Gravity Die Casting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 27.13 Billion |

| Market Size (2031) | USD 32.66 Billion |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gravity Die Casting Market Analysis by Mordor Intelligence

gravity die casting market size in 2026 is estimated at USD 27.13 billion, growing from 2025 value of USD 26.14 billion with 2031 projections showing USD 32.66 billion, growing at 3.79% CAGR over 2026-2031. The demand for lightweight vehicle architectures, the broader use of high-strength aluminum and magnesium alloys, and the adoption of tilt-pour automation systems are the primary factors for target market growth. Advanced tilt-pour units, driven by technology, are significantly shortening production cycles. This boost in productivity is helping to maintain cost efficiency, even as energy and alloy prices continue to fluctuate. At the same time, additive-manufactured cores enable foundries to cast intricate internal geometries, shifting the gravity die casting market toward high-value, precision parts for electric drivetrains and aerospace turbines. Competition comes from high-pressure die casting in large-volume parts, yet gravity casting retains an edge where dimensional stability, pressure tightness, and mechanical strength command price premiums. Operators aligning with best available technique standards gain an edge as the European Union's stringent regulations on VOC emissions hasten the shift to water-based release agents and cleaner melting technologies.

Key Report Takeaways

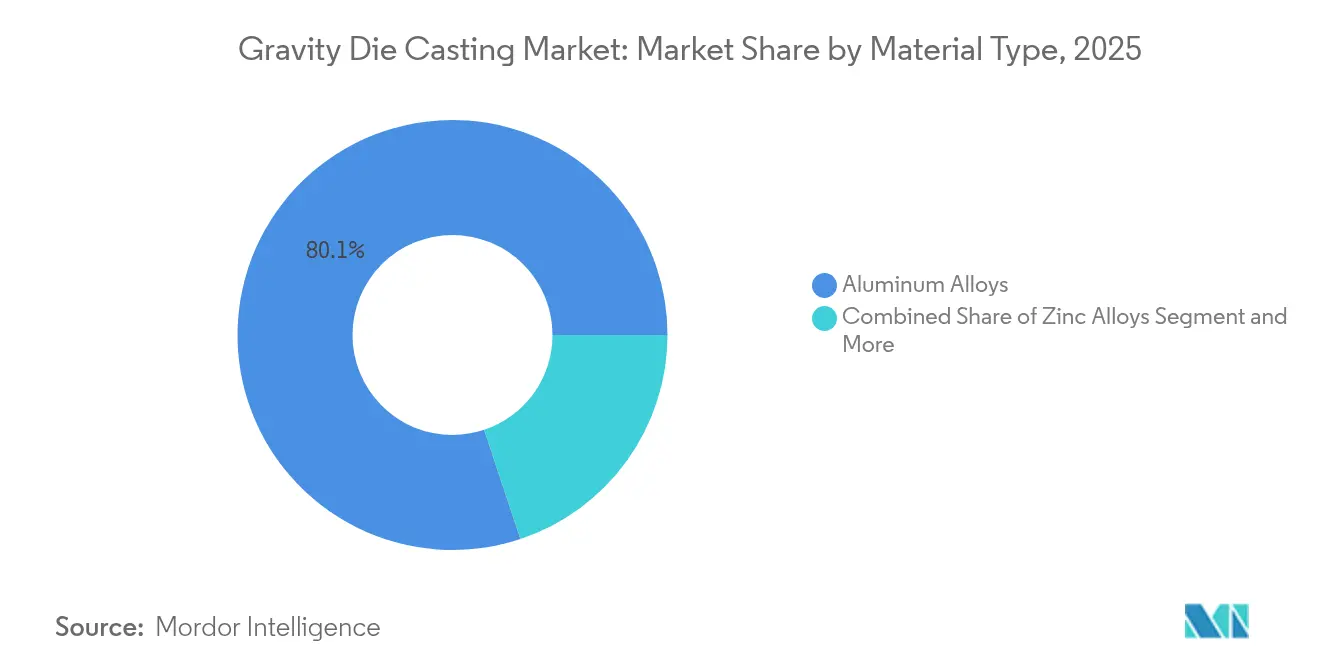

- By material type, aluminum alloys led the gravity die casting market with 80.12% of the market share in 2025, while magnesium alloys are forecast to expand at a 4.68% CAGR through 2031.

- By application, automotive components contributed a 62.55% share of the gravity die casting market size in 2025, whereas aerospace parts are expected to advance at a 4.61% CAGR through 2031.

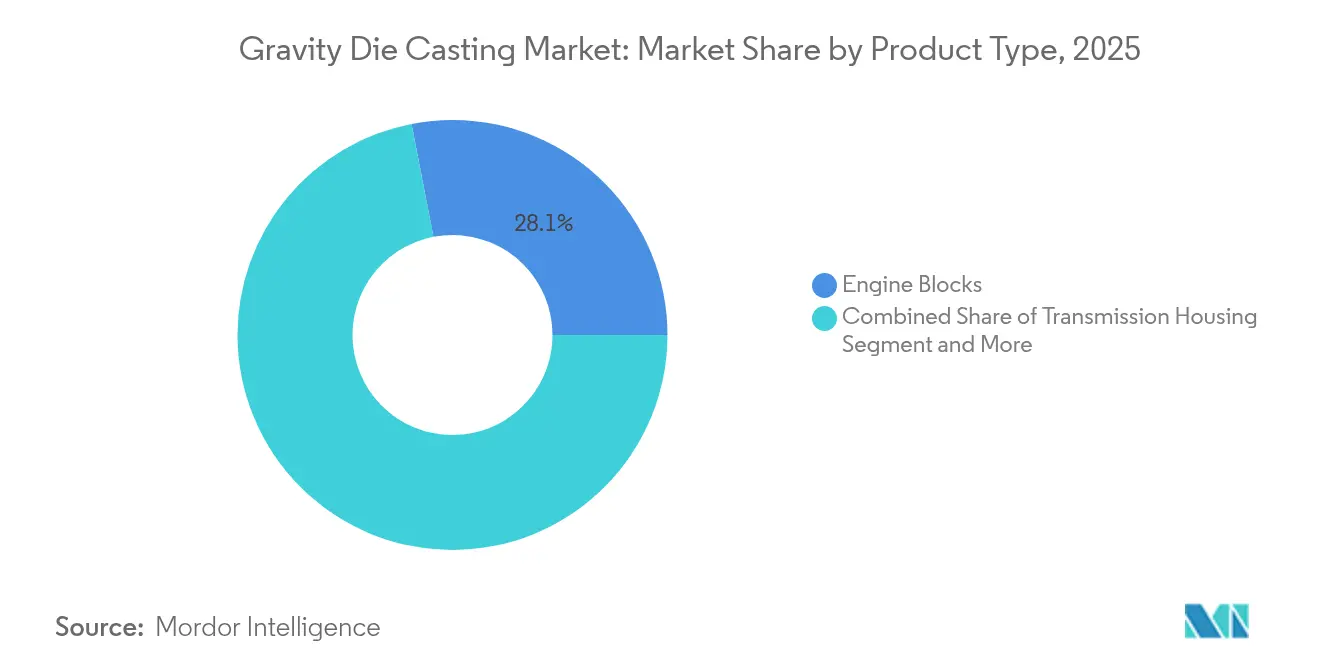

- By product type, engine blocks accounted for 28.05% of the gravity die casting market share in 2025, and structural components are projected to grow at a 4.97% CAGR through 2031.

- By process type, standard gravity die casting held a 73.84% share of the gravity die casting market size in 2025; tilt-pour variants are expected to exhibit the highest forecast CAGR of 5.06% from 2026 to 2031.

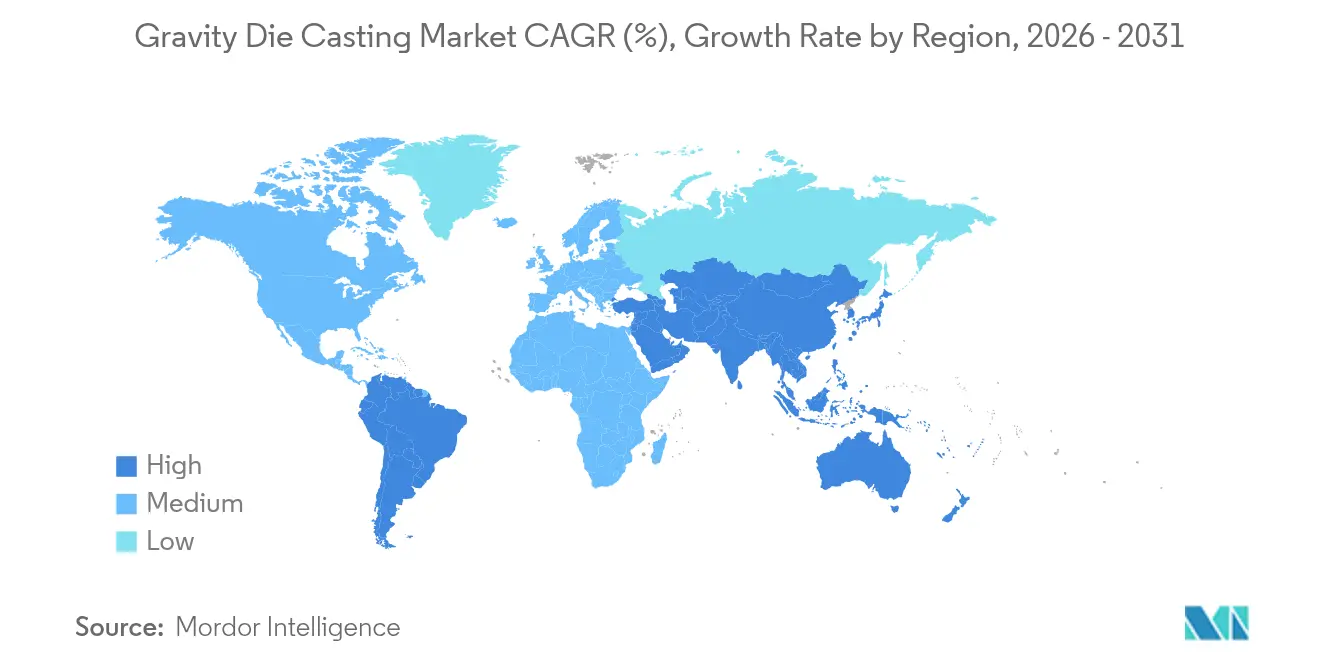

- By geography, the Asia-Pacific region held a 46.78% market share in gravity die casting in 2025, whereas South America is expected to exhibit the fastest regional CAGR of 4.78% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gravity Die Casting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact of CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-Strength Alloy Adoption | +1.2% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Tilt-Pour Automation Gains | +0.9% | Global, early adoption in Asia-Pacific | Short term (≤ 2 years) |

| EV Lightweighting Push | +0.8% | Global, Asia-Pacific and North America | Medium term (2-4 years) |

| Fuel-Efficiency Mandates | +0.6% | EU and North America | Medium term (2-4 years) |

| Low-VOC Compliance Demand | +0.4% | European Union | Long term (≥ 4 years) |

| AM Complex Core Designs | +0.3% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption of High-Strength Gravity-Cast Alloys

Advanced A356 and A380 formulations enhance fluidity while maintaining mechanical integrity, allowing designers to replace cast parts with forgings in chassis brackets and steering housings. Nanoparticle-reinforced AA7075 achieves near-wrought tensile properties and mass savings in thin-wall turbine wheels, illustrating how alloy innovations enable complex parts to remain within the gravity die casting market[1]Guan-Cheng Chen et al., “Nanotechnology Enabled Casting of Aluminum Alloy 7075 Turbines,” nature.com. By incorporating rare earth elements, developers of magnesium alloys have addressed concerns related to galvanic corrosion and flammability. This advancement paves the way for magnesium casting in aerospace structures and electric vehicle gearbox covers. Safran's patents on advanced super-alloy blade blanks underscore the growing dominance of gravity casting over investment casting in medium-temperature turbine stages. As more alloys become available for higher-temperature operations, the applications for gravity casting are expanding.

Automation and Tilt-Pour Productivity Gains

Servo-controlled tilt-pour cells cut fill turbulence and oxide inclusion, lifting first-pass yield rates and trimming cycle time [2]John Hall, “Principles of Gravity Die Casting (GDC) Using Reverse Tilt,” cmhfoundry.com. Across Europe and the United States, robotics is addressing skilled labor shortages, facilitating continuous unmanned operations, and boosting production flexibility. For instance, KUKA's automated cells are refining workflows by logging pour profiles and relaying them to cloud-based dashboards. Such insights enable predictive maintenance, which activates when thermal patterns shift, ensuring consistent quality and minimizing downtime. Additionally, Chinese manufacturers are enhancing material efficiency and cutting waste by adopting reverse-tilt casting techniques, especially for symmetric gear housings. This approach, which dispenses with extended runner systems, not only optimizes metal use but also streamlines production. Collectively, these innovations are transforming the die casting industry, combining automation, data analytics, and process advancements to enhance efficiency, reduce scrap, and meet the demands of high-mix manufacturing.

Automotive and EV Lightweighting Push

As automakers shift to electric vehicles, lightweight aluminum and magnesium components are increasingly preferred to reduce vehicle weight. Gravity casting is gaining traction for producing critical parts, such as battery enclosures, motor housings, and suspension knuckles, due to its structural integrity and design flexibility. Tesla's integration of major gravity-cast components in its structural battery packs not only simplifies assembly but also boosts stiffness. This move is reshaping industry norms and urging other OEMs to reconsider their manufacturing approaches. Moreover, Honda and other companies are advancing sustainability by using recycled materials and efficient casting methods. As electric powertrains transition to higher-voltage platforms, demand for components that manage thermal loads is increasing. Gravity-cast aluminum, with superior thermal shock resistance, is gaining traction. OEMs in North America and Asia are adopting gravity die casting for parts requiring dimensional stability under thermal cycling, emphasizing its growing role in automotive manufacturing.

Regulatory Fuel-Efficiency Mandates

Tightening fuel economy and emissions regulations in the United States and the EU are driving automakers to adopt weight reduction strategies. Gravity die casting enables significant weight savings and streamlined production, reducing costs and supporting environmental compliance. In China, policies linking internal combustion vehicle compliance to new-energy vehicle production are accelerating the adoption of aluminum casting for components such as exhaust manifolds and control arms, reshaping domestic OEM priorities. Furthermore, upcoming regulations, such as Euro 7, which limits brake and tire particulate emissions, are expected to boost demand for lightweight unsprung components, highlighting the value of gravity-cast aluminum for its strength and reduced mass. Rising compliance costs are pushing automakers to invest in premium casting solutions. Gravity die casting, with its advantages, is becoming a strategic choice for balancing sustainability and performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Pressure Die Casting Substitution in High-Volume Parts | -0.7% | Global, especially automotive hubs | Short term (≤ 2 years) |

| Aluminum/Magnesium Price Volatility | -0.5% | Global, higher in cost-sensitive regions | Medium term (2-4 years) |

| Tilt-Pour Operator Shortage | -0.3% | North America and Europe | Medium term (2-4 years) |

| Giga-Casting Cannibalization Risk | -0.4% | Global, EV production zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HPDC Substitution in High-Volume Parts

High-pressure die casting (HPDC) is increasingly used for producing components such as housings and brackets due to its fast cycle times and cost efficiency. Expanding manufacturing capacity enhances scalability, reduces unit costs, and makes HPDC a competitive alternative to gravity casting. Advancements in high-ductility alloys enable thinner walls that meet crash standards, supporting lightweighting without compromising safety. Global platform sharing among OEMs allows a single mold set to be used across multiple sites without requiring revalidation, streamlining logistics, and speeding up the time-to-market. HPDC’s superior surface finishes often eliminate the need for secondary machining on components like wheels and brackets, further strengthening its cost advantage over gravity casting in high-volume, cost-sensitive applications.

OEM Giga Casting Cannibalization Risk

Major automakers, such as Tesla, BMW, and Volvo, are now producing significant structural rear underbody components in-house. This marks a notable departure from their previous dependence on external gravity casting vendors. This shift towards vertical integration is not just a strategic move; it's altering the competitive dynamics of the industry. Traditional suppliers in structural casting are already feeling the pinch, with noticeable reductions in their order volumes. Giga casting cells are massive, high-tonnage systems designed to produce intricate, consolidated parts, requiring substantial capital investments. This financial hurdle acts as a gatekeeper, allowing only the industry's major players, as well as the OEMs, to step through. As an increasing number of automakers adopt this advanced casting model, Tier-1 gravity casting suppliers find themselves squeezed, particularly in terms of revenue within the structural segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum Dominance Faces Magnesium Challenge

Aluminum held an 80.12% gravity die casting market share in 2025, driven by global recycling initiatives and standard alloys, which strike a balance between flow and tensile strength. Magnesium is set to outpace at a 4.68% CAGR through 2031 as breakthroughs in rare-earth alloying tackle flammability, pushing the gravity die casting market toward lighter drive casings in premium EVs. Aluminum benefits from a vast scrap network that supplies most of its foundry feedstock, dampening raw material cost swings and supporting sustainable product claims under EU ecodesign audits. Asian smelters offer low-carbon primary aluminum backed by hydroelectric power, raising interest from European OEMs seeking Scope 3 emission cuts.

Aluminum’s dominance persists in heat-exchanger plates, cylinder heads, and inverter housing lids, where silicon additions confer casting fluidity and pressure tightness. Magnesium, meanwhile, is expanding beyond die-cast transmission cases into firewall stiffeners and seat frames, due to shot-peen surface hardening, which increases fatigue life to 10 million cycles at 100 MPa. Incentives in Europe for vehicles with a curb weight of under 1,000 kg add extra impetus for Mg penetration.

By Application: Automotive Leadership Meets Aerospace Acceleration

The automotive component accounted for 62.55% of the gravity die casting market size in 2025, primarily due to long-term contracts for engine blocks and transmission housings. In contrast, the aerospace parts are forecasted to grow at the fastest rate, with a 4.61% CAGR from 2026 to 2031. Automakers shifting to hybrid and battery platforms are maintaining gravity-cast engine blocks for range-extender modules and larger turbo-diesel programs aimed at commercial pickups. Structural vehicle parts, such as subframes and suspension knuckles, often justify gravity casting when the strength requirements exceed those of HPDC alloys.

In aerospace, cast aluminum ribs and winglet fittings reduce machining waste compared to billet routes, presenting a compelling cost case as airlines ramp up deliveries after a 2020–2023 downturn. Defense programs seeking higher thrust-to-weight turbines are evaluating gravity-cast super-alloy stator vanes that replace costlier investment-castings. Electronics castings are another bright spot; 5G base-station housings demand EMI shielding and thermal paths that gravity cast aluminum provides more efficiently than extruded boxes.

By Product Type: Engine Blocks Lead While Structural Components Surge

Engine blocks maintained a 28.05% share of the gravity die casting market in 2025. Manufacturers are turning to high-silicon aluminum to reduce liner wear, enabling the creation of lighter engine blocks that still maintain robust bore durability. Structural components, projected to grow at a 4.97% CAGR to 2031, benefit from Tesla's inspired design consolidation, which replaces multiple stampings and welds with a single rear underbody structure, thereby enhancing efficiency and reducing material usage. Cast structure adoption spreads to battery floor plates and shock-tower brackets that cannot meet crash-zone strain energy with extrusions alone.

Transmission housings still rely on gravity casting for pressure tightness across automatic, DCT, and e-axle formats, maintaining high foundry utilization even as pure ICE demand softens. Wheel castings face stagnation as forged aluminum wheels attract premium customers; OEMs position gravity cast wheels for mid-range models, where cost is a priority over weight savings.

By Process Type: Standard Methods Dominate Despite Tilt-Pour Innovation

Standard gravity die casting accounted for 73.84% of the gravity die casting market size in 2025, reflecting decades of capital amortization and operator familiarity. Pour riser design, gating simulations, and incremental automation plug-ins continue to raise output per handset line. Tilt-pour lines, expanding at 5.06% CAGR to 2031, win orders for thin-wall complex housings where laminar fill reduces oxide defects. Reverse-tilt fills symmetric parts from the center, removing runners and saving metal mass. OEMs valuing zero-defect parts per million (ppm) for critical e-motor housings pay premiums that cover the higher cell cost.

Servo tilt angle profiles captured by IoT sensors feed AI algorithms that predict die-coat degradation hours before leaks occur. Plants integrating robotic ladling and furnace auto-dosing report overall equipment effectiveness on manual lines. Still, many small foundries delay upgrades until volume migrations justify capital expenditures, which prolongs the dominance of standard vertical pouring.

Geography Analysis

Asia-Pacific held 46.78% of the gravity die casting market share in 2025, anchored by China’s extensive alloy supply chain and vertically integrated casting clusters. Regional governments subsidize Industry 4.0 retrofits that embed sensors in ladles and dies, driving digital adoption faster than in Europe. Japan’s aerospace and precision electronics sectors sustain premium demand for high-integrity castings, while South Korea’s Tier-1 suppliers leverage robotics to export e-axle housings to US transplants.

South America is expected to record the fastest CAGR of 4.78% through 2031, driven by automotive nearshoring to Brazil and Mexico as the United States OEMs diversify their sourcing. Mining expansions in Chile and Peru require large crusher frames and excavator arms, which favor thick-section, gravity-cast components over fabricated ones. Local content mandates in Brazil stimulate regional die design centers, shortening lead times and lowering import duties on critical tooling. North America prioritizes automation to counter skilled labor shortages, with Michigan and Ontario plants installing robotic tilt-pour lines linked to cloud-based quality dashboards. Environmental permitting processes remain comparatively lenient versus EU rules, yet rising energy costs encourage closed-loop furnace heat recovery projects. Europe tightens VOC and dust rules, raising compliance costs but creating opportunities for exporting low-carbon aluminum castings. The Middle East and Africa are emerging as key markets, focusing on aircraft MRO parts and defense shells.

Regulatory Landscape

Regulation affecting gravity die casting is being shaped by product-quality expectations for automotive aluminum castings and by environmental disclosure requirements linked to vehicle circularity and carbon reporting. In China, QC/T 273-2025 (implemented November 1, 2025) formalizes technical requirements and test methods for automotive aluminum-alloy die castings, tightening qualification expectations for suppliers serving domestic OEM programs.

Environmental compliance and traceability demands are also becoming procurement gates for foundries supplying global platforms. In March 2026, the China Foundry Association implemented T/CFA 0501-2026 (Green Casting Evaluation Standard), introducing quantitative evaluation items such as carbon footprint accounting, recycled material rates, and VOC monitoring, and EU-facing exporters have been asked to provide self-assessment documentation against this standard. In the European Union, Council and Parliament documentation in 2026 on supply-chain material disclosure and vehicle circularity places more emphasis on material data transparency across the automotive value chain, while the CBAM phase-in starting in 2026 raises the importance of emissions reporting for imported metal-intensive components, including castings.

Value Chain Analysis

The gravity die casting value chain starts with aluminum and magnesium inputs (primary metal and scrap), followed by alloying, melting and holding furnaces, and permanent-mold tooling design and manufacture. Foundry operations then carry out pouring (standard gravity or tilt-pour), heat treatment, trimming, and inspection, with downstream steps including machining, surface treatment and coating, assembly into modules, and shipment to OEMs and Tier-1 integrators for automotive, aerospace, electronics, and industrial machinery applications.

Equipment and process technology suppliers (tilt-pour cells, robotics, MES and quality systems) and standards bodies influence capability upgrades and qualification, while logistics and regional sourcing shape delivered cost. Recent value-chain shifts include consolidation and footprint expansion: in February 2026, Nemak completed its acquisition of GF Casting Solutions' automotive business, adding an R&D center in Switzerland and nine plants across Austria, China, Germany, Romania, and the United States, which increases its ability to supply multi-region programs and standardize processes across sites. Capacity localization is also visible in Europe, where Horse Powertrain invested EUR 45 million in a tilting gravity die casting facility in Valladolid, Spain, designed to lift annual cylinder head output by 20%, supporting shorter supply lines for regional powertrain demand and higher-process-control casting routes.

Competitive Landscape

Regional specialists and diversified metal groups keep the gravity die casting industry fragmented, although consolidation has begun as scale and environmental compliance become increasingly important. Nemak's 2025 acquisition of GF Casting Solutions' automotive division for USD 336 million makes it the largest independent supplier with 47 plants and a mix of standard and tilt-pour lines[3]“Nemak Completes Acquisition of GF Casting Solutions' Automotive Business,”, Nemak, nemak.com.

Safran has patented a new gravity casting method for turbine blade blanks, reducing scrap waste compared to the traditional investment casting technique. In East Asia, manufacturers like Sinto and EKK Eagle are eyeing greenfield projects. They're providing integrated tilt-pour solutions, merging furnaces, robotics, and MES software into one seamless package, all in a bid to boost their market presence through efficient implementation.

Despite high-profile OEM in-house giga casting rollouts, Tier-1 suppliers still win complex housings, inverter lids, and power distribution boxes, where qualification cycles and metallurgical specifications deter vertical entry. Suppliers with additive core capability and VOC-compliant die-coats charge 10–15% price premiums, but OEMs accept these for reduced scrap and faster PPAP approval. The market remains open for mid-tier specialists to capture aerospace and renewable-energy components that demand tight tolerances and corrosion-resistant alloys.

Gravity Die Casting Industry Leaders

Georg Fischer AG

Nemak SAB de CV

Ryobi Limited.

Linamar Corporation

Endurance Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities concentrate on high-integrity, pressure-tight, and dimensionally stable castings where gravity and tilt-pour processes retain an advantage over high-pressure die casting, particularly for powertrain and e-mobility housings, thermal-management components, and safety-critical chassis parts. The report base-year mix (aluminum alloys at 80.12% share in 2025 and automotive at 62.55% application share) points to automotive as the largest demand pool, but content is shifting toward electrified drivetrains and higher-thermal-load components that benefit from controlled filling and lower oxide inclusion. Investments targeted at tilting gravity die casting create practical whitespace for suppliers that pair automation with repeatable metallurgy and inspection to meet OEM validation cycles.

Geographic and capability expansion programs offer evidence of where incremental demand and sourcing are being built. In February 2026, Horse Powertrain committed EUR 45 million to Spain's first tilting gravity die casting facility in Valladolid, targeting a 20% increase in cylinder head capacity to 360,000 units annually, which indicates near-term pull for higher-control gravity casting in Europe. At the same time, large-scale integrated casting investments in China, such as Dongfeng commencing operations of 16,000-ton and 10,000-ton die-casting lines in Wuhan in January 2026 for battery casings and structural components, underscore the differentiation boundary: gravity die casters can separate through complex housings, inverter lids, transmission and e-axle housings, and other parts where qualification depth and mechanical-property requirements favor tilt-pour automation, additive-manufactured cores, and VOC-compliant die-coats rather than pure scale.

Recent Industry Developments

- February 2026: Nemak completed the acquisition of GF Casting Solutions' automotive business, bringing an R&D center in Switzerland and nine production facilities across Austria, China, Germany, Romania, and the United States into its footprint. The closing consolidates lightweight casting capacity and process know-how under a single Tier-1 supplier, strengthening multi-region supply options for OEM platforms. It also supports portfolio repositioning toward electrification and high-value castings where automation and qualification depth drive margins.

- July 2025: Nemak signed a definitive agreement to acquire GF Casting Solutions' automotive division for an enterprise value of USD 336 million. The transaction marked a major consolidation move in global automotive cast components, increasing scale and broadening customer access across regions. The deal also reinforced the rising importance of compliance-ready operations and technology capability as sourcing differentiators.

- May 2024: GF Casting Solutions announced plans to invest USD 184 million at its Augusta plant to enhance production capability and operational efficiency. The expansion targeted higher-quality casting output and improved competitiveness in supplying demanding automotive programs. It reflected the capital intensity of upgrading foundry operations for tighter quality, productivity, and sustainability requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from gravity die casting services and finished cast components made using permanent molds, across common nonferrous alloys and end-use part demand globally.

Scope exclusions: Excludes high-pressure die casting, sand casting, investment casting, and post-casting machining or coating revenue when it is priced and sold as a separate service.

Segmentation Overview

- By Material Type

- Aluminum Alloys

- Zinc Alloys

- Magnesium Alloys

- By Application

- Automotive Components

- Electrical and Electronics

- Aerospace Parts

- Industrial Machinery

- Consumer Goods

- By Product Type

- Engine Blocks

- Transmission Housings

- Wheels

- Die-Cast Housings

- Structural Components

- Others

- By Process Type

- Standard Gravity Die Casting

- Tilt-Pouring Gravity Die Casting

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by grounding the model in real industrial signals that can be checked year to year. We reference public sources such as manufacturing output series from national statistical offices, UN Comtrade trade flows for cast parts and nonferrous products, and energy and industrial production indicators from agencies such as the IEA.

To keep the casting context correct, we also read technical and market-facing sources such as ASM International publications, peer-reviewed foundry and materials journals, and association material from organizations like NADCA and regional foundry bodies. Company annual reports, investor decks, and press releases are then used to understand capacity additions, alloy shifts, and end-market exposure, and paid subscriptions for company financials and patent databases are used selectively to fill gaps on smaller private firms and process trends. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs come from interviews and structured surveys with foundries, mold and equipment ecosystem participants, and procurement or engineering stakeholders from key end-use industries such as automotive and industrial machinery. Since demand patterns differ by region, we validate assumption ranges across APAC, EMEA, and the Americas, and we re-check any large differences that show up between production signals, trade movement, and price trends.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 44% |

| Mid tier: 59% | Functional/Unit leaders: 30% | EMEA: 34% |

| Smaller Players: 16% | Managers: 58% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built first through a top-down approach where manufacturing output, end-use production, and trade data are used to reconstruct the addressable casting demand pool, then it is converted into value using observable pricing progression. To keep totals realistic, we corroborate the outcome with selective bottom-up checks, such as sample supplier roll-ups, capacity utilization logic for key regions, and volume by typical part families multiplied by indicative ASP ranges.

Inputs used in the model include automotive and industrial production trends, light-weighting intensity for aluminum and magnesium components, alloy price direction as a pass-through factor, foundry capacity additions and utilization, and the mix shift between gravity die casting and alternative casting routes for similar parts. Where direct volume signals are not clean, gaps are handled using proxy indicators like export intensity, installed manufacturing base, and expert-validated utilization ranges, and then assumptions are tightened through follow-up calls.

For forecasting, scenario analysis is used so near-term volatility in end markets and metal pricing is separated from longer-cycle adoption drivers. Scenario weights are aligned to what industry respondents consider a practical base case for new program launches, capacity ramp-up speed, and expected price realization.

Data Validation & Update Cycle

Outputs are checked using triangulation across independent signals, including regional production patterns, trade movement direction, and the implied revenue per unit of end-use output. If a region or year shows unusual jumps, it is reviewed again for currency timing, one-off plant events, or double counting between in-house and outsourced casting activity, and then escalated for analyst review before sign-off.

Reports are refreshed annually, and interim updates are made when material events occur, such as large capacity announcements, major end-market shocks, or sustained changes in alloy pricing. Before delivery, we do a fresh pass on key assumptions and the latest public data releases so clients receive an updated view consistent with the model logic.

Mordor Intelligence's Gravity Die Casting Market Size Versus Other Published Estimates

Different published market sizes for gravity die casting can look far apart, even when they all use USD, because each publisher chooses its own process coverage, pricing logic, and base year timing. Small changes in what is counted as gravity die casting revenue, and how hybrid casting routes are treated, typically explain most of the spread.

Some estimates appear to fold in adjacent casting processes or a wider set of downstream services, which can inflate the value when compared at face value. In the Mordor Intelligence model, the number is limited to gravity die casting value for castings and related service revenue, and it excludes high-pressure die casting and standalone post-casting operations that are billed separately.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 27.13 B (2026) | |

| Global Consultancy A | USD 27.67 B (2026) | Uses a slightly broader process and end-use mapping in its public definition, and the pricing build-up appears to assume higher average realized values across regions, which can lift the 2026 total. |

| Industry Publisher B | USD 4.20 B (2025) | Likely sizes a narrower subset of gravity die cast components or a limited material/application set, which compresses the value versus a full-market view, and the base year choice also makes direct comparison harder. |

Taken together, the table shows that most variation comes from process scope and how value is attributed across services versus adjacent operations. By tying the estimate to observable production signals, trade direction, and practical price ranges validated through interviews, the output stays traceable and repeatable even when public data is imperfect.

Key Questions Answered in the Report

How large is the gravity die casting market today?

The gravity die casting market size stood at USD 27.13 billion in 2026 and is projected to reach USD 32.66 billion by 2031.

Which region dominates demand for gravity die cast products?

Asia-Pacific leads, accounting for 46.78% of global gravity die casting market share in 2025.

How are environmental rules affecting foundry operations?

EU standards on Best Available Techniques (BAT) are curbing VOC emissions, spurring the shift towards water-based die coatings, and prompting consolidations among compliant facilities.

What material captures the biggest portion of gravity die cast volumes?

Aluminum alloys command 80.12% of total cast volumes, supported by mature recycling loops and widespread specification in automotive and aerospace components.

Page last updated on: