Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 38.37 Billion |

| Market Size (2031) | USD 49.39 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

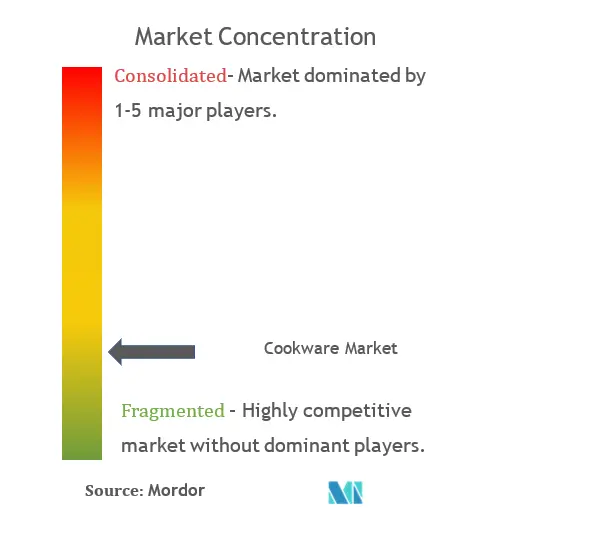

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cookware Market Analysis by Mordor Intelligence

The Cookware Market size is projected to expand from USD 36.48 billion in 2025 and USD 38.37 billion in 2026 to USD 49.39 billion by 2031, registering a CAGR of 5.18% between 2026 to 2031.

Heightened PFAS restrictions, rapid urbanization, and a visible consumer tilt toward premium, multipurpose products steer this momentum. Regulatory shifts in Minnesota, New York, and the European Union accelerate adoption of ceramic and cast-iron lines, while Asia-Pacific’s compact apartments fuel demand for space-saving, induction-compatible sets. North America has the largest regional position yet faces price volatility in steel and aluminum that squeezes margins. Digital channels gain ground as direct-to-consumer models furnish data-rich insights that brick-and-mortar stores cannot, prompting omnichannel overhauls across the cookware market.

Key Report Takeaways

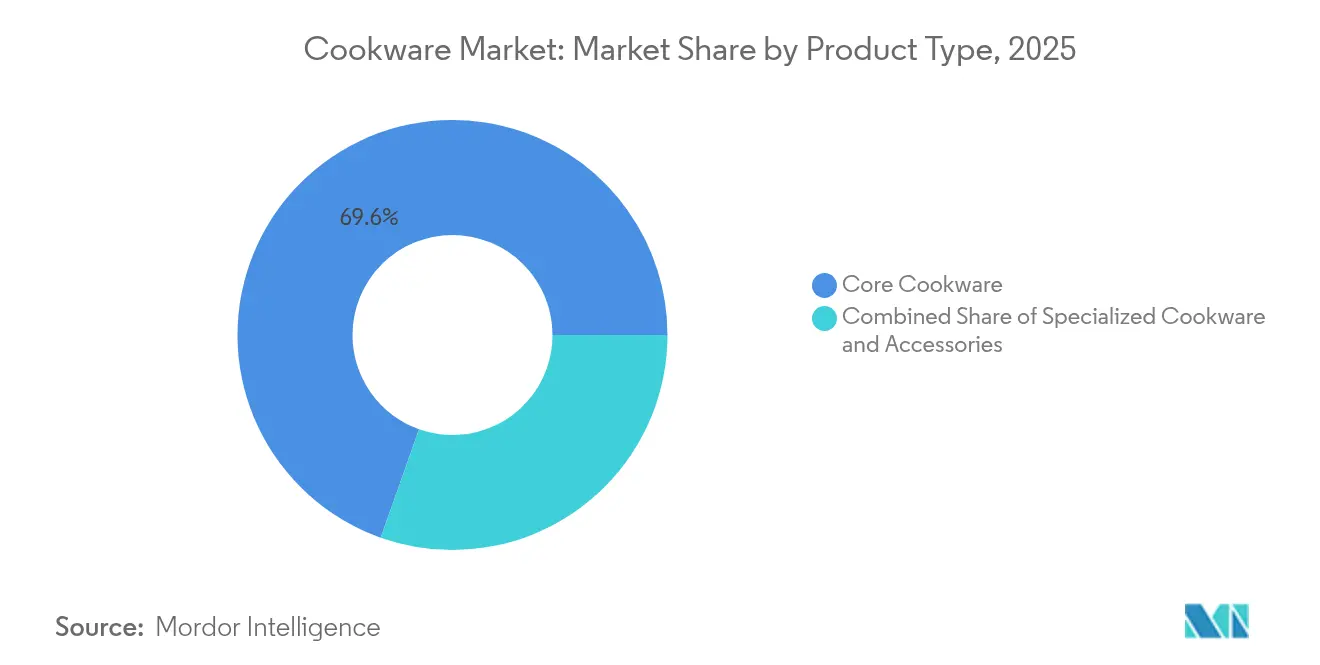

- By product type, core cookware led with 69.58% revenue share in 2025; specialized cookware is advancing at a 6.97% CAGR through 2031.

- By material, stainless steel held 34.12% of cookware market share in 2025, while cast iron is projected to grow at a 6.12% CAGR to 2031.

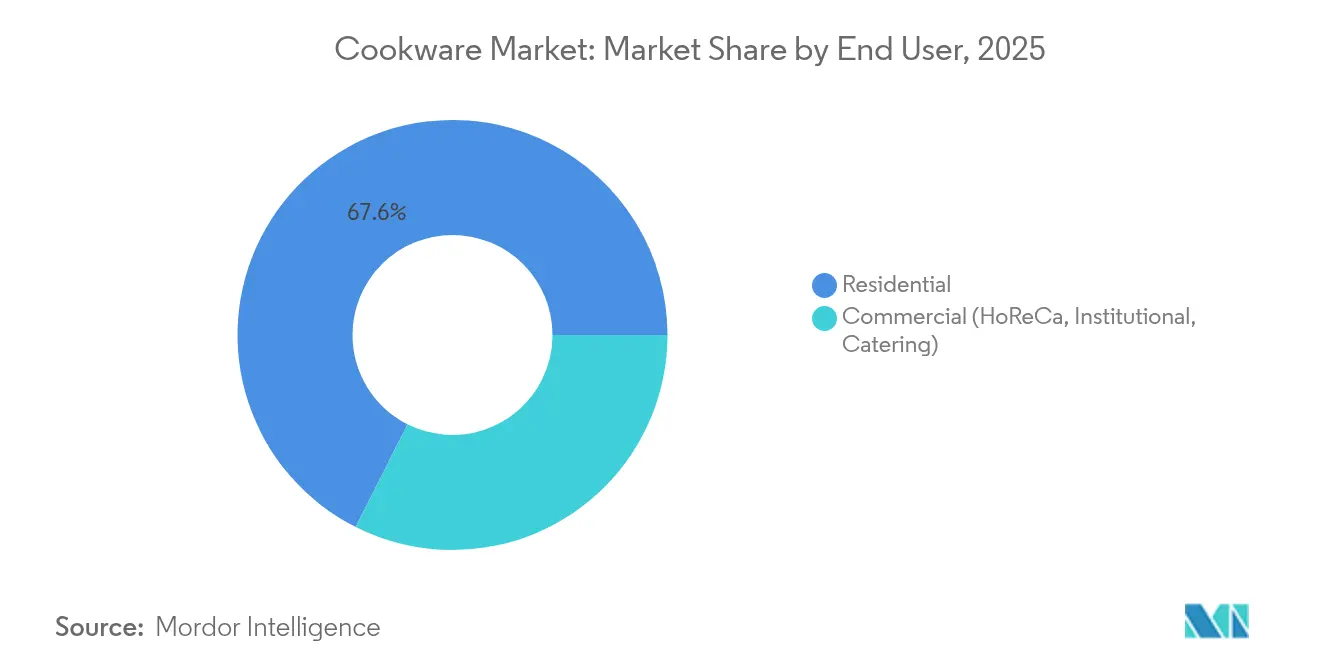

- By end user, residential applications accounted for 67.57% of the cookware market size in 2025 and commercial demand is rising at a 5.69% CAGR through 2031.

- By distribution channel, offline retail retained 64.48% share of the cookware market in 2025; online sales are set to expand at a 6.28% CAGR through 2031.

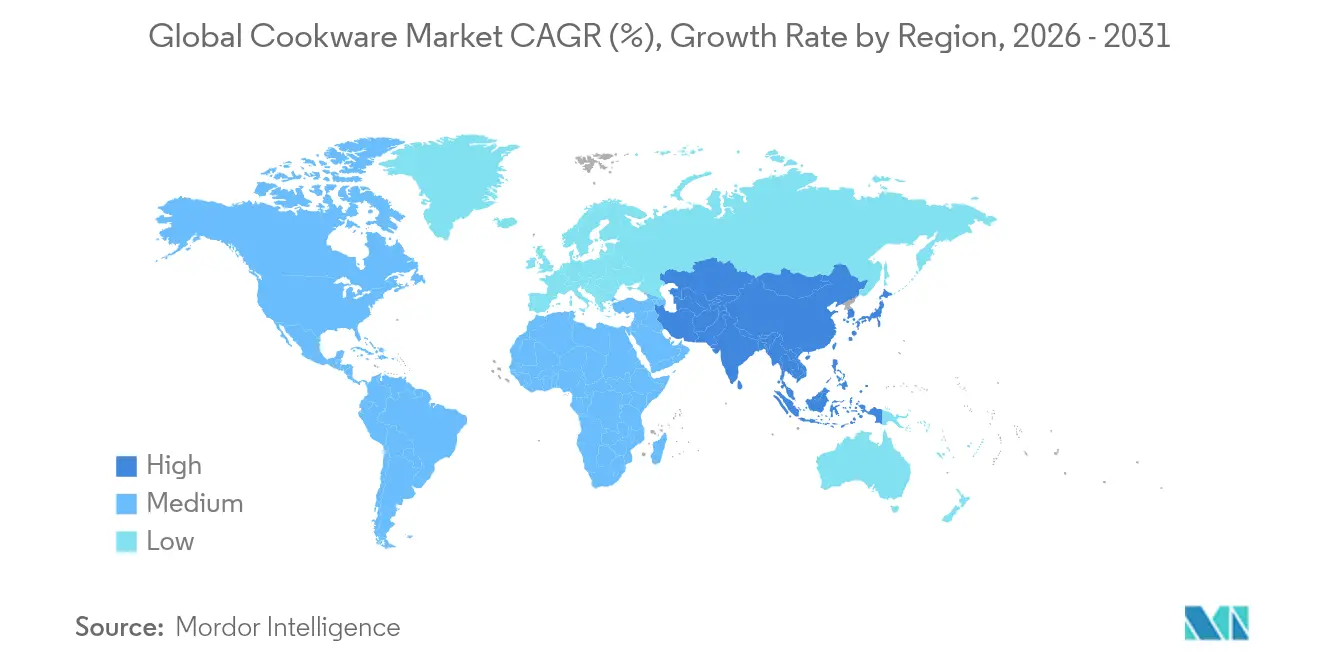

- By geography, North America occupied 35.80% share in 2025, while Asia-Pacific is slated to accelerate at a 7.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cookware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes & kitchen renovations | +1.2% | Global, strongest in Asia-Pacific emerging markets | Medium term (2-4 years) |

| Booming e-commerce kitchenware sales | +0.8% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Induction-compatible cookware demand surge | +0.6% | Europe & Asia-Pacific core markets | Medium term (2-4 years) |

| Urbanization & nuclear households in Asia-Pacific | +0.9% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| PFAS phase-out accelerating ceramic & cast-iron uptake | +0.7% | North America & EU regulatory zones | Short term (≤ 2 years) |

| Electrification policies favoring magnetic cookware | +0.5% | EU & select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes & Kitchen Renovations

Kitchen renovation waves tighten replacement cycles as consumers trade basic aluminum for stainless steel and cast iron. National Kitchen & Bath Association professionals observe 72% of homeowners requesting biophilic materials that align with natural cooking philosophies[1]Source: National Kitchen & Bath Association, “2025 Design Trends Report,” nkba.org. Induction cooktops increasingly feature in remodels, steering buyers toward magnetic-ready sets that command premium margins. Across emerging Asia-Pacific cities, rising middle-class purchasing power elevates demand for durable collections that double as lifestyle symbols. Premium upgrades generate profit cushions that help manufacturers offset volatile raw-material costs, sustaining steady expansions in the cookware market.

Booming E-commerce Kitchenware Sales

Photo-ready product pages, chef endorsements, and real-time consumer reviews spur online conversion. Web-focused challengers bypass retail mark-ups, making gourmet-grade pans accessible to first-time buyers. E-commerce ecosystems supply granular shopper data, allowing agile releases of limited-edition colors and influencer-curated bundles that resonant with a social-media audience. Strong logistics networks shorten delivery windows, eroding a key advantage of in-store shopping. As subscription-based replenishment models emerge, recurring revenue streams stabilize cash flow for fledgling cookware labels. Social media influence drives purchasing decisions, particularly for aesthetically appealing cookware brands that photograph well for food content creation.

Induction-Compatible Cookware Demand Surge

Government efficiency mandates and higher home-energy costs push households toward induction cooktops that boast 40-50% energy gains over gas[2]Source: MDPI, “Induction Cooking Technology Review,” mdpi.com. Manufacturers reply with tri-ply builds marrying an aluminum core to a magnetic stainless base, preserving fast heat while satisfying induction sensors. European appliance retailers spotlight induction kitchens at trade shows, drawing mainstream buyers beyond early adopters. Hybrid designs open price tiers for budget households, broadening the cookware market addressable pool. This technological shift forces traditional cookware manufacturers to redesign product lines, creating opportunities for specialized induction-focused brands to capture market share from established players.

Urbanization & Nuclear Households in Asia-Pacific

Smaller apartments reshape cooking habits from communal feasts to quick, single-pot meals. Stackable sets and fold-flat handles answer tight storage. China exported 4.48 billion household appliances in 2024, a 20.8% leap driven by compact designs suited to city micro-units[3] Source: General Administration of Customs PRC, “2024 Household Appliance Export Statistics,” customs.gov.cn. Manufacturers localize size ranges and surface coatings to regional cuisines, from stir-fry-oriented carbon steel to non-stick tawa plates for Indian flatbreads. These tailored offerings multiply SKUs yet deepen brand loyalty in diverse metropolitan pockets. Urban consumers prioritize convenience and efficiency, driving demand for non-stick surfaces and easy-cleaning materials that accommodate busy lifestyles and smaller kitchen spaces.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (steel, aluminum) | -0.9% | Global manufacturing hubs | Short term (≤ 2 years) |

| Mature markets’ long replacement cycles | -0.6% | North America & Western Europe | Long term (≥ 4 years) |

| ESG scrutiny on PTFE emissions | -0.4% | EU & North America regulatory zones | Medium term (2-4 years) |

| Slow adoption of smart/IoT cookware over privacy fears | -0.3% | Global, strongest in privacy-conscious markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Steel, Aluminum)

World Bank forecasts sustained high metal prices through 2025 as geopolitical tensions strain ore supplies[4] Source: World Bank, “Metals Price Forecast 2024-25,” worldbank.org. Tennessee-based Heritage Steel absorbed USD 75,000 in tariffs and anticipates USD 200,000 more, forcing a 15% list-price jump after 50% cost spikes. In Europe, nickel and chromium scarcities lift stainless premiums while Italian mills battle elevated energy bills, tightening margins. Larger manufacturers hedge with multiyear contracts and captive recycling loops, but smaller labels face profit erosion, stalling innovations and threatening exits from the cookware market. Price volatility creates competitive advantages for vertically integrated manufacturers with captive raw material sources over smaller brands dependent on spot market pricing.

Mature Markets’ Long Replacement Cycles

North American and Western European households often retain cookware for 7-10 years, suppressing unit turnover. Extended warranties and refurbishing services stretch product lifespans further, tempering fresh sales despite premiumization. Promotional events tied to holidays stimulate short-lived upticks yet seldom offset dormant periods. Brands counter with aesthetic refreshes, seasonal colorways and limited collaborations, that lure collectors but fail to expand total cookware market volume meaningfully. Consumer education remains insufficient to overcome skepticism about connected kitchen devices, limiting market penetration to early adopters and technology enthusiasts rather than mainstream cooking households.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialized Cookware Gains Momentum

Specialized vessels captured growing attention even as core lines retained 69.58% share of the cookware market in 2025. Dutch ovens and casserole pans ride a home-baking wave sparked during lockdowns and sustained by social-media recipe challenges. Ethnic tools such as idli steamers or tamagoyaki pans answer the craving for authentic regional flavors, helping the cookware market penetrate culinary niches once served mainly by specialty shops. Integrated accessory sales—replacement lids, silicone grips, and modular organizers—add high-margin baskets, supporting brand ecosystem strategies. Pressure cookers and steamers maintain steady demand in Asian markets where traditional cooking methods emphasize efficiency and nutrient retention, while Western markets rediscover these tools through health-conscious cooking movements and time-pressed lifestyles seeking convenient meal preparation solutions.

Specialized cookware emerges as the fastest-growing segment at 6.97% CAGR through 2026-2031, reflecting consumers' expanding culinary interests and social media influence promoting authentic ethnic cooking techniques. Consumers treat cookware as experiential gear supporting hobbies akin to photography or cycling. Video tutorials propel adoption of task-specific items, while gift shoppers view enamel-coated cast-iron ovens as lifetime presents. IKEA’s sol-gel series provides mass-market access to PFAS-free non-stick benefits, democratizing premium technologies previously restricted to boutique labels. Overall, the specialized lane strengthens loyalty and spurs cross-selling, cushioning revenue against commoditization of standard skillets in the cookware market.

By Material: Cast Iron Renaissance Drives Growth

Stainless steel anchored 34.12 % of the cookware market share in 2025, favored for resilience and professional aesthetics, yet cast-iron skillets are set to outpace at 6.12% CAGR to 2031. Heritage branding by Lodge and Le Creuset resonates with Gen Z consumers pursuing sustainability through long-lasting goods. Seasoned cast iron, naturally non-stick when properly maintained, alleviates PFAS concerns and earns viral traction in cooking forums. Ceramic and glass build presence as regulators turn the screws on PTFE, though thermal-shock resistance and price hurdles cap their march. Carbon steel emerges as a midpoint, combining heat retention with lighter weight, attracting restaurant stylings into home kitchens and diversifying the cookware market.

Enameled cast-iron upgrades mitigate rust worries and enable vibrant color palettes that double as tableware. Meanwhile, aluminum retains stronghold in entry-level kits and commercial frying operations thanks to conductivity and cost parity. Fraunhofer’s Plaslon® promises new PFAS-free coating longevity, opening upgrade paths without sacrificing release performance. This additives race underscores R&D’s role in safeguarding differentiation and margin within an otherwise price-sensitive cookware market.

By End User: Commercial Segment Accelerates

Residential cooks remain the backbone, representing 67.57% of the cookware market size in 2025, yet cafeterias, canteens, and hospitality kitchens propel faster 5.69% CAGR through 2031. U.S. foodservice equipment tallied USD 35.97 billion in 2023, advancing 7.1% annually on kitchen modernization mandates. India’s hotels, restaurants, and institutions expect 8% yearly revenue gains to 2028, signaling robust bulk-order pipelines. Operators favor stainless cladding for durability across high-BTU burners and commercial dishwashers, boosting average order value.

Institutional clients increasingly weigh total cost of ownership, rewarding suppliers whose pans last through thousands of cycles with minimal re-seasoning or warping. Training packages and on-site maintenance contracts anchor long-term relationships, lowering churn. Brands historically consumer-centric develop pro-grade offshoots, mirroring athletic-wear crossovers that began on courts before migrating to streetwear. This two-way innovation flow enriches both household and commercial segments, widening margins across the cookware market. The commercial segment's growth creates opportunities for specialized manufacturers focusing on foodservice applications, while residential-focused brands explore commercial-grade product lines targeting serious home cooks seeking professional performance.

By Distribution Channel: Digital Transformation Accelerates

Brick-and-mortar still absorbed 64.48% of transactions in 2025, supported by tactile trials and gift-registry services. Yet online revenues are scaling at a 6.28% CAGR as sophisticated 3-D configurators let shoppers rotate pans, view stovetop fit, and compare diameter conversions. Direct-to-consumer storefronts harvest first-party data, enabling recipe-driven retargeting that lifts repeat purchases. Marketplaces extend geographic reach, letting micro-brands tap global demand without warehousing abroad.

Store chains pivot toward experiential retail, live demos, cooking classes, and chef residencies, to justify foot traffic. Hybrid fulfillment models such as “buy online, pick up in store” trim shipping costs and satisfy instant-gratification cravings. Commercial buyers stick to distributors for consolidated invoicing, but procurement portals inch into that space too. Winning suppliers orchestrate inventory across channels to avoid stock-outs that could send shoppers to rivals, reflecting a new rule: every touchpoint is a potential point of sale in the cookware market.

Geography Analysis

North America’s 35.80% hold in 2025 mirrors robust discretionary spending and a renovation culture that revitalizes cookware drawers. Minnesota’s PFAS prohibition, effective January 2025, and New York’s planned 2026 PTFE curbs compel rapid formula shifts. Domestic makers like Le Creuset invested USD 30 million in South Carolina logistics to quicken roll-outs of compliant lines. Canadian and Mexican middle-class expansion under USMCA terms adds peripheral lift, while tariffs on Chinese steel push some buyers toward locally sourced sets.

Asia-Pacific leads growth at a 7.06% CAGR, standing at the epicenter of urbanization and rising wages that expand the cookware market more than any other region. China’s 20.8% jump in 2024 appliance exports underscores manufacturing agility coupled with surging domestic appetite. In India, a swelling youth population embraces induction-ready cookware as household electrification widens; government schemes encouraging clean cooking stoke demand for PFAS-free alternatives. Japanese and Korean consumers, already accustomed to compact kitchens, gravitate to premium multi-layer pans that fit rice cookers and induction hobs alike, bolstering average selling prices.

Europe’s steady pace hides divergent undercurrents: Nordic nations pioneer sustainable design cues that ripple outward, while Germany’s subdued construction sector dampens stainlessteel s consumption. The European Chemicals Agency’s proposal to bar wide PFAS groups adds complexity for continental suppliers, but first movers gain export credibility as regulations spread to other jurisdictions. Italy’s escalating energy tariffs pressure local forges, leading some brands to relocate enameling processes to lower-cost neighbors. Eastern European consumers, meanwhile, trade up as incomes rise, cushioning Western softness and helping sustain overall regional contributions to the cookware market.

Competitive Landscape

The cookware market is witnessing a delicate dance between fragmentation and a slow march towards consolidation. While global giants like Groupe SEB, Meyer, and Newell leverage their scale in R&D and forge key channel partnerships, they find themselves challenged by agile digital newcomers, adept at captivating audiences with their drop-style product launches. These digital-first brands often rely on social media platforms to create buzz and drive direct-to-consumer sales, disrupting traditional retail channels. As compliance burdens mount from PFAS bans and ESG reporting, it's the larger players with deeper pockets that benefit, subtly pushing smaller entities either towards niche specialties or prompting them to consider acquisition exits. Additionally, the rising consumer demand for sustainable and ethically produced cookware is further pressuring smaller players to adapt or exit the market.

Strategic maneuvers are increasingly leaning towards vertical integration and localized production, serving as buffers against currency fluctuations and shipping uncertainties. Le Creuset's expansion in South Carolina is a calculated move, slashing transit times for U.S. consumers and reducing dependency on overseas manufacturing. Meanwhile, Tramontina is ramping up its Brazilian foundries, ensuring a tariff-free supply to its Mercosur neighbors and strengthening its regional presence. With raw material costs on the rise, companies are either locking in multi-year contracts for metals or pivoting towards a circular approach, investing in scrap materials that can be melted down in kilns. This shift not only mitigates cost volatility but also aligns with growing environmental regulations and consumer preferences for eco-friendly products.

Material science is at the forefront of innovation: trade shows buzz with discussions on plasma-sprayed ceramic layers, carbon-steel hybrids, and recycled-aluminum cores. These advancements aim to enhance durability, heat distribution, and overall performance, catering to both professional chefs and home cooks. Meanwhile, IoT-enabled pans are seeing a diminished presence on shelves, as consumers seem less swayed by connectivity features. This trend underscores a broader sentiment: when it comes to purchasing decisions, performance, safety, and aesthetics reign supreme. Reflecting this shift, marketing strategies are evolving, with budgets now favoring collaborations with creators and dynamic live-stream demonstrations. These approaches not only engage tech-savvy consumers but also provide an interactive platform to showcase product features, highlighting the industry's changing landscape and the importance of adapting to new discovery paths.

Cookware Industry Leaders

Meyer Corporation

Groupe SEB SA

Newell Brands

Tramontina SA

TTK Prestige Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Weber LLC and Blackstone Products merged to form Weber Blackstone, widening outdoor cooking coverage with grills and griddles

- February 2025: CFS Brands acquired Mercer Culinary, enhancing its commercial kitchen portfolio.

- November 2024: Le Creuset committed USD 30 million to a new South Carolina distribution facility slated for March 2026 operation.

- April 2024: IKEA introduced HEMKOMST, MIDDAGSMAT, and HUSKNUT sol-gel ceramic cookware as part of its PFAS phase-out pledge.

Global Cookware Market Report Scope

Cookware is one of the most widely demanded products as people adopt urbanization. A complete background analysis of the global cookware market includes an assessment of the economy, a market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles covered in the report.

The cookware market is segmented by product, material, application, and geography. By product, the market is sub-segmented into pots & pans, spoons, wok turners, whisks, and soup ladles. By material, the market is sub-segmented into stainless steel, aluminum, glass, and others. By application, the market is sub-segmented into residential and commercial. By geography, the market is sub-segmented into North America, Europe, Asia-Pacific, South America, and the Middle East.

The report offers market size and forecasts in value (USD) for the above segments.

By Product Type (Value)

| Core Cookware | Pans (Fry/Saute, Grill, Wok/Kadhai, Crepe) |

| Pots (Sauce, Stock, Dutch Oven) | |

| Pressure Cookers & Steamers | |

| Cookware Sets | |

| Specialized Cookware | Dutch Ovens & Casseroles |

| Specialty Cookware (Idli, Appam, BBQ Grill Pan, etc.) | |

| Bakeware (Ovenware, Muffin trays, Cake tins, etc.) | |

| Accessories (Lids, Handles) |

By Material (Value)

| Stainless Steel |

| Aluminium |

| Cast Iron |

| Carbon Steel |

| Copper |

| Ceramic/Glass |

| Silicone |

| Other Coated Substrates |

By End User (Value)

| Residential |

| Commercial (HoReCa, Institutional, Catering) |

By Distribution Channel (Value)

| Offline Retail | Super/Hypermarkets |

| Department Stores | |

| Specialty Stores | |

| Online | E-commerce Marketplaces |

| Brand Webshops | |

| B2B / Direct Sales |

By Geography (Value)

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type (Value) | Core Cookware | Pans (Fry/Saute, Grill, Wok/Kadhai, Crepe) |

| Pots (Sauce, Stock, Dutch Oven) | ||

| Pressure Cookers & Steamers | ||

| Cookware Sets | ||

| Specialized Cookware | Dutch Ovens & Casseroles | |

| Specialty Cookware (Idli, Appam, BBQ Grill Pan, etc.) | ||

| Bakeware (Ovenware, Muffin trays, Cake tins, etc.) | ||

| Accessories (Lids, Handles) | ||

| By Material (Value) | Stainless Steel | |

| Aluminium | ||

| Cast Iron | ||

| Carbon Steel | ||

| Copper | ||

| Ceramic/Glass | ||

| Silicone | ||

| Other Coated Substrates | ||

| By End User (Value) | Residential | |

| Commercial (HoReCa, Institutional, Catering) | ||

| By Distribution Channel (Value) | Offline Retail | Super/Hypermarkets |

| Department Stores | ||

| Specialty Stores | ||

| Online | E-commerce Marketplaces | |

| Brand Webshops | ||

| B2B / Direct Sales | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the cookware market in 2026?

The cookware market size stands at USD 38.37 billion in 2026 with a projected 5.18% CAGR to 2031.

Which material category is growing fastest?

Cast iron leads growth with a 6.12% CAGR through 2031 due to PFAS-free appeal and social-media influence.

Who are the key players in Global Cookware Market?

Werhahn Group, Groupe SEB, Meyer Corporation, Fissler and Target are the major companies operating in the Global Cookware Market.

Which region is expected to expand most quickly?

Asia-Pacific is poised for a 7.06% CAGR to 2031, fueled by urbanization and rising disposable incomes.

How are PFAS regulations affecting product development?

Bans in Minnesota, planned EU restrictions, and retailer policies accelerate shifts to ceramic and enameled cast-iron lines.

What role do online sales play in cookware distribution?

E-commerce is the fastest-growing channel at a 6.28% CAGR, leveraging direct-to-consumer data and influencer marketing.

Page last updated on: