Soundproof Curtains Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.13 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soundproof Curtains Market Analysis by Mordor Intelligence

The Soundproof Curtains Market size was valued at USD 2.29 billion in 2025 and is estimated to grow from USD 2.41 billion in 2026 to reach USD 3.13 billion by 2031, at a CAGR of 5.33% during the forecast period (2026-2031). Sustained growth comes from hybrid-work patterns that elevate acoustic privacy to a basic workplace requirement, green-building scorecards that award credits for low-carbon acoustic treatments, and IoT sensors that expose previously hidden noise problems in offices, schools, and hospitals. The pace appears moderate, yet high-performance products built around recycled PET felt and natural fibers are displacing legacy PVC laminates because regulators now place a monetary value on end-of-life recyclability. Manufacturers that combine verified fire resistance, humidity resilience, and embedded sustainability reporting are capturing disproportionate visibility on public-sector and Fortune 500 procurement lists. Competitive intensity is rising as incumbents accelerate product launches to pre-empt price-focused entrants from Asia-Pacific, signaling that scale and certification depth are becoming the new entry barriers.

Key Report Takeaways

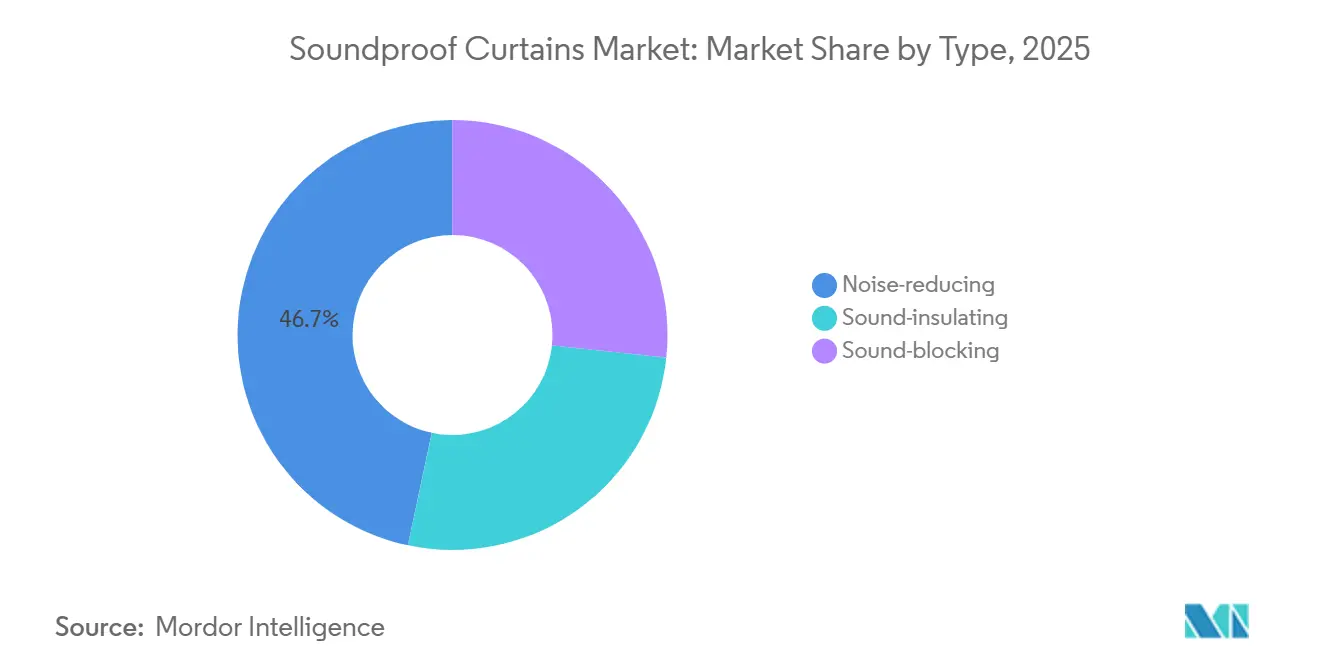

- By type, noise-reducing curtains led with 46.68% of the soundproof curtains market share in 2025, while sound-blocking variants are advancing at a 5.72% CAGR through 2031.

- By material, glass wool maintained 30.11% share of the soundproof curtains market size in 2025, but recycled PET felt is forecast to post the highest segment growth at 5.60% CAGR to 2031.

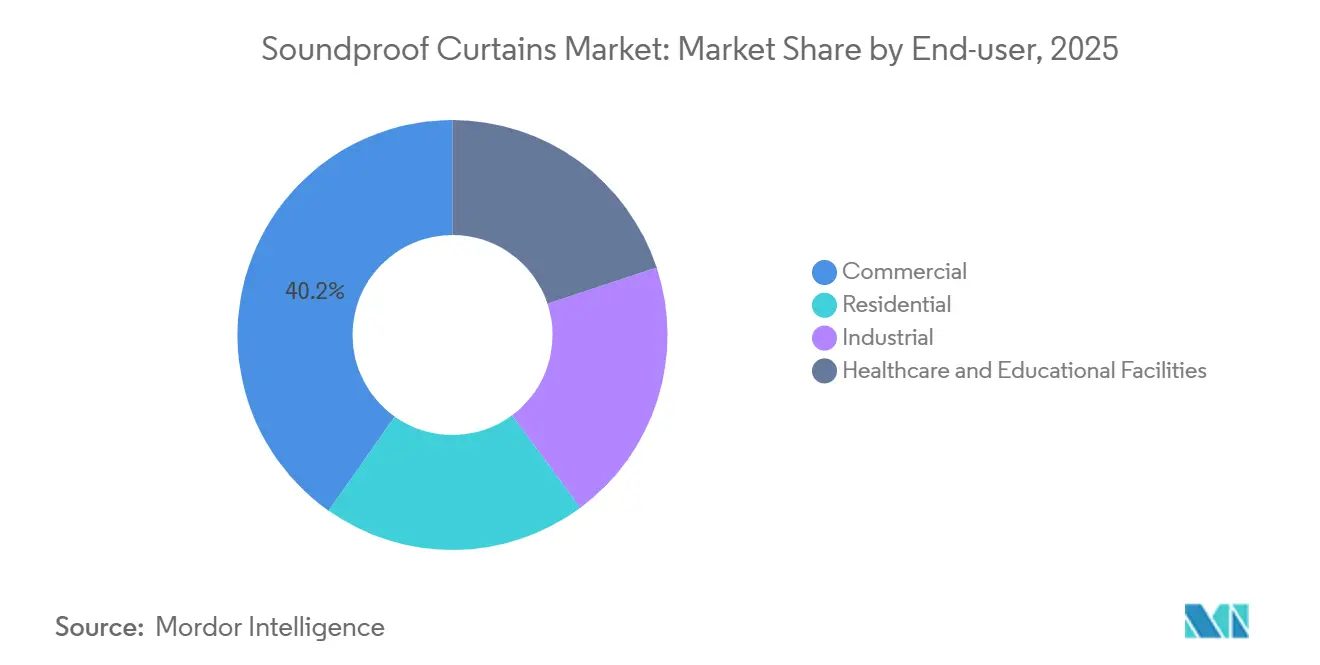

- By end-user, commercial facilities held 40.22% of 2025 demand, yet residential retrofits are recording the fastest growth at 5.89% CAGR through 2031.

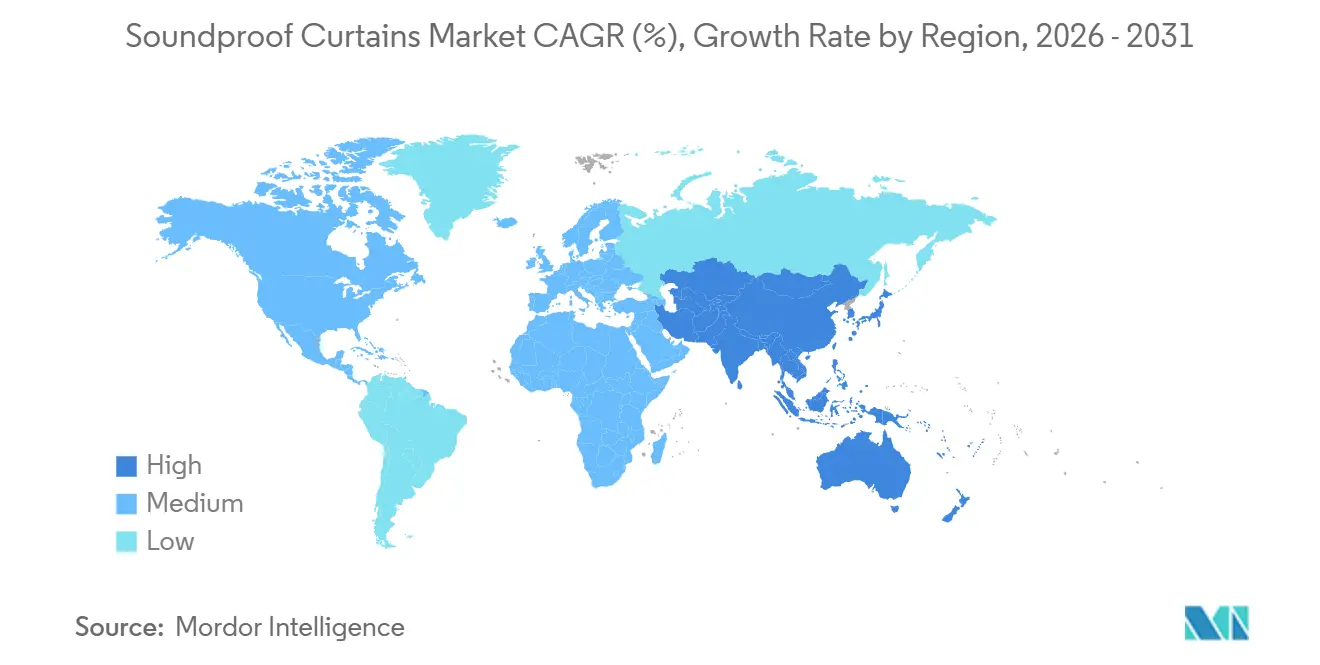

- By geography, Asia-Pacific accounted for 41.78% of 2025 revenue and is projected to expand at a 6.05% CAGR through 2031, outpacing every other region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soundproof Curtains Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in remote-working and home-studio culture | +1.20% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Industrial noise-exposure limits becoming stricter | +0.90% | Global, led by North America and EU; spillover to ASEAN and India | Long term (≥ 4 years) |

| Green-building credits rewarding acoustic comfort | +1.10% | North America, EU, and Australia; emerging in China and UAE | Medium term (2-4 years) |

| IoT-enabled acoustic monitoring spurring retrofit demand | +0.80% | North America and EU commercial real estate; pilot deployments in Singapore and Japan | Long term (≥ 4 years) |

| Circular-economy mandates favoring recyclable drapes | +1.00% | EU core, with early adoption in California and British Columbia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industrial Noise-Exposure Limits Becoming Stricter

With OSHA and European Union (EU) regulators ramping up audits on sound levels in factories and warehouses, operators are now investing in engineering controls whenever decibel readings exceed the threshold over an 8-hour shift[1]Occupational Safety & Health Administration, “Occupational Noise Exposure,” osha.gov . Movable barriers, increasingly adopted by automotive, e-commerce, and food-processing plants, are not only more cost-effective than rigid enclosures but also offer the added advantage of being relocated during layout changes. Quarterly noise-monitoring mandates, introduced in 2025 across Germany, France, and Italy, have resulted in a spike in order backlogs for heavy vinyl-laminate curtains known for their high attenuation. In the rapidly expanding Asia-Pacific markets, multinationals are aligning their worker-safety reporting with stringent European Union (EU) standards, leading to a heightened demand for certified acoustic drapes, even in areas where local regulations are still evolving.

Green-Building Credits Rewarding Acoustic Comfort

Developers are turning to curtain-based absorption systems, which complement ceiling panels and sound masking, as LEED v4.1 awards credits for indoor acoustic quality and WELL v2 sets background limits[2]U.S. Green Building Council, “LEED v4.1 Indoor Environmental Quality,” usgbc.org . These acoustic credits are in high demand among landlords, as LEED-certified offices can command premium rents in major cities, establishing a direct link between curtain investments and revenue boosts. Certification bodies are now emphasizing Environmental Product Declarations that spotlight embodied carbon, sidelining PVC-laminate products due to their recyclability issues. Suppliers like Knauf Insulation are integrating bio-based binders into their glass-wool cores, ensuring compliance with VOC and formaldehyde standards, and aligning their acoustic products with green-building criteria.

IoT-Enabled Acoustic Monitoring Spurring Retrofit Demand

Affordable sensor networks are producing intricate noise maps, pinpointing issues like low-frequency HVAC noises and elevator shaft sounds that often evade periodic audits. By early 2024, Soundsensing had gathered extensive data from various buildings, prompting retrofits in sites where violations were identified. Facility managers are now swiftly deciding on targeted curtain installations, a marked acceleration from previous timelines. With acoustic key-performance indicators now featured on building-automation dashboards alongside temperature and air quality metrics, multitenant landlords are deploying these dashboards across their properties, indicating a rising curtain demand through the forecast period of 2026-2031.

Circular-Economy Mandates Favoring Recyclable Drapes

Effective since January 2025, the European Union's (EU) Extended Producer Responsibility requires textile suppliers to bear the costs of collection and recycling, making landfill-bound PVC composites a less viable choice. Curtains crafted from recycled PET felt, which contain a high percentage of post-consumer bottles, achieve commendable NRC ratings and use considerably less energy than virgin polyester, aligning with the Scope 3 emission targets of corporate buyers. Autex’s carbon-negative Embrace wool panels are not only setting a benchmark in sustainability but are also gaining traction in public-sector tenders where embodied-carbon disclosure is mandatory. Fabricators neglecting recyclability may find themselves excluded from key supplier lists in the near future.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance degradation in humid climates | -0.60% | Southeast Asia, coastal India, Gulf Cooperation Council states, and tropical Africa | Short term (≤ 2 years) |

| Fire-safety certification gaps in emerging markets | -0.50% | Middle-East, Africa, and South Asia, where NFPA and EN standards remain voluntary | Medium term (2-4 years) |

| Limited recyclability of multi-layer PVC composites | -0.40% | EU and North America, where EPR schemes penalize non-recyclable materials | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Performance Degradation in Humid Climates

When relative humidity exceeds 70%, polyester-fiber curtains experience a drop in attenuation. Test observations indicate that swollen fibers reduce internal porosity. In coastal regions such as Indonesia, Vietnam, and the Philippines, humidity levels often exceed 80% for most of the year. This discrepancy leads to a gap between laboratory STC ratings and real-world performance. Untreated organic fabrics, which are susceptible to mold and mildew, emit odors that violate healthcare hygiene standards, necessitating premature replacement. Currently, specifiers lack a unified humidity-resilience label and rely on anecdotal evidence, which extends tender cycles. Without a dedicated ISO standard, humidity challenges have persisted, hindering adoption in tropical growth markets.

Fire-Safety Certification Gaps in Emerging Markets

In several Middle-Eastern and African nations, certain standards are merely optional. This gap allows non-certified imports to undercut the prices of compliant curtains. Consequently, multinationals are gravitating toward pricier EU-rated curtains for their facilities. This choice has bifurcated demand, clearly distinguishing between premium and budget-conscious channels. While Europe shows a demand for specifically rated melamine-foam products, these face hurdles in regions lacking regulations, where polyurethane alternatives dominate. In light of toxic smoke emissions from recent warehouse fires, insurers are pushing local authorities to implement stricter regulations. However, with legislative reforms potentially taking time, achieving global uniformity in standards remains a daunting task.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Sound-Blocking Variants Gain as Hybrid Work Normalizes

Sound-blocking curtains are projected to grow at a 5.72% CAGR during the forecast period of 2026-2031, gradually reducing the 46.68% revenue share held by noise-reducing products in 2025. This trend highlights the demand among end-users for complete acoustic isolation during video calls, where every decibel is critical. As a result, the market for soundproof curtains, particularly sound-blocking variants, is expanding at a faster rate than overall demand. This growth is supported by specifications that align with enterprise procurement criteria. In mixed-use buildings, owners are increasingly selecting sound-blocking curtains for party walls to effectively shield apartments from the after-hours noise of adjacent retail entertainment.

Sound-insulating curtains, which combine noise reduction with blackout and thermal benefits, are gaining popularity in colder regions, where energy savings justify the higher costs. Moondream’s patented design features a metalized layer that reflects mid-frequency noise and a cotton-felt backing that absorbs internal echoes, showcasing a blend of diverse performance attributes. While industrial buyers have traditionally preferred heavy vinyl laminate to meet noise reduction standards, lighter residential-grade blocking curtains are now achieving comparable performance levels, narrowing the distinctions between user categories.

By Material: Recycled PET Felt Disrupts Glass Wool Dominance

Glass wool, long lauded for its fire resistance and thermal conductivity, accounted for 30.11% of 2025's revenue. However, recycled PET felt is projected to grow at 5.60% during the forecast period of 2026-2031, closing the gap as policies promoting a circular economy find value in avoiding landfills. Contractors frequently grant extra LEED points to PET-felt curtains over glass wool, thanks to the former's superior post-consumer content. This tilt in preference sways competitive tenders towards felt. While fire-rated glass wool is the preferred choice for hospitals and data centers seeking Euroclass A1 non-combustibility, standard PET felt falls short of this standard without sacrificing recyclability through chemical additives.

Rock wool, known for its high-temperature resilience, caters to furnaces and power-generation housings. On the other hand, while plastic foams raise flammability alarms, they attract budget-minded retrofits. Natural fibers, now a staple in boutique hotels, command a premium but cater to biophilic designs that enhance wellness. High-density vinyl laminate dominates the soundproof curtain market for factories. However, research and development efforts are shifting towards bio-vinyl formulations to sidestep EPR recovery fees. Germany’s WAVE project offers a forward-looking perspective, crafting 3D acoustic forms from surplus sheep wool, hinting at a future where petrochemical foams might be replaced.

By End-User: Residential Retrofit Outpaces Commercial New-Build

Residential buyers are projected to lead all segments with a 5.89% CAGR during the forecast period of 2026-2031, driven by the ongoing trend of hybrid work and a cultural shift toward media creation at home. Consequently, the market for soundproof curtains in both single-family and multifamily residences is poised to eclipse commercial sales by the decade's end. Homeowners are turning to acoustic treatments not only for home offices but also for nurseries and bedrooms that share walls. Retailers have observed a notable uptick in weekend sales, especially for do-it-yourself kits equipped with magnetic tracks, catering to renters who prefer installations without wall drilling.

Nonetheless, commercial offices still command the largest revenue share at 40.22% in 2025, primarily due to the prevalent trend of open-plan retrofits. In 2025, WELL audits highlighted a notable initial failure rate concerning speech privacy, leading landlords to add curtain partitions for certification compliance. Healthcare facilities are deploying curtains to bridge the gap between actual ward noise and the WHO's recommended standards, ensuring better patient recovery. In industrial environments, users lean toward modular drapes that can swiftly adapt to changes on the assembly line, while educational institutions are choosing mid-range options to boost speech clarity in classrooms, avoiding any structural modifications.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 41.78% of global revenue and is projected to grow at a 6.05% CAGR through the forecast period of 2026-2031, fueled by China's export-driven factories and India's urban expansion. Qingdao Catilan, having boosted its 2024 revenue, predominantly exports to North America and Europe, reinforcing the region's leadership in standardized curtain supplies. Guangdong Chuangya, leveraging scale and competitive labor, exports most of its production overseas, pricing its products significantly lower than Western counterparts. Japan and South Korea are pivoting towards high-margin natural fibers and recycled PET variants, resonating with consumer environmental concerns. In coastal ASEAN cities, humidity-related challenges are curbing polyester sales, prompting intensified research and development into moisture-resistant blends.

North America showcases a split landscape. Coastal hubs such as New York, Seattle, and Toronto prioritize LEED-compliant drapes with explicit Environmental Product Declarations (EPDs), while inland states focus on upfront costs, sourcing Asia-Pacific products via consolidation centers in Canada and Mexico. The United States tops per-capita spending, aided by corporate policies reimbursing employees for home-office acoustic enhancements. At the same time, Canada's Extended Producer Responsibility (EPR) regulations, effective July 2025, are mandating heightened recycled content in public initiatives.

Europe sets the gold standard for environmental compliance. Since 2000, the bloc has made significant strides in PVC recycling, and with the new Green Deal, aims to double textile-waste recovery by 2030. Curtains lacking end-of-life take-back schemes face buyer penalties, leading to a rise in PET felt and wool usage. Fire regulations in EN 13501-1 are rigorously enforced, effectively excluding non-certified imports from public tenders. Additionally, energy price fluctuations are prompting facility owners in Germany and Italy to favor multi-layer curtains, which offer substantial winter heating savings.

Regions such as South America, the Middle-East and Africa are ripe for exploration. In Brazil, high-rise markets in São Paulo and Rio emphasize acoustic privacy, sidestepping stringent fire ratings, allowing cost-effective polyurethane products to dominate. In the Gulf Cooperation Council, mega-projects such as Saudi Arabia's Neom are receptive to premium suppliers but demand rapid turnarounds, benefiting vendors with local storage. While currency shifts in South Africa curtail import volumes, e-commerce is stepping in, delivering small-format curtains to consumers. However, a lack of standardized benchmarks across these regions depresses average selling prices and elongates the payback period for certification investments.

Competitive Landscape

The soundproof curtains market is moderately fragmented, with no single player commanding global revenues. Kinetics Noise Control, between June 2025 and March 2026, rolled out several acoustic barrier products, aiming to strengthen its foothold in North-America industrial retrofits. In a parallel move, Hunter Douglas is riding the wave of sustainability, unveiling its HeartFelt Islands ceiling panels. These panels, boasting a Cradle to Cradle Bronze certification, position the company favorably in the green-building procurement landscape.

Chinese manufacturers are aggressively pricing their products and ensuring swift lead times. However, their failure to meet NFPA and EN fire test standards limits their reach in regulated markets. To bolster their market stance, many have set up fulfillment centers in Vancouver and Monterrey, a strategy designed to cut delivery times and sidestep U.S. tariffs. Conversely, midsize specialists in Europe, such as Moondream, are harnessing design patents to protect their niche margins. They have pivoted to direct-to-consumer online sales, effectively dodging distributor mark-ups.

As the market looks to the future, it is setting its sights on innovations. These include humidity-resilient composites tailored for tropical climates and smart curtains embedded with RFID tags that transmit maintenance data to digital twins. Yet, these cutting-edge advancements come with hefty capital demands, a hurdle for smaller regional players. This landscape suggests a looming wave of consolidation, especially with rising costs tied to sustainability reporting and third-party audits. Significantly, there has been a surge in private-equity interest, highlighted by recent cross-border transactions centering on brands with certified supply chains and strong e-commerce footprints.

Soundproof Curtains Industry Leaders

Acoustical Surfaces Inc.

Flexshield Group Pty Ltd

Hunter Douglas

Moondream

Sound Seal

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Impact Acoustic has partnered with NCS+ to enhance accessibility to acoustic solutions. This collaboration streamlines the integration of color and material for designers and architects through digital workflows, fostering innovation and accessibility in the soundproof curtains market.

- March 2024: Impact Acoustic received the prestigious "iF Design Award 2024" for its ARCHISONIC Cotton round acoustic material, highlighting its focus on innovation and design excellence. This recognition is expected to drive advancements in the soundproof curtains market by promoting the adoption of high-performance acoustic materials.

Global Soundproof Curtains Market Report Scope

Soundproof curtains are specifically designed to manage sound waves by blocking, absorbing, and reducing noise transmission. These curtains are made using dense fabrics, multiple layers, and acoustic-grade materials, creating a quieter and more controlled sound environment.

The Soundproof Curtains Market is segmented by type, material, end-user, and geography. By type, the market is segmented into sound-insulating, noise-reducing, and sound-blocking. By material, the market is segmented into glass wool, rock wool, plastic foams, natural fibers, high-density vinyl laminate, and recycled PET felt. By end-user, the market is segmented into residential, commercial, industrial, healthcare and educational facilities. The report also covers the market size and forecasts for soundproof curtains in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Sound-insulating |

| Noise-reducing |

| Sound-blocking |

| Glass Wool |

| Rock Wool |

| Plastic Foams |

| Natural Fibers |

| High-density Vinyl Laminate |

| Recycled PET Felt |

| Residential |

| Commercial |

| Industrial |

| Healthcare and Educational Facilities |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Sound-insulating | |

| Noise-reducing | ||

| Sound-blocking | ||

| By Material | Glass Wool | |

| Rock Wool | ||

| Plastic Foams | ||

| Natural Fibers | ||

| High-density Vinyl Laminate | ||

| Recycled PET Felt | ||

| By End-user | Residential | |

| Commercial | ||

| Industrial | ||

| Healthcare and Educational Facilities | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the soundproof curtains market?

The soundproof curtains market stands at USD 2.41 billion in 2026 and is forecast to reach USD 3.13 billion by 2031 at a 5.33% CAGR from 2026 to 2031.

Which region is growing fastest in acoustic-curtain uptake?

Asia-Pacific leads growth with a projected 6.05% CAGR thanks to China’s manufacturing scale and India’s infrastructure boom.

What material is taking share from glass wool?

Recycled PET felt is advancing at a 5.60% CAGR because circular-economy rules monetize its high post-consumer content.

Why are residential purchases accelerating?

Hybrid-work policies and at-home content creation push homeowners to invest USD 200-600 per room in curtains that meet corporate video-call standards.

What certifications influence procurement in mature markets?

Fire ratings such as NFPA 286 and EN 13501-1, plus LEED, WELL, and cradle-to-cradle material disclosures, drive product selection among corporate and public buyers.

Page last updated on: