Extrusion Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.19 Billion |

| Market Size (2031) | USD 9.19 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

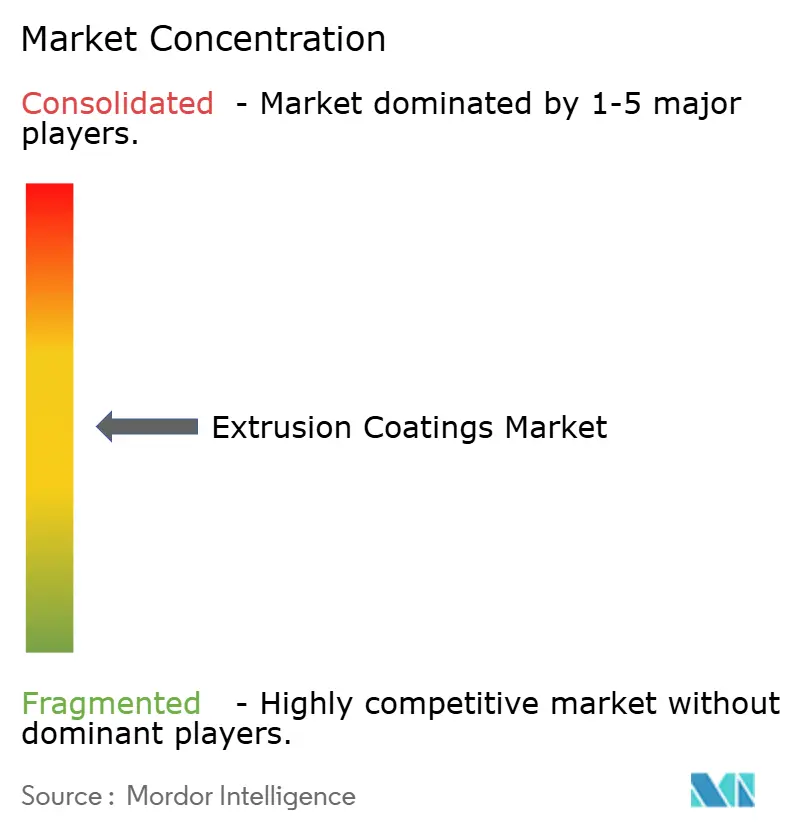

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Extrusion Coatings Market Analysis by Mordor Intelligence

The extrusion coatings market size was valued at USD 6.85 billion in 2025 and estimated to grow from USD 7.19 billion in 2026 to reach USD 9.19 billion by 2031, at a CAGR of 5.02% during the forecast period (2026-2031). Rapid uptake of barrier-enhanced polymers in liquid food formats, e-commerce mailers, and sterile pharmaceutical packs anchors the current demand base. Regulatory tailwinds—from the European Union’s Packaging and Packaging Waste Regulation to national recycled-content mandates—are accelerating shifts toward mono-material structures, while steady urbanization in Asia-Pacific expands end-market volumes. Volatility in polyolefin feedstock pricing and the sector’s carbon footprint remain headwinds, yet sustained investments in bio-based resins and advanced mechanical recycling temper these risks. Market leaders are countering cost pressure through vertical integration, long-term supply contracts, and pilot lines that validate recyclable coating architectures at commercial scale.

Key Report Takeaways

- By material, polyethylene held 42.12% of the extrusion coatings market share in 2025; ethyl vinyl acetate is forecast to post the fastest 5.67% CAGR through 2031.

- By substrate, paperboard and cardboard accounted for 52.10% of the extrusion coatings market in 2025, whereas polymer films are poised to expand at 6.34% CAGR between 2026-2031.

- By application, liquid packaging led with 48.41% revenue share in 2025, while medical packaging is advancing at a 7.52% CAGR to 2031.

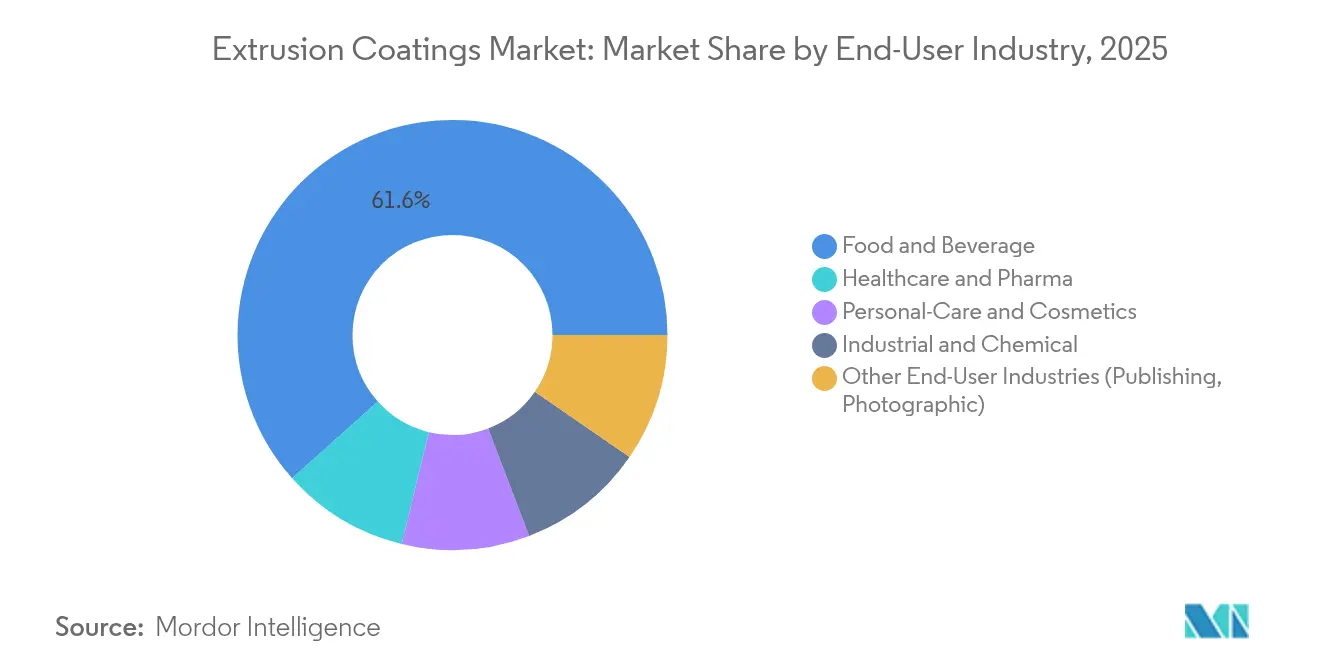

- By end-user industry, food and beverage commanded 61.60% of the extrusion coatings market size in 2025; healthcare and pharmaceuticals will grow the fastest at 7.31% CAGR to 2031.

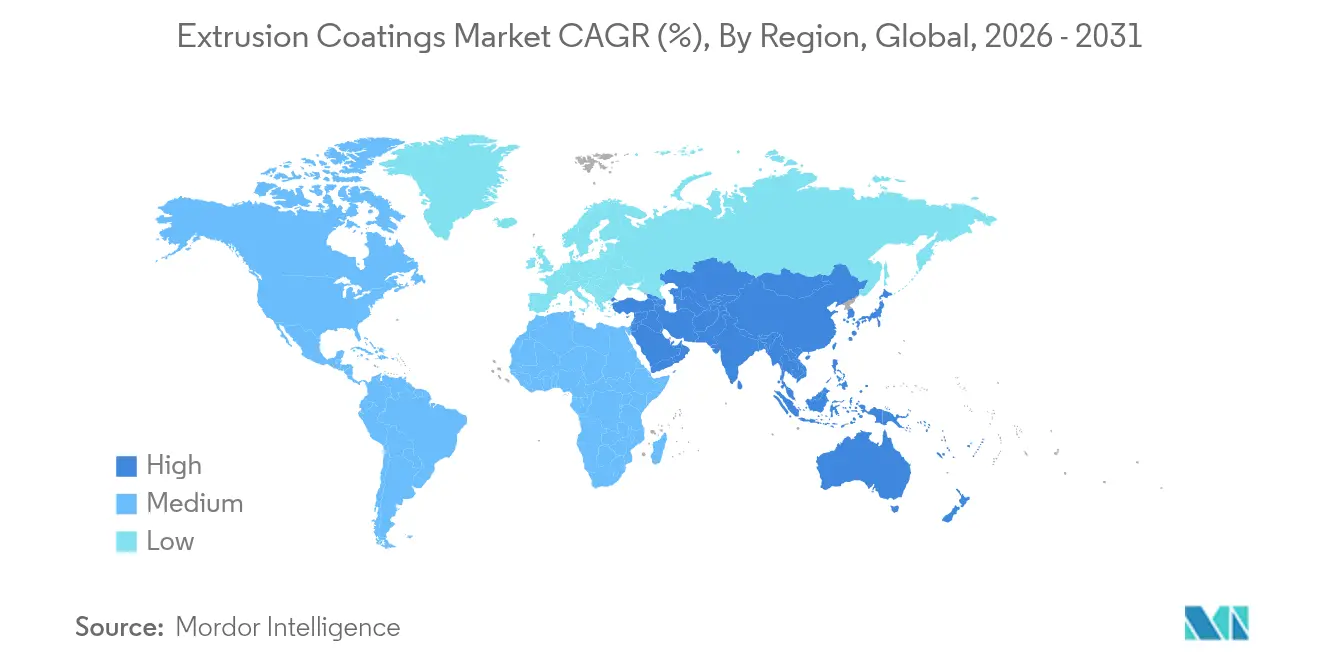

- By geography, Asia-Pacific dominated with 56.70% share of the extrusion coatings market size in 2025 and is projected to grow at 6.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Extrusion Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for liquid & flexible food packaging | +1.2% | Global, with APAC core leadership | Medium term (2-4 years) |

| Surge in e-commerce protective packaging volumes | +0.9% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Expansion of sterile medical & pharma packaging | +0.8% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Recyclable mono-material structures adoption | +0.7% | EU regulatory push, global adoption | Medium term (2-4 years) |

| Increasing usage in construction applications | +0.6% | APAC core, MEA emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Liquid & Flexible Food Packaging

Liquid food cartons and lightweight pouches capture 48.95% of the extrusion coatings market in 2024, a share reinforced by limited cold-chain infrastructure in emerging economies and brand owner preference for shelf-stable formats. New biomass-derived LDPE and EVA grades launched in 2024 match incumbent barrier performance yet cut fossil feedstock by 20%[1]Dow-Mitsui Polychemicals, “Launch of Biomass-Derived EVA and LDPE,” mitsui.com. Packaging converters are leveraging these resins to downgauge laminate thickness and reduce logistics weight without sacrificing heat-seal integrity. Combined with plant-based dairy alternatives gaining shelf space, the outlook affirms steady volume gains across Asia and Latin America.

Surge in E-commerce Protective Packaging Volumes

Fulfilment centers require coating layers that withstand automated forming, high-speed sealing and last-mile handling. Metallocene-catalyzed PE delivers the clarity, slip, and puncture resistance needed for this workflow, prompting brand owners to specify films with 30–50% recycled content that still meet ASTM shipping drop tests. Although the sector lacks definitive global volume data, converter order books reveal double-digit growth since 2023, confirming e-commerce as a resilient demand pillar for extrusion coatings market participants.

Expansion of Sterile Medical & Pharma Packaging

Medical pouches, blister-lid foils, and IV-solution overwraps rely on extrusion-coated structures for controlled oxygen and moisture transmission rates. Regulatory reviews of food-contact polymers under 21 CFR 174-178 tighten extractables limits, spurring adoption of high-purity EVA and EBA grades that satisfy both barrier and biocompatibility criteria[2]Food and Drug Administration, “Food-Contact Substance Notifications Update,” fda.gov. Personalized medicine and biologics intensify these requirements, lifting the value share of specialized medical formats within the broader extrusion coatings industry.

Recyclable Mono-material Structures Adoption

EU rules mandating recyclable packaging by 2028 triggered a wave of PE-dominant film designs that maintain less than 5% EVOH while achieving ≤ 0.4 cc/m²-day oxygen permeability. Commercial launches such as Saica Monoflex and Reifenhäuser’s EVOH-lean barrier lines confirm technical feasibility and demonstrate 20% energy savings in mechanical recycling loops. Converters anticipate premium pricing for verified “designed-for-recycling” laminates, reinforcing this driver’s positive CAGR contribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High polyolefin feedstock price volatility | -0.8% | Global, with APAC manufacturing concentration | Short term (≤ 2 years) |

| Increasing carbon-footprint regulations | -0.6% | EU regulatory leadership, global adoption | Medium term (2-4 years) |

| Shift toward water-based barrier alternatives | -0.4% | Developed markets, gradual emerging market adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Polyolefin Feedstock Price Volatility

Average PE contract prices in China swung by more than USD 120/ton between Q1 and Q4 2024, compressing converter margins and triggering procurement shifts toward spot purchases. Integrated producers buffer volatility through internal ethylene supply, yet small and midsized coaters face working-capital stress, occasionally delaying new line investments. While futures contracts and strategic stockpiling offer partial relief, raw-material uncertainty remains a near-term drag on the extrusion coatings market.

Increasing Carbon-Footprint Regulations

Lifecycle-based levies under the EU Packaging and Packaging Waste Regulation expand compliance spend on audits, disclosure, and low-carbon feedstocks. Producers like Braskem have responded with bio-circular PP derived from used cooking oil, reducing cradle-to-gate CO₂-eq by up to 70% versus fossil benchmarks[3]Braskem America, “Bio-Circular Polypropylene Announcement,” braskem.com. However, qualifying new grades across multi-national supply chains lengthens time-to-market and elevates technical service costs, challenging firms with limited R&D budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polyethylene Dominance Meets EVA Innovation

Polyethylene captured 42.12% of the extrusion coatings market share in 2025 and continues to anchor high-volume liquid and flexible packaging. Advancements in metallocene catalysis lift toughness and optics, while chemical-recycling initiatives promise circular feedstock at scale; one commercial line already delivers 30,000 t/y and targets 500,000 t/y by 2026. Ethyl vinyl acetate, expanding at 5.67% CAGR, secures medical and specialty food niches due to superior adhesion and low-temperature flexibility. Blending EVA with LDPE also enables mono-material laminate architectures that fit mechanical recycling streams. Polypropylene, PET, and specialty acrylates fill durability, high-barrier, or high-heat slots but remain secondary volume contributors. Continuous resin innovation underscores why the extrusion coatings market maintains a diversified polymer slate even as circular-economy mandates tighten.

A second wave of growth is evident in engineered blends that lower seal initiation temperature, cut energy use, and meet glycol-based sterilization cycles for biologics. These functional enhancements raise switching costs for converters, cementing polyethylene’s role as the workhorse resin within the broader extrusion coatings industry. By contrast, EVA’s rising volume encourages backward-integration moves among Asia-Pacific suppliers keen to ensure consistent VA content and food-contact compliance.

By Substrate: Paper Dominance Challenged by Film Innovation

Paperboard and cardboard accounted for 52.10% of the extrusion coatings market size in 2025, reflecting their entrenched role in aseptic cartons and take-out foodservice. Specialty biopolymer additives launched in 2025 allow downgauging up to 50% while maintaining grease resistance, helping brand owners align with fibre-recycling goals. Polymer films, growing at 6.34% CAGR, benefit from high line speeds, downgauged thickness, and expanding applications in collation shrink and mailer films. Cast PP variants now match BO-PP clarity and bag-making efficiency yet cost up to 15% less, accelerating their penetration into dry food and personal-care wraps. Metal foils remain indispensable for moisture-critical pharma packs despite recyclability challenges. Specialty fabrics and non-wovens fill chemical-resistant industrial slots, but their adoption is tempered by cost and process complexity.

Technological cross-pollination is notable: solvent-less primer chemistries originally developed for film lines are being re-formulated for paperboard, giving converters a common toolkit across substrate platforms. This convergence emphasizes the strategic value substrate agility provides in an era where the extrusion coatings market must balance barrier performance, recyclability, and cost discipline simultaneously.

By Application: Medical Packaging Disrupts Liquid Leadership

Liquid cartons and pouches preserved their 48.41% hold on the extrusion coatings market size in 2025, buoyed by ambient dairy demand in emerging economies and plant-based beverage launches in the West. However, medical packaging’s 7.52% CAGR through 2031 resets the growth hierarchy. Regulatory scrutiny of extractables and sterilization compatibility fuels rapid adoption of high-purity EVA and EBA coatings that sustain drug efficacy over extended shelf lives. Flexible food wraps, stand-up pouches, and dry-mix bags remain stable contributors, whereas industrial wrapping progressively migrates to PP-based systems for enhanced chemical resistance.

This vibrancy underlines how the extrusion coatings market continuously pivots toward high-value niches when legacy segments saturate. In practice, converters retool lines with modular feedblocks so a morning run of juice-carton stock can switch to breathable medical-pouch laminate by afternoon, limiting downtime and maximizing asset yield.

By End-User Industry: Healthcare Acceleration Challenges Food Dominance

Food & beverage retained 61.60% of the extrusion coatings market share in 2025, thanks to escalating packaged-food penetration, especially in Latin America, where large processors boosted export-oriented capacity by double digits. Yet healthcare & pharmaceuticals will outpace all sectors at 7.31% CAGR, powered by biologics, home-infusion therapies, and sterile barrier mandates. Personal-care and cosmetics stay aligned with premium brand aesthetics, turning to matte-finish PE blends that elevate shelf presence. Chemical and industrial liners seek durability and chemical inertia, favoring PP and HDPE coatings. Publishing and photography rest on small, specialized runs but command margin premiums for unique tactile and optical effects.

Brand owners in every vertical now score suppliers on lifecycle metrics as closely as on cost, pushing converters to document carbon intensity per square meter. That shift embeds environmental performance as a commercial differentiator across the extrusion coatings industry.

Geography Analysis

Asia-Pacific commanded 56.70% of the extrusion coatings market size in 2025 and is poised to compound at 6.08% CAGR through 2031 on the back of large-scale resin expansion and rising disposable incomes. China’s sustained polymer self-sufficiency strategy and India’s USD 87 billion petrochemical build-out furnish abundant raw materials, while rapid urbanization intensifies packaged-food and e-commerce penetration. SABIC’s joint venture ethylene unit in Fujian, breaking ground in 2024, reinforces localized resin supply circa 2027.

North America leverages advanced recycling pilots and stringent FDA packaging norms to sustain technology leadership. Dow’s divestment of non-core adhesive assets in late 2024 frees capital for circular-polymer scale-ups aimed at future demand. Europe maintains policy influence via recycling and carbon targets that compel rapid reformulation but also unleash premium pricing for compliant barrier solutions. Capacity additions in Mexico—such as AkzoNobel’s USD 3.6 million extrusion-coatings line—signal North American realignment to serve regional converters.

South America, the Middle East, and Africa expand from a lower base yet post robust gains. Saudi Arabia’s USD 1.5 trillion infrastructure pipeline lifts demand for corrosion-resistant wraps, while the GCC paints and coatings sector is projected to reach USD 4.5 billion by 2027. These regions offer strategic greenfield opportunities for mid-tier players aiming to diversify beyond saturated Western markets.

Competitive Landscape

The extrusion coatings market remains moderately fragmented. Global majors—Dow, DuPont, SABIC, and LyondellBasell—pair proprietary catalyst platforms with multi-continent plant networks to secure feedstock and customer lock-in. Competitive positioning now hinges on certified recyclability, scope-3 emissions disclosures, and collaboration with machinery OEMs that refine die designs for thinner, more uniform coatings. This triad of capabilities differentiates incumbents and cements the extrusion coatings market’s shift toward sustainability-led innovation cycles.

Extrusion Coatings Industry Leaders

LyondellBasell Industries Holdings BV

SABIC

Dow

Borealis AG

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: UPM Specialty Papers and Eastman introduced an advanced biopolymer-extrusion coated paper packaging concept designed for food applications requiring grease and oxygen barriers. This solution combines Eastman’s biobased and compostable Solus performance additives with BioPBS biopolymer, extrusion-coated onto UPM’s compostable and recyclable barrier base papers.

- June 2024: AkzoNobel announced an investment of USD 3.6 million in its coil and extrusion coatings manufacturing facility in Garcia, Mexico. This initiative aims to enhance production capacity and operational efficiency to better serve customers across North America, including Mexico and the southwestern United States.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the extrusion coatings market as all polymer layers, typically low-density polyethylene, ethylene-vinyl acetate, or polypropylene, applied through a melt-extrusion die directly onto paperboard, polymer films, foil, or other substrates to deliver barrier, heat-seal, or decorative functions for packaging and industrial wraps. This study tracks only virgin, factory-produced coatings sold into end-use converters during 2019-2030.

Scope exclusion: coatings applied by extrusion lamination or coil-coating lines are outside our numbers.

Segmentation Overview

- By Material

- Polyethylene

- Low Density Polyethylene (LDPE)

- High Density Polyethylene (HDPE)

- Other Polyethylenes (LLDPE & m-LLDPE, etc.)

- Ethyl Vinyl Acetate (EVA)

- Ethyl Butyl Acrylate (EBA)

- Polypropylene

- Polyethylene Terephthalate

- Other Materials

- Polyethylene

- By Substrate

- Paperboard and Cardboard

- Polymer Films

- Metal Foils

- Other Substrates (Woven Fabrics and Non-wovens, etc.)

- By Application

- Liquid Packaging

- Flexible Packaging

- Medical Packaging

- Personal-Care and Cosmetics Packaging

- Photographic Film

- Industrial Packaging/Wrapping

- Other Applications (Corrosion Protection, etc.)

- By End-User Industry

- Food and Beverage

- Healthcare and Pharma

- Personal-Care and Cosmetics

- Industrial and Chemical

- Other End-User Industries (Publishing, Photographic)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We interviewed plant engineers at Asian and North American packaging converters, purchasing managers at three resin suppliers, and regional association experts in Europe and Latin America. Their insights on coating-weight drift, downtime cycles, and regulatory timelines enabled us to close data gaps and refine regional penetration assumptions.

Desk Research

Our analysts first mapped demand drivers through open statistics such as UN Comtrade shipment codes for coated paper, Eurostat PRODCOM output of liquid cartons, the U.S. Census Quarterly Plastics report, and ICIS polymer price benchmarks, which helped ground material costs. Industry bodies, such as FoodPack Europe and the Flexible Packaging Association, provided annual converter capacity and resin utilization ratios, while peer-reviewed work in Polymer Engineering & Science clarified layer-thickness norms for barrier packs.

To test company-level signals, we pulled financials from D&B Hoovers and global news flows from Dow Jones Factiva, cross-checking revenue splits of leading resin makers and coating line builders. The sources named are illustrative; many other public and proprietary references were consulted throughout data validation.

Market-Sizing & Forecasting

The core model starts with a top-down build that reconstructs coated-substrate demand from liquid-carton and flexible-packaging production volumes published by national statistics offices, which are then multiplied by average coat-weights confirmed through primary calls. Selective bottom-up checks, converter line counts and sampled average selling price × volume, tune the totals before sign-off. Key variables include LDPE feedstock prices, global beverage-carton output, e-commerce parcel growth, regional food-safety packaging rules, and substitution rates toward mono-material structures; each variable is projected through a multivariate regression that feeds our 2025-2030 forecast. When granular capacity data is missing, we interpolate using historical utilization patterns from similar substrate classes.

Data Validation & Update Cycle

Model outputs pass three rounds of variance checks against trade data, price trends, and converter financials. Any anomaly above a preset threshold triggers re-contacts. Reports refresh yearly; material regulatory shifts or force-majeure events prompt interim updates, and we perform one last audit just before delivery.

Why Mordor's Extrusion Coatings Baseline Earns Trust

Published estimates often diverge because each firm picks its own substrate mix, resin basket, and refresh cadence, which finally produces very different totals.

Key gap drivers for rivals include counting cast-film lamination as extrusion coating, omitting medical and industrial wraps, relying on uniform global average selling prices, or five-year-old baseline data that ignores recent resin inflation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.85 B (2025) | Mordor Intelligence | - |

| USD 5.80 B (2024) | Regional Consultancy A | Excludes polymer-film substrates and adjusts volumes with 2019 coat-weights |

| USD 6.30 B (2024) | Global Consultancy B | Counts only food packaging; liquid carton data sourced from limited company disclosures |

Taken together, the comparison shows that Mordor's disciplined scope selection, annual refresh cycle, and dual validation steps give decision-makers a balanced, transparent baseline that they can trace back to clear variables and repeat with confidence.

Key Questions Answered in the Report

What is the current Extrusion Coatings Market size?

The extrusion coatings market size is USD 7.19 billion in 2026 and is forecast to reach USD 9.19 billion by 2031.

Which material leads the extrusion coatings market?

Polyethylene dominates with 42.12% share in 2025, supported by continual advancements in metallocene catalysis and recycling integration.

Which application is growing fastest?

Medical packaging is the fastest-growing application, registering a 7.52% CAGR thanks to stringent barrier requirements in pharmaceutical supply chains.

Why is Asia-Pacific the largest regional market?

Asia-Pacific holds 56.70% share due to vast polymer production capacity, rapid industrialization, and expanding packaged-food demand across China and India.

Page last updated on: