Direct Methanol Fuel Cell Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

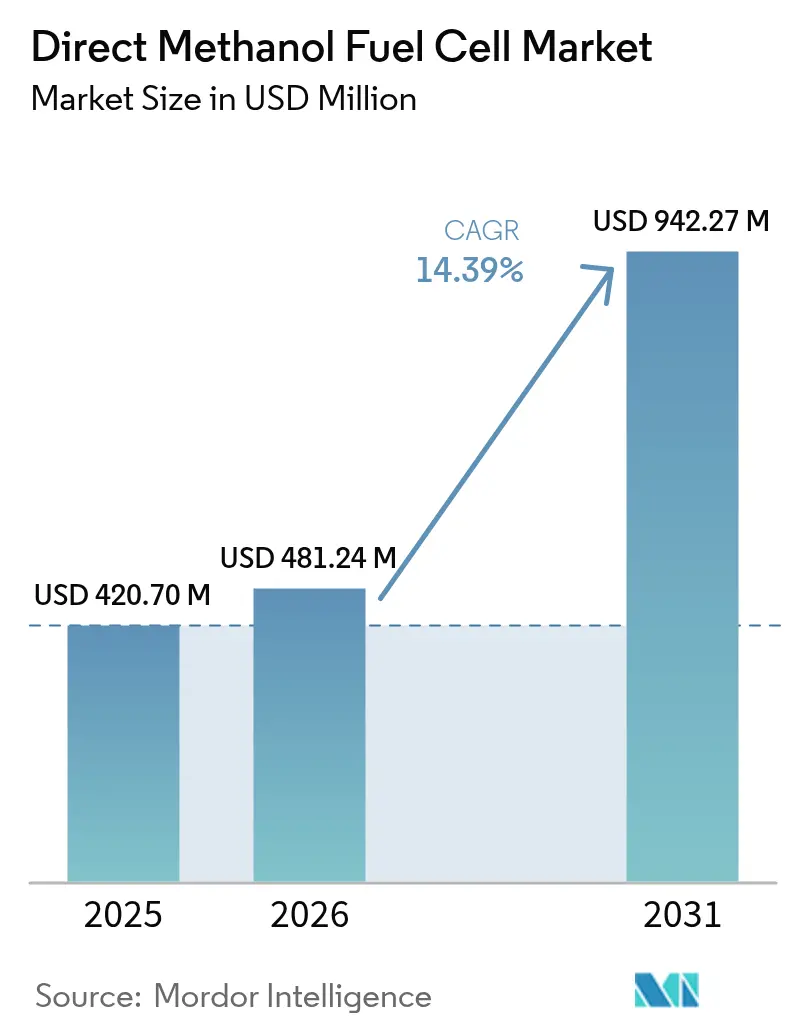

| Market Size (2026) | USD 481.24 Million |

| Market Size (2031) | USD 942.27 Million |

| Growth Rate (2026 - 2031) | 14.39% CAGR |

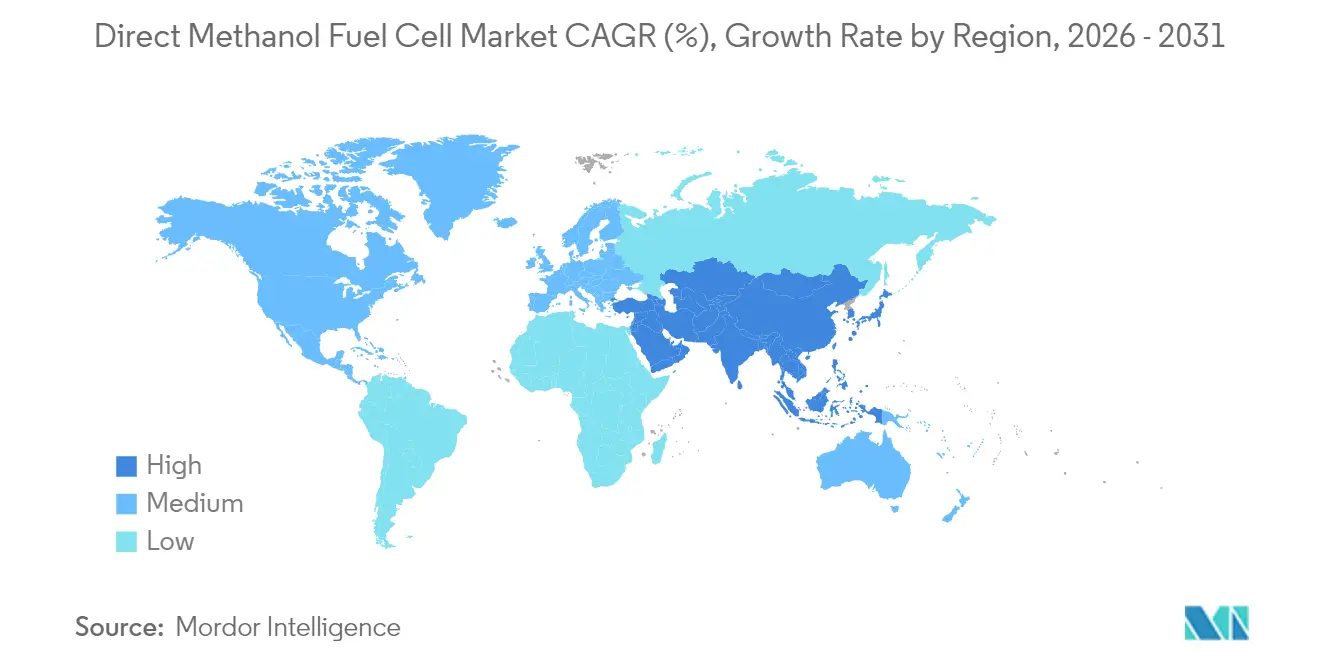

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Direct Methanol Fuel Cell Market Analysis by Mordor Intelligence

Direct Methanol Fuel Cell market size in 2026 is estimated at USD 481.24 million, growing from 2025 value of USD 420.70 million with 2031 projections showing USD 942.27 million, growing at 14.39% CAGR over 2026-2031.

Growing demand for silent portable power in military operations, expanding telecom infrastructure in remote regions, and methanol’s favorable storage attributes over compressed hydrogen underpin this expansion. Military programs in NATO member states are fielding methanol‐powered auxiliary units that eliminate acoustic and thermal signatures, while telecom operators turn to the technology for tower backup where grid reliability is low. Component innovation, especially within membrane electrode assemblies, has begun to cut catalyst loadings and improve methanol crossover resistance, opening cost-down pathways. Competitive dynamics favor firms that combine proprietary stack components with integrated fuel logistics, making technology differentiation more important than pricing. Regionally, Asia-Pacific has emerged as the pace-setter through government programs linking clean energy goals with industrial policy, creating volume opportunities for component suppliers and system integrators.

Key Report Takeaways

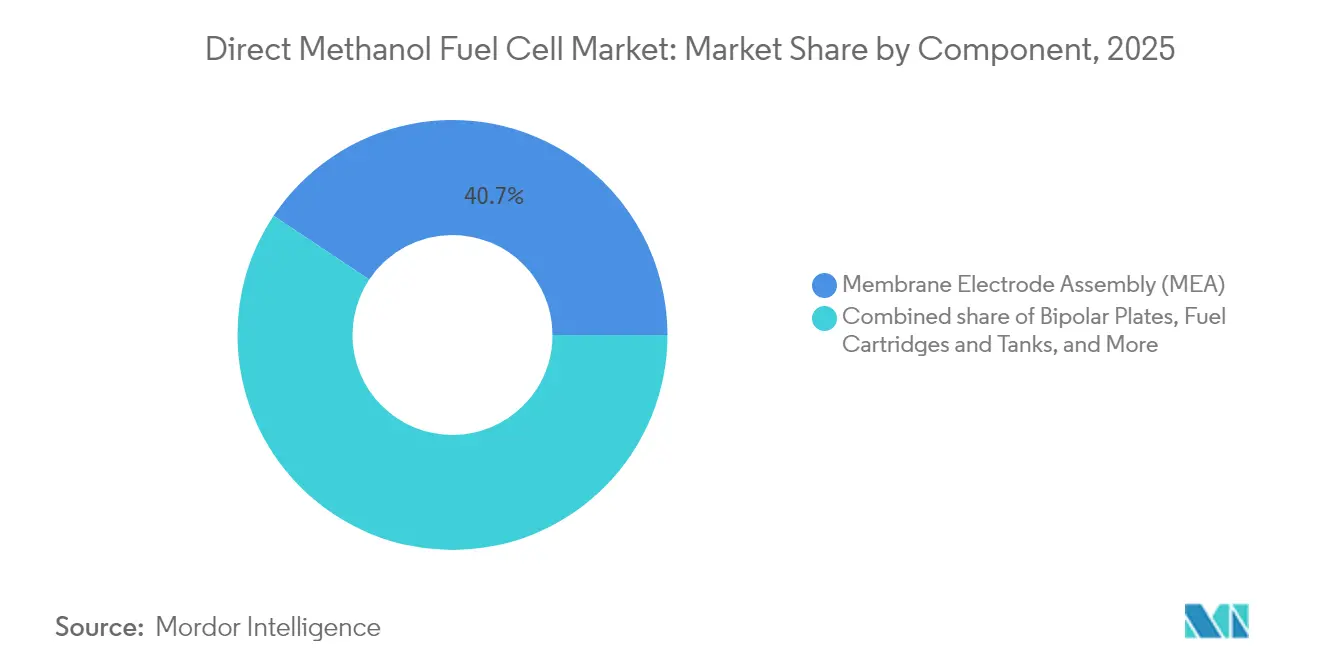

- By component, membrane electrode assemblies held 40.65% of the direct methanol fuel cells market share in 2025 and are advancing at a 15.08% CAGR to 2031.

- By power output, the 100 W–1,000 W category accounted for 55.40% of the direct methanol fuel cells market size in 2025 and is projected to grow at a 14.55% CAGR through 2031.

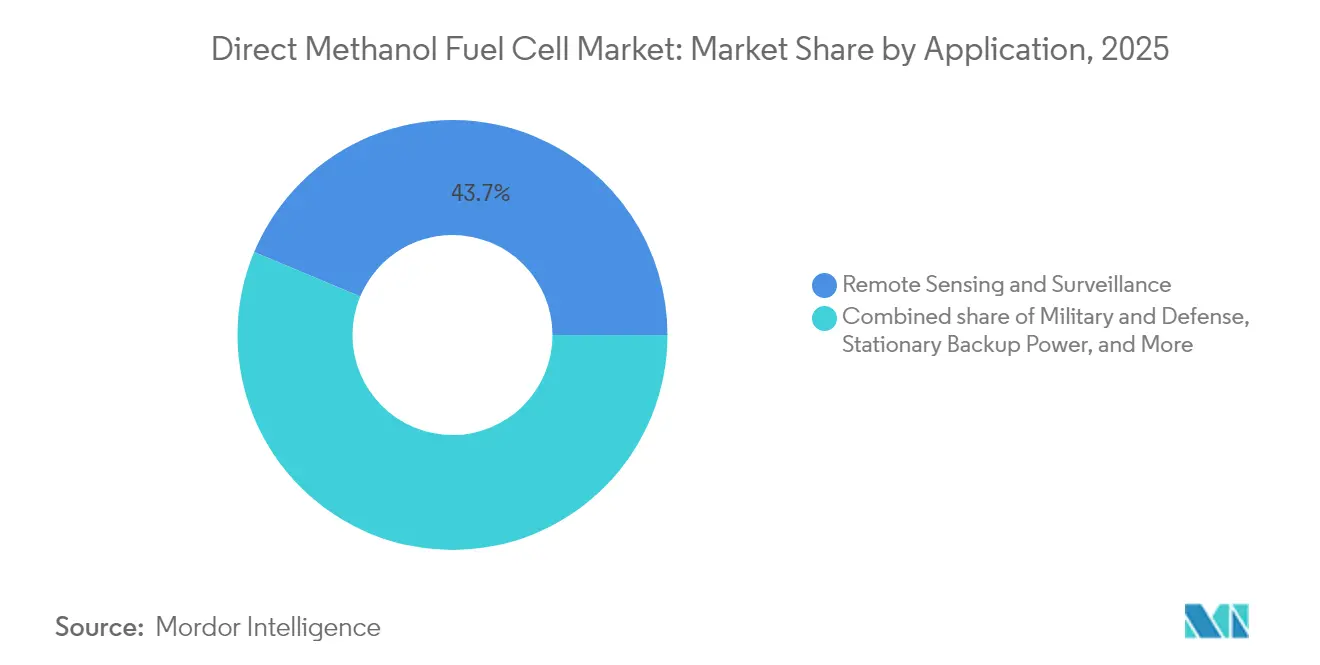

- By application, remote sensing and surveillance captured 43.70% of 2025 revenues; military applications are expected to post the fastest 16.12% CAGR to 2031.

- By end-user, telecom operators led with 36.60% revenue share in 2025; military and defense is forecast to expand at a 15.95% CAGR through 2031.

- By region, North America led with 37.50% revenue share in 2025, while Asia-Pacific is set to post the highest 18.20% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Direct Methanol Fuel Cell Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Military demand for silent portable power | +3.2% | Global, NATO focus | Medium term (2-4 years) |

| Rising telecom tower backup installations in remote areas | +2.8% | Asia–Pacific, MEA, Latin America | Short term (≤ 2 years) |

| Methanol price stability versus hydrogen | +2.1% | Global | Long term (≥ 4 years) |

| EU defense-focused carbon targets | +1.9% | Europe and allies | Medium term (2-4 years) |

| Mini-UAV endurance requirement above 8 h | +1.7% | North America, Europe, APAC | Medium term (2-4 years) |

| Maritime emissions rules for auxiliary power | +1.5% | Global, strongest in EU and California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Military demand for silent portable power

Stealth requirements in modern warfare prohibit internal combustion generators' acoustic and thermal signatures. Methanol fuel cells operate electrochemically, eliminating detectable vibrations and exhaust, which allows soldiers and autonomous platforms to remain concealed while powering electronics. The US Department of Defense funds a roadmap that spans soldier-worn chargers, ground vehicles, and submerged platforms.[1]US Department of Energy, “Fuel Cell Technologies Office 2025 Target Metrics,” energy.gov NATO demonstrations of the EMILY 3000 portable system validated five-day missions without refuel, prompting follow-up supply contracts from the Bundeswehr. Liquid methanol delivers three times the volumetric energy density of compressed hydrogen at 350 bar, easing battlefield logistics. R&D programs now integrate methanol reformers with PEM stacks so common logistic fuel grades can be used without high-pressure cylinders. As militaries broaden electrification strategies, procurement guidelines increasingly specify low acoustic profiles, accelerating the adoption of direct methanol units in radio relay, radar, and mobile command assets.

Rising telecom tower backup installations in remote areas

Mobile operators expanding 4G and 5G footprints into sparsely populated zones must guarantee uptime where the grid is weak. Deployments in Indonesia and northern Canada show methanol fuel cells can keep base transceiver stations online for 72 hours on a single 80 L cartridge, replacing diesel generators that require monthly refueling runs. Operators cite silent operation, negligible maintenance, and sub-5-minute refuel time as key purchase criteria. Methanol’s liquid state at ambient conditions avoids the bulky composite cylinders that hydrogen systems need, lowering site capex and permitting delivery by standard fuel trucks. Combined with solar panels and lithium-ion buffers, direct methanol fuel cells now meet new-build tower specifications that cap infrastructure weight and footprint. The value proposition is amplified by regulators in India and Nigeria who tighten emissions limits around diesel gensets, nudging operators toward cleaner power options.

Methanol price stability versus hydrogen

Global methanol is produced from natural gas, coal, and increasingly captured CO₂ using green hydrogen, creating a diversified supply base that tempers price swings. CME Group forecasts demand rising from 113 million t to more than 170 million t by 2040, providing scale economics that help offset feedstock volatility. Cost curves show green methanol reaching USD 315–350 t by 2050, whereas renewable hydrogen is expected to cost USD 2.7 kg, translating into higher delivered energy prices. Importantly, methanol can travel through conventional chemical tankers and intermediate bulk containers without the cryogenic or high-pressure conditioning that hydrogen requires, reducing delivered-cost uncertainty for end users such as defense logistics agencies and remote mining operators. Long-term offtake agreements are therefore easier to structure, which underpins capital investment decisions in direct methanol fuel cells projects across the stationary and maritime segments.

EU defence-focused carbon targets

The FuelEU Maritime regulation obliges vessels over 5,000 GT calling at EU ports to cut greenhouse-gas intensity 2% in 2025 and by 80% by 2050.[2]European Maritime Safety Agency, “FuelEU Maritime Regulation Overview,” emsa.europa.eu Naval auxiliaries and coast guard fleets examine methanol auxiliary power units that can operate on e-methanol synthesized from captured CO₂ and renewable hydrogen. Defense procurement agencies in Germany and the Netherlands have already introduced tender criteria that add scoring weight to life-cycle emissions. Methanol fuel cells provide an immediate compliance path because they avoid particulate filters and after-treatment equipment required by diesel gensets. Shore facilities also gain by lowering Scope 1 emissions and aligning with national net-zero targets. This regulatory certainty incentivizes European yards to design vessels with methanol-ready fuel-cell rooms, accelerating the learning curve and order pipeline for direct methanol fuel cells suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Platinum–ruthenium catalyst cost and supply risk | −2.4% | Global | Long term (≥ 4 years) |

| Low volumetric efficiency versus Li-ion above 1 kW | −1.8% | Global | Medium term (2-4 years) |

| Methanol transport restrictions on passenger aircraft | −1.2% | Global aviation routes, strongest impact in North America & EU | Medium term (2-4 years) |

| OEM hesitancy after early consumer-electronics failures | −0.9% | Global, concentrated in consumer electronics markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Platinum–ruthenium catalyst cost and supply risk

South Africa and Russia account for nearly 80% of primary platinum and ruthenium output, exposing the supply chain to geopolitical and labor disruptions. The World Platinum Investment Council projects that hydrogen and fuel cell applications will demand 875 koz platinum annually by 2030, tightening availability for other sectors. Catalyst layers in direct methanol fuel cells currently use up to 6 mg PGM cm² to combat CO poisoning, directly linking stack cost to metal spot prices. Research led by the US Department of Energy targets ≤3 mg PGM cm² loading and ≥300 mW cm² peak power density by 2030 ENERGY.GOV. Single-atom ruthenium anchored on graphene sheets has delivered encouraging oxygen-reduction kinetics, but durability under cycling remains under validation. Recycling initiatives can only supply 10-15% of projected demand this decade, so developers pursue non-PGM catalysts and high-entropy alloys, although these are unlikely to reach volume commercial readiness before 2030.

Low volumetric efficiency versus Li-ion above 1 kW

At outputs greater than 1 kW, system packaging becomes a challenge. State-of-the-art DMFC stacks yield around 181 mW cm² at 80 °C, translating into larger footprints than battery packs delivering over 700 W kg for the same volume. High-density applications like electric refrigerated trucks favor lithium-ion with auxiliary diesel heaters. Hybrid solutions that pair a 5 kW methanol stack for base load with a Li-ion pack for transients alleviate power density limitations but add weight and complexity. Progress in inkjet-printed catalyst layers trimmed dead volume by 15% and improved current distribution uniformity, yet large‐scale adoption is slowed by qualification cycles. Consequently, the direct methanol fuel cells market continues to be dominated by 100 W–1,000 W installations where volumetric constraints are less acute.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: MEA drives innovation leadership

Membrane electrode assemblies controlled the largest 40.65% revenue share in 2025, and the segment is expected to post the fastest 15.08% CAGR through 2031. High-performance polyvinyl-alcohol composite membranes now show methanol permeability below 1 × 10⁻⁶ cm² s and proton conductivity above 70 mS cm at 60 °C, metrics that approach Nafion while using non-fluorinated backbones. Cross-linked variants incorporating 5-sulfosalicylic acid further improve durability under thermal cycling. Within bipolar plates, niobium-titanium coatings have lifted electrical conductivity 42.6% and thermal conductivity 3.5%, exceeding US Department of Energy targets and narrowing the cost gap with stainless steel baseline. Additive manufacturing allows serpentine flow-field geometries that optimize reactant distribution and water management, lowering stack differential pressure losses by 18%. Fuel cartridges and balance-of-plant components grow parallel as portable and stationary integrators demand turnkey solutions. Emerging bio-based membranes sourced from bacterial cellulose register a conductivity of 62.2 mS cm and open circular-economy opportunities. Continuous advances ensure the direct methanol fuel cells market benefits from cost reductions alongside reliability gains.

By Power Output: Mid-range dominance reflects application sweet spot

The 100 W–1,000 W class captured 55.40% of the direct methanol fuel cells market size in 2025 and is forecast to retain leadership with a 14.55% CAGR to 2031. Units in this range offer the optimal compromise between refuel interval, footprint, and capital cost for telecom, surveillance, and auxiliary military uses. Sub-100 W devices serve niche consumer electronics and sensor nodes where maintenance callouts are expensive. Above 1 kW, hydrogen PEM and solid oxide systems provide higher power density, limiting DMFC’s share to marine auxiliary power and off-grid industrial sites. Recent demonstrations of a 200 kW maritime stack prove scalability yet remain pre-commercial. Overall, the mid-range segment will continue to command investment as integrators pursue modular architectures that can parallel multiple 500 W stacks for redundancy while staying within form-factor constraints.

By Application: Remote sensing leads current deployment

Remote sensing and surveillance accounted for 43.70% of 2025 revenue because unmanned platforms and environmental monitoring stations value silent, long-duration operation. AI-enabled stack controllers that adjust fuel feed and airflow in real time have improved fuel utilization by 6%, further extending autonomy. Military applications show the highest 16.12% CAGR to 2031, aided by funded programs in Europe and North America prioritizing energy resilience. Portable power for outdoor recreation, construction, and events maintains steady uptake, especially where regulations limit diesel gensets. Marine and leisure craft adoption accelerates under stricter harbor emissions limits. Stationary backup power grows more slowly yet remains a stable revenue stream for tower and data-center applications that need extended runtime without on-site staff.

By End-User Industry: Telecom operators drive current revenue

Telecom operators held 36.60% of total revenue in 2025 as network rollouts in Southeast Asia, Africa, and Latin America relied on methanol fuel cells to complement solar arrays for off-grid sites. The military is the fastest-growing customer category at a 15.95% CAGR, led by NATO modernization budgets emphasizing silent watch capabilities. Oil, gas, and mining companies deploy methanol units for well-head monitoring and safety systems, citing high sulfur tolerance relative to proton-exchange hydrogen stacks. Industrial and construction segments adopt portable DMFC generators to comply with urban noise ordinances. Consumer electronics brands have not re-entered the market at scale since early handset chargers faltered on cost, but improved cartridge logistics and stack miniaturization could revive interest after 2027.

Geography Analysis

North America generated 37.50% of global revenue in 2025, underpinned by defense allocations prioritizing quiet power sources and telecom hardening across remote territories. Federal R&D funding surpasses USD 7 billion for hydrogen and related technologies, giving regional suppliers an innovation edge. California’s Air Resources Board lists methanol as an exempt alternative marine fuel, adding maritime upside in Pacific ports. Despite leadership, the region faces rising cost competition from Asian manufacturers that benefit from scale efficiencies.

Asia–Pacific is projected to grow at an 18.20% CAGR through 2031, propelled by industrial policy coordination and widespread manufacturing capacity. Korea commands more than 1 GW of installed fuel-cell capacity across all chemistries, making it a component hub. China has overtaken Japan in fuel cell vehicle fleet size by focusing on buses and logistics trucks that share methanol fueling stops with stationary power units. Japan retains technical leadership and is expanding demonstrations in smart-city power grids. India and ASEAN nations deploy DMFC towers in universal service obligation projects, raising regional volumes over the outlook period.

Europe continues to influence technology direction via stringent emissions standards. The FuelEU Maritime rule began on 1 January 2025 and mandates 2% greenhouse-gas intensity reduction, triggering methanol retrofit inquiries for auxiliary generators. Germany’s Bundeswehr placed repeat orders for portable methanol units after field trials confirmed a five-day silent watch at Arctic temperatures. The Benelux region launched its first e-methanol plant using a 1.25 MW PEM electrolyzer to supply inland shipping, anchoring local demand growth. Southern and Eastern Europe report scattered pilot deployments aligned with EU recovery funds that earmark clean portable power for critical infrastructure.

Regulatory Landscape

Direct methanol fuel cell (DMFC) systems sit between fuel cell safety and performance standards and chemical handling rules for methanol, with compliance requirements differing by end-use (portable, stationary backup, maritime auxiliary, or mobility). International standardization is primarily anchored in the IEC 62282 series for fuel cell technologies, including updates for small stationary systems such as IEC 62282-3-201:2025 and IEC 62282-3-202:2025, which define test methods that manufacturers and integrators use to qualify products for deployments like telecom backup and remote infrastructure power.

Beyond IEC, national frameworks shape system and cartridge design, labeling, and safety certification. China’s dedicated DMFC system safety standard, GB/T 33983.1-2017, supports local conformity approaches for DMFC hardware. In Europe, environmental and product stewardship regimes such as REACH for chemicals affect methanol supply, transport documentation, and materials selection across the DMFC balance of plant. Maritime decarbonization policy, including FuelEU Maritime (effective 1 January 2025), also increases focus on verifiable lifecycle emissions and onboard safety validation for auxiliary power systems using methanol-derived fuels.

Competitive Landscape

The direct methanol fuel cells market is moderately fragmented, with fewer than ten vendors accounting for most global shipments, yet none exceeding a 20% share. SFC Energy leverages vertically integrated stacks and NATO certifications to secure premium defense contracts. Blue World Technologies introduced a high-temperature PEM design at 180 °C that achieves 55% electrical efficiency, offering a compelling life-cycle cost for marine customers. Johnson Matthey divested its Catalyst Technologies division to Honeywell for GBP 1.8 billion, allowing each firm to focus on core competencies while maintaining a technology licensing nexus for large e-methanol projects.

Strategic partnerships dominate growth strategies: SFC acquired Ballard Power Systems’ Scandinavian stationary-power assets to consolidate regional presence, while HIF Global selected Johnson Matthey eMERALD catalysts for a 700,000 t y e-methanol plant in Uruguay. R&D focuses on low-PGM catalysts, high-temperature membranes, and AI-assisted balance-of-plant controls. Nature Energy reports autonomous algorithms that raised fuel utilization 4 percentage points during a 1,000-hour durability run. Barriers to entry remain high due to certification costs and the need for global cartridge distribution, yet falling membrane costs and open-innovation programs can enable specialized entrants targeting unmanned aviation and field sensors over the next five years.

Direct Methanol Fuel Cell Industry Leaders

SFC Energy AG

Blue World Technologies ApS

Johnson Matthey Plc

Horizon Fuel Cell Technologies

Ballard Power Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Defense, public security, and critical infrastructure deployments are creating whitespace for DMFC systems that combine quiet operation and simplified liquid-fuel logistics with long-duration power in the 100 W to 1,000 W range, with scaling supported by hybrid architectures. The most visible demand signal appeared in May 2026, when SFC Energy announced an order of approximately EUR 42.7 million to supply fuel cell systems for operations in Ukraine under the German Federal Government Enablement Initiative, indicating procurement-backed pull for field-proven methanol fuel cell power.

Portfolio expansion toward reformer-based and hybrid configurations widens the gap between sub-1 kW portable DMFC and multi-kW stationary needs for off-grid and semi-permanent sites, including remote surveillance, telecom towers, and expeditionary power. In July 2026, SFC Energy signed an agreement to acquire key assets from Siqens GmbH, including patented methanol reformer fuel cell technology, reflecting continued consolidation around IP and system integration that can broaden product coverage from portable cartridges to higher-duty stationary packages. Separately, R&D targets aimed at lowering platinum-group metal loadings and improving power density continue to support cost-down pathways for membrane electrode assemblies, keeping qualification against IEC test methods and integrated fuel logistics as key enablers for suppliers.

Recent Industry Developments

- July 2026: SFC Energy secured a follow-up order of about CAD 3.1 million from a North American mobile surveillance solutions provider for EFOY Pro 2800 methanol fuel cells. The repeat business points to commercialization momentum for DMFC in remote video surveillance, where runtime and low-maintenance operation reduce service visits and support longer autonomous deployments.

- May 2026: SFC Energy announced an order worth approximately EUR 42.7 million to supply fuel cell systems to Ukraine under the German Federal Government Enablement Initiative. As the companys largest single order, it reinforces the defense and security use case for methanol-based, rapidly deployable power and supports scale benefits across stacks, balance-of-plant, and cartridge logistics.

- June 2024: Blue World Technologies completed testing of a 200 kW high-temperature PEM maritime fuel cell module designed to run on green methanol at its Aalborg, Denmark facilities. The milestone supports DMFC-adjacent methanol fuel cell adoption in marine auxiliary power, where emissions rules and port requirements are pushing shipowners toward alternative onboard generation solutions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from direct methanol fuel cell systems and related stack and balance-of-plant hardware that convert methanol to electricity for portable, stationary, and specialized mobility end uses across major regions.

Scope exclusions: Hydrogen PEM fuel cells, solid oxide fuel cells, and pure methanol fuel supply sales that are not bundled with DMFC hardware are excluded.

Segmentation Overview

- By Component

- Membrane Electrode Assembly (MEA)

- Bipolar Plates

- Fuel Cartridges and Tanks

- Balance-of-Plant (BoP) Hardware

- Others

- By Power Output

- Below 100 W

- 100 to 1,000 W

- Above 1,000 W

- By Application

- Portable Power

- Military and Defense

- Remote Sensing and Surveillance

- Marine and Leisure Craft

- Stationary Backup Power

- Other Niche Uses

- By End-User Industry

- Military Organisations

- Telecom Operators

- Oil and Gas and Mining

- Industrial and Construction

- Consumer Electronics OEMs

- Transportation and Logistics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting model structure and to set boundary conditions for adoption and supply availability. We referenced public sources such as the International Energy Agency, US Department of Energy fuel cell program material, US Energy Information Administration methanol and energy price series, and customs trade statistics for methanol related flows and fuel cell related HS codes where available.

On the industry side, we also reviewed company annual reports, investor presentations, press releases, and technical papers to understand typical power ranges, use case requirements, and how DMFC products are positioned versus batteries and other fuel cells. A paid subscription for company financials and news was used to check revenue disclosures and capacity announcements, and a patent database was used to track activity around membranes, catalysts, and stack designs. These desk sources are illustrative only, and we also used other public documents to collect data, cross-check assumptions, and fill in gaps.

Primary Interviews and Surveys

Primary work focused on validating how DMFC units are being purchased and deployed across portable power, backup power, and niche industrial and defense-style uses, and then translating that into pricing and volume assumptions. We spoke with manufacturers, component specialists, channel partners, and system integrators across APAC, EMEA, and the Americas to close gaps from desk research and stress-test model inputs before finalization.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 42% |

| Mid tier: 50% | Functional/Unit leaders: 36% | EMEA: 35% |

| Smaller Players: 22% | Managers: 49% | Americas: 23% |

Market-Sizing & Forecasting

The main sizing build used a top-down approach where the demand pool was reconstructed from addressable device and backup power deployments, then DMFC penetration rates by use case and region were applied, and value was derived using typical system pricing. We then corroborated the totals with selective bottom-up checks, including sampled vendor shipments, distributor channel checks, and ASP multiplied by estimated unit volumes, which helped adjust outliers.

Inputs that mattered most included average selling prices by watt class, the split of portable versus stationary deployments, replacement and service intervals for key stack parts, methanol price direction that can influence operating economics, and regional procurement patterns for remote power and defense-type applications. For forecasting, we ran scenario analysis and then narrowed the range using expert views on adoption timing, policy support for low-emission power, and the commercialization pace of improved membranes and catalysts. Where bottom-up signals were thin for smaller countries, we filled gaps using regional analogs and then checked those assumptions against interview feedback.

Data Validation & Update Cycle

Model outputs were compared against independent signals such as published fuel cell shipment commentary, announced production expansions, and observed pricing ranges, and then any variances were reviewed before sign-off. When an input caused an unusual step change for a region or application, the assumption was revisited and, where needed, respondents were re-contacted to confirm whether the shift was real or an artifact.

Reports are refreshed annually, with interim updates when material events occur, including major product launches, policy changes, or supply disruptions. Before delivery, an analyst completes a fresh pass across the key inputs and conversions so clients receive an updated view aligned with the latest available information.

Mordor Intelligence's Global Direct Methanol Fuel Cells Market Market Size Measured Against Other Published Estimates

Published market sizes for direct methanol fuel cells can differ by a wide margin because the counted products and the conversion from units to dollars are not handled the same way everywhere. Differences also show up when a source uses an earlier base year, assumes faster price erosion, or applies a broader definition that blends in adjacent fuel cell technologies.

Fuel cartridges and bulk methanol supply sit outside Mordor Intelligence's scope, which is why totals can look smaller than estimates that bundle recurring fuel spend with hardware revenue. Gaps also come from how portable power shipments are treated, whether military and remote sensing deployments are counted as a distinct demand pool, and if currency conversion uses an annual average versus a point in time.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.48 B (2026) | |

| Trade Journal A | USD 3.40 B (2024) | This estimate appears to use a broader value definition that can blend system hardware with component-level and application-wide spend, and it also starts from a different base year, which changes the implied adoption curve. |

| Global Consultancy B | USD 2.64 B (2023) | The figure is anchored to an earlier base year and may be aggregating DMFC with adjacent stack and system categories across applications, and the forecast window and price assumptions are not clearly tied to watt-class ASP behavior. |

The spread across sources mostly reflects scope and value accounting, rather than a disagreement that DMFC demand is growing. By keeping the model tied to identifiable DMFC hardware deployments and then validating pricing and volumes through interviews, we can offer a practical number that is easier to replicate and update as new signals emerge.

Key Questions Answered in the Report

What is the current value of the direct methanol fuel cells market?

The market is valued at USD 481.24 million in 2026 and is expected to reach USD 942.27 million by 2031, reflecting a 14.39% CAGR.

Which component segment grows the fastest?

Membrane electrode assemblies lead growth with a 15.08% CAGR through 2031, driven by advances in low-permeability composite membranes.

Why are telecom companies major adopters of DMFC systems?

Telecom operators use methanol fuel cells for tower backup in off-grid areas because the systems provide silent, long-duration power with minimal maintenance and simple liquid refueling.

How do upcoming maritime regulations affect DMFC demand?

The FuelEU Maritime rule requires ships visiting EU ports to cut greenhouse-gas intensity starting in 2025, prompting shipowners to consider methanol auxiliary power units that comply without after-treatment.

What limits DMFC penetration in high-power applications above 1 kW?

Current power density and packaging constraints make lithium-ion batteries or hydrogen PEM fuel cells more volumetrically efficient at outputs above 1 kW, although hybrid configurations offer a partial workaround.

What is the main supply-chain risk for DMFC production?

Dependence on platinum-group metals, particularly platinum and ruthenium sourced mainly from South Africa and Russia, poses cost and availability risks until non-PGM catalysts mature commercially.

Page last updated on: