Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

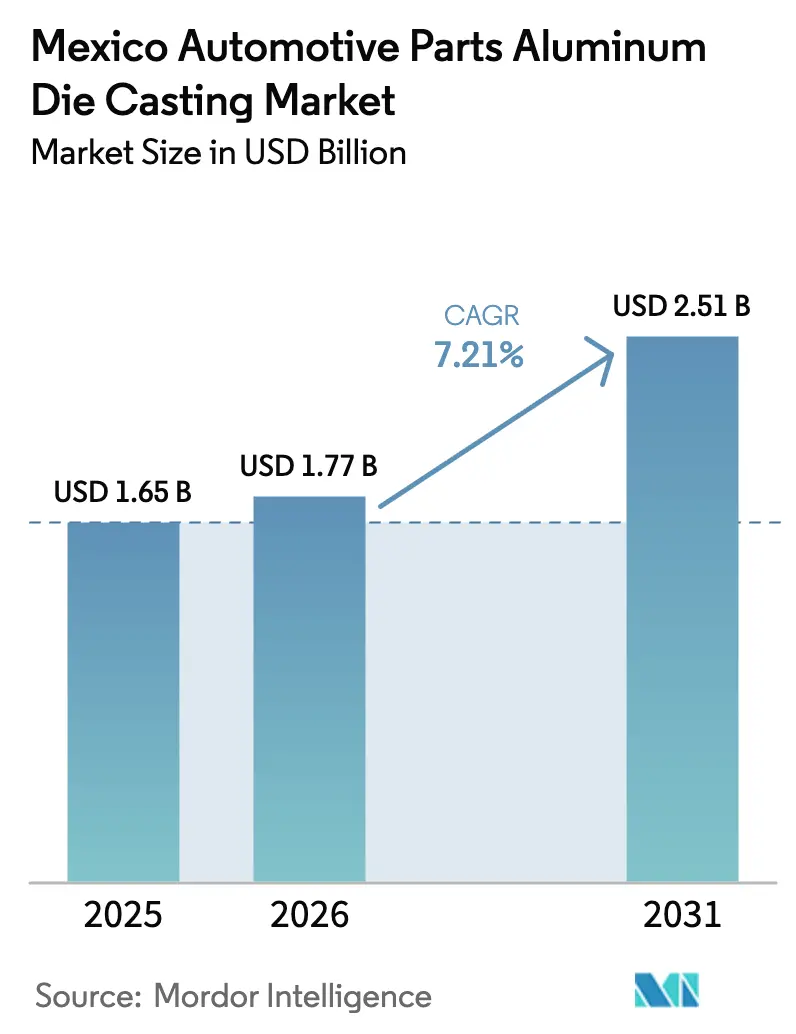

| Base Year Market Size (2025) | USD 1.65 Billion |

| Market Size (2026) | USD 1.77 Billion |

| Market Size (2031) | USD 2.51 Billion |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

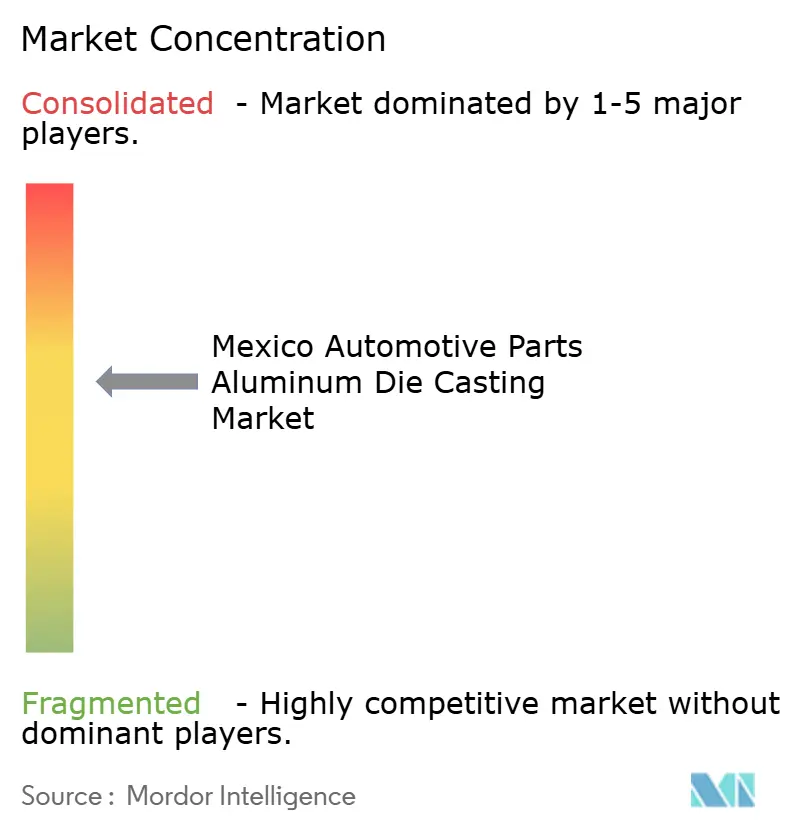

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Automotive Parts Aluminum Die Casting Market Analysis by Mordor Intelligence

The Mexican automotive parts aluminum die-casting market size is projected to expand from USD 1.65 billion in 2025 and USD 1.77 billion in 2026 to USD 2.51 billion by 2031, registering a CAGR of 7.21% between 2026 and 2031. Strong integration with North American electric-vehicle programs, fast-rising giga-casting adoption, and regional-value-content thresholds under USMCA are sustaining demand for high-integrity aluminum castings. Automakers are consolidating up to 70 stamped-steel parts into single structural castings, shaving vehicle mass and assembly time. Tariff structures that penalize non-North American aluminum, together with a USD 2.5 billion wave of 2024 near-shoring investments, are redirecting supply chains toward Mexican foundries. Meanwhile, silver linings in secondary-aluminum remelt and AI-enabled zero-defect lines are widening capability gaps between incumbents and smaller shops. Lingering headwinds include natural-gas–linked aluminum price swings and a 62% shortage of qualified die-casting technicians.

Key Report Takeaways

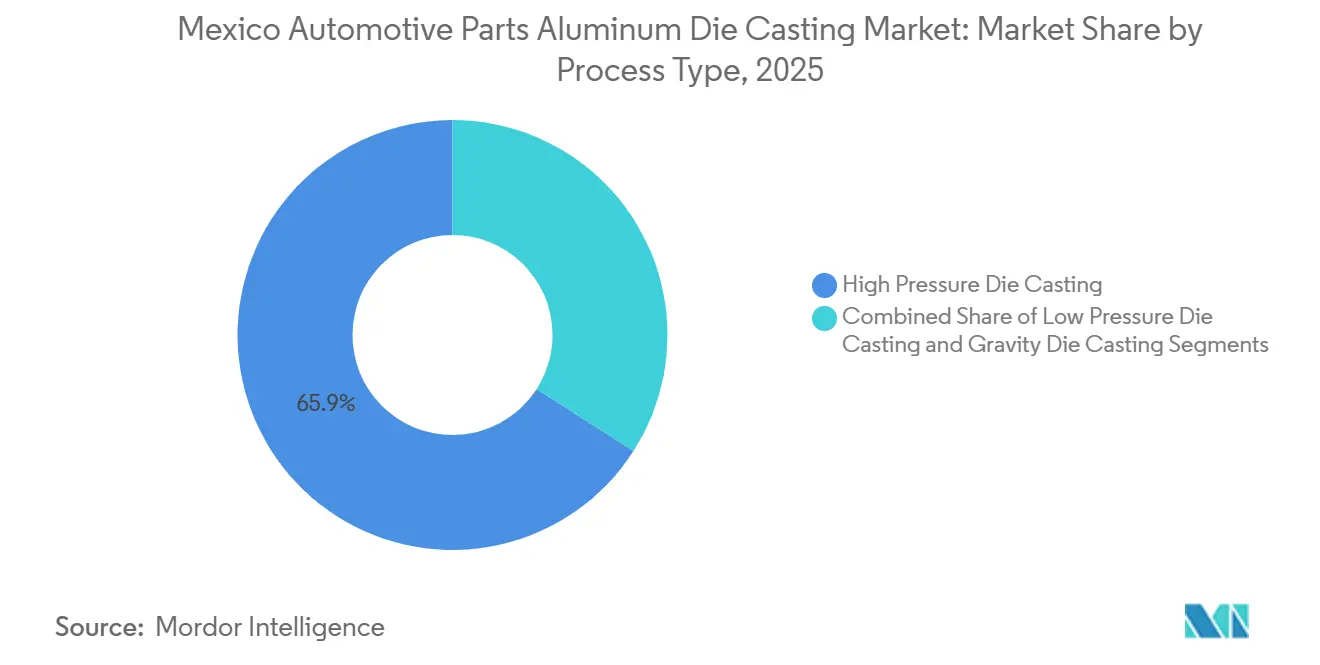

- By process type, high-pressure die casting led with 65.92% of Mexico's automotive parts aluminum die casting market share in 2025; low-pressure die casting is projected to expand at a 9.51% CAGR through 2031.

- By vehicle type, passenger cars commanded 71.91% of the Mexican automotive parts aluminum die-casting market in 2025, while commercial vehicles are advancing at an 8.28% CAGR through 2031.

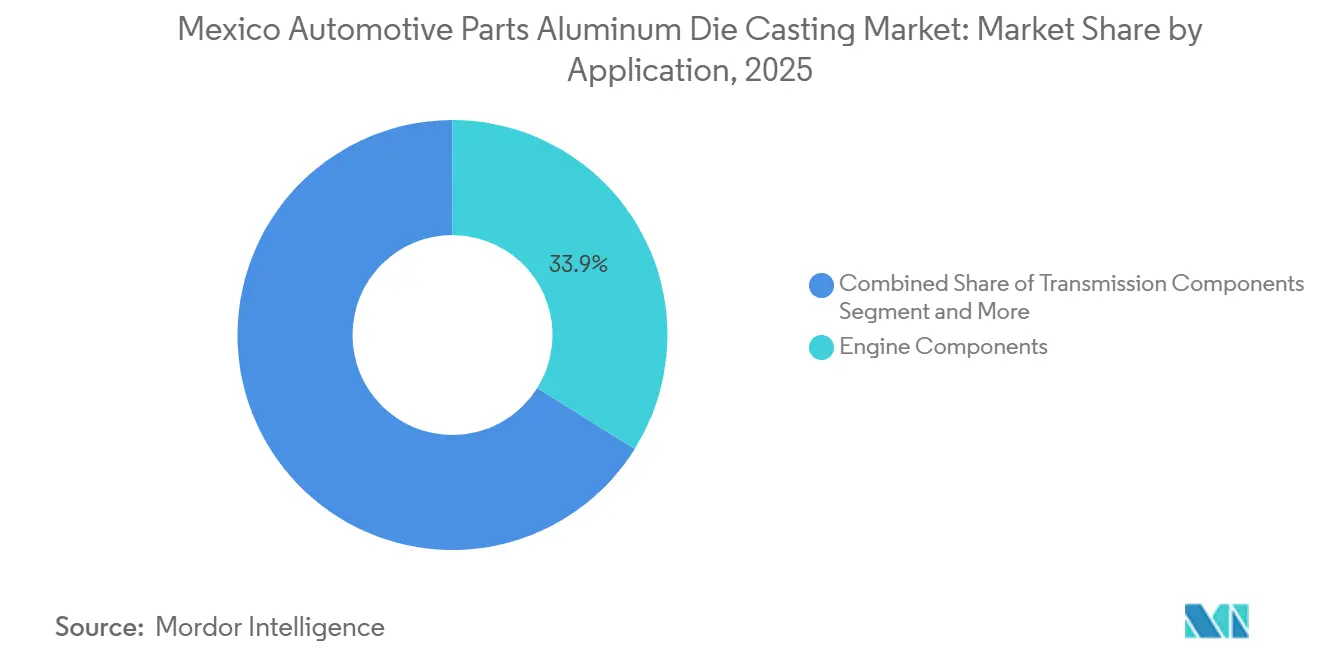

- By application, engine components accounted for a 33.90% share in 2025, and structural components are growing at a 12.45% CAGR through 2031.

- By distribution channel, OEM shipments held 83.85% of 2025 revenue, whereas the aftermarket is rising at a 7.29% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Automotive Parts Aluminum Die Casting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Giga-Casting Demand Surge | +1.5% | Nuevo León, Coahuila, Guanajuato | Medium term (2-4 years) |

| OEM Lightweighting Mandates | +1.8% | Guanajuato, San Luis Potosí, Nuevo León, Querétaro | Long term (≥ 4 years) |

| USMCA Aluminum Sourcing Rule | +1.2% | Coahuila, Nuevo León, Chihuahua, Estado de México | Short term (≤ 2 years) |

| Near-Shoring of Tier-1 Supply Chains | +1.0% | Nuevo León, Querétaro, Aguascalientes, Coahuila | Medium term (2-4 years) |

| Zero-Defect Casting Lines | +0.6% | Guanajuato, Nuevo León, San Luis Potosí | Medium term (2-4 years) |

| Remelt and Scrap Valorization | +0.5% | Nuevo León, Coahuila, Durango | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Related Giga-Casting Demand Surge

Tesla’s Monterrey Gigafactory and Rivian’s forthcoming R2 platform are accelerating a switch to single-piece structural castings that replace dozens of welded parts, cut vehicle mass by double-digit kilograms, and compress assembly time[1]"R2: Built to Overdeliver Manufacturing for the highest performance, capability and quality", Rivian, stories.rivian.com. Nuevo León and Coahuila host the majority of new giga-press installations, giving local foundries sub-48-hour delivery windows into United States plants. Chinese tier-ones such as Tuopu Group view Mexico as a tariff-safe bridgehead, bringing giga-press know-how that intensifies competition. Structural castings, rear underbodies, battery trays, and front subframes dominate volumes, yet the USD 8-12 million price tag for a vacuum-assisted cell restricts participation to capital-rich incumbents. Early adopters are setting tolerance benchmarks below ±0.3 mm, raising the bar for late-moving peers.

HPDC Shift Driven by OEM Lightweighting Mandates

Original equipment manufacturers are chasing fleet-wide weight reductions to extend electric-vehicle range, pushing suppliers toward high-pressure die casting (HPDC) for thin-wall components. HPDC delivers near-net shapes in under 90 seconds, eliminating secondary machining and holding tight tolerances that stamped steel cannot match. Nemak’s latest Monterrey line pairs vacuum assist with closed-loop remelt to meet stringent porosity targets, setting a performance benchmark for the cluster. Guanajuato and San Luis Potosí are following suit, with new HPDC cells sized for suspension knuckles, control arms, and motor mounts. Because the process supports both legacy power-train parts and emerging EV structures, HPDC remains the backbone technology even as newer routes gain momentum.

USMCA 70% North American Aluminum Rule

The trade pact’s 70% regional-content threshold went into effect in 2025, forcing Mexican foundries to source billet or scrap from North American smelters or recyclers[2]By David Bartle, "US aluminium industry urges USMCA tariff harmonization", Fastmarkets, fastmarkets.com. Plants with in-house remelt furnaces now enjoy a cost and compliance edge, while import-dependent shops face duty exposure. Coahuila and Nuevo León are attracting secondary-aluminum projects that close the loop between automakers’ stamping lines and die-casting furnaces. This self-contained ecosystem reduces lead times and carbon footprints, both of which are prized by global OEMs. The rule simultaneously shields the sector from low-priced Asian billet, reinforcing pricing power for compliant suppliers.

Near-Shoring of Tier-1 Supply Chains

Geopolitical risk and freight delays have pushed tier-one suppliers to relocate casting programs from Asia to Mexico, channeling fresh investments. Magna’s Ramos Arizpe campus and Xusheng’s new Coahuila complex illustrate how global majors are hedging tariff exposure while staying within trucking distance of United States assembly plants. Nuevo León, Querétaro, and Aguascalientes offer bilingual engineering talent and North-South logistics corridors that beat ocean lead times by months. However, the inflow strains the local labor pool and grid capacity, making infrastructure roll-outs a parallel priority. For suppliers able to execute, near-shoring locks in customer intimacy and just-in-time reliability that Asian sites struggle to match.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminum Price Volatility | -0.8% | Nuevo León, Coahuila, Estado de México | Short term (≤ 2 years) |

| Skilled-Labor Scarcity | -0.7% | Guanajuato, Querétaro, San Luis Potosí, Nuevo León | Medium term (2-4 years) |

| Capital-Intensive HPDC Equipment | -0.6% | Nuevo León, Coahuila, Guanajuato | Long term (≥ 4 years) |

| "Smelt-and-Cast" Rule Tightening | -0.4% | Coahuila, Chihuahua, Nuevo León | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aluminum Price Volatility Linked to Energy Costs

Aluminum spot prices in Mexico move with natural-gas futures, compressing margins when gas prices spike and fixed-price casting contracts are in place. Although recent tariff relaxations eased raw-metal costs, the nation still relies on imported primary aluminum, leaving plants vulnerable to Gulf Coast supply disruptions. Electricity-market reforms that favor state utilities have lifted industrial power tariffs, adding a second cost lever outside foundries’ control. Without long-term hedging or closed-loop scrap programs, smaller shops risk cash-flow squeezes that delay equipment upgrades. In response, larger players bundle energy-efficiency projects with renewable power purchase agreements to stabilize input costs over multiyear horizons.

Skilled-Labor Scarcity for Die-Casting 4.0

A shortage of engineers and mechatronics technicians of over 50% is slowing the adoption of AI-enabled inspection and digital twin systems across Mexican foundries. Universities and cluster groups have launched targeted training centers, yet graduate throughput trails the surge in automation projects. Wage inflation and high turnover complicate compliance with IATF 16949 training records, exposing smaller plants to audit risk. Some tier-one suppliers now backfill roles with offshore specialists, raising payroll complexity and cultural barriers. Until the talent gap narrows, human-capital constraints will cap output growth even where equipment investments are fully funded.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Type: HPDC Scale and LPDC Momentum

High-pressure die casting commanded 65.92% of Mexico's automotive parts aluminum die casting market share in 2025, cementing its status as the process of choice for engine, transmission, and chassis programs. Its short cycle times and ability to hit near-net shapes make it indispensable to volume-oriented original equipment manufacturers. Foundries rely on their mature tooling ecosystem, broad alloy compatibility, and well-documented quality controls to keep reject rates low. Because the process integrates easily with on-site machining and assembly, suppliers can meet just-in-time delivery commitments to assembly plants on both sides of the border. The dominance of HPDC also reflects long-standing relationships between automakers and local toolmakers that continuously refine die-life and surface-finish standards.

Low-pressure die casting is the fastest-growing process segment, expanding at a 9.51% CAGR through 2031, driven by demand for vacuum-tight integrity in battery enclosures and motor housings. It offers slower fill rates that minimize turbulence, giving engineers confidence in leak-free castings for electric-vehicle thermal systems. Plants that add LPDC cells can pivot between structural and electrical parts without overhauling existing HPDC lines, earning preferred-supplier status on new platforms. Equipment makers now bundle LPDC furnaces with automated ladling and real-time X-ray inspection to shorten learning curves for first-time adopters. As electrification deepens, foundries capable of running both processes side by side will hold the broadest catalog of casting solutions.

By Vehicle Type: Passenger Dominance and Commercial Upswing

Passenger vehicles held 71.91% of Mexico's aluminum die-casting market share in 2025, reflecting the country’s role as a global export hub for compact cars and sport-utility models. Consistent model calendars give foundries predictable call-offs for engine blocks, gear housings, and suspension pieces. Automakers favor geographically close suppliers that can synchronize deliveries with tightly sequenced final-assembly lines. As light-vehicle programs adopt more aluminum for crashworthiness and fuel-economy standards, passenger-car demand keeps HPDC machines running near capacity. The enduring scale of this segment also anchors the tooling and maintenance ecosystem that supports smaller specialty runs.

Commercial vehicles represent the fastest-growing end-use, advancing at an 8.28% CAGR to 2031 as fleets electrify long-haul tractors and delivery vans. Electric drivetrains add significant battery mass, prompting chassis engineers to swap steel rails and cross-members for lighter aluminum castings. Suppliers that certify large-section parts win contracts with truck makers seeking to preserve payload and extend range. Tier-one integrators are already aligning press tonnage and alloy recipes to serve both Class-8 platforms and light-commercial vans from shared campuses. Over the forecast window, a rising stream of commercial orders will diversify revenue for foundries previously tied almost entirely to passenger programs.

By Application: Engine Breadth and Structural Surge

Engine components accounted for 33.90% of Mexico's automotive parts aluminum die-casting market share in 2025, underscoring the continued importance of internal-combustion powertrains in export programs. Multiple castings per engine, blocks, heads, oil pans, and anchor steels are in demand even as hybridization spreads. Decades of process know-how make engine parts a defensible revenue pillar for foundries, with established machining centers and metallurgical labs ensuring consistent tolerances. Close collaboration with powertrain design teams helps suppliers stay ahead of alloy changes and thermal stresses introduced by turbocharging and downsizing. This entrenched workflow keeps engine castings in the product mix for the foreseeable future.

Structural components are the fastest-growing application, rising at a 12.45% CAGR as giga-casting condenses welded body assemblies into single aluminum pieces. These large, complex castings cut workstation counts and streamline crash-energy pathways, making them central to new electric-vehicle platforms. Foundries investing in 6,000-ton and above payload presses and vacuum-assist technology gain preferred status on underbody and battery-tray contracts. Mastery of die temperature control and alloy flow extends tool life, lowering total cost of ownership for both supplier and automaker. Over time, structural parts are poised to outpace drivetrain castings as the signature growth engine of the sector.

By Distribution Channel: OEM Primacy and Aftermarket Lift

Original equipment shipments dominated Mexico's automotive parts aluminum die casting market, accounting for a significant 83.85% of the total revenue in 2025. This stronghold can be attributed to the stringent quality, logistics, and traceability demands set by automakers. Furthermore, integrated campuses that merge casting, machining, and subassembly processes have successfully locked in multi-year contracts, ensuring consistent line rates. Close proximity to assembly plants reduces inventory buffers, making on-time performance a critical differentiator. In-house metallurgical labs and IATF 16949 certification further solidify supplier positions in OEM rosters. This channel also funds capital-intensive press upgrades, ensuring continuous technology refresh.

The aftermarket channel is the fastest-growing route, advancing at a 7.29% CAGR as Mexico’s aging vehicle parc and the United States tariff dynamics redirect sourcing away from Asia. Independent foundries leverage flexible tooling to deliver small-batch replacement housings, brackets, and cooling plates on compressed lead times. E-commerce platforms and regional distributors amplify reach, offering cast parts to repair shops and fleet managers that demand quick turnaround. Because aftermarket buyers focus on availability and fit rather than brand labels, cost-optimized casting lines can win share without replicating full OEM audit protocols. Diversifying into this channel cushions suppliers against assembly-plant downtime and model-year shifts.

Geography Analysis

Nuevo León houses the country’s most mature die-casting cluster, anchored by Nemak’s flagship complex and multiple tier-one suppliers serving United States plants across the Texas border. Proximity to export highways shortens lead times, while a dense vendor network supplies tooling, heat-treatment, and surface-finish services within a single metro area. Government incentives and technical universities further reinforce the ecosystem, attracting continuous equipment upgrades and pilot lines for next-gen alloys. As a result, Nuevo León sets quality and automation benchmarks that ripple through national supply chains.

San Luis Potosí is emerging as the fastest-growing region, propelled by BMW’s decision to localize electric-vehicle assembly and by supplier investments in AI-enabled casting cells. The state’s automotive cluster has partnered with universities to offer mold maintenance and PLC programming curricula, narrowing the talent gap that constrains other regions. New industrial parks provide ready utility hookups for large presses, reducing commissioning lead times. With both greenfield sites and brownfield expansions on the docket, San Luis Potosí is positioned to absorb demand that outpaces capacity in longer-established hubs.

The interplay between these two regions shapes Mexico’s competitive map. Nuevo León offers depth, scale, and export logistics that pull global OEM programs into its orbit, while San Luis Potosí supplies the headroom for new entrants and advanced processes that older plants may struggle to retrofit. Suppliers operating in both locations can hedge against local disruptions, spreading labor and infrastructure risk. Over the forecast window, capacity additions in San Luis Potosí will relieve pressure on Nuevo León, yet the latter’s first-mover advantages in giga-casting and remelt integration should preserve its leadership position.

Competitive Landscape

Five companies, Nemak, Bocar Group, Magna International, Linamar Corporation, and GF Casting Solutions, anchor the field, yet none lead, yielding a moderate market concentration. Vertically integrated leaders recycle internal scrap through closed-loop furnaces, shielding margins from spot-aluminum swings and meeting USMCA sourcing thresholds. AI-equipped vision systems now feed proprietary process datasets that refine die coatings and shot curves, erecting knowledge barriers for smaller rivals.

Strategic divides hinge on press tonnage. Plants capable of ≥ 6,000-t giga-casting lock in structural contracts for rear underbodies and battery trays, while legacy 1,200-t cells risk relegation to low-margin engine and transmission work. Battery-thermal-management housings, aftermarket replacements, and rheocasting for semi-solid structural parts present openings for agile challengers. Chinese entrants, Xusheng and Minglida Precision Technology, offer turnkey giga-press installations at 20-30% lower capex, but their relative lack of IATF 16949 pedigrees constrains penetration into safety-critical programs.

Mexico faces a persistent talent shortage, which inadvertently solidifies the position of established players. For instance, Nemak and Bocar Group have set up in-house academies in collaboration with tech universities. Meanwhile, smaller independent firms grapple with staffing challenges, particularly in finding PLC programmers and digital-twin analysts. As automation becomes more prevalent, these challenges in both capital and human resources are likely to solidify a winner-takes-most scenario extending through 2031.

Mexico Automotive Parts Aluminum Die Casting Industry Leaders

-

Nemak

-

Bocar Group

-

Magna International

-

Linamar Corporation

-

GF Casting Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mercedes-Benz unveiled its new S-Class model, simultaneously debuting the TURBUDRUCK die-casting technology for mass-producing aluminum alloy wheels.

- April 2025: FEV, a key player in automotive and industrial equipment, teamed up with 18 global partners from the automotive and metal sectors. Together, they embarked on the MeGiCast consortium project, exploring the promise of giga casting for streamlined vehicle body production.

Mexico Automotive Parts Aluminum Die Casting Market Report Scope

The Mexico automotive parts aluminum die casting market report covers the growing demand and adoption of aluminum die castings in the country’s Automotive Sector, Technological developments, Latest Product Developments, and market shares of players operating in the market.

The Mexican Automotive Parts Aluminum Die Casting market is segmented by process type, vehicle type, application, and distribution channel. By Process Type, the market is segmented into High-Pressure Die Casting, Low-Pressure Die Casting, and Gravity Die Casting. By Vehicle Type, the market is segmented into Passenger Vehicles and Commercial Vehicles. By Application, the market is segmented into Engine Components, Transmission Components, Structural Components, Drivetrain Components, Body Assemblies, and Others. By Distribution Channel, the market is segmented into OEM and Aftermarket. Market forecasts are provided in terms of Value (USD) and Volume (Units).

By Process Type

| High Pressure Die Casting |

| Low Pressure Die Casting |

| Gravity Die Casting |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

By Application

| Engine Components |

| Transmission Components |

| Structural Components |

| Drivetrain Components |

| Body Assemblies |

| Others |

By Distribution Channel

| OEM |

| Aftermarket |

| By Process Type | High Pressure Die Casting |

| Low Pressure Die Casting | |

| Gravity Die Casting | |

| By Vehicle Type | Passenger Vehicles |

| Commercial Vehicles | |

| By Application | Engine Components |

| Transmission Components | |

| Structural Components | |

| Drivetrain Components | |

| Body Assemblies | |

| Others | |

| By Distribution Channel | OEM |

| Aftermarket |

Key Questions Answered in the Report

What drives the recent surge in aluminum giga-casting projects in Mexico?

Automakers are consolidating up to 70 stamped-steel parts into single aluminum castings, cutting mass and assembly time while satisfying USMCA regional-value rules.

What is the growth outlook for low-pressure die casting?

Low-pressure cells serving battery enclosures and motor housings are advancing at a 9.51% CAGR through 2031 as electric-vehicle architectures demand lower porosity levels.

Why is skilled labor considered a restraint for the sector?

An over 50% shortage of engineers and PLC technicians slows adoption of AI-enabled production lines and raises wage pressures, limiting smaller shops’ capacity expansion.

Which segments are gaining fastest in the aftermarket channel?

Replacement demand is strongest for transmission housings, suspension brackets, and EV thermal-management castings as Mexico’s vehicle fleet averages 14 years of age.

Page last updated on: