Dura Substitutes Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

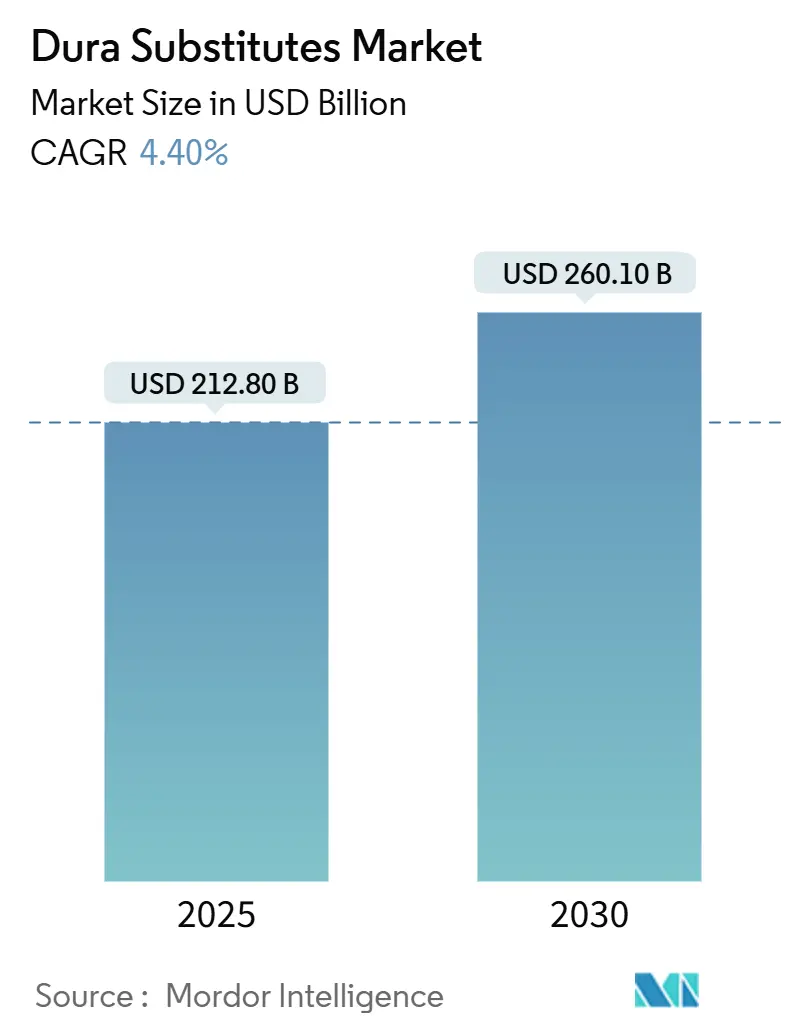

| Market Size (2025) | USD 212.80 Billion |

| Market Size (2030) | USD 260.10 Billion |

| Growth Rate (2025 - 2030) | 4.40% CAGR |

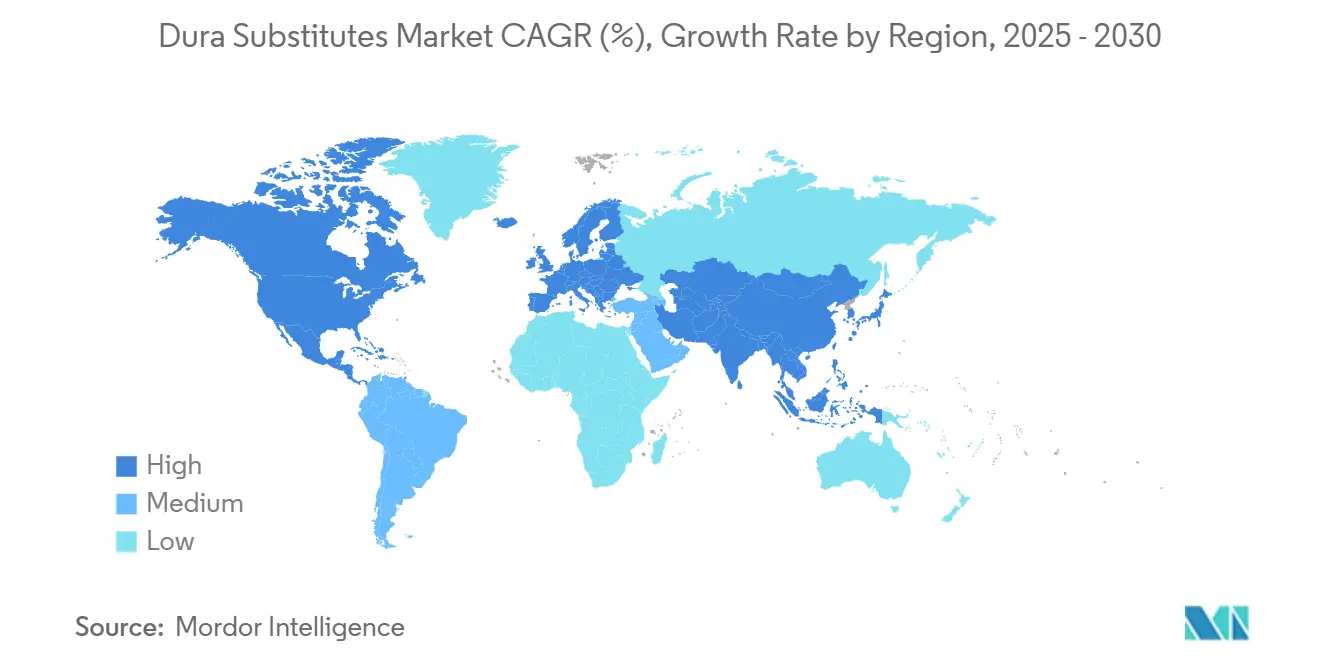

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dura Substitutes Market Analysis by Mordor Intelligence

The dura substitute market size stood at USD 212.8 million in 2025 and is forecast to reach USD 260.1 million by 2030, reflecting a 4.4% CAGR throughout the period. Sustained growth springs from the convergence of population aging, steady upticks in traumatic brain injuries, and greater surgeon confidence in advanced neurosurgical biomaterials. North America keeps its lead on procedure volumes and reimbursement depth, while Asia Pacific adds incremental momentum as hospitals expand neurosurgical capacity, particularly in China and fast-growing ASEAN economies. Companies are responding with next-generation biologic and synthetic matrices, 3D-printed custom grafts, and polymer chemistries that support minimally invasive approaches. Regulatory agencies have accelerated approvals of dura substitutes, robotic platforms, and closed-loop neuro-modulation devices, but persistent scrutiny around manufacturing practices and sterility prompts tighter quality systems. Competitive intensity has sharpened as multi-platform device makers pursue targeted acquisitions and joint ventures to broaden their neurosurgical footprints.

Key Report Takeaways

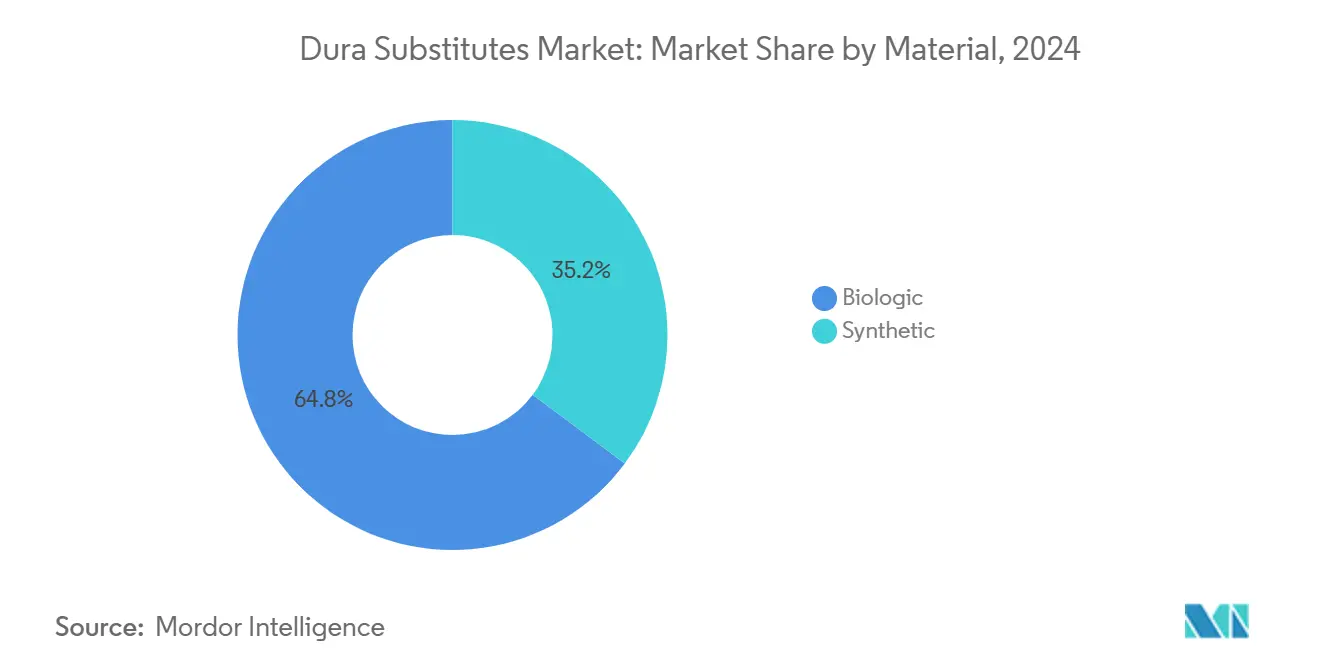

- By material, biologic grafts led with 64.8% of the dura substitute market share in 2024. Whereas synthetic grafts are projected to be the fastest-growing segment, expanding at a CAGR of 6.8% through 2030.

- By product configuration, onlay sheets captured 46.2% of the market in 2024, while 3D-printed custom grafts are projected to expand at an 8.5% CAGR through 2030.

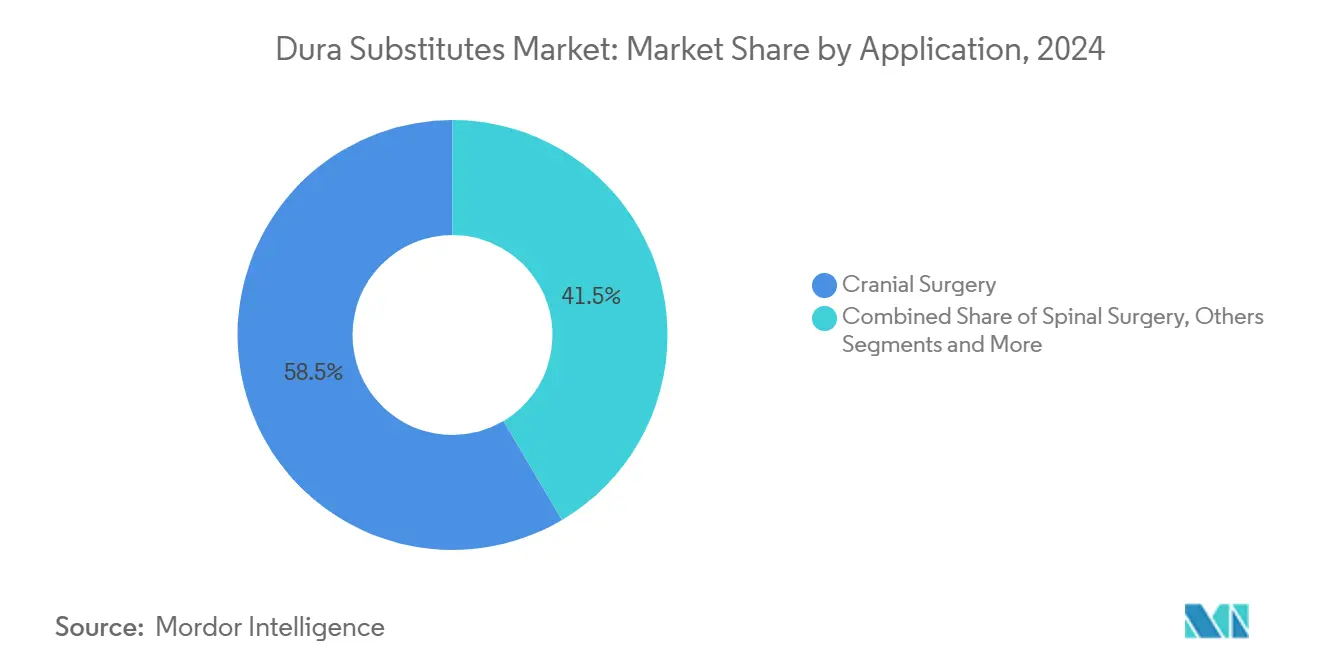

- By application, cranial surgery accounted for 58.5% of the market size in 2024, with spinal surgery advancing at a 5.2% CAGR through 2030.

- By end user, hospitals held a 72.4% revenue share in 2024, while ambulatory surgical centers are expected to grow at the highest CAGR of 4.1% through 2030.

- By geography, North America commanded 38.6% of the market size in 2024, while Asia Pacific is forecast to grow at a 7.6% CAGR through 2030.

Global Dura Substitutes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Rise In Neurosurgical Procedures | +1.20% | Global, particularly North America & Europe | Long term (≥ 4 years) |

| Increasing Adoption Of Minimally Invasive Duraplasty | +0.80% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rising Incidence Of Traumatic Brain Injuries Globally | +0.60% | Global, with higher impact in LMICs | Short term (≤ 2 years) |

| Surge In Regulatory Approvals & Product Launches | +0.40% | North America & Europe | Short term (≤ 2 years) |

| Development Of Antimicrobial & Drug-Eluting Dura substitutes | +0.30% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Growing Reimbursement Support For Regenerative Biomaterials | +0.20% | North America & select EU markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population Drives Unprecedented Neurosurgical Demand

The proportion of U.S. residents aged 65 and older will reach 20% by 2030, a demographic shift strongly correlated with chronic subdural hemorrhage and degenerative spinal conditions that necessitate dural repair. Medicare projections indicate sustained expansion in single-level and multilevel spinal instrumentation procedures through 2050, with biologic matrices such as collagen-based DuraGen widely selected for defect coverage.[1]John M. Rhee, “Projections of Single-Level and Multilevel Spinal Instrumentation Procedure Volume and Associated Costs for Medicare Patients to 2050,” Spine, pmc.ncbi.nlm.nih.gov European epidemiology mirrors these patterns, as meningioma resections and aneurysm clippings in octogenarians increase year after year. Across developed economies, the average neurosurgical case mix is trending older, thereby lifting the baseline demand for substitute dura that integrates quickly with compromised host tissue. These dynamics underpin predictable volume growth in the dura substitute market and reinforce the strategic importance of geriatric-focused clinical protocols.

Minimally Invasive Techniques Revolutionize Surgical Approaches

Robotic navigation, endoscopic corridors, and tubular retractors are reshaping duraplasty requirements. Medicare data show synthetic spinal dura substitute codes rising 161.86% between 2000 and 2021 as surgeons favor pliable, suture-free materials that fit through small incisions.[2]Ahmed Jalal et al., “Trends in Medicare procedural and reimbursement rates for spinal CSF leak repair (2000–2021),” The Journal of Neurosurgery-Focus, thejns.org Johnson & Johnson’s VELYS Active Robotics platform, cleared in 2024, offers sub-millimetric guidance that reduces graft trimming time and supports rapid watertight closure. Surgeons report that fully synthetic matrices fabricated from poly(lactic-co-glycolic acid) and poly-p-dioxanone withstand manipulation without fraying, making them suitable for spine endoscopy and keyhole cranial approaches. Minimally invasive momentum is also redirecting purchasing toward pre-hydrated pads, flowable putties, and 3D-printed anatomically matched constructs that minimize suture workload. Collectively, these advances reinforce premium pricing power for differentiated biomaterials inside the dura substitute market.

Global TBI Burden Intensifies Treatment Requirements

The Global Burden of Disease Study logged 20.84 million new traumatic brain injury cases in 2021, with falls as the leading cause among older adults. In the United States, age-adjusted TBI mortality climbed to 24.6 per 100,000 in 2020, peaking in the ≥85 years cohort.[3]Aditya Shah, “Mortality Trends of Traumatic Brain Injuries in the Adult Population of the United States: A CDC WONDER Analysis from 1999 to 2020,” BMC Public Health, bmcpublichealth.biomedcentral.com Such epidemiology fuels chronic subdural hematoma evacuations, decompressive craniectomies, and dural augmentation procedures across tertiary care hospitals. Economic analyses show Medicare spending of USD 37 million for TBI-related operations in 2021, much of which is allocated to grafts, sealants, and infection mitigation. As low- and middle-income countries scale trauma networks, they represent additional upside for cost-optimized synthetic substitutes, thereby expanding the total reachable dura substitute market.

Regulatory Innovation Accelerates Product Development

The U.S. FDA cleared more neurosurgery-adjacent devices in 2024 than any prior year, including adaptive deep brain stimulation, acellular tissue-engineered vessels, and spine guidance software. Medtronic’s asleep DBS approval and the CD Horizon ModuLeX spinal system exemplify the cross-pollination of neuromodulation, navigation, and graft technologies. Nevertheless, manufacturers face heightened Inspectional Observations, as highlighted by the December 2024 warning letter to Integra LifeSciences for sterility deviations. Such enforcement encourages proactive investment in clean-room validation and end-to-end traceability, ultimately uplifting product reliability and clinician trust in the dura substitute market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Biologic Grafts | -0.70% | Global, particularly emerging markets | Medium term (2-4 years) |

| Post-Operative CSF Leaks & Infection Risks Limiting Adoption | -0.50% | Global | Long term (≥ 4 years) |

| Stringent Regulatory & Clinical Evidence Requirements | -0.30% | Global, most stringent in North America & EU | Medium term (2-4 years) |

| Competition From Dural Sealants & Adhesives | -0.20% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Biologic Graft Costs Constrain Market Accessibility

Collagen-based xenografts command list prices up to 3× higher than synthetic meshes, constraining adoption in cost-sensitive systems even though clinical series report 0% foreign-body reactions and 1.9% infection incidence across 1.4 million implants. Compounding the challenge, Medicare reimbursement for spinal dura closure declined 26.02% between 2000 and 2021 despite growing procedural counts. Hospitals in Latin America and Southeast Asia often substitute lower-cost polyurethane films or autologous fascia to manage budget caps. Pricing pressure is therefore prompting vendors to streamline manufacturing, scale 3D-printing lines, and bundle grafts with sealants to deliver economic value, steps that may temper the negative impact, yet remain a tangible drag on dura substitute market expansion.

CSF Leak Complications Drive Conservative Surgical Approaches

Retrosigmoid craniotomy cohorts reveal CSF leak rates as high as 31%, a statistic that reinforces the need for watertight closure techniques and secondary sealant layers. Although dural sealant patches reduce leakage relative to suture-only repair, infection rates remain unchanged, underscoring surgeon caution when selecting foreign materials. Prospective trials of hydroxyapatite cement and nanofibrous patches continue to show promise but have yet to achieve broad reimbursement coverage. Until randomized multicenter evidence matures, some surgeons will default to autograft fascia or suture-centric closure, slightly diluting potential volume in the dura substitute market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Biologics Anchor the Market as Synthetic Momentum Builds

Biologic matrices secured 64.8% of the dura substitute market share in 2024, buoyed by more than 1 million successful implantations and decades of peer-reviewed validation. This dominance derives from predictable tissue integration, low immunogenicity, and surgeon familiarity. The synthetic cohort, however, is climbing at a 6.8% CAGR from 2025 to 2030 as polymer science delivers higher tensile strength and tighter porosity control. Early adopters cite mechanically robust fibers and favorable price points as reasons for switching, particularly in spinal fusion, where long suture lines increase operative time. Over the outlook period, biologics will retain primacy in complex cranial reconstruction, yet composite synthetics that incorporate antimicrobial agents are expected to narrow the gap, progressively diversifying vendor revenue across the dura substitute market.

Momentum in the synthetic class is headlined by Cerafix, a fully synthetic scaffold combining poly(lactic-co-glycolic acid) and poly-p-dioxanone that exhibits superior pull-out resistance during watertight closure. Xenografts remain the biologic workhorse, given their reliable supply chains and standardized collagen matrices, while allografts fill niche requests for matched histology in extensive skull base surgery. Autograft fascia lata remains an option where material cost or infection risk outweighs incremental operative time. Overall, pricing flexibility and sterilization advances ensure both material classes will coexist, sustaining durable buyer choice inside the dura substitute market.

By Product Configuration: Established Onlay Sheets Confront 3D-Printed Customization

Onlay sheets captured 46.2% of the dura substitute market size in 2024, thanks to wide operating-room availability, straightforward suture placement, and compatibility with both cranial and spinal indications. Surgeons value their predictable handling when reconstructing standard oval-shaped defects encountered in tumor resections and laminectomies. Custom 3D-printed grafts, though nascent, are scaling at an 8.5% CAGR and hold promise for irregular defects in skull base, sacral cyst, and pediatric deformity surgery. The shift aligns with the broader transition toward patient-specific implants facilitated by high-resolution intra-operative imaging and additive manufacturing platforms.

Flowable hydrogels and fibrin sealant-based plugs remain preferred for narrow corridors where sheet manipulation is impractical. Suturable patches with prefabricated eyelets continue to serve posterior fossa procedures where intracranial pressure spikes demand extra fixation. Over the forecast window, hybrid kits pairing pre-measured flowables with reinforcing mesh are likely to appear, broadening surgeon armamentaria and underpinning diversified revenue in the dura substitute market.

By Application: Cranial Supremacy Meets Spinal Acceleration

Cranial surgery represented 58.5% of the dura substitute market size in 2024, reflecting high volumes of aneurysm clipping, meningioma excision, and traumatic decompression. The aging profile of intracranial tumor patients, combined with wider MRI screening, perpetuates steady cranial demand. Spinal indications are projected to expand faster, climbing at a 5.2% CAGR, as degenerative disc disease and minimally invasive decompressions proliferate. Endoscopic spine techniques rely on pliant grafts that can be rolled and delivered through 8 mm ports, features that favor newer synthetics.

Ear, nose, and throat applications, including vestibular schwannoma resection, use thin vascularized flaps supplemented by small graft pads to avert CSF rhinorrhea, forming a secondary but rising segment. Peripheral nerve and traumatic extremity reconstructions leverage smaller graft sizes yet contribute incremental volume. Overall, diversified clinical pathways protect baseline growth in the dura substitute market while enabling vendors to price tactically across indication tiers.

By End User: Hospitals Retain Primacy as ASCs Gain Momentum

Hospitals generated 72.4% of revenue in 2024 because complex cranial cases and multilevel spine fusions necessitate advanced imaging, intensive monitoring, and multidisciplinary teams. Nonetheless, ambulatory surgical centers are recording the briskest expansion at a 4.1% CAGR as insurers steer appropriate lumbar decompressions and microdiscectomies to lower-cost outpatient venues. Successful endoscopic lumbar foraminotomies in octogenarians demonstrate the safety envelope of ASC neuro-orthopedic programs, a development that reshuffles procurement channels.

Specialty neurosurgical centers are gaining visibility for subdural hematoma evacuation, radiosurgery backup, and pediatric craniosynostosis correction. These focused facilities adopt bundle purchasing for grafts, sealants, and hemostats to support lean inventories, persuading manufacturers to craft value-based pricing packages. Such diversification across care settings assures recurring demand and competitive balance inside the dura substitute market.

Geography Analysis

North America controlled 38.6% of dura substitute market size in 2024, underpinned by high procedure density, favorable reimbursement, and entrenched supplier relationships. Aging baby boomers drive consistent cranial and spine caseloads, while academic centers accelerate protocol adoption of drug-eluting matrices. Reduced Medicare payments, however, are encouraging bulk purchasing and value analysis committees to scrutinize premium biologic grafts, presenting unit price pressure for incumbent vendors.

Europe sustains mature uptake through established neurosurgical societies and rigorous CE-mark pathways. German and Scandinavian hospitals especially favor xenograft collagen mats for skull base reconstruction, citing long safety records. Budget constraints, nonetheless, foster pilot use of low-cost polyurethane films in Southern European systems, a dynamic that may widen price segmentation across the dura substitute market.

Asia Pacific is the fastest-growing region, advancing at a 7.6% CAGR between 2025 and 2030. China’s Healthy China 2030 blueprint and accelerated device approvals have elevated local manufacturing and import substitution strategies. Public hospitals in Tier 1 cities now incorporate 3D-printed custom cranial plates and matching dura patches into trauma pathways. ASEAN nations, propelled by private equity investment into tertiary centers, are opening bid opportunities for mid-priced synthetic meshes that balance cost and performance. Latin America and the Middle East & Africa trail in adoption but represent long-term upside as neurosurgical residency programs and emergency transport systems modernize.

Competitive Landscape

The dura substitute market displays moderate concentration, with the top five suppliers controlling about 55% of global revenue. Integra LifeSciences, Medtronic, and B. Braun anchor the biologic portfolio, while Johnson & Johnson’s DePuy Synthes and Stryker target synthetic innovation and robotics integration. Integra’s acquisition of Acclarent in 2024 added ENT exposure worth USD 1 billion, diversifying its graft pull-through into skull base procedures. Stryker’s planned divestiture of its U.S. spinal implants franchise to Viscogliosi Brothers will spawn VB Spine, a channel-focused entity with exclusive access to Mako Spine and Copilot guidance, potentially reshaping procurement alignments in 2026.

Regulatory headwinds remain a strategic wild card. The FDA’s December 2024 warning to Integra catalyzed internal remediation and opened contract opportunities for rivals that comply with ISO 13485:2016 sterilization clauses. Meanwhile, Medtronic leverages AI-driven patient-reported outcome dashboards to bundle postoperative data analytics with its graft and hardware kits, differentiating on longitudinal value. Smaller entrants are pursuing orphan indications and antimicrobial coatings to capture neurological intensive care units. Collectively, these maneuvers indicate a market where technological breadth and regulatory resilience weigh as heavily as price in winning share.

Dura Substitutes Industry Leaders

Integra LifeSciences Holdings Corp.

Medtronic plc

Stryker Corp.

B. Braun Melsungen AG

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Integra LifeSciences broadens its portfolio with DuraGen Plus Square 2, a collagen-based matrix shipped through McKesson that conforms to curved neural surfaces, forms a watertight barrier against cerebrospinal fluid, and gradually resorbs without the need for sutures.

- April 2025: Elutia confirmed that its EluPro biologic graft will be introduced at HRS 2025. The material is positioning itself as a next-generation option that emphasizes biologic integration for reliable dural repair in cranial and spinal cases.

- February 2025: Integra LifeSciences published a peer-reviewed analysis showing that DuraSeal lowers overall treatment costs compared with traditional fibrin glue by reducing postoperative cerebrospinal fluid leaks.

Global Dura Substitutes Market Report Scope

| Biologic | Xenograft |

| Allograft | |

| Autograft | |

| Synthetic | ePTFE |

| Polyurethane | |

| Other Polymers |

| Onlay (sheet) |

| Suturable (patch) |

| Flowable / Fibrin sealant-based |

| 3D-printed custom grafts |

| Cranial Surgery |

| Spinal Surgery |

| Others (ENT, Trauma, Peripheral Nerve) |

| Hospitals |

| Specialty Neurosurgical Centers |

| Ambulatory Surgical Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Biologic | Xenograft |

| Allograft | ||

| Autograft | ||

| Synthetic | ePTFE | |

| Polyurethane | ||

| Other Polymers | ||

| By Product Configuration | Onlay (sheet) | |

| Suturable (patch) | ||

| Flowable / Fibrin sealant-based | ||

| 3D-printed custom grafts | ||

| By Application | Cranial Surgery | |

| Spinal Surgery | ||

| Others (ENT, Trauma, Peripheral Nerve) | ||

| By End User | Hospitals | |

| Specialty Neurosurgical Centers | ||

| Ambulatory Surgical Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global value of dura graft demand and how fast is it growing?

Demand stood at USD 212.8 million in 2025 and is projected to climb to USD 260.1 million by 2030, reflecting a 4.4% CAGR.

Which material class—biologic or synthetic—accounts for the larger share of dura graft usage today?

Biologic collagen-based matrices hold the lead with 64.8% share thanks to long clinical track records and strong surgeon familiarity.

How quickly are custom 3D-printed dura substitutes expected to expand over the next five years?

Custom 3D-printed grafts show the fastest adoption, advancing at an estimated 8.5% CAGR through 2030 as imaging-to-implant workflows mature.

Why is Asia Pacific viewed as the most promising growth territory for dura graft suppliers?

Hospital expansions, rising neurosurgical capacity, and supportive device-registration reforms are driving a 7.6% CAGR in the region through 2030.

What factor is currently the biggest cost barrier for wider adoption of biologic dura substitutes?

Premium pricing—often three times higher than synthetic meshes—remains the chief hurdle, especially for budget-constrained hospitals.

How are robotic and minimally invasive techniques influencing product development strategies?

These approaches favor thin, foldable, and suture-less grafts that can be delivered through small ports, prompting suppliers to engineer stronger yet more pliable synthetic and hybrid materials.

Page last updated on: