the revenue, leveraging their scale and customer relationships. Pure-play startups such as Everspin, Weebit Nano, Avalanche Technology, and Crossbar license intellectual property and partner with foundries to sidestep fab investments. Technology differentiation drives competition as suppliers race to deliver lower write latency, higher endurance, and wider temperature ranges. Samsung’s 1-gigabit STT-MRAM prototype positions the firm to displace DRAM in persistent cache tiers. Everspin focuses on stand-alone modules for enterprise storage where unlimited endurance justifies price premiums. Foundry partnerships are critical; TSMC’s 22-nm eMRAM and GlobalFoundries’ 12-nm eMRAM provide fabless designers with reliable supply paths.

Standards-body participation also shapes the field as companies influence JEDEC interfaces that could lock in architectural advantages. Vertical integration is emerging: Infineon and Renesas embed MRAM into microcontrollers to secure differentiated automotive portfolios. Patent filings focus on tunnel-junction engineering and selector devices for cross-point arrays, with Samsung, Intel, and TSMC collectively holding more than 40% of the granted MRAM patents as of 2024. The emerging non-volatile memory industry thus balances incumbent scale with startup agility.

Emerging Non-Volatile Memory Industry Leaders

Samsung Electronics Co. Ltd.

SK Hynix Inc.

Micron Technology Inc.

Intel Corporation

Western Digital Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: SK Hynix earmarked USD 3.87 billion to expand its South Korean memory fabs, dedicating a portion of the outlay to spin-transfer-torque MRAM pilot lines that will serve automotive and enterprise storage customers.

- October 2025: TSMC reported that monthly production on its 22 nm embedded MRAM platform has surpassed 10,000 wafer starts, confirming strong demand from fabless automotive-MCU designers and edge-AI accelerator vendors.

- September 2025: Samsung Electronics and GlobalFoundries have entered a joint-development pact to co-optimise embedded MRAM process modules for automotive-grade microcontrollers on GlobalFoundries’ 12 nm FinFET node, targeting Level 3– 4 autonomous-driving workloads across a -40 °C to 150 °C temperature range.

- August 2025: Micron announced a USD 200 million phase-change memory R&D center in Boise, Idaho, focusing on radiation-hardened variants for satellites and avionics in partnership with the U.S. Department of Defense.

- July 2025: Infineon Technologies and STMicroelectronics formed a strategic alliance to co-develop embedded ferroelectric RAM for ultra-low-power automotive and industrial MCUs, aligning the product roadmap with ISO 26262 functional-safety needs.

- June 2025: Weebit Nano completed the qualification of its resistive RAM on SkyWater Technology’s 130 nm radiation-hardened platform and secured a USD 15 million, three-year production contract with an undisclosed aerospace prime for satellite memory systems.

Global Emerging Non-Volatile Memory Market Report Scope

Non-volatile memory is a computer memory that can retain information stored on it even when turned off. Emerging non-volatile memory technologies promise advanced and novel memories for storing more data at less cost than the expensive-to-build silicon chips utilized by renowned consumer gadgets such as cell phones, digital cameras, portable music players, and others. Among several alternatives, spin-transfer torque random access memory, phase change memory, and resistive random-access memory (RRAM) are key emerging technologies.

Emerging non-volatile memories are best suited for neuromorphic computing applications because they are small cell-sized and can store several synaptic weights. The end-user industries considered part of the study include consumer electronics, industrial, enterprise, and other sectors in various geographies. Further, the market is segmented by type, including stand-alone and embedded. Also, the study includes the impact of COVID-19 on the market.

| Magnetoresistive RAM (MRAM) |

| Resistive RAM (ReRAM) |

| Phase-Change Memory (PCM) |

| Ferroelectric RAM (FRAM) |

| 3D XPoint / Other Emerging |

| Stand-Alone |

| Embedded |

| Consumer Electronics |

| Industrial |

| Enterprise and Data Center |

| Automotive and Transportation |

| Healthcare and Medical Devices |

| Aerospace and Defense |

| Other End-user Industries |

| Cache Memory and Enterprise Storage |

| Mobile Phones and Wearables |

| Industrial and Automotive Control |

| Mass Storage |

| Embedded MCU and Smart Cards |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Memory Technology | Magnetoresistive RAM (MRAM) | ||

| Resistive RAM (ReRAM) | |||

| Phase-Change Memory (PCM) | |||

| Ferroelectric RAM (FRAM) | |||

| 3D XPoint / Other Emerging | |||

| By Type | Stand-Alone | ||

| Embedded | |||

| By End-user Industry | Consumer Electronics | ||

| Industrial | |||

| Enterprise and Data Center | |||

| Automotive and Transportation | |||

| Healthcare and Medical Devices | |||

| Aerospace and Defense | |||

| Other End-user Industries | |||

| By Application | Cache Memory and Enterprise Storage | ||

| Mobile Phones and Wearables | |||

| Industrial and Automotive Control | |||

| Mass Storage | |||

| Embedded MCU and Smart Cards | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the emerging non-volatile memory market?

The market stands at USD 8.31 billion in 2026 and is projected to reach USD 18.8 billion by 2031.

Which memory technology leads in revenue share?

Magnetoresistive RAM held 36.74% of 2025 revenue due to early automotive and industrial adoption.

Why is automotive demand rising so sharply?

Centralized domain controllers for Advanced Driver Assistance Systems require instant-on, high-temperature, high-endurance storage, driving a 21.05% CAGR from 2026 to 2031.

Which region generates the largest revenue?

Asia Pacific accounted for 40.35% of 2025 revenue, supported by Samsung, SK Hynix, and TSMC pilot lines.

What is the biggest technical hurdle to wider adoption?

High fabrication cost and yield challenges at sub-20 nm nodes raise wafer prices and slow the path to cost parity with flash.

How concentrated is supplier power?

The four largest vendors control about 55% of revenue, indicating moderate concentration rather than monopoly control.

Page last updated on: