Market Overview

| Study Period | 2020 - 2031 |

|---|---|

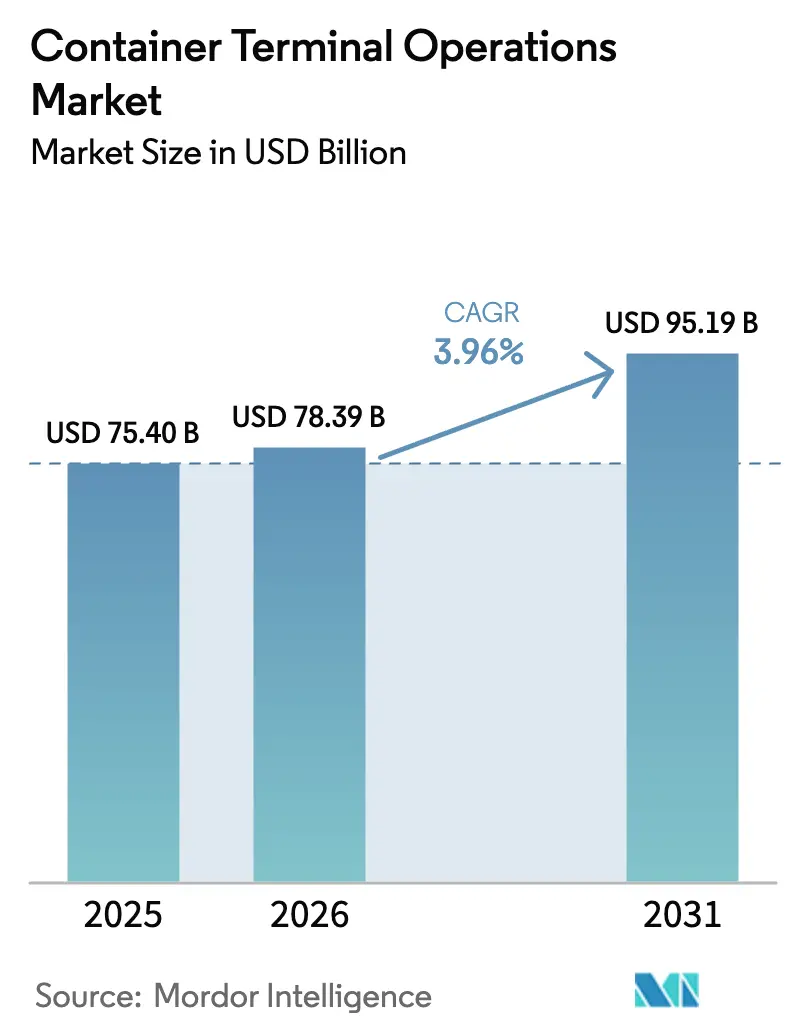

| Market Size (2026) | USD 78.39 Billion |

| Market Size (2031) | USD 95.19 Billion |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Container Terminal Operations Market Analysis by Mordor Intelligence

The Container Terminal Operations Market size was valued at USD 75.40 billion in 2025 and estimated to grow from USD 78.39 billion in 2026 to reach USD 95.19 billion by 2031, at a CAGR of 3.96% during the forecast period (2026-2031).

Robust demand for trade-facilitating infrastructure, the arrival of container vessels above 18,000 TEU, and steady investment in digital automation underpin this trajectory. Stevedoring revenues remain dominant, but rapid growth is shifting toward transportation and value-added logistics as operators extend inland. Asia-Pacific retains leadership with 41% 2024 share, supported by 52 fully automated Chinese ports and continuing public investment Business-Standard. Consolidation is gathering pace as operators chase scale advantages, while ESG-linked financing is lowering capital costs for greener equipment Maersk.

Key Report Takeaways

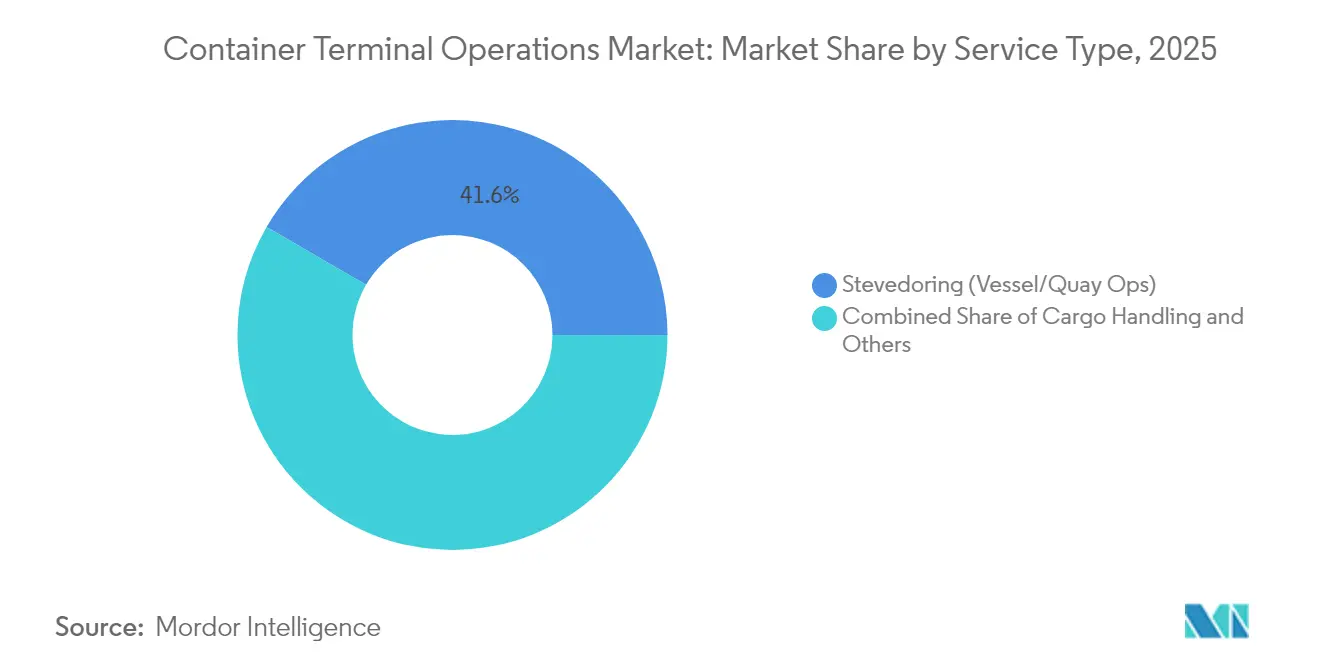

- By service, stevedoring led with 41.62% of container terminal operations market share in 2025; transportation services are projected to log the fastest 3.98% CAGR through 2031.

- By ownership model, state-owned facilities held 50.55% share in 2025, whereas public-private partnerships are advancing at a 4.62% CAGR.

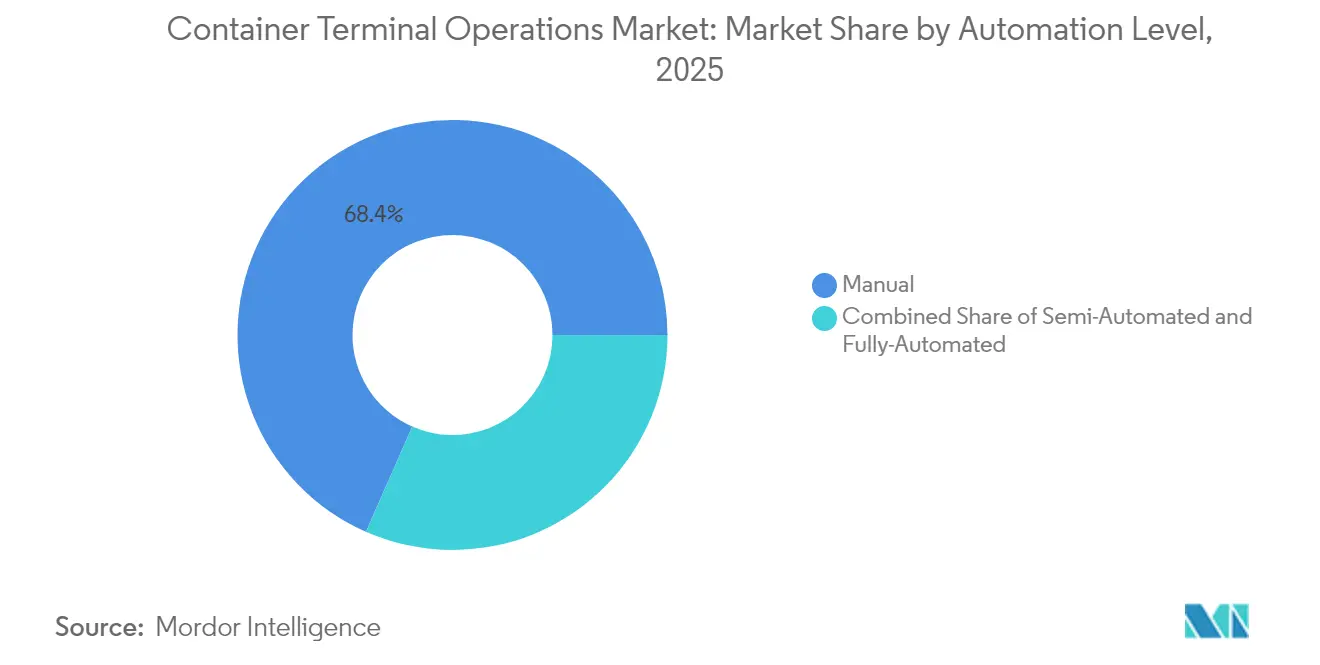

- By automation level, manual terminals still accounted for 68.41% share in 2025, yet fully automated sites are expanding at a 4.02% CAGR.

- By container type, general boxes commanded 60.44% share in 2025, while reefer throughput is forecast to accelerate at 4.29% CAGR.

- Geographically, Asia-Pacific captured 40.72% share in 2025 and is on track for the fastest 4.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Container Terminal Operations Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mega-vessel deployments (≥18k TEU) | +0.8% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Digitised supply-chain visibility demands from BCOs | +0.6% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Government-led port capacity expansions | +0.9% | Asia-Pacific core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Near-shoring fuelling intra-regional feeder volumes | +0.5% | North America, Europe, with emerging impact in Asia-Pacific | Medium term (2-4 years) |

| ESG-linked financing lowering cost of green terminal upgrades | +0.4% | Global, with early adoption in Europe and North America | Long term (≥ 4 years) |

| Emerging Arctic sea-route creating new hub requirements | +0.2% | Northern Europe, Russia, with connectivity to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Mega-Vessel Deployments Reshaping Terminal Infrastructure

Record-size ships intensify berth depth, crane outreach, and yard capacity demands. Qingdao’s automated dock moved 60.6 boxes per crane-hour in December 2024, more than double conventional productivity. Peaks created by fewer but larger calls are prompting mid-tier operators to justify automation even at modest volumes. PSA’s SGD 20 billion Tuas Port fully automated and slated for 65 million TEU embodies this mega-vessel-ready blueprint. Smaller Asian and European gateways are now vying for cascading 14,000 TEU ships, which strains conventional layouts and accelerates retrofit programs. As equipment makers bundle AI platforms with hardware, payback periods narrow, further embedding automation into the container terminal operations market[1]“Chinese Ports Get Smarter with Automation Push,” CGTN, cgtn.com.

Digitized Supply-Chain Visibility Demands Transform Operations

Shippers insist on real-time container milestones, pushing terminals to roll out IoT-enabled cranes, yard vehicles, and gate systems. APM Terminals fitted 2,500+ assets with sensors by 2024, delivering predictive maintenance and live status feeds. Standardized APIs now integrate terminal data directly into cargo-owners’ TMS platforms, shrinking dwell times and paperwork. Computer-vision inspections flag damaged containers automatically, while edge processing slashes latency during peak moves. Competitive edge increasingly stems from data granularity and interoperability rather than berth length alone, encouraging new pricing models based on visibility services in the container terminal operations market[2]“Port AGV Successfully Went to Sea,” TZBotAutomation,tzbotautomation.com.

Government-Led Port Capacity Expansions Drive Long-Term Growth

China’s 14th Five-Year Plan and India’s Sagarmala Program steer double-digit billion-dollar outlays toward deepwater berths, smart yard tech, and green equipment Business-Standard. Brazil will auction 42 concessions through 2026, mobilizing USD 2.37 billion to modernize legacy piers. Such state-backed projects attract ocean carriers seeking reliable hub nodes, which then magnify throughput, justifying the next financing tranche creating a virtuous cycle for the container terminal operations market[3]“APM Terminals Granted the Renewal of the Concession in the Port of New York–New Jersey,” inforMARE, informare.it.

Near-Shoring Fuels Intra-Regional Feeder Network Expansion

Factory relocation toward consumption markets lifts regional feedership volumes. AD Ports Group already fields 49 feeder vessels that touch 78 ports across 28 nations, booking record EBITDA in 2024. Mexican gateways captured double-digit import growth as North-American buyers rerouted away from trans-Pacific corridors. Smaller terminals capitalize on shorter haul cycles but must fine-tune berth productivity to sustain frequent calls. Digital slot-booking and dynamic stowage planning mitigate schedule risk, reinforcing regional supply-chain resilience within the container terminal operations market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Landside congestion & hinterland bottlenecks | -0.7% | Global, particularly acute in North America and Europe | Short term (≤ 2 years) |

| High CAPEX for full automation retrofits | -0.5% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Geopolitical chokepoint risks (e.g., Bab-el-Mandeb) | -0.4% | Global, with acute impact on Europe-Asia trade routes | Short term (≤ 2 years) |

| Tightening IMO emissions rules impacting diesel equipment ROI | -0.3% | Global, with earlier compliance pressure in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Landside Congestion Constrains Terminal Productivity Gains

Truck shortages, aging rail links, and chassis imbalances erode quay-side gains by throttling gate moves. U.S. Gulf and Atlantic ports extended gate hours in 2025, yet yard density still spiked beyond 90% during import peaks. Operators are funding near-dock rail hubs and inland depots—ventures that require cooperation with multiple agencies and add complexity to the container terminal operations market.

High CAPEX Requirements Limit Automation Adoption

A fully automated greenfield terminal can exceed USD 1 billion, with payback horizons over a decade. Low-volume facilities struggle to clear investment hurdles without throughput guarantees. Vendors have responded with scalable automation modules, but integration risks persist, deterring cash-constrained port authorities. Divergent global labor regulations also complicate cost-benefit appraisals for the container terminal operations market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service – Stevedoring Remains Core While Transportation Accelerates

Stevedoring held 41.62% of container terminal operations market share in 2025, reflecting its role as the revenue anchor of vessel-handling activities. Transportation accounted for just 27.45% yet is projected to deliver a 3.98% CAGR, powered by integrated rail and trucking corridors that pull gateways deeper into inland logistics. The container terminal operations market size for transportation services is forecast to reach USD 37.45 billion by 2031, widening margins through bundled door-to-door offerings. Terminals now monetize value-added cargo-care, customs brokerage, and digital scheduling, enhancing customer retention. Simultaneously, cargo-handling services yard moves, plugging reefers, and hazardous storage provide a resilient mid-tier revenue cushion.

The shift toward inland control reflects strategic bets on diversified income streams and tighter customer intimacy. Operators deploy TOS-linked truck appointment modules and RFID gate systems that cut motor-carrier waits by up to 40 minutes. Growing e-commerce import volumes further spur transload facilities adjacent to quays. As near-shoring gains steam, regional transportation networks become decisive competitive levers in the broader container terminal operations market.

By Ownership Model – PPP Momentum Challenges State Dominance

State entities controlled 50.55% of global throughput in 2025, but public-private partnerships are pacing at 4.62% CAGR, aligned with sovereign goals for efficiency and capital relief. The container terminal operations market size under PPP frameworks is projected to top USD 42.1 billion by 2031, reflecting multi-decade concession pipelines in Africa, Latin America, and South Asia. PPP deals often embed performance covenants that drive technology adoption faster than purely state-run siblings, reinforcing a virtuous circle of reinvestment.

Large operators leverage cross-portfolio synergies in procurement, training, and data analytics, raising entry barriers for smaller independents. Meanwhile, transparent tender rules and improved dispute-resolution mechanisms entice institutional investors seeking infrastructure-linked yields. This convergence of policy incentives and private capital accelerates transfer of modern practices across the container terminal operations industry.

By Automation Level – Manual Terminals Persist Yet Full Automation Gains Ground

Manual sites still represent 68.41% of active terminals, but fully automated facilities are expanding at 4.02% CAGR through 2031. The container terminal operations market size for automated systems is projected to exceed USD 23.1 billion by 2031 as operators chase labor savings and safer environments. China alone counted 52 robotic ports by late 2024, showcasing AI-guided quay cranes, autonomous container carriers, and 5G mesh networks.

Semi-automation remains an on-ramp for mid-volume berths, typically starting with auto-gates and remote-controlled RTGs, balancing productivity and cost. Equipment suppliers now bundle lifecycle software updates and cyber-security patches, lowering integration hurdles. The rise of ESG-linked loans at favorable rates is tilting project economics further toward full digitalization, reshaping competitive hierarchies within the container terminal operations market.

By Container Type – General Cargo Dominates, Reefer Segment Outpaces

General-purpose boxes generated 60.44% of 2025 moves, reflecting the ubiquity of dry consumer goods. Yet reefer lifts are forecast to compound at 4.29% CAGR, fueled by global vaccine flows, perishable food demand, and stricter cold-chain governance. Reefer-focused terminals command higher unit revenues thanks to electricity surcharges and monitoring fees. Some Asian hubs now allocate dedicated reefer berths with plug-in densities above 1,200 sockets, securing pharmaceutical traffic.

OOG/project cargo and IMO-classified dangerous goods remain niche slices yet command premium tariffs and deepen customer reliance. AI-enabled yard planning optimizes stowage for over-dimension boxes, reducing double-handling. Collectively, these specialized moves reinforce revenue diversity and resilience across the container terminal operations industry.

Geography Analysis

Asia-Pacific contributed 40.72% of 2025 throughput and is poised for a 4.52% CAGR through 2031, bolstered by Chinese mega-hub construction, India’s Sagarmala roll-out, and Southeast Asia’s green-field projects. The region’s container terminal operations market size for automated facilities is projected to double by 2030, anchored by Singapore’s multiphase Tuas investment and Malaysia’s Port Klang expansion. National governments subsidize electrified yard equipment and mandate carbon-neutral targets, reinforcing Asia-Pacific’s innovation edge.

North America and Europe present mature gateways where modernization, digital twins, and emissions compliance take precedence. APM Terminals’ USD 500 million Elizabeth project in New York-New Jersey introduces hybrid straddle carriers and solar canopies, reflecting tighter regional regulations. European terminals experienced Red Sea reroutings in 2024, highlighting the need for flexible berth scheduling and multi-directional rail corridors to mitigate supply-chain shocks.

Middle East & Africa and South America constitute emergent growth zones. AD Ports Group’s USD 251 million Luanda modernization and USD 250 million Pointe-Noire financing demonstrate rising foreign capital appetite. Brazil’s concession wave targets greener cranes and longer quay walls, aiming to lift regional competitiveness. These investments cultivate diversified trade routes, lowering dependency on traditional East-West corridors and supporting incremental gains for the container terminal operations market.

Competitive Landscape

Global operators such as PSA International, APM Terminals, and Hutchison Ports collectively control more than half of world throughput, yielding moderate concentration. Scale unlocks procurement leverage, integrated TOS platforms, and cross-regional customer packages, but rising PPP concessions invite region-specific challengers. CMA CGM’s purchase of Santos Brasil assets and AD Ports Group’s African portfolio show how acquisitions extend network reach and market power.

Automation acts as a strategic moat: early adopters report 25% lower per-move labor costs and 15% higher crane productivity. Vendors like ZPMC and Kalmar partner with software specialists to deliver “terminal-as-a-service” models that bundle hardware, analytics, and maintenance under multiyear contracts. ESG mandates further stratify players; those able to tap green finance at discount rates can front-load electrification, reinforcing customer appeal.

Regulatory harmonization is progressing, with ISO 14001 and ISPS certifications becoming table stakes for major carrier calls. The convergence of technology, finance, and regulation is sharpening competitive boundaries and establishing new benchmarks in the container terminal operations market.

Container Terminal Operations Industry Leaders

APM Terminals (A. P. Moller-Maersk)

PSA International

Hutchison Ports

DP World

COSCO Shipping Ports

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: APM Terminals Elizabeth secured a 33-year concession renewal at the Port of New York-New Jersey with planned investments exceeding USD 500 million for terminal modernization and zero-emission equipment procurement, strengthening Maersk's North American terminal network.

- March 2025: Congo Terminal raised USD 250 million to expand Pointe-Noire quay length to 2 km.

- March 2025: APM Terminals Elizabeth secured a 33-year extension with a USD 500 million upgrade plan.

- January 2025: CMA CGM completed its acquisition of Santos Brasil terminal operations, marking the largest South American terminal M&A transaction of 2024-2025 and expanding the French shipping giant's integrated logistics capabilities across Latin America's key container gateways.

Global Container Terminal Operations Market Report Scope

Container Terminal Operation and Cargo Handling Container terminals are designated for the handling, storage, and possibly loading or unloading of cargo into or out of containers, and where containers can be picked up, dropped off, maintained, stored, or loaded or unloaded from one mode of transport to another (that is, vessel, truck, barge, or rail). The main activity of a container terminal is the transfer of cargo units from one transport modality to another.

A complete background analysis of the Container Terminal Operation market, which includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles, are covered in the report. The impact of COVID-19 has also been incorporated and considered during the study.

The container terminal operations market is segmented by service (stevedoring, cargo handling and transportation, and other services), cargo type (dry cargo, crude oil, and other liquid cargo), and geography (North America, Europe, Asia-Pacific, and Latin America, and Middle-East and Africa). The report offers the market size in value terms in USD for all the above mentioned segments.

By Service

| Stevedoring (Vessel/Quay Ops) |

| Cargo Handling |

| Transportation |

| Other Services |

By Ownership Model

| State-Owned |

| Public-Private Partnership |

| Private / Independent |

By Automation Level

| Manual |

| Semi-Automated |

| Fully Automated |

By Container Type

| General |

| Reefer |

| OOG / Project |

| Dangerous Goods (DG) |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Service | Stevedoring (Vessel/Quay Ops) | |

| Cargo Handling | ||

| Transportation | ||

| Other Services | ||

| By Ownership Model | State-Owned | |

| Public-Private Partnership | ||

| Private / Independent | ||

| By Automation Level | Manual | |

| Semi-Automated | ||

| Fully Automated | ||

| By Container Type | General | |

| Reefer | ||

| OOG / Project | ||

| Dangerous Goods (DG) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the container terminal operations market?

The market stands at USD 78.39 billion in 2026, supported by mega-vessel calls and growing automation deployments.

How fast will global terminal revenues grow through 2031?

Revenues are projected to expand at a 3.96% CAGR, reaching USD 95.19 billion by 2031.

Which region leads current throughput?

Asia-Pacific accounts for 40.72% of 2025 volume, aided by extensive Chinese and Southeast Asian capacity expansions.

Which service segment is growing quickest?

Transportation services tied to inland logistics are forecast for a 3.98% CAGR, outpacing traditional stevedoring.

What share do automated terminals hold today?

Fully automated sites represent 31.59% of global facilities, but they are advancing at 4.02% CAGR as capital costs fall.

How are ESG mandates influencing investment?

Access to lower-cost, sustainability-linked loans is accelerating electrification and green equipment adoption across major hubs.

Page last updated on: