Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.94 Billion |

| Market Size (2031) | USD 2.92 Billion |

| Growth Rate (2026 - 2031) | 8.52% CAGR |

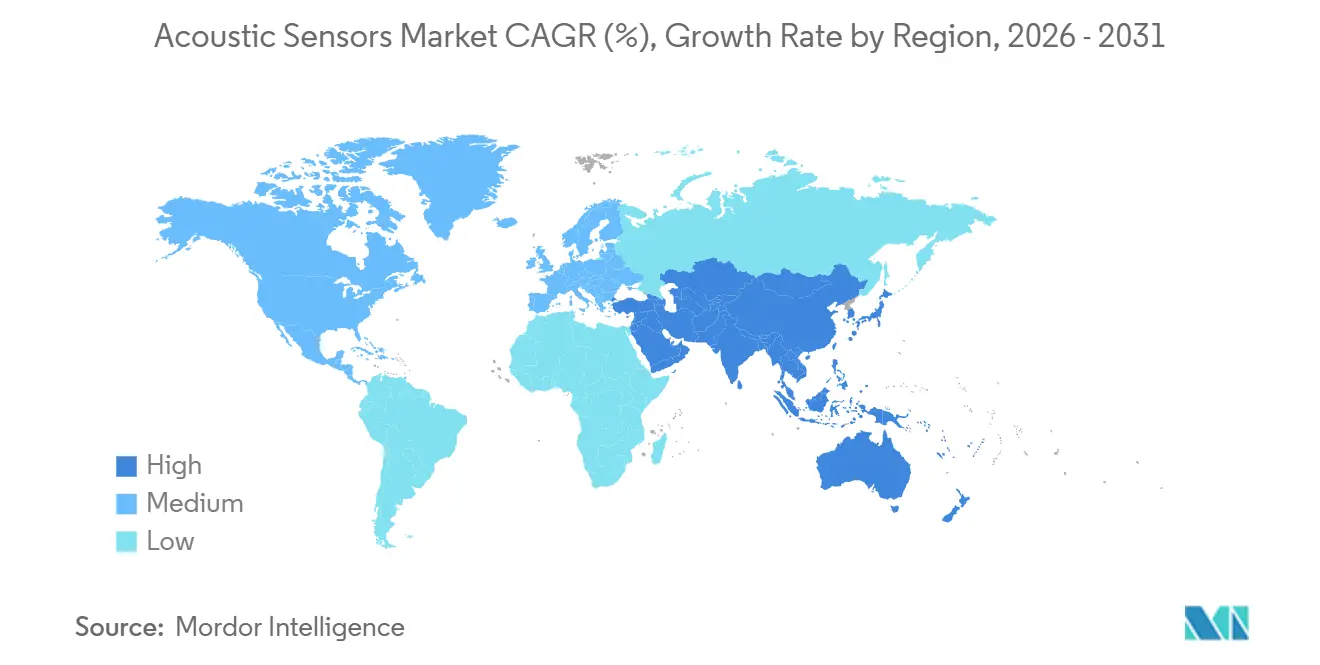

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

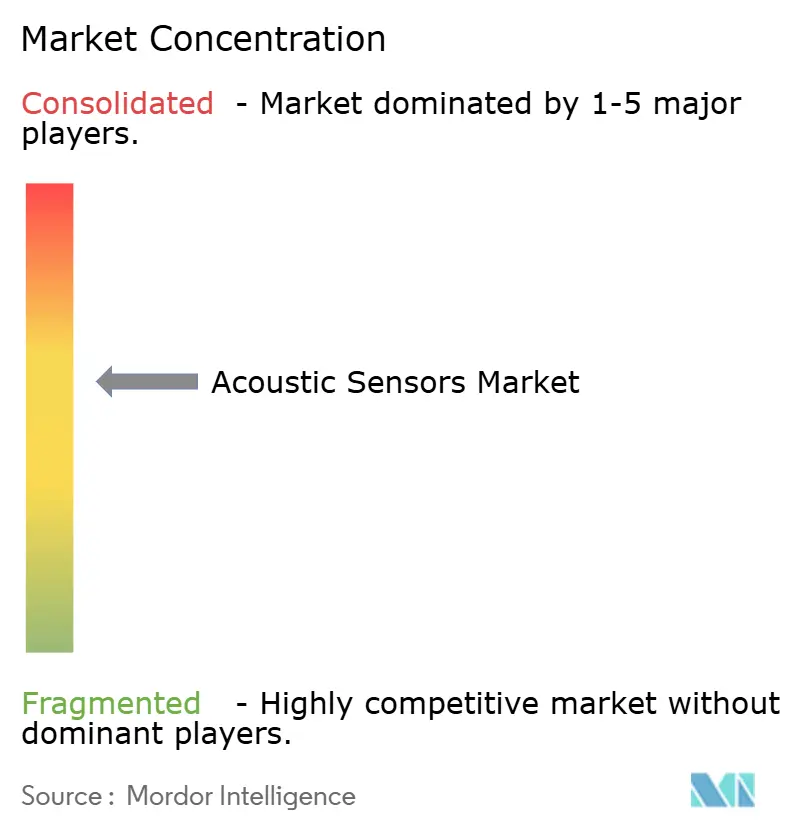

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acoustic Sensors Market Analysis by Mordor Intelligence

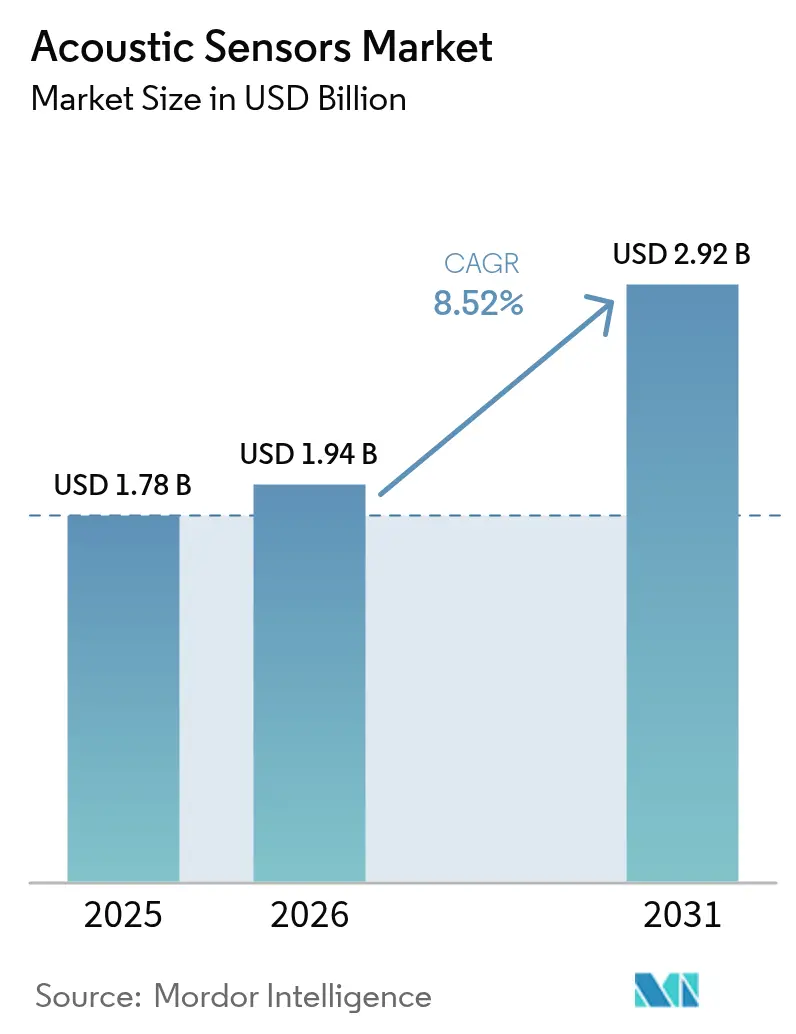

The acoustic sensors market size is expected to grow from USD 1.78 billion in 2025 to USD 1.94 billion in 2026 and is forecast to reach USD 2.92 billion by 2031 at 8.52% CAGR over 2026-2031. Rapid 5G and Wi-Fi 7 deployments, electrified-vehicle platforms that demand battery-free torque and pressure sensing, and the proliferation of industrial Internet of Things (IIoT) programs are expanding installed bases across telecom, automotive, and process-industry end users. Wireless form factors are growing faster than wired ones as operators retrofit legacy assets located in hazardous zones. Asia-Pacific leads both production and consumption because Chinese, Japanese, and South Korean manufacturers control ceramic powder synthesis, wafer processing, and module assembly capacity. Bulk acoustic wave (BAW) technology is gaining momentum in 6 GHz-plus filters for 5G base-stations, while flexible piezoelectric films promise sub-USD 1 disposable sensing surfaces for consumer and medical wearables.

Key Report Takeaways

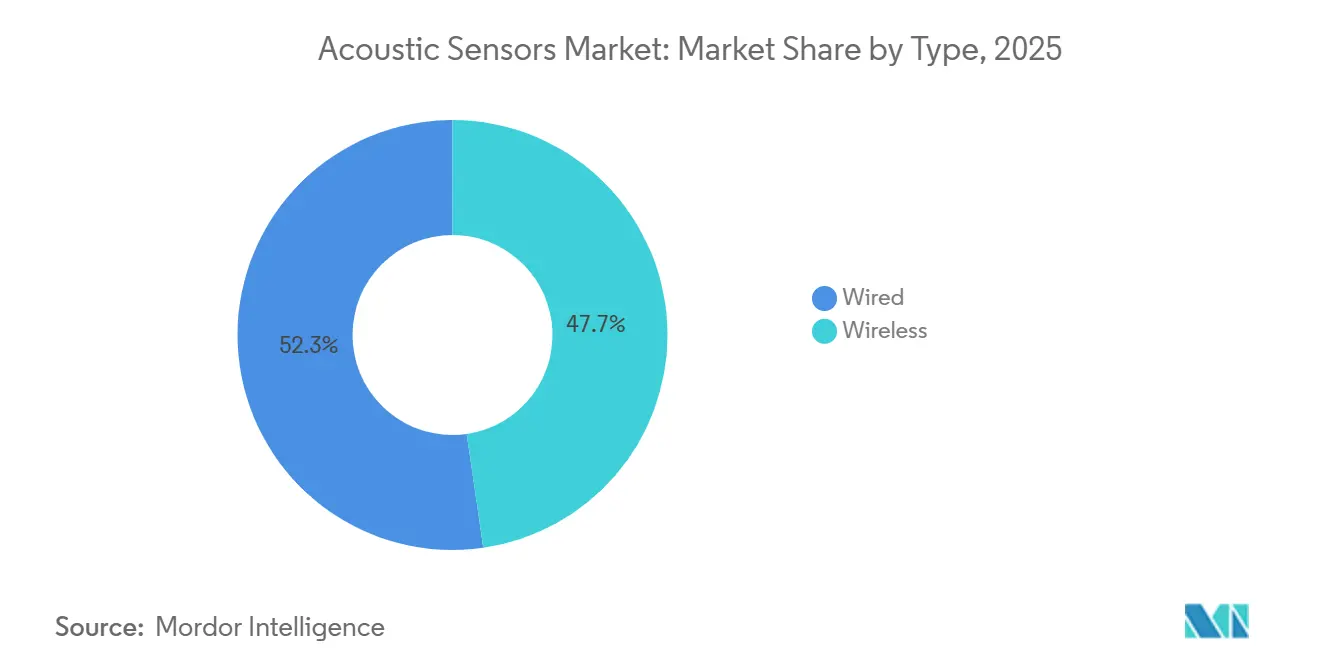

- By type, wireless configurations commanded 47.72% of the acoustic sensors market share in 2025, and are expanding at an 8.67% CAGR through 2031.

- By wave type, surface acoustic wave (SAW) devices held 55.81% revenue share in 2025, whereas BAW technology is projected to advance at an 8.79% CAGR over 2026-2031.

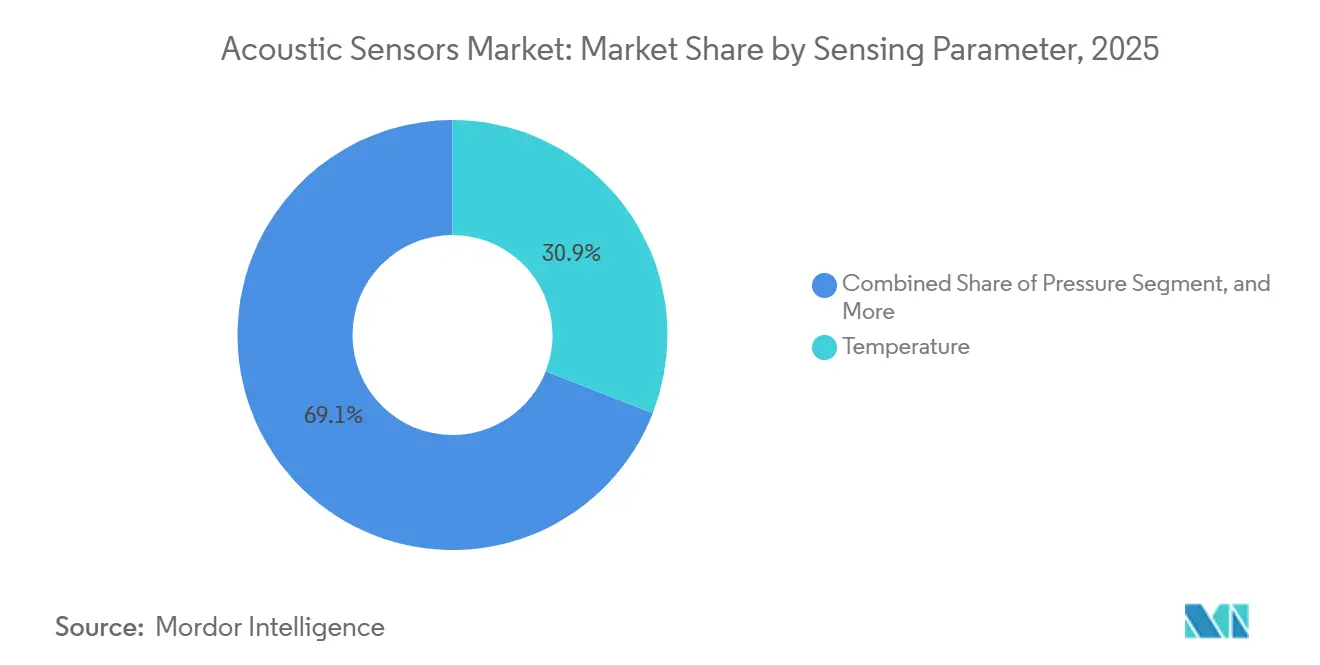

- By sensing parameter, temperature sensing led with 30.92% of the acoustic sensors market size in 2025; pressure measurement is the fastest-growing parameter at an 8.71% CAGR to 2031.

- By application, automotive led with 28.63% revenue share in 2025, while healthcare is set to expand at a 9.02% CAGR through 2031.

- By geography, Asia-Pacific generated 39.77% of 2025 revenue and is forecast to grow at a 9.16% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acoustic Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G and Wi-Fi 7 roll-outs raising demand for high-frequency SAW/BAW filters | +2.1% | Global, with concentration in North America, China, South Korea, Japan | Medium term (2-4 years) |

| Automotive shift to EVs and ADAS accelerating wireless, battery-free sensor adoption | +1.8% | North America, Europe, China | Medium term (2-4 years) |

| Growth of industrial IoT and predictive-maintenance programs | +1.5% | APAC core, spill-over to Europe and North America | Long term (≥ 4 years) |

| Printed and flexible piezoelectric films enabling ultra-low-cost sensing surfaces | +0.9% | Global, early adoption in consumer electronics hubs (China, South Korea) | Long term (≥ 4 years) |

| Miniaturized MEMS microphones powering voice-UI proliferation in wearables and hearables | +1.3% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Government regulations mandating real-time environmental and infrastructure monitoring | +1.0% | Europe, North America, select APAC markets (Japan, Singapore) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G and Wi-Fi 7 Roll-Outs Raising Demand for High-Frequency SAW and BAW Filters

Mobile-network operators activated 1.2 million 5G macro base stations worldwide in 2025, each integrating 12-16 BAW duplexers that meet sub-1.8 dB insertion-loss benchmarks needed for urban link budgets.[1]Qorvo, “BAW Filter Technology for 5G Infrastructure,” qorvo.com Wi-Fi 7 access points entered volume production during late 2024; their 6 GHz radios rely on BAW filters that suppress adjacent-channel interference below -50 dBc, a target conventional SAW devices cannot achieve above 5.5 GHz. Broadcom’s scandium-doped FBAR-7 node widened filter bandwidths by 15%, lowering resonator counts per duplexer and trimming die area by 25%. Spectrum auctions across India and Brazil, plus densification in the United States, add 2.1 percentage points to the acoustic sensors market growth outlook.

Automotive Shift to EVs and ADAS Accelerating Wireless, Battery-Free Sensor Adoption

Electric-vehicle drivetrains employ 8-12 wireless SAW torque transducers that harvest interrogation energy, eliminating slip rings and maintenance cycles.[2]Transense Technologies, “SAW Torque Sensors for EV Drivetrains,” transense.com Transense sensors deployed in BMW’s iX3 cut ownership costs by USD 180 per vehicle over 10 years. BAW-based tire-pressure modules in Tesla’s 2025 Model 3 refresh lowered false alarms by 40% while boosting phase-noise performance beyond ISO 21750 guidelines. Euro 7 rules effective July 2025 require real-time particulate-filter monitoring, a specification that non-contact SAW temperature probes satisfy, adding 1.8 percentage points to long-term demand.

Growth of Industrial IoT and Predictive-Maintenance Programs

Manufacturers installed 18 million wireless vibration and temperature nodes during 2025, up 28% year over year, to supervise pumps, compressors, and conveyors.[3]Honeywell International, “Forge Predictive Maintenance Platform,” honeywell.com SAW tags operating at 433 MHz transmit through 30 centimeters of concrete, enabling retrofits without Ethernet cabling. Honeywell’s Forge platform helped petrochemical plants cut downtime by 22%, translating to USD 4.2 million in average annual savings per site. Siemens integrated native SAW support into MindSphere, accelerating root-cause diagnostics to 48 hours. China’s “Made in China 2025” subsidies and India’s Production-Linked Incentive program amplify IIoT roll-outs, contributing 1.5 percentage points to CAGR.

Printed and Flexible Piezoelectric Films Enabling Ultra-Low-Cost Sensing Surfaces

Screen-printed PVDF and PZT composite films as thin as 50 µm allow disposable pressure-mapping arrays priced below USD 1 per sheet. TE Connectivity launched a 104-key flexible keyboard overlay in March 2025 that shrank bill-of-materials costs by 65% while enabling waterproof laptops. MIT researchers improved PVDF charge coefficients to 85 pC N⁻¹ by adding 8% graphene, maintaining flexibility through 100,000 bend cycles. Commercial roll-to-roll processes are forecast for 2028, and this innovation stream lifts forecast CAGR by 0.9 percentage points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Temperature-drift and packaging challenges in harsh environments | -1.2% | Global, acute in oil and gas, aerospace sectors | Medium term (2-4 years) |

| Competition from optical and capacitive alternatives in high-precision niches | -0.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Semiconductor supply-chain volatility pushing lead-times and input costs higher | -0.7% | Global, most severe in Asia-Pacific wafer supply | Short term (≤ 2 years) |

| Fragmented material standards hindering cross-platform interoperability | -0.5% | Global, regulatory friction in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Temperature-Drift and Packaging Challenges in Harsh Environments

SAW resonators on quartz shift -34 ppm °C⁻¹, degrading pressure accuracy below ±2% full scale in exhaust systems cycling from -40 °C to 180 °C. Dual-resonator compensation doubles die size and adds USD 1.10 to cost, while langasite substrates remain 3.5× pricier than quartz. High-temperature co-fired ceramic housings introduced in 2024 withstand 250 °C but raise sensor cost by USD 0.95. Field returns driven by hydrogen-sulfide ingression reached 18% in 2025. The restraint subtracts 1.2 percentage points from the baseline acoustic sensors market CAGR.

Competition From Optical and Capacitive Alternatives in High-Precision Niches

Fiber-optic Bragg gratings owned 62% of civil-infrastructure strain monitoring in 2025 due to sub-microstrain resolution and electromagnetic immunity. The Øresund Bridge replaced SAW gauges after ±15 µε drift over six-month calibrations. Capacitive MEMS accelerometers such as Analog Devices’ ADXL357 offer <10 µg Hz⁻½ noise, beating SAW gyroscopes’ bias instability and extending battery life by 18 months in seismic stations. The cost premium of optical solutions is tolerated in Europe and North America, clipping 0.8 percentage points from the acoustic sensors market trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Wireless Configurations Capture Retrofit and Hazardous-Zone Demand

Wireless units held 47.72% acoustic sensors market share in 2025 and are advancing at 8.67% per year, lifted by refinery, chemical, and mining operators that value retrofit simplicity. IEC 60079-11 revisions in 2024 raised permissible energy limits, allowing SAW tags to function safely in Zone 0 explosive atmospheres. Wireless sensors cut installed cost by USD 420 per point on offshore platforms because technicians avoid helicopter visits.

Wired designs still dominate high-bandwidth tasks such as ultrasonic flow metering, where 1 Mbit s⁻¹ throughput and sub-millisecond latency are mandatory. Honeywell’s Model 1604 wired SAW torque probe samples at 10 kHz inside Tesla’s Berlin press lines, trimming scrap by 12%. Hybrid power-plus-wireless-data topologies are emerging in building automation, enabling 24 V DC power while preserving placement flexibility. Consequently, wired demand continues to rise at a slower 7.8% clip.

By Wave Type: BAW Gains on 5G Filter Demand Despite SAW’s Incumbent Position

SAW devices contributed 55.81% of 2025 revenue because smartphone duplexers cost under USD 0.40 at scale. Yet BAW filters are forecast to expand at 8.79% annually through 2031 due to sub-1.8 dB insertion loss above 3 GHz and 10 W continuous-power handling.

Qorvo boosted BAW shipments 47% in 2025 on Chinese and United States macro cell upgrades. The transition to scandium-doped aluminum nitride raised coupling coefficients from 6.5% to 9.2%, enabling 15% wider channel bandwidths. Emerging Lamb-wave variants address biosensing, and TDK’s shear horizontal BAW gyroscope achieved 0.003 ° s⁻¹ bias instability for automotive safety controllers.

By Sensing Parameter: Pressure Measurement Accelerates on Process-Industry Digitization

Temperature sensing owned 30.92% of 2025 revenue; however, pressure modules exhibit the fastest 8.71% CAGR to 2031 as chemical and pharmaceutical plants instrument every vessel.

Endress and Hauser’s Cerabar PMP23 SAW transmitter meets ±0.25% accuracy at 40 MPa without signal-conditioners. Torque sensing, 14% share in 2025, is surging in e-mobility gearboxes. Humidity, mass, and viscosity remain single-digit niches yet comply with ISO 10012 traceability rules updated in 2024.

By Application: Healthcare Overtakes Automotive Growth as Wearables Scale

Automotive kept the largest 28.63% stake in 2025, led by tire-pressure, exhaust-gas temperature, and wireless torque probes. Healthcare grows the quickest, at 9.02% CAGR, as wearable and implantable devices exploit piezoelectric biocompatibility. Medtronic’s Reveal LINQ cardiac monitor operates 4.5 years on a single cell using a BAW accelerometer.

Abbott’s FreeStyle Libre 3 downsized to 5 mm modules by replacing analog front ends with SAW encoders, lifting adherence by 18%. Consumer electronics, industrial, aerospace, and environmental verticals round out the opportunity set for the acoustic sensors market.

Geography Analysis

Asia-Pacific generated 39.77% of the acoustic sensors market size in 2025 and is poised for a 9.16% CAGR through 2031. China budgeted CNY 18 billion (USD 2.5 billion) in 2025 to reach 40% filter self-sufficiency by 2027. Japanese leaders TDK and Murata operated 14 SAW lines that shipped 2.4 billion units and sustained >38% gross margins. India’s Production-Linked Incentive program lured USD 340 million into new assembly bases, and South Korea committed USD 280 million for BAW R&D in March 2025.

North America ranked second at 26% share in 2025. U.S. Department of Defense Trusted Foundry awards of USD 120 million secured domestic SAW supply for secure communications. General Motors integrated wireless torque probes across Ultium platforms, opening a USD 45 million annual demand pool. Canada’s National Research Council invested USD 16 million in printable piezoelectric research for bridge monitoring. Mexican Tier-1 production jumped 19% to 48 million units, underscoring the North American manufacturing corridor.

Europe supplied 23% of 2025 revenue. Germany’s Sensor4.0 initiative dispensed EUR 95 million (USD 102 million) to advance predictive-maintenance sensors. The European Union’s revised Industrial Emissions Directive compels 12,000 facilities to adopt continuous SAW gas monitors by 2027. Safran installed 1,200 wireless temperature nodes at LEAP turbofan lines, slicing scrap 8%. The United Kingdom’s National Physical Laboratory released calibration protocols that unlock custody-transfer approval for SAW pressure devices. South America, the Middle East, and Africa together accounted for the remaining 12%, led by Brazilian offshore oil and Saudi Arabian petrochemicals.

Competitive Landscape

The acoustic sensors market is moderately fragmented, the top five vendors—Murata Manufacturing, TDK Corporation, Kyocera, Honeywell International, and Microchip Technology—held 42% combined revenue in 2025. Vertical integration keeps Murata and TDK cycle times to 18 days and gross margins above 35%. Kyocera secured 14 patents on langasite and gallium-orthophosphate crystal cuts, attacking turbine and downhole niches. Transense Technologies and SENSeOR monetize battery-free torque and high-temperature platforms that earn 15-20% pricing premiums.

Capacity expansions dominate strategy. TDK earmarked USD 180 million for a new Akita SAW facility that will lift output by 400 million units in 2027. Murata finished a USD 95 million wafer-level packaging build-out in December 2024, trimming BAW package height to 0.55 mm for slim smartphones. Honeywell and TE Connectivity formed a joint program on flexible PVDF arrays that targets USD 85 million revenue by 2029.

Acquisitions tighten portfolios. Microchip Technology bought Vectron International for USD 165 million, grafting oven-controlled crystal oscillators and voltage-controlled SAW sources onto its embedded timing stack. Boston Piezo-Optics is piloting hybrid acoustic-optical sensors that merge SAW resonators and fiber-Bragg gratings for dual temperature-strain readouts. Patent filings in temperature-compensated cuts and hermetic packages climbed 18% year over year, signaling escalating R and D to tackle harsh-environment drift.

Acoustic Sensors Industry Leaders

Murata Manufacturing Co., Ltd.

TDK Corporation

KYOCERA Corporation

Honeywell International Inc.

Microchip Technology Inc. (Vectron International)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Murata Manufacturing plans to invest USD 200 million in a new bulk acoustic wave filter plant in Singapore, aiming to serve emerging 6G infrastructure needs. Production is slated to start in Q2 2026, and the site will be able to turn out 500 million units a year, positioning the company to secure an early foothold in next-generation wireless systems.

- September 2025: TDK Corporation has broadened its industrial IoT portfolio by acquiring German specialist SENSeOR SAS for EUR 120 million (USD 128 million). The deal, finalized in September 2025, brings advanced surface acoustic wave technology for harsh-environment monitoring and strengthens TDK’s presence in Europe’s automation market.

- August 2025: KYOCERA Corporation earned FDA clearance for its biocompatible acoustic sensors intended for implantable medical devices. This milestone, announced in August 2025, clears the way for commercial use in long-term cardiac monitoring and opens a high-value path for acoustic sensing in regulated healthcare applications.

- July 2025: Honeywell International won a USD 45 million contract from the European Space Agency in July 2025 to supply acoustic sensors for satellite structural-health monitoring. Deliveries are scheduled for 2027, underscoring the growing role of acoustic sensing in safeguarding critical aerospace assets.

Global Acoustic Sensors Market Report Scope

Acoustic sensors provide a signal by rapidly shifting a diaphragm back and forth, which causes the air surrounding the diaphragm to be displaced and produces an acoustic wave. Typically, ultrasonic frequencies are used by acoustic distance sensors.

The Acoustic Sensors Market Report is Segmented by Type (Wired, Wireless), Wave Type (Surface Acoustic Wave, Bulk Acoustic Wave), Sensing Parameter (Temperature, Pressure, Torque, Humidity, Mass, Viscosity), Application (Automotive, Aerospace and Defense, Consumer Electronics, Healthcare, Industrial, Environmental Monitoring, Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Type

| Wired |

| Wireless |

By Wave Type

| Surface Acoustic Wave (SAW) |

| Bulk Acoustic Wave (BAW) |

By Sensing Parameter

| Temperature |

| Pressure |

| Torque |

| Humidity |

| Mass |

| Viscosity |

By Application

| Automotive |

| Aerospace and Defense |

| Consumer Electronics |

| Healthcare |

| Industrial |

| Environmental Monitoring |

| Other Applications |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Type | Wired | |

| Wireless | ||

| By Wave Type | Surface Acoustic Wave (SAW) | |

| Bulk Acoustic Wave (BAW) | ||

| By Sensing Parameter | Temperature | |

| Pressure | ||

| Torque | ||

| Humidity | ||

| Mass | ||

| Viscosity | ||

| By Application | Automotive | |

| Aerospace and Defense | ||

| Consumer Electronics | ||

| Healthcare | ||

| Industrial | ||

| Environmental Monitoring | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the acoustic sensors market in 2031?

The acoustic sensors market is projected to reach USD 2.92 billion by 2031.

Which configuration is growing faster, wireless or wired?

Wireless acoustic sensors are expanding at an 8.67% CAGR through 2031, outpacing wired alternatives.

Which region leads in revenue and growth?

Asia-Pacific generated 39.77% of 2025 revenue and is forecast to grow at 9.16% CAGR, the fastest worldwide.

Why are BAW devices gaining share over SAW?

BAW filters handle higher frequencies and power, making them essential for 5G base-stations and Wi-Fi 7 equipment.

Which end-use segment is expected to grow the quickest?

Healthcare is the fastest-growing application, advancing at a 9.02% CAGR as wearables and implantables scale.

Page last updated on: