Gigacasting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

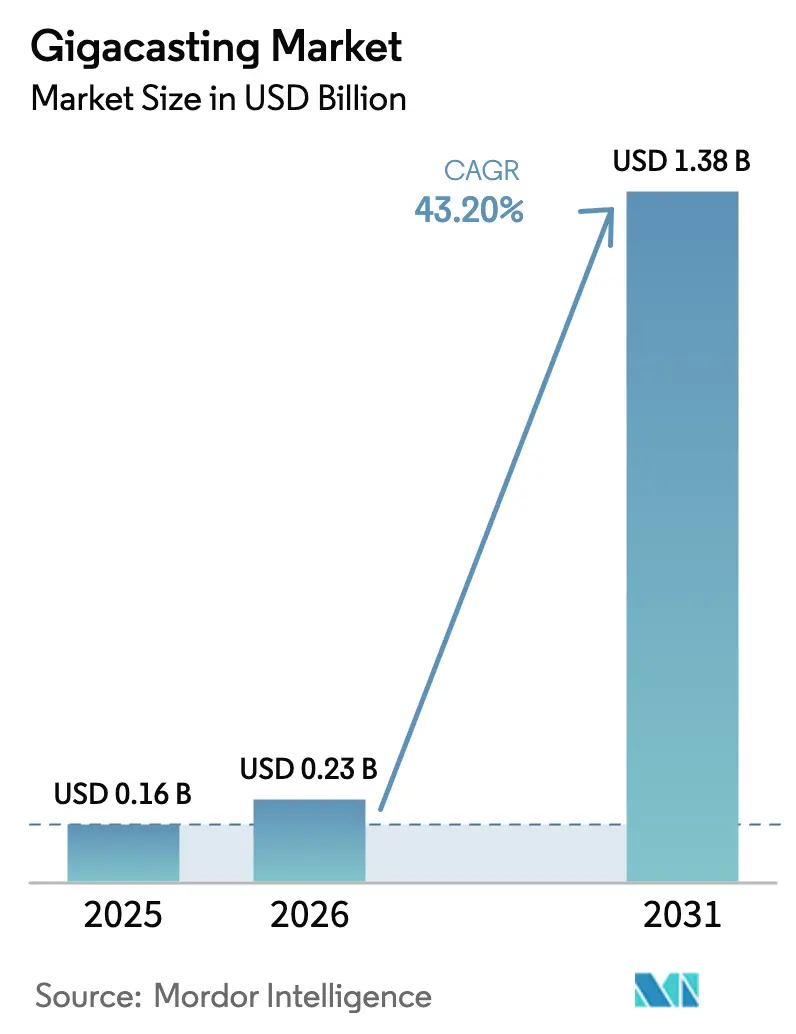

| Market Size (2026) | USD 0.23 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 43.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gigacasting Market Analysis by Mordor Intelligence

gigacasting market size in 2026 is estimated at USD 229.12 million, growing from 2025 value of USD 0.16 billion with 2031 projections showing USD 1.38 billion, growing at 43.20% CAGR over 2026-2031. This rise underscores automakers’ tight focus on large-format high-pressure die casting, which collapses scores of steel stampings into a handful of aluminum components. Tesla’s move from 171 stamped parts to two rear under-body castings in the Model Y cut direct manufacturing expense by up to 40%. Similar cost-down examples, faster takt times, and stricter CO₂ regulations continue to expand the gigacasting market footprint across every major production region. Passenger-car electrification, rising recycled-aluminum premiums, and modular press lines further amplify demand, while the shortage of skilled welders nudges OEMs toward highly automated casting cells.

Key Report Takeaways

- By application, body assemblies led with 58.05% gigacasting market share in 2025, whereas under-body and battery housings are poised to sprint ahead at a 46.20% CAGR to 2031.

- By material, aluminum alloys captured 73.85% of the gigacasting market size in 2025; magnesium alloys headline the growth table at 45.60% CAGR through 2031.

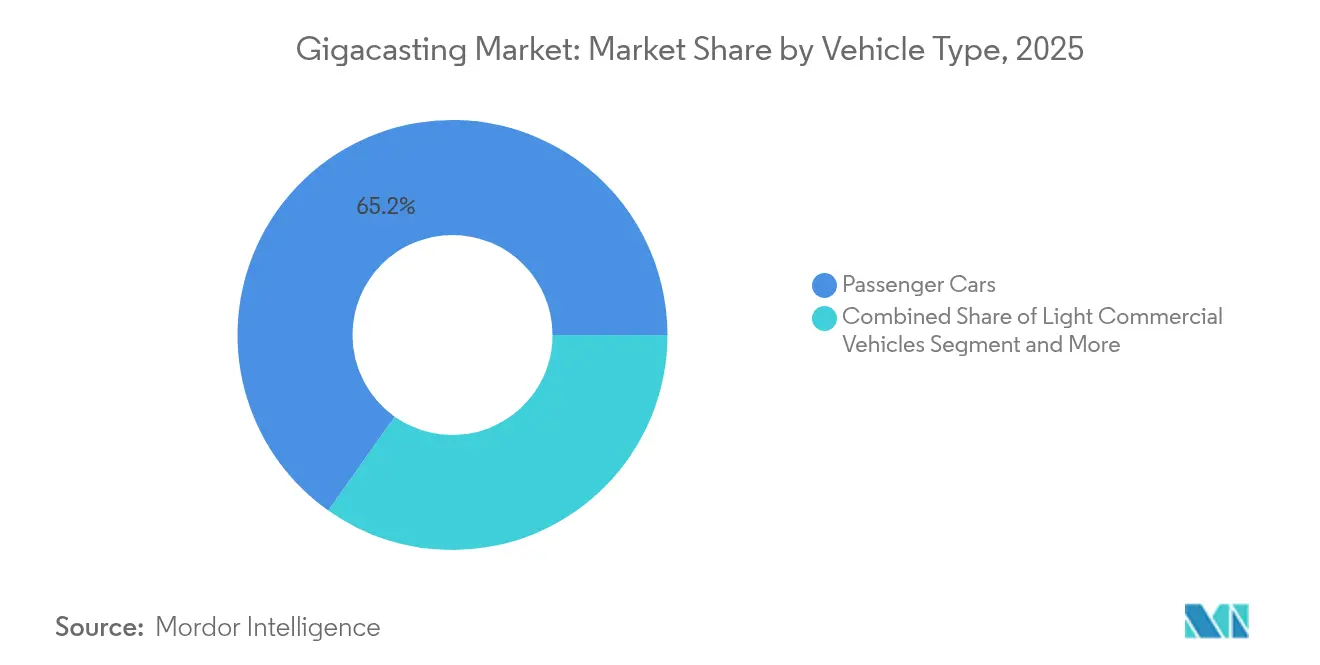

- By vehicle type, passenger cars commanded a 65.20% share of the gigacasting market size in 2025 and will expand at 47.30% CAGR between 2026-2031.

- By press tonnage, the 6,000 to 8,000 t segment retained 44.60% revenue share in 2025, while presses above 10,000 t are forecast to accelerate at 54.30% CAGR.

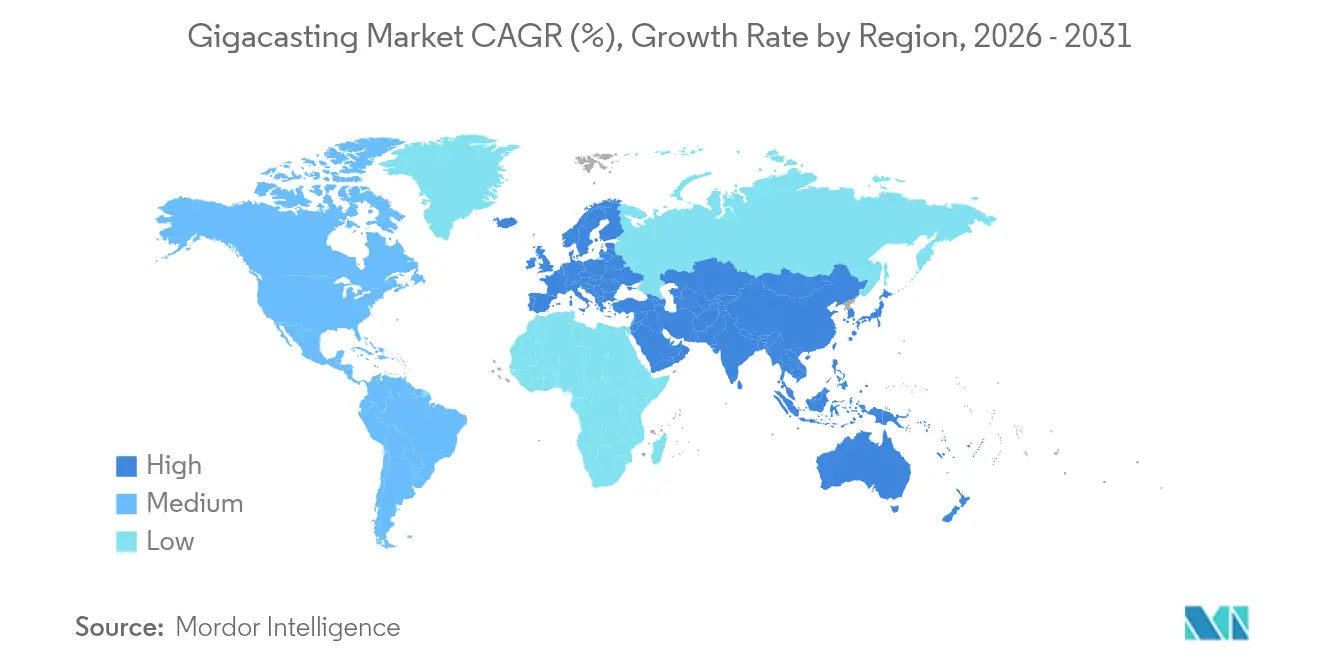

- By geography, Asia-Pacific controlled 48.40% of the gigacasting market in 2025 and is projected to compound at 47.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gigacasting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scale-up of Battery Electric Vehicle (BEV) Volumes | +12.5% | Asia Pacific core, spill-over to North America & Europe | Short term (≤ 2 years) |

| Lightweight Consolidated Vehicle Structures | +8.2% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Per-part Cost & Takt-time Reduction | +7.8% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Skilled-Welder Shortage favoring automation | +4.7% | North America & Europe | Short term (≤ 2 years) |

| Carbon-credit Premiums for Recycled Aluminum | +3.1% | Europe & North America | Long term (≥ 4 years) |

| Modular Giga-press Lines for Variant Flexibility | +2.9% | Global, premium & luxury first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Scale-up of BEV Production Volumes

Global BEV assembly plants are adding giga press cells faster than conventional weld lines. Hyundai earmarked USD 21 billion for North American electrification that includes high-tonnage casting lines at its Metaplant America complex [1]“Investment Plan for North American Electrification,” Hyundai Motor Group, hyundaimotorgroup.com. Ford re-tooled Cologne into an all-electric center using more than 600 robots to shorten body shop flow time. Battery housing demands deep, one-piece structures for crash and thermal performance, and gigacasting offers the shortest path to those geometries. As annual BEV volumes climb toward multi-million-unit levels, economies of scale lift the gigacasting market well beyond niche status.

Demand for Lightweight, Consolidated Vehicle Structures

Gigacasting lets automakers pull mass out of the body-in-white without sacrificing stiffness. Tesla’s rear casting lowered part count by 70 components and saved material, welding, and logistics costs. Aluminum’s high strength-to-weight ratio pairs with design freedom, so a single large casting can integrate crash-energy paths that once required dozens of stampings. Japanese Tier-one Ryobi is shifting capacity toward large aluminum castings, targeting 20% total-manufacturing-cost relief. Weight savings dovetail with stricter fleet-average CO₂ limits and range expectations in battery vehicles. As more models adopt skateboard battery packs, under-body castings become natural enablers for load-path optimization and packaging efficiency.

Per-part Cost & Takt-time Reductions vs. Multi-part Body-in-White

Replacing hundreds of welded steel parts with one casting slashes cycle time per vehicle. Tesla removed 1,600 welds and 300 robots, trimming direct cost by 40% on the Model Y line. A giga-press can drop sixty castings an hour, while Toyota’s trial cell forms large body modules in roughly three minutes. Lower part inventories shrink in-plant logistics, quality-check stations, and supplier tooling—creating a cascading cost advantage. Capital avoidance also enters the equation: fewer framing gates and welding fixtures mean smaller body shops for the same nameplate volume.

Shortage of Skilled Welders Pushing OEMs to Casting Automation

In mature markets, welding talent is aging out faster than new tradespeople enter. Eliminating hundreds of welds with a giga-casting simplifies labor planning and reduces defect risk. Tesla’s switch carved out an entire welding sub-line and lifted dimensional precision at the same time. Japanese supplier Aisin has mirrored the strategy as it prepares next-generation e-powertrain brackets. The automation pushes steadies’ production even during labor crunches and aligns with industry-wide moves toward lights-out manufacturing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upfront CAPEX for ≥ 6,000 t Presses | -6.8% | Global, hardest on smaller OEMs | Short term (≤ 2 years) |

| Energy-Price-Driven Alloy Supply Tightness | -4.1% | Europe & energy-import regions | Short term (≤ 2 years) |

| Collision-Repair Complexity & Insurance Cost | -3.2% | North America & Europe | Medium term (2-4 years) |

| Scrap & Porosity Risk Above 12,000 t | -2.9% | Global, quality-critical segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX for ≥ 6,000 t Presses

A single 9,000 t giga-press carries a price tag in the tens of millions. Volvo’s Slovakian plant ordered twin IDRA units and budgeted EUR 855 million for the surrounding foundry, trim line, and infrastructure [2]“9,000-ton Giga Press for Volvo Cars,” IDRA Group, idragroup.com. Tier-one Nemak spent USD 18 million just to add two 4,500 t machines inside an existing facility—illustrating that even mid-range tonnage means deep pockets. Smaller brands struggle to amortize that spend over modest volumes, slowing widespread adoption and nudging the gigacasting market toward financially robust players.

Energy-price-driven Aluminum-alloy Supply Tightness

Electricity can exceed 60% of the total smelter cost. A study in Energy & Environment pegged aluminum’s energy intensity at up to 65 GJ per ton. High power tariffs pushed several European smelters offline in 2024, creating a 4-million-ton supply gap in the United States that would need five new smelters to close [3]“Closing the U.S. Aluminum Supply Gap,” Aluminum Association, aluminum.org. Tight billet supply hardens price volatility and complicates the feedstock model for high-volume gigacasting cells.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Battery Housings Drive Structural Innovation

Body assemblies held 58.05% of the gigacasting market share in 2025 and remain core to most rollouts, yet battery and under-body castings are expanding at 46.20% CAGR. The gigacasting market size tied to battery housing is forecast to widen sharply as every BEV adopts a floor-mounted pack needing rapid heat dissipation and crash load pathways. Tesla’s rear casting success story quickened the transition, while Handtmann installed Bühler Carat-610 cells to mass-produce pack frames for European EV programs.

Demand also grows for integrated tunnel castings that combine side rail, cross-member, and pack mounts in one pour. Engine and e-drive housings mark a transitional zone; internal-combustion castings taper while new e-motor mounts enter. Transmission castings decline as single-speed drivetrains rise. Niche aerospace and industrial uses surface in R&D pipelines, but automotive applications overwhelmingly steer the near-term gigacasting market.

By Material: Magnesium Alloys Challenge Aluminum Dominance

Aluminum retained 73.85% of 2025 revenue due to its favorable mix of weight, cost, and scrap-loop efficiency. Even so, magnesium’s 45.60% CAGR positions it as the stand-out gainer. Research published by SAE shows high-temperature Mg alloys holding structural integrity at 300 °C, opening doors for motor-inverter mounts. Concurrently, new super-ductile Al-Si-Mg grades meet crash performance while enabling thinner sections in giga-press molds.

Steel suppliers defend their share through advanced castable steels for battery enclosures; ArcelorMittal unveiled prototypes promising comparable crash metrics with easier recycling. Titanium or zinc remain niche options due to cost or density penalties. Whether aluminum keeps its lead will rest on scrap availability, energy prices, and multi-alloy press capabilities.

By Vehicle Type: Passenger Cars Sustain Dual Leadership

Passenger cars delivered 65.20% of 2025 revenue and are tracking a 47.30% CAGR, confirming their role as both volume anchor and growth engine for the gigacasting market. Ford’s BlueOval City will rely on giga-presses for next-generation electric pickups and crossovers. Hyundai’s Metaplant targets 1.2 million units yearly, likewise, structured around large-format die casting.

Light commercial vans join the curve as e-commerce pushes operators toward zero-emission fleets. Medium and heavy trucks inch forward, but battery mass remains a hurdle. Across all segments, lower total part count and tighter assembly real estate favor casting economics, ensuring passenger cars continue to headline adoption.

By Press Tonnage: Large Equipment Drives Future Growth

Presses above 10,000 t will gallop at 54.30% CAGR to 2031, even though 6,000-8,000 t remains the volume sweet spot today with 44.60% share. IDRA pioneered the 9,000-t class used by several OEMs, and Bühler’s Carat series reaches 92,000 kN, touting zero-scrap ambitions. Larger tonnages support one-piece SUV side structures and pick-up bed castings, edging the practical envelope outward.

Yet, cost and plant-floor footprint slow universal uptake, keeping mid-range machines dominant for sedans and compact crossovers. The gigacasting market size for presses between 8,001-10,000 t is expected to expand steadily as global programs migrate from pilot to high-rate production.

Geography Analysis

Asia-Pacific held 48.40% of 2025 revenue and is projected to expand at 47.90% CAGR to 2031, powered by China’s dominance in lithium-ion battery supply and rapidly scaling BEV assembly capacity. Chinese foundries already operate multiple 6,000-8,000 t presses for local OEMs, and Ryobi aims for 20% cost relief by producing large aluminum castings in Hiroshima. Japan and South Korea add momentum through supplier-led investments and Hyundai’s USD 21 billion North American electrification commitment, which still leverages Asian equipment design. India remains at an early stage but offers policy support for EV supply-chain localization, suggesting future upside for regional giga-press installations.

North America follows with a concentrated wave of OEM capex that underpins the gigacasting market. Ford’s USD 2 billion Cologne Electric Vehicle Center overhaul and USD 5.6 billion BlueOval City complex integrate large-tonnage casting cells for next-generation pickups and crossovers. General Motors earmarked USD 4 billion for U.S. plant upgrades to reach 2-million-unit annual output, much of which relies on single-piece aluminum structures. Aluminum billet supply is a constraint, as the United States faces a 4 million t shortfall that keeps Canadian imports critical.

Europe balances strict carbon policy with elevated power prices, shaping a nuanced adoption curve. Volvo’s Kosice site committed EUR 855 million for twin 9,000 t IDRA presses to start production in 2026. Germany’s premium OEM cluster advances digital-twin foundries but must manage electricity-cost volatility. South America contributes limited volumes today, while Gulf energy exporters explore vertically integrated aluminum and casting projects; both regions hinge on foreign direct investment from global automakers seeking diversified footprints.

Competitive Landscape

Competition spans two interlinked layers: giga-press makers and automotive integrators. IDRA Group capitalized on first-mover cachet, shipping 8,000 t units to Tesla and 9,000 t cells to Volvo. Buhler counters with Carat presses offering real-time vacuum control and predictive maintenance dashboards. Haitian debuts cost-aggressive alternatives to court Chinese Tier-one suppliers, intensifying price pressure.

On the OEM side, Tesla remains vertically integrated, owning die shops and alloys to secure supply. Traditional automakers favor strategic alliances: Hyundai pairs with global casters for U.S. output, while Ford contracts specialist Tier-ones for trim and machining. Digital-twin ecosystems add a fresh differentiator—BMW and GM deploy AI to compress launch timelines, potentially shaving quarters off program cycles. White-space exists in commercial vehicles, aerospace ribs, and renewable-energy housings where casting know-how can migrate.

Capital discipline shapes the playing field. Only brands with multi-billion-dollar programs can sign off on > 10,000 t press halls. Meanwhile, equipment suppliers race to embed data services, selling uptime guarantees that anchor long-term revenue beyond original hardware.

Gigacasting Industry Leaders

IDRA Srl (subsidiary of LK Technology)

Buhler AG

Yizumi Holdings

UBE Machinery Corporation

Shibaura Machine Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: UBE Machinery unveiled UH7300 (7,300 t) and UH4500 (4,500 t) die-casting machines for battery-electric structural parts.

- February 2025: Honda confirmed mega-casting integration at its Ohio complex, enabling flexible EV-hybrid-ICE production by late 2025.

- May 2024: Nissan announced that future EV platforms will adopt giga-casting to streamline cost and complexity.

Global Gigacasting Market Report Scope

Gigacasting involves using high pressure to cast intricate parts with advanced technology, typically using lightweight materials like aluminum. These components are used in large aluminum body parts, such as the entire underside of a vehicle.

The gigacasting market is segmented by application and geography. By application, the market is segmented into body assemblies, engine parts, transmission parts, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market sizing and forecast have been done based on the value (USD).

| Body Assemblies |

| Under-body/Battery Housings |

| Engine and e-Drive Parts |

| Transmission and Driveline Parts |

| Others |

| Aluminum Alloys |

| Magnesium Alloys |

| Advanced High-Strength Steel (AHSS) Castings |

| Other Non-ferrous Alloys |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| 6,000 to 8,000 t |

| 8 001 to 10 000 t |

| Above 10,000 t |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Body Assemblies | |

| Under-body/Battery Housings | ||

| Engine and e-Drive Parts | ||

| Transmission and Driveline Parts | ||

| Others | ||

| By Material | Aluminum Alloys | |

| Magnesium Alloys | ||

| Advanced High-Strength Steel (AHSS) Castings | ||

| Other Non-ferrous Alloys | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| By Press Tonnage | 6,000 to 8,000 t | |

| 8 001 to 10 000 t | ||

| Above 10,000 t | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the gigacasting market?

The gigacasting market stands at USD 229.12 million in 2026 and is forecast to reach USD 1.38 billion by 2031.

Which region leads the gigacasting market?

Asia-Pacific holds 48.40% of 2025 revenue and is projected to grow fastest at 47.90% CAGR through 2031.

How do giga-presses reduce manufacturing cost?

A single casting can replace hundreds of welded parts, cutting robots, weld spots, and takt time, which translates into a 40% cost drop for Tesla’s Model Y frame.

Which materials dominate gigacasting?

Aluminum alloys command 73.85% of revenue, while magnesium alloys are the fastest-growing material group at 45.60% CAGR.

Page last updated on: